Nasdaq-100 and S&P 500 index inclusion mechanics and timelines

The proliferation of passive investment strategies over the past three decades has fundamentally restructured the microstructure of global equity markets. As an estimated $13.5 trillion to $20 trillion in capital is now systematically benchmarked to flagship market-capitalization-weighted indices such as the S&P 500, the mechanics of index inclusion have evolved from routine administrative procedures into systemic liquidity events 12. When an index provider adjusts its constituent list, passive mutual funds and exchange-traded funds (ETFs) are contractually mandated to replicate these changes. This generates mechanical, price-agnostic demand that forces immediate capital allocation. This structural rigidity creates a complex financial ecosystem characterized by anticipatory arbitrage, transient price distortions, and localized liquidity shocks.

The June 12, 2026, initial public offering (IPO) of SpaceX (ticker: SPCX) serves as an unprecedented empirical stress test for these market mechanics. Entering the public markets at an implied valuation of approximately $1.75 trillion, the company represents one of the largest market capitalization debuts in history 345. However, its capital structure - characterized by an exceptionally low public float of roughly 4.3% - presents a severe supply-demand imbalance when interacting with the rigid rules of passive capital allocators 16. Major index providers have responded to the influx of mega-capitalization private companies with divergent methodological updates, creating a bifurcated landscape of index eligibility. This report provides an exhaustive analysis of index inclusion mechanics, the contrasting structural frameworks of the Nasdaq-100 and S&P 500 methodologies, the quantitative impact of the SpaceX IPO, the behavior of institutional arbitrageurs, and the hidden costs borne by passive investors during large-scale index rebalancing events.

Structural Frameworks of U.S. Equity Indices

The construction and maintenance of equity indices dictate the flow of passive capital across the global financial system. While often perceived by retail investors as objective, macroeconomic reflections of the stock market, indices are governed by highly specific, proprietary, and rules-based methodologies. These methodologies determine security eligibility based on complex evaluations of market capitalization, liquidity profiles, corporate governance structures, and financial viability.

S&P 500 Methodology and the Profitability Hurdle

The S&P 500 is arguably the most influential equity benchmark in the global financial system. Unlike purely mechanical, purely quantitative indices, the S&P 500 is governed by an Index Committee that retains subjective discretion over constituent additions and deletions, though it operates within a strict quantitative framework 76. This subjective layer allows the committee to preserve the index's historical mandate as a representation of high-quality, fundamentally sound large-cap domestic equities.

To qualify for S&P 500 inclusion, a corporate entity must satisfy several rigorous criteria evaluated precisely at the time of the index reconstitution. Primarily, the unadjusted total company-level market capitalization must exceed a specific, dynamically adjusted threshold, which was set at $22.7 billion effective July 1, 2025 67. Furthermore, the security-level float-adjusted market capitalization (FMC) must be at least 50% of this company-level minimum threshold 6.

A defining and frequently debated characteristic of the S&P 500 methodology is its strict profitability hurdle. To be considered for inclusion, a prospective constituent must report positive Generally Accepted Accounting Principles (GAAP) net income for its most recent quarter, as well as for the sum of its most recent four consecutive quarters 67. This acts as a quality filter, intentionally excluding hyper-growth technology companies that prioritize market share and capital expenditure over near-term positive earnings. Furthermore, the security must possess an Investable Weight Factor (IWF) of at least 0.10, indicating that a minimum of 10% of the company's outstanding shares are freely floated and available for public trading 67. The liquidity profile must also demonstrate a float-adjusted liquidity ratio (FALR) of at least 0.75, coupled with a minimum monthly trading volume of 250,000 shares in each of the six months immediately preceding the evaluation date 67.

Newly public companies, including traditional IPOs and entities formed via Special Purpose Acquisition Companies (SPACs), face a rigid seasoning requirement. These securities must be traded on an eligible U.S. exchange - such as the NYSE or Nasdaq Global Select Market - for a minimum of 12 months before they can even be considered by the Index Committee 66.

S&P Dow Jones Indices has historically demonstrated a willingness to revise its structural prohibitions, though it remains highly protective of its core quality mandates. In 2017, following the high-profile IPO of Snap Inc., which offered only non-voting shares to the public, the provider barred all future companies with multiple share classes (including high-vote/low-vote structures and Up-C structures) from joining the S&P Composite 1500 family 89. This decision aimed to protect passive investors from being forced to allocate capital to entities with entrenched management and diminished shareholder voting rights. However, following extensive consultation with institutional market participants, this restriction was reversed in April 2023, restoring eligibility for multi-class share companies provided they meet all other fundamental criteria 8910. Despite this newly adopted flexibility regarding corporate governance, the S&P Index Committee firmly rejected a May 2026 proposal that sought to waive the GAAP profitability and 12-month seasoning requirements for mega-cap IPOs, thereby preserving the index's traditional quality-filter mandate 6.

Nasdaq-100 Methodology and the Fast Entry Provision

The Nasdaq-100 Index, which tracks the 100 largest non-financial domestic and international companies listed on the Nasdaq stock exchange, operates with a distinctly different structural philosophy. It prioritizes the representation of aggregate market capitalization and technological innovation over historical financial profitability 1112.

In direct response to a growing pipeline of mega-capitalization private companies remaining private for longer periods before listing, Nasdaq executed a sweeping overhaul of its inclusion rules, which became effective on May 1, 2026. This methodology update was specifically designed to mitigate the temporal lag between a massive public listing and its reflection in the benchmark, ensuring that passive investors gain immediate exposure to the market's most valuable newly listed entities 413.

The cornerstone of this methodology update is the "Fast Entry" rule. If a newly listed company's full market capitalization ranks within the top 40 of current Nasdaq-100 constituents - a threshold representing approximately $100 billion in market value based on mid-2026 figures - it entirely bypasses the standard three-month seasoning requirement. Under this provision, eligibility is evaluated as of the end of the security's seventh trading day, and the security is typically added to the index after 15 trading days 1213.

To accommodate the modern trend of low-float IPOs, Nasdaq also fundamentally altered its liquidity requirements. Previously, the index mandated a minimum 10% free float for inclusion, which had historically created abrupt "revolving door" volatility for low-float stocks hovering near the threshold 11. The May 2026 update eliminated the 10% absolute minimum float requirement. Instead, the methodology applies a dynamic weighting multiplier for companies with exceptionally low floats. A low-float stock can be introduced to the index at a weight reflecting up to three times its actual freely tradeable shares, strictly capped by its full listed market value 341113.

Critically, a Fast Entry addition does not necessitate the immediate, disruptive removal of an existing constituent. The index is permitted to temporarily expand beyond 100 members until the next scheduled annual reconstitution in December, thereby removing a significant structural friction that previously made index committees reluctant to add large newcomers mid-cycle 1213.

Index Methodology Comparison

The divergent approaches of major index providers dictate the flow of passive capital during large-scale public listings. The table below summarizes the core mechanical differences between the major large-cap benchmarks as of mid-2026.

| Methodological Requirement | S&P 500 Index | Nasdaq-100 Index | FTSE Russell (U.S. Equity) |

|---|---|---|---|

| Primary Exchange Listing | Eligible U.S. Exchanges (NYSE, Nasdaq, Cboe) | Strictly Nasdaq-affiliated exchanges | Broad U.S. exchange eligibility |

| Financial Sector Inclusion | Eligible (~13.1% index weight) | Strictly Excluded | Eligible |

| Profitability (GAAP) | Positive (Most recent quarter & trailing 4 quarters) | No profitability requirement | No profitability requirement |

| Standard Seasoning | 12 full months post-IPO | 3 full calendar months post-IPO | Next scheduled quarterly rebalance |

| Fast-Track IPO Entry | None (Proposal rejected June 4, 2026) | "Fast Entry" (Top 40 market cap, ~15 days) | 5th trading day for mega-cap IPOs |

| Minimum Public Float | 10% (Investable Weight Factor $\ge$ 0.10) | None (Replaced by 3x float multiplier limit) | 5% threshold relaxed (investable market cap used) |

The SpaceX Initial Public Offering Dynamics

The structural divergence in index methodologies has profound implications for SpaceX, which executed the largest IPO in financial history on June 12, 2026. This specific listing serves as the optimal catalyst for examining how massive passive capital pools absorb extreme market events under highly constrained supply conditions.

Capital Structure, Valuation, and the Float Constraint

SpaceX priced its public offering at a fixed $135 per share, successfully raising $75 billion at a target valuation of approximately $1.75 trillion 3414. This valuation immediately positioned the aerospace and telecommunications conglomerate among the largest publicly traded enterprises in the United States, surpassing the previous global IPO record set by Saudi Aramco ($29.4 billion in December 2019) by a vast margin 4515.

Despite its staggering total valuation, the IPO's capital structure is characterized by an exceptionally narrow public float. SpaceX floated only 4.3% of its total outstanding shares 1. Of this thin slice, 30% - equivalent to roughly $22.5 billion, or a mere 1.3% of the total company - was specifically allocated to retail investors through brokerage platforms such as Robinhood, Fidelity, and Charles Schwab 11617. The remaining 95.7% of the total equity is governed by deliberately staggered lock-up agreements designed to prevent immediate insider selling 116. This structure creates an environment where the price discovery of a $1.75 trillion business is dictated entirely by the trading velocity of just 4.3% of its shares, a condition heavily susceptible to supply-and-demand mechanics rather than pure fundamental valuation consensus 1.

Consolidated Financials and Profitability Metrics

Fundamentally, SpaceX operates as a conglomerate with diverse and highly distinct operational profiles. The company's Starlink satellite internet division has evolved into a highly profitable, cash-generative engine. As of the first quarter of 2026, Starlink reported an operating profit of $1.19 billion on $3.26 billion in revenue, accounting for roughly 69% of the parent company's consolidated top-line revenue 521.

However, this profitability is completely offset by the immense capital requirements of the company's other divisions. The consolidated corporate entity reported a net loss of $4.94 billion for the full year 2025, followed by a $4.28 billion net loss in the first quarter of 2026 alone 161421. These staggering losses were primarily driven by aggressive capital expenditures in artificial intelligence infrastructure, notably the acquisition and integration of xAI and the ongoing development of the Colossus supercomputer, which is actively leased to partners such as Anthropic 141721. The company's balance sheet also reflects significant leverage, carrying $29.1 billion in total long-term debt, including a $20 billion short-term bridge loan maturing within six months of the listing 1.

The Eligibility Timeline and Forced Buying Triggers

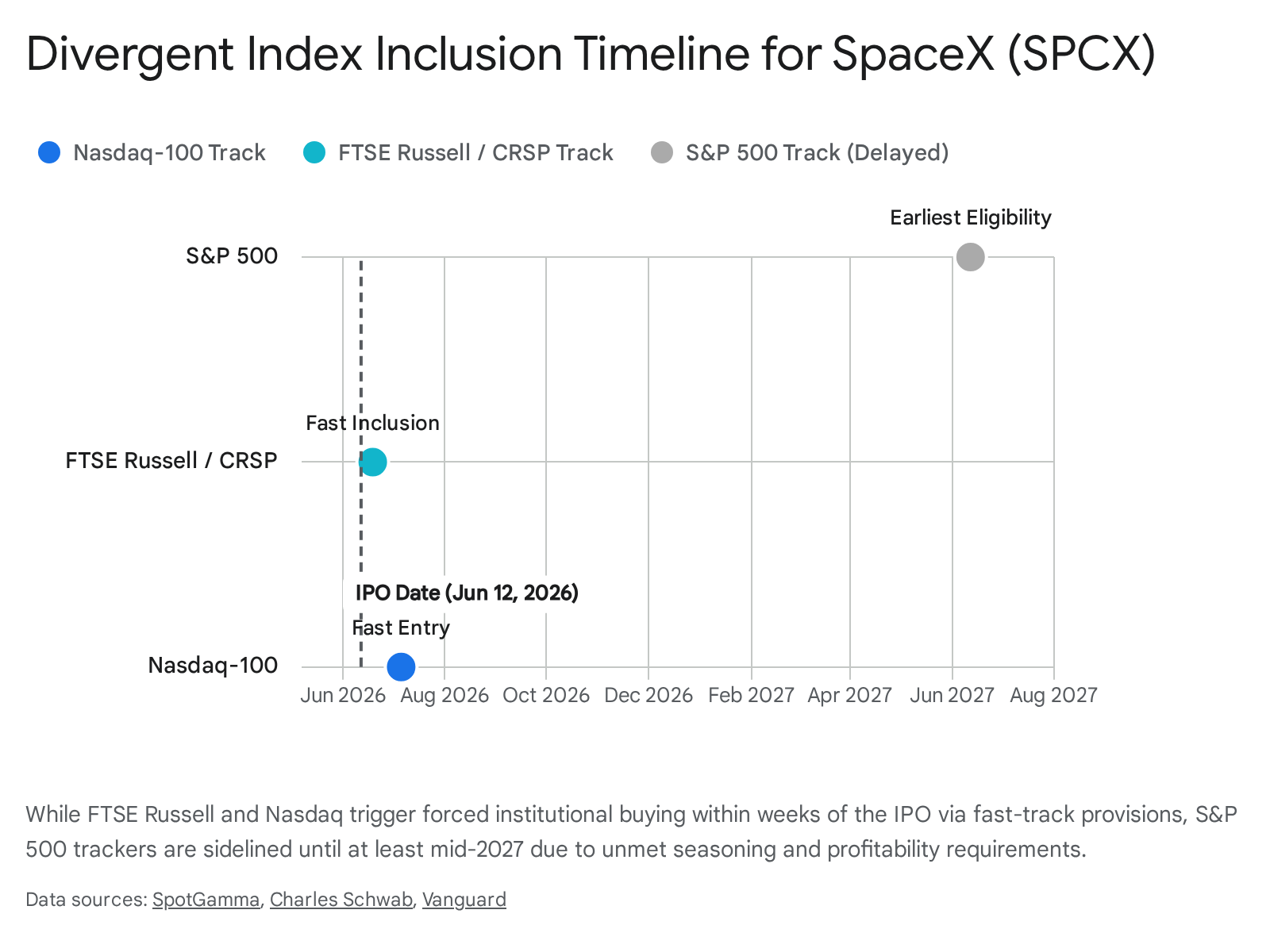

The intersection of SpaceX's historic valuation, severely restricted public float, and negative GAAP earnings triggers a staggered and highly consequential sequence of index inclusion events. Because the three major index families maintain disparate eligibility rules, the mechanical, mandatory buying by passive funds is fragmented across multiple distinct chronological milestones.

For indices tracking the Center for Research in Security Prices (CRSP) - such as the massive Vanguard Total Stock Market ETF (VTI) and Vanguard Total World Stock ETF (VT) - inclusion mechanics are incredibly rapid. Vanguard confirmed that these vehicles would incorporate SPCX by the close of the fifth trading day post-IPO, capturing the initial burst of passive demand 618. Similarly, FTSE Russell implemented its fast-entry protocols, allowing the stock to join the Russell US Equity Indexes along a highly compressed timeline 61619.

The most significant immediate liquidity event is dictated by the Nasdaq-100 methodology. Because SpaceX's $1.75 trillion valuation easily clears the top-40 market capitalization threshold required for the newly implemented Fast Entry provision, the index committee evaluates the stock on its seventh trading day. This sets the stage for formal addition to the Nasdaq-100 approximately 15 trading days post-IPO, landing in late June or early July 2026 61224.

Conversely, the strict methodological rigidity of the S&P 500 places it on an entirely different trajectory. The June 4, 2026, decision by S&P Dow Jones Indices to reject the proposal to waive its profitability and seasoning rules ensures that SpaceX is categorically excluded from the benchmark. Because it fails the 12-month seasoning requirement, the 10% minimum float requirement, and the four-quarter GAAP profitability test, SPCX cannot enter the S&P 500 until at least mid-2027 161620. This exclusion effectively sidelines an estimated $14 billion in immediate forced passive buying from funds tracking the S&P 500, delaying this capital influx by a year or more 116.

Mechanics of Forced Institutional Buying

The divergence in eligibility timelines exposes the underlying mechanics of "forced institutional buying." When an index provider formally adds a security to a benchmark, the universe of passive funds - ranging from institutional mutual funds to retail-facing ETFs - are legally or methodologically mandated to purchase the newly added stock at its specified index weight 2621.

The execution of these mandates is severely constrained by the need to minimize tracking error. Passive fund managers are evaluated almost entirely on their ability to perfectly replicate the daily return of their benchmark index. To achieve this, these funds typically execute massive bulk orders exactly at the market-on-close (MOC) price on the effective date of the reconstitution. If they were to spread their buying over several days to minimize market impact, the resulting price deviations would generate unacceptable tracking error against the benchmark 2621.

Scale of Passive Replication

The scale of capital forced into motion by a mega-cap inclusion is vast. The Nasdaq-100 is tracked by approximately $1.4 trillion in total capital, encompassing physical ETFs (such as the $300 billion Invesco QQQ), mutual funds, derivative ecosystems including futures and options, and complex structured products 45. Institutional data modeling firm Intropic estimated that the coordinated actions of Nasdaq, FTSE Russell, and MSCI would mechanically lock approximately 30% of SpaceX's available free-float shares into passive investor portfolios within 15 days of the listing 28.

This massive capital inflow occurs entirely independent of active fundamental analysis. Passive funds do not evaluate the $1.75 trillion valuation or the 92x price-to-sales multiple; their systems simply read the updated index weights and execute buy orders 4516. Furthermore, index rebalancing is a zero-sum capital allocation process. To purchase a massive incoming constituent like SPCX, index funds must engage in proportional selling of existing constituents. In the Nasdaq-100, the companies facing the largest absolute dollar volume of selling pressure are the largest incumbents: Apple, Microsoft, Nvidia, Meta, and Alphabet. While this rebalancing outflow is a fraction of a percent relative to the multi-trillion-dollar market caps of these incumbents, the selling is highly concentrated within the exact same two-week window that SPCX begins trading, creating a cross-market liquidity event 629.

Float Constraints and Reflexivity

The severity of forced buying is mathematically amplified by the treatment of low-float securities. Ordinarily, modern capitalization-weighted indices utilize free-float adjustments to prevent highly illiquid, closely held stocks from commanding outsized weights, which would incur prohibitive transaction costs for passive replicators 1819.

However, under the revised Nasdaq rules implemented in May 2026, the 3x float multiplier completely alters the equilibrium. For a company like SpaceX, offering roughly $75 billion in float at the IPO price, the multiplier allows the index to assign it an effective market capitalization of approximately $225 billion 3. This adjustment places the company in the top 30 constituents by index weight, generating a mechanical demand that vastly exceeds the physical supply of freely trading shares 3.

This structural mismatch initiates a "reflexive feedback loop." The initial wave of anticipatory and passive buying against a constrained 4.3% float inevitably drives the share price higher 128. As the share price increases, the company's total market capitalization expands. Because index weights are dynamic, this expanded market capitalization dictates an even larger weighting in the benchmark, thereby forcing passive funds to demand an even greater volume of shares 2822. This cycle continues until supply naturally expands, typically through the expiration of insider lock-up agreements or secondary equity offerings.

Quantitative Analysis of the Index Inclusion Effect

The predictability of index reconstitution events has historically spawned a sophisticated ecosystem of quantitative arbitrage. Because passive index funds represent massive, price-agnostic, and predictable order flow, sophisticated active market participants attempt to identify and trade ahead of these mandates. This anticipatory trading is the genesis of the "Index Inclusion Effect."

Historical Decay and Arbitrage Efficiency

The Index Inclusion Effect refers to the sustained abnormal positive returns generated by a stock between the date its addition to a major benchmark is announced and the effective date of its inclusion 2. Academic literature has tracked this anomaly for decades. Early studies, such as those by Shleifer (1986), documented that stocks added to the S&P 500 experienced abnormal average returns of approximately 3% 23. This anomaly peaked during the rapid expansion of index investing in the 1990s, where additions generated an average abnormal return of 7.4% 2324.

However, more recent quantitative research reveals that the index effect underwent a profound structural decay. Over the decade spanning 2010 to 2020, the average abnormal return for S&P 500 additions plummeted to a mere 0.3%, and the corresponding negative abnormal returns associated with deletions nearly evaporated entirely, dropping from -16.1% in the 1990s to -0.6% in the 2010s 2324.

This attenuation was historically driven by two primary mechanisms of market efficiency: 1. Algorithmic Front-Running: As index methodologies became highly transparent and rule-based, quantitative hedge funds and statistical arbitrageurs developed models to predict additions and deletions months before the official announcements. By purchasing the likely candidates early, these arbitrageurs smoothed out the price shock. When the official announcement occurred and passive funds finally submitted their massive buy orders on the effective date, the arbitrageurs sold their accumulated inventory, extracting the alpha and providing necessary liquidity to the passive funds 232425. 2. Corporate Liquidity Provision: Corporate treasuries have also adapted to the mechanics of index demand. Research by Tamburelli (2024) and others highlights that companies newly added to major indices tend to aggressively issue new shares - or sell treasury stock - in the immediate days following the announcement. By issuing new equity directly into the inelastic demand generated by passive trackers, firms effectively arbitrage their own stock, dampening the inclusion price spike while raising capital at highly favorable valuations with minimal market impact 2425.

Resurgence Driven by Retail Market Demographics

Despite the long-term trend of structural decay, the index inclusion effect has experienced a localized resurgence in the post-pandemic era. Research published by Goldman Sachs Global Investment Research indicates that since the COVID-19 pandemic, the rise of highly active retail trading has reignited the inclusion pop 7.

This resurgence is characterized by the interaction of retail enthusiasm with rapid corporate growth. Many modern, highly visible technology companies experience such precipitous increases in valuation that they "leapfrog" the S&P 400 MidCap Index entirely, moving directly from un-indexed status into the S&P 500 7. This leapfrogging creates a concentrated, high-visibility event that overwhelms the traditional, orderly liquidity provision of institutional arbitrageurs. When retail investors aggressively bid up the stock upon the inclusion announcement, they exacerbate the price momentum. Historical case studies of this dynamic include Tesla's historic addition in 2020, which generated a massive 53.35% return between its announcement and effective dates, and the anticipated dynamics surrounding the SPCX listing in 2026 723.

Hidden Costs of Index Rebalancing and Passive Attrition

While passive investing is universally championed by asset managers for its low stated expense ratios and broad market diversification, the rigid mechanics of index tracking conceal invisible, systemic structural costs that degrade long-term investor performance.

The Avoidable Costs of Mechanical Rebalancing

When an index rebalances, passive funds are forced into a position of severe adverse selection. A seminal 2023 study by Arnott, Brightman, Kalesnik, and Wu, titled "The Avoidable Costs of Index Rebalancing," meticulously quantified the performance drag inherent in capitalization-weighted indices 26262736. The researchers demonstrated that capitalization-weighted indices inherently follow a momentum-driven strategy at the point of reconstitution: they systematically add stocks that have experienced recent, massive price appreciation (and therefore trade at highly elevated valuation multiples) and delete stocks that have suffered severe price declines (trading at depressed valuation multiples) 262736.

The empirical results of this mechanical process are striking. Arnott's research demonstrates that in the year immediately following a reconstitution of the S&P 500, the discretionary deletions (the relative "losers") typically outperform the additions (the relative "winners") by an average of 22% 262637. Because index funds are forced to buy high and sell low at the exact moment of peak market visibility, they incur a hidden performance drag. The study concludes that simple rule modifications - such as delaying reconstitution trades by three to twelve months - could add up to 23 to 25 basis points (0.23% to 0.25%) in annual performance to index fund investors 262637. This represents a hidden fee that easily dwarfs the stated single-digit basis point expense ratios of modern flagship ETFs.

Execution Costs and Tracking Error Variance

Further research corroborates the scale of this structural friction. A 2025 study by Tasitsiomi, "On the Hidden Costs of Passive Investing," analyzed the implicit trading costs funds incur when fixated on maintaining zero tracking error 2637. By waiting until the market close on the reconstitution day to execute massive block orders, passive funds create perfectly predictable trading patterns that sophisticated market participants actively exploit.

Hendrix, Liu, and Roberts (2024) further quantified this execution penalty, finding that over the period from 2019 to 2023, the price for index additions surged by an average of 9 basis points relative to non-rebalanced stocks in the fleeting 10 seconds between 4:00 PM on reconstitution day and the final market close 26. The following morning, the price abruptly reversed by an average of 13 basis points. This intra-day volatility confirms that passive investors consistently pay a premium to execute at the closing auction, effectively transferring wealth to the institutional liquidity providers and statistical arbitrageurs who warehoused the shares in anticipation of the mechanical flow 26.

Prime Brokerage Mechanics and Arbitrage Logistics

The extraction of this hidden value from passive index funds requires immense capital capacity and highly specialized infrastructure, which is facilitated almost entirely by global prime brokerages. Prime brokers - dedicated divisions within tier-one investment banks - provide hedge funds with the necessary leverage, securities lending capabilities, and execution algorithms required to execute massive event-driven, index-rebalancing, and merger-arbitrage strategies 282930.

Leverage and Balance Sheet Constraints

During periods of intense IPO activity and concentrated index rebalancing, prime brokerage desks operate at peak capacity. Hedge funds utilize prime brokerage margin to lever up their long positions in anticipated index additions while simultaneously shorting the broader index or specific constituent deletions to hedge out broad market beta 293031. The profitability of these capital-intensive trades relies heavily on the prime broker's cost of capital and the availability of cheap stock borrow.

However, the post-2008 regulatory environment fundamentally altered this dynamic. Regulatory frameworks, specifically the implementation of the Supplementary Leverage Ratio (SLR) under the Basel III and Dodd-Frank regimes, explicitly require large financial institutions to hold capital against their total leverage exposure, encompassing both on-balance-sheet assets and off-balance-sheet exposures 30. As documented by researchers at the Federal Reserve Bank of New York, these tighter regulatory constraints disincentivize prime brokers affiliated with Global Systemically Important Banks (G-SIBs) from dedicating unlimited balance sheet space to low-margin hedge fund leverage 30. Consequently, the maximum leverage allowed for complex arbitrage trades is considerably lower than in previous decades, making the arbitrage process more sensitive to minor fluctuations in financing costs 30.

NAV Triggers and Liquidity Management

Because arbitrageurs operate with high leverage on tight spreads, they are uniquely vulnerable to sudden market dislocations. Prime brokerage agreements enforce strict risk-management parameters, most notably Net Asset Value (NAV) triggers. If a hedge fund's NAV declines by a predetermined percentage within a specific timeframe (e.g., a month or quarter), the prime broker retains the contractual right to terminate the trading relationship, seize collateral, and force the immediate liquidation of the fund's portfolio 2832.

During extreme volatility events, a crowded arbitrage trade - such as front-running an index inclusion - can rapidly reverse. If the anticipated passive flow is smaller than expected, or if retail selling overwhelms the index demand, the highly levered arbitrageurs face immediate margin calls 32. The subsequent forced deleveraging requires these funds to abruptly unwind their positions, aggressively selling the addition candidates and buying back their short hedges. This unwinding process creates cascading liquidity vacuums and exacerbates market volatility, underscoring the systemic fragility inherent in the interaction between levered active capital and rigid passive mandates.

Short Squeeze Mechanics and Low-Float Market Microstructure

The combination of an exceptionally low free float, massive mechanical passive demand, and active institutional hedging introduces severe tail risks into the market microstructure, most notably the elevated threat of a violent short squeeze.

"Float Shrink" and Liquidity Theory

A short squeeze materializes when a heavily shorted security experiences sudden, unforeseen upward price momentum. This momentum forces short sellers - who have borrowed shares and sold them with the obligation to repurchase them later - to aggressively buy back shares in the open market to cap their theoretically infinite losses 434445. This forced buying creates a self-reinforcing upward spiral, completely disconnecting the asset's price from any traditional metric of fundamental value.

The vulnerability of an asset to a short squeeze is deeply tied to its liquidity profile, a dynamic explored by quantitative analysts under the concept of "float shrink" or liquidity theory. This framework posits that stock prices are frequently a direct function of available market liquidity rather than underlying corporate fundamentals 3347. When the available supply of tradeable shares shrinks - whether through corporate buybacks, insider lock-ups, or massive absorption by buy-and-hold passive index funds - the market becomes acutely sensitive to even modest demand shocks 4533.

Short Squeeze Vulnerability in SPCX

In the context of the SPCX IPO, the index inclusion mechanics construct a highly combustible environment. Hedging activities by various market participants inherently drive up short interest in newly listed, high-profile equities. For instance, authorized participants managing ETF creation and redemption processes, options market makers delta-hedging their derivative exposures (with SPCX options commencing trading mere days after the IPO), and statistical arbitrageurs actively shorting to exploit pricing inefficiencies all require a steady supply of borrowable shares 631.

When Nasdaq's Fast Entry rule forces the passive ecosystem to mechanically absorb roughly 30% of SPCX's tiny 4.3% public float within the first 15 trading days, the absolute supply of freely trading, borrowable shares is drastically reduced 2829. This constriction causes critical metrics, such as the "days-to-cover" ratio (which measures how many days of average trading volume it would take to close all outstanding short positions), to spike exponentially 4345.

In this constrained environment, any unexpected positive catalyst - or even a sustained retail buying frenzy coordinated across social media platforms - can fatally trap institutional short sellers 4345. The resulting rush to cover short positions into a market completely devoid of available supply can result in violent, cascading price dislocations. These dislocations do not merely affect speculative traders; they actively distort the market capitalization metrics upon which the entire index architecture relies, feeding back into the reflexive loop of passive capital allocation 2944.

Conclusions and Structural Outlook

The unprecedented scale and unique capital structure of the SpaceX IPO serve to illuminate the hidden, systemic mechanics that govern modern equity markets. The divergent handling of this historic listing by the major index providers underscores a critical philosophical rift in benchmark construction.

The S&P 500's steadfast adherence to fundamental quality filters - specifically its unwavering requirement for GAAP profitability and historical seasoning - preserves the benchmark's long-standing integrity. By rejecting the rapid inclusion of a $1.75 trillion entity carrying a $4.94 billion annual net loss, the index committee effectively insulates its passive investors from the immediate volatility and speculative pricing of unseasoned, cash-burning enterprises 1616. However, this structural rigidity inherently guarantees that the world's most tracked index will chronically under-represent the cutting-edge technological infrastructure of the modern economy during its highest-growth, pre-profitability phases.

Conversely, the proactive methodological adjustments instituted by the Nasdaq-100 to rapidly absorb mega-cap IPOs via Fast Entry mechanisms ensure that the index immediately captures the market beta of emerging global monopolies 413. Yet, this representational accuracy is achieved at a significant cost: it legally forces its massive passive investor base to underwrite the execution risks of low-float, highly volatile assets whose valuations are dictated largely by constrained supply dynamics and future expectations rather than current financial fundamentals 429.

As the capital structure of entities like SpaceX inevitably evolves, the staggered expiration of insider lock-up agreements will incrementally release the remaining vast majority of the equity into the public float 11416. Each subsequent expansion of the free float will compel index providers to recalculate their weighting multipliers, triggering secondary and tertiary waves of forced institutional buying across the ecosystem 3. For modern investors, understanding these mechanical capital flows, the resulting hidden transaction costs imposed on passive funds, and the sophisticated arbitrage ecosystems designed to exploit them is now just as critical to evaluating expected market returns as traditional corporate fundamental analysis.