Solo entrepreneurship in the age of artificial intelligence

The integration of generative artificial intelligence (AI) into entrepreneurial workflows has fundamentally altered the mechanics of firm creation. By drastically reducing the marginal cost of coding, content generation, and operational administration, AI has enabled single individuals to execute tasks that previously required multidisciplinary teams. This technological shift has sparked a rapid increase in the proportion of solo-founded startups globally. However, while AI undeniably lowers the barrier to entry, a comprehensive analysis of venture capital deployment, product performance data, and organizational scaling metrics reveals a more complex reality. Surviving and scaling as a solo founder requires navigating market saturation, distribution bottlenecks, and the persistent advantages of multi-founder teams.

The democratization of production capacity has led to intense competition, shifting the primary entrepreneurial bottleneck from product development to distribution, customer acquisition, and trust-building. Furthermore, empirical data suggests that while solo founders can iterate faster and operate with lower burn rates, multi-founder teams retain a structural advantage in capturing top-tier market outcomes and securing institutional venture capital. This report evaluates the changing dynamics of solo entrepreneurship, comparing economic mechanics, regional ecosystems, performance outcomes, and capital acquisition in the AI era.

Foundational Shifts in Startup Formation

The conventional wisdom of the venture capital ecosystem has historically penalized solo founders, operating on the assumption that a single individual cannot possess the requisite cross-functional skills or emotional resilience to scale a high-growth enterprise. Recent demographic data indicates that founders are increasingly ignoring this convention, driven by the operational leverage provided by advanced technology.

Global Startup Volume and Demographic Trajectories

Startups remain a driving force in the global economy, with estimates indicating the existence of over 150 million startups worldwide, with approximately 50 million new entities established annually 1. The United States leads this metric with 1.56 million active startups, followed by the United Kingdom and India 1. Within this massive volume of firm creation, the internal composition of founding teams is undergoing a significant transformation.

Data sourced from tens of thousands of startups on the equity management platform Carta illustrates a steady, accelerating shift toward solo entrepreneurship in the United States. Prior to the mainstream proliferation of generative AI, the solo founder model was relatively niche. However, the commercialization of advanced large language models (LLMs) between 2022 and 2024 acted as a distinct catalyst for single-person enterprise creation.

| Year | Percentage of U.S. Startups with a Solo Founder |

|---|---|

| 2017 | 17.0% 1 |

| 2019 | 23.7% 23 |

| 2023 | 29.0% 1 |

| 2024 | 35.0% 156 |

| H1 2025 | 36.3% 237 |

As demonstrated by the data, the percentage of newly incorporated U.S. startups led by a single founder has more than doubled since 2017, with growth accelerating sharply between 2023 and 2025. Conversely, larger founding teams are becoming less frequent; in 2024, only 16% of new startups had three founders, 7% had four, and 4% had five - representing the lowest levels in a decade 1.

The Emergence of Non-Technical Founders

This phenomenon is not isolated to the United States. In China, an April 2026 report from the accelerator community Honghub documented a structural shift in the profile of independent company builders. Analyzing a landscape heavily influenced by automation, the report found that a staggering 75% of solo founders in China now come from non-technical backgrounds 8. Operations and growth specialists are currently just as likely to launch tech ventures (26%) as formally trained engineers (25%) 8.

This reversal from the pre-2020 landscape is attributed directly to the collapse of the marginal cost of producing code. As AI models have become proficient at generating complex user interfaces and application logic on demand, the traditional prerequisite of a computer science degree has been bypassed 8. Even among founders with technical backgrounds, nearly half now prioritize deep industry knowledge over proprietary technical patents as their core competitive advantage 8.

Economic Mechanics of Artificial Intelligence Integration

The primary mechanism making solo entrepreneurship viable at scale is the extreme compression of organizational requirements and initial operational expenditures. Generative AI allows a single operator to perform tasks across multiple domains without expanding headcount.

Labor Arbitrage and Development Costs

The core economic advantage of the modern solo founder is access to asynchronous, low-cost digital labor. Research tracking the Chinese market indicates that for every $1 a solo founder spends on AI tools, they gain the equivalent of $72 in developer labor 8. This 72x labor advantage fundamentally alters the runway calculation for new businesses.

In traditional paradigms, launching an initial minimum viable product (MVP) required a team of specialized workers. A standard mid-sized enterprise software project might cost between $100,000 and $500,000 to implement due to data preparation, engineering effort, and infrastructure setup 9. A fully traditional software MVP could take three to six months and require designers, developers, and quality assurance engineers 10.

With the advent of AI coding assistants and automated design tools, a solo founder possessing AI fluency can build a production-quality MVP in three to six weeks 11. This speed is achieved because AI tools can handle routine coding tasks, generate user interfaces, and draft standard legal documents, effectively removing the need to hire early employees or agencies for these functions 101112. Consequently, the solo founder operates with a dramatically lower burn rate, granting them a longer runway to test hypotheses and pivot before capital exhaustion 1314.

| MVP Development Parameters | Traditional Development Approach | AI-Augmented Development Approach |

|---|---|---|

| Typical Timeline | 3 to 6 months 1011 | 3 to 6 weeks 11 |

| Initial Capital Requirement | High (salaries, contractors, agencies) 1015 | Low (software subscriptions, API usage) 7 |

| Primary Execution Focus | Core functionality, predictable step-by-step logic 417 | Speed to market, automated workflows, experimentation 104 |

| Iterative Friction | High (requires team consensus and rework) 1018 | Low (solo decision-making, fast iteration) 1318 |

While AI significantly reduces the cost of version 1.0, successful founders maintain strict capital discipline. Industry best practices recommend a 60/40 budget allocation rule: utilizing 60% of available funds for the initial build and reserving 40% for iteration based on real user feedback 17.

Operational Expenditure Compression

Beyond the initial product build, AI systems compress ongoing operational expenditures. Tasks such as market research, competitor analysis, customer support, and financial modeling - which previously necessitated distinct departments or external agencies - are now managed through sophisticated AI technology stacks 7125. A well-optimized stack organized around content generation, operations, customer relationship management, and data analytics can cost a solo founder less than $150 a month 7.

However, the implementation of AI is not devoid of maintenance costs. For larger organizations and complex implementations, annual AI maintenance typically equals 15 - 30% of the original build cost due to infrastructure scaling, model fine-tuning, and security overhead 9. Despite these ongoing costs, the return on investment (ROI) for enterprise AI adoption is substantial. Across industries, organizations using generative AI report an average ROI of 3.7x per dollar invested, with top adopters achieving returns as high as 10.3x 6.

Regional Variations in Startup Ecosystems

The viability of solo entrepreneurship is intimately tied to the maturity and funding dynamics of regional ecosystems. While the U.S. market is experiencing a surge in individual builders backed by deep capital reserves, global venture markets display distinct characteristics that dictate how, and if, solo founders can scale.

North America and Market Dominance

The United States remains the undisputed heavyweight in global venture capital, providing a fertile environment for highly experimental solo ventures. In 2025, U.S. private AI investment hit $109.1 billion, representing a massive concentration of capital 7. Furthermore, U.S. startup funding reached $162.8 billion in just the first half of 2025 8. The deep liquidity in the U.S. market allows solo founders to access robust early-stage capital, angel networks, and specialized AI accelerators that are scarce in other regions 2324.

The European Tech Landscape

The European tech ecosystem has matured significantly, reaching a combined public and private valuation of approximately $4 trillion in 2025, representing 15% of the continent's GDP 910. However, European startup funding stabilized at roughly $44 billion in 2025, a fraction of the U.S. total 910.

A defining characteristic of the European market is its heavy focus on deep tech, which captured 36% of all European VC dollars in 2025 (up from 19% in 2021) 910. Deep tech ventures - which often involve complex hardware, biotechnology, or foundational scientific research - are highly resistant to the solo-founder model. These sectors require substantial capital expenditures, laboratory infrastructure, and multidisciplinary PhD-level teams 27. Consequently, solo founders in Europe are largely confined to SaaS, consumer products, and niche B2B software where capital requirements are lower 27.

Latin America Venture Capital Markets

In 2024, capital raised by startups in Latin America increased by 26% year-over-year, reaching approximately $4.5 billion across roughly 750 deals 112912. This growth outpaced Europe but highlights a highly concentrated market; Brazil and Mexico together drew roughly 70% of Latin American VC dollars 29.

For solo founders, the Latin American market presents a distinct challenge: capital is increasingly flowing toward later-stage companies. In 2024, 65% of the capital allocated to Latin American startups was directed toward growth or late-stage rounds (up from 46% in 2023) 11. Median Series A round sizes stabilized at $10 million, while seed-stage funding remained highly selective 12. With an ecosystem defined by "fewer rounds, but more money," solo founders in Latin America face intense pressure to reach profitability quickly, as early-stage risk capital is scarce 1129.

Southeast Asia Startup Dynamics

The Southeast Asian startup ecosystem has transitioned from a period of aggressive consumer "blitzscaling" toward measured maturity, focusing on vertical SaaS, industrial software, and embedded fintech 3132. Funding in the region dropped to $2 billion in the first half of 2025, representing a stark contrast to the $25 billion raised in 2021 3233.

Similar to Latin America, late-stage deals in Southeast Asia surged (140% growth in H1 2025), while seed funding collapsed by 50% 33. Funding is also hyper-concentrated geographically, with Singapore capturing 92% of all regional tech funding 83233. The strain on early-stage liquidity means that solo founders in Southeast Asia must navigate a highly constrained environment. They are forced to prove unit economics and capital efficiency much sooner than their Western counterparts, utilizing AI not just for speed, but for basic survival 3233.

| Region | H1 2025 Startup Funding | Ecosystem Characteristics and Solo Founder Implications |

|---|---|---|

| North America (U.S.) | ~$162.8 Billion 8 | Deep liquidity; high tolerance for experimental and AI-native solo ventures; robust seed and angel networks. |

| Europe | ~$44 Billion (Annualized estimate) 910 | Maturing $4T market; 36% of funding allocated to deep tech, creating high barriers for solo operators outside of standard SaaS. |

| Latin America | ~$4.5 Billion (2024 Total) 2912 | Capital concentrated in Brazil and Mexico; 65% of funding goes to late-stage, severely constraining early-stage solo founders. |

| Southeast Asia | ~$2.0 Billion 3233 | High concentration in Singapore (92%); seed funding dropped 50%, forcing solo founders to prioritize immediate profitability over scale. |

Shifting Skill Paradigms for Entrepreneurs

Because the technical execution of building digital products is increasingly commoditized by AI, the skill sets required to succeed as a founder have fundamentally shifted. The bottleneck for new ventures is no longer technical constraints, but rather market validation and distribution strategy.

The Transition from Technical Execution to Domain Expertise

In the pre-AI era, a solo founder attempting to build a B2B software product was required to possess deep technical engineering capabilities 11. Today, AI platforms lower the cost of expertise, allowing individuals to code, design, and market without formal training 3435. As a result, the value of purely routine technical work is decreasing, while skills related to critical thinking, problem framing, and domain expertise are heavily amplified 35.

This dynamic is fostering the rise of founders who act as system orchestrators. Competitive advantage now stems from recognizing nuanced workflow gaps within specific industries, understanding complex regulatory environments, and mastering B2B sales dynamics 536. Technology alone is insufficient; many AI-augmented startups fail because they pursue highly competitive markets with products disconnected from actual customer demand 36. Success requires deep validation - interacting directly with customers to understand pain points, language patterns, and economic incentives before writing a single line of AI-generated code 36.

AI Infrastructure Management and Workforce Composition

To operate at the capacity of a full team, solo founders must transition from treating AI as a casual assistant to managing it as core operational infrastructure. Effective solo founders treat AI agents as junior employees, providing them with clear standard operating procedures, brand guidelines, and review checklists 15.

This shift mirrors broader macroeconomic trends in workforce composition. A 2026 global survey of chief executive officers by Oliver Wyman indicated that over 40% of organizations plan to cut junior roles in the near term and shift their workforce toward mid-level or senior positions 13. AI agents are increasingly capable of performing tasks at the level of a junior developer or copywriter, but they lack the judgment calls derived from on-the-job experience 13. For the solo founder, this confirms that leveraging AI is not a substitute for strategic wisdom. AI can execute the tactics, but the founder must possess the experience to set the strategy and evaluate the quality of the output 155.

Performance Outcomes and Product Distinctiveness

While it is operationally easier to launch a company as a solo founder, empirical evidence regarding ultimate performance outcomes presents a paradox. AI enables solo founders to be highly innovative and experimental, yet multi-founder teams continue to dominate the upper echelons of sustained startup success.

Experimentation and Market Differentiation

A comprehensive 2026 study analyzing over 160,000 entrepreneurial entries on the platform Product Hunt evaluated the impact of generative AI on product launches 1415. The researchers measured "product distinctiveness" - a metric capturing how rare a product's combination of attributes is relative to peers launched simultaneously 14.

Following the public release of ChatGPT-3.5, product distinctiveness increased across the board. However, the magnitude of this change was substantially larger for solo founders. Difference-in-differences estimates showed that solo ventures experienced an approximately 4% larger increase in product distinctiveness relative to team ventures in the post-ChatGPT period 14. This indicates that AI acts as an equalizing tool for experimentation, allowing solo founders to safely explore unfamiliar regions of the product space and test novel combinations of features without the coordination tax or financial risk associated with team-based ventures 1315.

Market Noise and the Distribution Bottleneck

The unintended consequence of collapsing development costs is extreme market saturation. Because anyone can build software cheaply, the internet is flooded with digital products, creating a distribution bottleneck that heavily penalizes solo operators with limited bandwidth.

Data from an analysis of 76,822 launches on Product Hunt highlights this friction. In 2021, the platform saw a record 12,137 launches, a 32% increase from 2019 4041. However, while launch volume exploded, average user engagement per product dropped by 47% 40. Furthermore, the conversion rate for achieving "Product of the Day" status shrank from 22% in 2019 to 15% in 2021 40. Achieving top-tier visibility yields massive returns - products earning "Product of the Day" receive a 419% boost in upvotes compared to non-featured products - but the competition for that attention is fiercer than ever 41.

When execution is cheap, "good enough" products become ubiquitous 13. To cut through the noise, a founder must orchestrate sophisticated pre-launch distribution channels, build waitlists, engage in active community management, and perfect product positioning 42. Building these distribution channels requires sustained human effort and relational trust. If a solo founder expends their limited energy orchestrating AI to build the product, they risk failing at the critical distribution phase 13.

The Persistence of Team Advantages at Scale

The Product Hunt study revealed a critical limitation to the solo founder surge: the expansion of solo entrepreneurship is largely characterized by low-commitment, experimental entries that do not translate into the highest-quality outcomes 14. The data clearly demonstrates that team-based ventures remain increasingly dominant in the top tiers of platform rankings 1415.

This outcome is reinforced by organizational psychology research. A study by Harvard Business School researchers at Procter & Gamble introduced the concept of the "Cybernetic Teammate" 16. The researchers found that while individuals using AI could produce ideas equal in quality to a two-person team operating without AI, a team that also utilized AI produced the highest-quality solutions overall 16. Specifically, ideas ranking in the top 10% were three times more likely to originate from human teams using AI rather than individuals working with AI 16.

Therefore, while AI elevates the baseline capability of a solo founder, it also elevates the capabilities of competing teams. When a solo founder competes against a small team utilizing the same AI tools, the team's ability to run multiple critical threads simultaneously (parallelism) generally secures market dominance 13.

Failure Rates and Risk Mitigation Strategies

When evaluating whether it is "harder" to be a solo founder, baseline startup mortality metrics must be examined. The path to startup success is inherently difficult, with longitudinal data confirming that approximately 90% of all startups eventually fail 144.

Baseline Startup Mortality Metrics

According to aggregate data, roughly 20% to 21.5% of new businesses fail within their first year, 45% to 48.4% fail by year five, and 65% fail by the ten-year mark 645. First-time founders face particularly steep odds, achieving only an 18% success rate, whereas entrepreneurs who have previously built a successful business operate with a 30% success rate 14445.

An analysis of failed startups highlights that the primary drivers of mortality are rarely technical limitations. The most common cause of failure, cited in 42% of cases, is a lack of product-market fit (creating a product no one wants) 644. Running out of funding accounts for 29% of failures, while team issues - including skills gaps and poor hiring decisions - contribute to 23% of startup collapses 644.

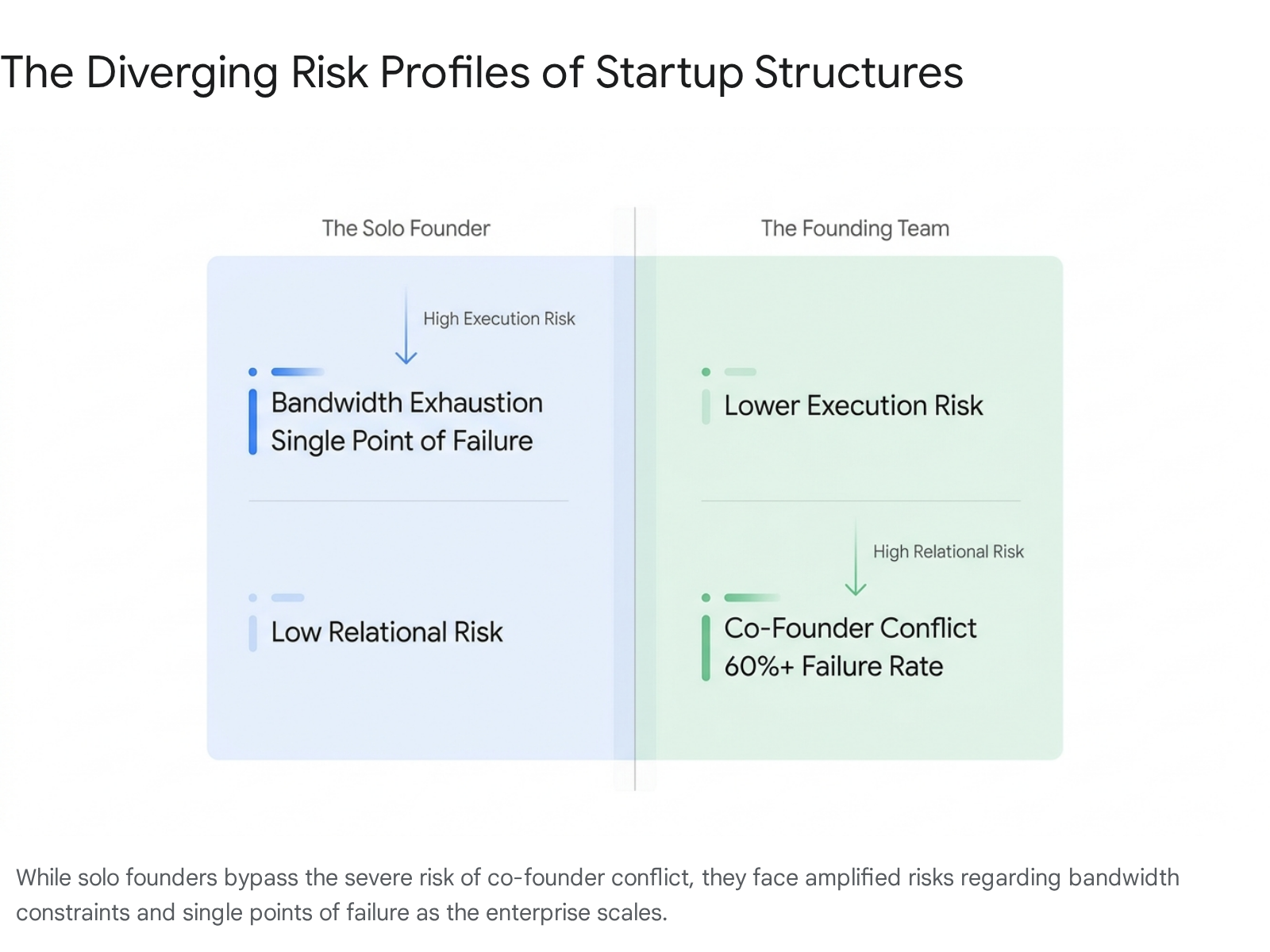

The Co-Founder Conflict Variable

Despite data suggesting that startups with co-founders are generally more likely to succeed than solo ventures, multi-founder teams carry a unique and highly lethal risk: human friction 4445. Research indicates that up to 65% of startup failures are directly attributable to co-founder conflict 46.

Disagreements over strategic vision, roles, equity distribution, and work ethic can permanently derail an otherwise promising venture 4647.

Solo founders inherently bypass this specific risk. They operate without the need for internal consensus, avoiding awkward equity negotiations and the emotional toll of partnership breakdowns 46. Furthermore, solo founders often reach profitability faster due to their streamlined decision-making processes, zero coordination tax, and radically lower administrative overhead 1346.

```xml

Hiring Velocity and Equity Distribution

Because they lack internal partners, solo founders must eventually build teams to scale. Interestingly, data from Carta reveals that startups with a single founder hire their first employee faster than multi-founder teams. The median time from incorporation to first hire for a solo founder is 399 days, compared to 480 days for multi-founder companies 2. Engineering remains the most common first hire, reflecting the need to transition from AI-generated MVPs to robust technical architectures 27.

When they do hire, solo founders possess a significant structural advantage regarding equity. Because they do not split equity at incorporation (unlike the 45.9% of two-person teams that split equity equally), solo founders maintain a compounding ownership advantage 1. This superior equity position grants solo founders strategic flexibility, allowing them to utilize larger equity grants to attract top-tier early employees or specialized advisors without suffering unacceptable personal dilution 1427.

Venture Capital Allocation and Institutional Bias

A significant hurdle for solo founders is interacting with institutional capital. Despite the proven operational leverage of AI and the absence of co-founder conflict, the venture capital (VC) ecosystem maintains a strong, systemic bias toward founding teams.

Disparities in Capital Deployment

Extensive data confirms a profound disconnect between the rate of solo business formation and the allocation of venture capital. While solo founders represented over 35% of all new U.S. startups in 2024, they accounted for only 17% of the startups that successfully closed a VC round that year 16. Furthermore, solo-led companies received only 14.7% of the total cash raised in priced equity rounds 2.

This disparity is fundamentally driven by investor risk management frameworks. Venture capitalists view co-founders as a necessary redundancy - a hedge against the "bus factor" (the risk of a solo founder falling ill, burning out, or making catastrophic decisions without peer review) 48. Teams provide internal checks and balances, reducing the likelihood of a single individual pursuing an unvalidated idea in an echo chamber 17. High-profile accelerators, such as Y Combinator, continue to express a preference for founding teams, citing the intense emotional burden of entrepreneurship and the need for complementary skill sets 518.

Valuation Equivalence Across Funding Stages

Despite the extreme difficulty in securing initial institutional backing, data indicates that when solo founders successfully pass VC filters, they are not penalized on valuation.

A prevalent myth in the startup ecosystem is that solo founders must accept worse financial terms - a so-called "solo tax." However, equity data reveals that solo- and multi-founder companies experience nearly identical dilution across early funding stages 1427. At the Priced Seed stage, a mild bias may pull median valuations down slightly due to less competitive bidding, but by Series A, valuations and dilution levels are statistically indistinguishable between solo and team-led companies 1427.

The culmination of this dynamic is that solo founders who survive to later stages retain significantly more personal wealth. After raising an initial funding round, the average multi-founder team collectively holds 56.2% of their startup's equity; by Series B, that collective figure drops to 23% 1. In contrast, solo founders hold roughly 50% more personal equity by Series B compared to the lead founder of a co-founded startup, assuming comparable valuation levels 14.

Institutional Investment Strategies

While generalist VC funds remain hesitant, specialized capital is beginning to adapt to the AI-augmented solo founder model. AI-specialist funds and programs evaluate startups on entirely different theses 24. For example, a16z's Speedrun accelerator offers specialized programs for highly technical early-stage founders, providing $500,000 upfront and over $5 million in compute credits - effectively eliminating the need for early infrastructure capital 2451. Similarly, Kleiner Perkins launched a $3.5 billion fund in 2025 dedicated exclusively to AI startups, acknowledging the rapid capital efficiency of modern software businesses 24.

Scaling Limitations and the One-Person Unicorn Concept

The ultimate test of the solo founder model in the AI era is the pursuit of massive scale. The technology industry is currently captivated by the hypothesis of the "one-person unicorn" - a company achieving a $1 billion valuation or revenue metric operated indefinitely by a single founder augmented by autonomous AI agents 55253. Prominent industry figures have predicted this milestone will be reached within the decade 5254.

Theoretical Viability and the Reality Check

As of early 2026, no verified one-person unicorn exists 19. Zero companies with three or fewer full-time employees have achieved an independently verified valuation of one billion dollars, whether through a venture capital round, acquisition, or public listing 19. Startups frequently cited by the media as precursors to this model actually employ significant teams. For example, Safe Superintelligence (SSI), valued at $32 billion, employs approximately 20 individuals, while the AI coding assistant Cursor (Anysphere) generates $100 million in annual revenue but relies on a staff of nearly 50 54. In 2024 - 2025, the median AI startup that achieved unicorn status still required 203 employees 54.

While an AI-augmented solo operator can undeniably generate millions in revenue through product-led growth (PLG) SaaS or digital distribution platforms, achieving a billion-dollar valuation historically requires network effects, market dominance, and strategic acquisition value - mechanisms that do not automatically follow from individual software productivity 5419.

Regulatory Friction and Enterprise Complexity

Furthermore, as companies scale, they encounter structural, real-world friction that AI cannot easily resolve. Regulatory compliance is a primary obstacle. Emerging legal frameworks, such as the EU AI Act (2025) and India's AI Code of Ethics (2025), enforce strict requirements for bias mitigation, data consent, and auditability 54. In the first quarter of 2025, 41% of solo-AI startups in the European Union failed initial compliance checks 54. Legal liability, enterprise vendor security assessments, and complex institutional negotiations require human accountability and specialized personnel 54.

Bandwidth Exhaustion and Strategic Plateaus

Perhaps the most significant challenge making the solo founder's journey harder today is the sheer exhaustion of managing multiple critical business functions simultaneously. While AI replaces repetitive cognitive labor and generates code, it does not replace the bandwidth needed for parallel processing across complex business domains 135.

As a startup scales from product validation to market capture, tasks such as closing six-figure enterprise sales deals, managing B2B partnerships, handling security compliance, and navigating edge cases compound rapidly 13. Human trust remains paramount in enterprise transactions; corporate clients buy from humans, and these relational activities cannot be fully automated by LLMs 135. Ultimately, a solo founder remains a single point of failure. If the founder focuses entirely on product architecture, they risk neglecting distribution; if they focus on sales, the product stagnates.

Conclusion

Is it harder to be a solo founder in the age of AI? The answer depends entirely on the phase of the entrepreneurial lifecycle being evaluated.

In the "zero-to-one" phase - encompassing ideation, minimum viable product development, and initial market validation - it is demonstrably easier to be a solo founder today than at any point in history. The profound labor leverage provided by AI systems effectively removes the absolute requirement for technical co-founders, collapses initial development costs, and extends financial runways, allowing individuals to test and iterate at unprecedented speeds.

However, in the "one-to-scale" phase, succeeding as a solo founder presents extreme difficulties. The democratization of building has resulted in hyper-competitive, saturated markets where product differentiation is fleeting and distribution is paramount. Furthermore, the operational complexity of scaling a business - managing enterprise sales, navigating stringent regulatory compliance, and executing strategic pivots - strains the temporal limits and bandwidth of a single individual. Institutional venture capital continues to heavily favor founding teams, meaning solo founders must largely rely on bootstrapping or achieving exceptional early profitability to survive.

Ultimately, artificial intelligence is a profound operational multiplier, but it does not expand the emotional capacity of a single human being. The solo founders who achieve sustained, outlier success in the AI era will not be those who attempt to automate every function of a traditional corporation in isolation. Rather, they will be those who leverage AI to operate with ruthless simplicity in highly specific niches, utilizing technology to augment their domain expertise while recognizing when to integrate human capital to overcome the inevitable frictions of scale.