Cryptocurrency Exchange Regulatory Risk in 2026

The global cryptocurrency exchange industry has reached a critical regulatory inflection point in the middle of 2026. Following years of overlapping jurisdictional claims and regulation-by-enforcement paradigms, major financial markets have formalized distinct operational frameworks for digital asset intermediaries. This maturation fundamentally alters the risk profile and valuation metrics of market participants, transitioning regulatory compliance from a theoretical legal risk to a formalized operational cost structure. In the United States, a change in presidential administration and leadership at the Securities and Exchange Commission (SEC) has triggered the dismissal of legacy enforcement actions and introduced proposed safe harbors for token issuers 122. Concurrently, the European Union is executing the final phase of its Markets in Crypto-Assets (MiCA) regulation, requiring all Crypto-Asset Service Providers (CASPs) to secure full authorization by July 1, 2026, or face immediate operational cessation 34.

Against this macroeconomic and regulatory backdrop, cryptocurrency exchanges are aggressively acquiring regional licenses to secure market share and legitimize their operations ahead of anticipated public offerings. The trajectory of Payward Inc., operating globally as Kraken, serves as a primary case study for institutional analysts. Once heavily scrutinized by the SEC - resulting in a $30 million settlement and the suspension of its U.S. staking services in 2023 - Kraken has systematically restructured its compliance architecture 5. By 2026, the firm has relaunched compliant staking in the U.S., secured CASP status under MiCA, expanded into the Middle East under the Virtual Asset Regulatory Authority (VARA), and navigated complex private-market valuations ahead of a delayed Initial Public Offering (IPO) 6798. This report provides an exhaustive analysis of the SEC enforcement posture, the MiCA implementation landscape, and the financial implications of Kraken's global licensing strategy compared to public benchmarks such as Coinbase.

United States Securities and Exchange Commission Posture

The posture of the U.S. SEC in 2026 demonstrates a stark departure from the aggressive litigation strategy that characterized the 2022 - 2024 period. Under the leadership of Chairman Paul Atkins, the agency has reoriented its focus toward capital formation, inter-agency harmonization, and the establishment of principles-based regulatory perimeters for digital assets 910.

Legacy Enforcement Dismissals

In early 2025, the SEC began exercising prosecutorial discretion to systematically dismiss or pause several high-profile enforcement actions against major cryptocurrency exchanges, including Coinbase, Binance, and Kraken 2210. The SEC explicitly stated that these dismissals rested on a judgment to facilitate ongoing efforts to reform the regulatory approach, rather than on a definitive assessment of the fundamental merits of the alleged claims 211.

For Kraken, the dismissal of the November 2023 lawsuit - which had accused the exchange of commingling customer funds and operating as an unregistered securities exchange, broker, dealer, and clearing agency - removed a significant legal overhang 211. The case was dismissed with prejudice in March 2025, meaning the agency cannot refile the same charges against the company 2. This pivot allowed Kraken to allocate capital toward product expansion rather than external legal defense, a critical financial advantage given that competitor Coinbase spent upwards of $50 million on external legal fees fighting its respective charges prior to their dismissal 11. Democratic lawmakers, including Representative Maxine Waters, have heavily criticized these dismissals, alleging political influence and a retreat from investor protection mandates, pointing to the substantial political donations made by crypto firms during the 2024 election cycle 22.

The broader resolution of legacy lawsuits is also evident in the conclusion of the SEC's litigation against Ripple Labs. After a federal judge ruled in 2023 that programmatic sales of XRP on secondary exchanges did not constitute investment contracts, Ripple was ordered in August 2024 to pay a $125 million civil penalty exclusively for its direct institutional sales 12. By March 2025, the SEC formally dropped its appeal of the 2023 ruling, creating a binding legal reference point that normal trading of tokens on public exchanges generally does not satisfy the Howey test 12. This established precedent significantly lowers the listing risk for exchanges operating in the U.S.

Staking Compliance and Regulatory Overhaul

The cessation of hostile enforcement allowed exchanges to overhaul and relaunch yield-generating products. Kraken's regulatory history with staking serves as an illustrative example of this compliance evolution. In February 2023, the SEC charged Kraken with failing to register the offer and sale of its crypto asset staking-as-a-service program, arguing that investors lost control of their tokens and took on platform-associated risks without adequate disclosure 513. Kraken settled the charges without admitting guilt, agreeing to cease the program for U.S. clients and paying $30 million in disgorgement and civil penalties 51314.

Following the shift in SEC leadership, Kraken introduced a heavily revised, compliance-conscious staking product in January 2025 617. The restructured product, initially rolled out to clients in 37 states, utilizes a bonded staking model. Rather than pooling assets and promising a guaranteed yield untethered to network realities, the new model explicitly delegates staked assets to validators that handle transaction validation and block production 5617. These validators pass network rewards back to clients, minus transparent administrative fees. The platform explicitly discloses the inherent risks, including potential loss from slashing penalties, bonding periods, and asset depreciation, thereby satisfying the agency's demand for fair and truthful disclosure 17.

Regulation Crypto Assets and Proposed Safe Harbors

To replace the void left by halted enforcement actions, Chairman Atkins introduced the "Regulation Crypto Assets" framework, which was submitted to the Office of Information and Regulatory Affairs (OIRA) in early 2026 prior to public comment 1516. This framework establishes bespoke compliance pathways for developers and token issuers. By clarifying the primary issuance market, the SEC directly reduces the secondary-market listing risks for exchanges.

| Component | Description | Thresholds and Conditions |

|---|---|---|

| Startup Exemption | A non-exclusive, time-limited registration exemption for early-stage protocol developers. | Up to $5 million over a four-year window. Requires principles-based disclosures on a public website (similar to a whitepaper) 11617. |

| Fundraising Exemption | A new offering exemption for investment contracts involving certain crypto assets. | Up to $75 million across any 12-month period. Requires the filing of disclosure documents including financial statements 1517. |

| Investment Contract Safe Harbor | An off-ramp allowing specific digital assets to exit the legal definition of a security. | Applies once the issuing team fully completes or permanently ceases the "essential managerial efforts" promised during fundraising 151617. |

Table 1: The three primary components of the SEC's proposed Regulation Crypto Assets framework, designed to provide practical compliance pathways for digital asset issuers 1151617.

SEC and CFTC Joint Jurisdictional Taxonomy

A persistent source of systemic risk for U.S. cryptocurrency exchanges has been the jurisdictional friction between the SEC and the Commodity Futures Trading Commission (CFTC). On March 17, 2026, the two agencies issued a landmark joint interpretation establishing a unified federal framework for assessing digital assets and outlining how the Howey test applies to digital-asset transactions 181920.

The interpretation introduced a five-category token taxonomy designed to reduce regulatory arbitrage and provide market participants with predictable asset classifications 1921. Crucially, the release expressly classified Bitcoin and Ether as non-security digital commodities, solidifying CFTC jurisdiction over their spot transactions 10.

| Taxonomy Category | Definition and Characteristics | Examples |

|---|---|---|

| Digital Commodities | Assets linked to the programmatic operation of a functional crypto system, deriving value from supply/demand rather than managerial efforts. | Bitcoin (BTC), Ether (ETH) 1021. |

| Digital Collectibles | Assets designed to be collected or used, conveying rights to digital representations (e.g., artwork) without intrinsic economic rights. | CryptoPunks, Chromie Squiggles 21. |

| Digital Tools | Crypto assets that perform a practical, non-financial function or provide access to decentralized computing resources. | Utility tokens 1021. |

| Stablecoins | Assets designed to maintain a stable value relative to a fiat currency or other reference asset. | GENIUS Act-compliant stablecoins 1021. |

| Digital Securities | Assets sold as part of an investment contract where purchasers rely on the essential managerial efforts of an identifiable promoter. | Early-stage, centralized protocol tokens 1021. |

Table 2: The joint SEC-CFTC five-category crypto asset taxonomy established in the March 2026 interpretive release 1021.

Additionally, the guidance clarified that activities such as protocol mining, protocol staking, wrapping, and airdrops generally do not involve securities transactions inherently, provided the programmatic design does not create expectations of profit derived solely from the managerial efforts of identifiable promoters 1819. This interpretation was accompanied by a Memorandum of Understanding (MOU) establishing "Project Crypto" as a joint initiative for regular data sharing, cross-training, and coordinated enforcement 2021.

Legislative Action and the CLARITY Act

Despite alignment at the executive agency level, comprehensive market structure legislation remains stalled in the U.S. Congress, leaving the industry reliant on agency interpretations rather than durable statutory frameworks. The Digital Asset Market Clarity Act (CLARITY Act), which seeks to formally codify the SEC-CFTC jurisdictional boundaries, passed the House of Representatives with a bipartisan margin of 294-134 in July 2025 2223.

Senate Delays and Probability of Enactment

On May 14, 2026, the Senate Banking Committee advanced the CLARITY Act by a vote of 15-9, with thirteen Republicans joined by two Democrats 2223. If enacted, the bill would mandate that client assets be held by a qualified custodian and kept strictly separate from firm funds, require crypto firms to register with the CFTC, and establish minimum capital thresholds 7.

However, the legislation's future on the Senate floor remains highly uncertain due to a congested legislative calendar preceding the August recess 2227. The bill must be merged with text from the Senate Agriculture Committee before a floor vote can occur 22. Significant disputes remain regarding conflict-of-interest language, stablecoin yield rules, and illicit finance provisions 22. Specifically, the American Bankers Association has lobbied to close perceived loopholes that would allow exchanges to bypass bans on paying interest on payment stablecoins, while crypto advocates argue these yields are fundamental to decentralized finance 2425.

Consequently, institutional analysts have adjusted their expectations. Galaxy Research lowered its estimate of the probability that the CLARITY Act becomes law in 2026 from 75% down to 60%, noting that if Senate Majority Leader John Thune does not schedule floor time by July, the procedural window will effectively close until after the midterm elections 27. In response, a coalition of over 200 crypto companies, including Kraken and Coinbase, sent an urgent letter to Senate leadership on June 9, 2026, demanding a floor vote and emphasizing the necessity of preserving Section 604 - the Blockchain Regulatory Certainty Act (BRCA) - which shields non-controlling software developers from federal money transmission prosecution 2324.

European Union Markets in Crypto-Assets Implementation

While the U.S. navigates evolving agency interpretations and legislative bottlenecks, the European Union has transitioned into a period of strict, harmonized enforcement under the Markets in Crypto-Assets (MiCA) regulation. Formally known as Regulation (EU) 2023/1114, MiCA replaces a fragmented network of national laws with a single regulatory regime across all 27 EU member states, granting passportable operating rights while imposing severe operational standards on market participants 2627.

Expiration of the Grandfathering Period

The most pressing regulatory event for exchanges in the EU is the July 1, 2026, deadline, marking the absolute end of the MiCA transitional "grandfathering" period 42628. Under Article 143(3) of the regulation, entities that were legally providing crypto-asset services under applicable national laws prior to December 30, 2024, were temporarily permitted to continue operations without immediate compliance 2629. Several member states, including France, Luxembourg, and Malta, adopted the full 18-month transitional window to allow firms to prepare applications 2628.

As of July 1, 2026, any entity providing crypto-asset services to EU clients without a formalized MiCA license is in direct breach of EU law and faces immediate enforcement action 42830. The European Securities and Markets Authority (ESMA) has explicitly warned that unauthorized entities must have implemented robust, credible wind-down plans 30. These plans must arrange for the orderly offboarding of clients without causing economic harm, such as organizing the transfer of crypto-assets to an authorized CASP or to a self-hosted wallet 30. Furthermore, ESMA has stated that offshore entities are strictly prohibited from soliciting EU clients outside the narrow exception of reverse solicitation, effectively centralizing the European market around a smaller cohort of highly capitalized, fully compliant operators 430.

Operational Compliance and Technical Standards

The operational burden of maintaining a MiCA license in 2026 is governed by ESMA's highly detailed Level 2 and Level 3 technical standards, which dictate the precise mechanisms of compliance 329.

A key operational hurdle introduced for trading platforms is the standardization of data reporting. CASPs are required to maintain order book records using a standardized, machine-readable JSON schema to ensure cross-border comparability and facilitate market surveillance by National Competent Authorities (NCAs) 29. Similarly, crypto-asset whitepapers must comply with the iXBRL format requirement 29.

Furthermore, ESMA's guidelines on the prevention and detection of market abuse require CASPs to implement sophisticated transaction monitoring systems to detect insider trading and market manipulation, directly modeled on traditional finance's Market Abuse Regulation (MAR) framework 2731. CASPs must also adhere to guidelines for assessing the knowledge and competence of their staff (applicable from July 2026), ensure the segregation of client assets, and implement rigorous anti-money laundering and countering the financing of terrorism (AML/CFT) processes 262732.

Stablecoin Oversight and NFT Classification

MiCA imposes its strictest rules on stablecoins, classifying them as either Asset-Referenced Tokens (ARTs) or E-Money Tokens (EMTs) 3. Issuers face stringent capital and reserve requirements and must provide holders with direct redemption rights, reflecting regulators' views of stablecoins as potential systemic risks 327. These specific provisions (Titles III and IV) entered into application early, on June 30, 2024 2627.

Regarding Non-Fungible Tokens (NFTs), MiCA explicitly excludes "unique and non-fungible" digital assets from its scope 27. However, ESMA employs a "substance over form" principle, indicating that fractionalized NFTs or those issued in large, interchangeable collections may be functionally reclassified as fungible crypto-assets and subjected to MiCA regulation 27. ESMA is expected to publish dedicated guidelines on precise NFT classification by late 2026 27.

The Kraken Global Licensing Landscape

To survive the consolidation of the global crypto market driven by escalating compliance costs, Kraken has aggressively pursued jurisdictional licenses, shifting from a technology-first startup to a regulated global financial intermediary.

European Economic Area Authorization

Kraken successfully navigated the MiCA transition, securing its operational footprint across Europe ahead of the deadline. Through its subsidiary, Payward Europe Solutions Limited, Kraken obtained full authorization as a CASP from the Central Bank of Ireland (CBI), holding registration number C468360 37. This license grants Kraken passporting rights to offer crypto-asset custody, exchange, execution of orders, and portfolio management services across all 30 EEA states 837.

In addition to its CASP status, Kraken maintains complementary regulatory licenses in the region to support traditional finance integrations. Payward Ireland Limited operates as an authorized E-Money Institution (EMI), permitting the facilitation of fiat credit transfers, while Payward Europe Digital Solutions (CY) Limited holds a Markets in Financial Instruments Directive (MiFID) license in Cyprus to offer regulated investment and ancillary services, including derivatives trading for advanced users 837.

Middle East Expansion via VARA

Seeking to capitalize on the migration of institutional capital to jurisdictions with clear digital asset frameworks, Kraken secured regulatory approval from Dubai's Virtual Asset Regulatory Authority (VARA) in May 2026 73839. Under the VARA framework, Kraken's local subsidiary, Payward FZCO, operates as a licensed Broker-Dealer and Investment/Management platform 39.

This authorization enables Kraken to offer spot trading, over-the-counter (OTC) services, margin trading, staking, and institutional access via Kraken Prime directly to UAE residents 383940. Crucially, the VARA license allows clients to deposit and withdraw funds directly in UAE dirhams (AED), providing a secure fiat on-ramp connected to the exchange's global liquidity network 3839. By establishing a fully supervised local entity, Kraken satisfies VARA's strict segregation and risk disclosure rules, positioning itself favorably against offshore exchanges attempting to service UAE citizens 738.

Regulatory Friction in Singapore and Asia

Conversely, Kraken's expansion has faced insurmountable regulatory friction in specific Asian jurisdictions, notably in Singapore. The Monetary Authority of Singapore (MAS) has implemented some of the world's most restrictive consumer protection frameworks for digital assets 41. Under the Financial Services and Markets Act 2022 (FSM Act), MAS established a deadline of June 30, 2025, mandating that any locally based digital token service provider must cease offering services overseas unless properly licensed 3334. Firms violating this directive face fines of up to SGD 250,000 and potential imprisonment 33.

In 2026, MAS expanded its regulatory perimeter by enforcing a strict ban on retail crypto lending and staking, citing the opacity and risks of these activities for non-institutional investors 41. Furthermore, MAS mandated a 90% cold storage requirement for all customer assets held by licensed exchanges and implemented strict Travel Rule reporting for transfers above SGD 1,500 41.

Faced with these stringent capital requirements and the prohibition of its core yield-generating products, Kraken has opted not to maintain a license in Singapore 37. The exchange explicitly restricts services to Singaporean residents and does not offer DeFi Earn products in the jurisdiction 37. This decision reflects a strategic retreat from markets where compliance costs and product restrictions severely limit the addressable revenue pool.

Compliance Operations in Australia and North America

In Australia, Kraken operates through Bit Trade Pty Ltd, registered with AUSTRAC as a Digital Currency Exchange 44. To comply with Australia's implementation of the Financial Action Task Force (FATF) Travel Rule, Kraken rolled out mandatory verification protocols in March 2026 for all crypto transfers involving private, self-custodied wallets 45. Users are required to undergo self-certification via existing Two-Factor Authentication (2FA) or execute a digital signature to prove private key ownership before withdrawing funds, aligning the platform with domestic anti-money laundering obligations 45. Furthermore, derivatives are offered to Australian wholesale clients via an authorized representative agreement with Beaufort Fiduciaries Pty Ltd 35.

In North America, Kraken functions as a registered Restricted Dealer with the Ontario Securities Commission in Canada and maintains federal Money Services Business (MSB) registration with FINTRAC 37. In the United States, its acquisition of the CFTC-licensed futures broker NinjaTrader for $1.5 billion has provided Kraken with the necessary infrastructure to offer regulated margin and derivatives trading 93637. In Bermuda, Payward Digital Solutions Ltd holds a Class F license from the Bermuda Monetary Authority, serving as a broker for tokenized equities and derivatives for international clients 3744.

| Jurisdiction | Operating Entity | License / Registration Status | Primary Regulator |

|---|---|---|---|

| EEA (Europe) | Payward Europe Solutions Ltd | CASP (MiCA) | Central Bank of Ireland 37 |

| UAE (Dubai) | Payward FZCO | Broker-Dealer / Investment | VARA 39 |

| Australia | Bit Trade Pty Ltd | Digital Currency Exchange | AUSTRAC 44 |

| Canada | Payward Canada, Inc. | Restricted Dealer / MSB | OSC / FINTRAC 37 |

| Bermuda | Payward Digital Solutions Ltd | Class F Digital Asset Business | Bermuda Monetary Authority 37 |

| Singapore | N/A | Unlicensed / Restricted | MAS 37 |

Table 3: Overview of Kraken's primary international regulatory licenses and registrations as of mid-2026, demonstrating its shift toward localized, regulated entities 373944.

Financial Valuations and Regulatory Compliance Costs

The disparate paths taken by cryptocurrency exchanges to achieve compliance directly influence their financial performance, operational efficiency, and attractiveness to institutional capital. In 2026, the contrast is most evident when analyzing the valuation metrics of the privately held Kraken against the publicly traded Coinbase.

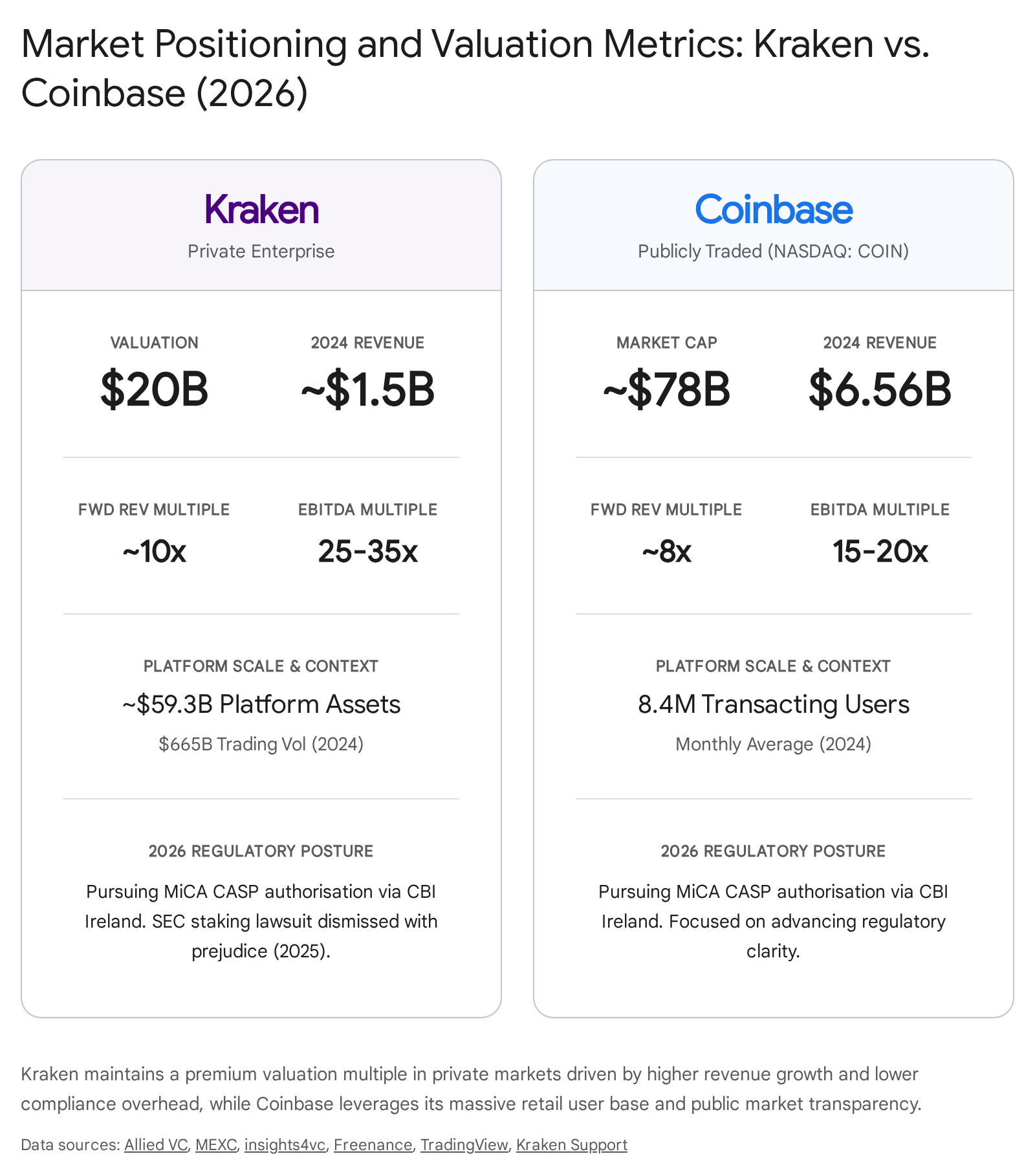

Institutional Competitiveness Against Coinbase

Both Kraken and Coinbase operate as the premier, U.S.-rooted, regulation-conscious exchanges with vastly cleaner enforcement records than offshore competitors 38. However, their operational models differ significantly. Coinbase caters heavily to retail investors through a streamlined user experience, generating massive fee revenue but incurring substantial overhead to maintain its public company transparency and broad asset listing framework 383940. In its 2024 Form 10-K, Coinbase reported $6.56 billion in total revenue, up from $3.1 billion the prior year, generating an operating income of $2.3 billion 4142. The platform boasted 8.4 million Monthly Transacting Users (MTUs) and highlighted the launch of its smart wallet and the Base L2 protocol 41. As a public entity, Coinbase carries Aon-syndicated crime insurance historically around $255 million, adding a layer of institutional trust 38.

Conversely, Kraken positions itself as a "profit-focused," security-first exchange optimized for active, serious traders and institutional clients 43. Kraken Pro offers meaningfully lower retail trading fees (0.16% maker / 0.26% taker) compared to Coinbase Advanced (0.40% maker / 0.60% taker), sacrificing margin per trade to capture high-frequency volume 38. Kraken's financial discipline allowed it to rebound robustly from the crypto winter, generating $1.5 billion in revenue in 2024, followed by an estimated $1.5 billion in just the first three quarters of 2025 3637.

The Kraken Initial Public Offering Delay

Despite its robust financial performance and product diversification, Kraken's path to public markets has encountered significant turbulence regarding valuation expectations. In November 2025, parent company Payward Inc. confidently filed a confidential draft S-1 with the SEC, concurrent with an $800 million funding round that valued the company at $20 billion 374344. This primary capital raise represented a 33% increase from its $15 billion valuation secured just two months earlier 4345. At the $20 billion mark, Kraken traded at a significant premium to Coinbase on a relative basis - roughly 10x projected revenue and 25 - 35x adjusted EBITDA, compared to Coinbase's 8x revenue and 15 - 20x EBITDA multiples 363745.

Furthermore, Kraken's valuation per user approximated $1,000, nearly double Coinbase's ratio, signaling strong private investor confidence in its institutional focus and expansion into traditional finance 3645.

However, the exchange ultimately paused its targeted Q1 2026 listing. Executive leadership cited deteriorating macroeconomic factors, tightening global liquidity, and cooling spot trading volumes across the cryptocurrency sector 374647. The delay underscores the fundamental reality of the cryptocurrency exchange business model: revenue remains highly cyclical and inextricably tethered to the underlying volatility and speculative interest in digital assets 3747. As Bitcoin prices retreated from peak levels and trading activity cooled entering 2026, the prospect of defending a 10x revenue multiple in public markets became untenable 454647.

This hesitation resulted in a marked correction in secondary market valuations. By April 2026, Deutsche Börse Group acquired a $200 million secondary stake in Kraken, giving the Frankfurt Stock Exchange operator a 1.5% fully diluted stake 9. This transaction occurred at an implied valuation of $13.3 billion, representing a 33% discount from the November 2025 peak 937. Market analysts note that public investors are increasingly evaluating crypto platforms based on durable profitability, stablecoin infrastructure, and regulatory moats rather than cyclical volume spikes 394748.

Kraken's executive leadership, including co-CEO Arjun Sethi, now targets a public listing in the second half of 2026 or potentially 2027, maintaining the confidential S-1 active while awaiting optimal market conditions 9384037. A successful listing will ultimately depend on the finalization of the SEC's proposed "Regulation Crypto Assets" safe harbors and the passage of legislative frameworks like the CLARITY Act, both of which would substantially de-risk the U.S. operating environment and justify a premium valuation for public shareholders.