Persistence of Price Momentum in Modern Financial Markets

Introduction

The momentum factor - the empirically robust phenomenon wherein financial assets that have performed well in the recent past continue to outperform, while past losers continue to underperform - remains one of the most enduring and fiercely debated anomalies in modern financial economics. Originally formalized in the seminal work of Jegadeesh and Titman (1993), the momentum premium has consistently challenged the strong and semi-strong forms of the Efficient Market Hypothesis (EMH) 1134. Unlike traditional, characteristic-based risk factors such as size, value, or quality, momentum does not inherently map to static corporate balance sheets or fundamental metrics. Instead, it captures dynamic, time-series, and cross-sectional predictability derived from historical price behavior, investor sentiment, and the slow diffusion of information across global markets 42.

In recent years, the explosion of algorithmic execution, high-frequency trading (HFT), and machine learning models has fundamentally altered market microstructure. This technological shift has raised profound questions among institutional allocators and quantitative researchers regarding the potential decay, adaptation, or persistence of the momentum premium. A comprehensive 2025/2026 evaluation by Baltussen et al., drawing on over 150 years of data and thousands of portfolio specifications across 46 countries, provides a definitive answer: the momentum premium is neither a statistical artifact nor a product of data mining 3. Across more than a century of out-of-sample testing, an idealized long-short momentum strategy has historically delivered highly significant annualized returns of 8% to 9%, boasting t-statistics that transcend specific market cycles, regulatory regimes, and technological eras 37.

However, momentum in the 2020s is not the same monolithic, pure-price strategy of the 1990s. As modern financial markets have evolved, so too has the academic and institutional understanding of this anomaly. Recent empirical literature published in leading journals, including the Journal of Finance, indicates a transition toward a multidimensional framework - incorporating factor momentum, residual momentum, and network spillover effects - to navigate the unique complexities of algorithmic environments 4105.

This exhaustive research report provides a nuanced, expert-level analysis of the momentum factor. It evaluates competing theoretical frameworks (behavioral versus rational pricing models), investigates geographical robustness beyond U.S. equities, explores the application of momentum in alternative asset classes like cryptocurrencies and commodities, and dissects the anatomy of momentum crashes. Furthermore, it explicitly corrects prevalent retail misconceptions and outlines the severe structural frictions - such as Payment for Order Flow (PFOF) markups, algorithmic latency arbitrage, and short-term capital gains tax drag - that render institutional momentum strategies highly restrictive, and often mathematically infeasible, for modern retail swing traders.

Clarifying Momentum: Structural Typologies and Misconceptions

Before analyzing the theoretical and empirical mechanics of the momentum premium, it is critical to establish precise definitions. The democratization of financial data has led to widespread misinterpretations of quantitative concepts, frequently resulting in retail market participants conflating rigorous systematic momentum with basic charting heuristics.

Retail Misconceptions: Growth Investing and Moving Averages

A pervasive misconception among retail investors is the conflation of cross-sectional momentum with traditional "growth" investing 12. Growth investing is fundamentally a forward-looking, fundamental methodology; it is predicated on forecasts of earnings expansion, revenue growth trajectories, and macroeconomic cycles. Momentum, conversely, is strictly backward-looking and inherently agnostic to underlying valuation metrics, long-term fundamental forecasts, or corporate narratives. A systematic momentum portfolio will seamlessly rotate from high-growth technology equities into defensive utilities, energy stocks, or even distressed debt if the relative, intermediate-term price trend dictates such a shift 67.

Secondly, retail swing traders frequently assume that momentum is synonymous with simple moving average (SMA) crossovers (e.g., a "Golden Cross" where a 50-day SMA crosses above a 200-day SMA) 1516. While SMA crossovers serve as rudimentary, absolute trend-following filters, institutional cross-sectional momentum relies on relative ranking across a vast, diversified universe of assets 171819. The standard academic specification, famously denoted as the $J=12, K=1$ model, evaluates cumulative returns over the prior 12-month formation period ($J$), but intentionally skips the most recent month before the 1-month holding period ($K$). This 1-month skip is a critical quantitative mechanism designed to avoid the negative autocorrelation introduced by market microstructure frictions, bid-ask bounce, and short-term liquidity reversals 19821. Strategies relying on unadjusted short-term SMA crossovers are highly vulnerable to these micro-reversals, degrading the true momentum premium.

Cross-Sectional vs. Time-Series Momentum

To execute momentum systematically, quantitative researchers and asset managers broadly utilize two distinct methodological frameworks: Cross-Sectional Momentum (CSMOM) and Time-Series Momentum (TSMOM). Both approaches exploit the continuation of asset returns, but they exhibit fundamentally different risk profiles, portfolio construction constraints, and specific market vulnerabilities 1229.

Cross-sectional momentum operates on relative outperformance. It involves evaluating a specific universe of assets, sorting them into deciles or quintiles based on their formation-period returns, and subsequently taking an equally weighted or value-weighted long position in the top-performing group ("winners") and a short position in the bottom-performing group ("losers") 110. This strategy is inherently market-neutral in its gross dollar exposure, but as will be discussed in subsequent sections, it is subject to intense time-varying systematic factor betas 310.

Time-series momentum, brought to prominence in the modern literature by Moskowitz, Ooi, and Pedersen (2012), operates on absolute performance. It evaluates each asset independently against its own historical return trajectory 1821. If an asset's past excess return over a specified lookback period is positive, the strategy takes a long position; if the past excess return is negative, it takes a short position 1718. TSMOM effectively captures the positive autocorrelation in individual asset returns and forms the foundational basis for Managed Futures and Commodity Trading Advisor (CTA) strategies across global markets 511.

The following table provides a comprehensive structural comparison of these two dominant momentum paradigms.

| Dimension | Cross-Sectional Momentum (CSMOM) | Time-Series Momentum (TSMOM) |

|---|---|---|

| Core Methodology | Relative ranking. Buys the top $N$-percentile of assets and shorts the bottom $N$-percentile within a defined universe. | Absolute trend. Buys a specific asset if its past return is $>0$, shorts if its past return is $<0$. |

| Benchmark Requirements | Requires a broad, highly liquid cross-section (e.g., S&P 500, Russell 3000, MSCI EM) to generate statistically robust winner/loser spreads. | Evaluates assets entirely independently. Can be applied to single instruments or fragmented asset classes without requiring a peer group benchmark. |

| Net Market Exposure | Dollar-neutral by design (capital allocation is balanced between long and short legs), though structural beta exposure varies wildly depending on the market regime. | Unconstrained net exposure. Can be entirely net long across the portfolio in persistent bull markets, or entirely net short during synchronized global bear markets. |

| Typical Holding Periods | 3 to 12 months, almost universally utilizing a 1-month skip period prior to formation to circumvent short-term microstructural reversals. | Highly variable; often 1 to 12 months, but algorithmic and HFT variants successfully operate intraday or over multi-year macroeconomic horizons. |

| Primary Risk and Vulnerabilities | Highly susceptible to extreme "momentum crashes." Severe tail risk when heavily shorting high-beta distressed losers that suddenly surge during sharp market rebounds. | Generally exhibits smoother absolute performance globally, but is highly vulnerable to prolonged, choppy, range-bound markets where rapid trend failures cause continuous "whipsawing." |

| Factor Subsumption & Interdependence | Highly sensitive to industry momentum and broad factor momentum; often viewed by risk-based theorists as a mechanical manifestation of underlying systematic factor autocorrelations. | Research across global futures markets indicates TSMOM strategies frequently subsume individual country or asset-specific CSMOM in rigorous international spanning tests. |

Theoretical Underpinnings: Behavioral vs. Rational Pricing Models

The persistent nature of the momentum premium over 150 years necessitates a rigorous theoretical explanation that reconciles its existence with modern asset pricing theory. In a perfectly efficient market, any publicly observable, predictable pattern should be rapidly arbitraged away by sophisticated capital 2. The theoretical literature remains deeply divided between two primary paradigms: behavioral models driven by cognitive limits, and rational models predicated on risk-based pricing and limits to arbitrage.

Behavioral Explanations: Underreaction, Delayed Overreaction, and the Disposition Effect

Behavioral models assert that momentum exists and persists because human investors, and the institutions they manage, are boundedly rational and suffer from systemic, predictable cognitive biases 2. The most prominent theoretical framework, developed by Hong and Stein (1999), postulates a market populated by two distinct classes of agents: "newswatchers" and "momentum traders." Newswatchers focus on fundamental data but underreact to private or gradually diffusing public information due to conservatism bias 212. Because information diffuses slowly across the market, prices adjust sluggishly, creating an initial, slow-moving price trend.

Subsequently, momentum traders (trend-followers) detect and attempt to exploit this trend. However, because momentum traders rely on univariate historical price heuristics rather than fundamental intrinsic valuation, their collective capital inflows push the asset price past its fair fundamental value, creating a delayed overreaction 212. Eventually, fundamentals reassert themselves, leading to the long-term price reversals (mean reversion) frequently observed in momentum studies at the 3- to 5-year horizon 27. In this model, the very attempt to arbitrage the initial underreaction creates the subsequent overreaction.

Additional behavioral support stems from the "disposition effect" - the well-documented psychological tendency of investors to sell winning positions too early to lock in gains, and hold losing positions too long to avoid realizing a loss 328. This artificial selling pressure on winners and reluctance to sell losers anchors prices near their historical averages, delaying the full absorption of new, directional information and manufacturing a persistent momentum premium.

Rational and Risk-Based Pricing Models

Conversely, rational asset pricing models, deeply rooted in the Fama-French tradition, argue that momentum profits are not free arbitrage opportunities derived from human error, but are rather exact compensation for bearing specific, undiversifiable systematic risks.

A primary risk-based explanation centers on time-varying systematic risk and extreme tail-risk exposure. Momentum strategies implicitly write out-of-the-money put options on the broader market 31012. During severe market dislocations and high-volatility regimes, the negative skewness and excess kurtosis of the momentum portfolio expand drastically 2112. Rational investors demand a high expected premium during "normal" economic periods to compensate for the catastrophic, unhedgeable left-tail events (momentum crashes) inherent in the strategy's construction.

Furthermore, risk-based literature highlights the role of liquidity risk and macroeconomic cash-flow uncertainty. As Clifford Asness identified in his 1997 research, momentum is notably stronger among stocks characterized by high idiosyncratic volatility, large growth opportunities, and risky cash flows 12. These underlying equities carry the immense risk that projected actual growth will fail to materialize. Consequently, recent winners command a forward-looking return premium to compensate for their heightened exposure to sudden liquidity shocks and aggregate macroeconomic deterioration 1912.

More recent dynamic programming frameworks incorporate regime-switching models - for instance, transitioning between high and low ESG-sentiment regimes or volatile macroeconomic states. These models demonstrate that optimal momentum allocations require rapid, extreme shifts in risk appetite that standard investors cannot physically or psychologically tolerate, thereby allowing the premium to persist 21. Ultimately, modern academic consensus leans toward a synthesis: behavioral biases initiate and sustain the cross-sectional price trends, while severe structural limits to arbitrage - such as catastrophic tail risk, high transaction costs, and institutional capital constraints - prevent quantitative arbitrageurs from fully neutralizing the anomaly 4313.

Modern Empirical Findings (2023+): The Multidimensional Era and Factor Momentum

Research published between 2023 and 2026 in top-tier journals, including the Journal of Finance and Journal of Financial Economics, has rigorously evaluated whether the momentum premium has decayed in modern, highly algorithmic markets. The empirical findings indicate that while pure, simplistic price-based momentum experiences periods of severe drawdown, the anomaly itself has neither decayed nor disappeared. Instead, the focus of cutting-edge institutional quant funds has adapted into what researchers now term a "multidimensional" framework 330.

The Rise of Factor Momentum

A paradigm-shifting development in recent asset pricing literature (e.g., Ehsani and Linnainmaa, 2022; Arnott, Kalesnik, and Linnainmaa, 2023) is the identification and formalization of "Factor Momentum." This research posits that cross-sectional momentum observed in individual equities is largely a mechanical manifestation of autocorrelation within underlying fundamental risk factors (such as Value, Quality, Size, or Low Volatility) 43132. Factors themselves exhibit significant time-series persistence: if the Value factor outperforms the broader market in a given month, it is statistically highly likely to outperform in subsequent months 51434.

By applying Principal Component Analysis (PCA) to a vast "factor zoo" of established anomalies, researchers demonstrated that time-series momentum in the largest principal components subsumes traditional stock-level momentum 51536. This profound finding indicates that traditional stock momentum investors are implicitly timing slow-moving macroeconomic capital flows into specific investment styles, rather than identifying unique, firm-level mispricings 334. When momentum is isolated by neutralizing these systematic factor exposures, the purely "idiosyncratic" or residual firm-level momentum exhibits substantially smoother returns, unique alpha generation, and dramatically lower susceptibility to broader market crashes 337.

Low Equity Risk Premiums and the Ascendance of Alpha

Looking forward through the remainder of the decade, institutional research positions multidimensional momentum as a critical structural necessity. Robeco's 2025 quantitative outlook projects a near-zero Equity Risk Premium (ERP) for U.S. markets spanning the 2025 - 2029 period 6. In such compressed environments, traditional market beta fails to deliver sufficient compounding for pension funds and endowments. Historically, systematic factor strategies - particularly active momentum and value - exhibit highly stable, and often rising, alphas during low-return market cycles 6. Robeco's empirical data notes that in low-return environments, the annualized alpha contribution of momentum increases from 3.9% to 4.9%, and astoundingly, alpha's share of total portfolio returns surges from a mere 25% (in bull markets) to 89% 6. Consequently, institutional capital is executing a secular migration away from passive market-cap weighting toward active, multidimensional factor composites.

Multidimensional Composites in Practice

To harvest this alpha while suppressing volatility, modern institutional momentum relies on an equal-weighted composite of alternative signals, expanding far beyond 12-month trailing price returns: 1. Fundamental Momentum: Exploiting investor underreaction to fundamental business shifts by utilizing analyst earnings revisions and standardized unexpected earnings (SUE) 338. 2. Residual Momentum: Regressing stock returns against the Fama-French five-factor model and trading the residuals. This isolates purely firm-specific news, stripping away the noise of the broader market and sector movements 337. 3. Network and Supply-Chain Momentum: Utilizing advanced natural language processing (NLP) on SEC 10-K filings to map complex corporate linkages. This strategy trades the lagged momentum spillover between economically linked peer firms that share common analyst coverage or opaque customer/supplier relationships 31039. Because these links are less visible to retail participants, the underreaction is more severe, yielding highly significant alpha 39. 4. Anchor-Based Momentum: Exploiting powerful behavioral biases, such as the 52-week high effect, where investors use a stock's recent peak as a psychological anchor, creating predictable continuation patterns when prices break out 340.

These multidimensional approaches have demonstrated superior Sharpe ratios, dramatically lower drawdowns, and stronger t-statistics compared to traditional pure price momentum alone, remaining highly robust across recent algorithmic market cycles 3.

Global Robustness: Europe, Asia, and Emerging Markets

A critical test of any financial anomaly is its out-of-sample persistence across discrete geographical domains, varying regulatory regimes, and distinct cultural market behaviors. The empirical evidence aggregated between 2023 and 2026 overwhelmingly confirms that momentum is a robust global phenomenon, though it manifests with highly specific regional nuances 341.

Developed Markets: Europe and Beyond

In developed European equities, pooled autoregressive models analyzing the twenty-four main equity indices from 2000 to 2020 confirm the persistent predictability of the time-series momentum factor. These strategies yield statistically significant returns of approximately 0.71% per month above the market benchmark, surviving rigorous testing against six-factor models 816. Similarly, the MSCI Europe Momentum Index demonstrates consistent, historical outperformance against its parent index during standard trending market conditions, delivering annualized returns of 13.30% in 2023 and 20.13% in 2024, far outpacing broader regional benchmarks 43.

Asian Markets: The Retail Contrarian Anomaly

Implementation in Asian markets reveals fascinating microstructural behaviors, primarily driven by the extreme dominance of retail traders in specific jurisdictions. Research focusing on the segmented Chinese equity market - comparing domestic-retail-dominated A-shares with foreign-institutional-dominated B-shares - uncovers a powerful dynamic. In China, domestic retail investors act overwhelmingly as aggressive short-term contrarians; they systematically sell recent winners to lock in gains and buy recent losers hoping for a reversion 17.

Paradoxically, this contrarian retail liquidity provision actually amplifies the momentum profits for institutional trend-followers. Empirical studies show that momentum profits are substantially larger (reaching 1.8% to 2.3% per month) when institutional algorithms buy intermediate-term winners that are simultaneously facing heavy net-selling pressure from retail participants 17. The momentum effect is essentially fueled by the retail sector's premature disposition effect.

Emerging Markets (EM): Structural Barriers and Volatility Paradoxes

Emerging Markets (EM) present the most complex structural challenges for momentum investing. While extensive empirical surveys of EM equities identify a statistically significant long-term momentum premium, its practical exploitation is severely hampered by high transaction costs, profound liquidity fragmentation, and elevated idiosyncratic volatility 145. The MSCI Emerging Markets Momentum Index exhibits substantial tracking error, elevated portfolio turnover, and staggering maximum drawdowns exceeding 66% during crisis periods, highlighting the raw danger of the region 1819.

A critical divergence between Developed and Emerging Markets occurs in the application of quantitative risk management. In U.S. and European markets, dynamic volatility-scaling - where a strategy's leverage is systematically reduced when ex-ante market volatility spikes - historically improves the momentum Sharpe ratio and mitigates crashes 40. Yet, recent empirical tests on the MSCI EM universe reveal that volatility scaling spectacularly fails to improve performance. Mechanically reducing volatility in EM equities destroys the annual return, compressing it from 7.55% to a mere 3.05%, thereby decimating the Sharpe ratio (dropping from 0.48 to 0.23) 1. This indicates that in emerging markets, sudden spikes in broad market volatility frequently coincide with the most profitable momentum trend initiations, reflecting a unique environment where delayed overreaction relies on periods of high macroeconomic uncertainty to fully manifest 145.

Expanding the Asset Class Frontier: Options, Cryptocurrencies, and Commodities

The momentum factor is not constrained to global equities; it is a pervasive, macro-level phenomenon observed across commodities, forex, and digital assets. Evaluating momentum in these alternative, highly algorithmic 24/7 markets reveals vital data regarding market microstructure and algorithmic exploitability.

Options Factor Momentum

Recent research published in the Journal of Finance (2023) has uncovered highly profitable momentum within the options market. By constructing delta-hedged option portfolios, researchers found that options with high historical returns continue to significantly outperform options with low historical returns over horizons ranging from 6 to 36 months 511. Crucially, unlike traditional stock momentum, option return continuation is not followed by long-run reversal, suggesting a distinct mechanism . Furthermore, "option factor momentum" fully subsumes standard option momentum, mirroring the equity market finding that individual asset trends are heavily driven by underlying factor persistence 511.

Cryptocurrencies: The Weekend Effect and Perpetual Friction

Between 2020 and 2025, rigorous empirical analysis of digital assets demonstrated that traditional cross-sectional momentum yields poor risk-adjusted returns due to extreme idiosyncratic volatility and social-media-driven short-squeezes 2122. Shorting "loser" altcoins is exceedingly dangerous, leading to a structural "long-leg bias" where momentum profitability is almost entirely derived from long-only trend following 22. Consequently, Time-Series Momentum (TSMOM) dominates crypto factor strategies. TSMOM algorithms utilizing a 28-day look-back period generated Sharpe ratios of 1.51, substantially outperforming a static market baseline 22.

Furthermore, crypto momentum exhibits a highly distinct "weekend effect." Algorithmic momentum execution over weekends systematically yields superior absolute returns and lower drawdowns compared to weekday trading 22. This is attributed to the withdrawal of institutional HFT capital over the weekend, leaving price discovery to retail participants. The pronounced behavioral biases of retail traders (herding, FOMO) create cleaner, highly exploitable momentum vectors that algorithms can easily harvest 22.

However, real-world exploitation faces immense structural frictions. Over 93% of crypto volume is routed through perpetual futures contracts, which utilize a continuous funding rate mechanism to tether the derivative to the spot price 22. In strong bullish momentum regimes, the funding rate exacts a severe toll on long positions, operating as a relentless "funding rate tax" that mathematically erodes capital appreciation over extended holding periods, making long-term momentum holds highly inefficient 22.

The Anatomy and Mitigation of Momentum Crashes

Despite its high historical average returns, cross-sectional momentum is notoriously susceptible to catastrophic drawdowns, colloquially termed "momentum crashes." The authoritative framework for understanding these devastating events was established by Daniel and Moskowitz (2016) 1040.

Momentum crashes do not occur randomly. They are highly conditionally predictable and cluster in specific, extreme macroeconomic environments: namely, rapid market rebounds ("panic states") immediately following deep, prolonged bear markets characterized by high ex-ante volatility 31040.

The mechanism is deeply structural. During a severe bear market, a standard momentum strategy dynamically rebalances. Past winners (the long side of the portfolio) tend to be defensive, low-beta equities that fell less than the broader market. Past losers (the short side) consist of distressed, highly levered, high-beta equities that plummeted in value 310. Consequently, the momentum portfolio inadvertently takes on a massive negative market beta.

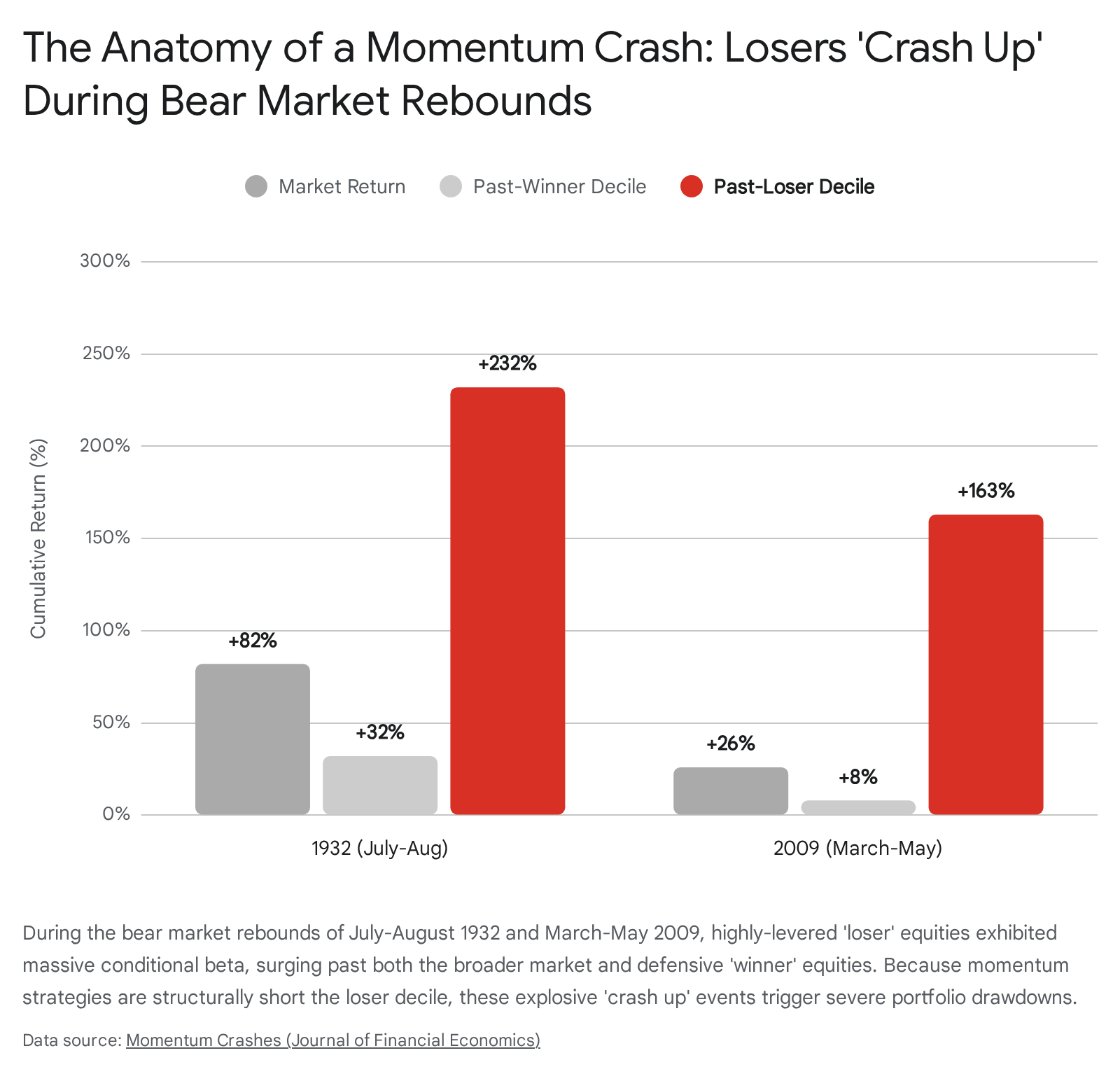

When the market suddenly rebounds, the common stock of distressed loser firms behaves exactly like an out-of-the-money call option on the firm's underlying asset value 310. As the immediate risk of bankruptcy dissipates in the market rally, the losers experience explosive, non-linear upside. The beta of the loser decile can spike above 3.0, while the beta of the winner decile drops below 0.5 310. Because the momentum strategy is structurally short the losers and long the sluggish winners, it suffers agonizing losses. The losers do not crash down; they "crash up" 10.

The data underlying these events is stark. In the 1932 crash (July to August), the broader market rose 82%, but the loser decile surged an astounding 232%, while winners rose only 32%. The Winner-Minus-Loser (WML) strategy returned a catastrophic -74.36% in August 1932 alone 1049. Similarly, in the 2009 rebound (March to May), the market rose 26%, losers spiked 163%, and winners lagged at 8%, causing a -45.52% return for the strategy in April 2009 1049.

To mitigate these crashes, modern institutional implementations utilize dynamic volatility scaling. By utilizing expanding window and rolling 5-year volatility estimates, institutions dynamically scale down their momentum exposure (reallocating to cash) when ex-ante market volatility enters elevated "panic states" 40. Daniel and Moskowitz demonstrated that a dynamic strategy based on forecasts of momentum's mean and variance approximately doubles the Sharpe ratio of a static momentum strategy and severely attenuates left-tail minimum returns, increasing minimum returns from -69.3% to -26.87% 4049.

Implementation Frictions for the Modern Retail Swing Trader

While academic research extols the robust theoretical premium of the momentum factor, realizing these returns in live portfolios is fraught with severe execution hazards. A critical dichotomy exists between institutional quantitative infrastructure and the retail swing trader environment. For retail participants, attempting to systematically harvest cross-sectional momentum is overwhelmingly inefficient due to three primary structural constraints: High-Frequency Trading (HFT) competition, Payment for Order Flow (PFOF) spread markups, and aggressive short-term capital gains tax drag.

HFT Competition and Latency Arbitrage

The 2020s have witnessed the deep integration of Artificial Intelligence and high-frequency trading (HFT) algorithms into market-making architecture 5051. HFT systems dramatically enhance broad market liquidity and narrow quoted bid-ask spreads during normal regimes 1520. However, they operate on microsecond latencies, enabling systematic latency arbitrage.

When a retail momentum trader identifies a technical breakout or a moving-average validation, their manual or simplistic API execution is vastly outpaced by institutional algorithms. Institutional quant desks utilize Smart Order Routing (SOR) to fragment large orders across dark pools and multiple lit exchanges to prevent information leakage 53. Retail traders, routing through single brokerage endpoints, suffer immediate slippage on breakout entries, often filling at the highest end of the spread right as a micro-reversal begins 1653. Furthermore, algorithmic withdrawals during sudden volatility spikes (such as the 2010 Flash Crash) create severe liquidity fragility, magnifying downward momentum and triggering retail stop-loss orders in a cascading effect 50.

PFOF Spread Markups and Execution Quality

The advent of "zero-commission" retail trading has been subsidized almost entirely by the Payment for Order Flow (PFOF) model. Under PFOF, retail brokerages route client orders directly to wholesale market makers (such as Citadel Securities or Virtu Financial) rather than routing them to public lit exchanges 542122. The concentration is immense; in 2025, 96% of retail equities and 94% of retail options orders were internalized by these wholesalers 23.

While wholesalers frequently offer marginal "price improvement" against the National Best Bid and Offer (NBBO) 22, the structural consequence for retail momentum traders is highly negative. First, PFOF effectively segregates "uninformed" retail flow away from institutional flow, allowing wholesalers to capture the spread seamlessly, knowing they are trading against amateur capital 5324. Second, the spread markup is highly punitive for options, which retail traders increasingly use to gain leveraged momentum exposure. Research indicates that the PFOF fees generated per 100-share options contract are drastically higher (up to 100% more revenue) than for standard equities, incentivizing brokers to encourage retail options trading despite wider bid-ask spreads and severe execution opacity 542425. A momentum strategy, which requires high continuous turnover to rebalance between rapid winners and losers, faces compounded hidden costs as spread slippage accumulates, easily erasing the theoretical annualized premium 1660. This structural conflict of interest has led to PFOF being banned in the UK and facing severe restrictions in the EU by 2026, though it remains dominant in the US 5461.

The Short-Term Capital Gains Tax Drag

Perhaps the most formidable obstacle for the retail momentum trader is taxation. By its very structural design, a momentum strategy holds winners and cuts losers rapidly. In a standard U.S. taxable account, this continuous portfolio turnover (often exceeding 100% to 200% annually) guarantees that the vast majority of realized profits are classified as short-term capital gains 6226. Short-term gains are taxed at ordinary income rates, which can approach 40% for high-earning individuals.

Institutional quant funds (e.g., AQR) employ advanced, algorithmic tax-aware strategies to mitigate this drag. These algorithms actively harvest short-term losses to offset gains, utilize relaxed short-selling constraints to mathematically realize highly-taxed short-term losses against long-term gains, and meticulously defer the realization of specific tax lots to optimize post-tax yield 6226. A 2018 study on AQR's live momentum funds demonstrated that these tax-optimization techniques successfully lowered the effective tax rate of a high-turnover strategy from 11.4% to just 5.3% 62. For a retail investor lacking robust, portfolio-level algorithmic tax optimization, the tax drag on a high-turnover momentum strategy can easily erode 200+ basis points of return annually 16. Consequently, pure momentum implementations are often deemed mathematically infeasible for retail participants outside of tax-advantaged accounts (such as IRAs), forcing retail capital toward passive indexing or lower-turnover value strategies 1664.

Conclusion

The momentum factor remains an enduring, formidable anomaly within the global financial architecture. Driven fundamentally by the intersection of bounded human behavioral biases (underreaction, disposition effect, herding) and complex rational risk premia (tail-risk exposure, varying factor betas, macroeconomic liquidity risks), the momentum premium has reliably persisted across more than 150 years of market history. In the current highly algorithmic era, the anomaly has not decayed; rather, it has evolved from simplistic price-trend strategies into highly sophisticated, multi-dimensional composites encompassing fundamental, residual, factor, and network-spillover signals.

However, the nature of its exploitation is heavily stratified. Institutional allocators, armed with deep quantitative resources, successfully leverage risk-managed, multidimensional momentum to generate uncorrelated alpha - a structural necessity in environments facing compressed equity risk premiums. Yet, for the retail swing trader, the theoretical purity of the momentum factor breaks down rapidly under the weight of modern market microstructure. Extreme volatility crashes during bear market rebounds, structural execution slippage from HFT latency arbitrage and PFOF internalization, and severe short-term capital gains tax penalties render naive retail momentum trading highly inefficient. Ultimately, while momentum is an "eternal" feature of asset pricing, successfully harvesting its premium requires an institutional caliber of dynamic risk management, sophisticated execution routing, and algorithmic tax optimization that remains largely out of reach for the casual market participant.