Microsoft's Strategic and Financial Position in OpenAI Post-IPO

Corporate Restructuring and Governance Shift

The transition of OpenAI from a non-profit-controlled capped-profit entity to a standard corporate structure represents a highly complex governance reorganization. This transition, initiated in late 2025 and refined through corporate funding rounds in early 2026, fundamentally altered Microsoft's strategic and financial position within the company, shifting the dynamic from an exclusive dependency to a bounded commercial partnership.

The Public Benefit Corporation Transition

In October 2025, OpenAI officially completed its recapitalization, shifting its core operations into a Delaware Public Benefit Corporation (PBC) named OpenAI Group PBC 122. This restructuring was driven by the incompatibility of the original capped-profit structure - which limited investor returns to a 100x multiple - with the expectations of public equity markets ahead of a planned Initial Public Offering (IPO) 3. The non-profit OpenAI Foundation retained an equity stake, but its absolute governance control over the commercial entity was dissolved in favor of a standard equity-based corporate oversight model 3.

Under Delaware corporate law, directors of a PBC are legally required to balance the pecuniary interests of shareholders with the specific public benefits outlined in the corporate charter 54. For OpenAI, this dual mandate requires corporate leadership to balance financial returns with the founding mission of ensuring that artificial general intelligence (AGI) benefits humanity 54. The conversion process required extensive negotiations with regulatory bodies, specifically the attorneys general of Delaware (Kathy Jennings) and California (Rob Bonta), who scrutinized the fair market valuation of the non-profit's assets and the preservation of its charitable mission 756. The conversion also faced and ultimately survived legal challenges from original co-founder Elon Musk, who sued to block the restructuring and made an unsuccessful $100 billion bid to acquire the non-profit 75.

Dissolution of the Capped-Profit Framework

The original OpenAI Limited Partnership (OpenAI LP) operated under an unusual charter where investor profits were capped 78. When Microsoft invested its initial $1 billion in 2019, followed by subsequent multi-billion dollar tranches, the returns on these investments were structurally limited 789. The transition to a standard Delaware C-Corporation erased this cap entirely, allowing Microsoft and other institutional investors to realize uncapped upside on their equity positions 3. This structural alignment was a prerequisite for accessing standard public equity markets, as standard public investors expect uncapped upside and governance rights compatible with Securities and Exchange Commission (SEC) requirements 3.

Equity Distribution and Dilution Mechanics

The restructuring established a new capitalization table that clarified the ownership stakes of major entities, which subsequently underwent significant dilution during pre-IPO capital raises.

Cap Table Restructuring

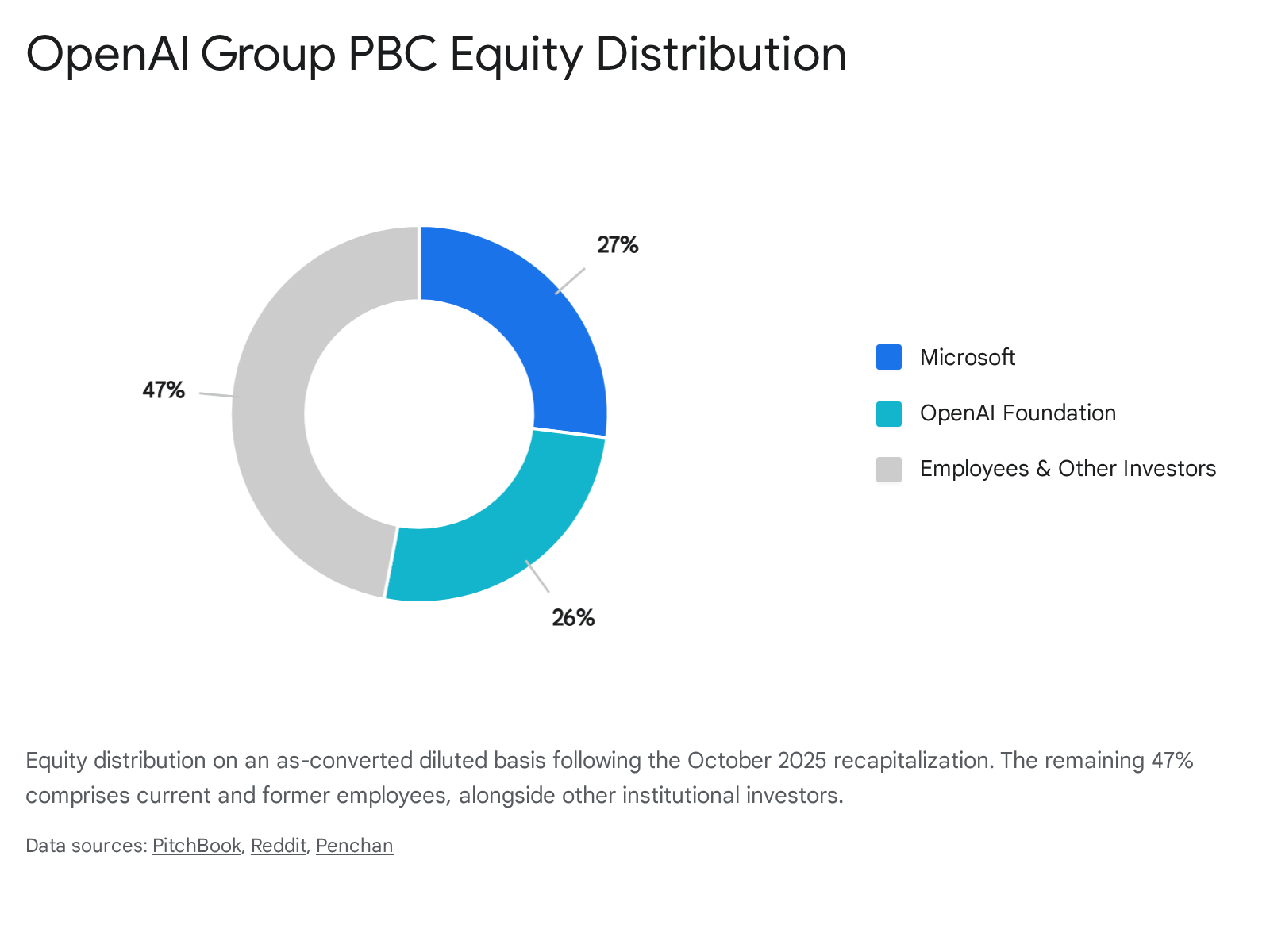

The late 2025 restructuring formalized the equity distribution at a $500 billion valuation 1310. The OpenAI Foundation received a 26% equity stake in the new for-profit entity, a position valued at approximately $130 billion at the time of the recapitalization 2211. Microsoft's stake, previously reported as 32.5% on an as-converted basis in the capped-profit subsidiary, was adjusted to approximately 27% on an as-converted diluted basis 21112.

The remaining 47% of the equity was distributed among current and former employees and a syndicate of external investors 21117.

This 26% stake held by the Foundation is intended to act as a permanent philanthropic endowment, with an initial commitment of $25 billion allocated toward global health initiatives and AI safety research 1613.

The 2026 Funding Round and Dilution

The capitalization structure faced immediate pressure and dilution during subsequent funding events. In early 2026, OpenAI closed a massive funding round that pushed its post-money valuation to $852 billion 314. This funding round, classified as a Series C, introduced substantial new capital from entities such as SoftBank, which committed approximately $64.6 billion for an 11.75% stake in the fully diluted cap table 1714. The round expanded the investor base to include Amazon, Nvidia, Coatue, Sequoia, and BlackRock-affiliated funds 1714.

While Microsoft's nominal share count remained static at an estimated 2.7 billion shares of as-converted common stock, the introduction of new Series C preferred shares inherently diluted the percentage ownership of earlier investors 1415.

| Shareholder Category | Reported Share Volume (Estimates) | Equity Class | Key Notes |

|---|---|---|---|

| Microsoft Corporation | 2,700,000,000 | Common Stock (As-Converted) | Principal cloud partner; stake initially valued at $135B 14. |

| OpenAI Foundation | 2,600,000,000 | Foundation Equity | Warrants included for future valuation multiples 614. |

| Current Employees (Pool) | 1,600,000,000 | Stock Options / RSUs | Vested and unvested tranches 14. |

| SoftBank Group Corp. | N/A (11.75% stake) | Series C Preferred | ~$64.6B commitment; anchor investor for data centers 14. |

| Sam Altman (CEO) | 0 | None / Pending | Anomalous 0% founder equity at the $852B valuation 14. |

Liquidation Preferences and Executive Compensation

The 2026 funding rounds included liquidation preferences designed to protect the principal of late-stage investors in downside exit scenarios 15. As OpenAI prepares for its IPO, the preferred stock held by these late-stage investors will automatically convert to standard Class A common stock 15.

Notably, leaked capitalization data from early 2026 indicated that CEO Sam Altman held a 0% ownership stake, labeled as "None/Pending" 14. While the transition to a C-Corp was partially intended to facilitate standard executive equity compensation mechanisms like Restricted Stock Units (RSUs), Altman's lack of immediate equity at the $852 billion valuation remains an anomaly in standard Silicon Valley corporate governance 314.

For Microsoft, the IPO represents a massive liquidity event. At the $852 billion valuation, Microsoft's converted stake commands an implied value exceeding $228 billion, representing a return of more than 17x on its estimated historical investment of roughly $13 billion 1617. Post-IPO lock-up periods notwithstanding, the conversion to freely tradable public equity provides Microsoft with a financial mechanism to systematically monetize its stake. Liquidating tranches of this equity could fund Microsoft's own vast capital expenditure requirements without necessitating debt issuance or pressuring its proprietary stock 17.

Revenue-Share Agreements and Financial Architecture

The financial architecture binding Microsoft and OpenAI extends beyond equity ownership into direct operational cash flows. The cornerstone of this relationship was a revenue-sharing agreement that dictated how the financial yields of OpenAI's commercialization were divided. In 2026, this agreement underwent a radical renegotiation that redefined the financial trajectory of both organizations.

The Capped-Profit Renegotiation of 2026

Under the terms established prior to the 2025 restructuring, OpenAI was obligated to remit 20% of its total revenue to Microsoft 1819. This ongoing royalty was intended to compensate Microsoft for its early capital risk and the provision of heavily subsidized Azure compute resources used to train the GPT foundational models 10. Initially, this payment structure had no absolute financial ceiling, extending indefinitely until the theoretical achievement of AGI 20.

In April 2026, the two companies executed a comprehensive amendment to this agreement. The revised contract maintained the 20% revenue share rate but imposed a hard aggregate cap of $38 billion on total payments from OpenAI to Microsoft, extending through the year 2030 182021. Furthermore, Microsoft agreed to terminate the reciprocal revenue share it previously paid to OpenAI for the resale of OpenAI models through the Azure OpenAI Service 2223.

| Contractual Element | Pre-April 2026 Structure | Post-April 2026 Structure |

|---|---|---|

| OpenAI Payments to Microsoft | 20% of ongoing revenue | 20% of revenue, hard cap at $38 billion total 20. |

| Duration of Payments | Indefinite until AGI verification | Fixed end date of 2030 19. |

| Microsoft Payments to OpenAI | Revenue share on Azure model sales | Terminated completely 2223. |

| Total Projected OpenAI Liability | Estimated up to $135 billion | Hard cap at $38 billion 18. |

This renegotiation acts as a massive financial catalyst for OpenAI. Internal financial projections indicated that the uncapped 20% royalty could have cost OpenAI up to $135 billion by 2030; the $38 billion cap therefore generates an estimated $97 billion in projected long-term savings for the AI developer 1820. By converting an open-ended, scaling liability into a fixed and predictable cost model, OpenAI vastly improved its unit economics and financial profile for prospective public market investors, smoothing the pathway for an IPO 2024.

Accelerated Cash Flow Implications

While the $38 billion cap structurally benefits OpenAI over the long term, the contract renegotiation included concessions that heavily benefit Microsoft's immediate operational cash flow. Prior agreements afforded OpenAI the option to defer portions of its revenue-share payments until 2032, a mechanism designed to help the rapidly scaling startup preserve operating capital 18.

The April 2026 amendment eliminated this deferral option entirely. Consequently, OpenAI is required to accelerate its cash payments, with projected remittances to Microsoft increasing from an originally estimated $4 billion to roughly $6 billion for the 2026 fiscal year 18. For Microsoft, this accelerates the realization of returns on its initial investments, converting a deferred asset into immediate liquid capital that can be reinvested into its own proprietary AI infrastructure buildouts 18.

Termination of the Artificial General Intelligence Clause

The most legally unorthodox mechanism in the historical Microsoft-OpenAI partnership was the "AGI Clause." Originally drafted to protect OpenAI's non-profit mission, the clause stipulated that if OpenAI achieved Artificial General Intelligence - defined broadly as a highly autonomous system that outperforms humans at most economically valuable work - Microsoft's access to the technology, its intellectual property licenses, and its revenue-share entitlements would be immediately terminated 72225.

The interpretation and execution of this clause became a severe point of friction. Initially, OpenAI's board held the unilateral authority to declare AGI, representing a catastrophic unquantified risk to Microsoft's core AI product strategy 922. In the October 2025 restructuring, the companies attempted to mitigate this by shifting the authority to declare AGI away from the board and delegating it to an independent expert panel 1222.

However, the April 2026 agreement erased the AGI clause entirely from the financial architecture. The $38 billion revenue share cap and the expiration dates of the agreements are now fixed to calendar dates (2030 and 2032) and operate completely independent of OpenAI's technological progress or any declaration of AGI 192223. This removal eliminates a massive asymmetric risk for Microsoft, ensuring that its financial returns and IP access cannot be suddenly revoked by a subjective technological milestone 1825.

Azure Dependency and Infrastructure Commitments

The foundation of the Microsoft-OpenAI alliance has historically been rooted in data center infrastructure. Microsoft's Azure cloud provided the massive computational resources required to train frontier models, while OpenAI's models drove unprecedented enterprise adoption of Azure services 326. The post-restructuring era introduces a recalibration of this dependency, balancing massive fixed commitments with newfound multi-cloud flexibility.

The Azure Consumption Contract

As part of the October 2025 restructuring, OpenAI committed to purchasing an incremental $250 billion in Azure cloud services over a multi-year period 121627. This consumption contract is staggering in scale, representing one of the largest single vendor commitments in the history of the technology sector.

For Microsoft, this $250 billion commitment acts as a critical de-risking mechanism for its own massive capital expenditures. Microsoft has rapidly expanded its data center footprint, with capital expenditures projected to exceed $40 billion in a single quarter by 2026 17. The guaranteed consumption from OpenAI provides Microsoft with multi-year visibility into Azure revenues, effectively underwriting the cost of building out what Microsoft executives refer to as a "planet-scale AI factory" 28.

Removal of Compute Exclusivity

In exchange for the $250 billion consumption guarantee and the revenue share adjustments, Microsoft relinquished its exclusive grip on OpenAI's infrastructure and distribution. Historically, Microsoft held a "right of first refusal" to serve as OpenAI's compute provider, and Azure was the exclusive cloud infrastructure for deploying OpenAI's commercial API 121623.

The April 2026 agreement dismantled this exclusivity 2223. OpenAI is now legally and contractually permitted to serve its full suite of products to customers across competing cloud platforms, including Amazon Web Services (AWS) and Google Cloud 2223. While Microsoft Azure remains OpenAI's "primary" cloud partner - with OpenAI products shipping first on Azure unless Microsoft chooses not to support them - the end of exclusivity allows OpenAI to meet enterprise customers where their data currently resides 222434.

This decoupling was an operational necessity for OpenAI ahead of an IPO. Enterprise customers operating in multi-cloud environments were historically hesitant to migrate highly secure, proprietary data entirely to Azure simply to access OpenAI models 23. By securing the freedom to deploy on AWS and Google Cloud, OpenAI vastly expanded its total addressable market 2329.

Project Stargate and Independent Data Centers

OpenAI's infrastructure strategy has evolved beyond renting traditional cloud capacity to directly shaping the physical data center landscape. The most prominent example of this strategy is "Project Stargate," a $500 billion joint venture announced in January 2025 involving OpenAI, Oracle, and SoftBank 303132.

Stargate aims to construct a network of massive AI data centers across the United States to secure the gigawatt-scale power required for training future frontier models 3031. While the project faced internal disputes regarding risk allocation and execution through early 2026, OpenAI successfully secured a $30 billion, 4.5-gigawatt capacity agreement directly with Oracle 3233.

| Stargate Project Location | Partner / Developer | Target Capacity / Status |

|---|---|---|

| Abilene, Texas | Oracle / Crusoe Energy | 500,000 sq ft facilities under construction; initial flagship site 3234. |

| Saline, Michigan | Oracle / Walbridge | 1-gigawatt campus ("The Barn"); ground broken in 2026 35. |

| Shackelford County, Texas | Oracle / SoftBank | Evaluating site integration with regional grid 36. |

| Doña Ana County, New Mexico | Oracle / SoftBank | Active site evaluation phase 36. |

| Lordstown, Ohio | SoftBank | Advanced data center design in pre-construction 36. |

The sheer scale of these developments has strained local resources, with states like Idaho and Utah advancing legislation to curb data center water usage, and local municipalities offering massive tax abatements (such as Abilene's 85% property tax reduction) to secure the construction jobs 43.

Microsoft's absence from the core Stargate consortium highlights the limits of the Azure partnership. While OpenAI will consume $250 billion in standard Azure compute, the capital requirements for next-generation gigawatt data centers exceed the risk tolerance of any single cloud provider 3137. OpenAI's willingness to partner with Oracle and SoftBank for these mega-projects demonstrates a strategic imperative to diversify its physical infrastructure supply chain away from total reliance on Microsoft 831.

Intellectual Property Rights and License Expiration

The transfer and licensing of intellectual property is the mechanism by which Microsoft translates its financial investment into product integration. The restructuring fundamentally altered the duration, scope, and exclusivity of these IP rights.

Non-Exclusive Licensing Through 2032

Under the revised agreements, Microsoft's license to utilize OpenAI's intellectual property for models and products was extended through the year 2032 122223. This ensures that Microsoft's core product suite - including Microsoft 365 Copilot, GitHub Copilot, and Bing - has guaranteed access to OpenAI's frontier models for the foreseeable future 38.

However, the nature of this license was downgraded from exclusive to non-exclusive 222325. Previously, Microsoft held an exclusive commercial license for OpenAI models, which served as a massive competitive moat against other enterprise software providers 3. The shift to a non-exclusive license permits OpenAI to directly license its technology to other enterprise software companies, hardware manufacturers, and cloud providers 23. This transition allows OpenAI to maximize the commercialization of its models, albeit at the cost of Microsoft's unique competitive differentiation 20.

Post-AGI Intellectual Property Contingencies

As noted, the removal of the AGI clause drastically changed the IP landscape. Previously, if AGI was achieved, Microsoft would theoretically lose access to the underlying IP 25. The October 2025 and April 2026 renegotiations secured Microsoft's IP rights to models and products through 2032, explicitly including "models post-AGI, with appropriate safety guardrails" 1216.

Furthermore, Microsoft secured specific rights to OpenAI's research IP - defined as the confidential methods used in the development of models and systems 12. These research rights remain active until 2030, or until an independent expert panel verifies the achievement of AGI, whichever occurs first 1234. Notably, the agreement expressly excludes Microsoft from accessing IP related to consumer hardware products, preserving OpenAI's optionality following its $6.5 billion acquisition of Jony Ive's hardware startup, io Products 1046.

This framework establishes a hard sunset for the technology transfer. After 2032, Microsoft will no longer have guaranteed, licensed access to OpenAI's frontier models. This expiration date is forcing Microsoft to rapidly build internal AI capabilities - such as its Phi family of small language models and the development of internal frontier models - to ensure platform continuity in the next decade 2647.

Product Cannibalization and Market Strategy

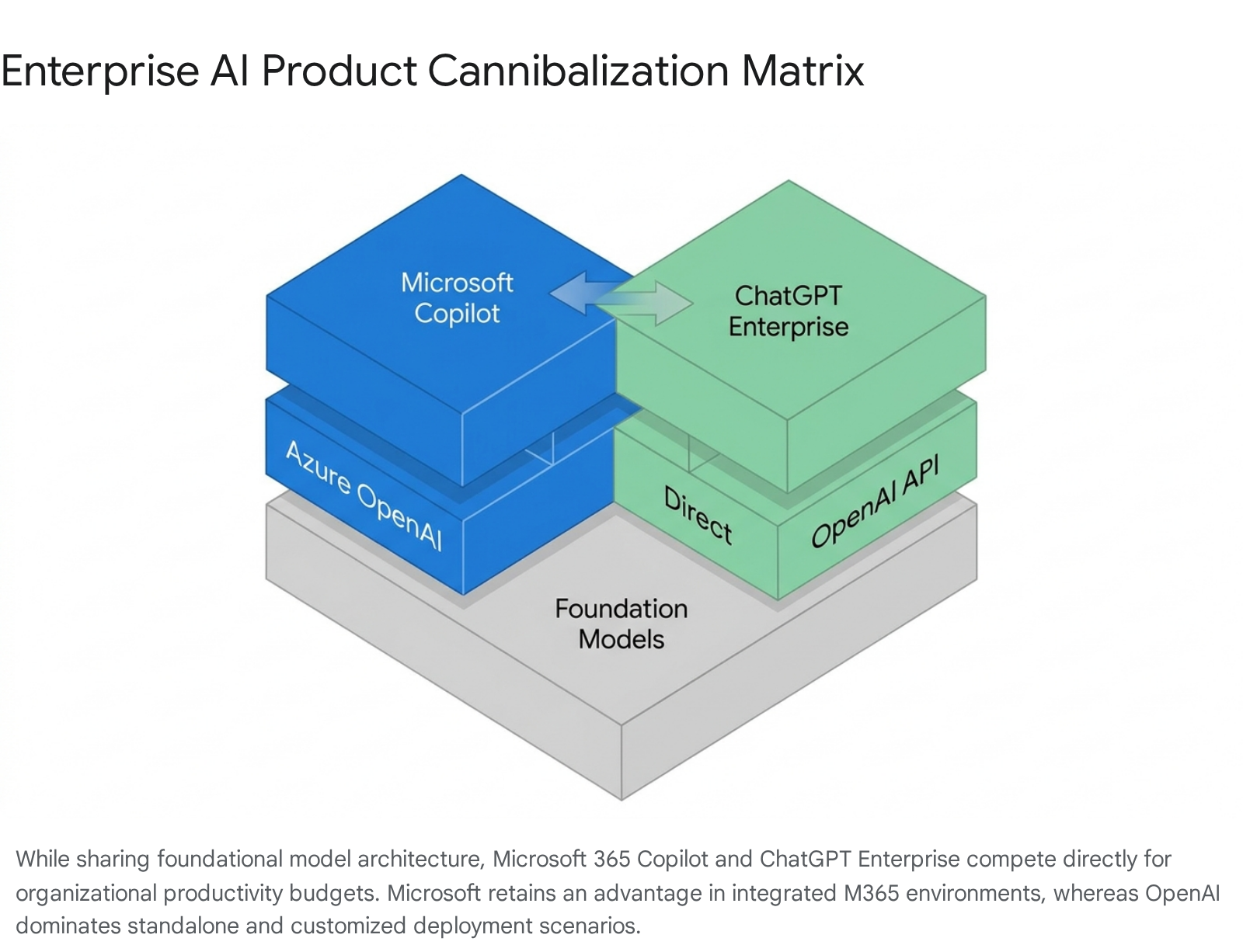

As OpenAI matures from an applied research lab into a commercial enterprise software company, the operational overlap between OpenAI and Microsoft has transformed the relationship from a pure partnership into what industry analysts term "coopetition." Both companies are aggressively targeting the same enterprise IT budgets, leading to distinct product cannibalization dynamics.

Microsoft Copilot Versus ChatGPT Enterprise

The most direct point of conflict lies in the deployment of end-user AI assistants. Microsoft is heavily pushing Microsoft 365 Copilot, an AI assistant deeply embedded within its existing productivity suite (Word, Excel, Teams, Outlook) 473940. Conversely, OpenAI is marketing ChatGPT Enterprise as a standalone, highly capable reasoning engine 5051.

While both platforms utilize the GPT-4 and GPT-5 class of foundational models, their value propositions differ radically based on their integration points 395241. Microsoft Copilot grounds its outputs in tenant data via the Microsoft Graph, whereas ChatGPT operates via an isolated chat interface that requires manual data provision or API integrations 505242.

Market pricing also diverges. Microsoft 365 Copilot requires an existing E3 or E5 license and charges an additional $30 per user, per month 5556. ChatGPT Enterprise relies on a standalone contract, typically pricing around $60 per user, per month, but providing access to more advanced functionalities such as the Code Interpreter for Python execution, Custom GPTs, the Canvas iterative workspace, and Sora video generation - features not natively available in standard Copilot deployments 40524156.

The market data indicates a bifurcated adoption strategy among large enterprises. Microsoft Copilot is favored for structured workflows where access to internal corporate data provides immediate context, such as summarizing Teams meetings or drafting Outlook responses 5057. However, for tasks requiring complex reasoning, deep research, arbitrary code execution, or specialized agent creation, enterprises favor ChatGPT Enterprise due to its superior user interface and immediate access to OpenAI's latest reasoning models (such as the o1 and o3 series) 4058.

Enterprise Data Governance and Security Frameworks

The divergence between the two products is most pronounced in data governance. For highly regulated industries, Microsoft Copilot presents a lower barrier to entry because it operates within the existing Microsoft 365 trust boundary 4360. Copilot automatically respects and enforces existing sensitivity labels, Azure Rights Management encryption, and Data Loss Prevention (DLP) policies configured by the organization's IT department 4361.

ChatGPT Enterprise, while SOC 2 compliant and guaranteeing that enterprise data is not used for foundational model training, operates in a separate OpenAI-managed environment 476062. Procuring ChatGPT Enterprise requires establishing a parallel governance framework, separate identity access management, and new auditing trails 5060.

However, Microsoft's tight integration carries inherent risks. Poorly configured permissions within Microsoft SharePoint can lead to Copilot surfacing sensitive organizational data to unauthorized users via the semantic index 5061. Consequently, OpenAI's isolated environment is sometimes viewed as a cleaner sandbox for exploratory enterprise AI workflows, bypassing the complexities of legacy IT permissions 60.

Orchestration and Custom Agent Infrastructure

Microsoft's strategic response to this cannibalization is to shift the battleground from raw model capability to enterprise orchestration. Through products like Copilot Studio, Microsoft is building the infrastructure for custom enterprise agents via low-code drag-and-drop interfaces 415763. Microsoft calculates that Chief Information Officers will prefer to build bespoke AI tools within their existing Azure identity and security perimeter rather than managing a fragmented ecosystem of standalone OpenAI applications 5763.

Regulatory Scrutiny and Antitrust Dynamics

The depth of the Microsoft-OpenAI integration inevitably triggered regulatory scrutiny across multiple global jurisdictions. Regulators recognized that traditional merger control frameworks were ill-equipped to handle massive financial investments masquerading as strategic partnerships, prompting investigations into whether Microsoft exercised "de facto control" over OpenAI's operations.

United Kingdom Competition and Markets Authority

In the United Kingdom, the Competition and Markets Authority (CMA) launched a formal investigation in December 2023 to determine if the partnership constituted a relevant merger situation under the Enterprise Act 2002 4445. The investigation focused on whether Microsoft's multi-billion dollar investments, combined with its exclusive Azure contracts, gave it control over OpenAI's commercial policy 4446.

In March 2025, after a 16-month inquiry overseen by CMA executives Joel Bamford and Sarah Cardell, the regulator concluded the investigation, determining that the partnership did not qualify for further merger review 44454748. The CMA acknowledged that Microsoft held "material influence" over OpenAI dating back to 2019 4448. However, the regulator found that this influence had not escalated to "de facto control" 4448.

Crucially, the CMA cited the recent evolution of the partnership - specifically, the negotiations that reduced OpenAI's compute reliance on Microsoft by opening the door to Oracle, and the end of Azure exclusivity - as a primary reason for clearing the arrangement 4448. By granting OpenAI the freedom to utilize competing cloud architectures, Microsoft effectively insulated the partnership from accusations of monopolistic infrastructure control 2344.

European Commission Investigations

The European Union approached the partnership through a markedly different regulatory lens. While the European Commission, under Executive Vice President Margrethe Vestager, similarly concluded that Microsoft had not acquired control over OpenAI on a lasting basis under the EU Merger Regulation, the regulator did not drop its scrutiny of the broader AI market dynamics 4950.

Instead, the Commission pivoted its investigation to focus on anti-competitive behavior and exclusivity clauses 4950. The EU sent formal information requests to investigate whether Microsoft leveraged its market power to block AI competitors from accessing essential resources or if it engaged in illegal tying and bundling practices 4950. The dissolution of the Azure exclusivity clause in April 2026 was highly correlated with the pressure of this ongoing European antitrust scrutiny 4950.

The European regulatory environment simultaneously penalized walled-garden approaches to AI integration across the sector. Following complaints from competitors like Slack and Alfaview, the Commission forced Microsoft into legally binding commitments to unbundle its Teams platform from its core Office 365 productivity suites in Europe 5152. In a parallel case involving consumer APIs in June 2026, the European Commission, led by Teresa Ribera, ordered Meta to reinstate free access to the WhatsApp Business API for rival AI assistants (including those from OpenAI and Microsoft), citing potential abuses of dominant market position 535455. This aggressive regulatory posture in the EU ensures that Microsoft cannot legally bind OpenAI into an exclusive software ecosystem without risking massive fines, reinforcing the necessity of the non-exclusive licensing agreements 5455.