Leveraged ETF rebalancing and gamma squeezes in SpaceX equity

Market Structure of the SpaceX Initial Public Offering

The June 12, 2026, initial public offering of Space Exploration Technologies Corp. (SpaceX) fundamentally altered the landscape of global capital markets. Transitioning from a closely held aerospace operator into a publicly traded conglomerate, SpaceX bypassed traditional price discovery to launch at a fixed valuation. Priced at $135 per share, the offering distributed 555.6 million Class A common shares, raising $75 billion and securing an immediate debut valuation of approximately $1.77 trillion 12. When incorporating the underwriter greenshoe option of 83.3 million shares (worth an additional $11.2 billion), the total capital absorption dwarfs all historical precedents, substantially eclipsing the previous record of $35.4 billion set by Saudi Aramco in 2019 13.

However, the absolute magnitude of the capital raise masks the acute structural vulnerabilities inherent in the listing's market microstructure. The intersection of severe float scarcity, aggressive retail participation, structural passive index inclusion, and the immediate deployment of single-stock leveraged exchange-traded funds (LETFs) has established a foundational environment highly susceptible to liquidity cascades and runaway gamma squeezes.

Float Scarcity and Order Book Fragility

Despite representing the largest public offering in financial history, the newly issued Class A shares account for approximately 4% of the company's total outstanding equity 1. The remaining 96% of the equity is held by early investors, corporate insiders, and employees, all of whom are governed by stringent, staggered lock-up agreements tied to the company's future quarterly earnings reports 1. Founder and CEO Elon Musk, who retains 42% of the common equity and exercises 79% of the corporate voting power through a dual-class supervoting share structure, is subjected to a full one-year lock-up period 4.

This extreme float scarcity fundamentally distorts the liquidity profile of the underlying stock (ticker: SPCX). In secondary market trading, the depth of the limit order book is disproportionately shallow relative to the company's massive $1.77 trillion market capitalization. In traditional market dynamics, a mega-cap technology equity possesses sufficiently deep bid and ask reserves to absorb large institutional block trades without triggering massive price dislocations. SPCX, however, trades with the available free float of a mid-cap entity. Consequently, even modest institutional or retail buying pressure can rapidly deplete the available liquidity at a given price level. This structural bottleneck results in widened bid-ask spreads, sudden intraday price gaps, and a heightened sensitivity to momentum-driven order flows 135.

Retail Allocation and Order Oversubscription

Adding to the complexity of the float dynamics is the unusual retail distribution strategy deployed by the underwriting syndicate. SpaceX explicitly targeted an unprecedented 30% retail allocation, reserving roughly $22.5 billion of the offering for individual investors routed through brokerages such as Robinhood, Fidelity, Charles Schwab, SoFi, and E*TRADE 13. Historical norms for offerings of this scale typically cap retail allocations at 5% to 10%, heavily favoring institutional clients 3.

Despite this massive carve-out, the retail demand overwhelmingly outstripped the available supply. Institutional order books recorded over $150 billion in demand against the $75 billion total supply, while retail orders reportedly exceeded $100 billion 136. With the offering running roughly three to four times oversubscribed, the vast majority of retail requests received only fractional fills or were left entirely unfilled. This massive reservoir of unmet demand was mechanically deferred to the secondary market, guaranteeing aggressive market-buy pressure at the opening bell on June 12 as unallocated capital chased the limited public float 78.

Passive Index Mandates and Inelastic Demand

The immediate buying pressure on the constrained float was further exacerbated by the structural integration of SPCX into major global benchmark indices. Recognizing the systemic scale of the listing, major index providers implemented modified inclusion frameworks. MSCI announced that SPCX would be eligible for early inclusion in its Global Standard Indexes starting June 13, 2026, the day immediately following the debut 19. Furthermore, modified Nasdaq-100 Fast Entry rules positioned SPCX to enter the index within 15 trading days, with potential inclusion in the Russell indices within five sessions 6.

Passive index funds operate with strictly inelastic demand. Portfolio managers operating these vehicles are legally mandated by their prospectuses to replicate benchmark index weights, regardless of the underlying asset's fundamental valuation, technical overextension, or immediate trading price 610. As these passive vehicles enter the market to acquire billions of dollars in SPCX equity to satisfy their benchmark obligations, they are forced to compete for the extremely limited 4% free float. This dynamic establishes a rigid, price-agnostic baseline of buying pressure that effectively removes a substantial portion of the active price discovery mechanism from the market, establishing the initial upward momentum required to ignite derivative-driven feedback loops.

Fundamental Valuation and Segment Divergence

The intense speculative frenzy surrounding SpaceX is anchored in a highly polarized fundamental narrative. Following a complex sequence of corporate mergers - most notably the February 2026 acquisition of the artificial intelligence firm xAI (which previously absorbed the social platform X) - SpaceX transitioned from a pure-play aerospace manufacturer into a vertically integrated space, connectivity, and AI conglomerate 4611. The company's S-1 filing partitions the business into three distinct operating segments, each exhibiting wildly divergent financial profiles.

Business Segment Financial Performance

An analysis of the consolidated financials reveals a corporate structure defined by extreme contrasts between cash generation and capital expenditure. The consolidated business generated $18.67 billion in revenue in 2025 but recorded a total net loss of $4.94 billion 611. At the $135 IPO price, the $1.77 trillion valuation commands a staggering multiple of roughly 94 times trailing revenue, a premium that aggressively prices in decades of flawless technological execution 1612.

| Business Segment | 2025 Revenue | 2025 Profitability Profile | Strategic Context and Margin Profile |

|---|---|---|---|

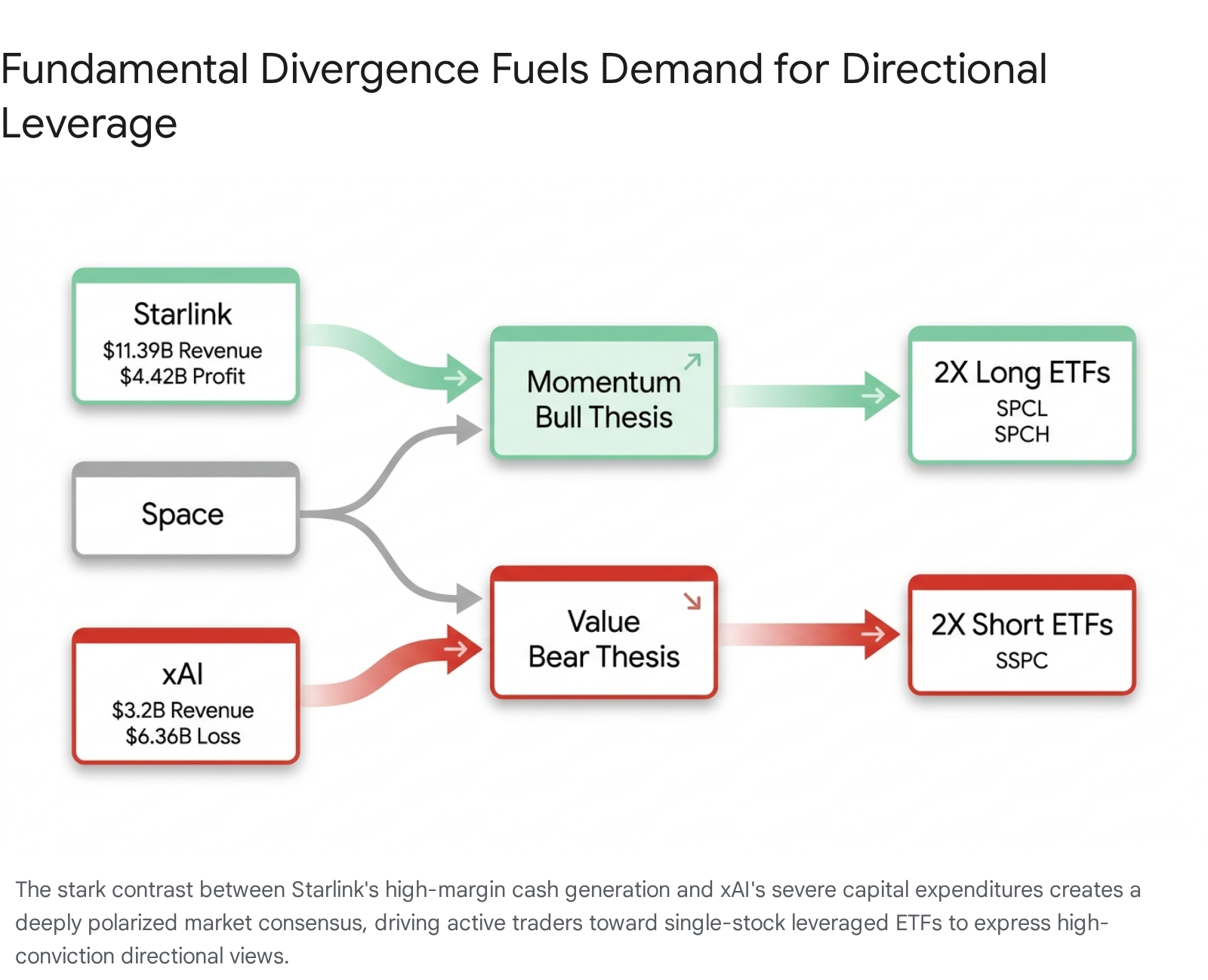

| Connectivity (Starlink) | $11.39 Billion | $4.42 Billion Operating Profit | Functions as the enterprise's cash engine. Maintains a 63% adjusted EBITDA margin with over 10.3 million active subscribers. Average revenue per user (ARPU) compressed from $99 to $66 as the service scaled globally 91213. |

| Space (Launch & Starship) | ~$4.08 Billion (Est.) | Moderate Operating Loss | Represents the legacy foundation. Dominates the global payload delivery market but requires massive, ongoing R&D expenditures to fund the commercialization of the fully reusable Starship architecture 369. |

| Artificial Intelligence (xAI) | $3.20 Billion | $6.36 Billion Operating Loss | The primary driver of the corporate deficit. Houses the Grok LLM and the Colossus supercomputer. Burned $12.7 billion in annual capital expenditure, including $7.7 billion in Q1 2026 alone. Carries a $20 billion bridge loan maturing 15 months post-IPO 11213. |

Polarization of Market Sentiment

The financial divergence between the highly profitable Starlink network and the cash-incinerating xAI division fuels a deeply bifurcated market consensus. The bullish thesis, championed by institutional growth investors and momentum traders, views SpaceX as an unassailable technological monopoly. This perspective relies on Starlink's 50% year-over-year revenue growth and the estimated $26.5 trillion total addressable market for orbital AI data centers, assuming the successful deployment of xAI infrastructure via Starship logistics 611.

Conversely, the bearish thesis focuses on the immediate financial realities of the S-1 filing. Value-oriented analysts emphasize the severe valuation multiple, noting that even if Starlink were valued at a generous 20x EBITDA multiple ($144 billion), the remaining $1.6 trillion of the market cap requires speculative leaps regarding unproven AI hardware returns and long-term debt servicing capabilities 12. The integration of the $20 billion xAI bridge loan - much of which was utilized to acquire Tesla Megapacks and other infrastructure - creates an immense near-term capital burden that relies heavily on continuous access to highly favorable equity markets 61112.

This stark bimodal outlook - viewing the company either as the foundational infrastructure of the future digital economy or as an over-leveraged, significantly overvalued asset - is the exact catalyst that drives active market participants away from spot equity and toward high-leverage directional instruments.

Pre-IPO Price Discovery and Offshore Derivatives

The magnitude of the speculative appetite for SpaceX did not materialize solely on the morning of June 12. Because private market access had historically been gated to accredited investors and constrained by shallow liquidity, retail and institutional traders sought alternative venues for price expression. This demand birthed synthetic, 24/7 perpetual futures markets on decentralized and offshore cryptocurrency exchanges, most notably Hyperliquid and Binance, which facilitated sophisticated pre-IPO price discovery for weeks prior to the Nasdaq listing 1415.

Synthetic Perpetual Futures Markets

Trading under the ticker xyz:SPCX, these pre-IPO perpetual contracts were launched on Hyperliquid's Trade.xyz platform on May 18, 2026. Unlike traditional derivatives that rely on external data oracles to derive pricing from a spot market, these pre-IPO contracts functioned as their own closed-loop oracles, with pricing determined entirely by the internal order book dynamics of the platform 1416.

Initially, the speculative euphoria surrounding the impending listing drove the implied share price of the perpetual contracts significantly above the official $135 reference level. Transactions clustered in the $180 to $200 range, implying a theoretical market capitalization nearing $2.5 trillion 1415. The scale of this offshore activity was massive, definitively proving the institutional viability of synthetic pre-IPO markets. Across Hyperliquid, Binance, Coinbase International, and OKX, the total cumulative trading volume exceeded $2.2 billion, with open interest surpassing $215 million and daily volumes routinely eclipsing $250 million on peak days 1415.

Predictive Capacity and Bid-Ask Spread Compression

As the June 12 listing date approached, the efficiency of these offshore markets improved dramatically. Institutional arbitrageurs and quantitative funds, recognizing the utility of these instruments following the highly accurate pricing of the Cerebras (CBRS) IPO earlier in the year (where Hyperliquid perps priced the open within 1.3%), began deploying capital into the SPCX contracts 1415.

This institutional participation caused a massive compression in execution costs. At launch, the median hourly bid-ask spread on Hyperliquid SPCX contracts was a highly illiquid 1.04% (approximately 1.0 basis points). By the first week of June, median spreads had tightened to approximately 0.05 basis points, representing a 95% compression and reducing total execution costs to near 5.0 basis points for institutional-scale block trades 16.

| Venue Category | Reference Metric | Implied Share Price (Early June 2026) | Significance |

|---|---|---|---|

| Official IPO Pricing | Fixed Roadshow Price | $135.00 | Established the baseline corporate valuation and the anchor for immediate LETF exposure 317. |

| Private Secondary Markets | Accredited Block Trades (Forge, Hiive) | $128.00 - $136.64 | Reflected illiquid, pre-listing private market sentiment heavily constrained by availability 217. |

| Offshore Perpetual Futures | Aggregated VWAP (Hyperliquid, Binance) | $155.00 - $170.00 | Acted as the primary, highly liquid, 24/7 price discovery mechanism predicting the massive opening premium 141517. |

The hyper-efficiency of the tightening spread forced the perpetual futures to converge downward from their initial euphoric highs, settling at an aggregated volume-weighted average price (VWAP) of $155 on the eve of the IPO 1415. This pre-market anchoring fundamentally altered the psychology of the Nasdaq debut. Retail and institutional actors had been conditioned by the synthetic markets to view $155 - a 15% premium to the offering price - as the fair market-clearing equilibrium. Consequently, when SPCX spot trading opened, the equity instantly gapped up to trade in the $150 to $172 range, validating the predictive capacity of the offshore liquidity pools and setting the stage for aggressive leveraged momentum trading 181920.

Mechanics of SpaceX Single-Stock Leveraged ETFs

The financialization of the SpaceX IPO occurred instantaneously. Unlike historical mega-IPOs where the derivatives ecosystem required weeks or months to mature around the underlying asset, asset managers explicitly timed the launch of single-stock leveraged ETFs to capture the immediate volatility of the SPCX opening session. Single-stock ETFs are a relatively recent innovation in the retail market, abandoning traditional index diversification to track the daily performance of a single underlying corporate equity through the use of total return swaps and listed options 212223.

Profile of Leveraged Exchange-Traded Products

Three primary leveraged instruments were established to synthesize the volatility of the SpaceX debut: SPCL, SPCH, and SSPC.

| Ticker | Issuer | Target Leverage | Direction | Inception Date | Expense Ratio | Structural Strategy |

|---|---|---|---|---|---|---|

| SPCL | Defiance ETFs | 200% (2x) | Long (Bull) | June 12, 2026 | 1.31% | Uniquely anchored exposure at the $135 fixed IPO price, capturing the entirety of the Day 1 opening gap 2425. |

| SPCH | Leverage Shares | 200% (2x) | Long (Bull) | June 15, 2026 | 0.75% | Cost-leadership model utilizing swaps to maintain a daily 2x long mandate 2627. |

| SSPC | Leverage Shares | -200% (-2x) | Short (Bear) | June 15, 2026 | 0.75% | Inverse leveraged instrument allowing traders to short the momentum without facing hard-to-borrow fees 2829. |

Defiance ETFs secured a critical first-mover advantage by launching the Defiance Daily 2X Space ETF (SPCL) on the exact day of the SpaceX listing. In a highly unusual structural maneuver, SPCL established its initial swap exposure explicitly at the $135 IPO price, rather than waiting for the open market price discovery which was indicating a much higher premium 2530. By doing so, SPCL immediately absorbed the leveraged upside of the listing pop, cementing itself as the primary vehicle for high-risk retail and institutional day-traders seeking magnified exposure from the very first tick. Despite a relatively high expense ratio of 1.31%, the immediate availability of the instrument secured substantial early trading volume 2431.

Leverage Shares followed the subsequent Monday, June 15, launching both a 2X Long (SPCH) and a 2X Short (SSPC) ETF on the Cboe BZX Exchange. Operating with a highly competitive 0.75% expense ratio - roughly 30% to 40% lower than the category average for comparable synthetic products - these funds provided a complete, two-sided toolkit for active traders. The dual launch allowed market participants to navigate the violent price swings without relying on traditional margin accounts or navigating the exorbitant hard-to-borrow fees typical of heavily shorted, newly public low-float equities 283233.

Mathematical Mechanics of Daily Rebalancing and Volatility Decay

To achieve their stated objective of delivering exactly 200% or -200% of the daily price movement of SPCX, these single-stock LETFs rely heavily on derivative counterparties, primarily major financial institutions executing swap agreements 2934. The critical operational constraint for these funds is the word "daily." The leverage target is strictly confined to a single trading session. At the close of each market day, the fund's adviser must systematically rebalance the portfolio's notional exposure to maintain the precise 2x or -2x ratio relative to the fund's newly calculated net asset value (NAV) 2935.

Over holding periods extending beyond one day, the mathematics of daily compounding create a structural phenomenon known as "volatility decay" or "beta slippage." Because the leverage is reset at the end of every session, returns over longer periods become highly path-dependent. The required percentage gain to recover from a percentage loss is geometrically magnified, creating an inherent drag on performance in oscillating markets 2136.

Historical analogues in the single-stock LETF sector provide a stark warning regarding this decay. During early 2025, the GraniteShares 2x Long NVDA Daily ETF (NVDL) experienced a period of elevated volatility. While the underlying NVIDIA stock fell approximately 35% from peak to trough, the daily compounding effect of the 2X LETF resulted in a massive 67% drawdown for NVDL shareholders 37.

When applied to the extreme volatility of the SPCX post-IPO window, this mathematical certainty forces rational participants to utilize SPCL, SPCH, and SSPC strictly as tactical, short-term momentum instruments. Active traders must constantly rotate in and out of the funds intraday to avoid overnight gap risks and compounding decay. This high-frequency rotation further drives transaction volumes in the derivatives space, contributing indirectly to the velocity of the underlying equity 2228.

Daily Rebalancing Feedback Loops in Low-Float Environments

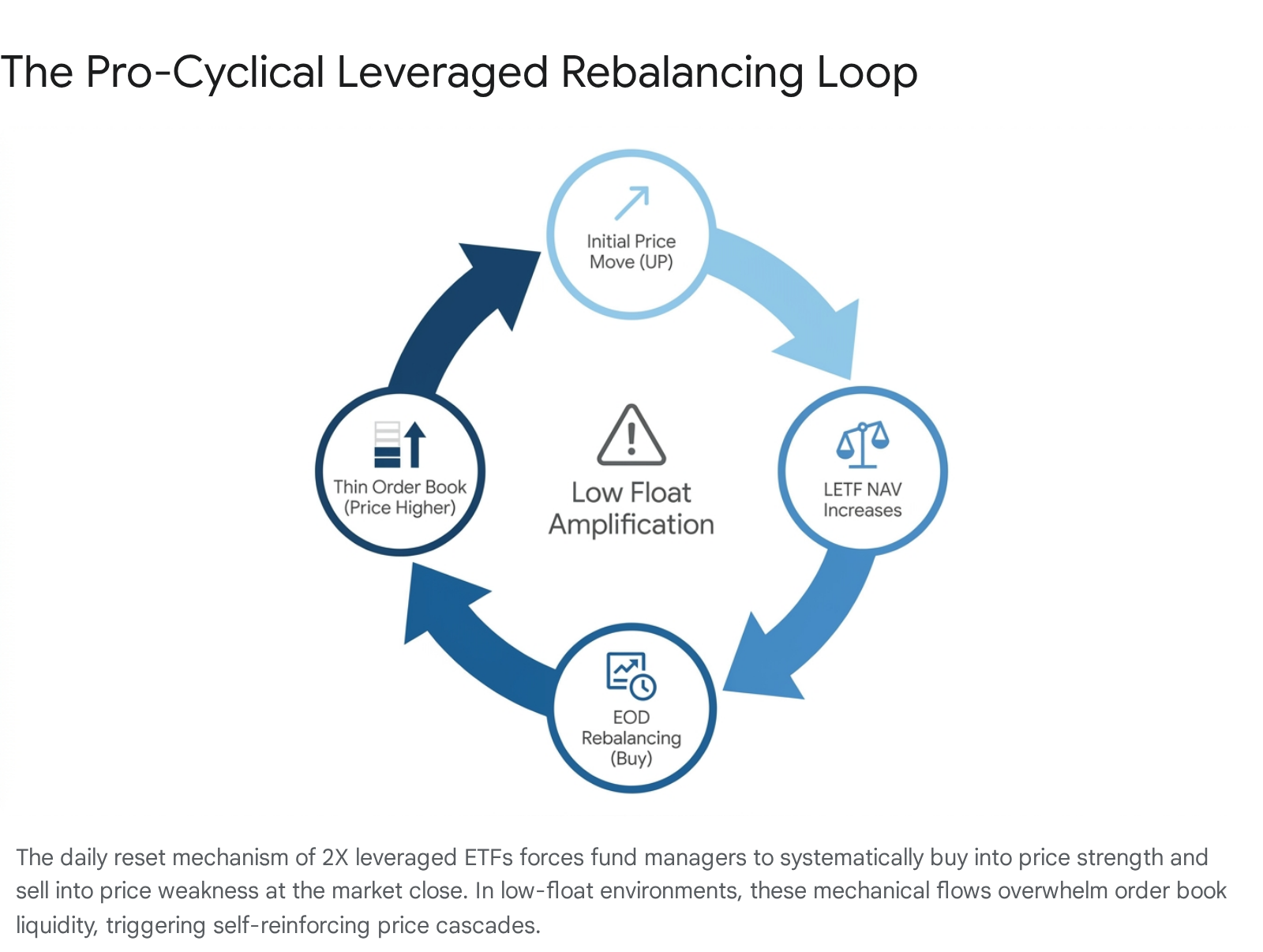

The daily reset mechanism of single-stock LETFs is not merely an internal portfolio management procedure; it generates vast external market externalities. The rebalancing of these funds creates structural, price-agnostic, pro-cyclical trading flows that directly and severely impact the price of the underlying equity 1029.

Interaction Between ETF Rebalancing and Underlying Spot Prices

To maintain a constant 2x leverage ratio, a long LETF like SPCL or SPCH must mechanically increase its notional exposure when the underlying stock rises, and decrease its exposure when the stock falls.

If SPCX experiences a 10% intraday surge, the NAV of the 2X Long ETF theoretically increases by 20%. To align the new, larger asset base with the 2x exposure mandate for the following trading session, the fund's swap counterparties must acquire additional SPCX shares (or equivalent delta exposure) immediately prior to the market close 2938. Therefore, the ETF is structurally forced to buy into strength.

Conversely, if SPCX suffers a 10% drop, the ETF's NAV contracts by 20%. The fund must then sell into weakness to deleverage its shrinking asset base and avoid exceeding its 2x mandate. Paradoxically, the 2X Short ETF (SSPC) exerts the exact same directional pressure on the underlying market. To maintain a -200% inverse target, SSPC must aggressively buy (cover short exposure) as prices rise to reduce leverage, and short more aggressively as prices fall to increase exposure 2938.

The Constant Leverage Trap

When SPCL, SPCH, and SSPC accumulate substantial assets under management, their combined end-of-day rebalancing flows become a massive, price-insensitive force. In a highly liquid, mature mega-cap equity, these flows are easily absorbed by the deep limit order book. However, in the severely starved 4% free float of SPCX, these mechanical buy/sell orders execute against a shallow pool of available liquidity.

This creates a dangerous self-reinforcing feedback loop: an initial intraday rise in SPCX forces all related LETFs (both long and short) to buy more SPCX at the market close.

This concentrated buying pressure overwhelms the shallow order book, pushing the price even higher into the closing bell. The artificially inflated closing price then dictates a higher starting point for the next session, demanding even more buying if the momentum continues 2939.

Dealer Hedging and Gamma Exposure

The secondary, and potentially more violent, force amplifying SPCX volatility stems from the options market. Because the retail demand for the IPO was so heavily marginalized by the lack of direct share allocations, a massive contingent of retail capital immediately pivoted to the options market to secure synthetic exposure 4041. Options provide outsized leverage for a fraction of the capital cost, making them the preferred venue for speculative fervor.

Options Market Maker Obligations

When a retail trader purchases a short-dated call option on SPCX (betting that the price will rise rapidly), a professional market maker or institutional dealer is typically on the other side of that trade, selling the call. Crucially, market makers are not in the business of taking directional bets; their objective is to capture the bid-ask spread and remain completely market-neutral 4243.

To achieve this neutrality, the market maker must execute a strategy known as delta hedging. Because the dealer is short a call option, they possess negative delta (they lose money if the stock goes up). To offset this exposure, the dealer must purchase shares of the underlying SPCX stock in the spot market. If the price of SPCX continues to rise, the delta of the short call option increases at an accelerating rate - a dynamic governed by the option's "gamma" 4044.

Mechanics of the Gamma Squeeze

A "gamma squeeze" materializes when this structural hedging requirement collides with a highly illiquid underlying asset. In a positive gamma environment, the market maker is forced to continuously purchase more SPCX shares as the price moves higher, effectively chasing the rally they are trying to hedge against. As dealers execute these massive, price-insensitive market orders, they sweep through the shallow SPCX limit order book 4245.

This rapid consumption of liquidity drives the SPCX spot price even higher. The higher spot price further increases the gamma of the options, which in turn forces the dealers to buy even more shares, creating a runaway upward spiral entirely detached from the company's fundamental valuation 4041.

In traditional, mature markets, organic sellers eventually emerge to capitalize on the inflated prices, providing liquidity and halting the squeeze. However, because 96% of SPCX shares are locked up under staggered agreements, natural sellers are virtually non-existent during the post-IPO window 1. The market makers are forced to bid higher and higher to solicit shares from the tiny 4% free float, exacerbating the violent price trajectory.

The Liquidity Cascade Phenomenon

When the daily rebalancing requirements of LETFs (SPCL, SPCH, SSPC) synchronize with the forced delta-hedging flows of options dealers, the market structure reaches a critical failure point. Financial theorists and quantitative researchers refer to this convergence as a "liquidity cascade" 103945.

Pro-Cyclicality of Market Interventions

The traditional paradigm of corporate finance assumes that derivative prices are strictly derived from the underlying spot asset. In a liquidity cascade, the tail wags the dog: the volume, leverage, and structural imperatives of the derivatives market become so overwhelmingly large that they dictate the price of the underlying equity 1041.

Academic researchers and market structure experts refer to this modern dynamic as the "Squid Game Stock Market." In a highly relevant 2025 research paper by Acadian Asset Management, analysts observed a direct precedent in the Korean equity markets. During a concentrated speculative frenzy surrounding quantum computing micro-caps and semiconductor giants, Korean retail traders utilized 2X single-stock ETFs to acquire over 40% of the effective float of certain assets 46. By monopolizing the float through leveraged vehicles, these retail participants effectively became the "marginal price-setters." The institutions and dealers managing the derivative plumbing possessed inelastic, observable demand constraints, forcing them to execute trades that continually validated the retail-driven momentum 46.

SpaceX presents this exact structural anomaly, but on a macro scale. With passive index funds legally mandated to hold the stock, LETFs forced to rebalance daily, and options dealers trapped in gamma feedback loops, the traditional price discovery mechanism is entirely suspended 639.

Systemic Fragility and Margin Cascades

While gamma squeezes and LETF rebalancing generally drive prices upward during euphoric IPO windows, the mechanics of a liquidity cascade are inherently symmetric. The same structural forces that artificially inflate the asset pose a catastrophic risk of violent unwinding.

If a minor macroeconomic shock or technical resistance level triggers an initial sell-off in SPCX, the feedback loop reverses instantly. As the spot price falls, options dealers must rapidly dump their delta-hedge shares to maintain neutrality. Simultaneously, the LETFs must mechanically sell into the falling market to deleverage their shrinking NAVs. Stop-loss clusters from retail participants are triggered, and heavily leveraged margin accounts face forced liquidations 4045.

This synchronized selling pressure evaporates the bid-side of the order book. In the offshore derivatives markets, this can trigger Auto-Deleveraging (ADL) mechanisms. When exchange insurance funds are depleted by rapid liquidations, the exchange automatically forces the closure of profitable positions to cover the losses of bankrupt accounts, adding yet another layer of forced, price-agnostic selling 45. Because passive index funds do not act as active value buyers to support the falling price, the result is a market that is "fragile at the highs," where a minor directional shift can cascade into a severe collapse in asset value 3945.

Conclusion

The market dynamics surrounding the SpaceX IPO represent the apex of modern financialization, illustrating a profound disconnect between corporate fundamentals and equity market microstructure. Despite operating a cash-incinerating artificial intelligence division and relying heavily on future, unproven commercializations of its Starship architecture, the conglomerate commanded a record-shattering $1.77 trillion valuation 21113.

However, the day-to-day trading trajectory of SPCX is dictated not by its long-term technological viability, but by a highly fragile market plumbing. An unprecedented 96% lock-up creates a severely starved free float, rendering the order book exceptionally thin 13. Against this illiquid backdrop, the immediate introduction of single-stock leveraged ETFs - SPCL, SPCH, and SSPC - alongside dense retail options activity introduces massive, inelastic, pro-cyclical trading flows 2527.

As fund sponsors systematically rebalance their swaps at the market close, and options dealers continuously delta-hedge their gamma exposure, they are forced to execute transactions that overwhelm the shallow liquidity pool 383940. Investors interacting with SPCX or its derivative proxies are participating in an ecosystem governed by the mechanics of liquidity cascades rather than fundamental price discovery. While these vehicles offer the capacity for extraordinary short-term returns during gamma-driven momentum bursts, their structural design mathematically guarantees that any reversal in market sentiment will be amplified into violent, rapid drawdowns as the accumulated leverage is forcefully unwound.