Performance overshooting and disruption in mature industries

Theoretical Foundations of Performance Trajectory Overshooting

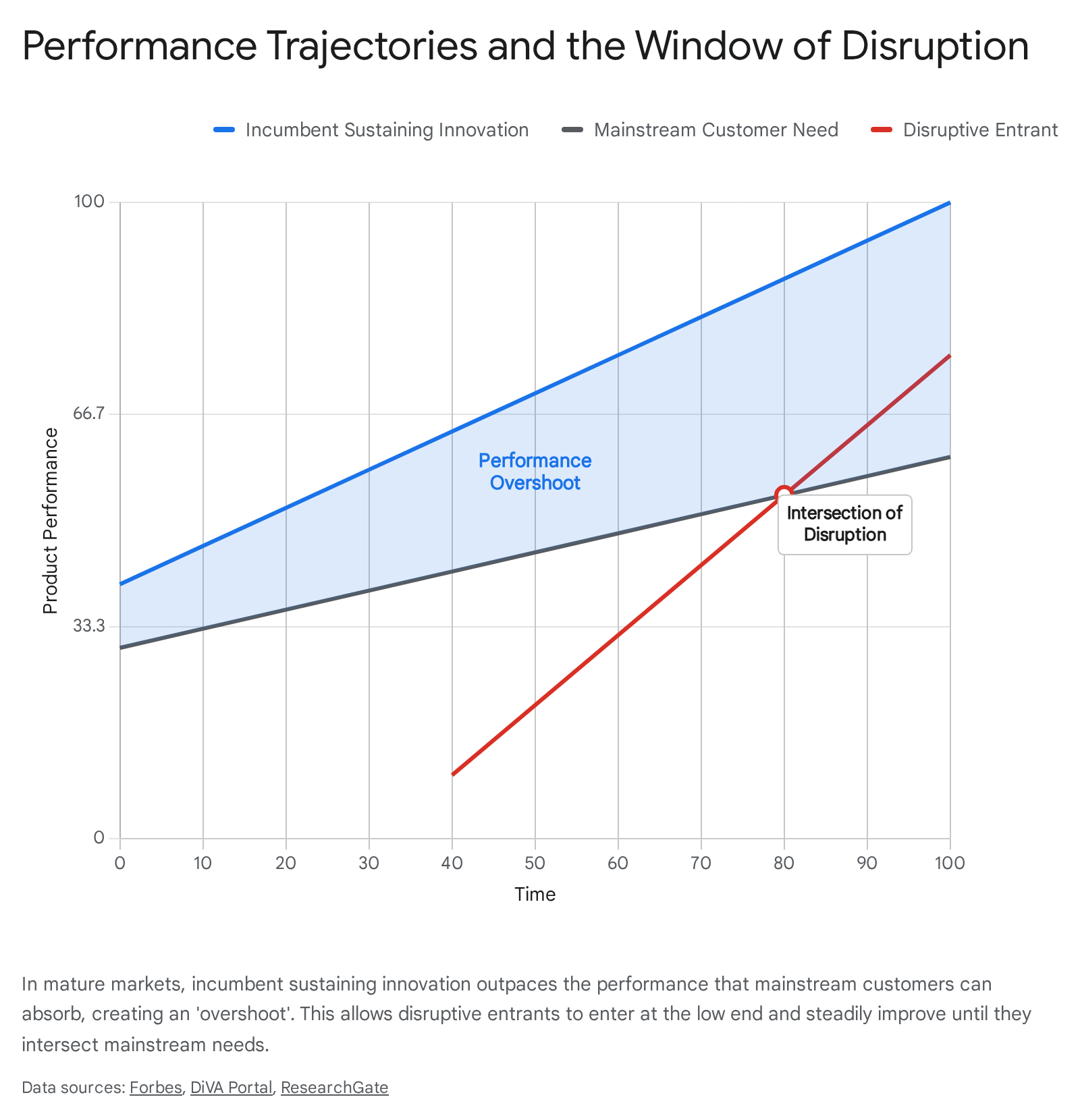

The concept of performance trajectory overshooting serves as the central causal mechanism within Disruptive Innovation Theory (DIT), initially formalized by Clayton Christensen in the mid-1990s. The framework fundamentally altered the discipline of strategic management by providing an empirical explanation for why dominant, well-managed incumbents routinely fail to maintain market leadership when confronted with specific types of technological and business model changes 12. At the core of this phenomenon is the interaction between two distinct trajectories: the rate at which a technology or product improves over time, and the rate at which customers within a given market can practically absorb or utilize those improvements 23.

In mature industries, established firms are heavily incentivized to pursue "sustaining innovations." These developmental efforts focus on improving the performance of existing products along dimensions that mainstream and high-end customers have historically valued 145. Driven by the pursuit of higher profit margins and the demands of their most lucrative clients, incumbents allocate vast capital and research and development (R&D) resources toward continuous product enhancement 24. However, the pace of technological progress frequently and inevitably outpaces the rate of change in actual, everyday customer needs 36.

When incumbents improve their products faster than the customer's inherent ability to utilize the new features, market overshooting occurs 26. The product becomes overly complex, highly specified, and increasingly expensive. At this juncture, the market dynamics undergo a structural shift. Customers who are "overshot" find themselves paying premiums for attributes and capabilities they neither need nor use, creating a massive economic vacuum at the lower tiers of the market 25.

This overshoot establishes the exact conditions required for disruptive innovation to take root 67. A disruptive entrant can introduce a product that is initially inferior by legacy mainstream performance metrics but possesses a novel mix of alternative attributes - such as being cheaper, smaller, simpler, or significantly more convenient 1. Because the disruptive product appeals to overserved customers at the low end of the market (low-end disruption) or to non-consumers who previously lacked access entirely (new-market disruption), the incumbent often ignores the emerging threat 18. The incumbent's existing business model, which relies on high gross margins and complex feature sets to satisfy financial markets, makes a defensive response against a low-margin, simplified product economically irrational from their perspective 14. Over time, the disruptive technology follows its own steep trajectory of improvement, eventually intersecting with the performance needs of mainstream customers and displacing the legacy incumbent 38.

Variations in Trajectory Velocity

The speed at which disruption unfolds is highly dependent on the velocity of the respective performance trajectories. In industries like computer disk drives - which Christensen referred to as the "fruit fly" of the business world due to their rapid generational turnover - technology improved at an exceptionally steep slope 3. In these environments, performance overshooting occurred rapidly, allowing new entrants to challenge and displace incumbents every few years 3. Conversely, in industries such as steel manufacturing or discount retailing, the performance trajectories exhibit much more gradual slopes, meaning the process of disruption, overshooting, and incumbent displacement played out over several decades 3.

Empirical Critiques and Theoretical Controversies

While Disruptive Innovation Theory has shaped management strategy and venture capital allocation for three decades, its empirical validity and theoretical purity have been subject to intense academic scrutiny. Scholars consistently argue that the broad, colloquial application of the term "disruption" has diluted its explanatory power, transforming it from a precise analytical framework into a generalized piece of marketing nomenclature applied to any successful new enterprise 9.

The Empirical Assessment of Disruption Elements

A pivotal critique of the framework was conducted by researchers King and Baatartogtokh in 2015. Their study sought to rigorously test the historical validity of DIT by evaluating 77 distinct historical cases of disruption across 77 industries 910. To ensure consistency and prevent hindsight bias, they surveyed 79 field experts regarding the specific transitional mechanics of each industry 9. The study specifically tested the four foundational elements of Christensen's theory: 1. The presence of incumbents improving along a trajectory of sustaining innovation. 2. The pace of sustaining innovation actively outstripping and overshooting customer needs. 3. Incumbents possessing, but failing to exploit, the capability to respond to the entrant. 4. Incumbents ultimately floundering and losing market dominance as a direct result of the disruption 910.

The empirical findings aggressively challenged the universal applicability of the overshooting model. The researchers found that the vast majority of commonly cited "disruptive" cases failed to adhere to the strict mechanical requirements of the theory.

| Theoretical Element of Disruptive Innovation | Percentage of Historical Cases Lacking the Element | Implications for the Overshoot Model |

|---|---|---|

| Sustaining Innovation Trajectory | 31% | Nearly a third of disruptions occurred without the incumbent pursuing traditional high-end sustaining improvements 9. |

| Performance Overshooting | 78% | The vast majority of disrupted markets did not feature incumbents exceeding the performance requirements of their users 9. |

| Capability to Respond | 39% | Many incumbents lacked the actual operational or technological capability to respond, contradicting the premise that failure is purely a business model choice 9. |

| Incumbent Displacement | 38% | A significant portion of incumbents survived the disruption, maintaining viability rather than floundering 9. |

Collectively, King and Baatartogtokh determined that only 9% of the examined cases perfectly matched all four elements and predictions of Christensen's original theory 9. This remarkably low empirical validation rate suggests that performance overshooting, while a powerful strategic narrative, is not a universal prerequisite for industry disruption. The researchers noted that the core assumption underlying overshooting - that sustaining innovation eventually produces a product that is "too good" - frequently conflicts with fundamental human nature. Consumers generally possess inherently insatiable demands for performance, availability, health outcomes, and convenience, making it difficult for an offering to ever truly be considered "too effective" in certain domains 9.

Ecosystem Perspectives and Theoretical Reframing

Recent scholarship in 2024 and 2025 by Shahzad Ansari and colleagues further unraveled theoretical controversies surrounding DIT, advocating for a fundamental shift away from the binary "incumbent versus disruptor" model 11. Ansari's research posits that modern market disturbances require a broader "challenger-incumbent" perspective that accounts for complex, multi-layered innovation ecosystems rather than isolated firm-to-firm warfare 111213.

Ansari identified six core controversies shaping the current academic and strategic discourse regarding disruption and overshooting 1113:

- Definitional Ambiguity: Deep disagreement persists over whether disruptive innovation represents an intrinsic characteristic of a specific technology (e.g., solid-state drives vs. hard disks) or whether it is merely a measure of ultimate market outcome and success 11. Furthermore, scholars debate whether disruption must be a rapid, sharp shock to a market or if it can manifest as a slow, transformational process 11.

- The Case-Study Conundrum: DIT relies heavily on historical, firm-centric case studies (e.g., rigid disk drives, mechanical excavators, integrated steel mills), raising legitimate questions about whether the mechanisms of disruption are generalizable across different economic eras, modern software environments, and varying capital structures 1113.

- Generalizability and High-End Disruption: The traditional framework struggles to explain prominent anomalies. For example, the Apple iPhone heavily disrupted the mobile phone market not by entering from the low end with cheaper, inferior technology, but by introducing a vastly superior, more expensive product - a phenomenon sometimes classified as "high-end disruption" 1113. Recognizing high-end disruption is critical for addressing the multifaceted dynamics of modern markets 13.

- Unit of Measure: Scholars remain divided on whether disruption should be measured at the level of the specific product technology, the individual firm, the broader business model, or the overarching innovation ecosystem encompassing multiple interdependent actors 1213.

- Outcome Bias: DIT literature frequently exhibits severe biases. "Incumbent survivor bias" over-emphasizes cases where market leaders catastrophically fail, while "pro-innovation bias" relies on the assumption that disruptive innovation is inherently positive, frequently ignoring negative societal externalities, ethical considerations, and systemic market damage 11. Modern data indicates that incumbents frequently survive, adapt, form partnerships, or simply acquire the disruptive threat to extend their long-term dominance 11.

- The Nature of DIT Theory (Performativity): Critics argue the theory is merely descriptive and only functions in hindsight, failing to provide ex-ante predictions of which startups will succeed 911. Conversely, Ansari conceptualizes DIT through the lens of "performativity." Under this view, DIT serves as a prescriptive, actionable blueprint - a shared managerial discourse - that executives use to jumpstart the innovation journey and align organizational resources, regardless of the theory's strict scientific predictive accuracy 11.

Measurable Indicators of Market Overshoot

Identifying the window of disruption opportunity requires moving beyond theoretical frameworks to observe quantitative, real-time signals of overshooting in mature industries. When a market enters the overshooting phase, several distinct indicators manifest in corporate financial metrics, product utilization rates, human resources environments, and aggregate consumer purchasing behavior.

Feature Fatigue and the Capability Versus Usability Trade-off

A primary, highly visible indicator of product overshooting is "feature bloat" or "featuritis" 14. In the relentless pursuit of sustaining innovation, manufacturers continuously increase a product's capability - defined strictly as the number of useful functions it can perform 1415. However, this unconstrained expansion frequently comes at the direct expense of usability. Examples abound in the consumer goods sector: coffeemakers offering 12 distinct drink options, automobile dashboards saturated with more than 700 distinct feature controls, and desktop mousepads that double as clocks, calculators, and FM radios 1415.

Empirical studies on feature fatigue reveal a fascinating paradox in consumer behavior that directly fuels the innovator's dilemma. Prior to purchase, consumers consistently favor high-feature models. When presented with choices, they heavily weight capability, equating a higher number of features with greater overall value, and will often actively customize products to include the maximum possible features 1415.

However, post-purchase, the reality of operating overly complex products fundamentally alters the consumer's value equation. Once the user is actually interacting with the product, usability begins to eclipse capability as the primary driver of satisfaction 1415. Customers experience profound feature fatigue, leading to frustration, increased customer support costs, and dissatisfaction. This ultimately reduces their long-term lifetime value to the firm, damages brand loyalty, and depresses subsequent upgrade cycles 1415. For product managers, this presents a severe strategic dilemma: designing high-feature models maximizes initial sales, but limits long-term profitability. The divergence between initial purchase incentives and long-term daily utility creates a structural vulnerability in the market that simplified, disruptive entrants easily exploit by offering products that perform a single core task exceptionally well 1516.

Declining Return on Research and Development Investment

Financial indicators also signal market overshooting, most notably through a systemic decline in Research and Development (R&D) Return on Investment (ROI). R&D ROI - typically defined as the ratio of new revenue in the current year against the previous year's R&D expense - measures a company's fundamental efficiency in converting innovation expenditures into tangible market growth 1917. In overshot markets, the marginal cost of achieving incremental performance improvements escalates exponentially, while the customer's aggregate willingness to pay for those improvements plateaus 2.

The global pharmaceutical industry provides a stark, quantifiable example of this dynamic. According to a comprehensive 2023 Deloitte analysis, the projected pharmaceutical R&D return on investment declined sharply to just 1.2% in 2022, marking a 13-year low and a severe drop from the 6.8% ROI recorded in 2021 18. This decline was driven by increased trial cycle times, rising drug development costs (which increased by roughly 13% in 2022 alone), and a troubling doubling of terminated developmental assets 18. Many of the abandoned projects were initially predicted to be high-revenue "blockbuster" drugs, highlighting the increasing difficulty of pushing the boundaries of medical capability profitably 18.

Similarly, in the Software as a Service (SaaS) sector, benchmark data highlights the disparity in R&D efficiency depending on the growth stage and market maturity.

| SaaS Company Revenue Stage | Average R&D ROI (Revenue generated per $1 of R&D spend) | Market Implications |

|---|---|---|

| High-Growth Public (Pre-IPO Peak) | ~$2.50 | Exemplified by companies like Snowflake and Hubspot prior to IPO; indicates high market fit and rapid absorption of new features 17. |

| Mature Growth ($100M - $500M) | ~$1.50 | Represents top-quartile performers maintaining efficient execution and aligning features with actionable customer demand 17. |

| Mid-Market Private ($50M - $100M) | ~$0.57 | Broad market average; indicates massive engineering investments are failing to yield proportional revenue, heavily signaling internal bloat or market overshooting 17. |

When internal R&D expenditures no longer translate into highly valued consumer features - evidenced by an ROI dropping below $1.00 - incumbents become highly vulnerable to agile entrants operating with significantly leaner cost structures and more targeted innovation pipelines. Furthermore, studies indicate that highly financially constrained firms often experience reduced R&D stickiness, forcing them to slash innovation budgets during downturns, which further exacerbates their vulnerability to disruptors 19.

Consumer Upgrade Elongation and Willingness to Pay

When performance consistently overshoots practical utility, end consumers inevitably alter their purchasing cadences. The global smartphone industry, historically characterized by rapid, annual replacement cycles driven by highly anticipated flagship technological leaps, is currently experiencing significant market elongation. According to comprehensive 2025 and 2026 consumer mobile survey data from Allstate Protection Plans and YouGov, the era of automatic, predictable annual smartphone upgrades is rapidly fading 202125.

While a baseline segment of users (25%) still expects to upgrade within a 1 to 2 year window, a rapidly growing contingent of the market is actively stretching device lifespans to 3 to 4 years (23%), and 21% are delaying upgrades entirely until their current device catastrophically breaks 202125. At the extreme end of the spectrum, only 3% of consumers report a willingness to replace a device within six months, and just 22% plan to upgrade within 12 months 2125.

This profound behavioral shift is driven by a clear plateau in the consumer's willingness to pay for incremental features. Consumers are pivoting their focus away from the "wow" factor of processing power and novel form factors, redirecting their purchasing criteria toward pragmatic constraints such as battery life, physical durability, and long-term software support longevity 21. Budgetary constraints are also highly evident; the percentage of likely buyers expecting to spend under $300 fell from 33% in 2023 to 22% in 2025, while interest in the mid-tier $301-$500 bracket rose from 15% to 23%, signaling a move away from ultra-budget devices but a firm rejection of ultra-premium flagships 20.

Interestingly, this cycle elongation has forced a "premiumization" effect in certain emerging markets, particularly the Middle East and Africa (MEA). In these regions, consumers treat smartphones not as disposable consumer electronics but as critical, long-term infrastructural investments required for mobile banking, digital identity, and gig-economy participation 26. Consequently, these consumers are willing to pay higher upfront costs for 5G-capable, durable devices intended to last three to five years, further suppressing the high-volume replacement velocity that previously defined the industry 26.

Performance Overshooting in Enterprise Software

The modern enterprise software and SaaS ecosystem represents one of the most pronounced, highly capitalized environments for performance trajectory overshooting in the global economy. Originally acting as massive disruptors themselves - by shifting heavy on-premise infrastructure burdens to the cloud and adopting highly flexible subscription pricing models - mature SaaS incumbents have now accumulated massive, complex platforms built to serve diverse global industries 2728.

The Crisis of Feature Bloat and License Waste

In a structural effort to continually justify recurring subscription revenues and capture upstream enterprise clients, legacy SaaS vendors continuously append new modules, highly specific workflows, and complex integrations to their core products 2722. This architectural approach inherently violates lean operational principles, ultimately forcing generic, bloated processes onto organizations under the guise of "industry best practices" 27.

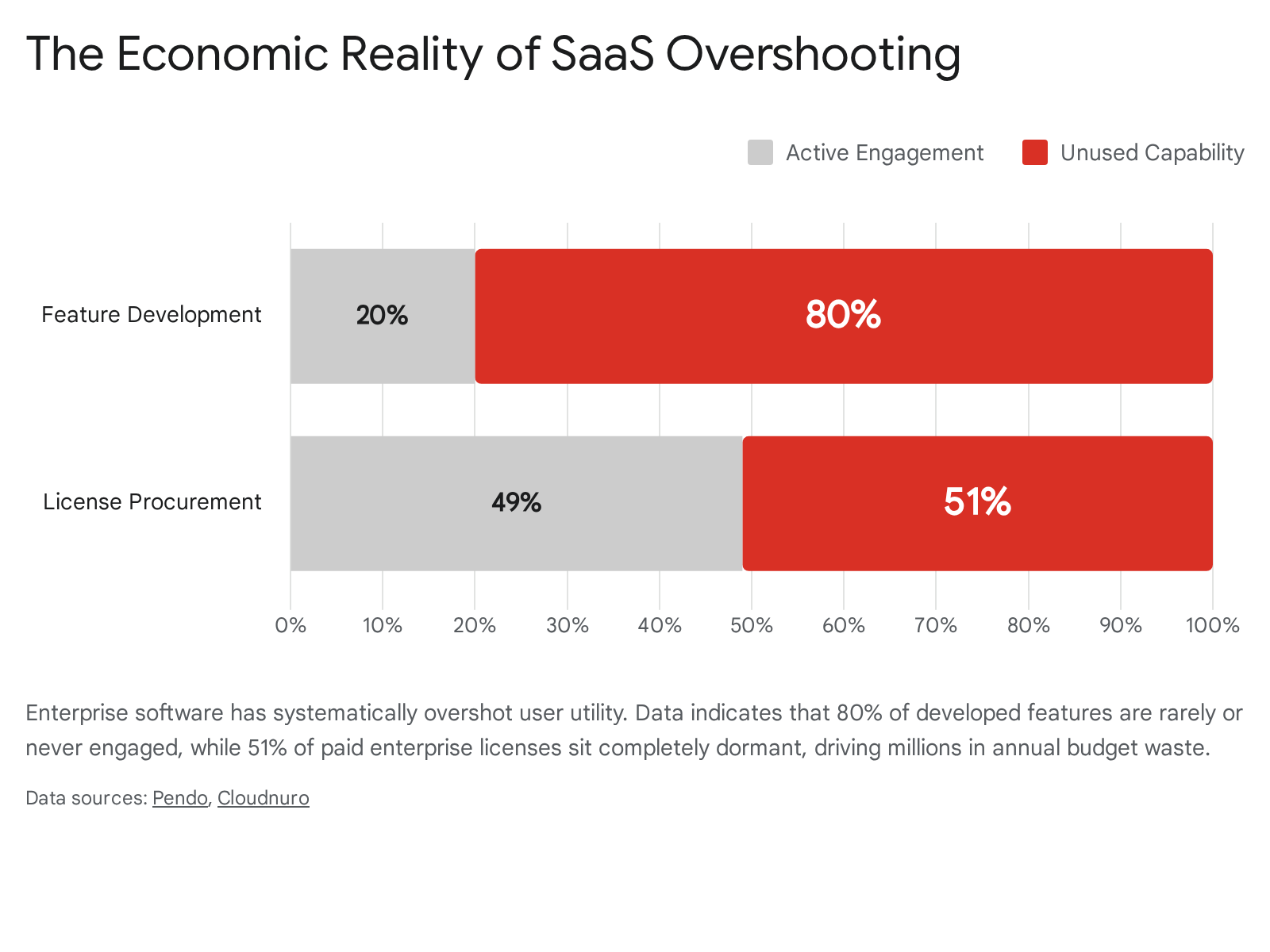

Recent, large-scale utilization analytics reveal the severe extent of this market overshooting. A massive 2024 analysis conducted by Pendo across 615 different software products found that an astounding 80% of deployed features are rarely or never used by end customers 2324. In fact, an extreme usage concentration exists where just 12% of a product's features generate 80% of daily user engagement 23. This dynamic scales to immense financial waste; across publicly traded cloud companies, this represents an estimated $29.5 billion in wasted research and development investment directed toward capabilities the market does not value 23.

The profound misalignment between software capability and actual, daily business utility extends directly to enterprise license allocation. Hard utilization data from Cloudnuro in late 2025 and 2026 indicates that 51% of enterprise SaaS licenses go completely unused - the highest waste rate ever recorded 2332. In these instances, the allocated users have not logged in for over 90 days, or have never logged into the system at all 32. Consequently, average enterprise organizations are wasting approximately $18 million annually on dormant subscriptions and premium tier access that sits entirely untouched 2232.

The Rip-and-Replace Tax and Strategic Vulnerability

Incumbent software providers enforce and monetize this overshooting through complex, monolithic data models that create exceptionally high switching costs and vendor lock-in 2728. Rather than innovating core platforms to meet specific, evolving user workflows, major SaaS providers prioritize financial engineering through acquisitions and aggressive price escalators, which routinely add 20% to 40% to base subscription costs - often mandated through involuntary AI feature surcharges 2732.

This dynamic creates a massive "rip-and-replace tax" that stalls broader business agility 27. Customers are forced to conform their lean internal operations to the generic, overly complex workflows dictated by the legacy software architecture. This growing operational friction, combined with widespread "SaaS sprawl" (where average enterprises hold over 270 overlapping applications), forms the exact structural market conditions required for a new wave of API-first, unbundled, and highly composable tools to disrupt the incumbents from below 2725.

Transitioning to Artificial Intelligence Consumption Models

The most immediate threat to overshot enterprise software is the rapid integration of advanced Artificial Intelligence (AI). AI agents are fundamentally altering the software pricing paradigm. For decades, software pricing was rigidly tethered to the "per-seat" metric - charging clients based on the number of individual human users requiring login access 26. However, as generative AI and autonomous agents increasingly execute complex, cross-system workflows, pull and interpret data contextually, and automate repetitive tasks, the absolute requirement for human seats declines drastically 27.

In this environment, incumbent software platforms are effectively being demoted to pure backend capability layers, while AI assumes the high-value role of the orchestration and coordination layer 27. Faced with a structurally contracting user base, major SaaS vendors are being forced into a painful pricing transition. Industry analysts, including IDC, firmly predict that by 2028, pure seat-based pricing will be largely obsolete, forcing up to 70% of legacy vendors to refactor their entire value propositions 26.

Vendors must shift toward consumption-based models or outcome-based pricing linked directly to agent interactions and token usage 26. This transition exposes a massive vulnerability for legacy firms; their heavily bloated feature sets and high switching costs no longer justify premium enterprise pricing when a thin, intelligent AI coordination layer can achieve the desired business outcome without requiring human employees to ever interact with the underlying software's user interface 2727.

Frugal Innovation as a Response to Western Overshoot

While Disruptive Innovation Theory frequently anchors its case studies in Silicon Valley software dynamics or historical American manufacturing, one of the most explicit, geographically observable reactions to Western performance overshooting occurs in emerging markets through the mechanism of "frugal innovation" 2829. Frugal innovation is not simply the practice of manufacturing cheap, inferior goods; rather, it is a highly systematic engineering methodology focused on redesigning products and processes from the ground up to strip away unnecessary costs, focus exclusively on core functionalities, and optimize performance for specific, severe local constraints 293031.

The Clean Slate Approach in Emerging Markets

Multinational corporations (MNCs) based in developed economies historically design high-end, complex products tailored to affluent consumers situated at the top of the economic pyramid 3233. These products implicitly rely on stable background infrastructure, high energy consumption, controlled climates, and highly trained support personnel 2831. These baseline conditions are virtually absent in many emerging markets across Asia, Africa, and South America, where institutional voids, extreme heat, heavy dust, and frequent power instability prevail 2831.

When Western incumbents attempt to capture market share in emerging markets, they typically engage in a flawed strategy of "slimming" - reducing material quality or replacing automatic electronic controls with manual mechanical ones to marginally lower costs, while maintaining the same fundamental, over-engineered product architecture 3134. This stripped-down approach routinely fails because the baseline technology remains fundamentally misaligned with local operational realities and the extreme price sensitivity of the consumer base.

True frugal innovators bypass this Western overshoot entirely by adopting a "clean slate," heavily constrained engineering mindset 2934. By entirely redefining the primary performance axis, these companies successfully target the massive, low-income demographic at the Bottom of the Pyramid (BoP) with "good enough" products that offer revolutionary price-to-performance ratios without sacrificing essential durability 283233.

Reverse Innovation and the Upmarket Migration

The healthcare, consumer appliance, and heavy industrial sectors provide clear, actionable examples of frugal innovation successfully challenging overshot incumbent business models:

- General Electric's MAC 400 ECG Machine: Traditional electrocardiogram machines (such as the legacy MAC 5500) designed for Western hospital environments are bulky, highly complex, and exceptionally expensive. Recognizing the market failure, GE's local R&D subsidiaries in India developed the MAC 400 specifically for rugged, rural environments. Built to operate reliably on battery power in areas with highly intermittent electricity, the device was offered at roughly $1,000 - a mere fraction of the cost of legacy systems - while maintaining strict, core diagnostic reliability 3034.

- Tata Swach Water Purification: Addressing the critical need for clean drinking water in areas lacking electrical grids, Tata engineers utilized locally sourced rice husks combined with silver nanoparticles to filter water entirely without electrical power. This highly effective, frugal solution purifies up to 1,500 liters of water for roughly 15 Euros, directly and aggressively undercutting high-end Western filtration systems that utilize UV-light and membranes costing upward of 200 Euros 31.

- Industrial Robotics: Toshiba constructed the THL series SCARA-Robot specifically for the Chinese manufacturing market. By focusing purely on core movement functionality, the low-priced, lightweight machine weighs 60% less than equivalent Western series and reduces total energy consumption by 20%, opening up automation to previously unserved low-margin factories 31.

Crucially, frugal innovations possess the inherent capacity for "reverse innovation" - the market phenomenon where products originally developed for low-income, resource-constrained emerging markets eventually migrate and disrupt the affluent home markets of Western incumbents 3135. Products like GE's portable Vscan ultrasound have successfully migrated back to developed nations, definitively demonstrating that once a disruptive trajectory is established at the extreme low end, it can travel upmarket to threaten legacy profit pools worldwide 3133.

Artificial Intelligence and the Next Disruption Cycle

The rapid, unprecedented acceleration of Artificial Intelligence (AI) capabilities in the mid-2020s represents a profound technological paradigm shift. AI is currently functioning simultaneously as a powerful sustaining technology for highly capitalized incumbents and a highly disruptive force that acutely exposes the performance overshooting of traditional software architectures 3637.

Scaling Laws and the Utility Plateau

The contemporary development of Large Language Models (LLMs) currently exhibits a severe, structural performance trajectory dilemma. Foundational AI scaling laws dictate that proportionally increasing model parameters, raw compute power, and training data yields predictable, linear improvements in model performance 38. Consequently, AI model size and computational requirements have grown exponentially. Data indicates that from 1950 to 2010, compute scaled at roughly 1.5x per year, but from 2010 to 2025 (spanning from early deep learning architectures to massive Transformers), compute growth accelerated to 4.2x per year 38.

However, deep empirical evidence suggests this brute-force scaling is beginning to experience diminishing returns in practical, everyday business reliability, leading to a unique, modern form of technological overshooting 48. While larger models routinely pass highly complex synthetic benchmarks and academic tests, deployed AI models frequently struggle with real-world, dynamic stability.

Systemic issues such as "model drift" - where performance visibly decays over time due to changing human input patterns - and recursive data collapse (the degradation of models trained heavily on AI-generated synthetic data) severely impact enterprise reliability 48. Furthermore, while a massive model might score 90% on a generalized academic benchmark, true business utility requires strict factual accuracy, absolute security, and low latency; generating hallucinated data limits the technology's application in high-stakes analytical environments 4849. Thus, the massive capital investments poured into cutting-edge, general-purpose foundation models may be drastically overshooting the exact reliability, governance, and cost constraints required by typical enterprise users 39.

Open-Source Models and Low-End Disruption

A real-time, textbook manifestation of Christensen's theoretical framework occurred in early 2025 with the abrupt emergence of DeepSeek, a Chinese AI startup. While dominant, heavily funded Western players like OpenAI pursued a highly resource-intensive, closed-source strategy aimed at maximizing raw reasoning capabilities (targeting the absolute high end of the capability market), DeepSeek systematically captured the market from below 251.

By aggressively utilizing Mixture-of-Experts (MoE) architectures and advanced model lightweighting techniques, DeepSeek drastically reduced both training and ongoing inference costs 3851. Their open-source models (such as DeepSeek-R1) offered near-GPT-4 level performance at a fraction of the computational price, directly catering to the massive global developer ecosystem seeking affordable, easily deployable infrastructure rather than purely theoretical reasoning limits 251. This event perfectly mirrored the historical disruption of Intel by ARM processors - where Intel's singular focus on high-margin, absolute processing performance left the market vulnerable to highly efficient, lower-power alternatives that eventually came to completely dominate the mobile computing landscape 2.

Strategic Frameworks for Incumbent Defense

As the mechanical realities of performance overshooting and structural disruption become evident across diverse global industries, the strategic focus for leadership shifts toward how incumbents can proactively identify their own vulnerabilities and implement robust defensive architectures.

Creative Accumulation and Ecosystem Integration

While traditional Disruptive Innovation Theory heavily assumes the inevitable displacement and collapse of established incumbents (the process of creative destruction), empirical market data reveals that established firms frequently survive and thrive by executing a highly disciplined strategy of "creative accumulation" 611. This strategy requires a delicate, concurrent management approach: simultaneously fine-tuning and evolving existing legacy technologies at a rapid pace to maintain vital cash flows, while aggressively acquiring, developing, and integrating novel technologies and resources into superior overall solutions 6.

Furthermore, incumbents hold massive systemic advantages that pure-play, agile disruptors severely lack, primarily in the form of deep financial reserves, established regulatory and compliance architectures, and massive proprietary datasets 40. A comprehensive survey found that incumbent companies control approximately 80% of the world's data 40. In the modern era, this provides a critical, nearly insurmountable moat against startups, particularly in training localized, highly accurate AI systems tailored to specific enterprise workflows 40. By effectively leveraging this data advantage to build specialized AI copilots for their massive installed user bases, incumbents can successfully fend off disruption and actually extend their market dominance 1128.

Redefining the Axes of Competitive Performance

The most fatal, recurring error for incumbents facing disruption is continuing to measure market performance along historical, legacy axes. To accurately detect the opening window of disruption, corporate leaders must possess the foresight to identify what the new basis of competition will be once the primary historical dimension has been fully satisfied and overshot 26.

For example, when commercial airline passengers became heavily overserved by the luxury, hub-and-spoke routing, and expansive service offerings of legacy national carriers, Southwest Airlines correctly identified that the new critical performance axis was "miles per route flown" on short-haul, point-to-point routes. By optimizing gate turnaround times and drastically slashing fares, they captured the market 2. Similarly, in modern B2B software, when functional feature parity is reached across competitors, the primary competitive axis rapidly shifts away from "capabilities" toward "ease of deployment," "system interoperability," or "consumption cost efficiency."

To effectively counter impending disruption, incumbents must routinely conduct rigorous feature utilization analyses to financially quantify the extent of their own overshooting 22. If vast segments of a product portfolio are generating near-zero daily usage, the firm is highly exposed to an unbundling attack. To ensure long-term survival, organizations must actively incubate structurally autonomous teams tasked with building low-cost, simplified, "good enough" alternatives targeting their own neglected or overserved customer segments - effectively acting to aggressively disrupt themselves before an external entrant can capitalize on the market vacuum 4142.

Conclusions

Performance trajectory overshooting remains one of the most critical and predictive precursors to widespread industry disruption. The phenomenon is deeply rooted in a fundamental economic misalignment: established companies, driven by strict margin requirements, institutional inertia, and the demands of their most profitable clients, inherently improve their products at a velocity that consistently exceeds the average customer's practical capacity for absorption.

Whether observed through the lens of massive feature bloat and license waste in modern enterprise SaaS platforms, the profound elongation of smartphone upgrade cycles due to a plateauing willingness to pay for incremental hardware improvements, or the systemic failure of Western multinationals to penetrate emerging markets without adopting strict frugal engineering principles, the underlying pattern remains remarkably consistent. When basic usability is sacrificed for sheer technical capability, and product costs detach from pragmatic, daily utility, an economic vacuum rapidly forms at the lower tiers of the market.

However, contemporary empirical research and market observation clearly indicate that the traditional, highly publicized fate of the disrupted incumbent - total catastrophic displacement - is not an inevitability. The innovation ecosystem has evolved significantly. The emergence of open-source artificial intelligence models and autonomous software agents demonstrates that modern disruption is now heavily reliant on fundamental business model reinvention, moving far beyond simple technological inferiority to capture the vital coordination layer of modern business operations. For mature industries to survive the inevitable window of disruption, they must continuously audit their own performance trajectories, proactively shed the hubris of feature bloat, leverage their vast proprietary data assets, and cultivate the organizational agility to deploy simplified, highly efficient innovations before agile challengers permanently seize the market.