FAFSA vs CSS Profile: Do You Need to Submit Both

The Free Application for Federal Student Aid (FAFSA) is a universally required, free federal form that unlocks government-funded grants and student loans. In contrast, the College Scholarship Service (CSS) Profile is a supplemental, fee-based application used by approximately 250 highly selective colleges to distribute their own private institutional endowments. While the FAFSA utilizes a simplified formula to assess basic income and assets, the CSS Profile demands a highly detailed audit of a family's financial life, including primary home equity and noncustodial parent income, making both applications essential for students targeting competitive universities.

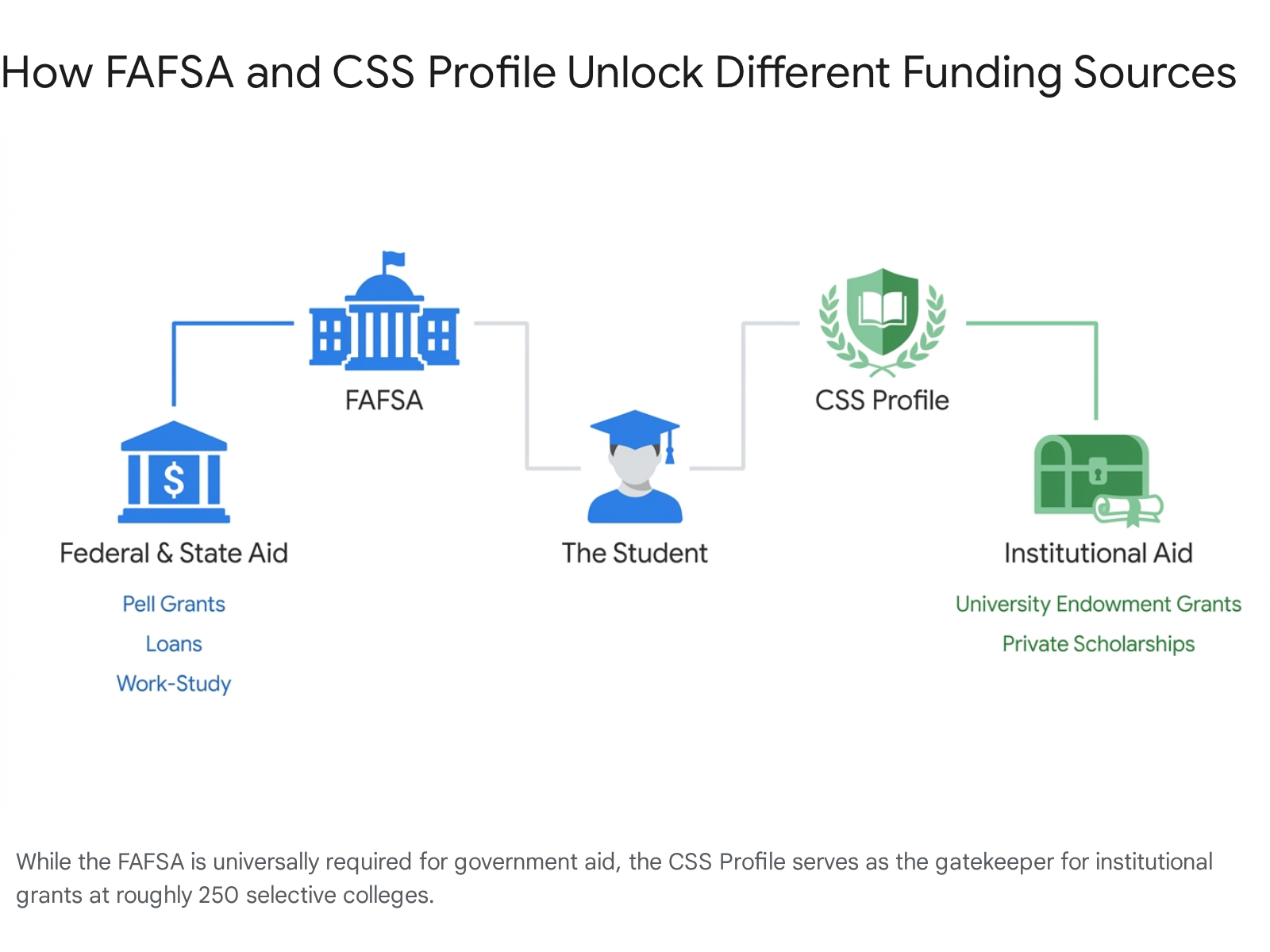

The Fundamental Divide: Federal vs. Institutional Aid

Navigating the landscape of higher education financing requires an understanding of the two primary mechanisms that assess a family's ability to pay: the FAFSA and the CSS Profile. While both applications attempt to measure financial strength, they serve entirely different entities, rely on distinct mathematical methodologies, and unlock separate pools of capital 12.

The FAFSA is administered by the U.S. Department of Education. Its fundamental purpose is to calculate a student's Student Aid Index (SAI), which replaced the Expected Family Contribution (EFC) in recent legislative updates 34. The SAI acts as a standardized federal metric that determines a student's eligibility for federal funds, most notably Pell Grants, federal direct subsidized and unsubsidized loans, and the federal work-study program 145. The FAFSA is universally accepted and serves as a mandatory prerequisite for almost every accredited degree-granting institution in the United States 15. Furthermore, state governments heavily rely on FAFSA data to distribute state-level grants and scholarships 16.

The CSS Profile, conversely, is a proprietary application administered by the College Board, the private organization responsible for the SAT and Advanced Placement (AP) examinations 678. It is currently utilized by roughly 250 to 300 institutions 5910. The institutions that mandate the CSS Profile are predominantly highly selective, well-endowed private colleges (such as Harvard, Yale, Stanford, and the Massachusetts Institute of Technology) alongside a select group of prestigious public flagships (including the University of Virginia, the University of Michigan, and the University of North Carolina at Chapel Hill) 5910.

Because these selective institutions are distributing their own institutional funds rather than taxpayer dollars, they require a significantly more granular view of a family's financial circumstances than the federal government requires 111. The CSS Profile uses an Institutional Methodology (IM) rather than the Federal Methodology (FM) used by the FAFSA 2512. This Institutional Methodology is explicitly designed to capture complex financial structures, illiquid wealth, and deeper financial capacity that the simplified FAFSA formula intentionally excludes 5.

Feature-by-Feature Structural Comparison

To understand how these applications diverge in practice, a direct comparison of their features and requirements illuminates the structural differences between federal and institutional aid philosophies.

| Feature Area | FAFSA (Free Application for Federal Student Aid) | CSS Profile (College Scholarship Service) |

|---|---|---|

| Administering Body | U.S. Department of Education | The College Board |

| Financial Cost | Always free of charge 1214. | $25 initial fee; $16 per additional school (waivers apply) 71215. |

| Institutional Adoption | Nearly all accredited U.S. higher education institutions 15. | Approximately 250 to 300 highly selective institutions and scholarship programs 5910. |

| Funds Unlocked | Federal aid (Pell Grants, federal loans, work-study) and state-level grants 124. | Non-federal institutional aid, university grants, and private scholarships 124. |

| Methodology Used | Federal Methodology (Calculates Student Aid Index / SAI) 512. | Institutional Methodology (Customizable by each participating college) 512. |

| Primary Home Equity | Strictly excluded from asset calculations 1314. | Generally required and assessed, though individual colleges may apply income-based caps 131516. |

| Divorced / Separated Parents | Requires financial data only from the parent who provided the most financial support over the past year 311. | Typically requires comprehensive data from both the Custodial Parent and the Noncustodial Parent 61317. |

| Sibling Discount | Eliminated. No adjustment is made for families with multiple children enrolled in college simultaneously 318. | Retained. The formula actively adjusts expectations downward when multiple siblings are enrolled in college 3419. |

| Small Businesses & Farms | Excluded for businesses with 100 or fewer employees and family-resided farms (starting 2026-2027) 202126. | Included. Families must report the full net worth and underlying assets of small businesses and farms 61013. |

| Medical Expenses | Excluded from the standard formula 22. | Frequently considered to lower the family's expected contribution 61022. |

Who Actually Needs to File Both Applications?

A critical strategic decision for college applicants involves determining which forms are necessary. If an applicant is targeting community colleges, regional public universities, or less selective private institutions, the FAFSA is generally the only financial aid application required 59. Public university systems overwhelmingly rely on the FAFSA to disburse state-funded financial aid and federal allocations. Because state schools typically operate with different funding mandates and lower tuition bases than elite private schools, they rarely possess the endowment structures required to offer their own highly customized need-based grants 9.

Conversely, if an applicant's list includes the Ivy League, elite liberal arts colleges, or highly selective private research universities, filing the CSS Profile is virtually mandatory 79. Even students applying to top-tier public flagships such as the University of Virginia, the University of North Carolina at Chapel Hill, and the University of Michigan must submit the CSS Profile to be considered for specific institutional aid programs 51028.

The Illusion of Sticker Price for Middle-Income Families

A persistent myth deters many middle-income families from applying to CSS Profile institutions. Because selective private colleges routinely feature "sticker prices" that approach or exceed $80,000 to $100,000 per academic year, many families assume these schools are financially inaccessible 23. Consequently, they avoid the CSS Profile altogether under the mistaken belief that their moderate income disqualifies them from meaningful aid.

Financial aid experts stress that avoiding these institutions is a significant strategic error 523. While CSS Profile schools maintain high published tuition rates, they also control the largest institutional endowments in the country 511. These schools utilize the detailed data from the CSS Profile to ensure their grant money targets families with demonstrated need.

Because the CSS Profile accounts for regional cost of living, extraordinary medical expenses, and the costs of supporting multiple dependents, middle-class families frequently receive massive institutional grants at these schools 19. In many scenarios, a student's net out-of-pocket cost to attend a private Ivy League or elite liberal arts college is actually lower than the cost of attending an in-state, FAFSA-only public university 1119. Families must not assume that the CSS Profile inherently yields a worse financial outcome simply because it demands more rigorous documentation.

Assessing Financial Strength: Competing Methodologies

The reason identical families can receive vastly different financial aid assessments stems from the conflicting methodologies used by the two applications 1224. The federal government relies on a broad, generalized formula designed for mass processing. In contrast, institutions using the CSS Profile seek a holistic understanding of a family's true net worth, intentionally digging into areas that the FAFSA ignores 511.

The Return of the Sibling Discount

Historically, the federal financial aid formula recognized the immense burden of paying for multiple college tuitions simultaneously. If a family had two children in college, their expected contribution was essentially divided in half. However, recent sweeping changes to the FAFSA - enacted through the FAFSA Simplification Act - entirely eliminated this "sibling discount" 18. Under the new Federal Methodology, a family with one child in college and a family with three children in college appear mathematically identical in terms of their calculated Student Aid Index, severely reducing aid eligibility for families with overlapping college enrollments 318.

The CSS Profile, however, deliberately retained the sibling discount in its Institutional Methodology 34. Private institutions recognize that a family's disposable income drops precipitously when supporting multiple undergraduates. Therefore, families with more than one child in college often find that CSS Profile schools offer vastly superior institutional aid packages, directly counteracting the federal government's removal of the sibling benefit 3519.

Primary Home Equity Assessments

The most heavily debated variance between the two forms is the treatment of a family's primary residence.

The FAFSA entirely shields primary home equity. Families are not required to report the value of the home they live in, ensuring that real estate appreciation does not penalize their federal aid eligibility 1314.

The CSS Profile explicitly targets primary home equity. The application requires families to report the purchase year, purchase price, current market value, and the outstanding mortgage balance of their primary residence 141631. Because real estate values in certain markets have surged, many middle-income families appear incredibly wealthy on paper despite lacking liquid cash - a phenomenon known as being "house rich but cash poor" 1631.

If a college assessed 100% of a family's home equity at the standard 5% institutional assessment rate, the family's expected contribution could skyrocket, potentially forcing them to take out high-interest home equity loans simply to pay tuition 141531. Recognizing this danger, CSS Profile institutions handle home equity through varied institutional policies:

- Income-Based Caps: The most common approach is to cap the assessable home equity based on a multiplier of the parents' income 141516. For example, many colleges cap home equity at 1.2 times or 2.0 times the family's adjusted gross income 1415. If a family earns $100,000 annually but possesses $500,000 in home equity, a college with a 1.2x cap will only count $120,000 of that equity as an available asset, protecting the remaining $380,000 15.

- Full Assessment: A smaller contingent of schools believes home equity is a liquid asset and assesses 100% of the reported value without any caps 1516.

- Complete Exclusion: Certain elite institutions, including Stanford University, Harvard University, and the University of Chicago, choose to ignore home equity entirely, mimicking the FAFSA approach to maintain affordability for middle-class homeowners in expensive coastal markets 1523.

Because each CSS Profile school applies its own proprietary formula, a family's expected contribution can swing by tens of thousands of dollars depending solely on which college is processing the application 1624.

Small Businesses and Family Farms

For families who own small businesses or agricultural properties, the 2026-2027 academic year brings a massive policy reversal on the FAFSA. Previous simplification efforts had mandated that all families report the net worth of their small businesses and farms as available assets, which devastated financial aid for agricultural and entrepreneurial households 2032.

Following widespread backlash, the One Big Beautiful Bill Act (OBBBA) successfully reversed this policy for the 2026-2027 award year 2032. The FAFSA once again explicitly excludes the net worth of small businesses (defined as family-owned operations with 100 or fewer full-time equivalent employees), family farms upon which the family resides, and family-controlled commercial fisheries 202126.

The CSS Profile offers no such exemptions. Institutions using the CSS Profile demand comprehensive reporting on the net worth, equipment, inventory, and real estate holdings of all family businesses and farms, regardless of employee headcount 61013. Business owners must be prepared to submit detailed tax schedules to support their CSS Profile applications.

Retirement Accounts and Medical Expenses

A prevalent anxiety among parents is that colleges expect them to liquidate their 401(k) retirement portfolios to fund their children's education. Fortunately, neither the FAFSA nor the CSS Profile counts the actual balance of recognized, qualified retirement accounts (such as 401(k)s, 403(b)s, IRAs, and pension funds) as available assets 1325.

Historically, the FAFSA penalized families by adding their prior-year retirement contributions back into their total income, artificially inflating their perceived financial strength 1325. Recent updates to the FAFSA calculation have largely eliminated this penalty, meaning contributions to workplace retirement plans are no longer uniformly added back to the Student Aid Index 3.

The CSS Profile does require families to report their total retirement account balances 111325. While this alarms many parents, financial aid officers generally do not factor these balances into the institutional need formula 132425. Instead, colleges collect this data to ensure the family's broader financial narrative is coherent and that wealth is not being inappropriately hidden in non-standard financial vehicles.

Additionally, the CSS Profile differs from the FAFSA by allowing families to report extenuating expenses. While the FAFSA ignores high living costs, the CSS Profile actively collects data on out-of-pocket medical and dental expenses, eldercare costs, and the expense of sending younger siblings to private K-12 schools 101922.

Navigating Divorce: The Noncustodial Parent Profile

For students from divorced or separated households, the FAFSA and the CSS Profile utilize conflicting definitions of parental responsibility, severely altering aid outcomes.

The FAFSA operates on a simplified metric: a dependent student is only required to report the income and assets of the single parent who provided the most financial support during the previous 12 months 3611. If the parents provide exactly equal support, the FAFSA mandates using the data of the parent with the higher income 3. The financial profile of the noncustodial parent is entirely ignored by the federal government 11.

The CSS Profile fundamentally assumes that both biological or adoptive parents bear a lifelong financial obligation to fund a student's higher education, regardless of legal custody agreements, alimony arrangements, or explicit divorce decrees stating otherwise 17. To enforce this philosophy, the vast majority of CSS Profile institutions require the noncustodial parent to complete a parallel application known as the Noncustodial Parent Profile 132627. The college then aggregates the financial strength of both households to determine the student's institutional aid package 6.

Petitioning for a Noncustodial Parent Waiver

The requirement to provide noncustodial financial data creates severe logistical and emotional hurdles for families dealing with absent, uncooperative, or estranged parents. The CSS Profile system does not automatically account for these fractures; students must actively petition each individual college for a Noncustodial Parent Waiver 172829.

Colleges review waiver requests with extreme scrutiny. Waivers are never granted simply because a noncustodial parent refuses to complete the form, refuses to pay for college, or points to a divorce decree exempting them from educational expenses 2930.

To successfully obtain a waiver, applicants must typically prove exceptional circumstances, which generally fall into three categories: 1. Documented Abuse: A verifiable history of domestic violence or abuse involving the student and the noncustodial parent 2839. 2. Legal Restrictions: Active court orders, such as restraining orders, that legally prohibit the noncustodial parent from contacting the student 2839. 3. Total Abandonment: A significant, documented history of zero contact and zero financial support spanning multiple years 172840.

The burden of proof relies on a formal waiver request form, a detailed personal statement outlining the history of the estrangement, and mandatory third-party documentation 28293039. Colleges require corroborating letters from objective professionals who have direct knowledge of the family dynamic, such as high school guidance counselors, social workers, clergy members, or therapists 282931. Letters written by family members, family friends, or divorce attorneys are explicitly rejected by most financial aid offices 282930.

Each college adjudicates the waiver request independently; a student may have their waiver approved by one university and denied by another 172830. If denied, the college will expect the noncustodial parent's financial contribution, potentially jeopardizing the student's ability to afford the institution 1739.

Application Logistics: Costs, Deadlines, and Fee Waivers

The logistical pathways for submitting the FAFSA and the CSS Profile differ heavily in terms of financial cost, system architecture, and deadlines.

The FAFSA, staying true to its name, is universally free to submit 1214. The CSS Profile, however, imposes a financial burden on applicants. The College Board charges a $25 initial application fee, which includes the cost of processing and transmitting the report to a single institution. Every additional institution requested by the student incurs an extra $16 fee 71415. A student applying to ten selective CSS Profile colleges would face a bill of $169 15. Furthermore, if a noncustodial parent is required to file, they are charged a flat, one-time fee of $25, regardless of the number of schools receiving the data 42.

Qualifying for CSS Fee Waivers

To prevent these fees from deterring low- and middle-income applicants, the College Board issues automatic fee waivers for domestic undergraduate students who meet specific criteria 912. An applicant qualifies for an unlimited number of CSS Profile submissions at zero cost if they meet any of the following conditions: * The student's family Adjusted Gross Income (AGI) is $100,000 or less 153233. * The student qualified for an SAT fee waiver during high school 273233. * The student is an orphan or a ward of the court and is under the age of 24 273233.

When a student qualifies for a fee waiver, their noncustodial parent also receives a fee waiver, provided the noncustodial household's AGI also falls below the $100,000 threshold 942. Eligibility is determined automatically within the application portal based on the data entered 1534. International students generally do not qualify for automatic fee waivers and must seek alternative arrangements directly with their target colleges 91542.

Navigating Deadlines

Financial aid deadlines require meticulous tracking, as missing a submission window can result in the total loss of institutional or state funding.

Both the FAFSA and the CSS Profile traditionally open on October 1st for the upcoming academic year 36946. Following technical delays in previous years, the U.S. Department of Education confirmed the return to the standard October 1st launch for the 2026-2027 cycle, accompanied by early beta testing periods 64635.

While the absolute federal deadline to submit the FAFSA is June 30th at the end of the academic year, relying on the federal deadline is a critical error 646. State governments distribute their localized financial aid on a strict, first-come, first-served basis 4636.

| State / Program | FAFSA Deadline for 2026-2027 Cycle | Priority Rule |

|---|---|---|

| California (Cal Grant) | March 2, 2026 | Strict postmarked deadline 37. |

| New York | June 30, 2027 | Matches federal deadline 37. |

| North Carolina (UNC System) | June 1, 2026 | Priority consideration 637. |

| Alaska (Education Grant) | ASAP after Oct 1, 2025 | Awards made until funds deplete 637. |

| Nevada (Opportunity Grant) | ASAP after Oct 1, 2025 | Awards made until funds deplete 37. |

CSS Profile deadlines are entirely dictated by the individual colleges and typically align with admissions deadlines 922. For students applying Early Decision or Early Action, CSS Profile deadlines frequently fall in early to mid-November 910. Regular Decision deadlines typically cluster in January or February 910. Following the submission of the CSS Profile, many colleges utilize the Institutional Documentation Service (IDOC) to securely collect uploaded copies of the family's federal tax returns and W-2s, ensuring the data submitted matches official IRS records 926.

Removing Barriers: FSA ID Updates for Contributors Without an SSN

A historically severe bottleneck in the FAFSA process impacted mixed-status families where a parent (designated as a "contributor") did not possess a Social Security Number (SSN) 50. Because the FAFSA mandates digital signatures from all contributors, parents without SSNs previously had to navigate a complex, manual identity validation process via a dedicated government email address, leading to massive delays and application failures 5051.

For the 2026-2027 FAFSA cycle, the U.S. Department of Education entirely overhauled this system to improve accessibility. The manual email validation process has been paused 5051. Now, contributors without an SSN can create their StudentAid.gov accounts (FSA IDs) by completing a built-in digital attestation and certification directly on the website 505138.

If manual validation is triggered, the Department has massively expanded the list of acceptable identity documents. Where previously fewer than 10 documents were accepted, the list now includes over 30 options, permitting the use of foreign passports, Consular ID cards (Matricula Consular), U.S. Border Crossing Cards, and municipal identification 505138. This ensures that all contributors can securely sign the application and consent to the FUTURE Act Direct Data Exchange (FA-DDX), which pulls relevant tax data directly from the IRS 503839.

2026-2027 FAFSA Updates: The One Big Beautiful Bill Act

Students applying for the 2026-2027 academic year face a fundamentally altered federal financial aid landscape. On July 4, 2025, the "One Big Beautiful Bill Act" (OBBBA) was signed into law, initiating sweeping structural changes to Pell Grants, federal loan limits, and repayment options that officially take effect on July 1, 2026 20544041.

The legislation is designed to aggressively curtail long-term federal student debt by restricting borrowing capacity, which will force many families to reevaluate how they cover tuition gaps 4258.

Sweeping Changes to Federal Borrowing Limits

The OBBBA implements stringent new caps on federal borrowing that dismantle the previous unlimited lending structures.

Under prior regulations, the Parent PLUS Loan allowed parents of dependent undergraduates to borrow up to the full Cost of Attendance, minus any other financial aid received 43. Beginning July 1, 2026, Parent PLUS loans are strictly capped. Parents may now only borrow a maximum of $20,000 per academic year per dependent student, with a hard lifetime aggregate limit of $65,000 per student 42444546. These limits are combined, meaning if two parents attempt to borrow separately for the same child, their combined borrowing cannot exceed the $20,000 annual cap 46.

The Graduate PLUS Loan program, which allowed graduate and professional students to borrow up to their full cost of attendance, has been entirely eliminated for new borrowers 54424445. Graduate students are now restricted exclusively to Direct Unsubsidized Loans, which feature strict caps: $20,500 annually and a $100,000 aggregate lifetime limit 54424447. Certain professional programs allow up to $50,000 annually with a $200,000 lifetime limit 544245.

Furthermore, the OBBBA institutes a universal lifetime federal loan limit. Independent students and graduate borrowers now face a combined lifetime borrowing cap of $257,500 across all federal direct loans 544244.

Legacy Provisions for Current Borrowers

To prevent the sudden disruption of education for students already enrolled, the legislation includes critical legacy provisions 434548.

If a student is actively enrolled in an academic program as of June 30, 2026, and they (or their parents) received a federal loan disbursement for that specific program prior to July 1, 2026, they are grandfathered into the previous borrowing rules 434648. These legacy borrowers may continue to access Graduate PLUS or unlimited Parent PLUS loans for up to three academic years (through June 30, 2029) or until they complete their current degree program, whichever comes first 40434446.

However, transferring to a different university, switching academic programs, or taking a formal leave of absence immediately voids this legacy status, permanently subjecting the borrower to the new, restrictive limits 4348.

Loan Proration and Less-Than-Full-Time Enrollment

Historically, students enrolled at least half-time were eligible to receive their full annual federal loan limits. The OBBBA abolishes this flexibility by implementing a strict "schedule of reduction" for part-time enrollees 434546.

Effective July 1, 2026, federal loan eligibility is intrinsically tied to a 24-credit annual benchmark (12 credits per semester to be considered full-time) 4041. If a student enrolls in fewer than 12 credits in a semester, the university is legally required to prorate and reduce their federal loan disbursement in direct proportion to their missing credits 41434546. If a student drops a class mid-semester, the financial aid office must actively recall and reduce the previously disbursed loan funds to match the new enrollment intensity 414346.

Pell Grant Caps, Cutoffs, and Expansions

The Federal Pell Grant system - the largest source of need-based gift aid - undergoes simultaneous restriction and expansion under the OBBBA.

For the 2026-2027 award year, the U.S. Department of Education has fixed the maximum scheduled Pell Grant at $7,395, with a statutory minimum award of $740 496650.

However, eligibility for these funds is now governed by aggressive new disqualification rules:

- The SAI Hard Cutoff: The OBBBA introduces a strict eligibility cliff. Students with an Student Aid Index (SAI) of $14,790 or higher are entirely disqualified from receiving a Pell Grant, regardless of other financial factors. This represents a hard ceiling where an SAI equal to or greater than twice the maximum Pell Grant amount ($7,395) results in zero aid 20406650. The only exception is for dependents of deceased servicemembers and public safety officers 406650.

- The Full-Ride Penalty: Students who receive non-federal grants or institutional scholarships that cover 100% of their Cost of Attendance (COA) are explicitly disqualified from receiving a federal Pell Grant 20215440. Previously, students could use Pell funds to cover living expenses even if a scholarship covered tuition and board; this is no longer permitted 2021.

- Foreign Income Inclusion: In a specialized but highly impactful change, the foreign earned income exclusion reported on federal taxes is now added back into the family's Adjusted Gross Income (AGI) when determining Pell eligibility 21404466. This modification will likely disqualify many expatriate families from federal aid 2144.

Simultaneously, the OBBBA expands the Pell Grant's reach by launching "Workforce Pell" eligibility 544258. Beginning in 2026, Pell Grants can be utilized to fund approved short-term, career-focused certificate programs and workforce development pathways, extending federal support beyond traditional two- and four-year degree programs 544258.

Bottom line

The FAFSA and the CSS Profile serve fundamentally different purposes in the college financing ecosystem. The FAFSA is a free, universally required gateway to federal grants and strictly capped government loans, relying on a simplified formula that protects home equity and small businesses. In contrast, the CSS Profile is a rigorous, fee-based application used by elite institutions to distribute massive private endowments, requiring deep audits of illiquid wealth, medical expenses, and noncustodial parent incomes. As the 2026-2027 academic year introduces sweeping federal changes under the One Big Beautiful Bill Act - including strict $14,790 SAI cutoffs for Pell Grants and hard caps on Parent PLUS borrowing - families must diligently file both applications on time to maximize their access to both government safety nets and institutional generosity.