Disruptive and sustaining innovation theory

Introduction: The Intellectual History of a Misunderstood Paradigm

Since its formal introduction by Clayton M. Christensen and Joseph Bower in their 1995 Harvard Business Review article, "Disruptive Technologies: Catching the Wave," and its subsequent expansion in Christensen's seminal 1997 book, The Innovator's Dilemma, the theory of disruptive innovation has fundamentally altered the landscape of strategic management 112. Originally developed to explain the counterintuitive phenomenon of why well-managed, industry-leading companies consistently lose their market dominance despite adhering to established best practices - such as listening closely to their most profitable customers and investing heavily in new technologies - the theory posited that these very practices create systematic and fatal vulnerabilities 434.

The early iteration of the theory focused heavily on "disruptive technologies," relying on exhaustive analyses of the disk drive and mechanical excavator industries 25. However, by 2003, with the publication of The Innovator's Solution, co-authored with Michael E. Raynor, Christensen formally replaced the term "disruptive technology" with "disruptive innovation" 5. This semantic shift represented a profound evolution in the theoretical framework: Christensen recognized that very few technologies are intrinsically disruptive or sustaining in character 56. Rather, it is the underlying business model enabled by the technology, and the strategic positioning of that model against incumbent profit formulas, that generates the disruptive impact 56.

Despite this clarification, over the ensuing decades, the term "disruption" has been co-opted, diluted, and vernacularized. From Silicon Valley startups to mainstream financial media, it has evolved into a generic buzzword used to describe any breakthrough technology, any successful new entrant, or any rapid shift in market share 7108. This linguistic inflation has stripped the theory of its predictive power and diagnostic utility. When every successful innovation is retroactively labeled "disruptive," the strategic prescriptions originally developed by Christensen become dangerously misapplied, leading corporate boards to execute panicked defensive maneuvers against threats that require entirely different strategic responses 8910.

This comprehensive report seeks to restore the structural rigor of Christensen's original framework while extending its application to modern phenomena. By explicitly debunking pervasive misconceptions, providing a granular breakdown of the theory's core mechanics, and synthesizing profound scholarly critiques, this analysis contextualizes the theory within the realities of the 2020s and beyond. Furthermore, it expands the geographic and technological scope of the discussion, examining how contemporary digital ecosystems, Software-as-a-Service (SaaS) architectures, Generative Artificial Intelligence (GenAI), and the rise of frugal innovation in emerging economies like India and China both validate and challenge Christensen's foundational hypotheses 111512.

The Core Mechanics: Sustaining Trajectories vs. Disruptive Intersections

To understand disruptive innovation, one must first clearly distinguish it from its conceptual opposite: sustaining innovation. The failure to differentiate between the two is the root cause of most analytical errors in contemporary business strategy, as the two types of innovation demand diametrically opposed managerial responses 1718.

The Trajectory of Sustaining Innovation

Sustaining innovations are improvements to existing products, services, or business models that maintain the current trajectory of competition 71913. These innovations can be incremental, such as adding a high-resolution camera to an established smartphone line, or they can be radical, breakthrough leaps, such as the telecommunications transition from 3G to 4G cellular networks 319. The defining characteristic of a sustaining innovation is not its technological sophistication, but rather its economic intent: it is designed to sell better-performing products to an incumbent's most demanding, and therefore most profitable, high-end customers 62114.

Incumbent companies almost universally win battles of sustaining innovation 3. Because these innovations align perfectly with the incumbent's existing profit formula, cost structure, and brand equity, the organization is highly motivated to invest the necessary capital to out-engineer any challengers 67. Their internal processes - from resource allocation algorithms to sales incentives and supply chain logistics - are flawlessly calibrated to execute sustaining improvements 34. When an entrant attempts to challenge an incumbent head-on with a sustaining innovation, the incumbent will simply leverage its superior resources to acquire the entrant or out-innovate them, effectively neutralizing the threat 8.

The Pathways of Disruptive Innovation

Disruptive innovation, conversely, describes a specific, gradual process by which a smaller company with fewer resources successfully challenges established incumbent businesses by entering a market with a product that is initially deemed inferior by mainstream standards 8910. Disruptive innovations introduce a completely new value proposition. They typically underperform established products in mainstream markets but offer other, previously unvalued benefits - they are generally simpler, more convenient, more accessible, and vastly less expensive 11815.

Christensen's refined theory identifies two distinct origins for disruptive innovations, both of which exploit areas of the market that incumbents rationally ignore 4724. The first is low-end disruption, which occurs when a disruptor targets overserved customers at the bottom of an existing market 37. These customers are frustrated by having to pay premium prices for complex features they do not utilize or value 414. The entrant uses a fundamentally lower-cost business model to offer a "good enough" product at a fraction of the price. Because the profit margins at the low end are inherently unattractive, incumbents rationally choose to flee upmarket toward their most demanding clients rather than fight a destructive price war, effectively abandoning the lower segment to the disruptor 313. The classic historical example of this is the steel mini-mill industry, which initially entered the market selling low-grade rebar - a product integrated steel mills were happy to abandon due to its abysmal margins 37.

The second origin is new-market disruption, wherein the disruptor creates a completely new market segment by targeting non-consumers 3716. These are individuals or organizations who historically lacked the financial resources, technical skill, or geographic access required to use the incumbent's complex product 43. Early personal computers were new-market disruptions relative to corporate mainframes; they were technologically inferior by every traditional metric, but they allowed individuals who previously had zero computing power to own a desktop device 3. Because the disruptor is competing against "non-consumption," the initial product only needs to be better than nothing at all 3.

Textual Breakdown: Mapping Product Performance vs. Customer Needs

At the heart of Christensen's framework is a defining visual heuristic - a two-dimensional chart mapping "Performance" on the vertical Y-axis against "Time" on the horizontal X-axis. This conceptual map visually encapsulates the relentless mechanics of the innovator's dilemma 17.

The Y-axis, labeled performance, represents whatever specific attributes mainstream customers historically value in a given industry. Depending on the sector, this could mean storage capacity in disk drives, resolution in digital photography, or fuel efficiency in automobiles 1727. Mapped across this space are two parallel customer trajectories with relatively shallow upward slopes. The upper trajectory represents the performance demanded by the most demanding, high-end customers, while the lower trajectory represents the needs of the least demanding, low-end customers 8. The shallow slope of these lines illustrates a crucial psychological and economic reality: the human ability to utilize and absorb performance improvements grows relatively slowly over time 1718.

Cutting aggressively across these shallow customer lines are much steeper lines representing technological progress. The fundamental physical law of the disruption model is that the pace of technological progress invariably outstrips the customer's ability to absorb those improvements 1718. When an incumbent's sustaining technology trajectory - a steep line starting high on the Y-axis - crosses above the upper customer trajectory, market overshoot occurs 1017. The incumbent is now providing complex, expensive attributes that even their best customers are increasingly unwilling to pay a premium for 17.

Simultaneously, the disruptor's technology trajectory begins below the lower customer line, operating in a space where the product is initially viewed as an unusable toy by the mainstream 2719. However, because the disruptor's trajectory is also steep, it eventually intersects the lower customer line, crossing the threshold to become "good enough" for the low-end market 518. Over time, driven by the relentless pursuit of higher margins, the disruptor improves its product, and its steep trajectory carries it into the mainstream, eventually intersecting the high-end customer line 5. At this nexus, disruption is complete. The disruptor now offers adequate performance for the mainstream but retains the lower costs, greater convenience, and higher accessibility honed during its initial incubation at the bottom of the market, effectively displacing the incumbent 51830.

The RPV Framework: Incumbent Structural Responses and Vulnerabilities

To understand why intelligent executives consistently allow disruption to occur, the operational mechanics must be viewed through Christensen's Resources, Processes, and Values (RPV) framework 42719. This framework explains that while large organizations appear robust, their internal architecture creates systemic rigidities 4.

An organization's resources - its cash, engineering talent, intellectual property, and physical assets - are highly flexible and can be directed toward almost any project 419. However, an organization's processes - the habitual, standardized ways in which employees work together to solve repeated tasks, such as product development, market research, and budgeting - become deeply entrenched over time 420. Even more rigid are an organization's values, which are the criteria by which management and employees prioritize investments and make daily decisions. In publicly traded incumbents, these values are almost entirely dictated by gross margin requirements and the sheer size of the revenue needed to sustain growth 4720.

When faced with a disruptive threat, an incumbent's values will immediately flag the new, low-margin opportunity as a highly inefficient use of capital 419. The market seems too small to move the needle on corporate earnings, and the margins are destructive to the company's financial profile. Consequently, middle management will rationally starve the disruptive project of resources 4. Even if visionary executive leadership forces a response, the organization's legacy processes will attempt to cram the disruptive model into the existing corporate structure 6. This integration inevitably neutralizes the disruption, transforming it into a sustaining innovation that carries the high overhead costs of the parent company, thereby destroying the low-cost advantage that made the disruption potent in the first place 6.

Therefore, Christensen's fundamental structural prescription for incumbents facing genuine disruption is to create a wholly independent, autonomous business unit 182122. This separate entity must have a distinct cost structure, unique profit formulas, and separate operational processes that allow it to be financially viable at the low margins dictated by the disruptive technology 1823. Operating entirely free from the parent company's legacy overhead, this unit can attack the low end of the market and eventually disrupt the parent company itself, ensuring the corporation survives the technological transition, even if its legacy business model does not 923.

Operational Mechanics: A Comparative Matrix

To operationalize the theory for modern strategic management, it is vital to contrast the structural and economic mechanics of sustaining versus disruptive innovations. The following matrix delineates how these innovations differ across key operational vectors.

| Operational Vector | Sustaining Innovation | Disruptive Innovation |

|---|---|---|

| Initial Performance Level | Superior to existing offerings; aggressively pushes the technological frontier. | Inferior on traditional metrics; initially considered a "toy" or inadequate by mainstream users. |

| Target Customer Segment | The most demanding, highest-paying mainstream or top-tier customers. | Overserved low-end customers, or "non-consumers" entirely outside the current market boundaries. |

| Value Proposition | Higher quality, greater functionality, and faster speeds. | "Good enough" core performance combined with unprecedented affordability, accessibility, or simplicity. |

| Profit Margin Trajectory | High initial margins that enable incumbents to fund extensive R&D and marketing. | Very low initial margins that rely on high volume or capital turnover; margins slowly expand as the product moves upmarket. |

| Incumbent's Economic Motivation | Highly motivated to win. The innovation defends core revenue and boosts overall profitability. | Motivated to flee or ignore. Responding would require cannibalizing high-margin sales to capture low-margin business. |

| Incumbent Structural Response | Easily integrated into the core business. Existing sales, engineering, and cultural processes are perfectly aligned. | Fails within the core business. To survive, the incumbent must establish an entirely autonomous, separate business unit with a distinct profit formula. |

| Displacement Mechanism | Direct, head-to-head technological warfare resulting in either incumbent victory or rapid acquisition of the entrant. | Asymmetrical "stealth" warfare. The entrant captures the bottom tier, forcing the incumbent to retreat upmarket until they run out of high-end niches. |

The comparative matrix underscores the necessity of accurate classification. Misidentifying a sustaining threat as a disruptive one, or vice versa, leads to catastrophic capital misallocation. For example, if an incumbent treats a disruptive threat like a sustaining one, they will attempt to compete by adding more expensive features to their high-end products, fundamentally failing to address the low-cost vulnerability eroding their foundation 191319.

Explicitly Debunking Pervasive Misconceptions

The semantic dilution of "disruptive innovation" has resulted in a pervasive misunderstanding of how market transitions actually occur. Analysts, venture capitalists, and technology journalists frequently misapply the label to any company that shakes up an industry, fundamentally misguiding executive strategy and setting false expectations for investors 91017.

Misconception 1: "Disruption" is a Synonym for Success or Technological Superiority

The most common and dangerous fallacy is equating disruption with technological brilliance, rapid success, or sudden commercial dominance 78. Disruptive innovations are not breakthrough technologies that make good products better 7. In fact, the theory insists that true disruptive innovations are initially inferior when judged by the traditional metrics of the mainstream market 1735. They succeed not by out-engineering the incumbent on legacy metrics, but by changing the basis of competition entirely - competing on affordability, simplicity, or convenience 7815. Furthermore, disruption is a protracted, evolutionary process, not a fixed point in time. It often takes years or decades for a disruptive entrant to improve its product enough to cross the mainstream threshold, meaning incumbents frequently have ample early warning signs that they systematically choose to ignore 81021.

Misconception 2: Incumbents Fail Because They Are Badly Managed

Another persistent myth is that incumbents who fall victim to disruption do so because they are bloated, lazy, or led by incompetent management teams who fail to see the future. The tragic irony at the core of Christensen's thesis is that established firms fail precisely because they are excellently managed 4310. They fail because they accurately listen to their best customers, rigorously analyze market data, and systematically direct capital toward projects with the highest historical return on investment 46. By behaving entirely rationally and responsibly toward their shareholders, they blind themselves to the asymmetrical threat growing in the low-margin periphery 37.

The Ultimate Misconception: Christensen's Assessment of Uber

Perhaps no company highlights the public misunderstanding of the theory better than Uber. Throughout the 2010s, Uber was universally hailed by the financial press and the technology sector as the ultimate "disruptor" of the global taxi industry 2921. However, in a heavily debated 2015 Harvard Business Review article, Christensen, Michael Raynor, and Rory McDonald explicitly stated that Uber's financial and strategic achievements did not qualify the company as genuinely disruptive under the academic definition of the theory 821.

Christensen laid out two specific, structural reasons why the disruptive label did not fit Uber. First, Uber lacked a low-end or new-market foothold 82437. It did not start by targeting non-consumers or the low end of the market. Instead, it launched in San Francisco - a mature, well-served taxi market - and initially targeted affluent consumers who were already in the habit of hiring rides 824. Its initial product, Uber Black, was a premium black-car service, not a stripped-down, low-cost alternative. Second, Uber experienced immediate mainstream adoption based on absolute superiority 1724. Disruptive innovations are supposed to be initially inferior and ignored by the mainstream until their quality catches up. Uber, however, was fundamentally better than traditional taxis from the moment of its launch, offering seamless mobile booking, driver rating systems, and frictionless cashless payment 1724.

Because Uber tackled incumbents head-on with a vastly superior product and business model, Christensen classified it as a sustaining innovation 32737. The fact that Uber devastated the legacy taxi industry does not alter its theoretical classification; sustaining innovations can be highly destructive to incumbents if the incumbents lack the structural, regulatory, or technological flexibility to adopt the new standard. Accurately classifying Uber as a sustaining innovation demonstrates that not every transformative corporate success story requires a disruptive playbook 1017.

Deepening the Scholarly Debate: Critiques, Rebuttals, and Predictive Validity

While immensely popular among corporate practitioners, disruptive innovation theory has faced rigorous academic scrutiny regarding its historical accuracy, methodological rigor, and ex-ante predictive validity 103525. The debate highlights the tension between grand management theories and granular historical reality.

Jill Lepore and "The Disruption Machine"

In a highly publicized and combative 2014 essay in The New Yorker titled "The Disruption Machine," Harvard historian Jill Lepore launched a scathing, multi-faceted critique of Christensen's theory 394041. Lepore argued that the theory was profoundly flawed, functioning less as a scientific framework and more as a secular religion for the technology sector 3525.

Lepore's primary critique centered on methodological cherry-picking and historical inaccuracy 3526. She criticized Christensen's reliance on hand-picked case studies, asserting that his historical cutoff points were arbitrary and designed to support his conclusions 53526. For example, she pointed out that several companies Christensen identified in 1997 as victims of disruption in the disk-drive and heavy excavation industries - such as Seagate Technology, U.S. Steel, and Bucyrus - had actually survived their respective technological transitions and remained dominant, highly profitable forces decades later 5. Furthermore, she cited Time Inc.'s failed Pathfinder web portal as an example where an incumbent's attempt to self-disrupt led to massive capital destruction, suggesting Christensen's prescriptions were highly risky 2.

Lepore also identified a severe logical circularity in the framework 235. She noted that the theory suffers from survivorship bias: if an established company fails, Christensen's adherents claim it is because it did not disrupt itself; if it succeeds, it has simply not failed yet. Conversely, if a disruptive startup fails, it is dismissed as part of the natural "epidemic failure" of innovation, but if it succeeds, it is retroactively crowned a brilliant disruptor 235. Culturally, Lepore viewed the modern obsession with disruption as a symptom of profound, post-2008 financial anxiety - an atavistic theory that stripped the Enlightenment idea of human progress of its moral aspirations, replacing it with a ruthless, terror-inducing paradigm of continuous corporate destruction 354027.

Academic Rebuttals and the Defense of Disruption

Lepore's critique triggered a massive academic and journalistic debate. Michael Raynor, Christensen's frequent co-author, published an exhaustive 5,800-word rebuttal that systematically dismantled Lepore's claims 240. Raynor pointed out a fundamental flaw in Lepore's scholarly approach: her "dismantling" of the theory was based almost exclusively on Christensen's first book from 1997, willfully ignoring the subsequent two decades of peer-reviewed refinement, including the 2003 publication of The Innovator's Solution, where the theory had explicitly addressed many of the anomalies she raised 40. Regarding historical accuracy, Raynor clarified that a single firm surviving a disruption does not invalidate the disruption of the broader industry model; U.S. Steel's ultimate survival through painful restructuring does not erase the reality that Nucor and the mini-mill technology permanently decimated the traditional integrated steel business model 2.

Economists and strategy scholars also weighed in on the theory's predictive validity. Economic theorist Josh Gans noted that while the theory's enthusiasts often overreach, it contains a profound "nugget of truth" regarding the specific mechanics of technologies that initially perform worse on standard metrics but possess a faster, compounding improvement trajectory 35. Lynne Kiesling, arguing from a Smithian-Austrian economic perspective, agreed with Lepore that identifying disruption often requires historical hindsight, but defended the theory's utility 35. Kiesling argued that Christensen's framework accurately captures the crucial difference between quantifiable risk (which can be managed through historical probability) and true Knightian uncertainty (which is inherent to the genesis of innovation and breaks historical relationships), making absolute prediction fundamentally impossible in any strategic model 35.

Quantitative Scrutiny: The King and Baatartogtokh Study

The most rigorous empirical test of the theory's predictive validity came from Andrew King and Balaji Baatartogtokh in a 2015 MIT Sloan Management Review paper 21025. To test the generalizability of the theory, they identified 79 historical experts and surveyed them regarding the 77 specific industry case studies cited by Christensen 1025. They attempted to validate the four core premises of the theory: that incumbents were improving along a sustaining trajectory, that this trajectory overshot customer needs, that entrants possessed a disruptive capability, and that incumbents were ultimately displaced 410.

Their findings were stark and highly critical. According to the assembled experts, only 9% of Christensen's case studies aligned perfectly with all four elements of the theory 102325. The underlying mechanics were frequently absent: in 31% of the cases, industry leaders were not actually on a trajectory of sustaining innovation, and in nearly 80% of the cases, the premise that sustaining innovation overshot mainstream customer needs did not hold 1025. Furthermore, in almost 40% of the cases, incumbent firms simply lacked the baseline capabilities to respond to the new threat (such as postal services trying to compete with email), meaning their failure was due to a lack of resources, not a paralyzing focus on high-margin customers 25. Finally, in 40% of the cases, incumbents were not actually displaced by the disruptive entrant 25. The study concluded that while disruptive innovation absolutely exists - and the 9% of matching cases prove it conclusively - the strict conditions required for its application are exceedingly rare, significantly limiting its broad predictive power 1025.

Broadening the Scope: Modern Digital Ecosystems, SaaS, and Platform Disruption (2023+)

As the global economy has transitioned from the hardware-centric eras of disk drives and integrated steel mills into the modern era of cloud computing, artificial intelligence, and platform economics, Christensen's theory requires significant translation to remain strategically applicable 2829. Recent developments highlight how digital architectures alter the physics of disruption.

Software-as-a-Service (SaaS) as Structural Disruption

The enterprise transition from traditional on-premise software to Software-as-a-Service (SaaS) provides a textbook modern example of disruption, but one that introduces entirely new operational and financial mechanics 12. Traditional software operated strictly on a "software as a product" model, requiring massive upfront capital expenditure (CapEx) for perpetual licenses, on-site hardware, networking infrastructure, and dedicated IT labor for maintenance and patching 12.

SaaS, enabled by the rise of cloud Infrastructure-as-a-Service (IaaS) providers, entered as a classic low-end disruption 12. Early SaaS platforms were functionally inferior to legacy on-premise systems; they lacked the deep, bespoke customization required by major enterprises. However, they offered an entirely new business model predicated on a multi-tenant architecture and pay-as-you-go, operational expenditure (OpEx) pricing 12. This removed the massive upfront barrier to entry, allowing SaaS providers to target mid-market companies and small businesses - entities that were effectively non-consumers of top-tier enterprise systems 12.

Furthermore, the operational mechanics of SaaS accelerated the disruption timeline. Multi-tenant architecture allowed vendors to monitor real-time usage and roll out incremental, continuous feature updates universally, bypassing the manual, risky upgrade cycles that plagued traditional software 12. Combined with the elasticity of the cloud - allowing systems to scale up during peak demand without hardware investment - SaaS providers experienced a rapid performance trajectory improvement. The sales cycle was also radically shortened through proof-of-concept (POC) pilots, reducing financial risk for buyers 12. Over time, this rapid innovation cycle allowed SaaS providers to sprint upmarket, ultimately displacing legacy on-premise deployments across Fortune 500 enterprises 12.

Platform Ecosystems and "Complementor" Disruption

Recent academic research (2023+) extends disruption theory beyond single firms, applying it to complex platform-based ecosystems 212930. In modern digital platforms - such as mobile app stores, social media networks, or gaming consoles - disruption often occurs not at the level of the end-user, but at the level of the complementor (the third-party developers and creators generating value for the platform) 30.

A comprehensive study examining 12 platform technologies in the U.S. video game console industry from 1993 to 2010 revealed a fascinating inversion of the traditional model 2930. When an incumbent platform owner introduces a highly advanced, next-generation architecture (which acts as a sustaining innovation to the end-user by offering better graphics and speed), it drastically steepens the learning curve and development costs for its complementors. This unintentionally disrupts the platform's own ecosystem 2930. The advanced capabilities create such high development challenges that complementors defect to rival, less technically challenging platforms 30. This research proves that in multi-sided digital ecosystems, ensuring that innovation does not overshoot the capabilities of the supply side is just as critical as managing the demand side 2930.

Generative AI: Disruptive Innovation or "Big Bang" Disruption?

The explosive rise of Generative AI (GenAI), specifically Large Language Models (LLMs) like ChatGPT and multimodal generators like Midjourney or Sora, has sparked intense debate regarding their classification within innovation frameworks 283148.

A 2025 academic analysis positions GenAI firmly as a classic disruptive innovation within the knowledge work and marketing sectors 31. The technology initially underperformed human experts in nuance, reasoning, and accuracy (frequently suffering from "hallucinations"). However, it offered extreme affordability, accessibility, and speed 2831. By democratizing content creation and data analysis, GenAI provided a "good enough" solution for small businesses and individuals previously priced out of high-end agency work or specialized consulting, establishing a massive new-market foothold before rapidly moving upmarket as the neural network capabilities improved 2831.

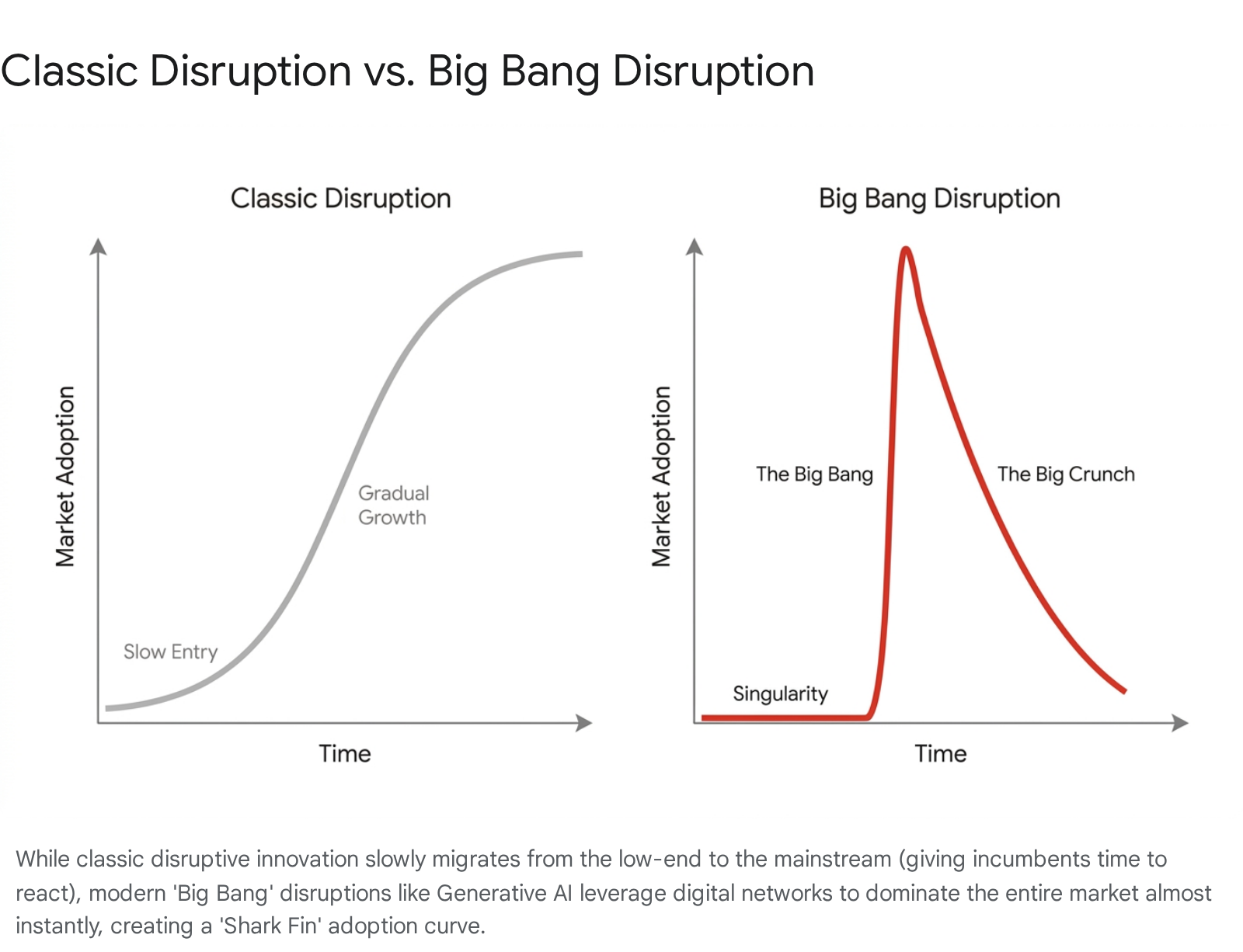

However, prominent strategy scholars like Larry Downes argue that GenAI represents an entirely different paradigm that breaks Christensen's model: the Big Bang Disruption 154849. Unlike Christensen's classic model - where an entrant slowly creeps upmarket over years or decades, giving incumbents time to notice the threat and flee to higher-margin niches - Big Bang Disruptions leverage exponential technologies (such as Moore's Law, ubiquitous cloud compute, and global broadband) to enter the market simultaneously better, cheaper, and more customized from the exact moment of launch 154932.

In a Big Bang Disruption, the technology is unencumbered by legacy assets and rapidly achieves a "singularity" point where adoption is nearly instantaneous 1549. The traditional adoption curve is replaced by a "Shark Fin" adoption curve, characterized by unprecedented, vertical market penetration 49. The traditional incumbent response - fleeing upmarket to higher-margin customers - is rendered impossible because the new technology wipes out the low end, middle market, and high end simultaneously, collapsing the old market order in a devastating "Big Crunch" 15. The rapid, global mainstream adoption of ChatGPT supports the argument that modern digital ecosystems compress the timeframe of disruption so severely that traditional defensive strategies, such as setting up autonomous business units, are simply too slow to execute 284832. Generative AI acts as an "uber-disruptor," breaking the rules of innovation across every industry concurrently 48.

Geographic Intersections: Frugal Innovation and Low-End Disruptions in Emerging Economies

Applying Christensen's theories strictly through a Western, Silicon Valley-centric lens overlooks the most fertile ground for low-end market disruptions today: the rapidly expanding emerging economies of the Global South, particularly India and China 113334. In these markets, disruption intersects deeply with the concept of frugal innovation 115335.

India: Frugal Innovation as Systems Disruption

Frugal innovation (often culturally contextualized as Jugaad in India) is not merely about stripping features to make cheap products; it is a profound, systemic re-engineering of the business model to achieve "more with less, for more" 113353. It specifically targets the massive "Bottom of the Pyramid" (BOP) demographic, which presents extreme institutional voids, severely low purchasing power, and vast infrastructure constraints 1133. Traditional Western innovation models, which prioritize technological sophistication and high-end features, are entirely ill-suited for this environment 1133.

The application of frugal business models is starkly illustrated by organizations such as the Aravind Eye Care System (AECS), which revolutionized ophthalmic surgery by applying assembly-line efficiency to cataract operations 1136. This process reduced costs by a staggering margin, making life-altering surgery accessible to marginalized communities while remaining financially sustainable 1136. Similarly, SELCO India applied frugal distribution and financing mechanisms to deliver off-grid solar solutions, while the GE MAC 400 represented an ultra-low-cost, battery-operated ECG machine developed exclusively for rural Indian clinics 1137. These frugal solutions often result in "reverse innovation," where hyper-efficient, low-cost products developed for severe constraints in the developing world eventually move upmarket and disrupt mature, bloated healthcare and consumer markets in the West 3637.

This frugal mindset is currently dictating India's strategic approach to Artificial Intelligence. While the US and China focus on a capital-intensive, sustaining innovation race to build massive frontier LLMs, India is pioneering the Frugal AI Stack 573839. Rather than competing on sheer parameter size and exascale compute, India's national AI Mission - backed by a targeted $230 million budget and 14,000 GPUs - prioritizes practical, accessible solutions 38. Indian startups like Sarvam AI are building highly efficient, localized, multilingual models designed to run on low-bandwidth edge devices, utilizing optimization techniques like quantization, pruning, and knowledge distillation to reduce training and deployment costs by up to 90% 573940. By focusing on outcome-linked scaling, shared compute pools, and seamless integration with India's Digital Public Infrastructure (DPI), India is establishing a formidable, low-end disruptive foothold in global AI 573839. This strategy prioritizes socio-economic utility and population-scale inclusion over raw, expensive performance, creating AI products that respect low willingness to pay and unforgiving hardware constraints 394162.

China: Re-architecting the Global Automotive Landscape

China's current dominance in the electric vehicle (EV) and clean-tech sectors offers perhaps the most dramatic, globally impactful contemporary execution of Christensen's low-end disruption theory 346342.

For over a decade, Western automakers viewed the transition to EVs strictly through a sustaining innovation lens. They entered the market at the extreme high end - exemplified by Tesla's Roadster and Model S, which were priced at massive premiums (frequently exceeding $100,000) to target affluent, early adopters 3. This market entry prompted legacy Western incumbents like Porsche and Mercedes to respond defensively with their own high-end luxury EVs, triggering a fierce, capital-intensive battle over the highest margin tier of the market 3.

Chinese manufacturers, led by entities like BYD, took the disruptive path 363. They targeted the domestic mass market - the extreme low end - which Western automakers had largely ignored due to poor margins. BYD introduced highly affordable, "good enough" electric vehicles optimized for short-range urban commuting, priced between $10,000 and $15,000 3. True to the behavioral predictions of Christensen's theory, Western incumbents (such as Ford and GM) responded to the low margins of the small-car segment by willingly abandoning it 3. They ceded the mass market to the Chinese, fleeing upmarket to focus their engineering and capital almost exclusively on highly profitable, large internal combustion engine (ICE) trucks and luxury SUVs 3.

However, by securing absolute dominance at the bottom of the market, Chinese automakers achieved immense economies of scale and aggressively vertically integrated their supply chains, particularly in critical battery manufacturing 334. This allowed for rapid technological improvement. Innovations such as CATL's "Chocolate Battery Swap" modular architecture - which drastically lowers R&D costs while building a shared ecosystem - and advancements in solid-state batteries are rapidly pushing Chinese EVs upmarket in performance and range 63. Aided by government policies like the Dual Credit Policy and propelled by the energy shock of recent global conflicts that increased the cost of fossil fuels, Chinese clean-tech exports have surged globally 426566. Today, Chinese manufacturers are not only dominating their massive domestic market but are exporting aggressively into Europe and emerging economies, capturing global market share and fundamentally threatening the survival of Western incumbents who have finally run out of high-end niches to retreat into 33465.

Conclusion

Clayton Christensen's theory of disruptive innovation remains one of the most powerful diagnostic frameworks in the history of strategic management, fundamentally altering how organizations perceive competitive threats 1418. By identifying the paradox that an incumbent's greatest strengths - relentless focus on core customers, stringent margin requirements, and disciplined resource allocation - are precisely the mechanisms that trigger their downfall, the theory provides indispensable foresight for corporate survival 44.

However, as scholarly critiques from Lepore, King, and others correctly highlight, disruption is not a universal law of commercial physics 103525. It is a specific strategic trajectory with rigorous, often rare boundary conditions 425. Falsely labeling sustaining innovations - such as Uber - as disruptive leads executives to execute the wrong defensive maneuvers, often resulting in the disastrous dismantling of profitable core businesses in a panic when standard, aggressive competitive retaliation would suffice 817.

As the global economy evolves, the theory must be contextualized alongside it. In the era of SaaS, Generative AI, and digital platforms, technological trajectories are accelerating exponentially, blurring the lines between gradual low-end disruption and instantaneous "Big Bang" market collapse 151230. Concurrently, the rise of frugal AI in India and the staggering scale of China's EV disruption prove that the core economic mechanics of low-end market entry and relentless upmarket migration are more potent than ever, particularly when applied on a global, geopolitical scale 345339. To survive the coming decades, corporate leaders must look past the vernacular buzzword, rigorously utilizing the true mechanics of disruption theory to monitor their blind spots, embrace structural autonomy, and recognize the lethal, existential potential of the seemingly "inferior" competitor.