Short Interest and Synthetic Supply in Low-Float Equities

The structural mechanics of modern equity markets face unique stress tests during the initial public offerings (IPOs) of mega-cap companies with artificially constrained public floats. This phenomenon, heavily concentrated in special purpose acquisition company (SPAC) mergers, corporate spin-offs, and listings engineered with massive insider retention, generates severe supply-and-demand imbalances within the securities lending market. When fundamental valuation metrics suggest significant downside risk, institutional investors and event-driven hedge funds aggressively seek to establish short positions. However, the lack of available physical shares to borrow drives the cost of financing to exorbitant levels.

In response to this mechanical friction, sophisticated market participants pivot to derivative markets to bypass physical borrow constraints, creating synthetic short exposure. This process relies heavily on options market makers who utilize specific regulatory exemptions to short stock without pre-borrowing, effectively manufacturing synthetic supply. While this provides immediate liquidity to a frozen market, it systematically displaces the settlement burden, resulting in massive accumulations of failed trades - categorized as fails-to-deliver (FTDs) - at the central clearinghouse level. The intersection of restricted physical floats, extreme borrow costs, options market arbitrage, and delayed settlement presents significant, ongoing challenges for prime brokerage risk management frameworks and global financial regulators.

Float Dynamics and the Securities Lending Ecosystem

The fundamental viability of short selling depends entirely on the availability of a liquid secondary market and a robust securities lending ecosystem. In a standard traditional IPO, the underwriting syndicate guarantees a wide distribution of shares to various institutional portfolios, mutual funds, and retail investors, establishing a baseline public float capable of supporting continuous two-way trading. However, alternative listing mechanisms have disrupted this equilibrium by introducing massive nominal market capitalizations built upon extremely thin trading floats.

Structural Constraints in Special Purpose Acquisition Companies

Special purpose acquisition companies (SPACs) merge with private companies to bring them public via a mechanism that frequently bypasses the rigorous institutional price-discovery process of a traditional IPO. The architecture of a SPAC merger involves heavy insider share retention, extended lock-up periods for private investment in public equity (PIPE) participants, and historically high redemption rates by the original SPAC shareholders prior to the merger's consummation. Consequently, when the "de-SPAC" transaction is finalized and the target company's ticker begins trading, the actual number of shares available for free trading (the public float) is often a fractional percentage of the company's total shares outstanding 12.

Because the total market capitalization of the enterprise is calculated using the total shares outstanding, the newly public company may achieve a "mega-cap" valuation - sometimes reaching tens of billions of dollars - while trading on a micro-cap float consisting of only a few million available shares. This structural scarcity creates a highly volatile pricing environment where minimal buying or selling pressure causes violent intraday price swings. Furthermore, because long-oriented institutional investors, mutual funds, and exchange-traded funds (ETFs) typically avoid holding unseasoned SPACs, the natural lending pool for these newly listed securities is virtually non-existent 3.

Securities Lending Market Imbalances

The securities lending market operates strictly on supply and demand dynamics. Prime brokers source shares from the long portfolios of their institutional clients - such as pension plans, endowments, and insurance companies - and lend them to short-selling hedge funds for an annualized fee 4. When a stock possesses a low float combined with high institutional skepticism regarding its valuation, the demand to borrow shares vastly outstrips the available supply.

This tension is tracked via the "utilization rate," a metric that measures the percentage of the total available lending pool that is currently deployed on loan. When utilization approaches 100%, the stock is formally designated as "hard-to-borrow" (HTB) by clearing firms 3. At this threshold, the cost to borrow (CTB) the stock - expressed as an annualized percentage fee paid by the short seller to the lender - increases non-linearly. While the average CTB for a highly liquid, large-cap stock is generally between 0.3% and 3.0%, the fee for a restricted-float mega-cap can rapidly exceed 100%, and in extreme squeeze scenarios, approach 800% 14.

The Mathematical Constraints of Elevated Borrow Costs

High borrow costs fundamentally alter the mathematics and viability of short selling. A short seller paying a 200% annualized borrow fee must see the stock decline by approximately 0.55% every single calendar day merely to offset the financing cost. This extreme carrying cost forces short sellers to continuously balance their fundamental conviction against the mechanical bleed of their portfolio's capital.

If the stock price remains flat, or worse, increases due to a retail-driven short squeeze, the mark-to-market losses combined with the daily borrow fees can rapidly trigger prime brokerage margin calls 23. The theoretical risk of short selling is infinite, but in low-float environments, the practical risk is accelerated by the compound pressure of illiquidity and exorbitant daily financing drains, forcing capitulation even when the underlying short thesis is fundamentally sound 2.

Case Studies in Structural Imbalance

The theoretical mechanics of borrow constraints and float restrictions are best observed through specific, recent market events involving mega-cap entities entering the public market. A comparison between highly constrained listings and traditionally structured IPOs highlights the direct, causal relationship between float size, borrow cost, and the subsequent rate of settlement failures.

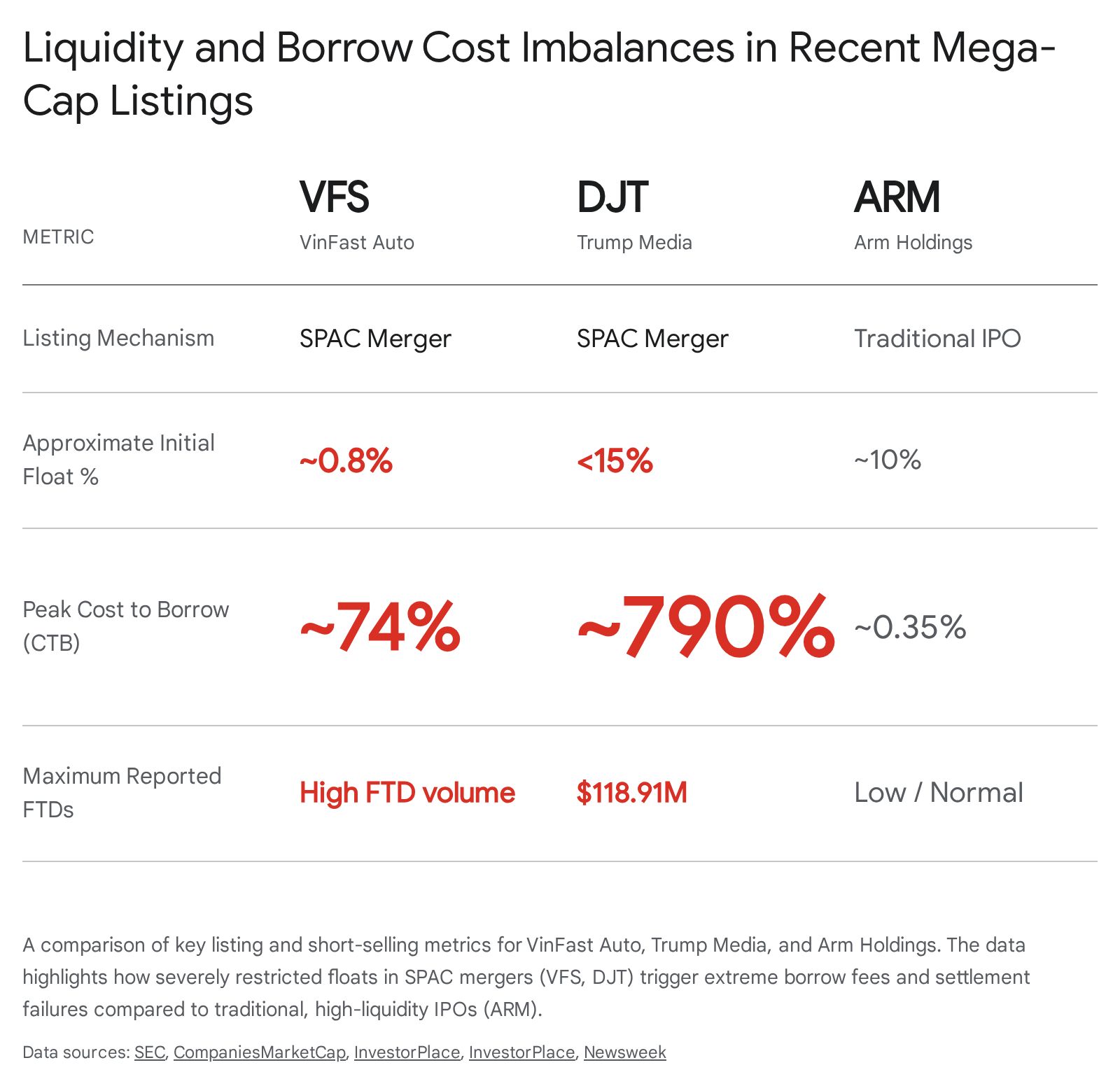

VinFast Auto: Extreme Market Capitalization Anomalies

VinFast Auto (VFS) completed its merger with Black Spade Acquisition and began trading on the Nasdaq on August 15, 2023 1. The transaction initially valued the Vietnamese electric vehicle manufacturer at approximately $23 billion. However, following a brief period of extreme market volatility, the company's market capitalization surged, briefly surpassing the valuations of entrenched legacy automakers like Ford and General Motors. This price action occurred despite the company's deep structural unprofitability; for instance, the company later reported a net loss of $1.12 billion in the first quarter of 2026 alongside heavy reliance on related-party funding from Vingroup to sustain operations 759.

The massive valuation disparity attracted intense short seller interest. However, the fundamental structure of the listing created a severe mechanical bottleneck: out of an implied 2.32 billion shares outstanding, the initial public float was estimated to be between a mere 17 million and 21 million shares 1. Consequently, while only about 1.2 million shares were sold short shortly after the listing (amounting to an insignificant 0.05% of total shares outstanding), this short interest represented roughly 6% of the available public float 1.

Because the vast majority of shares were controlled by Vingroup and its chairman, and thus legally restricted from the lending pool, securities lending utilization rates rapidly exceeded 92% 6. The cost to borrow VFS stock spiked to 74.04% within days of the listing, actively repelling fundamental short sellers who could not absorb the carry cost 1. Over subsequent months, as initial volatility subsided and marginally more shares entered the lending market, the borrow fee stabilized to a lower, yet still highly elevated, annualized rate of approximately 9.1% 11. While the exact daily fail-to-deliver volumes and specific daily borrow fee percentages for the precise 30-day window following the listing are unavailable in the public record 7, subsequent SEC data releases showed millions of euros in FTD volumes persisting through later quarters 8.

Trump Media and Technology Group Volatility

Trump Media & Technology Group (DJT) entered the public markets via a SPAC merger with Digital World Acquisition Corp (DWAC) in late March 2024. Similar to the VinFast event, the listing featured a stark divergence between corporate financial fundamentals and equity market valuation. For the nine months ended September 30, 2023, the company generated just $3.37 million in revenue and posted a net loss exceeding $712 million, yet commanded a market capitalization of approximately $7.5 billion shortly after the merger was consummated 21415.

The resulting fundamental demand to short the stock was overwhelming, rapidly establishing DJT as the most shorted SPAC in the United States by late March 2024 2. Prime brokers and institutional lenders, recognizing the extreme inelasticity of the short demand and the tiny pool of lendable shares, increased financing rates dramatically. Borrow fees for DJT reached an annualized rate of 157.57% in late March, and according to daily data from Interactive Brokers, surged to an extraordinary peak of 790% in early April before eventually sliding back to 124% as the underlying stock price began to decline 24.

The absolute scarcity of borrowable shares led to significant and prolonged settlement issues. DJT remained entrenched on the SEC's Regulation SHO Threshold List for 179 days, with maximum fails-to-deliver reaching $118.91 million in notional value on a single day 7. Due to the exorbitant carrying costs, short sellers who maintained their positions despite the high fees incurred severe mark-to-market and financing losses, which data analytics firm S3 Partners estimated at $158 million for the year by late March 2024 2. Although comprehensive daily FTD data and exact borrow fee trajectory charts for the first 30 days of trading are not publicly aggregated in the provided research material 7, the available data confirms a period of extreme systemic stress on the clearing ecosystem.

Arm Holdings as a Traditional Market Counterpart

By contrast, the listing of Arm Holdings (ARM) on September 14, 2023, provides a vital counter-example of how a traditional IPO structure mitigates the synthetic supply problem, even when the parent company retains massive ownership. SoftBank Group took Arm public, offering 95.5 million American depositary shares (ADSs) at $51.00 each, raising nearly $5 billion and valuing the semiconductor design company at over $54 billion 910. Following the listing, SoftBank retained a 90.6% ownership stake, meaning the true public float was technically less than 10% of the company 10.

Despite this relatively low float percentage relative to total shares, the absolute number of shares introduced to the market (95.5 million) provided exceptionally deep liquidity. Furthermore, because the listing was fully underwritten by major investment banks with extensive prime brokerage and equity distribution arms (including Barclays, Goldman Sachs, and J.P. Morgan), institutional distribution was widespread across mutual funds and ETFs 9. This diverse institutional distribution seeded the securities lending market effectively on day one. Consequently, the cost to borrow ARM shares remained completely normalized, hovering around 0.28% to 0.35% annualized, indicative of a highly liquid, stable security 11. The lack of borrow friction allowed natural, fundamental price discovery without the generation of massive FTDs or the need for options market synthetic supply.

| Metric | VinFast Auto (VFS) | Trump Media (DJT) | Arm Holdings (ARM) |

|---|---|---|---|

| Listing Mechanism | SPAC Merger | SPAC Merger | Traditional IPO |

| Total Valuation at Debut | ~$23 Billion | ~$7.5 Billion | ~$54 Billion |

| Estimated Initial Float | 17M - 21M Shares | Highly Restricted | 95.5M ADSs |

| Peak Cost to Borrow (Ann.) | ~74.04% | ~790.00% | ~0.35% |

| Settlement Stress Indicator | High FTD Volume | 179 Days on Threshold List | Normal Settlement |

Table 1: Comparative liquidity and short-selling metrics highlighting the divergence in market mechanics between restricted-float SPACs and traditional IPOs.

Options Market Arbitrage and Synthetic Supply Creation

When the physical cost to borrow a stock vastly exceeds the fundamental downside expected by an institutional investor, the physical short trade becomes economically unviable. Instead, sophisticated market participants transition to the options market to achieve equivalent directional economic exposure. This shift transfers the systemic burden of locating hard-to-borrow shares from the hedge fund to the options market maker.

Reverse Conversions and Put-Call Parity Distortions

To synthesize a short position without borrowing the physical stock, a trader utilizes an arbitrage strategy. The trader purchases an at-the-money put option and simultaneously sells an at-the-money call option with the exact same strike price and expiration date. This combination creates a "synthetic short" position, which perfectly mirrors the delta (directional pricing exposure) of a physical short sale 1920.

When a hedge fund executes this trade, an options market maker must take the other side, effectively becoming synthetically long the stock (short the put, long the call). To hedge this long exposure and return their trading book to a delta-neutral state, the market maker is forced to short sell the underlying physical stock 712.

This entire mechanism relies on fundamental options pricing theory, specifically put-call parity. Put-call parity dictates that the difference in price between a European-style call and a put of the same strike and expiration should equal the difference between the current stock price and the present value of the strike price 1213. However, in hard-to-borrow stocks, the exorbitant borrow fee acts mathematically as a massive, continuous negative dividend yield. Options pricing models dynamically account for this implied borrow rate. Consequently, the premium of put options becomes heavily inflated relative to call options 2023. Arbitrageurs attempting to exploit this apparent pricing disparity - by buying the artificially cheap call, selling the expensive put, and shorting the physical stock - find that the massive physical borrow fees they must pay entirely negate the apparent arbitrage profit 2023. The options market is highly efficient in pricing in the exact cost of the physical borrow constraint.

Early Exercise Risks in Hard-to-Borrow Environments

The massive inflation of put option premiums in hard-to-borrow securities introduces a significant and often overlooked mechanical hazard: "early exercise" risk. American-style options allow the holder to exercise their contractual right to buy or sell the underlying asset at any time before expiration 13. Typically, early exercise is mathematically sub-optimal because the option holder forfeits the remaining extrinsic time value of the contract 14.

However, when a stock is extremely hard to borrow (such as DJT peaking at a 790% borrow fee), a deep in-the-money put option may actually trade below its intrinsic value 1415. If a trader holds a deep in-the-money put on a severely restricted-float stock, the massive borrow fee they could earn by lending the physical stock (if they possessed it) outweighs the negligible time value remaining on the put contract. Therefore, the rational economic action is to early-exercise the put, forcing the option seller to immediately buy the stock. The put holder then takes the resulting cash and physical short position and lends the stock into the HTB market to capture the exorbitant lending rates 15. This dynamic creates persistent uncertainty for market makers and prime brokers attempting to manage delta-neutral books in low-float environments, as hedges can be abruptly dismantled by early assignment.

The Bona-Fide Market Maker Exemption

Under normal circumstances, the U.S. Securities and Exchange Commission's Regulation SHO requires broker-dealers to "locate" shares to borrow before executing any short sale 3. However, Regulation SHO Rule 203(b)(1) contains a critical, heavily debated exception: it allows options market makers to short sell without obtaining a locate if the short sale is connected to "bona-fide market making" activities 716.

By fulfilling the hedge fund's demand for the synthetic short options package, the market maker justifies shorting the underlying stock to hedge their book, utilizing the regulatory exemption to legally bypass the hard-to-borrow constraints. This arbitrage strategy is technically defined as a "reverse conversion" 712. The SEC has previously noted that in highly restricted floats, reverse conversions are often executed purely to meet a one-sided institutional demand for hard-to-borrow threshold securities. This allows large prime brokerage firms to acquire long stock positions hedged by synthetic short options 7. This mechanism legally manufactures "synthetic supply," injecting temporary liquidity into a frozen market but fundamentally delaying the reality of physical settlement.

The Architecture of Settlement Failures

While the bona-fide market maker exemption allows for the creation of synthetic supply at the exact moment of the trade, it does not absolve the market maker from the ultimate, mechanical requirement of trade settlement.

Continuous Net Settlement and Fails-to-Deliver

The U.S. equity market clears trades through the National Securities Clearing Corporation (NSCC) using a system called Continuous Net Settlement (CNS). If the market maker who shorted the stock to hedge their options position cannot actually locate physical shares to deliver to the buyer's clearing firm within the standard T+1 settlement cycle, the transaction results in a Fail-to-Deliver (FTD) at the NSCC 1718.

In highly illiquid mega-cap IPOs, these fails can accumulate rapidly. The SEC releases FTD data twice a month, demonstrating how heavily shorted, low-float stocks generate millions of dollars in rolling settlement failures as market makers continually roll their obligations rather than securing physical delivery 817.

Threshold Lists and Buy-In Mechanics

To combat chronic settlement failures, Regulation SHO Rule 204 mandates that clearing firms close out FTD positions in "threshold securities" within strict timeframes. A security is placed on the Reg SHO Threshold List if it exceeds a specific aggregate fail level for five consecutive settlement days 7. To close out the fail, the broker must execute a forced "buy-in," purchasing shares on the open market regardless of price 7.

However, in structurally constrained floats, forced buy-ins can trigger violent upward price spikes, further punishing short sellers and creating a dangerous feedback loop of volatility. The persistence of FTDs in stocks like DJT - which remained on the threshold list for an extraordinary 179 days with maximum FTDs of $118.91 million - suggests that the combination of market maker exemptions and synthetic supply creation effectively circumvents the original intent of prompt settlement 7. In 2025, petitions submitted to the SEC highlighted that aggregate FTDs across the market peaked at nearly $19.8 billion system-wide, arguing that these structural loopholes allow systemic risk to build up unchecked in the central clearinghouses 7.

| Market Mechanism | Primary Actor | Regulatory Status | Systemic Impact |

|---|---|---|---|

| Physical Short Sale | Hedge Funds / Retail | Requires "Locate" (Reg SHO 203) | Absorbs borrow pool, drives CTB higher. |

| Synthetic Short (Options) | Hedge Funds | Legal via standard options trading | Transfers borrow burden to Market Maker. |

| Reverse Conversion Hedge | Options Market Maker | Exempt from Locate (Bona-Fide Exemption) | Injects synthetic supply, delays settlement. |

| Fail-to-Deliver (FTD) | Clearing Broker | Triggers Buy-in protocols (Reg SHO 204) | Accumulates systemic risk in clearinghouse. |

Table 2: The mechanical pipeline of short exposure in constrained-float equities, from physical borrow exhaustion to eventual settlement failure.

Evolution of Prime Brokerage Risk Frameworks

The extreme volatility generated by low-float short squeezes, combined with the synthetic leverage facilitated by the options market, presents severe counterparty credit risk for prime brokers. The fundamental role of the prime broker is to provide clearing, custody, execution, and financing (including margin loans and stock borrowing) to their hedge fund clients 2919. When a hedge fund's short position moves violently against them in a low-float squeeze, the prime broker is directly exposed to the losses if the fund defaults.

Lessons from Archegos and Sovereign Bank Vulnerabilities

The prime brokerage industry has undergone a radical transformation in its risk management philosophy following the unprecedented market events of 2021, primarily the "meme stock" phenomenon and the catastrophic collapse of Archegos Capital Management 192032. In the Archegos implosion, prime brokers suffered massive, highly publicized losses - including a $5.5 billion hit to Credit Suisse and a $2.9 billion loss at Nomura - due to a combination of excessive margin extension, highly concentrated positions, and a fundamental lack of visibility into the client's total exposures across multiple competing dealers 2932.

The subsequent failure of regional U.S. banks in 2023 further underscored the fragility of liquidity networks in high-rate environments 33. In response to these consecutive stress tests, major prime brokers have fundamentally overhauled their credit underwriting and intraday risk assessment procedures 43221.

Dynamic Margining and Wrong-Way Risk Mitigation

The traditional risk model of relying on static, end-of-day Value-at-Risk (VaR) calculations has proven entirely inadequate for low-float equities, where prices can gap hundreds of percent intraday without fundamental news. To adapt, prime brokers have aggressively transitioned toward dynamic, real-time margining systems that require clients to post collateral continuously as market conditions fluctuate minute-by-minute 1920. Furthermore, prime broker risk committees now implement strict portfolio concentration limits, heavily penalizing funds that attempt to hold disproportionately large short positions in illiquid or restricted-float mega-caps 2919.

The collapse of Archegos also highlighted the systemic danger of "wrong-way risk" (WWR) and the opaqueness of synthetic derivatives, particularly Total Return Swaps (TRS) 29. Hedge funds frequently utilize TRS to gain economic exposure to a stock without triggering regulatory reporting thresholds or needing to locate physical borrow, as the prime broker holds the physical hedge on its own balance sheet 2935.

If a fund holds a massive synthetic short position via swaps on a low-float IPO, and the stock squeezes upward, the fund's equity is wiped out precisely when the prime broker needs them to post more margin. To combat this, prime brokers have elevated the calculation of loan-to-value (LTV) ratios when complex derivatives are involved 19. Margin requirements for hard-to-borrow, highly volatile equities are now frequently set at or near 100%, meaning the prime broker requires the hedge fund to fully collateralize the position in cash, neutralizing the leverage entirely and forcing funds to limit their exposure to low-float anomalies 1920.

Comparative Global Regulatory Frameworks

The structural friction between short sellers, synthetic supply creation, and settlement failures is regulated differently across major global jurisdictions. The stark divergence in international rules highlights the ongoing philosophical debate between prioritizing continuous market liquidity (via exemptions) and prioritizing rigid settlement discipline.

United States Regulation SHO and Reform Proposals

In the United States, short selling is governed by the SEC's Regulation SHO, implemented in 2005. As discussed, the framework relies on the "locate" requirement (Rule 203) and the "close-out" requirement (Rule 204) 37.

However, the efficacy of Regulation SHO in managing the modern phenomenon of low-float mega-cap IPOs is heavily contested by market structure analysts. Critics argue that the "reasonable grounds" standard for locates is too easily satisfied and rarely enforced rigorously 7. Furthermore, the bona-fide market maker exemption remains a glaring loophole, allowing options dealers to legally bypass the locate requirement to hedge reverse conversions, which systematically introduces uncovered short shares into the continuous net settlement system 717.

Recent petitions submitted to the SEC have argued that the persistence of multi-billion dollar FTDs reflects deep structural flaws. Proposals for reform suggest eliminating all market maker exemptions to locate rules, enforcing escalating monetary fines for FTDs, and requiring a mandatory, confirmed pre-borrow for all short sales, regardless of the entity executing the trade 7.

European Union Settlement Discipline

The European Union addresses short selling through the EU Short Selling Regulation (SSR), which came into full effect in late 2012 22. The EU SSR takes a markedly more stringent approach to settlement discipline than the U.S. framework.

Under the SSR, naked short selling of sovereign debt and equities admitted to trading on an EU trading venue is explicitly prohibited 2223. A short sale is only deemed legally "covered" if the seller has pre-borrowed the share, entered into a binding agreement to borrow, or holds an arrangement with a third party firmly confirming the shares have been located and reserved 22. The EU also enforces a two-tier transparency model, requiring private disclosure to regulators of net short positions exceeding 0.1% (adjusted from 0.2%) of issued share capital, and public disclosure for positions exceeding 0.5% 3824.

Crucially, the EU framework imposes strict penalties on the back end to enforce settlement. Every central counterparty (CCP) in a Member State must impose a mandatory "buy-in" procedure on any clearing member that fails to deliver shares within four business days of the settlement date 3825. If the buy-in fails, the CCP imposes daily cash fines on the failing party 25. Furthermore, the EU SSR applies extraterritorially; a hedge fund operating in New York executing a short sale on a Frankfurt-listed security must adhere entirely to the EU locate and disclosure rules 25.

Asian Market Restrictions and Mandatory Buy-Ins

Asian jurisdictions, particularly Hong Kong and South Korea, operate the most restrictive short-selling regimes globally, prioritizing retail market stability and settlement certainty over absolute institutional liquidity.

In Hong Kong, naked short selling is classified as a criminal offense punishable by severe fines and imprisonment 2441. The Securities and Futures Commission (SFC) enforces a strict pre-borrow requirement; brokers must ensure shares are physically secured before executing a short order 26. Furthermore, short selling is not permitted universally; the Hong Kong Stock Exchange restricts short sales to a specific list of "Designated Securities." To qualify, a stock must pass stringent eligibility tests, typically requiring a minimum market capitalization of HK$3 billion and a 12-month turnover ratio of not less than 60% 41. This rule inherently prevents the shorting of low-float, illiquid IPOs, entirely bypassing the borrow-squeeze dynamics seen in U.S. markets. If a failure to deliver does occur in Hong Kong, a compulsory buy-in process is initiated immediately on the T+2 settlement day 41.

South Korea represents the extreme end of the regulatory spectrum. The Korean regulatory framework views short selling predominantly as a systemic risk rather than a tool for fundamental price discovery. Consequently, South Korea has relied on direct government intervention to institute comprehensive bans on short selling during periods of market stress, with recent bans implemented during the COVID-19 pandemic and extended deep into 2025 to protect retail sentiment and investigate illegal naked shorting practices 41.

Structural Outlook

The complex interplay of short interest, extreme borrow costs, and synthetic supply in low-float mega-cap IPOs highlights a significant structural vulnerability in modern equity market architecture. When capital market mechanisms - such as heavily insider-weighted SPACs - generate multi-billion-dollar nominal valuations on artificially constrained free floats, they create an environment where fundamental price discovery is mathematically suspended.

The resulting imbalance triggers a predictable sequence of systemic stresses. First, inelastic demand from fundamental short sellers exhausts the physical lending pool, driving annualized borrow fees to unsustainable, triple-digit levels. Second, this physical borrow constraint forces institutional exposure into the options market, where reverse conversions are utilized to manufacture synthetic short exposure. Third, utilizing bona-fide market-making exemptions, options dealers hedge these synthetic positions without pre-borrowing, injecting phantom liquidity into the market that directly translates into massive, persistent fails-to-deliver at the clearinghouse level. Finally, this combination of extreme volatility and synthetic leverage poses severe counterparty risks, forcing prime brokers to transition to dynamic, highly restrictive margin frameworks to prevent contagion.

The stark regulatory divergence between the United States and jurisdictions like the European Union and Hong Kong underscores the philosophical debate regarding these dynamics. While the U.S. prioritizes continuous liquidity by offering exemptions that inadvertently fuel synthetic supply and delay settlement, international frameworks prioritize settlement discipline through mandatory pre-borrows, strict automated buy-ins, and designated shortable securities lists. As companies continue to remain private longer and enter the public markets through unconventional, low-float structures, the pressure on global regulators to harmonize settlement disciplines and close synthetic supply loopholes will only intensify.