Reverse innovation and developed market disruption

Origins and Theoretical Foundations of Reverse Innovation

For the latter half of the twentieth century, the paradigm of global commercial innovation was largely defined by Raymond Vernon's Product Life Cycle Theory, formulated in 1966. This macroeconomic framework posited that technologically advanced products are exclusively developed in capital-intensive, high-income countries (HICs) to satisfy the demands of affluent consumers 123. Under this conventional model, emerging economies were viewed merely as secondary recipients of these innovations. Multinational corporations (MNCs) would only export or shift manufacturing to low-income countries (LICs) once the technology matured, standardized, and required lower labor costs to maintain profit margins 12.

Consequently, the dominant corporate strategy for global expansion was downward adaptation, commonly referred to as "glocalization" 45. In this approach, Western corporations attempted to capture market share in developing nations by stripping expensive features from their established premium products, thereby creating cheaper, albeit watered-down, versions 567. However, glocalization frequently failed to resonate with the vast majority of consumers in emerging markets. By merely scaling down premium goods, MNCs produced offerings that were still too expensive for the masses, inadvertently targeting only the most affluent, elite segments of developing societies while ignoring the fundamental socio-economic constraints of the broader population 6.

A paradigm shift emerged at the intersection of academic theory and corporate practice in 2009. Dartmouth professors Vijay Govindarajan and Chris Trimble, alongside General Electric's then-CEO Jeffrey R. Immelt, codified a radical inversion of the traditional innovation model, coining the term "reverse innovation" 46. The concept, sometimes referred to as "trickle-up innovation" or "innovation blowback," describes a process whereby goods are developed specifically as inexpensive models to meet the unique needs of developing nations and are subsequently repackaged, upgraded, and exported for sale to Western buyers 6.

The fundamental driver of this phenomenon is the stark macroeconomic income gap between emerging and developed nations 4. For instance, a per capita income of roughly $3,000 in India necessitates solutions on an entirely different price-performance curve than a per capita income of $50,000 in the United States 4. Govindarajan argued that attempting to adapt a product designed for the American mass market downward to capture middle India is a structurally flawed endeavor 4. Instead, reverse innovation requires "clean-slate" engineering - forgetting the dominant logic that served the corporation in rich countries and building from the ground up 57.

This clean-slate approach demands what scholars term "strategic empathy" 8. Innovators must immerse themselves in the socio-economic and cultural realities of emerging markets through bottom-up research, acknowledging that unique solutions must be engineered to address absolute resource scarcity 8. Once these hyper-efficient, robust products achieve commercial viability in harsh, resource-constrained environments, they possess an intrinsic competitive advantage. When these products inevitably flow upward into HICs, they disrupt established incumbents by offering "good enough" performance at a fraction of the traditional cost, effectively altering the center of gravity for global research and development 479.

The Five Gaps Driving Emerging Market Innovation

The transition of an innovation from a developing market to a developed market is not a random occurrence; it is driven by specific systemic constraints that act as intense catalysts for radical problem-solving. Research identifies five primary "gaps" that separate emerging markets from developed markets. These disparities function as extreme incubators, forcing product developers to bypass incremental improvements and pursue breakthrough technological paradigms 1110.

The Performance Gap

Markets in LICs demand a paradigm of "value for many" rather than the traditional Western concept of "value for money" 10. Consumers in these regions require functional performance that meets basic standards, but at a hyper-reduced price point. The engineering challenge is exceptionally strict: to win over consumers in developing countries, product developers must provide roughly 100% of the core performance of an existing Western product at approximately 10% of the price 9. This forces engineers to eliminate superfluous features and focus entirely on the core utility of the product. A notable historical example is Narayana Hrudayalaya hospital in India, which utilized radical process innovations to perform world-class open-heart surgeries for $2,000, compared to upwards of $20,000 in the United States, while achieving a lower 30-day mortality rate (1.4% versus the US average of 1.9%) 11.

The Infrastructure Gap

Developing economies frequently lack the foundational public and private infrastructure taken for granted in the West, such as reliable electricity grids, paved roads, ubiquitous broadband internet, or advanced logistics networks 111. This absence forces engineers to design products that are robust, portable, and self-sustaining. For example, General Electric's development of the Vscan - a highly portable, battery-operated ultrasound scanner - was directly driven by the need to serve rural populations in China and India where traditional, bulky, grid-dependent ultrasound machines were useless 611. Once perfected for these harsh environments, the portable technology proved highly desirable in the US and Europe for rapid point-of-care diagnostics in emergency rooms and ambulances 11. Similarly, early heavy machinery exported to India by Siemens failed because the lack of logistical infrastructure prevented regular maintenance; Siemens was forced to engineer zero-maintenance equipment, which was later adopted globally due to its superior reliability 11.

The Sustainability Gap

Severe resource constraints, high population densities, and severe environmental pollution in rapid-growth emerging markets necessitate hyper-efficient, green technologies 1112. Because developing nations cannot afford the environmental externalities associated with the carbon-heavy industrialization paths historically taken by the West, they are highly incentivized to leapfrog directly to sustainable solutions. This constraint drives innovations in water desalination, off-grid renewable energy, and frugal manufacturing processes that require significantly less water and raw materials 911.

The Regulatory Gap

Emerging markets often possess less rigid regulatory frameworks and more agile institutional structures compared to the heavily regulated, litigious environments of the United States or the European Union 1113. While this can present risks, it also allows for faster iterative testing, clinical trials, and market deployment of breakthrough technologies. Innovators can test minimum viable products (MVPs) in real-world scenarios much faster, gathering behavioral data and refining the technology before facing the stringent compliance hurdles required to cross over into HICs 13.

The Preference Gap

Distinct cultural, social, and dietary preferences demand unique form factors, consumption models, and delivery mechanisms that differ radically from Western norms 11. Addressing these highly localized preferences often leads to the discovery of entirely new product categories that eventually find niche or even mass appeal in the developed world. The sports drink Gatorade, for instance, traces its underlying scientific origins to oral rehydration therapies developed during cholera epidemics in Bangladesh, addressing a critical localized need before being repackaged for athletic performance and global consumption 411.

Taxonomy of Resource-Constrained Innovation Types

As the academic literature surrounding emerging market innovation has matured, scholars have noted that "reverse innovation" is frequently conflated with related terminology such as frugal innovation, cost innovation, and good-enough innovation 112. While these concepts share an origin in resource-constrained environments, they represent distinct strategic approaches and product architectures.

Zeschky, Winterhalter, and Gassmann established a clarifying taxonomy to differentiate these phenomena, noting that misconceptions limit a manager's ability to craft proper development processes 1. Cost innovations primarily rely on process improvements and the arbitrage of local wage advantages in emerging markets to produce cheaper versions of standard Western goods; the core technology remains unchanged, but the manufacturing location shifts 1. Good-enough innovations take this a step further by actively tailoring the product to the resource-constrained market. Engineers strip away non-value-adding functions and redesign specific components to meet the exact, limited requirements of lower-income customers without compromising essential functionality 1.

Frugal innovations, conversely, do not merely reduce or adapt existing products. They represent entirely new product architectures and applications developed from scratch specifically for harsh, resource-constrained environments, generating an entirely new value proposition 112. Frugal innovations thrive on limitations, replacing costly R&D with efficient, localized problem-solving 7.

Crucially, reverse innovation is defined by its market trajectory rather than its product architecture. A reverse innovation can theoretically be a cost innovation, a good-enough innovation, or a frugal innovation, provided it successfully transfers from an emerging market environment to a developed-country market 112. It is the directional flow - from the periphery to the core, from the Global South to the Global North - that earns the classification 16.

Comparison of Innovation Paradigms

| Innovation Dimension | Traditional Glocalization | Cost & Good-Enough Innovation | Frugal Innovation | Reverse Innovation |

|---|---|---|---|---|

| Origin of R&D | High-Income Countries (HICs) | Emerging Markets | Emerging Markets | Emerging Markets |

| Primary Target Market | Affluent HIC consumers | Local low/middle-income markets | "Bottom of the Pyramid" | Originates in LICs, expands to HICs |

| Design Philosophy | Feature-rich, complex, premium | De-featured, process optimization | Clean-slate, ultra-low cost, robust | High-value, functional, scalable |

| Cost Structure | Capital-intensive R&D | Leverages low local labor costs | Resource-constrained efficiency | Maintains LIC cost basis in HIC |

| Incumbent Threat Level | Low (sustains status quo) | Low (localized competition) | Medium (captures new users) | High (disrupts core HIC markets) |

Data synthesized from Zeschky et al., Ostraszewska, and QMarkets. 1714

Mechanisms of Upward Adaptation and Crossover

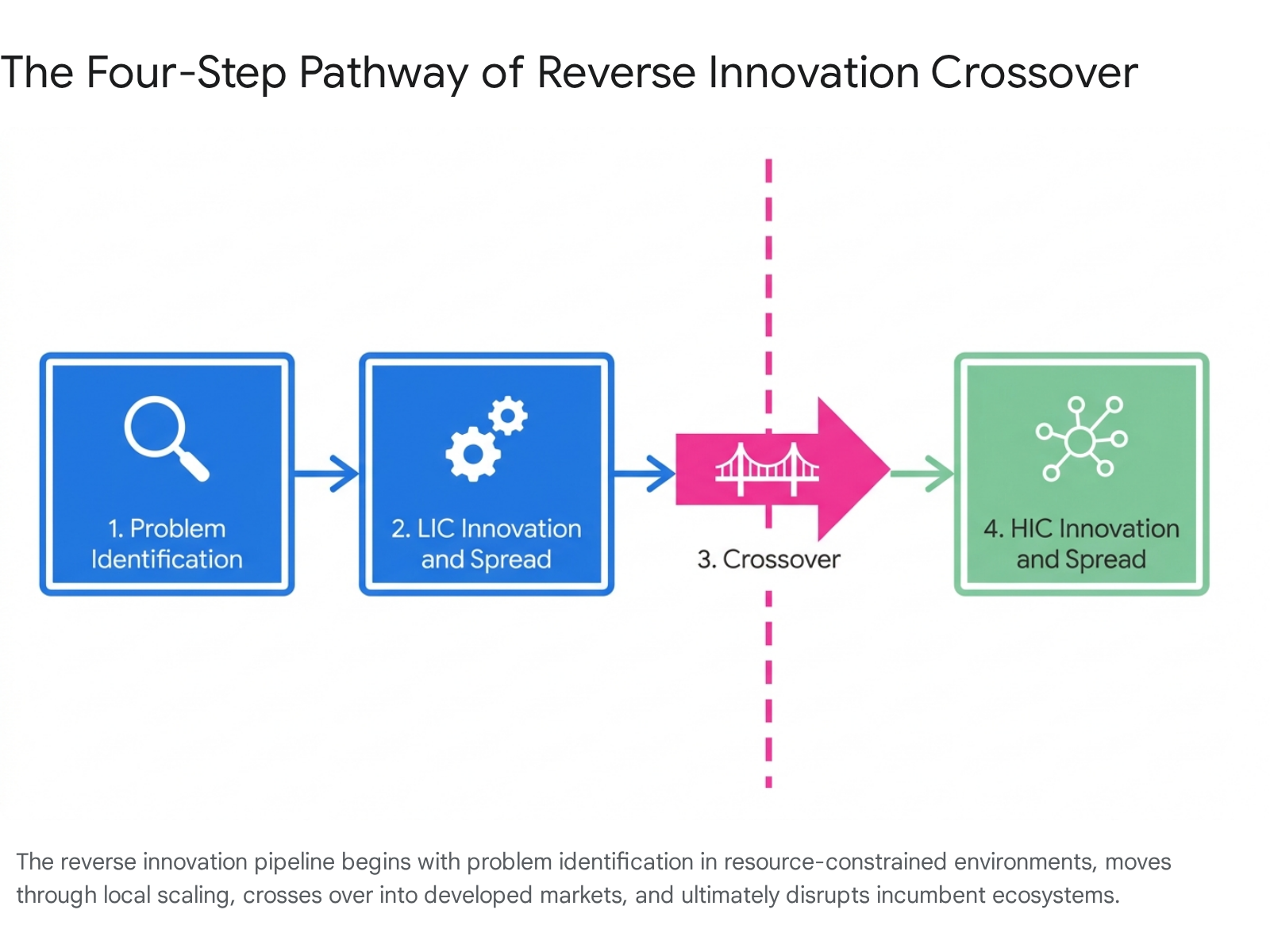

The structural process by which a localized emerging market innovation scales to become a global disruptor generally follows a sequential crossover model. Drawing from diffusion of innovation theory, this pathway maps the transition of an idea across two distinct innovation curves 10.

- Problem Identification: The process begins by identifying a core functional need that exists in both lower- and higher-income countries, but which is exacerbated by absolute constraints in the developing market (e.g., the need for cardiovascular diagnostics, reliable transportation, or secure financial transactions) 10.

- LIC Innovation and Local Spread: The product is engineered from a clean slate to meet the ultra-low price points and infrastructural deficits of the LIC. It is tested rapidly, leveraging the local environment as a living laboratory. As the product gains traction, it captures the local market by appealing to the "value for many" demographic 10.

- The Crossover Point: The innovation reaches a critical threshold of quality and performance. At this juncture, HIC consumers or corporations recognize that the frugal innovation, while lacking luxury features, fundamentally solves their problem at a highly attractive price point, effectively closing a previously unaddressed needs gap in the developed market 1110.

- HIC Innovation and Global Spread: The product is imported into the developed market. It often undergoes secondary adaptation or "re-engineering" to ensure compliance with stricter HIC safety standards, regulatory norms, and aesthetic expectations. Once adapted, it disrupts established product categories by offering an unbeatable price-performance ratio 1012.

The disruption of HIC incumbents by these crossover innovations is best understood through a neo-Schumpeterian analytical framework, which emphasizes the interaction between firm-level capabilities and institutional environments 15. Disruptive Innovation Theory, popularized by Clayton Christensen, suggests that incumbent firms rationally prioritize sustaining innovations that yield high profit margins from their most demanding, affluent customers 716. When an emerging market firm - or an agile HIC subsidiary operating in an emerging market - develops an ultra-low-cost product, the legacy incumbent views the innovation as financially unattractive due to its lower absolute margins and perceived inferiority 7.

This bounded rationality creates a strategic blind spot 17. As the frugal product is relentlessly refined in the hyper-competitive emerging market, its quality improves rapidly without a corresponding exponential increase in price 14. By the time the product crosses over into the developed market, it has achieved a price-performance ratio that legacy incumbents cannot match 15. Incumbents are hindered by complex supply chains, asset specificity, entrenched organizational routines, and an unwillingness to cannibalize their existing high-margin business models 1518. Furthermore, companies with excessive resources often exhibit a propensity to avoid risk and maintain the status quo, leaving them highly vulnerable to the entrepreneurial orientation of emerging economy multinational enterprises (EMNEs) that view reverse innovation as a primary vehicle for internationalization 7.

Automotive Sector Disruption and Chinese Electric Vehicles

The global automotive sector is currently experiencing one of the most profound reverse innovation shockwaves in modern industrial history, originating from China's electric vehicle (EV) and battery technology ecosystems. Historically, global automotive technology flowed linearly from legacy hubs in Detroit, Stuttgart, and Tokyo down to the developing world. However, China actively engineered a reversal of this dynamic. Utilizing a developmentalist state theory approach, China's dirigiste state coordinated a massive industrial policy encompassing critical minerals processing, battery engineering, domestic demand management, and charging infrastructure to leapfrog the established internal combustion engine (ICE) technological regime 15.

By building explicitly for the domestic Chinese market - a highly competitive, price-sensitive environment - Chinese original equipment manufacturers (OEMs) developed vehicles that defied Western expectations. In 2024, Chinese battery electric vehicles (BEVs) reached absolute price parity with fossil fuel vehicles, an achievement that continually eluded Western manufacturers 19. The sheer scale of production is unprecedented; in the first four months of 2025 alone, China's lithium-ion battery output surged by 68%, surpassing 473 gigawatt-hours (GWh), while battery exports in that same period reached approximately $21.7 billion 19. Consequently, China has established itself as the center of gravity for the automotive industry, accounting for nearly 80% of global EV battery output 20.

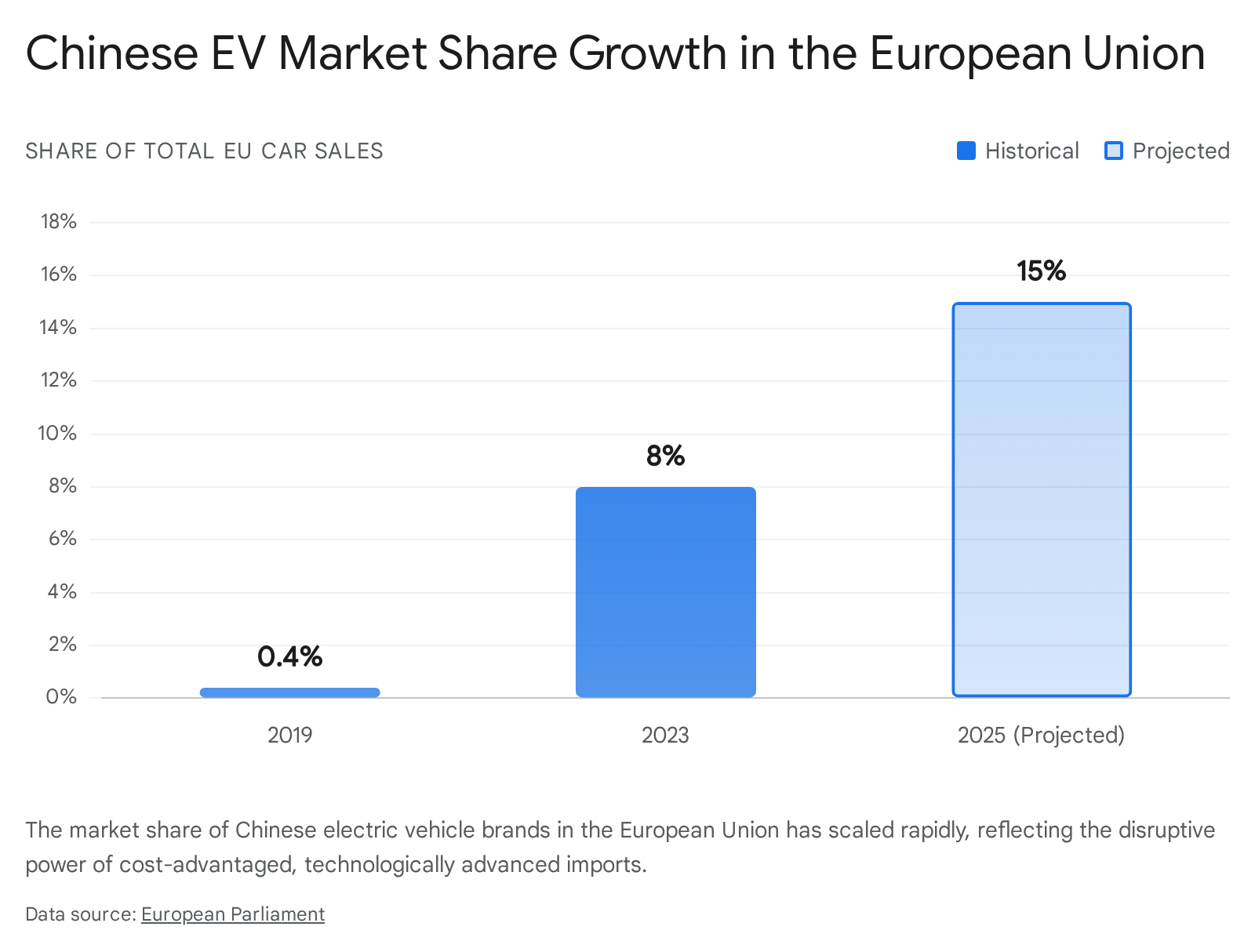

The disruption within Europe is severe and immediate. Between 2019 and 2023, the share of Chinese brands in European Union battery-electric car sales grew logarithmically from 0.4% to 8%, with projections pointing toward 15% market capture by the end of 2025 21.

Companies like BYD - which officially surpassed Tesla as the leading global producer of EVs in 2024 - and SAIC/MG have fundamentally disrupted the European automotive supply chain 2021. While Germany and the broader EU pursued fragmented industrial policies that lacked credible long-term commitments, allowing legacy incumbents to hedge and delay the EV transition to protect their ICE assets, Chinese firms achieved an insurmountable cost and technology advantage 15.

Recognizing the existential threat to an industry that generates 7% of the EU's GDP and supports nearly 14 million jobs, the European Commission initiated the largest anti-subsidy probe against China in its history in late 2023 21. This resulted in definitive countervailing duties imposed in late 2024, assigning specific tariffs ranging from 17.0% for BYD to 35.3% for SAIC, applied on top of the standard 10% base tariff 2021. However, experts warn that protectionist tariffs are insufficient to restore EU competitiveness 21. The reverse innovation trickle-up is now so entrenched that traditional European OEMs, facing technical obsolescence, are actively seeking joint ventures and partnerships with Chinese firms to access their superior software and battery architectures, a complete reversal of the 20th-century technology transfer dynamic 19.

Financial Sector Disruption and Algorithmic Underwriting

The financial services sector offers another powerful illustration of reverse innovation, specifically regarding the application of artificial intelligence (AI) in credit underwriting. Nubank, a digital-native banking platform originating in Brazil, exemplifies how solving complex constraints in a developing market creates a formidable weapon for global expansion. By Q1 2026, Nubank had scaled to over 135 million customers across Latin America, generating $5 billion in quarterly revenue, maintaining an exceptional 33% return on equity (ROE), and demonstrating immense pricing power and cost-to-serve advantages 2223.

Nubank's core innovation was developing a technological architecture capable of profitably underwriting credit for individuals historically excluded by traditional banking systems 22. In advanced economies, legacy credit scoring models depend heavily on historical repayment data housed in centralized credit bureaus (such as the FICO system in the United States). In emerging markets like Brazil and Mexico, vast segments of the population lack these formal credit files, rendering traditional underwriting impossible 24. To overcome this profound infrastructure gap, Nubank shifted away from traditional tabular feature engineering and developed nuFormer, a proprietary suite of transformer-based AI foundation models trained on over 600 billion behavioral transaction tokens 222425.

This system assesses live spending habits, app engagement, and real-time payment behavior rather than waiting for a legacy bureau file to exist. The result is unparalleled precision: Nubank reports that nuFormer delivered a 70% reduction in risk for equivalent populations compared to previous machine learning generations, and roughly three times the performance uplift seen in standard model refreshes 2226. Crucially, Nubank utilized these technological gains to increase its market share and sharpen customer selection rather than easing approval criteria, maintaining an early-stage credit delinquency ratio of just 5.0% despite aggressive expansion among the previously unbanked 2227.

Overcoming the US Neobank Cold-Start Problem

Having optimized this credit engine in the resource-constrained, high-risk, and macroeconomically volatile environments of Latin America, Nubank is now executing a textbook reverse innovation strategy by entering the highly competitive United States market 222324. In the US, traditional neobanks and fintech startups face a notorious "cold-start problem": they suffer from exorbitant customer acquisition costs (estimated by Javelin Strategy at $300 per customer, triple the global average), a lack of behavioral data to underwrite new users, and an inability to build profitable direct lending books due to restrictive sponsor-bank structures 24.

Nubank bypasses these barriers entirely by targeting the US Latino immigrant population - a demographic that contributes an estimated $4 trillion to the US GDP annually (making it the equivalent of the world's fifth-largest economy) but suffers from acute financial exclusion 24. Hispanic households in the US are five times more likely to be unbanked than White households, and 42% of Latinos had a credit application rejected between 2024 and 2026 24. Because traditional US credit bureaus cannot score immigrants lacking a Social Security number tied to a deep domestic credit file, these individuals are treated as subprime risks, despite often possessing reliable incomes and low default tendencies - a group analysts term "invisible primes" 24.

Because many of these individuals frequently travel and remit money from Brazil, Mexico, and Colombia, millions are already operating within the Nubank ecosystem 24. Nubank leverages its emerging-market AI engine to instantly read their cross-border transaction data, entirely bypassing the legacy US credit bureau system. Having secured conditional approval for a national bank charter from the US Office of the Comptroller of the Currency (OCC) in 2026, Nubank is positioned to deploy its hyper-efficient, battle-tested underwriting models to secure a highly profitable foothold in a mature HIC market with near-zero acquisition costs, directly disrupting US financial incumbents 2224.

Digital Public Infrastructure and Global Payment Systems

India's Unified Payments Interface (UPI) demonstrates how digital public infrastructure (DPI) developed to solve extreme inclusion challenges in the Global South can scale to disrupt mature, deeply entrenched financial ecosystems worldwide 2829. Launched in April 2016 by the National Payments Corporation of India (NPCI), UPI was designed with a monumental mandate: to transition an economy heavily reliant on physical currency - where cash accounted for over 90% of all transactions - into a digital-first ecosystem 2930.

To achieve this, the NPCI engineered an architecture framework with a set of standard Application Programming Interfaces (APIs) that enabled complete interoperability 28. UPI allows users to seamlessly and instantly transfer funds across multiple competing bank accounts and third-party mobile applications (such as Google Pay, PhonePe, and Paytm) 24/7, using a simple virtual ID or phone number, all with zero transaction fees for the consumer 282931. Accelerated by the Indian government's 2016 demonetization of high-value banknotes - which forced hundreds of millions to rapidly adopt digital payments - UPI achieved unprecedented scale 3031.

By 2023, UPI handled 117 billion financial transactions totaling $2.19 trillion in value, accounting for approximately 49% of all global real-time payment transactions 283233. In the single month of October 2024, the platform processed a historic 16.58 billion transactions across 632 integrated banks 32. The usage has evolved rapidly from simple peer-to-peer (P2P) transfers to complex person-to-merchant (P2M) transactions, which now comprise over 60% of total volume, empowering small-scale vendors and rural populations alike 2830.

Disrupting the Western Payments Oligopoly

In stark contrast, the payment systems in the United States and the European Union remain highly fragmented, lack universal interoperability, and are deeply reliant on high-fee card networks (such as Visa and Mastercard) 29. In the US, systems like Venmo or Zelle operate as siloed, closed-loop environments primarily suited for peer-to-peer transfers, lacking the universal merchant acceptance and centralized real-time settlement that UPI provides 2931.

UPI is currently executing a reverse innovation crossover into European markets. In early 2024, the NPCI partnered with the prominent French payment services firm Lyra Network to integrate UPI point-of-sale functionality in France, debuting the capability at the Eiffel Tower 333435. While the immediate goal was to facilitate frictionless, zero-fee remote bookings and dynamic QR code payments for the massive influx of Indian tourists abroad, the underlying technology poses a severe long-term threat to Western payment processors 3436. By offering a highly secure, real-time, cross-border payment solution featuring transparent exchange rates and bypassing the exorbitant merchant discount rates (MDR) mandated by legacy credit card companies, the reverse innovation of UPI sets a new global benchmark 33. It exposes the inefficiencies, friction, and rent-seeking behaviors embedded within HIC financial systems, providing a blueprint for the obsolescence of traditional Western banking rails.

Organizational Barriers and Implementation Failures

Despite the clear strategic advantages and global disruptive potential of reverse innovation, Western MNCs frequently fail to execute these strategies effectively. The literature indicates that the primary barriers are rarely technological; rather, they are deeply organizational, cultural, and structural 3738.

Traditional Western corporate work environments harbor interconnected obstacles that stifle the clean-slate thinking required for reverse innovation. These include rigid hierarchical structures that paralyze rapid decision-making, highly siloed R&D departments that prevent the cross-pollination of ideas, and bureaucratic processes that complicate the implementation of unstructured innovations 3738. Because reverse innovation inherently requires extreme decentralization - shifting strategic autonomy and P&L responsibility to local teams stationed in emerging markets - it directly conflicts with the centralized command-and-control structures that define legacy MNCs 41839.

Furthermore, HIC managers suffer from pervasive "cannibalization anxiety" 18. This is the institutional fear that introducing a highly functional, ultra-low-cost product developed in an emerging market will inevitably erode the premium pricing and high profit margins of their established domestic product lines 3. Instead of embracing the disruption, risk-averse leadership prioritizes short-term stability over long-term growth, burying the frugal innovation or refusing to allocate the necessary capital to scale it globally 3738. Additionally, severe legal and regulatory barriers in HICs - including strict tort liability, stringent standards of care, and complex health insurance reimbursement mechanisms - create a chilling effect, severely disincentivizing the importation of frugal healthcare innovations to countries like the United States 40.

The Necessity of Constraints: Over-Engineering vs. Frugality

The absolute necessity of the emerging market constraint is vividly highlighted when contrasted with homegrown Western innovation failures. In recent years, highly funded Silicon Valley projects like Quibi (a $1.75 billion short-form streaming failure) and Juicero (a $400 Wi-Fi-enabled juicing machine) collapsed spectacularly 4144. These HIC failures were characterized by massive capital deployment devoid of "ground truth." They were heavily over-engineered solutions searching for a problem, disconnected from real human constraints 4144. Quibi, for example, assumed a use case for on-the-go viewing that vanished during pandemic lockdowns, yet the company failed to pivot due to institutional arrogance and a refusal to acknowledge flawed assumptions 41.

Reverse innovation acts as an absolute antidote to this phenomenon. The severe resource constraints, low purchasing power, and lack of infrastructure in the Global South act as an uncompromising, Darwinian filter. By the time a product survives the emerging market, it is virtually guaranteed to possess absolute product-market fit and a hyper-efficient cost structure, immunizing it against the bloated over-engineering that plagues Western R&D 79.

The M-Pesa Anomaly: When Trickle-Up Fails

It is critical to acknowledge that reverse innovation is not an automatic or guaranteed process. Innovations that succeed brilliantly in one developing context can fail to cross over due to institutional misalignment.

The mobile money platform M-Pesa serves as a primary case study in expansion failure. Launched in Kenya in 2007 by Safaricom and Vodafone, M-Pesa revolutionized financial inclusion for the unbanked, leveraging a vast network of local retail agents to facilitate simple SMS-based money transfers 4243. Supported by early regulatory leniency and a near-monopoly telecom market share, M-Pesa became a cultural and economic phenomenon; by 2021, it boasted over 40 million users and processed over 11 billion transactions annually in Kenya alone 444546.

However, corporate attempts to execute a reverse innovation expansion of M-Pesa into other emerging markets (like India and South Africa) and lower-tier developed markets (like Romania) largely failed 4445. In India, M-Pesa encountered a vastly different and highly restrictive regulatory environment. The Indian central bank mandated physical presence requirements and stringent compliance guidelines that completely negated the agility of the mobile-only model 44. Furthermore, Vodafone failed to localize its service to specific Indian consumer preferences - such as the high demand for integrated utility bill payments - and faced insurmountable competition from entrenched local fintechs like Paytm, which had already captured 100 million users through aggressive marketing 44. Culturally, the high level of trust that Kenyans placed in mobile telecom operators was entirely absent in India, where consumers retained a strong preference for physical cash 4244. The M-Pesa case demonstrates that without deep cultural localization, precise regulatory alignment, and proactive strategic partnerships, the reverse innovation pathway breaks down entirely 4244.

Academic Critiques and Global South Perspectives

While reverse innovation is highly praised in corporate strategy and Western management literature as a panacea for growth, the theory has faced substantial academic critique, particularly from scholars situated in the Global South 747.

First, the terminology itself is heavily scrutinized by post-colonial scholars. Defining the flow of innovation from emerging economies to advanced economies as "reverse" exposes an inherently ethnocentric bias 5. It relies on the implicit, paternalistic assumption that the "normal" or "forward" flow of knowledge and technology is exclusively from the Global North to the Global South 347. By ordering global economies in hierarchies of development, the terminology reinforces center-periphery dynamics that other non-Western engagements with innovation 47.

Second, scholars argue that the practice of reverse innovation, as popularized by Western business literature, is highly extractive. By framing frugal innovations strictly through the lens of HIC corporate profitability and competitive advantage, the discourse reduces marginalized populations to "one-dimensional entities" that serve merely as test subjects and cheap laboratories for Western corporate R&D 47. Critics note that local innovations in India or Africa are often motivated by complex sociopolitical factors - such as human rights, community recognition, and mutual care - rather than purely market-driven utility 47. When Western MNCs appropriate these models solely to protect their global market share or boost quarterly revenues, they often strip the innovation of its local context and fail to address the systemic social, economic, and environmental injustices that necessitated the frugal innovation in the first place 4748.

Finally, within the realm of strategic management and international business theory, Disruptive Innovation Theory (DIT) and reverse innovation are critiqued for their exceptionally narrow focus on technological attributes and price-performance metrics. This myopic focus often ignores the broader socio-political, institutional, and firm-level dynamics required for genuine, sustainable technological transfer 16. Scholars emphasize that for emerging economy multinational enterprises (EMNEs) to truly benefit from their own ingenuity, they must retain strict ownership of their intellectual property, actively foster local entrepreneurial ecosystems, ensure proper succession planning, and resist simply acting as outsourced, low-cost R&D facilities for Western conglomerates 4950.

Strategic Imperatives for Multinational Corporations

To survive the paradigm shift initiated by reverse innovation, HIC incumbents must fundamentally restructure their research, development, and global management frameworks. The prevailing 20th-century strategy of maintaining core R&D exclusively in hubs like Silicon Valley, London, or Munich, while treating emerging markets as secondary, downstream sales territories, is structurally obsolete 111.

Organizations must aggressively decentralize their innovation networks. This requires granting full strategic autonomy, budgetary control, and P&L responsibility to local executive teams stationed in key emerging markets like India, Brazil, and China 4. These local teams must be empowered to pursue clean-slate engineering, actively encouraged to ignore the dominant logic of headquarters, and freed from the requirement to utilize legacy corporate architectures or expensive Western components 59.

Furthermore, corporate leadership must actively dismantle bureaucratic silos and foster an organizational culture that fundamentally tolerates the risk of failure - a necessary precondition for radical, resource-constrained experimentation 3738. If Western incumbents fail to overcome their cannibalization anxiety and refuse to disrupt their own legacy products with affordable, high-quality alternatives, indigenous EMNEs will inevitably cross over the geographic boundary and do it for them, permanently eroding the market share of the developed world's legacy institutions 318.