Stripe Profitability and Payment Infrastructure

Payment Volume Growth and Net Revenue Dynamics

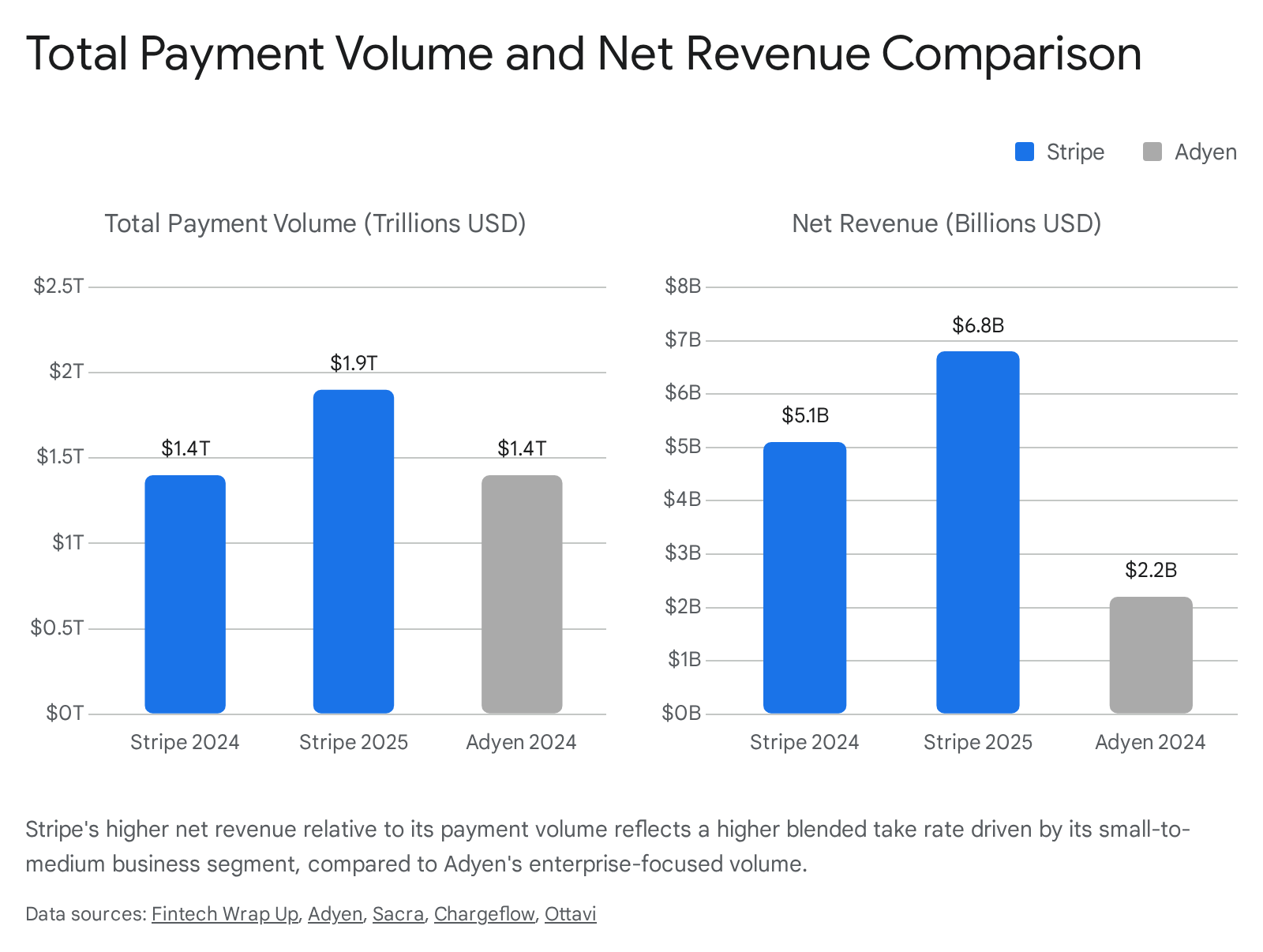

The financial trajectory of Stripe between the 2024 and 2025 fiscal years reflects a transition from high-velocity startup expansion to mature, profitable enterprise scale. In 2024, the total payment volume (TPV) processed across Stripe's global platform reached $1.4 trillion, representing a 38% year-over-year increase over the prior period 112. This volume scaled further by the end of 2025, growing an additional 34% to reach $1.9 trillion, a figure equivalent to approximately 1.6% of global gross domestic product (GDP) 434. This sustained volume expansion was accompanied by a structural shift from the cash-burn economics typical of venture-backed technology companies to durable profitability. Stripe returned to full-year profitability in 2024, posting a pre-tax profit of $101.9 million after a $1.2 billion pre-tax loss in 2023 4. The company maintained this profitability through 2025, with industry estimates suggesting the generation of $1.2 billion in earnings before interest, taxes, depreciation, and amortization (EBITDA) 4. While research inquiries frequently reference a $2.2 billion free cash flow figure for Stripe, current verified financial disclosures and analyst reports for the 2024 and 2025 fiscal years do not confirm this specific metric; the company has confirmed full-year profitability and robust cash flow positive status, but exact free cash flow numbers remain undisclosed as it operates as a private entity 1245.

A critical component of evaluating payment infrastructure economics is the analytical separation between gross merchandise value (GMV), gross revenue, and net revenue. Gross revenue represents the top-line fees collected from merchants, while net revenue is the capital retained after paying interchange fees, network assessments, and acquiring bank costs 86. In 2021, Stripe generated $12 billion in gross revenue and $2.5 billion in net revenue, implying a net take rate of roughly 39 basis points (bps) 36. By 2024, Stripe generated approximately $5.1 billion in net revenue, a 27.75% increase from the $4.0 billion generated in 2023 37. Estimates for 2025 indicate that Stripe generated $19.4 billion in gross revenue and between $5.84 billion and $6.8 billion in net revenue 43711.

The gross-to-net conversion reveals Stripe's blended take rate across its diverse merchant base. Historically, standard small-to-medium business (SMB) pricing is fixed at 2.9% plus $0.30 per online card transaction in the United States, with international cards incurring an additional 1.5% fee and currency conversion adding a 1% markup 12138. However, enterprise clients - which account for an estimated 50% to 60% of Stripe's total volume - negotiate significantly lower custom rates, sometimes approaching 2.2% plus $0.30 or shifting to interchange-plus pricing models 1112. As a result, Stripe's blended net take rate across all transactions is estimated at 35 to 39 basis points 611. For pure enterprise volume, the net take rate drops to approximately 16 to 20 basis points, heavily mirroring the economics of traditional enterprise acquirers 11.

The validation of Stripe's business model was further evidenced by its secondary market valuations. Following a period of macroeconomic contraction that saw Stripe's valuation fall from a peak of $95 billion in 2021 to $50 billion in early 2023, the company executed a tender offer in February 2025 valuing it at $91.5 billion 445. Exactly one year later, in February 2026, Stripe executed another tender offer that valued the company at $159 billion, representing a 74% year-over-year increase 471115. This valuation established the widest premium the company has ever held over public market competitors, valuing Stripe at approximately 17.9 times its 2024 net revenue 411.

The Revenue and Finance Automation Suite

While core payment processing remains Stripe's primary revenue driver - accounting for an estimated 80% to 85% of total revenue - it is inherently a commodity service characterized by intense competition and low gross margins 9. Payment processing gross margins typically range from 25% to 35% after accounting for interchange fees, network assessments, and operational expenditures 9. To drive operating leverage and secure a premium valuation multiple, Stripe has systematically expanded its Revenue and Finance Automation (RFA) suite, transitioning its economic profile from a transactional processor to a high-margin software-as-a-service (SaaS) ecosystem.

The RFA suite integrates Stripe Billing, Stripe Tax, Stripe Revenue Recognition, Stripe Sigma, and Stripe Data Pipeline into a cohesive financial back-office platform 101112. Because these software products require minimal variable costs per incremental transaction, their gross margins mirror traditional SaaS models, frequently exceeding 70% to 80% 912. In early 2025, the RFA suite passed a $500 million annualized revenue run rate, driven primarily by Stripe Billing, which manages nearly 200 million active subscriptions across more than 300,000 companies 14. Industry analysts project the suite will reach a $1 billion annual run rate by the end of 2026 43.

Billing and Subscription Economics

The monetization mechanics of these ancillary products rely on usage-based and transactional cross-selling. Standard payment processing incurs a base fee, but the utilization of RFA tools introduces incremental take rates 9. For example, Stripe Billing charges 0.5% of recurring revenue processed, capped at $1 million in billing volume (a maximum of $5,000 per month) 1313. For businesses operating on discrete invoicing rather than recurring subscriptions, one-off invoice payments incur a 0.4% fee on top of standard payment processing costs 1313. These fees are augmented by the planned acquisition of Metronome in late 2025, which further strengthens Stripe Billing's usage-based and consumption-pricing capabilities specifically tailored for software and AI-native businesses 7.

Tax and Compliance Automation

Stripe Tax automates the calculation, collection, and reporting of sales tax, value-added tax (VAT), and goods and services tax (GST) across dozens of international jurisdictions 1014. Stripe Tax operates on a pay-as-you-go model. For merchants utilizing the no-code integration with Stripe Checkout or Payment Links, the pricing is 0.5% of the total transaction volume in jurisdictions where the merchant is actively registered to collect tax 1516. Alternatively, merchants leveraging the discrete Stripe Tax application programming interface (API) for custom checkouts or multi-processor environments pay $0.50 per transaction call and $0.05 per calculation call, with ten free calculation calls included per transaction 1516. Registration services outside the United States, facilitated by partners like Taxually, incur additional regional fees, such as $500 for the Union One-Stop Shop (OSS) in Europe or $4,800 for registration in Japan 1516.

Radar and Fraud Mitigation

Risk mitigation tools introduce another layer of software revenue. Stripe Radar utilizes machine learning models retrained continuously across the entire Stripe network to identify and block fraudulent authorizations 1718. While basic Radar protection is included for all merchants, the advanced "Radar for Fraud Teams" product charges an additional $0.05 to $0.07 per screened transaction 121319. The economic value proposition for merchants justifies the cost; over the past two years, Radar models have reduced card testing by 80% and helped major enterprises capture substantial revenue 2. For example, car-sharing marketplace Turo recaptured an estimated $114 million in annual revenue through checkout optimization, while Forbes realized a 23% revenue uplift managing subscriptions via Stripe 117.

By stacking these software fees on top of core processing rates, Stripe effectively increases its net revenue per customer while simultaneously establishing high switching costs. A merchant utilizing Stripe for processing, billing, tax calculation, and fraud prevention is structurally integrated into the platform, lowering involuntary churn and increasing customer lifetime value 92021.

| Product Component | Core Functionality | Pricing Structure | Gross Margin Profile |

|---|---|---|---|

| Core Payments | Online and in-person transaction authorization and settlement. | 2.9% + $0.30 (Standard); Custom Interchange-Plus (Enterprise). | Low (25% - 35%) due to pass-through interchange and network fees. |

| Stripe Billing | Subscription management, metered billing, and invoicing. | 0.5% of recurring revenue; 0.4% per invoice payment. | High (SaaS standard, 70%+) |

| Stripe Tax | Automated tax calculation, collection, and obligation monitoring. | 0.5% per transaction (No-code); $0.50 per transaction (API). | High (SaaS standard, 70%+) |

| Stripe Radar | Machine learning fraud prevention and dispute management. | $0.05 per screened transaction for advanced fraud teams. | High (SaaS standard, 70%+) |

Operating Leverage and Incumbent Benchmarking

The competitive dynamics of global payment infrastructure are sharply illuminated when comparing Stripe's operational model to that of Adyen, its primary European competitor. Adyen operates exclusively as an enterprise-focused payment processor and acquirer, targeting multinational corporations with complex, high-volume, omnichannel needs 22. Because Adyen foregoes the fragmented SMB market and software platform aggregation, its payment volume closely rivals Stripe's, but its overall revenue and headcount structures differ entirely.

Adyen Enterprise Efficiency Comparison

In 2024, Adyen processed €1.29 trillion (approximately $1.4 trillion USD) in total payment volume, representing a 33% year-over-year increase 1303123. The company generated €1.99 billion in net revenue during this period 123. Crucially, Adyen maintains exceptional operating leverage, consistently achieving an EBITDA margin of 50% to 53%, with absolute EBITDA reaching €992.3 million in 2024 and pre-tax net income reaching €925.2 million 123.

This profitability is driven by an extraordinarily lean headcount and a unified, single-platform architecture. As of late 2024 and through 2025, Adyen operated with approximately 4,354 to 4,771 employees, generating an estimated €498,085 in revenue and €222,705 in profit per employee 243425. The vast majority of Adyen's engineering workforce is concentrated in its Amsterdam headquarters (approximately 1,230 employees), fostering a product-centric operating model without the overhead of decentralized legacy systems 36. Furthermore, Adyen's revenue is heavily weighted toward the Europe, Middle East, and Africa (EMEA) region, which contributed 58% of revenues in the second half of 2024, followed by North America at 27% 26.

In contrast, Stripe's pursuit of a comprehensive financial infrastructure platform - spanning SMBs, startups, enterprise clients, and independent software vendors - requires a substantially larger workforce. Following a 14% workforce reduction in 2022 and an additional targeted reduction of roughly 300 employees in early 2025, Stripe's headcount rebounded to approximately 8,140 to 8,500 employees by late 2025 4273940. The company stated internal targets to reach 10,000 employees by the end of 2025 to support its expanding product suite 3940. Stripe's engineering organization alone comprises over 3,378 employees, representing more than two-fifths of the total headcount 41.

While Adyen maximizes efficiency by focusing purely on high-volume, low-take-rate enterprise clearing (averaging 16.2 basis points) 11128, Stripe leverages high growth across an expansive product surface area. Stripe accepts higher initial operational expenditures to build adjacent software products, banking on the long-term compounding effects of the RFA suite to drive eventual software margins 1122. In essence, Adyen balances rapid growth with immediate cash-flow efficiency, whereas Stripe prioritizes capturing the maximum possible surface area of the internet economy.

| Metric (Fiscal 2024) | Stripe | Adyen | PayPal |

|---|---|---|---|

| Total Payment Volume | $1.4 Trillion | €1.29 Trillion (~$1.4T USD) | $1.7 Trillion |

| Volume YoY Growth | 38% | 33% | 10% |

| Net Revenue | ~$5.1 Billion | €1.99 Billion (~$2.2B USD) | $31.8 Billion |

| Employee Headcount | ~8,500 | ~4,354 | N/A (Broad Consumer/Merchant base) |

| Operating Margin / EBITDA | Profitable (Margin undisclosed) | 50% EBITDA Margin | 16.7% Operating Margin |

PayPal and Braintree Strategic Shift

As modern infrastructure providers like Stripe and Adyen capture global market share, legacy incumbents such as PayPal - and specifically its unbranded enterprise checkout solution, Braintree - have been forced to pivot their strategic focus. Acquired by PayPal in 2013, Braintree historically competed by offering highly aggressive, lower-priced processing rates to build a customer base of large multinational enterprises, including Uber and Spotify 29. This strategy effectively captured volume but suppressed profitability, resulting in a product line that was significantly less profitable than PayPal's branded consumer payment solutions 29.

By late 2024 and through 2025, under the leadership of CEO Alex Chriss and CFO Jamie Miller, PayPal enacted a strategic shift prioritizing profitable margin growth over pure payment volume 2930. During 2024, PayPal's unbranded processing segment (primarily Braintree) processed $572 billion in TPV 45. However, the company intentionally accepted slower volume growth in exchange for renegotiating contracts with its largest merchants to extract a healthier transaction margin profile 2930. PayPal's total payment volume reached $1.7 trillion for the full year 2024, growing 10%, but the unbranded segment's volume growth slowed and was projected to continue declining into late 2025 as the company reset its baseline 293031.

Instead of competing in a race to the bottom on commoditized processing rates, PayPal's new strategy requires enterprise merchants to adopt higher-margin risk services and payment orchestration layers 29. This indicates a broader market realization that unbranded enterprise payment processing cannot be sustained purely on volume; incumbent processors must attach value-added software services to defend margins against the technological moats built by agile competitors.

Regional Infrastructure and Licensing Dynamics

The global expansion of payment infrastructure requires navigating highly localized regulatory frameworks and banking systems. In the Asia-Pacific (APAC) region and broader emerging markets, Australian-founded fintech Airwallex has emerged as a formidable competitor to Stripe by prioritizing deep regulatory integration and local funds holding capabilities over pure payment gateway functionality 154748.

Airwallex, valued at $8 billion, generates approximately $1.3 billion in annualized revenue and processes nearly $300 billion in volume 154832. The company distinguishes itself through the aggressive acquisition of localized financial licenses. As of early 2026, Airwallex held approximately 90 regulatory licenses across 50 markets - a figure its CEO noted is roughly double that of Stripe 154832.

Japan and the Funds Transfer Service Provider License

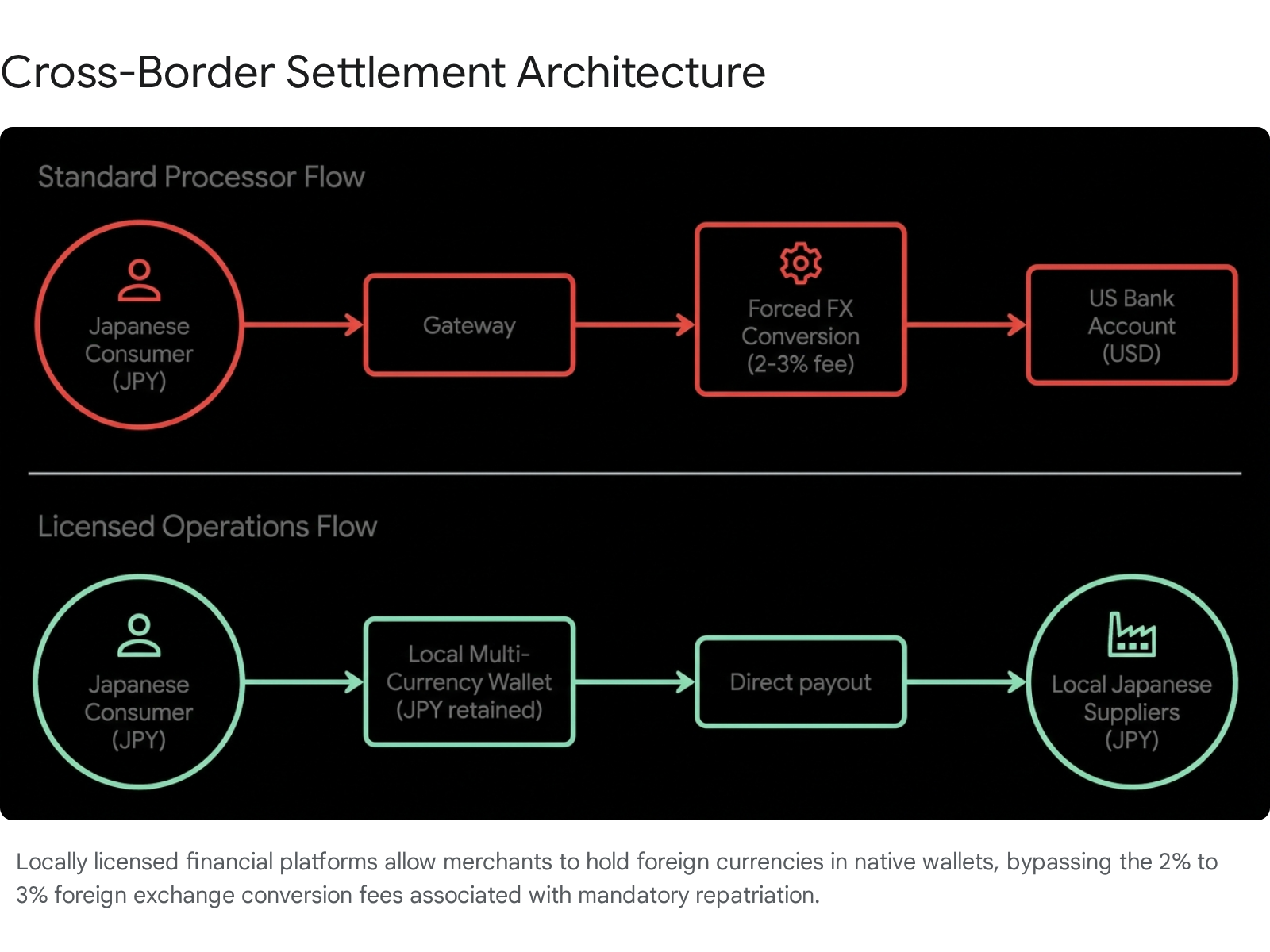

The economic advantage of this licensing strategy is most visible in complex regulatory environments like Japan. Under Japan's Payment Services Act (PSA), amended in 2021 and 2023 to facilitate cashless payments and regulate stablecoins, money transfer services are tightly controlled 3334. It took Airwallex seven years to obtain a formal funds transfer service provider license in Japan 1533. This specific regulatory classification yields a massive operational advantage. When legacy gateway providers or processors like Stripe and Square process a payment in Japan, regulatory constraints typically obligate them to immediately remit those funds directly to the merchant's external bank account 154832. If a US-based merchant sells to a Japanese consumer, this immediate repatriation forces a cross-border currency conversion, subjecting the merchant to hidden foreign exchange (FX) fees and conversion markups often totaling 2% to 3% 121552.

Because Airwallex possesses the necessary local licensing, it can legally hold customer funds within its own ecosystem without immediate external settlement 1532. This enables "like-for-like" settlement across 14 major currencies 5253. A US merchant can collect Japanese Yen, hold the Yen in a local Airwallex multi-currency wallet, and deploy those same funds to pay regional suppliers, payroll, or digital marketing expenses without ever converting the currency at interbank rates 155253.

This infrastructure design circumvents the traditional correspondent banking network, directly attacking the cross-border FX revenue that legacy processors rely on to pad their margins. Meanwhile, Stripe continues to optimize its Japanese market presence by integrating local alternative payment methods, notably enabling PayPay integration - a QR-code based system with over 68 million active users - and accelerating payout speeds to four business days 3536.

Latin American Market Fragmentation

The challenge of global payment routing is further exacerbated in Latin America, where digital commerce is projected to exceed $900 billion by 2026, with payments revenue expected to triple to $300 billion by 2027 37. Unlike the credit card-dominated ecosystems of North America and Europe, Latin America operates on highly fragmented alternative payment methods (APMs) and distinct sovereign currencies. Consumer preferences heavily favor these local options, with approximately 70% of Latin American consumers preferring local payment methods at checkout 3738. APMs, including digital wallets and real-time bank transfers, are expected to surpass traditional card volumes in key markets by 2026 38.

For example, Brazil's real-time payment system, Pix, has achieved unprecedented adoption and is forecasted to exceed credit cards in e-commerce usage 3738. Similarly, cash-voucher systems like OXXO in Mexico and bank-transfer systems like PSE in Colombia remain essential for consumer conversion 39.

While Stripe has expanded into Latin America, its structural model often poses hurdles for regional founders. Merchants building SaaS or digital products frequently rely on Stripe Atlas to incorporate a US C-Corporation, allowing them to access the US banking system and collect global payments in US dollars 3959. While highly efficient for business-to-business (B2B) or global software companies, this architecture creates severe friction for business-to-consumer (B2C) operations selling domestic physical goods or digital services to unbanked Latin American consumers who rely strictly on local APMs 3959.

This fragmentation has enabled regional specialists like dLocal and EBANX to command significant market share. dLocal offers a merchant-of-record model with a single API integration that processes pay-ins and payouts across multiple Latin American countries, Africa, and Asia 3960. This allows multinational enterprises to accept hyper-local payment methods without the regulatory burden of establishing local corporate entities in every jurisdiction 39. However, regional sentiment data indicates that while cross-border coverage is extensive, merchants frequently face operational challenges. Specifically, low Trustpilot scores and merchant reviews cite support unresponsiveness, opaque foreign exchange spread negotiations, fee stacking, and payout delays during edge-case chargeback disputes 395960.

| Infrastructure Provider | Primary Strategic Focus | Key Market Differentiator | Regional Strength |

|---|---|---|---|

| Stripe | Developer-first API, deep SaaS automation (RFA), and US/EU entity aggregation. | Market-leading checkout optimization and AI integration. | North America, Europe |

| Airwallex | Global financial operations, B2B treasury, and FX fee avoidance. | Deep portfolio of local banking licenses for like-for-like holding. | APAC, Emerging Markets |

| dLocal | Cross-border merchant of record for complex, highly regulated geographies. | Single API access to hundreds of fragmented APMs (Pix, OXXO). | Latin America, Africa |

A parallel disruption in cross-border infrastructure is occurring through stablecoin adoption. Traditional remittance inflows to Latin America, which reached $142 billion in 2025, incur average fees of 6.2% 37. Stablecoin transfers on efficient blockchain networks reduce this cost to between 0.5% and 1.5%, saving users up to 76% in fees 37. Stripe recognized this architectural shift, resulting in its acquisition of stablecoin orchestration platform Bridge in late 2024 and the rollout of crypto-native issuing protocols 45. By 2025, stablecoin payment volume on Stripe's network doubled to approximately $400 billion, with roughly 60% driven by B2B transactions, positioning the company to capture the projected $25.5 billion to $31.2 billion stablecoin remittance market in Latin America by 2026 437.

Artificial Intelligence Economics and Agentic Commerce

The most profound shift in the payment infrastructure landscape is the macroeconomic impact of artificial intelligence (AI). Stripe has positioned itself as the underlying financial engine for the generative AI boom, processing payments for 78% of the Forbes AI 50 cohort, including prominent developers such as OpenAI, Anthropic, Mistral, and Midjourney 15740.

AI Startup Growth and Compute Cost Pressures

The unit economics of AI companies differ drastically from traditional SaaS platforms. Due to immense initial compute costs for model inference and training, AI businesses operate under extreme pressure to monetize quickly rather than deferring profitability for user acquisition 40. This fundamentally alters billing architecture, forcing a shift away from flat monthly subscription seats toward complex, usage-based, and metered billing models (e.g., billing per token or API call) 1040.

Data collected by Stripe indicates that AI-native startups are growing significantly faster than their SaaS predecessors. On average, high-growth AI startups reach $1 million in annualized revenue in a median of 11 months - four months faster than the 2018 cohort of traditional SaaS companies - and scale from $1 million to $30 million five times faster 40. In 2025 alone, the number of companies reaching $10 million in annual recurring revenue within three months of launch doubled compared to the previous year 11.

Trial Abuse and Chargeback Risks

However, this rapid growth brings elevated operational risk regarding trial abuse and customer churn. Because free trial users in an AI application immediately consume expensive compute resources, fraudulent signups or coordinated bot attacks present a direct margin threat rather than just a marketing inefficiency 41. In response, payment processors must deploy advanced machine learning risk models. Stripe Radar evaluates signup telemetry to block risky authorizations in real time, preventing more than 3.3 million risky signups for eight high-growth AI businesses in a single month during 2026 241.

Additionally, the economics of AI micro-transactions are highly sensitive to fixed processing costs. For an AI feature that costs $0.03 in compute and is billed at $0.10, Stripe's standard fixed fee of $0.30 per transaction creates unsustainability 42. To combat this, merchants utilize credit packs or migrate to micro-payment infrastructures utilizing stablecoins, such as USDC on Base networks 42. Furthermore, Stripe instituted a $15 fee for merchants electing to counter disputes and chargebacks, heightening the financial risk for companies dealing with high volumes of involuntary churn or subscription forgetfulness, requiring sophisticated dunning management and revenue recovery tooling 43.

The shift of legacy SaaS vendors into the AI space also creates distinct legal and intellectual property challenges. When traditional software vendors embed AI, contracts must address the ownership of outputs generated by models trained on customer data, requiring updated representations and warranties regarding bias testing and compliance with frameworks like the NIST AI Risk Management Framework or ISO/IEC 42001 44.

Compliance and Liability in Autonomous Purchasing

Furthermore, the rise of "agentic commerce" - where autonomous AI software agents compare products, fill shopping carts, and execute payments on behalf of human users - presents unprecedented compliance and infrastructural challenges 445. McKinsey projections suggest global agentic commerce could reach $3 trillion to $5 trillion by 2030, with Gartner expecting 90% of B2B buying to be agent-mediated by 2028 67.

Existing payment regulations, such as the European Union's Second Payment Services Directive (PSD2) and its Strong Customer Authentication (SCA) mandate, are explicitly designed around verifying a human payer's identity through biometric or two-factor authentication 46. Furthermore, Anti-Money Laundering (AML) and Know Your Customer (KYC) obligations require verifying the purchaser's identity, which is procedurally complex when the buyer is software acting autonomously 67. When an AI agent autonomously executes a transaction, traditional concepts of contractual consent via click-wrap agreements fail because agents lack independent legal personality 47.

If an AI agent hallucinates or makes an incorrect purchase, the liability framework remains legally ambiguous 456746. Because no explicit agentic commerce legislation exists as of mid-2026, liability defaults to private enterprise contracts and merchant terms of service 67. To manage this, a fragmented ecosystem of authorization protocols has emerged across a four-layer stack encompassing Discovery, Checkout, Authorization, and Settlement 67.

| Payment Stack Layer | Functionality in Agentic Commerce | Leading Protocols |

|---|---|---|

| Discovery | Agent finds products and reads machine-readable documentation. | MCP (Model Context Protocol) |

| Checkout | Agent assembles and submits a shopping cart. | ACP (OpenAI / Stripe), UCP (Google) |

| Authorization | Cryptographic proof that a human approved the specific spend limit. | AP2 (Google), Visa TAP, Mastercard Agent Pay |

| Settlement | Final movement of fiat or stablecoin capital. | Traditional Cards, x402 (Stablecoins), MPP (Stripe) |

Solutions like Google's Agent Payments Protocol (AP2) and Visa's Trusted Agent Protocol (TAP) utilize cryptographically signed mandates to prove that a human explicitly delegated spending authority to an agent 67. Concurrently, Stripe and OpenAI have co-developed the Agentic Commerce Protocol (ACP) to securely route automated checkout flows, while Mastercard has introduced Agentic Tokens that bind card credentials to specific consent policies 467. The integration of these protocols will dictate which payment processors successfully navigate the regulatory ambiguity and capture the projected multitrillion-dollar agentic commerce market over the next decade.