Market Opportunities for Alternative AI Accelerators

Executive Summary

The global artificial intelligence hardware landscape of 2026 represents a profound structural departure from the monolithic GPU dominance that characterized the early generative AI boom. Driven by the exponential scaling of inference workloads, the maturation of hardware-agnostic compiler abstractions, and the strategic weaponization of semiconductor supply chains, the market has officially entered a multi-polar era. Nvidia's historical monopoly, anchored by its proprietary Compute Unified Device Architecture (CUDA) and formidable merchant silicon, is facing sophisticated circumvention across all layers of the technology stack.

This comprehensive analysis examines the macro- and micro-economic forces redefining AI compute. At the software layer, the proliferation of PyTorch 2.0 and OpenAI's Triton is actively eroding the CUDA moat, enabling seamless model deployment across heterogeneous hardware environments. At the architectural layer, novel designs such as Cerebras Systems' wafer-scale integration and Groq's deterministic dataflow - recently absorbed into Nvidia's own portfolio via a landmark $20 billion asset acquisition - are resolving the memory bandwidth bottlenecks inherent to High Bandwidth Memory (HBM) architectures. Financially, the impending Cerebras Initial Public Offering (IPO) tests the public market's appetite for vertically integrated, capital-intensive infrastructure providers, especially when measured against the stratospheric valuation multiples of fabless peers like Arm, Astera Labs, and Broadcom.

Concurrently, geopolitical friction has birthed a sprawling "Sovereign AI" market, projected to reach $301.6 billion by 2040, as nation-states aggressively mandate localized data residency and indigenous compute clusters. In the East, despite stringent United States export controls, Huawei's Ascend architecture is achieving highly viable cluster-scale performance, forcing a global reevaluation of the efficacy of semiconductor embargoes.

The Paradigm Shift: From Training Monopolies to Inference Economics

The initial AI infrastructure buildout was overwhelmingly characterized by the deployment of massive training clusters. However, market demand and the Total Addressable Market (TAM) have rapidly inverted, shifting the economic epicenter of artificial intelligence from model creation to model deployment.

The Diverging Economics of Training versus Inference

The economic profiles of model training and model inference are fundamentally distinct, requiring vastly different infrastructural approaches. Training is a batch-oriented, latency-insensitive process that demands colossal inter-chip bandwidth to process vast datasets over weeks or months 12. An enterprise might spend tens of millions of dollars to train a frontier model, representing a massive but occasional fixed capital expenditure. Inference, conversely, is a continuous, volume-driven, and highly latency-sensitive operational expense 23. Every chatbot query, automated enterprise decision, and real-time generation constitutes an inference event 13.

By 2026, inference workloads account for roughly 66% of all AI compute, an increase from one-third in 2023, with projections indicating a rise to 80% of total AI critical IT load capacity by 2030 12. Research from SemiAnalysis and Gartner corroborates this shift, predicting that 55% of AI-optimized Infrastructure-as-a-Service (IaaS) spending will support inference in 2026, reaching over 65% by 2029 23. Furthermore, the AI inference market is projected to grow from $106 billion in 2025 to $255 billion by 2030, reflecting a 19.2% compound annual growth rate 2.

According to Stanford's 2025 AI Index, inference costs have plummeted from $20.00 to $0.07 per million tokens 2. Yet, the sheer volume of global queries ensures that inference still comprises 80% to 90% of the lifetime operational cost of a production AI system 2. The financial imperative for data center operators is no longer strictly peak petaflops, but inference efficiency measured in cost-per-million-tokens and tokens-per-watt. At a hyperscale level, processing 1,000 tokens per second on a general-purpose GPU drawing 700 watts yields highly unfavorable unit economics compared to specialized application-specific integrated circuits (ASICs) 24.

Deployment Bifurcation: Hyperscale Data Centers versus Edge Computing

The shift from training to inference has deeply bifurcated physical hardware deployment, creating two distinct infrastructure ecosystems: the hyperscale mega-campus and the localized edge.

Mega-Clusters and Industrial Infrastructure Constraints

Training facilities are rapidly scaling into mega-campuses drawing between 100 megawatts and upwards of 1 gigawatt of power 1. Because training is latency-insensitive, these facilities are constructed wherever power and land are cheapest, regardless of proximity to population centers 1. Inference facilities, however, must target sub-50 millisecond response times to service consumer applications, requiring placement in premium urban locations with diverse fiber connectivity and strict uptime Service Level Agreements (SLAs) 1.

Operating these facilities introduces severe physical constraints. Establishing 100 MW mega-clusters requires exhaustive environmental and thermal engineering. Within these secure facilities, mitigating the thermal output of high-density racks (such as Cerebras' 27kW nodes or Nvidia NVL72 racks) is paramount. Facility managers increasingly rely on stringent industrial testing methodologies. For example, standards mirroring the ASTM E741 test methods for tracer gas dilution are critically adapted to model volumetric air changes and HVAC flow rates in enclosed data center hot-aisles 2. Furthermore, security mandates absolute uptime, requiring robust localized power generation. These sprawling backup generator farms rely on highly specific industrial components - such as Cummins Q1321 high-precision temperature sensors - to monitor critical thermal tolerances during grid disconnections 6. Such dependencies illustrate a profound reality: AI infrastructure scaling cannot be achieved through silicon alone; it requires mastering the underlying thermodynamic and industrial supply chains.

The Expansion of Edge AI

Simultaneously, the edge computing market is exploding, projected to grow from $168.4 billion in 2025 to $249 billion by 2030, with the Edge AI sub-segment expanding from $20.78 billion to $66.47 billion 7. Running optimized, quantized inference models on localized edge devices bypasses data center transit entirely 3.

By 2025, 75% of enterprise-generated data was projected to remain at or near the source 7. Silicon providers like Apple (Neural Engine), Google (Tensor), and Qualcomm are embedding sophisticated inference accelerators directly into consumer hardware 3. This trend delivers ultra-low latency, drastically reduces cloud bandwidth costs, and aligns with stringent data sovereignty and privacy mandates by enabling on-device training adaptation without uploading permanent records to the cloud 3.

The Erosion of NVIDIA's CUDA Moat: Software Abstractions

Nvidia's absolute dominance over the AI ecosystem has historically relied less on sheer silicon fabrication advantages than on the inescapable gravity of its software stack. For nearly two decades, deploying optimal deep learning models required low-level CUDA C++ programming 834. Developers were forced to manually manage thread indices, negotiate shared memory bank conflicts, and write warp-level primitives with precise register layout requirements 8. The switching cost to alternative architectures required total codebase rewrites, creating a self-reinforcing monopoly 4.

By 2026, this software lock-in has been profoundly weakened by the maturation of hardware-agnostic compiler stacks, most notably PyTorch 2.0 and OpenAI's Triton.

OpenAI Triton and the Compiler Abstraction

OpenAI's Triton has evolved from an experimental project introduced in 2021 into the default kernel layer for modern machine learning execution 811. With the release of PyTorch 2.0, the torch.compile function utilizes the Inductor backend to default to Triton code generation, rendering the underlying hardware architecture largely opaque to the end developer 8312.

Triton operates as a tiled-loop compiler where compute logic is written at the tile level in pure Python 83. The compiler automatically handles thread block layout, shared memory allocation, and hardware-specific instruction selection, translating the input into an LLVM intermediate representation before generating optimized PTX (Parallel Thread Execution) or CUBIN for Nvidia, or equivalent low-level instructions for AMD 83. This paradigm shift eliminates the need for C++ kernel development. Complex operations like FlashAttention, custom activations, and memory-efficient matrix multiplications are now entirely scripted in Python 8.

As engineering teams migrate to these Pythonic abstractions, strict code quality and linting standards have become paramount in kernel development. For instance, strict adherence to PEP-8 and the avoidance of ambiguous variable naming (enforced by the Python standard E741 rule regarding the letters 'l', 'O', or 'I') ensures that collaborative, open-source Triton kernels remain legible and free from transcription errors during complex mathematical compilations 56. While automated web-scrapers sometimes mistakenly index terms like E741 or Q1321 as AI valuation frameworks, in practice, they strictly denote the operational and syntactical infrastructure metrics required to scale AI development safely 266.

The strategic implications of Triton are staggering. As long as a hardware vendor writes an efficient Triton backend, their silicon instantly inherits compatibility with the vast PyTorch ecosystem 12. This has drastically reduced the barrier to entry for hyperscaler ASICs and bespoke inference chips. The purchasing decision has transitioned away from software compatibility and squarely toward raw economic metrics: performance-per-watt and cost-per-token 412.

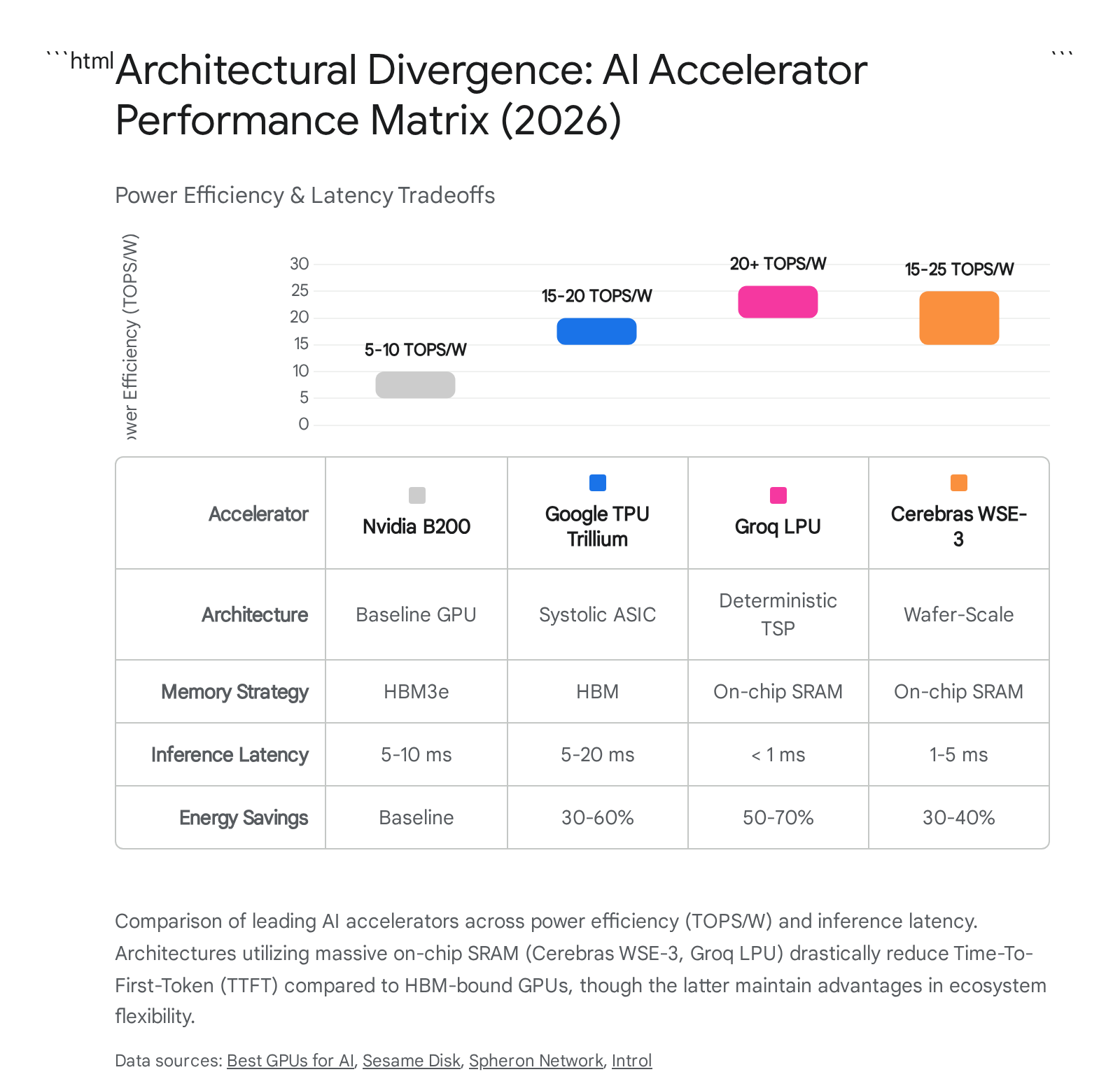

Architectural Divergence: The Non-GPU Matrix

Because inference is fundamentally bottlenecked by memory bandwidth rather than raw compute logic, traditional GPU architectures are inherently inefficient for autoregressive token generation. During the decode phase of a Large Language Model (LLM), the entire weight matrix and KV cache must be streamed from High Bandwidth Memory (HBM) to the compute cores for every single token 4717. The $3.35 \text{ TB/s}$ to $4.8 \text{ TB/s}$ limits of HBM3e impose a strict ceiling on Time-to-First-Token (TTFT) and total throughput 417. Alternative silicon architectures have emerged specifically to bypass this "memory wall."

The Cerebras Wafer-Scale Engine (WSE-3)

Cerebras Systems represents the most radical departure from traditional chip fabrication. Rather than dicing a 300mm silicon wafer into individual dies, Cerebras utilizes the entire wafer as a single monolithic processor 181920. The third-generation Wafer-Scale Engine (WSE-3), manufactured on TSMC's 5nm process, integrates 4 trillion transistors, 900,000 AI-optimized cores, and crucially, 44 GB of on-chip Static Random Access Memory (SRAM) 19202122.

By storing an entire 40-billion parameter model directly on-chip in SRAM, the WSE-3 achieves an internal memory bandwidth of $21 \text{ PB/s}$ 72123. This entirely eliminates the latency of off-chip HBM shuttling 7. For inference, the Cerebras CS-3 system can deliver over 2,500 to 3,000 tokens per second on models like Llama 3 70B and gpt-oss-120B, achieving TTFTs of 80-150ms 717. Furthermore, the decoupling of memory in the broader CS-3 architecture allows external memory scaling up to $1,200 \text{ TB}$, enabling the training of models with up to 24 trillion parameters without the complex pipeline and tensor parallelism scheduling required by Nvidia multi-GPU clusters 218.

The tradeoff is massive infrastructure customization; a single CS-3 node draws 15-27 kW, requiring specialized power delivery and cooling mechanisms far beyond standard data center racks 725. However, it achieves 3x higher compute-per-watt than an 8-GPU DGX system 7.

Groq's LPU and the $20B Nvidia Consolidation

Groq approached the memory bottleneck by designing a deterministic Language Processing Unit (LPU) based on a Tensor Streaming Processor (TSP) architecture 181920. The LPU features a single, wide pipeline of functional units executing operations in lock-step, paired with 230 MB to 500 MB of on-chip SRAM 41820. Because execution is entirely compiler-scheduled and deterministic, hardware control overhead is minimized, yielding TTFTs under 100ms and inference speeds up to 10x faster than GPUs at a fraction of the energy cost 171920. The LPU achieves roughly 150 TB/s in memory bandwidth - 45x more memory-bandwidth-capable per chip than an H100 SXM 4.

However, the industry landscape was upended in December 2025 when Nvidia executed a $20 billion "reverse acquihire" of Groq 92728. Structured to circumvent protracted Hart-Scott-Rodino (HSR) antitrust scrutiny, Nvidia licensed Groq's IP and absorbed its engineering leadership (including founder Jonathan Ross) while leaving a nominal cloud entity independent 272810.

The strategic rationale articulated by Nvidia CEO Jensen Huang at GTC 2026 was profound: Groq's LPU does not replace the GPU; it completes it 9. While Nvidia's NVLink 72 dominates standard batch workloads, extreme token generation (1,000+ tokens per second) limits out memory bandwidth 9. By integrating Groq LPUs alongside the upcoming Vera Rubin GPU architecture, Nvidia creates a hybrid rack that delegates bulk training to the GPU and ultra-fast, SRAM-bound decode inference to the LPU, achieving up to 35x better tokens-per-watt than Blackwell alone 928.

Hyperscaler ASICs and Ultra-Specialized Silicon

Cloud hyperscalers have aggressively deployed proprietary silicon to reduce capital dependence on merchant vendors. Google's 6th-generation TPU, Trillium, and the subsequent 7th-generation Ironwood, utilize advanced systolic arrays and specialized matrix multiply units 303132. Ironwood is estimated to deliver 4,614 TFLOPS per chip, operating at 60-65% higher energy efficiency than equivalent GPUs, making it a formidable internal alternative for Google Cloud tenants 32. Similarly, AWS has deployed over 500,000 Trainium2 chips - and the subsequent Trainium3 with 144GB HBM3e and 2.52 PFLOPS FP8 - primarily to service Anthropic's massive training workloads, representing the largest non-Nvidia AI cluster in production 32.

At the extreme end of specialization, startups like Taalas and Etched have abandoned general-purpose flexibility entirely. Taalas' HC1 chip hardwires specific models (like Llama 3.1 8B) directly into the silicon logic via "mask ROM recall fabric," achieving an unprecedented 17,000 tokens per second per user with zero HBM bottleneck 19. Etched's Sohu chip is a transformer-only ASIC that claims over 62,500 tokens per second per chip on Llama 70B by removing all hardware logic unnecessary for transformer operations 19.

Technical Architecture Comparison

To synthesize the capabilities of these disparate systems, the following matrix standardizes vendor claims against real-world deployment parameters observed in mid-2026.

| Accelerator Platform | Architecture Type | Memory Strategy | Peak Inference Throughput (Estimated Tokens/s) | Power Efficiency (TOPS/W) | Latency (TTFT) | Target Workload Profile |

|---|---|---|---|---|---|---|

| NVIDIA B200 | General GPU | 192GB HBM3E | ~353 (Llama 70B) | 5 - 10 | 5 - 10 ms | Flexible, universal compute, training-heavy workloads. |

| Google TPU v6 (Trillium) | Systolic ASIC | HBM / Matrix Units | Varies by cluster | 15 - 20 | 5 - 20 ms | Cloud-scale LLMs, tight Google Cloud integration. |

| AWS Trainium 3 | Cloud ASIC | 144GB HBM3e | Varies by cluster | 10 - 15 | 2 - 10 ms | AWS-native LLM training, Anthropic hosting. |

| Cerebras WSE-3 | Wafer-Scale | 44GB On-chip SRAM | ~2,100 - 3,000 | 15 - 25 | 1 - 5 ms | Ultra-large model training, high-throughput batch inference. |

| Groq LPU (Nvidia) | Deterministic TSP | 500MB On-chip SRAM | ~594 - 1,000+ | 20+ | < 1 ms | Real-time NLP, agentic AI, sub-millisecond latency. |

(Data aggregated from independent industry benchmarks and vendor filings 417193032)

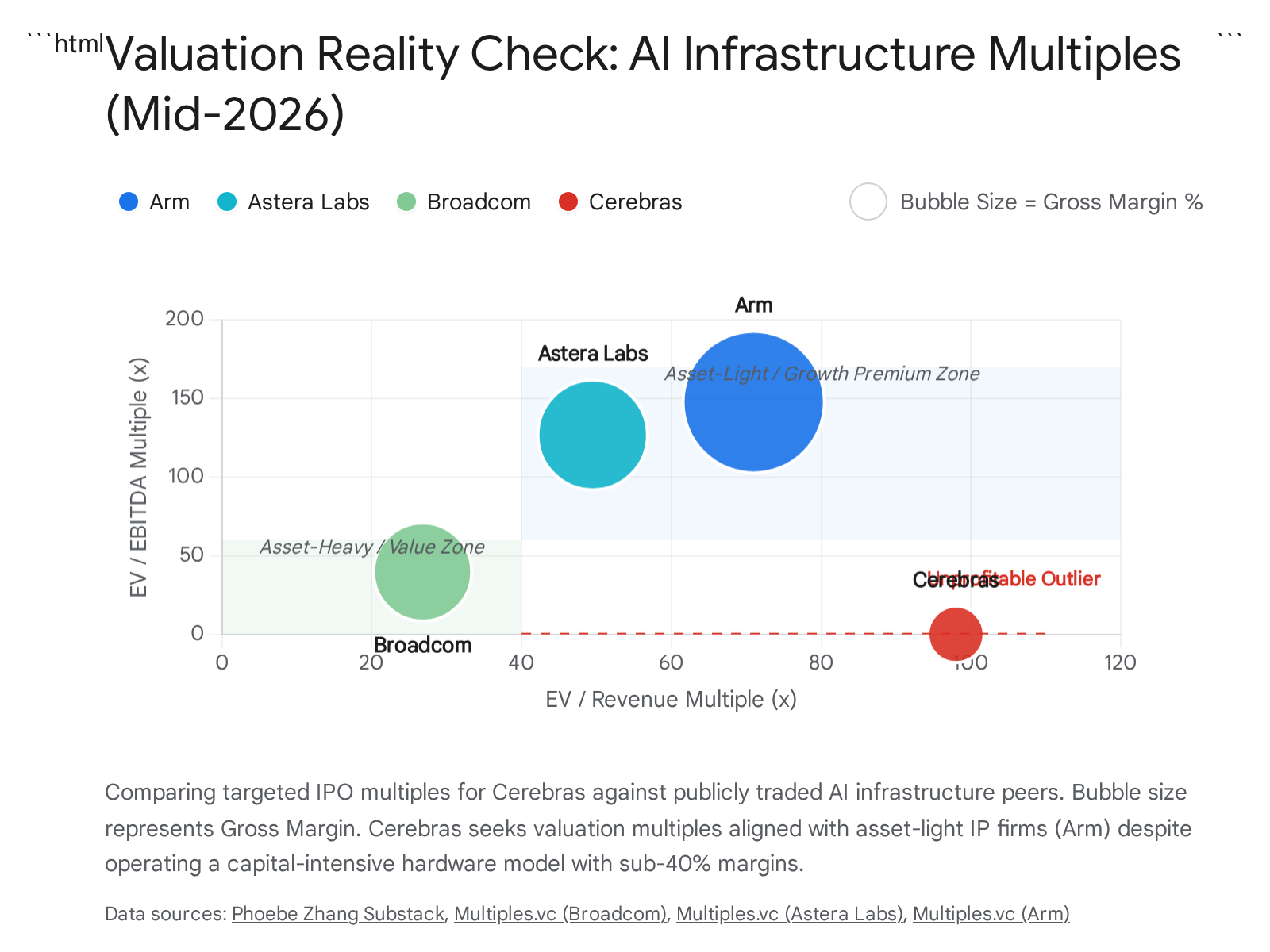

The Cerebras S-1 and Public Market Valuation Frameworks

The architectural triumphs of alternative silicon face a rigorous crucible in the public equity markets. Cerebras Systems' 2026 S-1 filing reveals a company exhibiting explosive top-line velocity, accompanied by profound structural and concentrated risks 333435.

Financial Trajectory and Margin Compression

Cerebras reported $25 million in revenue in 2022, accelerating to $78 million in 2023, $290 million in 2024, and reaching an estimated $510 million in 2025 - a 76% year-over-year increase 333436. Crucially, the company boasts a staggering $24.6 billion contracted backlog 3435. While this backlog provides theoretical revenue visibility through 2030, it is perilously concentrated. Historically, over 80% of revenue was derived from a single customer - the UAE-based G42 (now operating via Core42) 3337. The new backlog is dominated by a $20 billion compute agreement with OpenAI 3436.

A deeper analysis of the S-1 uncovers a troubling margin inversion. The standard narrative for hardware companies pivoting to Cloud/SaaS models involves trading lumpy, low-margin hardware sales for sticky, high-margin recurring software revenue. Cerebras is experiencing the exact opposite 34. Its legacy hardware sales operate at a 43% gross margin 34. However, the Cerebras Inference Cloud, which generated $152 million (30% of 2025 revenue), operates at a dismal 30% gross margin 34. Across 2025, cloud gross margins collapsed from 68% in Q1 to 16% in Q3 due to the immense capital expenditures required to stand up specialized data center capacity faster than utilization could scale 34. Overall corporate gross margins hover at 39% - a stark contrast to Nvidia's commanding 75% margins 35. GAAP net income appeared profitable at $237 million in 2025, but stripping out a one-time accounting adjustment on forward-contract liabilities revealed a $76 million non-GAAP net loss 35.

Valuation Multiples in the AI Infrastructure Cohort

Cerebras approaches its IPO seeking a valuation exceeding $50 billion 36. Evaluating this requires benchmarking against publicly traded semiconductor and AI infrastructure peers, particularly in the context of the 2026 market environment where the "Rule of 40" heavily dictates software and infrastructure multiples 38394041.

| Company | Enterprise Value (EV) | Revenue (LTM) | EBITDA (LTM) | EV/Revenue | EV/EBITDA | Gross Margin |

|---|---|---|---|---|---|---|

| Arm Holdings | $363B | $5.0B | $2.0B | 71.0x | 147.7x | 98% |

| Astera Labs | $59B | $1.0B | $453M | 49.5x | 126.8x | 76% |

| Broadcom | $2.3T | $87.0B | $43.0B | 26.8x | 39.7x | 68% |

| Marvell Tech | $252B | $5.5B* | $4.6B | ~45.0x* | 54.7x | 60%+ |

| Cerebras (Est.) | $50B+ | $510M | Negative | ~98.0x | N/A | 39% |

(Note: Marvell figures approximate based on TTM EV/EBITDA and market cap metrics 401112)

The data reveals a stark disconnect. Arm and Astera Labs command astronomical multiples ($EV/EBITDA$ > 125x) because they operate highly scalable, asset-light models. Arm is pure IP licensing (98% gross margin) 40; Astera Labs designs connectivity solutions without carrying massive data center CapEx (76% gross margin) 39. Astera and Marvell are currently enjoying a massive valuation tailwind due to surging demand for advanced memory controllers to mitigate HBM costs in data centers 44. Broadcom, a diversified giant, trades at a rational 39.7x $EV/EBITDA$ 38.

Cerebras is attempting to price its IPO at software/IP multiples ($\sim 98\text{x}$ EV/Revenue) while operating a highly capital-intensive, vertically integrated hardware and cloud deployment model with 39% gross margins 3536.

While the $24.6 billion backlog justifies a premium, the market must weigh whether Cerebras can physically build and power the bespoke mega-clusters required to recognize that revenue without annihilating its free cash flow. Morgan Stanley projects the company will burn approximately $3 billion across 2026-2027 just to scale the data center infrastructure required to meet the OpenAI demand 36.

Sovereign AI: Geopolitics and Industrial Policy

Beyond pure commercial enterprise, the AI infrastructure market is being radically reshaped by state-level interventions. The concept of "Sovereign AI" - infrastructure, data, and models physically contained and legally governed within a nation's borders - has evolved from a theoretical policy ambition into massive, capital-deployed procurement reality 737.

The global sovereign AI infrastructure market, valued at $24.8 billion in 2026, is forecast to reach $301.6 billion by 2040, expanding at a CAGR of 19.5% 4546. Gartner projects that by 2027, 35% of countries will be locked into region-specific AI platforms, necessitating an investment of up to 1% of national GDP into domestic AI infrastructure by 2029 1348.

National Compute Mandates and The Stack

The drive for sovereignty is predicated on data security, cultural preservation, and a strategic aversion to relying on U.S.-controlled hyperscalers. The Sovereign AI stack consists of four layers: localized storage (Layer 1), compute infrastructure (Layer 2), governance middleware (Layer 3), and sovereign foundational models (Layer 4) 714.

- The Middle East (UAE and Saudi Arabia): The Gulf states are aggressively converting hydrocarbon wealth into compute power. Saudi Arabia's Project Transcendence commits $100 billion to AI infrastructure, aiming to become a regional exporter of "digital energy" 5015. The UAE's MGX and G42 have heavily financed Sovereign AI initiatives. Core42 (a G42 company) recently partnered with Open Innovation AI to launch the Compass API platform, offering native SaaS enterprise models with strict data residency and jurisdictional compliance built directly into the architecture 37.

- Europe: Focused on regulatory compliance (GDPR and the EU AI Act), France committed €109 billion to national AI plans 501654. This massive budget is backing domestic champions like Mistral AI, deploying models on "cloud de confiance" infrastructure governed by strict SecNumCloud certifications to guarantee immunity from extraterritorial surveillance laws 1454.

- India and Japan: India's $1.2 billion IndiaAI Mission mandates the localized deployment of over 10,000 GPUs to train native, multimodal Indic-language models like BharatGen 1454. Japan has similarly pledged $740 million to build decentralized supercomputing capabilities aligned with domestic industrial robotics 754.

Despite these immense capital allocations, true 100% sovereignty remains a practical illusion. The AI supply chain is too complex. Every non-U.S. sovereign program remains exposed to Nvidia hardware supply chains, Taiwanese fabrication, and European lithography (ASML) 1417. Nations are not achieving total independence; rather, they are establishing "strategic autonomy" by controlling the data layers while navigating unavoidable global hardware dependencies 17.

The Eastern Vector: Huawei Ascend and Export Control Circumvention

Nowhere is the intersection of AI hardware and geopolitics more pronounced than in China. Prevented from acquiring Nvidia's Hopper and Blackwell GPUs by strict U.S. Commerce Department export controls since October 2022, China has catalyzed a massive import-substitution drive led by Huawei 165618.

The Huawei Ascend architecture is the bedrock of Chinese AI sovereignty. Operating under severe fabrication constraints - denied Extreme Ultraviolet (EUV) lithography machines - Huawei relies on SMIC's older 7nm (N+2 multi-patterning) processes 1858. Despite this node disadvantage against TSMC's 4nm and 3nm processes utilized by Nvidia, Huawei has achieved remarkable parity through architectural compensation.

The current-generation Ascend 910C, a dual-chiplet design offering 3.2 TB/s of memory bandwidth and 780 BF16 TFLOPS, delivers roughly 60% of the inference performance of an Nvidia H100 181960. To bridge this gap further, Huawei is aggressively testing the forthcoming Ascend 910D. Recognizing that it cannot match Nvidia's future Rubin GPUs (slated for 2026 with 8,300 TFLOPS FP8) on a chip-to-chip basis, Huawei is scaling laterally 19.

Utilizing the proprietary Da Vinci architecture with hybrid SIMD/SIMT execution for enhanced CUDA compatibility, Huawei deploys these chips in massive "SuperPoD" clusters 5819. The Atlas 960 SuperPoD links up to 15,488 Ascend chips with an internal $2 \text{ TB/s}$ interconnect, effectively creating a unified logical machine capable of 30 EFLOPS of FP8 compute 58.

The success of the DeepSeek models, trained partially on restricted H800 hardware and inferred natively on Ascend 910C clusters, proves that the "intelligence tax" of utilizing domestic, non-Western silicon has effectively vanished 1861. Research from Epoch AI confirms that the capability gap between open-weight models and frontier closed systems has shrunk to a mere three months, neutralizing the software advantage of Western hyperscalers 61. Huawei's ability to build competitive rack-scale performance out of sub-optimal 7nm silicon implies that US export controls have not halted Chinese AI advancement; rather, they have successfully incubated a fully independent, parallel hardware ecosystem 171819.

Conclusion

The era of a homogeneous AI infrastructure, predicated exclusively on Nvidia GPUs and the CUDA software stack, has definitively concluded. As the market looks toward the end of the decade, the landscape is defined by fragmentation and high specialization.

First, the democratization of software via compiler abstractions like PyTorch 2.0 and OpenAI Triton has permanently decoupled hardware from software, eroding Nvidia's highest barrier to entry. Second, the economic gravity of AI has shifted irreversibly from training to deployment. As inference comes to represent 80% of total compute load, ultra-low latency, SRAM-heavy architectures from specialized vendors (like Cerebras), or Nvidia's newly acquired Groq division, will dominate edge and specialized cloud data centers.

Third, financial realities are sobering the hardware market. Alternative vendors offer profound technological breakthroughs but face an unforgiving financial reality. Attempting to balance low-margin, capital-intensive infrastructure buildouts while demanding software-grade valuation multiples poses a severe risk in public markets, as evidenced by the scrutiny surrounding the Cerebras IPO.

Finally, AI compute is now universally classified as critical national infrastructure. Driven by data residency laws and geopolitical anxiety, hundreds of billions of dollars are flowing into regional sovereign clouds. In this fragmented landscape, there is no single "winning" chip. The optimal AI compute stack of 2026 and beyond is fundamentally heterogeneous: immense GPU mega-clusters for foundational training, specialized SRAM ASICs for high-volume inference, and indigenous sovereign architectures insulated from the weaponization of global trade.