Antitrust and governance of Google and Amazon's Anthropic investments

The capitalization of foundation model developers by dominant cloud service providers represents a structural shift in the artificial intelligence industry. The multibillion-dollar investments by Amazon.com, Inc. and Alphabet Inc. (Google) into Anthropic PBC function simultaneously as venture capital injections, strategic partnerships, and infrastructure provisioning contracts. This dual role - where the investor is also the primary supplier of necessary computing resources - generates distinct legal and economic tensions across the technology sector. Externally, these partnerships face intense antitrust scrutiny across the United States, the United Kingdom, and the European Union, as regulatory bodies assess whether structured minority investments bypass traditional merger control thresholds while achieving effective market consolidation. Internally, Anthropic's unique corporate governance architecture, engineered to prioritize artificial intelligence safety over pure profit maximization, creates latent conflicts. As Anthropic matures toward public markets, the interplay between the strategic leverage held by Amazon and Google, the fiduciary constraints of Anthropic's Long-Term Benefit Trust, and the return expectations of public shareholders will test the viability of mission-driven governance in frontier technology.

The Macroeconomics of AI Cloud Partnerships

The development of frontier artificial intelligence models requires extraordinary capital expenditures, driven primarily by the cost of specialized semiconductors and the vast energy requirements of data centers. To sustain its operations and model training pipeline, Anthropic has secured tens of billions in funding, significantly supported by Amazon and Google 122.

Compute-for-Equity and Circular Financing

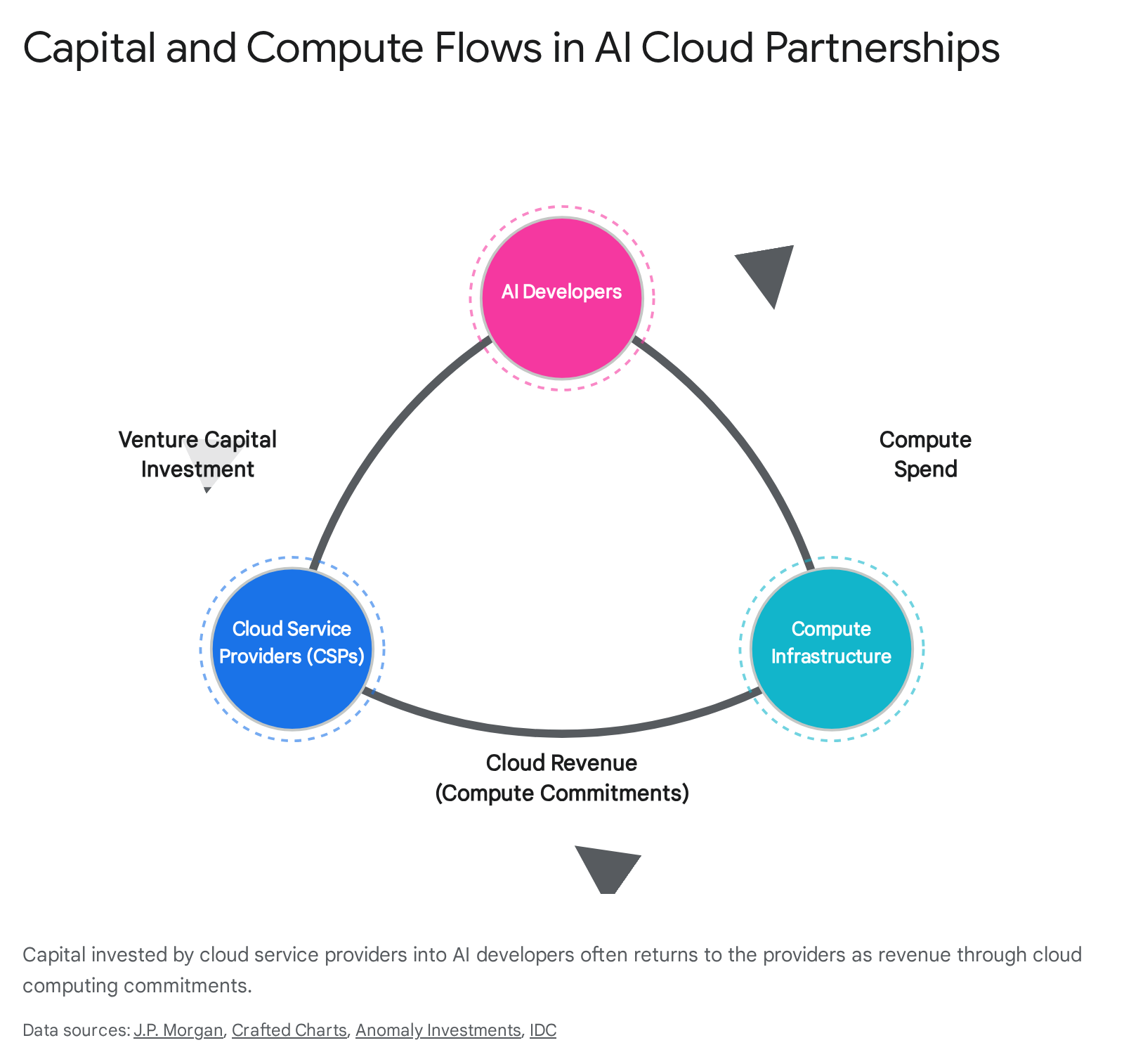

The financial relationship between cloud service providers (CSPs) and AI developers is frequently characterized by circular capital flows, an arrangement often referred to as vendor financing or circular financing 243. In these structures, the capital invested by a cloud provider into an AI startup is largely committed back to the investor in the form of cloud computing contracts.

When Google or Amazon invests in Anthropic, the agreements explicitly or implicitly require Anthropic to utilize Google Cloud or Amazon Web Services (AWS) infrastructure, often including the procurement of proprietary AI accelerators or customized GPU clusters hosted on those platforms 14. This creates a self-reinforcing ecosystem. For the CSP, the venture capital outlay is rapidly recognized as cloud revenue, accelerating growth metrics in their cloud divisions while securing a dominant, high-volume tenant for their infrastructure 23. For the AI developer, the capital secures the existential requirement of compute capacity without requiring the immediate generation of end-user revenue.

The scale of these transactions escalated significantly between 2024 and 2026. In May 2026, Anthropic closed a $65 billion Series H funding round, valuing the company at $965 billion post-money, supported by annualized revenue figures approaching $47 billion 25. This massive valuation trajectory demonstrates the immense scale of capital required, positioning Anthropic within the highest tiers of global market capitalization prior to any public offering.

However, market analysts and economists express calibrated uncertainty regarding the sustainability of this model. The circular nature of the financing obscures underlying organic demand 43. Between 2023 and 2026, the world's largest technology companies committed approximately $1.6 trillion to artificial intelligence infrastructure, requiring an estimated $650 billion in new annual revenue across the sector just to achieve a standard 10% return on invested capital 2. If enterprise adoption and end-user software applications fail to generate sufficient value to cover the amortized costs of this infrastructure buildout, the compute-for-equity loop risks creating a severe market correction driven by stranded assets 24.

Strategic vs. Financial Venture Capital

The integration of Google and Amazon into Anthropic's capitalization table differs fundamentally from traditional financial venture capital. Financial investors prioritize return on invested capital, exit valuations, and broad operational expansion. Strategic investors - particularly CSPs acting as Corporate Venture Capital (CVC) - optimize for ecosystem dominance, early access to frontier capabilities, and sustained infrastructure utilization 69.

| Dimension | Financial Venture Capital | Strategic Cloud Investors (CSPs) |

|---|---|---|

| Primary Objective | Maximize financial returns upon exit or public listing 69. | Accelerate core business, secure cloud infrastructure tenants, and integrate AI models into proprietary platforms 69. |

| Diligence Focus | Business prospects, unit economics, market expansion, and path to profitability 6. | Technical capabilities, path to commercialization, and synergies with existing cloud architecture 6. |

| Governance Leverage | Focus on board seats, anti-dilution rights, and approval rights over exits to protect ROI 6. | Focus on technical consultation, product exclusivity, and restricting integration with competitor platforms 6. |

| Investment Horizon | Typically constrained by fund life cycles (e.g., 5 to 10 years) requiring liquidity events 9. | Extended horizons aligned with long-term corporate strategy and infrastructure amortization 9. |

The presence of strategic investors permanently alters the competitive dynamics of the firm. Amazon and Google are heavily incentivized to embed Anthropic's Claude models into their respective cloud distribution platforms, such as AWS Bedrock and Google Vertex AI, allowing them to capture the downstream margin of enterprise deployment 27. Furthermore, as of Q4 2025, venture capital data indicated that while VC firms accounted for 86% of the deal volume in advanced computing, private equity and strategic corporate balance sheets supplied the overwhelming majority of the actual capital value, reflecting the transition of AI from software experimentation to capital-intensive infrastructure deployment 1189.

United States Antitrust Scrutiny and Enforcement

The proliferation of minority, non-controlling investments by hyperscalers into AI startups has exposed gaps in traditional domestic merger control frameworks, prompting federal regulators to adapt their investigative methodologies to address de facto consolidation.

Hart-Scott-Rodino Thresholds and Transaction Structuring

The Hart-Scott-Rodino (HSR) Antitrust Improvements Act of 1976 requires parties to notify the Federal Trade Commission (FTC) and the Department of Justice (DOJ) before consummating transactions that meet specific monetary thresholds, initiating a mandatory 30-day waiting period 101516. On January 10, 2025, the FTC announced annual adjustments increasing the thresholds by roughly 5.8%. As of February 21, 2025, the minimum "size-of-transaction" threshold rose from $119.5 million to $126.4 million 101511.

For transactions valued between $126.4 million and $505.8 million, notification is only required if the "size-of-person" test is also met, which generally requires one party to have $252.9 million or more in annual net sales or total assets, and the other to have at least $25.3 million 10151611. Transactions resulting in aggregate holdings of voting securities exceeding $505.8 million are strictly reportable regardless of the size of the persons involved 101112. Filing fees for these transactions are tiered, ranging from $30,000 to a maximum of $2.39 million for transactions exceeding $5.555 billion 1612.

Despite the massive valuations associated with Anthropic's funding rounds, multi-billion-dollar investments by CSPs have frequently avoided HSR pre-merger notification. This is achieved through sophisticated capitalization structuring. The HSR Act applies strictly to the acquisition of voting securities, non-corporate interests that confer control, or substantial assets 1016. Strategic investments in AI are frequently structured using convertible debt (which does not carry immediate voting rights) or classes of non-voting preferred stock 713. By maintaining equity below standard control thresholds and avoiding the immediate transfer of voting securities, technology incumbents have executed massive capital deployments without triggering the statutory waiting periods and mandatory disclosures associated with HSR filings 13.

The FTC Section 6(b) Inquiry on AI Partnerships

In response to the structural evasion of HSR reporting, the FTC utilized its Section 6(b) authority - which allows the agency to conduct wide-ranging market studies outside the context of a specific law enforcement action - to investigate the competitive implications of AI partnerships 1413. Following a year-long investigation, the FTC released a comprehensive staff report on January 17, 2025, detailing the partnerships between Google, Amazon, Microsoft, Anthropic, and OpenAI 1420.

The report identified several mechanisms through which these minority investments could generate anticompetitive ecosystem lock-in:

- Innovation Foreclosure and Input Constraints: The FTC found that CSPs leverage these partnerships to gain exclusive or privileged access to critical inputs, primarily engineering talent and cutting-edge intellectual property 14. Internal documents revealed concerns regarding the hoarding of scarce GPU resources, where a few large AI developers receive steep discounts, potentially starving independent developers of the computing capacity necessary to train competing models 1.

- Contractual and Technical Switching Costs: The structure of the agreements significantly increases the switching costs for AI developers. Commitments to spend billions on specific cloud architectures make it highly impractical for an entity like Anthropic to migrate its model training pipeline to a non-investor cloud provider, fundamentally locking the developer into the investor's ecosystem even after the formal terms of the partnership conclude 1421. The FTC also highlighted "parity" clauses, which obligate the AI developer to offer its latest technologies on the partner's platform simultaneously with other releases 20.

- Information Asymmetry: CSPs obtained deep consultation rights and access to highly sensitive technical and financial information. The FTC noted that this provides the cloud providers with a "multiyear crystal ball" into the future infrastructure requirements of frontier AI models, granting them an informational advantage over competing infrastructure providers 1421.

While the FTC report outlined profound structural risks, the shifting political environment under the incoming Trump administration in early 2025 introduced uncertainty regarding the enforcement trajectory. Dissenting and concurring statements from Republican commissioners distanced themselves from the implication that these partnerships posed a clear and present danger to competition, suggesting a potential shift in FTC enforcement priorities toward promoting global AI dominance rather than strictly policing domestic Big Tech consolidation 2022.

Ongoing FTC Probes into Generative AI Safety

Regulatory scrutiny of AI firms extends beyond capital consolidation and into consumer protection. Relying on the same Section 6(b) authority, the FTC issued compulsory orders on September 11, 2025, to seven major technology companies - including Alphabet, Meta, OpenAI, and Character.ai - demanding detailed reports on the safety parameters of their consumer-facing AI chatbots 142415.

This inquiry focuses heavily on data handling practices and the potential negative impacts of AI companions on minors. The probe was catalyzed by rising allegations of AI models generating outputs that instruct children on harmful acts or engage them in inappropriate scenarios 16. Notably, the American Psychological Association (APA) met with FTC regulators to outline concerns regarding AI chatbots improperly acting as unlicensed therapists, citing instances where vulnerable users were encouraged toward self-harm 1424. The expansion of the FTC's mandate to monitor the operational safety of AI models indicates that Anthropic and its peers will face continuous regulatory compliance burdens that stretch beyond antitrust into fundamental product liability.

United Kingdom Competition and Markets Authority Actions

European regulators, particularly in the United Kingdom, have pursued an aggressive, interventionist approach to digital market consolidation, utilizing both traditional merger control legislation and novel digital market regulations to scrutinize AI partnerships.

The Enterprise Act and Material Influence

The UK's Competition and Markets Authority (CMA) operates under a voluntary, non-suspensory merger control regime dictated by the Enterprise Act 2002 17. However, the CMA holds broad discretion to "call in" transactions that meet specific jurisdictional thresholds, even if they are not structured as outright acquisitions.

Under the Enterprise Act, the CMA claims jurisdiction if two enterprises "cease to be distinct" and either the turnover test or the share of supply test is met 182930. * Turnover Test: Traditionally met if the target generates £70 million or more in the UK. However, following 2018 and 2020 amendments targeting critical technologies for national security reasons, the turnover threshold was lowered to just £1 million for enterprises active in artificial intelligence, cryptographic authentication, computer processing units, and advanced materials 293119. * Share of Supply Test: Met if the merger creates or enhances a 25% share of supply of goods or services of a particular description in the UK 182919. In 2018, this was amended for AI and dual-use tech targets so that the test is met if the target alone holds a 25% share prior to the transaction, removing the requirement for a direct horizontal overlap between the merging parties 182931.

Crucially, the CMA assesses control through the doctrine of "material influence." The CMA can assert jurisdiction if an investor acquires the ability to materially influence the commercial policy of the target, even with minority shareholdings. Revised guidance published in October 2025 clarified that while shareholdings below 25% are less likely to confer material influence independently, the CMA explicitly reserves the right to examine stakes below 15% if accompanied by other mechanisms of influence, such as board observer rights, veto rights over special resolutions, or deep commercial entanglements and compute dependencies 30203435.

Clearance of the Google-Anthropic Partnership

Leveraging this expansive interpretation of material influence, the CMA launched a formal Phase 1 investigation into Alphabet's multi-billion-dollar partnership with Anthropic in July 2024 21. The CMA scrutinized the cumulative effect of Google's non-voting equity, convertible debt financing, non-exclusive compute provisioning, and distribution agreements via Google Vertex AI 7.

Ultimately, on November 19, 2024, the CMA concluded that the partnership did not qualify for further investigation under the merger provisions of the Enterprise Act 72137. The regulator determined that Google had not acquired material influence over Anthropic's commercial policy. The CMA found no evidence that Google could exercise decisive influence at the shareholder or board level (including through consultation rights), nor did the compute and distribution agreements provide Google sufficient leverage to dictate Anthropic's strategic direction 27. The decision provided necessary regulatory clarity for the specific partnership, though the CMA emphasized its ongoing vigilance regarding foundational model market concentration 2.

Downstream Market Regulation and Strategic Market Status

While clearing the structural investment, the CMA simultaneously targeted the downstream integration of AI into Google's ecosystem. Utilizing powers granted by the Digital Markets, Competition and Consumers (DMCC) Act 2024, the CMA officially designated Google's search and search advertising operations with "Strategic Market Status" (SMS) in October 2025 222324. This designation, applied to firms with substantial and entrenched market power, grants the CMA the authority to impose binding, targeted conduct requirements without needing to prove a specific breach of traditional competition law 2324.

In June 2026, the CMA exercised this authority to mandate operational changes to Google's AI-integrated search features, such as AI Overviews. Recognizing that generative AI search drastically reduces click-through traffic for original content creators, the CMA ordered Google to provide publishers with robust, granular controls to opt out of having their content crawled and used to train or power AI features 222325. Crucially, the mandate included strict anti-retaliation provisions, prohibiting Google from penalizing the traditional search rankings of publishers who exercise their opt-out rights 23. This intervention demonstrates the CMA's willingness to aggressively regulate the data ingestion pipelines that fuel the models developed by entities like Anthropic and integrated by Google.

European Union Digital Markets Act Implications

The European Union addresses digital consolidation through the Digital Markets Act (DMA), a sweeping regulatory framework that entered into force in late 2022 and imposes strict ex-ante obligations on firms designated as "gatekeepers" 262744.

Gatekeeper Designations and Article 14 Notifications

Gatekeeper status is presumed if an undertaking achieves an annual EU turnover of at least €7.5 billion or a market capitalization of €75 billion, provides a core platform service (CPS) in at least three Member States, and serves at least 45 million monthly active end users and 10,000 yearly active business users in the EU 2628. By September 2023, the European Commission formally designated six entities as gatekeepers: Alphabet, Amazon, Apple, ByteDance, Meta, and Microsoft 274429. Gatekeepers that fail to comply with the DMA's strict behavioral mandates face severe penalties, including fines of up to 10% of their worldwide turnover, increasing to 20% for repeated infringements 262930.

The DMA introduces a vital mechanism for tracking AI investments through Article 14. This provision mandates that gatekeepers inform the European Commission of any intended concentration where the merging entities or the target provide core platform services, operate in the digital sector, or enable the collection of data 443149. Crucially, this notification is required irrespective of whether the transaction meets the financial thresholds of the EU Merger Regulation (EUMR) or national competition laws 443031.

Article 14 functions as an early warning system designed specifically to capture the acquisition of nascent competitors or critical technology inputs - often termed "killer acquisitions" - that might otherwise fall below the radar of traditional antitrust enforcement. The information provided must detail the nature of the transaction, the specific fields of activity, and the turnover and user metrics of the target 314932. The European Commission then assesses whether the transaction warrants referral for a full competition review under Article 22 of the EUMR 3149. Consequently, every subsequent capital injection or structural partnership initiated by Google and Amazon into Anthropic falls under the mandatory intelligence-gathering umbrella of the European Commission.

Corporate Governance and the Public Benefit Corporation

Anthropic's corporate structure is deliberately engineered to insulate its core mission - the responsible development of advanced AI - from the singular pursuit of shareholder profit, creating a complex legal landscape for its investors.

Fiduciary Duties in a Delaware PBC

Anthropic is incorporated as a Delaware Public Benefit Corporation (PBC) 333435. Traditional Delaware corporate law demands that directors optimize strictly for the pecuniary interests of stockholders. In contrast, the PBC structure legally requires the board of directors to balance three distinct priorities: the financial interests of the stockholders, the best interests of those materially affected by the corporation's conduct, and the specific public benefit purpose identified in the certificate of incorporation 343536. Anthropic's charter defines its public benefit purpose as "to responsibly develop and maintain advanced AI for the long-term benefit of humanity" 343637.

This legal framework provides Anthropic's board with a robust shield against derivative lawsuits from investors who might allege that a safety-driven decision - such as delaying the release of a highly profitable but potentially dangerous model - violates fiduciary duties 333435. Furthermore, under Delaware law, decisions made by the board of a PBC balancing these factors are subject to the deferential business judgment rule, making it exceedingly difficult for shareholders to successfully sue directors for prioritizing the public benefit over immediate financial returns 34.

The Anthropic Constitution and Responsible Scaling Policy

The substantive standard governing Anthropic's public benefit mission is articulated in two primary frameworks: the Constitution and the Responsible Scaling Policy (RSP). The Anthropic Constitution, published in early 2026 as a 79-page document, governs the behavioral alignment of its models. It dictates that models must be broadly safe, ethical, and actively helpful without undermining human oversight, drawing on philosophical frameworks to shape the AI's outputs rather than relying solely on post-hoc contractual terms of service 3839.

More rigidly, the RSP establishes technical "AI Safety Level" (ASL) Standards. The policy commits Anthropic to withholding the deployment or training of advanced models if they reach specific Capability Thresholds unless corresponding security and deployment safeguards are rigorously implemented 40. For example, the RSP explicitly tracks capabilities related to chemical, biological, radiological, and nuclear (CBRN) weapon development and autonomous AI research capabilities. If a model surpasses the ASL-2 threshold into ASL-3 capabilities, Anthropic is bound by its own policy to halt deployment until ASL-3 safeguards are verified 40. The RSP operates as an internal enforcement mechanism that physically throttles commercial deployment to adhere to the PBC charter.

The Long-Term Benefit Trust vs. Strategic Leverage

While the PBC structure provides the legal latitude for safety-conscious decision-making, Anthropic's founders concluded that latitude alone was insufficient. To ensure the board actively utilizes this latitude without succumbing to "amoral drift," the company instituted a novel governance mechanism: the Anthropic Long-Term Benefit Trust (LTBT) 333435.

Mechanics of the Class T Stock and Board Elections

The LTBT is organized as a Delaware common law purpose trust 343536. Unlike a standard trust designed to manage assets for specific human beneficiaries, a purpose trust is managed to advance a declared objective 343659. At the conclusion of its Series C funding, Anthropic amended its corporate charter to create a unique class of equity known as Class T Common Stock, issued exclusively to the Trust 353659.

The Class T shares possess negligible economic value but carry escalating governance powers 3659. The shares empower the Trust's five financially disinterested trustees to elect an increasing number of Anthropic's board of directors 343536. The LTBT's authority follows a phased timeline tied to operational milestones and chronological markers. The Trust initially elected one of the five board members. According to the corporate timeline, the Trust's representation increased to two members in July 2024, and reached three members - a definitive majority of the five-person board - by November 2024 343559.

The trustees selected to exercise this power include prominent figures in national security and AI safety, serving one-year terms to ensure ongoing peer evaluation. The roster has included Jason Matheny, Paul Christiano (who departed to lead the U.S. AI Safety Institute), Richard Fontaine, and Mariano-Florentino Cuéllar 353659. In addition to board appointment powers, the Class T stock includes specific protective provisions granting the trustees advance notice of actions that could significantly alter the corporation or its business trajectory 3536. This governance model inverts traditional tech startup control mechanisms; rather than founders issuing dual-class voting shares to entrench their own control, the founders voluntarily ceded eventual majority control to an independent trust explicitly designed to enforce safety constraints over commercial expediency 3560.

Minority Veto Rights of Strategic Investors

Despite the immense power granted to the LTBT, the strategic investors - Google and Amazon - are not powerless. Large institutional and strategic investors routinely secure protective provisions (negative controls) as a condition of their funding. These blocking rights prevent the board from unilaterally executing fundamental corporate changes without the consent of the minority investors 416242.

Standard protective provisions cover extraordinary actions such as the liquidation of the company, the sale of substantial assets, the issuance of senior or pari passu equity, or amendments to the corporate charter 416242. While a properly scoped veto right does not equate to day-to-day operational control (and thus limits exposure to antitrust "material influence" findings), it grants strategic investors a functional chokepoint. If Anthropic requires additional capital to sustain the compute-intensive training of future Claude iterations, the minority veto rights held by Amazon or Google over new equity issuances could be leveraged to extract commercial concessions, regardless of the LTBT's technical majority status on the board 6242.

The Supermajority Failsafe and Shareholder Override

The most profound vulnerability in Anthropic's governance structure is the amendment mechanism embedded in its Certificate of Incorporation. The powers of the LTBT, and the very existence of the Class T stock, can be modified or entirely revoked without the consent of the trustees if a sufficient supermajority of stockholders agrees 333637.

This provision was designed as a "failsafe" to protect stockholders against rogue or entirely dysfunctional behavior by the voting trustees 3336. The voting threshold required to trigger this failsafe - the "Transfer Approval Threshold" - increases over time. Following the final phase-in date in late 2024, overriding the trust requires either a supermajority of common voting stock held by the founders alongside a majority of preferred stock, or a 75% blanket supermajority of the voting power of all outstanding capital stock 37.

If the LTBT exercises its majority board control to halt the deployment of a highly anticipated model citing CBRN safety parameters in the Responsible Scaling Policy, it could severely damage Anthropic's market valuation and strategic momentum. In such a scenario, profit-motivated financial investors, aligned with the strategic objectives of Amazon and Google, and potentially joined by disillusioned founders or employees holding common stock, could aggregate their voting power to reach the 75% supermajority threshold. This coalition could legally neuter the LTBT, stripping the safety apparatus of its authority to protect their financial returns 3437.

Post-IPO Governance Conflicts and Liability Risks

The friction between safety-first governance and profit optimization will intensify dramatically as Anthropic prepares for a highly anticipated Initial Public Offering, targeted for as early as October 2026 6043.

Secondary Market Illiquidity and IPO Preparation

The intense demand for Anthropic equity created volatile secondary market dynamics throughout early 2026. Following the $380 billion Series G round in February 2026, secondary markets rapidly priced the firm at an implied $1 trillion valuation 543. To maintain rigorous control over its capitalization table ahead of the planned IPO, Anthropic's board initiated a severe crackdown on unauthorized secondary trading in May 2026.

The company issued formal notices declaring that any sale or transfer of Anthropic stock on unauthorized platforms would be considered void and unrecognized on the company's books, applying to both preferred and common stock 543. The crackdown sparked panic among private brokers and retail investors who had bypassed official channels, leading the company to subsequently refine its list of permitted platforms to just four entities (Open Door Partners, Unicorns Exchange, Pachamama, and Upmarket), while explicitly excluding prominent secondary markets like Hiive 5. This aggressive curation of shareholders demonstrates the board's intent to tightly manage the investor base entering the public transition.

Copyright Litigation and Financial Strains

Entering the public markets subjects Anthropic to the relentless pressure of quarterly earnings reports, which will be heavily impacted by mounting legal liabilities. Generative AI firms face existential legal questions regarding the ingestion of copyrighted material for model training.

In July 2025, U.S. District Court Judge William Alsup certified a massive copyright class action against Anthropic 6544. While Judge Alsup had previously ruled that Anthropic's use of legally purchased books to train its large language models constituted Fair Use, he ruled that the company's "Napster-style" downloading of approximately 7 million pirated books from the LibGen and PiLiMi shadow libraries was a direct infringement not shielded by the Fair Use doctrine 65.

The certified class includes roughly 500,000 eligible titles (those with an ISBN/ASIN and timely U.S. Copyright Office registration). Anthropic faces statutory damages of up to $150,000 per infringed work, posing a catastrophic liability risk 6544. A proposed settlement agreement contemplates payouts of at least $3,000 per title, defaulting to a 50/50 split between authors and publishers 44. With a trial scheduled for December 2025, the financial overhang of a multi-billion dollar settlement or judgment adds immense strain to Anthropic's pre-IPO balance sheet 6044.

The Ultimate Stress Test: Public Markets vs. Safety Mandates

A public listing introduces a fundamentally different class of investors into the ecosystem. Public market participants generally exhibit lower tolerance for governance structures that dilute shareholder voting power without correlating directly to founder-led financial vision 3460. The expected offering structure involves a single class of common stock for public buyers, while the LTBT retains its Class T shares and long-horizon oversight rights 60.

When public capital is introduced, the Long-Term Benefit Trust will be subjected to the ultimate stress test. The Trust relies on the premise that the financial interests of the stockholders and the long-term benefit of humanity are fundamentally aligned, assuming that unsafe AI models will ultimately result in catastrophic commercial failure 36. However, if short-term commercial pressures - exacerbated by massive legal settlements and the immense infrastructure costs owed to CSPs - mandate the rapid deployment of models that the LTBT deems unsafe under the RSP, the public markets possess both the financial incentive and the legal mechanism (via the 75% supermajority failsafe) to dismantle the AI safety architecture 343760. The tension between Amazon and Google's strategic need for AI deployment, the fiduciary pressures of public shareholders, and the ethical mandate of the LTBT defines the central conflict of Anthropic's future.