What Is Plaid and Why Does Your Bank Use It

Plaid is a financial technology intermediary that securely connects your bank account to third-party applications like Venmo, Robinhood, and modern budgeting tools. By acting as a digital bridge, it allows these applications to verify your identity, check your balance, and facilitate payments without ever requiring them to store your actual banking password.

The Digital Plumbing of Modern Finance

To understand the necessity of Plaid, one must first look at the historical architecture of the consumer financial system. Before the rise of specialized data aggregators, the banking sector was built almost entirely for a physical, branch-based world. If a consumer wanted to initiate a wire transfer, apply for a personal loan, or verify their identity for a new financial service, the process often required a visit to a local bank branch, the physical mailing of voided checks, or the faxing of printed bank statements 1. As digital finance expanded rapidly in the early 2010s, a critical missing link became apparent to software developers. Connecting a modern, fast-moving application - such as a peer-to-peer payment platform or an automated savings tool - to the legacy, localized infrastructure of thousands of isolated banks was incredibly difficult, if not impossible 1.

Plaid was originally founded to build a consumer-facing budgeting application, but the founders quickly realized that the underlying data connection infrastructure they needed simply did not exist 1. They pivoted to solve this fundamental "chicken-and-egg" problem by building the necessary infrastructure themselves 12. Today, Plaid operates as the digital plumbing - or the proverbial "shovels and pans" of the fintech gold rush - facilitating communication across a highly fragmented ecosystem 14.

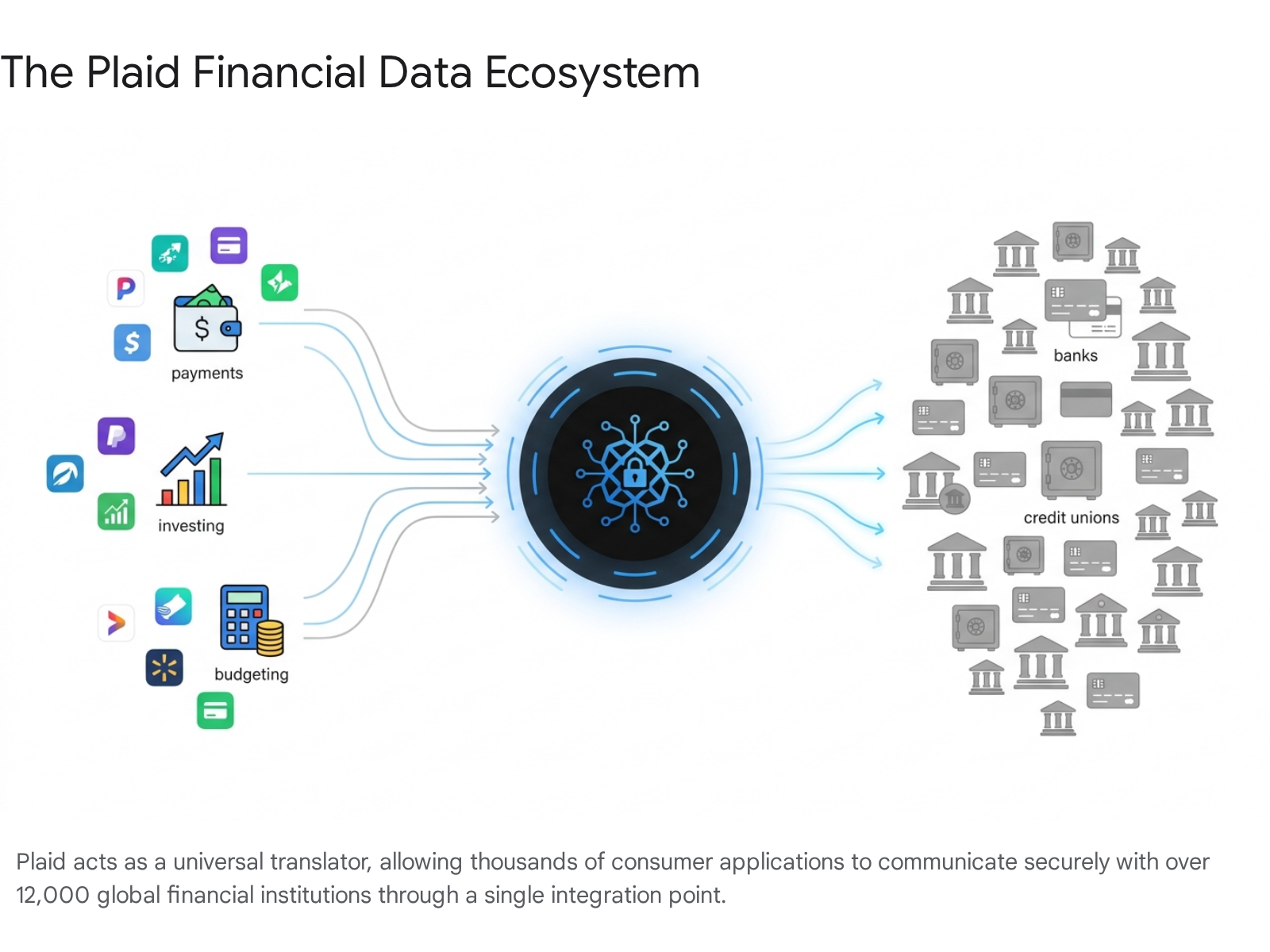

Instead of an application developer dedicating years to writing thousands of custom integrations to communicate individually with every major commercial bank, regional credit union, and digital wallet platform, the developer only needs to write a single integration to Plaid 52. Plaid then handles the complex routing, authentication, and data normalization across its massive network 45. As of the mid-2020s, this network spanned over 12,000 distinct financial institutions across the United States, Canada, the United Kingdom, and Europe 43.

The scale of this infrastructure is immense. By 2025, industry estimates indicated that at least half of all adults in the United States had interacted with Plaid's technology in some capacity, connecting over 500 million consumer accounts worldwide 445. The company's revenue reportedly rose more than 25% in 2024 alone as consumer demand for seamless digital financial experiences continued to outpace the capabilities of legacy banking interfaces 5.

Why Your Bank and Fintech Apps Use Plaid

When an individual downloads a new digital financial service and attempts to create an account, the application immediately faces a high-stakes challenge. It must verify that the user's bank account actually exists, confirm that the individual legally owns it, and ensure there are sufficient funds available to perform a transaction. Historically, achieving this involved the slow, friction-heavy process of micro-deposits, where an application would deposit two amounts of a few cents into the user's account and ask the user to verify the exact amounts days later 1. If the onboarding process takes days, modern consumers simply abandon the application.

Applications utilize Plaid because it offers a suite of Application Programming Interfaces (APIs) designed to instantly execute these verification tasks 526. An API is essentially a set of standardized rules and protocols that allows two different software programs to communicate and share data securely without exposing their underlying proprietary code to one another 26.

Core API Products and Functionality

Through this API layer, Plaid offers distinct products that power highly specific features within the financial applications we use daily. Rather than offering a single generic data feed, Plaid segments its network into specialized tools 511127.

The Auth and Balance products serve as the foundational layer for payments. When a user links an account, Auth instantly verifies the account and routing numbers to enable immediate Automated Clearing House (ACH) transfers, while Balance checks real-time funds availability to prevent costly overdrafts and failed payments 121415. For more complex financial management, the Transactions product retrieves up to 24 months of historically categorized transaction data across checking, credit, and student loan accounts. This data engine is what powers automated budgeting dashboards, allows apps to detect recurring subscription payments, and enables lenders to underwrite loans based on actual cash flow rather than relying solely on traditional credit scores 41112.

Plaid also heavily focuses on risk mitigation through its Identity and Signal products. Identity verifies the account holder's name, physical address, and email address against the bank's official records, helping applications comply with stringent Know Your Customer (KYC) regulations and prevent synthetic identity fraud 1216. Meanwhile, products like Signal and Monitor utilize machine learning across Plaid's massive network to assess the real-time risk of a transaction bouncing or to detect patterns of fraud before a transfer is finalized 7148.

Where Plaid Operates in the Ecosystem

The invisible, embedded nature of Plaid means consumers frequently use the service without realizing it. The technology powers the onboarding, funding, and data aggregation mechanisms for a vast array of the digital economy.

| Category | Typical Use Case | Example Applications Powered by Plaid |

|---|---|---|

| Payments & Wallets | Linking a primary checking account to instantly fund a digital wallet, split bills, or send peer-to-peer transfers. | Venmo, Cash App, PayPal, Wise, WorldRemit, Metal 15189 |

| Investing & Crypto | Verifying external funding sources to allow instant deposits for stock market trading or cryptocurrency purchases. | Robinhood, Coinbase, Kraken, Acorns, Wealthfront, M1 Finance 1518920 |

| Neobanks & Digital Banking | Funding a newly created digital-only bank account from an existing legacy, brick-and-mortar bank account. | Chime, Varo, Current, MoneyLion 1518920 |

| Lending & Cash Advances | Analyzing cash flow, verifying payroll income, and assessing transaction history to underwrite loans instantly. | SoFi, Earnin, Dave, Petal, Figure, Avant 718921 |

| Personal Finance | Aggregating checking, savings, and credit card data to provide a unified dashboard of an individual's net worth. | YNAB (You Need A Budget), Rocket Money, Copilot, Cleo 18922232410 |

For legacy financial institutions, cooperating with data aggregators like Plaid has shifted from a reluctant necessity to a strategic priority 5. Banks recognize that their customers demand the ability to use third-party fintech tools. By establishing secure, formal data-sharing agreements and dedicated APIs with Plaid, banks ensure their customers can access these modern tools without compromising the bank's own internal security infrastructure or overloading their servers with unauthorized access attempts 51112.

The Mechanics of a Plaid Connection

To understand why Plaid is widely considered a secure intermediary, it is necessary to examine the technical flow of how data is authorized and retrieved. A common and persistent misconception is that third-party applications - such as Venmo or Robinhood - hold and store the user's banking username and password directly. In a properly configured modern Plaid integration, this is fundamentally false 152829.

The connection layer is handled by a user-facing interface called Plaid Link. When a consumer opens an application and selects the option to add a funding source, the application initializes this Plaid-hosted module. For most fintech applications, this Link module is the very first touchpoint a user has with a bank connection, making its speed and reliability critical to the app's overall conversion rate 11.

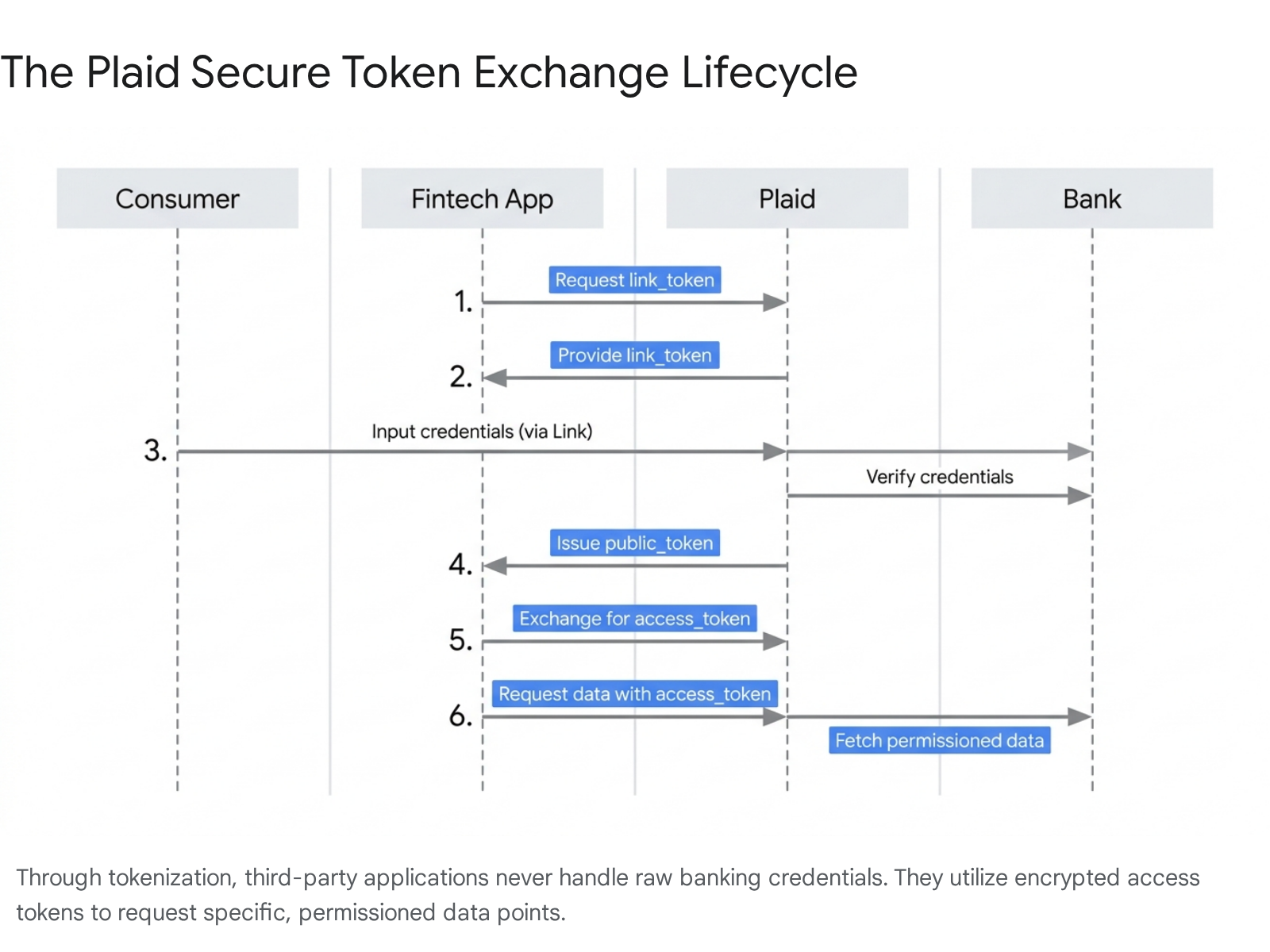

The Token Exchange Lifecycle

The data lifecycle follows a strict tokenization process designed to isolate credentials from the third-party developer. The flow begins when the application's backend server requests a temporary, single-use code called a link_token from Plaid 1613. The application passes this token to the user's mobile device or web browser to securely open the Plaid Link interface 13.

From this point forward, the consumer interacts entirely within the secure confines of Plaid Link. They search for their specific bank and are securely routed to an authentication screen. Depending on the technological maturity of the consumer's bank, this may involve logging in directly on the bank's secure portal (via a protocol called OAuth) or entering credentials securely into Plaid's encrypted system 1213. Plaid handles all necessary security hurdles, including sending and verifying Multi-Factor Authentication (MFA) codes via SMS or email 1216.

Once the consumer is successfully authenticated, Plaid Link generates a short-lived public_token and hands it back to the third-party application 1613. The application cannot use this public token to read any data. Instead, the application's backend server securely transmits this public_token back to Plaid's servers, exchanging it for a permanent access_token and an item_id, which represents the specific bank connection 1613.

The application securely stores this access_token in its database. Whenever the application needs to update a balance, fetch new transactions for a budgeting dashboard, or verify funds before a transfer, it sends a request containing the access_token to Plaid's API 21113. Plaid verifies the token, retrieves the specific requested data from the financial institution, and securely returns it to the application 211.

This tokenized architecture means the application developers never see, touch, or store the consumer's banking credentials. The application only holds an arbitrary string of characters that grants read-only permission for specific, explicitly authorized data types 21528.

The Evolution of Access: Screen Scraping to APIs

While the token exchange between Plaid and the third-party app is highly secure, the underlying method Plaid uses to connect to the actual bank has undergone a massive, industry-wide transformation. The ecosystem has spent the last several years shifting from a controversial, fragile legacy method known as "screen scraping" to a secure, industry-standard protocol known as OAuth 21214.

The Fragile Era of Screen Scraping

In its early days, before legacy banks offered dedicated data APIs to third parties, Plaid and other financial aggregators relied heavily on screen scraping 23233. Under this method, the consumer provides their banking username and password directly to the aggregator during the onboarding flow. The aggregator's software then securely stores these credentials and uses them to programmatically log into the bank's consumer-facing website 323334. Once logged in, the automated software simulates human behavior, "scraping" the HTML code of the webpage to read balances and extract transaction histories as if it were a human user looking at the screen 3234.

While screen scraping was an innovative bridge technology necessary to prove consumer demand for connected finance, it was fraught with systemic issues 233. Primarily, it required the aggregator to store the user's credentials - albeit in a highly encrypted state 3335. Furthermore, the connections were notoriously fragile. If a bank simply redesigned its website, altered its login button placement, or updated its password expiration policies, the screen scraping script would immediately break. This severed the connection, resulting in synchronization errors and forcing the user to manually re-authenticate their credentials 333435.

The Transition to OAuth and Direct APIs

As the fintech industry matured and transaction volumes skyrocketed, financial institutions and data aggregators collaborated to replace screen scraping with dedicated Application Programming Interfaces utilizing the OAuth (Open Authorization) 2.0 protocol 23415.

OAuth is a globally recognized, industry-standard authorization framework that allows users to grant third-party applications access to their information without ever sharing their underlying passwords 121516. When a consumer uses a Plaid-powered application that supports an OAuth connection, they are seamlessly redirected away from Plaid to their actual bank's website or mobile app to log in 323416. The bank verifies the user's identity, explicitly asks what specific data accounts they consent to share, and then issues a secure, revocable authorization token directly to Plaid 323416.

Comparing Technical Connection Methods

| Feature | Legacy Screen Scraping | Modern OAuth APIs |

|---|---|---|

| Credential Handling | The aggregator must collect and store the consumer's encrypted banking username and password 333435. | Credentials remain strictly with the bank; the aggregator only receives an authorization token 323435. |

| Security Risk Profile | Higher risk due to the centralized storage of login credentials by unauthorized third parties 333435. | Substantially lower risk; utilizes token-based authorization that can be instantly revoked 3235. |

| Connection Reliability | Highly fragile. Breaks if the bank updates its website UI, HTML structure, or changes password policies 3335. | Highly reliable. Built on stable, contractually maintained software endpoints designed for machine communication 3335. |

| Data Granularity | All-or-nothing access. The scraping bot sees everything the user would see on their screen 3435. | Granular access. The consumer can explicitly permission specific data sets (e.g., sharing a checking account, but hiding a mortgage) 3235. |

| Retrieval Performance | Slow. It can take 5 to 30 seconds as the software navigates through multiple web pages 35. | Fast. Direct data retrieval often occurs in roughly 500 milliseconds 35. |

By 2025, Plaid had successfully migrated the vast majority of its network traffic away from screen scraping and toward these API-driven integrations 212. To accelerate this transition across the long tail of smaller regional banks and credit unions, Plaid partnered with major identity management providers like Okta 121517. This partnership allowed financial institutions to adopt OAuth standards rapidly and securely, ensuring compliance with emerging industry standards mandated by consortiums like the Financial Data Exchange (FDX) 1517.

Security, Privacy, and the $58 Million Settlement

The sheer volume of sensitive financial data flowing through Plaid's network places the company under intense scrutiny regarding its security protocols and privacy practices.

From a purely technical standpoint, Plaid utilizes robust, bank-level security measures to protect data in transit and at rest. All data transmitted between the financial institution, Plaid's servers, and the end third-party application is encrypted using the Advanced Encryption Standard (AES-256) and Transport Layer Security (TLS) protocols 141528. Plaid's core infrastructure complies with strict industry certifications, including SOC 2 Type II and ISO 27001 14.

Furthermore, a pervasive myth surrounding aggregators like Plaid is that the company operates as a data broker, selling consumer transaction histories to third-party marketers for targeted advertising 2918. The company has explicitly and repeatedly stated, including in sworn statements by its executive team, that it does not and has never sold consumer data 1523. Plaid's core revenue model relies entirely on charging the application developers - such as Venmo or Robinhood - a transactional or subscription fee for utilizing the API infrastructure, rather than monetizing the underlying data itself 4.

The 2022 Class Action Privacy Lawsuit

Despite these technical safeguards, Plaid has faced significant legal challenges regarding its transparency, data minimization practices, and user interface design. In July 2022, a federal judge approved a $58 million class-action settlement stemming from consolidated litigation regarding Plaid's past privacy practices 18404142.

The consumers in the lawsuit alleged two primary grievances. First, they claimed that Plaid's older user interface was designed to mimic the login screens of individual banks so closely that users did not realize they were providing their credentials to a third-party aggregator rather than their own bank 184219. Plaintiffs argued this practice violated California's anti-phishing laws, which prohibit misrepresenting oneself to induce the handover of sensitive information 1842. Second, plaintiffs alleged that Plaid historically collected more transactional data than was strictly necessary for the specific application being used, exploiting its position as a middleman to aggregate vast amounts of transaction history without explicit consent 404219.

Outcomes and Interface Redesigns

While Plaid officially denied all allegations of wrongdoing and maintained that its practices were transparent, the court-approved settlement mandated sweeping changes to the company's business practices alongside the monetary payout 184019.

The $58 million fund distributed payments to affected users, covered $11 million in attorney fees, and directed unclaimed funds to privacy-focused organizations like Consumer Reports and the Privacy Rights Clearinghouse through cy pres awards 1819. More importantly, the injunctive relief required Plaid to permanently alter the Plaid Link interface to ensure total transparency. The redesign ensured users clearly understand Plaid's role as a middleman before they input any data 184041. Furthermore, the company was legally bound to minimize the data it collects moving forward and to delete vast troves of historical transactional data for users who had not actively connected accounts for specific transaction-based services 1819.

How to Manage and Revoke Your Plaid Data

A direct result of industry maturation and the 2022 privacy settlement is significantly enhanced consumer control over financial data. Historically, once a consumer linked a bank account to a budgeting application or payment tool, that connection persisted indefinitely - even if the consumer deleted the application from their smartphone 44. Plaid would continue to pull data in the background to ensure the application remained synced if the user ever returned.

Today, consumers have multiple, accessible avenues to audit, manage, and completely revoke third-party access to their financial data, ensuring they are no longer leaving a trail of active data connections across the internet.

Method 1: The Plaid Consumer Portal

In direct response to demands for greater transparency and as part of the settlement remediation, Plaid launched an official, consumer-facing dashboard located at my.plaid.com 23194420.

Consumers can navigate to this portal and create an account using the phone number and email address they typically associate with their financial applications 442046. Upon identity verification, the portal automatically queries Plaid's backend and presents a comprehensive list of every application that has ever accessed the user's financial institutions via Plaid's network 4446. Users can view exactly what types of data are currently being shared and can click "Disconnect" or "Remove" to sever the API link immediately 444621. This action instantly revokes Plaid's access, preventing any future data sharing or ACH transfer authorizations without needing to contact the third-party app directly 444621.

Furthermore, the portal allows users to execute their "Right to Delete," forcing the deletion of their historical financial data from Plaid's internal systems entirely, ensuring no residual data is stored beyond what is strictly required by anti-money laundering laws 23202249.

Method 2: Bank-Hosted Security Dashboards

As major financial institutions adopt modern OAuth APIs, they are increasingly offering centralized control panels within their own mobile banking apps and secure websites. This allows consumers to audit and sever third-party ties directly from the bank's side, providing a critical "belt-and-suspenders" approach to data security 1144.

| Financial Institution | How to Revoke Third-Party App Access |

|---|---|

| Chase Bank | Navigate to "Security & Privacy" and select "Linked apps and websites." This displays all active API connections, allowing users to uncheck specific accounts or revoke access entirely 2351. |

| Bank of America | Within the "Profile & Settings" menu, locate the "Security Center" and select "Manage Third-Party Access" to view and revoke active data-sharing consents 4424. |

| Wells Fargo | Access "Manage Connected Apps" under the security profile to monitor and revoke Plaid's authorization 51. |

| Citi | Navigate through Account Management settings to the linked accounts screen to revoke access on an app-by-app basis 44. |

| J.P. Morgan | Under "Settings," go to "Security & privacy," then scroll to "Linked apps" to view and manage shared data permissions 25. |

It is important to understand the technical limitations of these revocation methods. For some institutions, such as Wells Fargo, revoking Plaid's access at the bank level acts as a master switch, severing the connection for all Plaid-powered applications simultaneously, rather than disconnecting a single specific app 51.

Additionally, whether a consumer disconnects an app via the Plaid Portal or their bank's dashboard, the action only stops future data sharing. Any historical data that the third-party application (e.g., a budgeting tool) previously collected and stored on its own proprietary servers will remain there. To achieve complete data deletion, the consumer must contact that specific application directly and submit a privacy request 2124.

The Global Shift to Open Banking Regulation

The rules governing how intermediaries like Plaid operate, what specific data they can legally access, and how consumer consent is managed vary dramatically depending on geographic jurisdiction. The global shift toward "Open Banking" - the standardized practice of providing open access to financial data through secure APIs - is playing out very differently in the European and American markets 6555657.

The UK and European Standard: Regulation-Driven

In Europe and the United Kingdom, the Open Banking ecosystem was catalyzed by sweeping, top-down government mandates. The implementation of the revised Payment Services Directive (PSD2) across the European Union and the CMA9 mandate in the UK legally stripped incumbent banks of their historical monopoly over consumer financial data 6555657.

These regulations dictated that if a consumer explicitly consents, banks must share their financial data with authorized third parties. Crucially, the UK Open Banking Standard mandated a single, prescriptive technical specification that all major banks were legally required to implement consistently 555758. In this highly structured environment, data aggregators like Plaid cannot operate freely; they must undergo rigorous audits and be formally licensed by regulatory bodies - such as the Financial Conduct Authority (FCA) in the UK - as an Account Information Service Provider (AISP) or a Payment Initiation Service Provider (PISP) 61426.

Because the API endpoints are heavily regulated, well-documented, and standardized across the continent, the archaic practice of screen scraping was quickly rendered obsolete 555758. The ecosystem benefits from highly uniform consent frameworks, reliable connectivity, and clear legal liability rules, making the European market a global pioneer in secure financial data sharing 555860.

The United States: A Historic Market-Driven Approach

Conversely, the United States has historically operated a highly fragmented, industry-led model completely devoid of a single government mandate dictating technical standards for data sharing 5555661. Without legally mandated APIs forcing banks to open their vaults, data aggregators had to innovate rapidly to meet skyrocketing consumer demand. This lack of standardization is precisely what resulted in the heavy, prolonged reliance on screen scraping and the subsequent need for aggregators to negotiate complex, bilateral data-sharing agreements individually with thousands of different banks 51256.

The Catalyst: CFPB Section 1033

However, this "Wild West" paradigm in the United States is currently undergoing a massive, structural shift. In October 2024, the Consumer Financial Protection Bureau (CFPB) officially finalized its highly anticipated "Personal Financial Data Rights" rule, executing its authority under Section 1033 of the Dodd-Frank Act 561276328.

The CFPB's Section 1033 rule serves as the official regulatory foundation for Open Banking in the United States, transitioning the ecosystem toward a regulatorily supervised framework 61276529. While the rule is currently facing expected legal challenges from banking trade groups - which resulted in a temporary federal injunction pausing enforcement as of early 2026 - the finalized text establishes several fundamental, transformative consumer rights regarding financial data 6768:

- Mandated API Access: Covered financial institutions (data providers) are legally required to make consumer data - specifically including transaction history, account balances, and payment initiation details - readily available to authorized third parties in a standardized, machine-readable electronic format 33276330. This effectively mandates the universal transition to secure APIs and officially initiates the regulatory phase-out of screen scraping as a viable compliance method 332763.

- Zero-Fee Data Sharing: To foster competition and prevent incumbents from stifling innovation, banks are strictly prohibited from charging consumers or third-party applications arbitrary fees for accessing this baseline financial data 276730.

- Strict Data Minimization: The rule outright bans "bait-and-switch" data harvesting. Authorized third-party applications can only collect, use, and retain the exact data reasonably necessary to provide the specific product or service the consumer requested 276370. They are explicitly prohibited from secretly harvesting transaction data for unrelated secondary purposes, such as targeted advertising, cross-selling, or selling the data to third-party brokers 276370.

- Re-Authorization and Deletion: Consumer consent is no longer considered perpetual. API connections are valid for a maximum of 12 months, after which the consumer must be prompted to explicitly reauthorize access 27286731. Furthermore, if a consumer revokes access, data retrieval must cease immediately, and the deletion of collected data becomes the default regulatory practice 27286731.

The compliance timeline for Section 1033 was designed to be phased based on the asset size of the financial institution. The largest commercial banks were originally scheduled to achieve full compliance by April 2026, while the smallest covered institutions were given an extended runway until April 2030 to upgrade their legacy systems 276872.

Comparing Open Banking Regulatory Frameworks

| Regulatory Feature | UK & European Union (PSD2 / Open Banking Standard) | United States (Pre-2024 Market-Driven Era) | United States (Post-CFPB Section 1033) |

|---|---|---|---|

| Primary Driver | Top-down government mandate driven by the CMA, FCA, and EU Commission 655. | None. Purely industry-led innovation and market demand 5661. | Regulated by the CFPB utilizing authority under the Dodd-Frank Act 2763. |

| Technical Standardization | Standardized, uniform API specifications are mandated by law 555758. | Highly fragmented ecosystem relying on a mix of proprietary direct APIs and legacy screen scraping 556. | Legally mandates machine-readable developer interfaces (APIs) and phases out screen scraping 3363. |

| Data Usage Limitations | Bound by strict GDPR and PSD2 privacy regulations 5561. | Governed loosely by complex, dense Terms of Service agreements 61. | Explicitly bans secondary data use and sale; strictly limits data to the intended consumer use case 2770. |

| Consent Lifespan | Requires frequent consumer re-authentication (historically every 90 days) 658. | Perpetual access until manually discovered and revoked by the user 44. | Maximum 1-year access limit before explicit consumer re-authorization is legally required 2867. |

Scale and Future Outlook for Open Finance

The combination of regulatory clarity and improving API infrastructure has led to massive global adoption of open banking technologies.

In the United Kingdom, open banking has evolved from a niche fintech concept into everyday financial infrastructure. By late 2025, the UK ecosystem recorded over 16.5 million active open banking user connections, representing a significant portion of the adult population 733275. More notably, open banking is increasingly being used to actively move money, rather than just read data. The UK saw over 351 million successful open banking payments in 2025 - a 57% year-over-year increase - with consumers frequently using the technology to pay taxes directly to HMRC, settle credit card bills, and automate "me-to-me" transfers through sweeping Variable Recurring Payments (VRPs) 733233.

In the United States, despite the historical lack of regulation, consumer demand has driven comparable scale. Over 80 million US users actively interact with open finance tools, with Plaid's technology touching roughly half of all American adults by 2025 55573.

As the digital plumbing stabilizes, networks like Plaid are shifting their focus toward "intelligent finance." With reliable API connections secured, the next frontier involves using artificial intelligence and machine learning to analyze the vast streams of categorized transaction data. This enables advanced cash-flow underwriting models that expand credit access, highly accurate real-time fraud detection networks, and deeply personalized financial management tools that proactively guide consumer behavior 477734.

Bottom line

Plaid functions as the essential digital infrastructure connecting modern applications like Venmo and Robinhood to the vast, fragmented network of legacy banking systems. By utilizing specialized APIs, it allows consumers to securely share their financial data with budgeting tools, lenders, and payment platforms without ever exposing their raw banking passwords to those third parties. While the company has faced historical scrutiny over early practices like screen scraping and interface transparency, the industry is rapidly maturing. The widespread adoption of tokenized OAuth connections, the introduction of centralized consumer control portals, and the enforcement of the CFPB's new Section 1033 data rights rule are fundamentally securing the open banking ecosystem, ensuring that consumers retain ultimate control over who sees their financial data and for exactly how long.