Total Addressable Market Analysis and Non-consumption

The Paradigm Shift in Market Definition

In traditional corporate strategy and venture capital evaluation, the calculation of a Total Addressable Market (TAM) is predominantly constrained by existing consumption patterns. The standard methodology relies on top-down calculations that multiply the current price of a product by the existing number of buyers in a defined geographic or demographic segment 1. This static framework assumes that markets are rigid constructs bounded by the volume of consumers currently purchasing equivalent products or services. Consequently, businesses and early-stage ventures that rely on this methodology frequently find themselves trapped in zero-sum competition, fighting for fractional market share within highly commoditized and fiercely contested spaces 123.

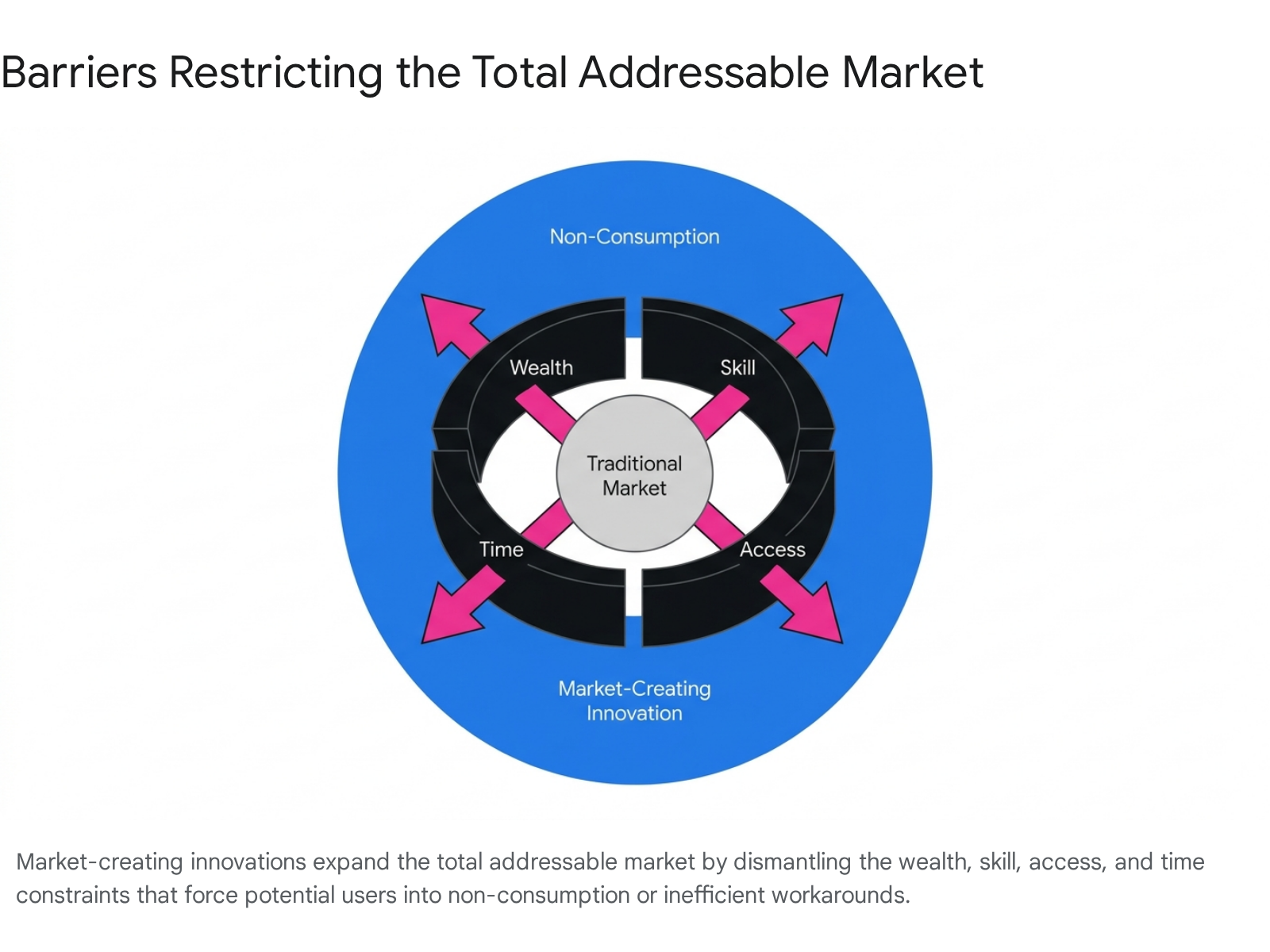

The concept of competing against "non-consumption" introduces a fundamental paradigm shift in how market opportunities are evaluated and scaled. Non-consumption occurs when potential consumers possess latent demand for a solution but are entirely excluded from the market due to insurmountable barriers, primarily wealth, skill, physical access, or time 23.

When organizations pivot their strategic focus from competing against incumbent products to competing against this non-consumption, they initiate market-creating innovations. These innovations transform complicated, expensive, or inaccessible products into simple, affordable solutions, thereby exponentially expanding the boundaries of the addressable market 245.

This comprehensive research report examines the theoretical frameworks, macroeconomic methodologies, and empirical evidence underlying the non-consumption thesis. By analyzing the Jobs-to-be-Done (JTBD) framework, the economics of the shadow market, and deep-dive case studies across Southeast Asia, Africa, and Latin America, the analysis demonstrates how targeting non-consumption redefines startup growth trajectories and venture capital allocation models.

Theoretical Foundations of Non-Consumption

To accurately size markets characterized by high levels of non-consumption, analytical frameworks must decouple market definitions from specific product categories. The theoretical underpinning for this detachment is the Jobs-to-be-Done (JTBD) framework, an innovation theory that recategorizes consumer behavior based on underlying intent 16.

The Jobs-to-be-Done Framework

Pioneered by researchers such as Anthony Ulwick and Clayton Christensen, the JTBD framework posits that customers do not strictly purchase products; rather, they "hire" products to accomplish specific tasks or make progress in a given context 16. Under this framework, a market is redefined not as an industry vertical or a demographic subset, but as a specific group of people combined with the core functional job they are attempting to execute 69.

This theoretical adjustment is critical for market sizing because functional jobs remain stable over time, whereas products, technologies, and competitive landscapes are highly transient 6. For example, the historical market for physical encyclopedias was decimated not because the market disappeared, but because the underlying job - finding accurate information quickly - was addressed by vastly superior digital search engines 1. Companies that defined their TAM based on the price and volume of encyclopedia sets failed to anticipate the total potential market of information seekers 1.

The JTBD framework evaluates market opportunities through specific, customer-defined metrics known as "desired outcomes" 610. A single functional job can involve between 50 and 150 desired outcomes, which represent the criteria customers use to measure success, such as minimizing rework, reducing execution time, or increasing certainty 610. By surveying populations to measure the importance of these outcomes against current satisfaction levels, analysts can calculate an "Opportunity Score" to identify hidden segments of opportunity where non-consumption or deep dissatisfaction prevails 611.

The Cost of Workarounds as a Market Proxy

When the barriers to consumption are too high, potential customers do not simply abandon their goals; they resort to "workarounds." Workarounds are inefficient, manual, or improvised solutions cobbled together to achieve a partial outcome 78. Analyzing the prevalence and cost of these workarounds provides a quantitative methodology for pricing latent market demand.

In the enterprise software sector, the absence of a unified platform often leads teams to rely on fragmented tools, such as external spreadsheets, manual data synchronization, and disjointed communication channels 89. These coping strategies impose significant operational penalties. A 2023 study from the MIT Sloan Management Review on knowledge worker productivity indicated that tool fragmentation reduces effective working time by an average of 20% 9. For a standard five-person team operating on a 40-hour work week, this equates to eight hours per week absorbed by tool overhead and manual processes rather than value delivery 9.

By quantifying the labor hours absorbed by these manual processes and multiplying them by average hourly labor rates, market analysts can establish a highly accurate bottom-up estimation of a customer's willingness to pay for an integrated solution 8. The presence of extensive workarounds indicates that incumbent solutions suffer from "cultural misfits" or architectural gaps, signaling a mature environment for market-creating innovation 10.

Methodological Shifts in Market Sizing

Traditional venture evaluation heavily relies on top-down analytical models. These models calculate TAM by identifying a massive macroeconomic figure and estimating an arbitrary percentage of market capture 11. When evaluating non-consumption, top-down models are fundamentally flawed because the macroeconomic figures are based on historical consumption that explicitly excludes the target population.

Bottom-Up TAM and Serviceable Available Market

To accurately assess markets defined by non-consumption, financial analysts and venture capitalists prioritize bottom-up analyses 1112. This methodology requires granular, primary data regarding the target customer profile, the specific job they are attempting to accomplish, their localized willingness to pay, and the logistical realities of the go-to-market strategy 11.

The standard formulas for evaluating market size must be adapted to account for the reduction in consumption barriers: * Total Addressable Market (TAM): Calculated as the total number of feasible customers multiplied by the average annual revenue per customer (ARPC) 12. When non-consumption barriers are lowered, the integer representing "total feasible customers" scales exponentially. * Serviceable Available Market (SAM): The segment of the TAM that can be realistically served by the company's current business model and geographic footprint 12. * Serviceable Obtainable Market (SOM): The practical percentage of the SAM the venture can capture in the near term, factoring in competitive dynamics and operational capacity 12.

In non-consumption models, willingness to pay is not benchmarked against incumbent competitor pricing, because incumbents do not serve this demographic. Instead, willingness to pay is benchmarked against the economic value of the achieved outcome or the reclaimed cost of previous workarounds 1811.

Quantifying the Shadow and Informal Economies

In many global markets, particularly in developing and transition economies, the inability to consume formal services drives massive populations into the informal or "shadow" economy 1314. The shadow economy encompasses all market-based production of legal goods and services that are deliberately concealed from public authorities to evade taxation, bypass regulatory bureaucracy, or avoid compliance with rigid labor standards 14151617.

Often referred to as "System D," the global shadow economy is vast. Estimates from the Organization for Economic Co-operation and Development (OECD) suggest that the informal economy employs approximately 1.8 billion people worldwide, representing an estimated total value of $10 trillion 13. In developing countries, the informal sector typically accounts for between 25% and 40% of national income, and can represent up to 70% of non-agricultural employment 1718.

For startups aiming to formalize transactions - such as digital payment platforms, micro-lending fintechs, and e-commerce infrastructure - the shadow economy represents the purest measure of non-consumption TAM. Because these activities are unrecorded in official Gross Domestic Product (GDP) statistics, econometricians employ several distinct methodologies to estimate their size 1419:

| Estimation Methodology | Mechanism of Measurement | Analytical Value for Startups |

|---|---|---|

| Currency Demand Method | Estimates the excess demand for cash in the economy, assuming shadow transactions are primarily cash-based to avoid detection 1420. | Identifies the total volume of unbanked capital available for capture by mobile money and digital wallet providers. |

| Electricity Consumption Method (Kaliberda & Kaufmann) | Uses electric power consumption as a physical proxy for overall economic activity, subtracting official GDP growth to find the unrecorded discrepancy 14. | Provides a baseline for industrial and manufacturing activity occurring outside the formal supply chain infrastructure. |

| Labor Force Discrepancy Method | Analyzes the statistical gap between the official labor force participation rate and actual population employment 1421. | Quantifies the available workforce for gig-economy platforms and on-demand labor marketplaces. |

Research indicates a high degree of elasticity and mobility between formal and informal sectors. For instance, hours worked in the shadow economy are highly responsive to changes in net wages and regulatory burdens in the official sector 22. When startups reduce the friction of formal participation - by offering zero-fee accounts, simplified compliance, or accessible credit - they effectively pull resources out of the shadow economy and into their Serviceable Available Market.

Market-Creating Innovation and The Prosperity Paradox

The operationalization of the non-consumption thesis at a macroeconomic scale is delineated by the "Prosperity Paradox," a framework detailing how innovation serves as the primary catalyst for lifting emerging markets out of poverty 245.

Transitioning from Push to Pull Strategies

Traditional development economics and market-entry strategies often rely on a "push" mechanism. This involves pushing resources, infrastructure, and complex existing products into markets that lack the underlying economic foundation to absorb or sustain them 3. These strategies frequently result in temporary successes that degrade once external subsidies are removed 3.

Market-creating innovations, conversely, execute a "pull" strategy. By identifying a pressing job-to-be-done among massive populations of non-consumers and designing a radically affordable, accessible solution, these ventures generate immense organic demand. This demand naturally "pulls" the necessary secondary infrastructure, regulatory frameworks, educational systems, and adjacent service ecosystems into the society 323.

Macroeconomic Metrics of Market Creation

Because market-creating innovations serve populations previously excluded by barriers of skill, wealth, access, or time, their success must be evaluated using metrics that capture systemic economic expansion rather than mere corporate revenue 35. While sustaining innovations (which make existing products better for current customers) and efficiency innovations (which reduce costs through resource elimination) are vital for corporate survival, they do not inherently expand the economic base 25.

The assessment of market-creating ventures includes the following macro-level indicators: * Instances of New Consumption Initiated: Tracking the absolute volume of users entering a formal market or utilizing a specific service category for the first time 4. * Size of the Market Created: Measuring the net-new gross merchandise value (GMV) or total payment volume facilitated by the platform, which directly contributes to national economic output 423. * Systemic Job Creation: Documenting the secondary and tertiary employment generated to serve the newly enfranchised non-consumer base. This includes decentralized agent networks, gig-economy workers, and localized merchant partners who form the distribution layer of the new market 424.

The net impact of pulling infrastructure into a market results in increased tax revenues, a shift in regional entrepreneurial culture, and the democratization of economic power across demographic strata 423.

Empirical Validation: Case Studies in Unlocking Non-Consumption

The theoretical expansion of the Total Addressable Market through non-consumption is empirically validated by examining the growth trajectories of category-defining technology firms across global markets. In Southeast Asia, Africa, and Latin America, specific startups have bypassed traditional market sizing constraints to achieve unprecedented scale.

Ride-Hailing and the SuperApp Ecosystem: Grab

When Grab (initially launched as GrabTaxi) entered the Malaysian market in 2012, a traditional market sizing analysis would have bounded the company's potential by the existing volume and revenue of the traditional taxi industry 253126. At the time, the conventional taxi market in Southeast Asia was heavily constrained by regulatory friction, a severe lack of pricing transparency, safety anxieties, and a heavy reliance on physical cash 2531. These factors relegated a massive portion of the urban population to non-consumers of private, on-demand transport 26.

Rather than competing strictly for the existing taxi ridership, Grab targeted the non-consumption of safe, reliable transport. The platform introduced mobile application booking, real-time driver tracking, and eventual integration of cashless payment systems 242527. This dismantled the anxieties and access barriers that prevented wider usage. Platform-integrated services effectively displaced the street-hail model by improving vehicle utilization and rider trust 27.

By removing the friction of localized transport, Grab executed a horizontal expansion strategy, evolving into a regional "SuperApp." Leveraging the high-frequency nature of their mobility user base, the company dramatically lowered the Customer Acquisition Cost (CAC) for adjacent services, expanding its TAM to include food delivery, grocery logistics, and digital financial services 24253435.

The scale of this unlocked market is massive. Analysts project that the overall Southeast Asian digital economy GMV could reach $1 trillion by 2030, fueled by AI-driven logistics and digital financial maturity 36. By the third quarter of 2025, Grab reported 48 million monthly transacting users (MTUs) and an on-demand Gross Merchandise Value (GMV) hitting a record $5.8 billion 2537. The company's full-year 2025 revenue reached between $3.38 and $3.40 billion 25. Furthermore, the company successfully monetized the attention of this newly created market through GrabAds, an advertising business generating an estimated 60% Adjusted EBITDA margin, representing a highly profitable secondary revenue stream that incumbent transport providers could never access 3435.

Digital Financial Inclusion: M-Pesa in Kenya

The deployment of mobile money in Kenya through Safaricom's M-Pesa platform serves as a definitive historical example of market-creating innovation. Prior to M-Pesa's launch in 2007, the traditional banking sector in Kenya was severely limited by inadequate physical branch networks, prohibitive minimum balance requirements, and high transaction fees 2829. Consequently, traditional market constraints resulted in only 26% of adults in Kenya possessing formal bank accounts 40. A conventional, top-down TAM analysis would have indicated a structurally unprofitable, niche market.

M-Pesa addressed the specific job-to-be-done of transferring money securely over long distances by leveraging the rapidly expanding penetration of mobile phones and establishing a decentralized network of local retail agents 283031. This operational model bypassed the need for physical banking infrastructure, effectively eliminating the barriers of wealth and geographical access 2930.

The results entirely redefined the financial landscape of the region. By mid-2025, Kenya achieved a 91% market penetration rate in mobile money, recording 47.7 million active subscriptions 32. In the 2025 fiscal year, M-Pesa handled transactions totaling KES 14.6 trillion (approximately USD 115 billion) 44. The platform's success demonstrates that the TAM for financial services was not the 26% of adults previously banked, but rather the entire economically active population.

Beyond payment facilitation, the platform initiated secondary economic expansions. Access to M-Pesa increased the probability of individuals subsequently joining the formal banking sector and decreased reliance on informal, risk-heavy savings mechanisms 2833. Furthermore, empirical studies have correlated mobile money adoption with broader socio-economic improvements, including stabilization of food prices and enhanced food security in rural agricultural communities, demonstrating the far-reaching externalities of unlocking non-consumption 34.

Neobanking Scalability: Nubank in Latin America

Nubank's trajectory in the Latin American financial sector provides compelling evidence of TAM expansion through the elimination of incumbent barriers. Founded in 2013, Nubank entered a Brazilian market functioning as an oligopoly, where the top five incumbent banks controlled over 80% of total banking assets 354836. This environment was characterized by high interest rates, bureaucratic branch-heavy cost structures, and exclusionary underwriting policies that effectively rendered millions of lower-income and younger Brazilians non-consumers of credit and digital banking 36.

A traditional market analysis would have focused exclusively on capturing market share from the existing revenue pools of the incumbents. Nubank, however, targeted the unbanked and underbanked by deploying a cloud-native, branchless operational model offering no-fee credit cards and intuitive mobile interfaces 353637. By processing billions of real-time data points, the firm successfully underwrote "thin-file" customers that traditional institutions rejected, achieving higher approval rates while maintaining sustainable loss ratios 35.

Because its digital-first cost structure operates up to ten times lower than that of legacy incumbents, Nubank could profitably serve demographic segments that traditional banks structurally ignored 38. The scale of this non-consumption capture is unprecedented. By the first quarter of 2026, Nubank reached approximately 114.7 million customers, surpassing traditional banking giant Bradesco to become the second-largest financial institution in Brazil by customer base, and penetrating roughly 61% of the country's adult population 5239.

In 2025, the company generated $16.3 billion in revenue with a Return on Equity (ROE) running at 30% to 33%, demonstrating that serving non-consumers is not solely a mechanism for user acquisition, but a highly profitable enterprise strategy when supported by radical operational efficiency 375440. Furthermore, the market expansion exhibits compounding characteristics; mature customer cohorts on the platform steadily expand their average revenue per active customer (ARPAC) as they adopt subsequent products, shifting the TAM expansion from horizontal acquisition to vertical monetization 395441. The model is now being replicated across the region, with operations in Mexico capturing 12 million customers and reaching a 13% adult population penetration rate 48.

Comparative Scale of Unlocked Markets

The fundamental shift in market size achieved by prioritizing non-consumption is clearly observable when contrasting historical baseline constraints with actual unlocked scale.

| Company | Core Region | Traditional Baseline Constraints (Pre-Launch) | Actual Unlocked Market Scale (Recent Data) |

|---|---|---|---|

| Grab | Southeast Asia | Highly fragmented, cash-reliant taxi industry with severe safety and utilization issues. | 48 Million MTUs; expansion to $5.8B quarterly on-demand GMV across mobility, food, and finance 25. |

| M-Pesa | Kenya | 26% of adults possessed formal bank accounts; reliance on physical branch networks 40. | 91% national mobile money penetration; 47.7 Million active subscriptions 32. |

| Nubank | Brazil | Oligopoly of 5 banks holding 80% of assets; high fees excluded low-income populations 36. | 114.7 Million customers; roughly 61% adult population penetration in Brazil 52. |

Artificial Intelligence and the Next Wave of Non-Consumption

The transition from the traditional software era to the deployment of generative and agentic artificial intelligence represents the next frontier in targeting non-consumption. While previous technological waves democratized access to digital distribution, communication, and basic financial ledgers, AI possesses the capability to democratize access to high-fidelity cognitive tasks and specialized expert services.

Services as the New Software

Venture capital analysts and industry researchers are documenting a structural shift in how future markets will be sized: a transition from selling software tools to selling automated outcomes, encapsulated by the thesis that "services are the new software" 42. The global market for services is vastly larger than the market for software; analytical estimates suggest that six dollars are spent on services for every one dollar spent on software 42.

Historically, highly skilled services - such as legal counsel, medical diagnostics, or bespoke agricultural consulting - were severely restricted by the limitations of human capital and billable hours. This created massive non-consumption among small and medium-sized enterprises (SMEs) and lower-income demographics who simply could not afford expert rates. The deployment of AI agents equipped with both intelligence and judgement capabilities allows startups to automate the execution of the work itself, rather than merely providing workflow software for human practitioners 42.

Emerging AI Startups Targeting Non-Consumption

Venture data from 2025 and 2026 highlights a cohort of startups actively deploying this thesis across traditional, high-friction sectors:

- Legal Tech Automation (Jurisphere): In India, Jurisphere secured $2.2 million in seed funding to build an outcome-based legal AI platform 4344. Rather than selling productivity software exclusively to existing corporate law firms, the company integrates AI workflows with a marketplace of legal professionals 4345. This architecture drastically lowers the cost and time barriers for SMEs and individuals who previously could not afford reliable legal representation for contract review or dispute resolution, opening a vast non-consumption TAM for legal outcomes 4344. Similarly, Manifest OS raised $60 million to build an AI-native legal platform designed to replace the billable hour model entirely with outcomes-based pricing 61.

- Predictive Agritech (Clisense): Smallholder farmers in Africa face severe crop volatility due to climate shocks but remain non-consumers of advanced meteorological and data science tools due to prohibitive costs, lack of reliable internet access, and literacy barriers 62. Clisense utilizes AI to translate complex satellite and climate data into hyper-local, agriculture-specific recommendations. Crucially, to overcome access barriers, these insights are delivered via SMS and interactive voice messaging in local languages, creating a net-new market for predictive agricultural insights among users previously reliant on generational intuition 62.

- SME E-Commerce Ecosystems (Yelen): In Francophone Africa, SMEs constitute over 90% of active firms, yet fewer than half engage in online sales due to technical friction and a lack of integration with informal logistics and mobile money 62. Startups like Yelen bypass complex coding requirements, allowing merchants to deploy digital storefronts integrated directly with local payment rails, effectively capturing the non-consumption of digital commerce infrastructure 62.

In these instances, AI functions as a profound market-creating innovation. The TAM is no longer sized by the number of existing software licenses sold to law firms or commercial agribusinesses. Instead, it is sized by the total volume of necessary legal contracts generated by the economy, or the total acreage of smallholder farms requiring optimization.

Venture Capital Perspectives on Capital Allocation

The paradigm shift toward targeting non-consumption fundamentally alters how venture capitalists evaluate startup viability and allocate capital. In volatile or down-market macroeconomic environments, top-tier venture firms prioritize capital efficiency and sustainable unit economics over models reliant on "growth at all costs" 4664.

Capital Efficiency and Bottom-Up Metrics

Evaluating startups that target non-consumption requires specific efficiency metrics, largely because market-creating innovations often necessitate heavy initial investments in market education or the subsidization of early adoption (e.g., the driver and consumer incentive structures utilized in ride-hailing networks) 3437.

Firms like Andreessen Horowitz (a16z) heavily rely on bottom-up analytical frameworks and rigorous tracking of operational metrics 1147. A critical metric is the "Burn Multiple," which measures the ratio of cash burned to net-new Annual Recurring Revenue (ARR) generated 46. When analyzing non-consumption, an efficient go-to-market motion is imperative to keep this multiple low.

If a startup utilizes a bottom-up adoption strategy - such as Nubank's reliance on word-of-mouth viral expansion, which accounted for 80% of their customer acquisition - it drastically reduces the Customer Acquisition Cost (CAC) 3547. A compressed CAC is vital because it allows the business model to sustainably support the lower initial Average Revenue Per User (ARPU) inherent in serving previously unbanked or lower-income populations, while still maintaining high Contribution Margin Lifetime Value (LTV) to CAC ratios 48. Additionally, metrics such as the Net Promoter Score (NPS) serve as vital leading indicators of retention and product-market fit among newly enfranchised consumers 11.

The Shift from Financial to Productive Capital

As the technology sector matures, the structural mechanics of venture capital are adapting to the extended time horizons required to fully exploit expanded TAMs. Prominent firms are restructuring their investment vehicles to align with the reality that creating a new market, building the necessary adjacent infrastructure, and scaling to serve tens of millions of new users is a process that extends well beyond standard fund lifespans.

For example, Sequoia Capital broke from the traditional 10-year closed fund cycle to establish "The Sequoia Fund," an open-ended structure designed to hold long-term positions in enduring companies 68. This evolution signifies a transition from purely speculative "financial capital" to "production capital," allowing the firm to support companies as they compound their advantages over decades to expand their markets globally 68.

Concurrently, as AI shifts the commercial focus from software tools to automated services, startups successfully executing outcome-based pricing models are demonstrating unprecedented velocity. Venture capitalists, such as Benchmark's Eric Vishria, note that AI application companies scaling efficiently to $100 million in ARR are achieving this milestone at rates five to ten times faster than historical Software-as-a-Service (SaaS) cohorts 49. This exponential velocity is the direct result of tapping into massive, previously dormant pools of demand - the global non-consumers of expert services.

Conclusion

The strategic mandate to compete against non-consumption radically alters the calculus of market definition, operational scaling, and venture capital allocation. When startups construct their Total Addressable Market based exclusively on the consumption parameters of existing incumbent products, they artificially constrain their growth potential and submit to fierce, zero-sum competition. By applying frameworks such as Jobs-to-be-Done, innovators can look past rigid product categories to identify the underlying functional tasks that massive populations are struggling to accomplish due to structural barriers of wealth, skill, access, and time.

Methodologically, transitioning to a non-consumption strategy requires abandoning top-down market share estimates in favor of rigorous bottom-up models that factor in the economic friction of manual workarounds and the immense scale of the informal shadow economy. The empirical successes of platform ecosystems like Grab, M-Pesa, and Nubank prove that methodically stripping away barriers to entry does not merely yield incremental market share; it triggers market-creating innovations that exponentially expand the TAM, pulling tens of millions of non-consumers into the formal digital economy.

As the global technology landscape rapidly evolves into the era of agentic artificial intelligence and automated service delivery, the frontier of non-consumption has shifted. While previous decades focused on providing basic financial and communicative access, the current era promises the democratization of specialized cognitive expertise. Startups that correctly identify this latent demand and deliver accessible, outcome-based solutions will continue to uncover total addressable markets far larger, and vastly more profitable, than those recognized by traditional economic forecasting.