Should You Pay Off Debt or Invest When Rates Are High

When interest rates are elevated, mathematically prioritizing the guaranteed return of paying off high-cost debt - such as credit cards averaging 24% - heavily outweighs potential market investments. However, individuals should always secure their employer's 401(k) match and build a baseline emergency fund before aggressively tackling low-to-moderate-interest loans. The decision ultimately hinges on your specific loan rates, behavioral tendencies, and whether your debt is fixed or variable.

For over a decade following the 2008 financial crisis, the personal finance landscape was defined by cheap money. With central banks holding benchmark rates near zero, mortgage rates hovered near 3% and savings accounts yielded virtually nothing. The math for consumers was relatively simple: borrow cheaply, invest the excess cash in a booming stock market, and comfortably capture the spread.

Today's economic environment demands a radically different approach. Following a persistent period of central bank rate hikes and sticky inflation, the cost of borrowing has surged. Household debt in the United States reached $18.8 trillion by early 2026 1. At the same time, leading financial institutions project that stock market returns over the next decade will be far more modest than the historic bull runs of the 2010s 23. This structural shift requires households to fundamentally recalculate how they deploy their next available dollar, balancing the need for long-term wealth accumulation against the immediate, compounding threat of high-interest debt.

The Baseline: Comparing Costs of Capital vs. Expected Returns

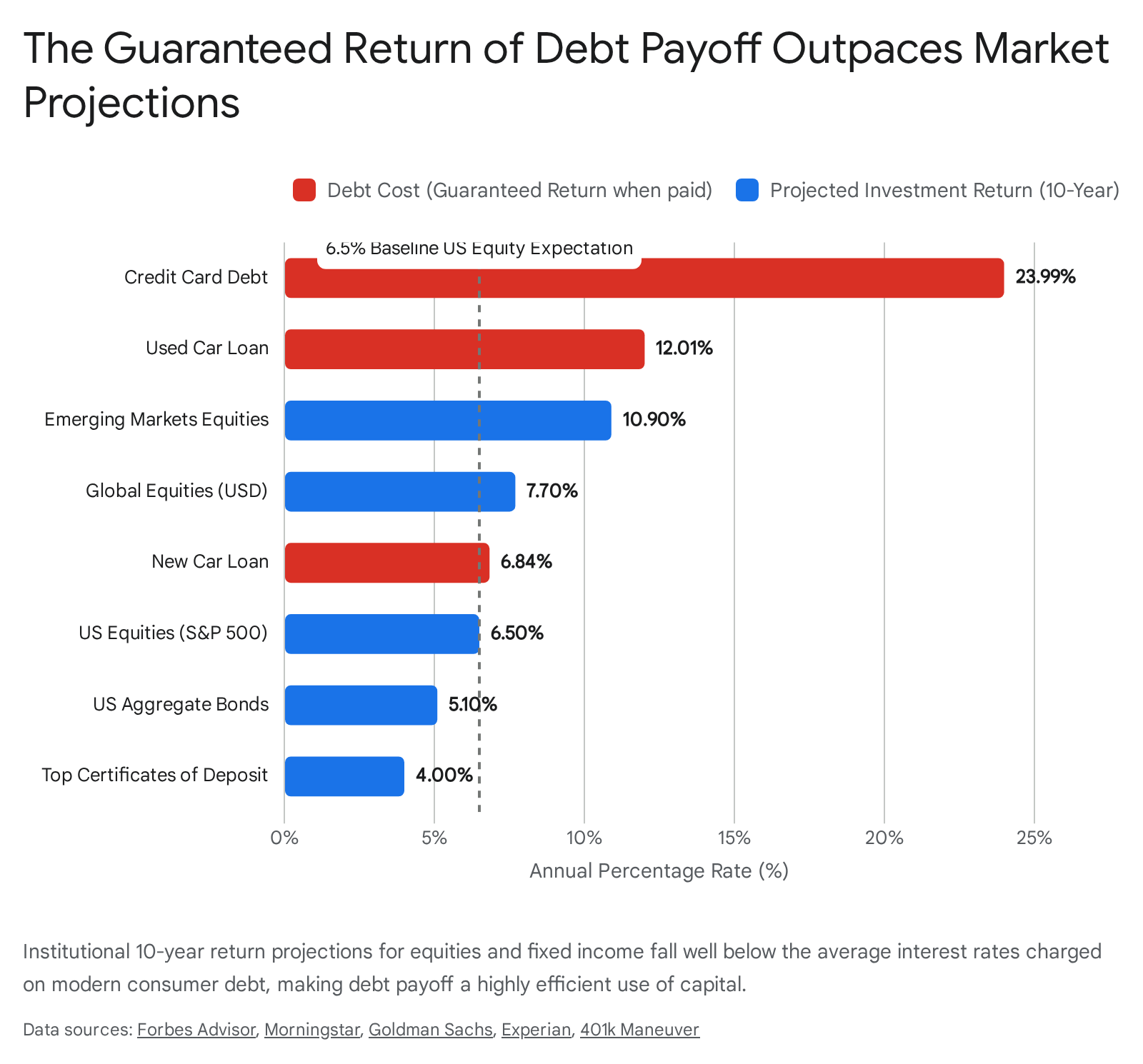

To make an informed decision on whether to aggressively pay down a debt or invest in the market, one must first understand the spread between the cost of capital and the expected return on investment. This spread dictates whether a household is experiencing positive or negative arbitrage.

The Staggering Cost of Modern Debt

Household debt balances have grown significantly across almost all categories, driven largely by persistent inflation and higher living costs. But it is the actual interest rates attached to this debt that have truly shifted the financial calculus.

Credit Cards: As of late 2025 and early 2026, the average credit card interest rate sits near a historic high of roughly 24% 45. Some non-prime store cards push even closer to 30% 4. Carrying a balance at this rate is universally considered a financial emergency. No reliable, legal investment in the public markets can outpace a guaranteed 24% hurdle rate. Every dollar applied to a credit card balance effectively yields a guaranteed, tax-free return of 24%.

Auto Loans: Vehicle financing has become a major wealth drain for the middle class. While the average new car loan rate for prime borrowers hovered around 6.37% to 6.80% in mid-to-late 2025, the picture is much darker for the used car market and for borrowers with less-than-perfect credit 56. Lenders rely heavily on credit scoring to price risk, creating massive disparities in the cost of capital for consumers buying identical vehicles.

| Credit Score Tier | VantageScore Range | Average New Car APR | Average Used Car APR |

|---|---|---|---|

| Super Prime | 781 - 850 | 5.18% - 5.25% | 6.82% - 7.13% |

| Prime | 661 - 780 | 6.27% - 6.87% | 9.06% - 9.98% |

| Non-Prime / Near Prime | 601 - 660 | 9.57% - 9.83% | 13.92% - 14.49% |

| Subprime | 501 - 600 | 13.17% - 13.18% | 18.86% - 19.42% |

| Deep Subprime | 300 - 500 | 15.77% - 16.01% | 21.55% - 21.85% |

| Data synthesized from Experian State of the Automotive Finance Market reports, Q2 - Q4 2025 5710. |

A deep subprime borrower paying 21% on a used car is facing costs similar to credit card debt. For these individuals, aggressively paying off the auto loan must take precedence over taxable brokerage investments.

Mortgages: While millions of homeowners locked in 30-year fixed rates below 4% prior to 2022, new buyers face rates fluctuating between 6% and 7% 8. The opportunity cost of holding a 7% mortgage is significantly different from holding a 3% mortgage, blurring the lines between when to invest and when to pay down principal.

Modest Expectations for Market Returns

While debt costs have risen, the long-term outlook for public equities has cooled due to elevated starting valuations, labor constraints, and shifting macroeconomic trends. Major asset managers have updated their 10-year to 15-year capital market assumptions for the 2025 - 2035 period, urging investors to tone down their expectations.

| Asset Manager | U.S. Equity 10-Year Annualized Forecast | Global Equity / Ex-U.S. Forecast | U.S. Aggregate Bond Forecast |

|---|---|---|---|

| J.P. Morgan | 6.7% | 7.0% (Global), 7.8% (Emerging) | ~5.0%+ (Forecasted robust term premia) |

| Goldman Sachs | 6.5% | 7.7% (Global), 10.9% (Emerging) | N/A |

| Vanguard | 2.8% - 4.8% | 7.3% - 9.3% (Global Developed) | 4.3% - 5.3% |

| Research Affiliates | 3.4% | N/A | 5.1% |

| Data synthesized from institutional Long-Term Capital Market Assumptions, 2025 - 2026 2391011. |

These forecasts reveal a striking consensus: broad U.S. equities are expected to return somewhere between 3.4% and 6.7% nominally over the next decade. When you compare a guaranteed 24% loss on credit card debt - or even a 10% loss on a used car loan - against an expected, highly variable 6.5% gain in the stock market, the winner is clear. You cannot borrow your way to wealth at double-digit interest rates.

The Financial Order of Operations (FOO)

Given the competing pressures of debt and investing, financial planners rely on a structured sequence known as the Financial Order of Operations (FOO). This framework removes the emotion from financial decision-making and dictates where the next dollar should logically go, preventing tactical paralysis 161213.

Step 1: Protect the Floor (Initial Emergency Fund)

Before paying an extra cent toward debt or investments, a household must establish a baseline emergency fund. This typically equates to enough cash to cover a primary insurance deductible - usually between $1,000 and $1,500 1613. Without this immediate cash buffer, any unexpected expense, such as a blown tire or a minor medical bill, will inevitably land back on a high-interest credit card. This cycle effectively undos any progress made on debt repayment and demoralizes the borrower 1920.

Step 2: Capture the Employer 401(k) Match

Even if a borrower is overwhelmed by 24% credit card debt, financial experts universally agree that they should almost never stop contributing to their 401(k) up to the level of their employer's match 41619.

The reasoning is purely mathematical. If an employer matches a contribution dollar-for-dollar, that is an immediate, guaranteed 100% return on investment. Even a standard formula of 50 cents on the dollar represents a 50% instant return 1612. No credit card interest rate and no speculative stock market rally can consistently compete with a 100% risk-free return. Pausing these contributions to pay off debt means leaving free compensation on the table. Over a 30-year career, the compound growth lost by skipping just a few years of employer matches can reduce a final retirement balance by hundreds of thousands of dollars 421.

If a borrower is in dire circumstances, they should scale back their 401(k) contributions only to the exact percentage required to capture the full match, redirecting all remaining cash flow toward debt 2122.

Step 3: Eliminate High-Interest Debt

Once the match is secured and a basic emergency fund is established, all excess cash flow should be directed like a laser at high-interest debt 1613.

The financial planning industry generally defines "high-interest debt" as anything carrying an annual percentage rate (APR) above 7% or 8% 162314. This category includes credit cards, personal loans, and modern auto loans. At these rates, the math definitively favors debt repayment over market investment. Every dollar used to pay down an 8% loan provides an 8% guaranteed, after-tax return - a benchmark that is incredibly difficult to beat consistently in public equities 1214.

Step 4 and Beyond: Full Emergency Fund and Maxing Accounts

Only after high-interest debt is completely eliminated should a household move to build a fully funded 3-to-6-month emergency reserve in a high-yield savings account (HYSA) 162025. Following that, the focus shifts to maximizing tax-advantaged accounts like Roth IRAs, HSAs, and the remainder of the 401(k) limit ($23,500 for individuals in 2025, plus catch-up contributions for those over 50) 161319.

Low-interest debt - such as an older 3% mortgage or a 4% federal student loan - sits at the very bottom of the priority list. Over a multi-decade horizon, a globally diversified equity portfolio will almost certainly outperform a 3% or 4% hurdle rate. Therefore, capital is far better deployed into index funds than into paying off cheap debt early 131925.

The Great Debate: Debt Snowball vs. Debt Avalanche

When confronting multiple debts simultaneously, borrowers are often paralyzed by which account to prioritize. Two prominent strategies dominate the behavioral finance landscape: the Debt Avalanche and the Debt Snowball 2627.

The Mathematical Optimizer: The Debt Avalanche

The debt avalanche focuses purely on mathematical efficiency. After making the required minimum payments on all accounts to stay current, you direct every extra dollar of cash flow toward the balance with the highest interest rate, regardless of the size of the balance 42715.

Mathematically, the avalanche is indisputably the fastest and cheapest route to a zero balance. By eliminating the most toxic, high-cost capital first, you stop the heaviest bleeding. You pay the absolute minimum in lifetime interest to the banks and reach debt freedom months faster than any other method 52616.

The Behavioral Optimizer: The Debt Snowball

The debt snowball, popularized largely by personal finance personalities like Dave Ramsey, actively ignores the interest rates. Instead, borrowers order their debts by balance size, from smallest to largest. Extra payments are applied to the smallest balance first 1617.

Why ignore the math? Because personal finance is largely driven by human behavior, not spreadsheets. Research from behavioral economists, including empirical analyses from Northwestern University and studies analyzing the Federal Reserve's Survey of Consumer Finances, has demonstrated that consumers who achieve quick, early victories by wiping out small accounts experience a surge in dopamine and motivation 163118.

This psychological momentum dramatically increases the probability that the borrower will actually stick to the plan over the grueling years required to become debt-free. As researchers note, habit-formation becomes essential when a task is long and difficult; tangibly crossing a debt off a list builds the behavioral reinforcement needed to survive the marathon 3118.

| Feature | Debt Avalanche | Debt Snowball |

|---|---|---|

| Target Priority | Highest interest rate first | Smallest balance first |

| Primary Advantage | Saves the most money on interest; mathematically optimal 2615. | Provides quick psychological wins; builds momentum and sustainable habits 2717. |

| Primary Disadvantage | Can lead to burnout if the highest-rate debt is massive and takes years to clear 1517. | Costs more in long-term interest; mathematically inefficient on paper 2615. |

| Best Suited For | Highly disciplined individuals motivated by spreadsheets and preserving capital 4. | Individuals who need visible progress and behavioral reinforcement to stay on track 1631. |

The Natural Overlap in the Real World

Interestingly, the fierce debate between these two methods is often rendered moot by reality. In many consumer debt portfolios, the two methods naturally overlap. Credit cards traditionally carry both the highest interest rates (often above 20%) and the smallest relative balances when compared to massive institutional loans like mortgages or student debt 5. Therefore, the mathematically optimal choice (the high-rate credit card) frequently happens to be the exact same account as the behaviorally optimal choice (the small-balance credit card). In these instances, the psychological path and the mathematical path become one and the same 515.

The Hidden Variable: Sequence of Returns Risk

When weighing debt payoff against investing, many people rely on simple "average return" calculators. They assume that if they can earn an average of 7% in the market, it makes mathematical sense to carry a 5% or 6% debt indefinitely. However, this logic completely ignores a critical financial hazard known as Sequence of Returns Risk 3334.

The Mechanics of Withdrawal Volatility

In the public markets, returns do not arrive in a smooth, predictable line. A 7% average annualized return over a decade might include a year where the market drops by 15%, followed by a year where it gains 24%, and then another where it drops 5% 3519.

During the "accumulation phase" of your career, when you are simply adding money to your 401(k), this volatility actually works in your favor through dollar-cost averaging. However, when you shift to the "distribution phase" in retirement and begin withdrawing funds to pay for living expenses, the order in which these returns occur becomes vital 3738.

If you experience severe negative returns early in your retirement timeline, it can permanently devastate your portfolio's longevity. Because the market is down, you are forced to sell a significantly higher volume of shares at depressed prices just to meet your fixed monthly living expenses. Those shares are now gone forever; they are no longer in the account to compound and grow when the market eventually recovers 3820.

Consider a classic hypothetical model: Two retirees both start with $500,000, both withdraw $25,000 a year, and both experience the exact same average market returns over 30 years - but in reverse order. Retiree A experiences a strong bull market in their first five years, while Retiree B experiences a severe bear market in their first five years. Despite identical average returns, Retiree A thrives and leaves a massive estate, while Retiree B completely runs out of money by year 18 38.

Debt Payoff as a Buffer Against Sequence Risk

Debt, unlike the stock market, operates on fixed mathematics. When you pay down debt, you lock in a guaranteed, risk-free rate of return. There is no market volatility, no sequence risk, and no anxiety.

For conservative investors or those approaching the "retirement red zone" (the five years before and after retiring), carrying a 6% or 7% mortgage into retirement introduces unnecessary sequence risk 34. By aggressively paying off the mortgage before retiring, you dramatically reduce your monthly fixed expenses. A lower baseline cost of living means you can withdraw far less from your volatile stock portfolio during a bear market. The guaranteed return of debt payoff effectively acts as a massive, stabilizing buffer against sequence of returns risk, ensuring your portfolio survives turbulent economic weather 333721.

Global Mortgage Structures and Opportunity Cost

The advice to invest instead of paying down a mortgage is not a universal truth; it is highly dependent on where you live. The underlying structure of global mortgage markets fundamentally alters how monetary policy affects the consumer, heavily influencing the risk calculus of household debt.

The U.S. 30-Year Fixed Anomaly

The United States is globally unique in its absolute dominance of the 30-year fixed-rate mortgage. This structure is not a product of the free market; it is largely made possible by government-sponsored enterprises (GSEs) like Fannie Mae, Freddie Mac, and Ginnie Mae. These agencies purchase and securitize the loans, effectively removing the long-term capital risk from local bank balance sheets and creating a massive secondary market for mortgage-backed securities (MBS) 222324. Currently, roughly 75% of the $13 trillion U.S. mortgage market is securitized 25.

Because of this unique system, an American homeowner who secured a 2.8% mortgage during the pandemic in 2020 will keep that exact interest rate and monthly payment through the year 2050, regardless of how high the Federal Reserve raises benchmark rates 26. For these U.S. homeowners, aggressively paying off a 3% mortgage while risk-free, high-yield savings accounts pay 4% or 5% is a mathematical error. The smartest move is to make the minimum payments, invest the difference, and allow inflation to slowly erode the real cost of the fixed debt over three decades 13.

The Global Variable Reality

In most advanced economies - including the United Kingdom, Canada, Australia, and much of Europe - mortgages are kept directly on the banks' balance sheets as portfolio loans 2227. Because banks cannot easily absorb 30 years of interest rate risk, the risk is passed directly to the consumer.

- Australia: The Australian market is highly sensitive to monetary policy, with approximately 70% of mortgages functioning entirely on variable rates 2848. As the Reserve Bank of Australia raises rates to fight inflation, homeowners see their required monthly payments increase almost immediately 26.

- United Kingdom and Canada: In these markets, mortgages are typically fixed for relatively short periods - usually two to five years - before they must be renegotiated and refinanced at prevailing market rates 252648.

- Securitization Rates: Compared to the U.S. rate of 75%, the U.K. securitizes only about 10% of its mortgage debt, while Australia and the Netherlands securitize a mere 5% 25.

| Country | Dominant Mortgage Structure | Rate Risk Bearer | Typical Securitization Rate |

|---|---|---|---|

| United States | 30-Year Fixed | Government / Investors (via MBS) | ~75% 25 |

| Canada | Short-Term Fixed (1 - 5 Years) | Consumer (at renewal) | Moderate 23 |

| United Kingdom | Short-Term Fixed (2 - 5 Years) | Consumer (at renewal) | ~10% 25 |

| Australia | Variable / Floating | Consumer (Immediate) | ~5% 25 |

When central banks aggressively hiked rates globally in 2022 and 2023, U.S. housing markets stayed remarkably resilient because current owners were perfectly insulated. In stark contrast, housing markets in Canada, Sweden, and Australia faced severe price corrections and cash-flow shocks as household debt became instantly more expensive 48.

The practical takeaway: If you live outside the U.S. and hold a variable or short-term fixed mortgage, paying down principal ahead of a rate reset is a highly defensive, lucrative strategy. Your debt cost is intrinsically linked to the current high-rate environment, making debt reduction a much higher priority than for an American borrower resting comfortably on a locked-in legacy rate.

Tax Implications: 2026 Legislation and Interest Deductions

Finally, when prioritizing investing versus debt payoff, a sophisticated plan must consider the after-tax cost of debt. The IRS allows taxpayers to deduct certain interest payments, which effectively lowers the real hurdle rate of borrowing. However, major legislative shifts taking effect in 2026 are altering this landscape.

The OBBBA and the New Tax Landscape

The Tax Cuts and Jobs Act (TCJA) of 2017 nearly doubled the standard deduction, causing the vast majority of taxpayers (around 92%) to stop itemizing their returns 29. If a taxpayer does not itemize, they receive zero tax benefit from paying mortgage interest, making the debt more expensive in real terms.

Many of these TCJA provisions were scheduled to sunset at the end of 2025. If fully allowed to expire, the standard deduction would have dropped back to roughly half its current level, pushing millions of Americans back into itemizing in 2026 and 2027 50. However, recent legislative maneuvers, notably the One Big Beautiful Bill Act (OBBBA), have permanently extended or modified several of these critical limits: * Mortgage Interest Limit: The $750,000 cap on acquisition indebtedness - which was reduced from the pre-2017 limit of $1 million - has been permanently locked in for newly issued mortgages. Mortgages issued prior to December 15, 2017, remain grandfathered at the $1 million limit 295152. Home equity loan interest remains largely non-deductible unless the funds are directly used to buy, build, or substantially improve the primary residence 2951. * State and Local Taxes (SALT): The heavily contested $10,000 SALT cap has been significantly expanded to $40,000 starting in the 2025 tax year, scaling upward by 1% annually through 2029 2930. However, this new cap phases out by 30% for every dollar a joint filer's Modified Adjusted Gross Income (MAGI) exceeds $500,000, fully reverting to $10,000 for earners over $600,000 30.

For a homeowner in 2026, checking whether your mortgage interest combined with your local property and state income taxes exceeds the robust standard deduction is crucial. If it does not, your mortgage interest is entirely unsubsidized by the government, and the "real" rate you pay is exactly what is printed on your statement 50.

Student Loan Interest Deductions

Borrowers can deduct up to $2,500 of interest paid on qualified student loans each year. Importantly, this is an "above-the-line" adjustment to income, meaning you can claim it regardless of whether you itemize or take the standard deduction 31323334.

However, this deduction phases out based on your income. For the 2025/2026 tax years, single filers with a MAGI over $85,000 (and joint filers over $170,000) see the deduction gradually reduced. It vanishes entirely for single filers earning $100,000 or more, and joint filers earning $200,000 or more 313335. If you are a higher-income earner who is phased out of this deduction, your student loan debt is functionally more expensive because it is paid entirely with after-tax dollars, increasing the mathematical incentive to pay it down faster 33.

Investment Margin Interest

For aggressive investors borrowing on margin, the IRS tracing rules allow you to deduct investment interest expenses - but only up to the amount of your net taxable investment income for the year 5936. This income includes ordinary dividends and short-term capital gains, but excludes qualified dividends and long-term capital gains unless the taxpayer makes a specific election to treat them as ordinary income 376238.

If your margin interest exceeds your investment income, the excess can be carried forward to future tax years 5936. While this makes margin loans generally more tax-efficient than personal loans or credit cards, the interest rate on the debt still must clear the hurdle of your expected, after-tax market returns to be a worthwhile endeavor. Given the high borrowing costs in 2026, relying on margin debt carries substantial risk if the market experiences a prolonged sideways or downward trend 6238.

Bottom line

In a high-interest environment, the core mathematics dictate that paying off expensive consumer debt - specifically anything carrying an APR above 7% to 8% - will consistently outperform volatile market investments. Earning a guaranteed, tax-free 24% return by paying off a credit card is a far superior use of capital than hoping for a 7% return in the equities market. However, financial mechanics must be balanced with human behavior; securing your employer's 401(k) match should remain absolutely non-negotiable to preserve long-term compounding, and utilizing the behavioral "debt snowball" method can provide the psychological momentum needed to stay the course. Ultimately, unless you reside in the U.S. and hold a legacy fixed-rate mortgage below 4%, heavily prioritizing debt elimination today is one of the most effective ways to guarantee your future returns and insulate your personal balance sheet against economic shocks.