The Beginner's Guide to Personal Finance

Mastering personal finance requires individuals to strategically prioritize capital allocation, aggressively manage debt, and harness the mathematical power of compound interest. By establishing a localized emergency buffer, optimizing employer benefits, and utilizing automated budgeting frameworks, households can transition from merely surviving paycheck to paycheck to building sustainable, long-term wealth.

The Intersection of Psychology and Money

If managing money were solely a matter of basic arithmetic, financial anxiety would be exceedingly rare. Instead, research indicates that roughly 53% of adults report that simply thinking about their financial situation induces anxiety, while 44% find discussing their finances highly stressful 1. The disconnect lies in the reality that personal finance is famously described as being 20% head knowledge and 80% behavior 2.

Traditional economic models - such as the Expected Utility Theory and the Efficient Market Hypothesis - have long assumed that humans act rationally, always seeking to maximize their wealth based on all available information 3. However, the academic discipline of behavioral finance has proven that real-world financial decisions are heavily influenced by cognitive biases, emotional triggers, and heuristics (mental shortcuts) that often sabotage long-term goals 456. Understanding these psychological hurdles is the foundational first step in any personal finance journey.

Cognitive Biases Shaping Financial Decisions

Academics and economists have identified several core biases that consistently derail sound financial planning:

- Loss Aversion: Coined by behavioral economists Amos Tversky and Daniel Kahneman in their foundational Prospect Theory, loss aversion dictates that the psychological pain of losing money is experienced far more intensely than the pleasure of gaining an equivalent amount 457. For a beginner, this often manifests as an irrational fear of investing in the stock market. Consequently, individuals hoard cash in low-yield savings accounts where it is slowly eroded by inflation, choosing a guaranteed loss of purchasing power over short-term market volatility 36.

- Overconfidence Bias: This is the tendency for individuals to overestimate their financial knowledge and their ability to predict market movements 45. Overconfident investors are significantly more likely to engage in excessive, rapid trading - often trying to "time the market" or pick individual winning stocks based on recent news. Research shows this behavior routinely leads to higher transaction costs and lower overall returns compared to simple, passive investing strategies 378.

- Herd Mentality and Recency Bias: Humans are inherently social creatures, which translates to a herd mentality in finance. Investors often follow the crowd into trendy assets at the peak of their valuation due to a fear of missing out, or they engage in panic-selling during a market downturn simply because others are doing so 347. This is compounded by recency bias, where individuals place undue weight on recent events, assuming a booming market will rise forever or a crashing market will never recover 348.

- Present Bias and Mental Accounting: People tend to heavily discount future rewards in favor of immediate gratification, making saving for a retirement that is forty years away feel distinctly unrewarding 9. Furthermore, individuals place money into different "mental accounts" based on its source or intended use. This can lead to highly irrational behaviors, such as keeping a $10,000 balance in a savings account earning a 4% yield while simultaneously carrying $5,000 in credit card debt that costs 24% annually, simply because the savings are mentally earmarked for "emergencies" 3.

Because humans are hardwired to make these cognitive errors, the most successful personal finance strategies are those that remove day-to-day decision-making from the equation. Automating savings, establishing strict budgeting rules, and adhering to a predefined order of operations can insulate portfolios from psychological blind spots.

The Financial Order of Operations (FOO)

Knowing exactly what to do with the next available dollar is the most common point of friction for beginners. Should one pay off student loans, save for a down payment on a house, or invest in a retirement account?

To solve this, financial professionals rely on prioritized roadmaps. While popular debt-reduction personalities advocate for rigid steps (such as paying off all non-mortgage debt before investing any capital), modern fiduciary advisors often utilize a more nuanced, mathematically optimized sequence known as the Financial Order of Operations (FOO) 611.

The FOO is a step-by-step strategy designed to balance the mathematical necessity of compound interest with the psychological need for risk mitigation, ensuring that every dollar deployed achieves its maximum potential.

Step 1: Establish an Immediate Safety Net

Before tackling consumer debt or investing for the future, individuals must protect themselves against minor financial shocks that would otherwise force them to borrow money. The immediate goal is to save enough cash in a liquid account to cover a household's highest insurance deductible (typically health or auto insurance, ranging from $1,000 to $5,000) 6. This initial cash reserve acts as a firewall, preventing a minor medical emergency or a vehicle repair from pushing a household into high-interest credit card debt 7.

Step 2: Claim the Employer Match

If an employer offers a retirement savings plan - such as a 401(k), 403(b), or the Thrift Savings Plan (TSP) - and matches employee contributions up to a certain percentage, contributing enough to capture that full match is the highest investment priority 67. An employer match is effectively a 50% to 100% guaranteed, instant return on investment. A return of this magnitude cannot be legally or reliably replicated anywhere else in the financial markets. Foregoing this step is the mathematical equivalent of refusing a portion of one's salary 6.

Step 3: Eradicate Toxic, High-Interest Debt

Not all debt is equal. "Toxic debt" generally refers to consumer debt with an annual interest rate exceeding 8% to 10%, primarily consisting of credit cards and payday loans 67. The stock market historically returns an average of around 7% to 10% per year after inflation 815. If an individual is carrying credit card debt at a 22% or 29% interest rate, no amount of investing will outpace the wealth destruction caused by that compounding debt 9. Paying off a 24% credit card provides a guaranteed, risk-free 24% return on capital 6.

Step 4: Fully Fund Emergency Reserves

Once high-interest debt is eliminated, the initial safety net must be expanded into a fully funded emergency reserve. This entails saving three to six months (or more, depending on geography and profession) of essential living expenses in a secure, accessible account 67. This reserve protects the household from catastrophic events like prolonged job loss or major medical crises without necessitating the liquidation of retirement assets .

Steps 5 and 6: Maximize Tax-Advantaged Retirement Accounts

With a secure financial foundation, focus shifts to aggressive wealth accumulation. The next priority is maximizing contributions to tax-advantaged accounts, specifically a Roth IRA and a Health Savings Account (HSA), before returning to max out employer-sponsored plans 610. * Roth IRA: Contributions are made with after-tax dollars, meaning no immediate tax deduction is realized. However, the investments grow entirely tax-free, and withdrawals in retirement are completely tax-free 1011. In 2025, the contribution limit for a Roth IRA is $7,000 for individuals under age 50 10. * Health Savings Account (HSA): Often labeled the ultimate retirement vehicle, an HSA offers a rare triple-tax advantage for eligible participants in high-deductible health plans. Contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses are tax-free 67.

After optimizing these individual accounts, individuals should return to their employer-sponsored 401(k) or 403(b) and increase contributions, striving to save a total of 15% to 25% of their gross household income across all investment vehicles 611.

Steps 7 to 9: Hyper-Accumulation and Low-Interest Debt

Only after securing a sustainable retirement trajectory should individuals focus on "abundance goals." These later steps include saving for a child's college education (e.g., funding a 529 plan), investing in taxable brokerage accounts, saving for a down payment on investment real estate, and eventually paying down low-interest debt, such as a primary mortgage or low-rate student loans 6117. Prioritizing the rapid payoff of low-interest debt too early in life starves a portfolio of the decades of compound growth it desperately needs 11.

| FOO Priority Level | Financial Action | Primary Objective | Relevant Accounts/Methods |

|---|---|---|---|

| Urgent | 1. Cover Highest Deductible | Prevent immediate reliance on credit during minor emergencies. | High-Yield Savings Account (HYSA) |

| Urgent | 2. Capture Employer Match | Secure guaranteed 50-100% returns via employer compensation. | 401(k), 403(b), TSP |

| High | 3. Eliminate Toxic Debt | Halt wealth destruction from high interest rates (>8-10%). | Avalanche or Snowball Method |

| High | 4. Full Emergency Fund | Insure against major job loss or medical events (3-12 months). | HYSA, Money Market Account |

| Medium | 5. Maximize Roth IRA & HSA | Utilize tax-free growth environments. | Roth IRA, HSA |

| Medium | 6. Maximize Employer Plans | Reach a 15-25% total gross income savings rate. | Traditional or Roth 401(k) |

| Low | 7-9. Future Goals & Low-Rate Debt | Fund college, buy real estate, prepay low-interest mortgage. | 529 Plan, Taxable Brokerage |

Budgeting Frameworks for Diverse Financial Profiles

A budget is simply the tactical execution of the Financial Order of Operations. Without a budget, it is impossible to direct capital to the appropriate steps efficiently. However, traditional budgeting - manually tracking every transaction on a complex spreadsheet - is tedious, mentally taxing, and frequently abandoned. Consequently, personal finance experts have developed several automated frameworks that align with different psychological profiles and income levels 192012.

The 50/30/20 Rule: Best for Beginners

The 50/30/20 rule is an intuitive, low-effort framework that requires minimal daily tracking. It divides a household's after-tax (take-home) income into three broad buckets: 1. 50% for Needs: Essential housing (rent or mortgage), groceries, utilities, basic transportation, insurance premiums, and minimum debt payments. 2. 30% for Wants: Dining out, subscriptions, hobbies, travel, and discretionary entertainment. 3. 20% for Savings and Debt Payoff: Emergency fund contributions, retirement investing, and extra principal payments on toxic debt 19202223.

This method is highly popular because it provides a big-picture guideline without requiring strict categorization of every purchase 1922. However, the 50/30/20 rule is increasingly difficult to implement in high-cost-of-living urban areas, where rent and utilities alone might consume 50% or more of an individual's take-home pay. In such cases, experts recommend adjusting the ratios to realistic alternatives, such as a 60/25/15 rule 20. For lower-income households, a 70/20/10 rule (allocating 70% to living expenses, 20% to savings, and 10% to debt or giving) ensures that the habit of saving remains intact even if the percentages shift 12.

Zero-Based Budgeting: Best for Debt Payoff

With Zero-Based Budgeting (ZBB), individuals assign a specific job to every single dollar they earn before the month begins. The core formula dictates that Income minus Planned Expenses, Savings, and Debt Payments must equal exactly zero 1920122223.

If a household brings home $4,000 a month, they must proactively allocate all $4,000 to distinct categories (e.g., $1,200 to rent, $400 to food, $300 to savings, $200 to transportation, etc.) 19. ZBB requires significant effort and ongoing tracking, often facilitated by digital tools like YNAB (You Need A Budget) or Monarch Money 1222. However, it provides maximum control, forces consumers to confront spending leaks, and prevents the common phenomenon where money simply "disappears" by the end of the month. ZBB is highly recommended for individuals aggressively fighting their way out of debt or managing tight, variable incomes 192012.

The Envelope System: Best for Overspenders

For those who struggle with impulse control - particularly in variable categories like dining out, entertainment, or apparel - the Envelope System relies on physical or digital friction. An individual allocates a set amount of cash for problem categories and places that cash in physical envelopes. When the dining out envelope is empty, the individual cannot eat at restaurants until the following month. There is no borrowing from other envelopes and no relying on credit cards 192012. Today, many modern banking applications offer "digital envelopes" or sub-accounts that replicate this behavioral boundary without requiring the inconvenience of physical cash 20.

| Budgeting Framework | Effort Level | Primary Mechanism | Best Suited For | Recommended Tools |

|---|---|---|---|---|

| 50/30/20 Rule | Low | Broad percentage buckets based on take-home pay. | Beginners, stable incomes, low-stress planners. | Rocket Money, Spreadsheets 12 |

| Zero-Based Budgeting | High | Every dollar assigned a job; Income - Expenses = $0. | Aggressive debt payoff, tight control seekers. | YNAB, EveryDollar 12 |

| Envelope System | Medium | Hard limits on specific spending categories using cash/sub-accounts. | Chronic overspenders, impulse buyers. | Cash, Digital Sub-accounts 2012 |

| Pay-Yourself-First | Low | Automating savings immediately; spending whatever is left. | Natural savers, investors, anti-budgeters. | Empower, Automated bank transfers 2012 |

The Academic Debate: Debt Repayment Strategies

Once a budget is established and a baseline emergency fund is funded, the next major hurdle for most beginners is eliminating existing consumer debt. Mathematical logic dictates one approach to this problem, while behavioral psychology dictates another. This tension has resulted in two distinct, widely debated debt payoff methodologies: the Debt Avalanche and the Debt Snowball.

The Debt Avalanche: Mathematical Optimization

The Debt Avalanche method dictates that a consumer makes minimum payments on all outstanding debts, but directs every spare dollar in their budget toward the debt with the highest interest rate, regardless of its total balance. Once that highest-rate debt is cleared, the consumer rolls those payments into the debt with the next highest interest rate 291325.

Mathematically, the Debt Avalanche is the undisputed champion. By eliminating the most expensive debt first, the borrower minimizes compounding interest, pays the least amount of total money to creditors, and achieves a debt-free status in the shortest possible chronological timeframe 292514.

The Debt Snowball: Behavioral Modification

Popularized heavily by financial entertainers and authors, the Debt Snowball method ignores interest rates entirely. Instead, the consumer lists all debts in ascending order from the smallest dollar balance to the largest. They pay minimums on everything, but aggressively attack the smallest balance first. Once the smallest debt is eradicated, the money previously allocated to it is "snowballed" into the payment for the next smallest debt 29132515.

This method capitalizes directly on human psychology. By securing quick, visible "wins" early in the process, the debtor receives a psychological boost and a dopamine hit that sustains their motivation through a long, arduous financial journey 292515.

Empirical Evidence on Repayment Efficacy

The efficacy of these two methods has been heavily researched in academic literature, yielding fascinating results that challenge purely mathematical assumptions.

A pivotal study published in the Journal of Marketing Research by Amar and Ariely (2011) explored the concept of "debt account aversion." Their research found that consumers naturally focus on reducing the total number of outstanding loans rather than minimizing the total mathematical debt across all loans. Even when researchers explicitly showed participants how much interest they were losing by paying small debts first, the participants largely ignored the math in favor of the emotional satisfaction of closing an account 3281617.

Further supporting the psychological approach, a 2014 study by the National Bureau of Economic Research (Brown & Lahey) found that individuals completed mildly unpleasant tasks significantly faster when the tasks were broken down into parts arranged in ascending order of size (smallest to largest). This research validated the core premise of the "small victories" approach, demonstrating that momentum plays a massive role in task completion 181920.

Furthermore, the financial penalty of choosing the Snowball method over the Avalanche method may not be as severe as critics claim. A 2018 empirical analysis of Federal Reserve data conducted at James Madison University concluded that while the Avalanche method is technically faster in the vast majority of cases, the Snowball method is a "very close competitor" that offers substantial psychological benefits 1415.

A comprehensive study by LendingTree analyzed average consumer debt loads - featuring a realistic mix of credit cards, auto loans, and student loans - and found that the difference in total money paid between the two methods was often negligible. In their most representative scenario, the total repayment time for both methods was exactly the same (57 months), and utilizing the mathematically optimal Avalanche method only saved the consumer a total of $29 over nearly five years of repayment 13.

Ultimately, if an individual is highly disciplined and motivated by spreadsheets, the Avalanche method will save every possible penny of interest. However, if a consumer has previously failed to stick to a debt payoff plan, or if they feel overwhelmed by the sheer number of creditors they owe, academic evidence suggests the Debt Snowball is the superior choice for ensuring behavioral adherence.

The Science and Geography of the Emergency Fund

An emergency fund is not an investment designed to build wealth; it is financial insurance. It is a pool of highly liquid cash designed to protect long-term investments and prevent households from taking on high-interest debt when disaster strikes.

The necessity of this buffer is stark. According to the Federal Reserve's 2024 Economic Well-Being report, only 63% of U.S. adults could cover a hypothetical $400 emergency expense using cash or its equivalent, leaving over a third of the population vulnerable to minor financial shocks 21. Furthermore, a national survey by Bankrate in late 2025 found that nearly one in four Americans (24%) possess absolutely no emergency savings 22.

The psychological toll of this vulnerability is profound. A comprehensive study by Vanguard revealed that individuals without emergency savings spend an average of 7.3 hours per week stressing about their finances, compared to only 3.7 hours for those with at least a $2,000 buffer 23. Furthermore, those lacking emergency savings reported significantly lower productivity at work due to financial distraction, and maintaining a basic $2,000 fund was associated with a 21% higher baseline financial well-being score 23.

Geographic Discrepancies: U.S. vs. European Safety Nets

The universal rule of thumb touted in personal finance literature is to save "three to six months of essential living expenses" 2237383940. However, macroeconomic research shows that this advice is heavily dependent on a country's established social safety net.

In the United States, personal financial risk is notably high. The U.S. relies on fragmented, largely privatized healthcare systems and comparatively weaker unemployment protections. In 2024, U.S. total health expenditure reached approximately $14,900 per capita - more than double the OECD average of roughly $6,000 for wealthy European nations 414224. Because a job loss in the U.S. frequently equates to an immediate loss of employer-sponsored health insurance, and out-of-pocket medical costs can quickly become catastrophic, American financial planners frequently push the emergency fund recommendation to six to twelve months of living expenses 382545.

Conversely, in many European countries, the state assumes a significant portion of individual risk. Universal, tax-funded healthcare systems ensure that a medical emergency does not result in personal bankruptcy, and robust wage-support programs provide a thicker safety net during economic downturns 414225. To fund these systems, European citizens typically pay higher taxes and social security contributions (e.g., France at 16% of GDP versus the U.S. at 6% in recent years) 25. Studies on asset poverty published in the journal Social Inclusion confirm that generous social security systems in Europe drastically reduce household vulnerability to sudden income shocks compared to the U.S. 462627. Therefore, for a securely employed salaried worker in Western Europe, an emergency fund of three to six months is generally highly sufficient 4528.

| Geographic & Employment Profile | Recommended Cash Buffer | Primary Rationale and Risk Factors |

|---|---|---|

| Western Europe (Salaried) | 3 to 6 months | Strong public healthcare; robust unemployment safety nets mitigate severe individual financial risk 4546. |

| United States (Salaried) | 6 to 9 months | High out-of-pocket healthcare costs; critical risk of losing health insurance linked directly to employment 4245. |

| Global (Self-Employed/Freelance) | 9 to 12+ months | Highly variable income; lack of employer severance packages; often excluded from standard state unemployment benefits 4528. |

Opportunity Cost and High-Yield Savings Accounts

An emergency fund must be highly liquid (accessible within 24 to 48 hours) and perfectly insulated from market volatility. It should never be invested in the stock market, where a crash could diminish the fund precisely when a job loss occurs.

For optimal balance, the standard vehicle is a High-Yield Savings Account (HYSA) or a Money Market Account (MMA) offered by FDIC or NCUA-insured online banks 37383929. While traditional brick-and-mortar banks pay a paltry national average of around 0.39% to 0.42% APY, HYSAs have historically offered rates exponentially higher, allowing cash reserves to somewhat pace with inflation without taking on principal risk 373031.

It is vital to understand that HYSA rates are variable and directly tied to the central bank's benchmark interest rates. As the Federal Reserve cuts interest rates to stimulate the economy - as occurred in late 2024 and throughout 2025 - HYSA yields naturally drop from peaks of 5.5% down toward the 3% or 4.5% range 37303153. Despite these rate drops, maintaining funds in an HYSA remains vastly superior to a traditional savings account, ensuring liquidity while mitigating the opportunity cost of holding cash 3031.

Investing and the Mathematics of Compound Interest

Saving money simply preserves existing wealth; investing is the mechanism used to build it. Because inflation constantly erodes the purchasing power of fiat currency, a dollar saved under a mattress loses value every year. To achieve financial independence or retirement, capital must grow faster than the rate of inflation.

Historically, the broader stock market (often represented by the S&P 500 index) has returned an average of roughly 7% to 10% per year over the long term, after adjusting for inflation 815.

The Democratization via Fractional Shares

A persistent barrier to entry is the myth that individuals need thousands of dollars to begin investing. This is no longer accurate. The rise of zero-commission brokerages (such as Robinhood, M1 Finance, and Fidelity) and the invention of fractional shares have entirely democratized the financial markets. Today, an investor can use as little as $1 to buy a fractional slice of an expensive blue-chip stock or an Exchange-Traded Fund (ETF) 3255563358.

For beginners, the consensus expert advice is to avoid the high risk of picking individual stocks. Instead, investors are encouraged to purchase broadly diversified, low-cost Index Funds or ETFs. These funds bundle hundreds or thousands of companies together (e.g., buying a proportional piece of the entire U.S. stock market in a single transaction), providing instant diversification and significantly lowering portfolio risk 5633.

The Unrelenting Power of Exponential Growth

The most critical factor in investing is not how much money an individual earns, nor is it achieving the highest possible annual return; it is time in the market.

Compound interest is the process where the returns on investments begin generating their own returns, creating an exponential snowball effect. To understand this mathematically, investors utilize the "Rule of 72," a fast mental model used to estimate doubling time. By dividing the number 72 by the expected annual return rate (e.g., 7%), an investor finds that their money will double roughly every 10 years without adding any additional principal 3435.

Because the growth is exponential rather than linear, the dollars invested in an individual's 20s do disproportionately more work than the dollars invested in their 40s. Every year delayed forfeits not just one year's growth, but decades of compounding on top of that year's growth 35.

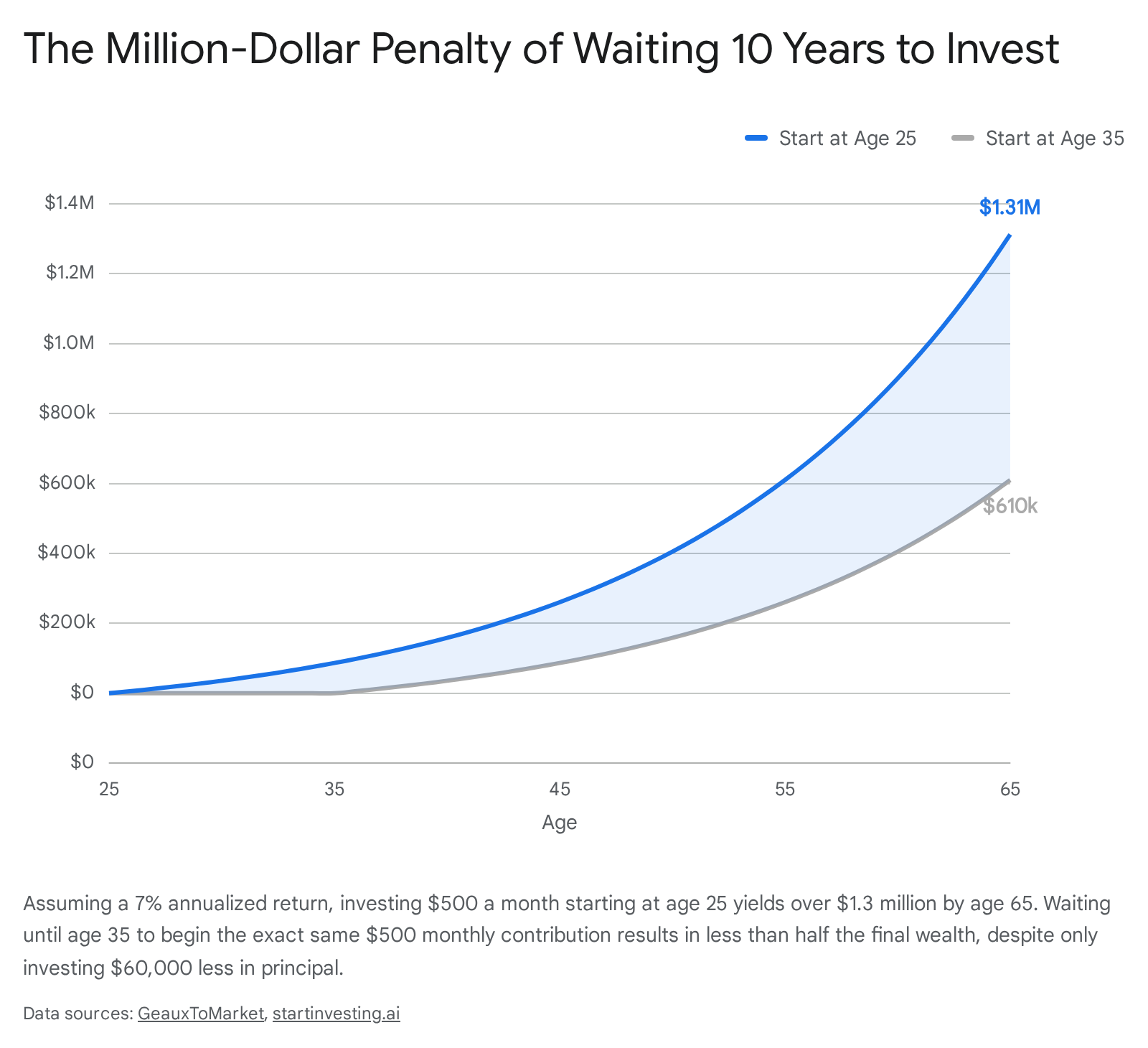

The Cost of Waiting: Age 25 vs. Age 35

To illustrate this mathematical reality, consider a comparison of two investors: * Investor A (Starts at 25): Invests $500 per month consistently from age 25 to age 65. * Investor B (Starts at 35): Invests the exact same $500 per month, from age 35 to age 65.

Assuming a standard 7% annualized return, Investor A will retire with approximately $1.31 million 8. Investor B, who waited just 10 years to begin, will retire with roughly $612,000 8. Investor B contributed only $60,000 less in out-of-pocket principal, yet lost out on nearly $700,000 in final wealth simply due to the compressed timeline 8.

The only way for Investor B to "catch up" to Investor A is to drastically increase their monthly contributions to a level (often 3 to 4 times the original amount) that is unsustainable for an average salary 8.

Financial Strategy in Volatile Global Economies

It is critical to note that nearly all standard personal finance advice - save a cash emergency fund, invest in local index funds, rely on domestic banks - is inherently Western-centric. It assumes a relatively stable economy with low, predictable inflation (typically targeted around 2% by central banks) 613663.

In macroeconomic environments plagued by systemic, hyper-inflationary pressures, the standard playbook is not just ineffective; it is financially destructive.

Consider countries like Argentina and Türkiye, which in recent years have faced inflation rates ranging from 75% to over 270% 37653839. In these environments, the local currency loses its purchasing power on a daily basis. The "invisible tax" of inflation means that holding a cash emergency fund in an Argentine Peso or Turkish Lira bank account is a guaranteed mathematical loss, even if the local bank offers an interest rate of 40% 61366540. When nominal interest rates remain below the actual inflation rate, the real return is deeply negative, rendering traditional saving impossible 373940.

Therefore, the fundamentals of personal finance shift drastically depending on geography and monetary stability: * In Low-Inflation Economies (US/EU): The strategy is Earn, Save, Invest locally. Cash is a safe harbor for short-term needs, and local stock markets are reliable long-term growth engines 61. * In High-Inflation Economies: The default behavior is to immediately convert local currency into assets that hold global value to survive the slow bleed of inflation. Citizens survive by purchasing foreign currency (usually US Dollars), acquiring tangible hard assets (real estate, vehicles, or even stockpiling non-perishable consumer goods), or utilizing digital stablecoins tied to the US Dollar to bypass volatile local banking systems and preserve value 61363765.

For the average individual in a stable economy, moderate inflation (3% to 5%) simply dictates that long-term wealth must be invested in equities or real estate rather than cash. Furthermore, during periods of higher inflation, consumers should prioritize paying off variable-rate debt (like credit cards) while retaining fixed-rate debt (like a low-interest 30-year mortgage), as inflation mathematically makes fixed-rate debt cheaper to pay off over time 634170.

Debunking Persistent Personal Finance Myths

Financial literacy is often hindered by outdated adages passed down through generations. To build a modern financial foundation, several persistent myths must be discarded:

Myth 1: Earning a high income automatically generates wealth. Wealth is not defined by income; it is defined by net worth (total assets minus total liabilities) 71. A physician earning $300,000 a year who spends $310,000 annually on luxury vehicles, massive mortgages, and vacations is accumulating debt, not wealth. Conversely, a teacher earning $60,000 who consistently invests a portion of their income into compound-interest accounts will mathematically achieve millionaire status over a working lifetime 7242. Wealth is measured by what is saved and invested, not by what is spent 72.

Myth 2: Debit cards are always better and safer than credit cards. While debit cards prevent consumers from spending money they do not possess, they offer vastly inferior consumer protections compared to credit cards. If a fraudster steals debit card information, they are directly draining a personal checking account, tying up cash needed for rent and groceries 7274. If a credit card is compromised, the fraudster is spending the bank's money, which is legally much easier to dispute and recover 72. Furthermore, responsible use of a credit card - paying the statement balance in full every single month to avoid all interest - builds a strong credit history, which is required to secure favorable mortgage rates, rent apartments, and reduce insurance premiums 72744344.

Myth 3: Buying a home is always a better financial decision than renting. The common adage that "renting is throwing money away" is a dangerous oversimplification. Homeownership carries massive, unrecoverable "sunk costs" that do not build equity: property taxes, homeowners association (HOA) fees, routine maintenance, structural repairs, and mortgage interest (which amortizes heavily in the first decade of a loan) 727443. Renting provides maximum geographical flexibility, highly predictable monthly liabilities, and zero maintenance costs 7274. If an individual plans to move within five years, or if they possess the discipline to invest the difference between their rent and what a total mortgage payment would cost directly into the stock market, renting frequently outperforms homeownership mathematically.

Bottom line

The foundation of personal finance relies on recognizing and controlling human behavior just as much as understanding mathematical principles. By establishing a prioritized order of operations - starting with a targeted emergency fund, eliminating toxic high-interest debt, and automating investments into diversified index funds - anyone can build long-term stability regardless of their starting income. Ultimately, time in the market is an investor's greatest asset, provided they continuously adapt these principles to their specific geographic reality and local monetary environment.