Market Entry and Expansion Sequencing Through Foothold Markets

Introduction to Foothold Market Theory

The strategic sequencing of market entry and subsequent expansion is a central problem for nascent enterprises and established firms entering new domains. Within the strategic management literature, the theory of disruptive innovation provides a structural explanation for how resource-constrained entrants can successfully challenge well-capitalized incumbents. The cornerstone of this theory is the concept of the "foothold market" - a specific entry point that allows a new technology or business model to take root without triggering an immediate, overwhelming competitive response from industry leaders 123.

Disruptive innovation describes a process rather than a discrete product event 45. It is characterized by an entrant introducing an offering that initially underperforms established products on the primary performance metrics valued by mainstream customers 16. Because these early iterations are often cheaper, simpler, or more convenient, they are dismissed by incumbent firms as inferior or unprofitable 16. The entrant secures a foothold in the periphery of the market, refines its technology and business model, and progressively moves upmarket. Eventually, the disruptive offering improves enough to satisfy the performance requirements of mainstream customers while retaining its inherent advantages in cost or convenience, resulting in the displacement of established competitors 37.

Understanding how foothold markets function requires an analysis of the economic motivations that govern resource allocation within incumbent firms. Established companies consistently prioritize "sustaining innovations" - improvements that allow them to sell better products for higher profits to their most demanding customers 268. The pursuit of higher margins dictates that incumbents allocate resources away from the least profitable segments of their market. Foothold strategies exploit this predictable behavior, turning the incumbent's rational pursuit of profit into a structural vulnerability 910.

The concept of disruptive innovation, coined by Harvard Business School professor Clayton Christensen in the 1990s, has become ubiquitous in business theory, though it is frequently misapplied to describe any general industry upheaval 37. True disruption relies on the deliberate sequencing of expansion from an initial, economically unattractive foothold 11. By examining the characteristics of footholds, the mechanics of asymmetric competition, the impact of digital networks, and the empirical evidence from global case studies, a comprehensive blueprint for sequential market expansion emerges.

Characteristics and Classification of Foothold Markets

A foothold is not simply any small or niche market; it must possess specific economic and competitive characteristics that shield the entrant from incumbent retaliation. Disruptive innovation theory identifies two distinct types of footholds from which sequential expansion can originate: low-end footholds and new-market footholds 478.

Low-End Disruptive Footholds

Low-end footholds emerge in existing markets where the trajectory of technological improvement has outpaced the ability of consumers to utilize it. In their drive to serve the most profitable tiers of the market, incumbents consistently "overshoot" the needs of lower-tier customers, providing products that are too complex or expensive for basic applications 512.

This overservice creates a vacuum at the bottom of the market. An entrant establishes a low-end foothold by introducing a product that is "good enough" for these less demanding customers, typically utilizing a low-cost business model 81314. Because the incumbent views these customers as their least profitable demographic, they lack the financial incentive to defend this segment. The margins are too thin to justify a price war, aggressive marketing campaigns, or the allocation of premium engineering resources 3916.

Historically, the steel industry provides a classic example of low-end foothold sequencing. Steel mini-mills entered the market by producing concrete reinforcing bars (rebar), which was the lowest-margin product for large, integrated steel mills 69. The integrated mills happily ceded the rebar market to the mini-mills, preferring to focus on highly profitable sheet steel 9. Operating without interference in this low-end foothold, the mini-mills progressively improved their technology to produce structural steel and eventually sheet steel, driving the incumbent integrated mills out of the market entirely 9. Similarly, the Taiwanese computer company ASUSTeK secured a low-end foothold by manufacturing simple circuit boards for Dell before expanding into a global consumer electronics brand 9.

New-Market Disruptive Footholds

While low-end footholds capture existing but overserved customers, new-market footholds are established by converting "non-consumers" into consumers 467. These footholds exist entirely outside the traditional value network of the incumbent industry. The target demographic consists of individuals or organizations that previously lacked the wealth, specialized skills, or access required to use the incumbent's product 3415.

Entrants establish a new-market foothold by introducing a product that is dramatically simpler, more accessible, or more affordable 3. Because the product is evaluated against the alternative of "nothing at all" rather than the high-performance standards of the incumbent's product, the initial performance hurdles are low 416. Incumbents ignore new-market footholds because they do not perceive the non-consumers as part of their addressable market, and the new value network initially generates revenue volumes that appear inconsequential to a large enterprise 81615.

The early personal computer (PC) operated as a new-market disruption. Early PCs were dismissed as children's toys because they lacked the processing power to compete with the minicomputers and mainframes marketed to large enterprises 1720. However, they appealed to hobbyists, small businesses, and students who could never afford a minicomputer 20. The early photocopier industry followed a similar pattern; while Xerox targeted large corporations with high-priced machines, disruptive entrants targeted school librarians and small bowling-league operators who previously relied on carbon paper 18. In the modern era, Florida Virtual School (FLVS) utilized policy-driven asymmetric motivation to secure a new-market foothold in online learning, serving students who required non-traditional scheduling before competing directly with brick-and-mortar schools 9.

| Characteristic | Low-End Footholds | New-Market Footholds |

|---|---|---|

| Target Audience | Overserved customers in the existing market. | Non-consumers; individuals lacking access or funds. |

| Incumbent Perception | Least profitable, highly price-sensitive segment. | Outside the defined addressable market; irrelevant. |

| Performance Standard | "Good enough" compared to incumbent over-engineering. | Better than the alternative of non-consumption. |

| Basis of Advantage | Lower cost structure and operational efficiency. | Simplicity, convenience, and accessibility. |

| Initial Impact on Incumbent | Margin improvement for the incumbent as they shed low-tier buyers. | No immediate impact; growth occurs in a new value network. |

Conceptual Distinctions: Footholds Versus Beachheads

In strategic literature and entrepreneurial practice, the concepts of the "foothold market" and the "beachhead market" are frequently conflated. However, they represent fundamentally different analytical frameworks derived from different theoretical lineages 1920. The foothold concept originates from Christensen's theory of disruptive innovation, focusing on resource allocation and structural economics 618. The beachhead concept originates from Geoffrey Moore's adaptation of the technology adoption lifecycle in Crossing the Chasm, focusing on psychographic segmentation and technology marketing 212522.

Target Audience and Strategic Intent

Moore's beachhead strategy is an aggressive, targeted marketing maneuver designed to transition a continuous or discontinuous innovation from the early market to the mainstream market 2523. Drawing explicitly from the World War II Allied invasion of Normandy, the strategy mandates concentrating overwhelming force on a small, strategic border area to secure a stronghold before advancing 212224.

A beachhead market is defined as a tightly bound segment of "pragmatist" customers who share similar business problems, buy similar products, and communicate with one another 2125. The strategic intent is to dominate this single segment to achieve market leadership, generate word-of-mouth validation, and secure referenceable case studies 2330. Unlike visionaries who buy on the promise of revolutionary change, pragmatists require a compelling reason to buy and a high degree of trust in the technology 2531. Once the beachhead is secured, the firm uses it as a launching pad to attack adjacent market segments in a "bowling pin" or "bowling alley" expansion strategy 253026. This stands in stark contrast to a "spray and pray" strategy, which attempts to address the entire market simultaneously with a generic message 2425.

Conversely, Christensen's foothold strategy is not about marketing to mainstream pragmatists; it is about finding a sanctuary from competition. The target audience for a foothold is specifically chosen because incumbents do not want them 931. The strategic intent is to grow quietly in an economically unattractive space, refining a new business model without triggering a defensive response from larger competitors 611.

Market Lifecycle Phasing

The beachhead strategy assumes that the product is ready for the mainstream but lacks the validation required by risk-averse buyers 2533. It is a solution to a marketing gap (the chasm) that exists between early adopters and the early majority 2634. Moore divides buyers into enthusiasts, visionaries, pragmatists, and conservatives, noting that positioning must shift from promising "state of the art" to "industry standard" as the company crosses the chasm 23.

The foothold strategy assumes the product is not yet ready for the mainstream. It is initially inferior on traditional performance metrics and requires a period of incubation 16. The foothold provides the necessary time and revenue to fund the technological trajectory that will eventually make the product acceptable to the mainstream 816.

| Parameter | Christensen's Foothold Market | Moore's Beachhead Market |

|---|---|---|

| Theoretical Origin | Disruptive Innovation Theory (Economics/Strategy) | Technology Adoption Lifecycle (Marketing/Psychographics) |

| Primary Challenge | Incumbent retaliation and resource allocation | The "Chasm" between early adopters and early majority |

| Target Customer | Overserved low-end buyers or non-consumers | Pragmatist buyers with an acute, urgent problem |

| Incumbent Response | Ignored or voluntarily ceded | Fiercely contested by existing vendors |

| Product Readiness | Inferior to mainstream alternatives; "good enough" | Ready for mainstream use; requires references/validation |

| Expansion Mechanism | Upmarket trajectory of technological improvement | "Bowling pin" expansion into adjacent demographic segments |

The Mechanics of Sequential Market Expansion

The successful utilization of a foothold market relies on a specific sequence of competitive dynamics. Disruption is not an event but a trajectory 6. The speed and success of this trajectory are governed by the interplay between the entrant's capabilities and the incumbent's structural incentives 1627.

Asymmetry of Motivation and Incumbent Flight

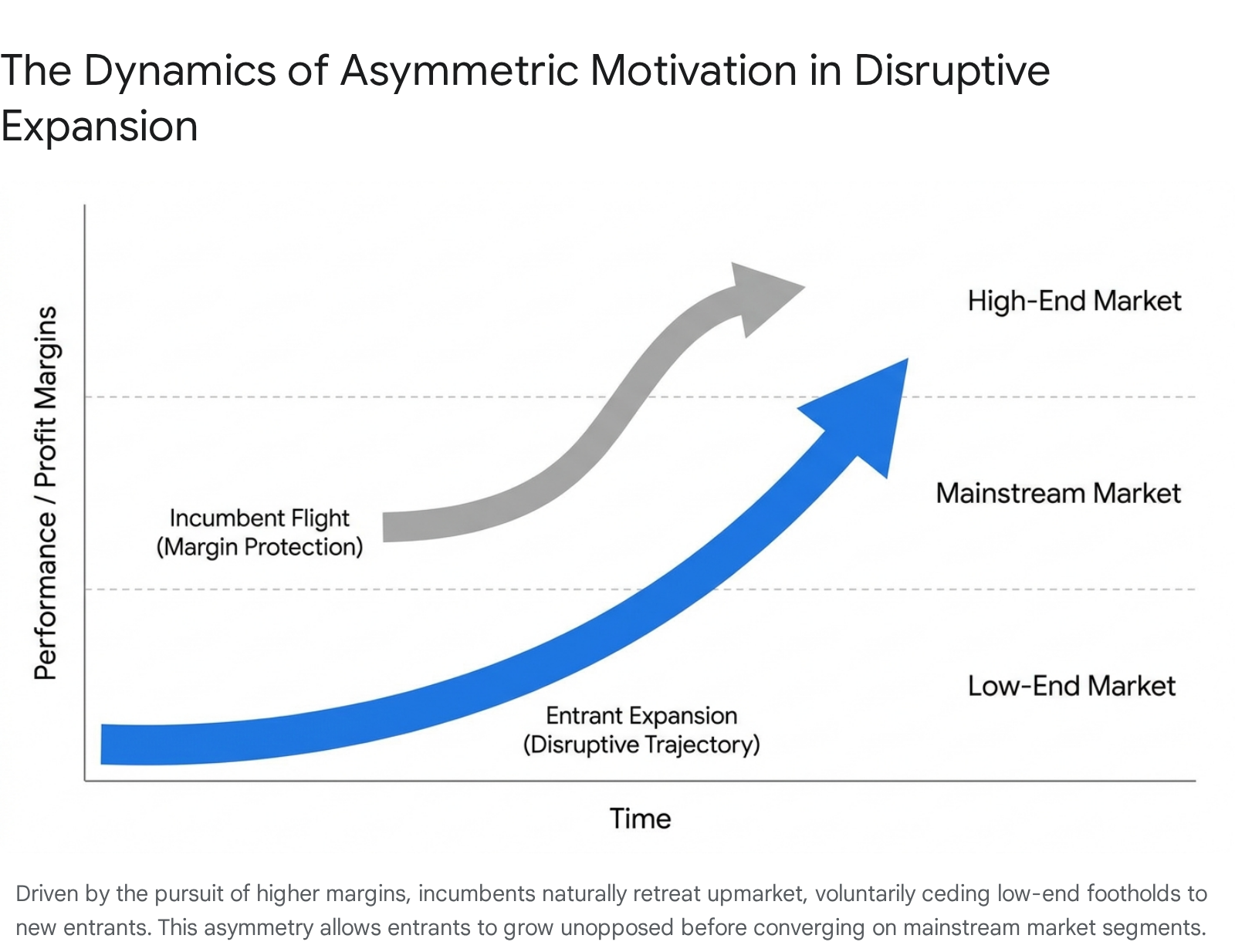

The most critical mechanism enabling sequential expansion is "asymmetry of motivation." This occurs when an entrant is highly motivated to pursue a market segment that the incumbent is equally motivated to abandon 2910.

When an entrant captures a low-end foothold, the incumbent faces a choice: fight to retain the least profitable customers by lowering prices, or flee upmarket to focus on high-margin, demanding customers 26. Because corporate resource allocation processes prioritize initiatives that maximize return on investment, incumbents almost invariably choose flight 28. They cede the low end of the market to the entrant.

This dynamic is devastatingly effective because, from the incumbent's perspective, ceding the low end appears to be a highly rational, positive financial development. As the incumbent sheds low-margin customers, its overall blended profit margin improves 28. The entrant is therefore protected by a "shield of asymmetric motivation," allowing it to operate and scale without facing the massive marketing budgets or pricing power of the industry leader 2.

Trajectory of Improvement and Mainstream Convergence

While operating within the foothold, the entrant begins to build "asymmetric skills" - capabilities tailored to a new context of use, such as extreme cost efficiency, streamlined supply chains, or unique user interfaces 216. Concurrently, the pace of the entrant's technological improvement generally outstrips the mainstream market's ability to absorb new performance 516.

Over time, the entrant's product iterates rapidly. It eventually crosses the threshold of what mainstream customers consider "good enough" 820. At this point, the entrant brandishes its asymmetric skills as a sword 2. The mainstream customer, evaluating the incumbent's highly expensive, over-engineered product against the entrant's affordable, sufficiently performant product, switches to the entrant 1620. The incumbent, having retreated to the highest tiers of the market and optimized its cost structure solely for premium delivery, finds its addressable market shrinking to a small niche of luxury or hyper-demanding users 28.

The Four Stages of Disruption

The sequencing from foothold entry to mainstream dominance generally follows a recognizable four-stage lifecycle, synthesizing Everett Rogers' diffusion of innovation with Steven Sinofsky's technology dynamics 272837:

- Stage 1: Disruption of Incumbent (Emergence): The innovative offering enters the market via a foothold. It is unpolished, functionally limited, and stands in stark opposition to the dominant product. It gains a small baseline of users while incumbents remain dismissive or entirely unaware of the long-term threat 272837.

- Stage 2: Rapid Linear Evolution (Improvement): The disruptor iterates the product based on feedback from early adopters. The focus shifts to "filling out" the product ecosystem, establishing reliable operational structures, and maturing from a ragtag startup operation into a structured enterprise capable of scaling 272837.

- Stage 3: Appealing Convergence (Mainstream Adoption): The disruptive technology meets the performance requirements of the mainstream. Mass adoption occurs as the value proposition - often an unbeatable price-to-performance ratio - becomes irrefutable. Incumbents experience sudden, severe market share erosion and belatedly attempt to acquire the disruptor or replicate the technology 2737.

- Stage 4: Complete Reimagination (Consolidation): The disruptor becomes the new incumbent. The industry is entirely restructured around the new baseline economics and technology. The original incumbents are either marginalized, acquired, or forced into bankruptcy, and the cycle prepares to repeat as new entrants target the new incumbent's lower tiers 272837.

Accelerants of Market Expansion: Digital Platforms, SaaS, and AI

The temporal timeline from foothold entry to mainstream disruption varies dramatically across industries. Historically, hardware and heavy manufacturing disruptions required decades to play out due to capital intensity, physical supply chain constraints, and slow production scaling 56. However, the digitization of the global economy has profoundly accelerated the disruption lifecycle, shrinking the window incumbents have to respond.

The Compression of Disruption Timelines in SaaS

In the realm of Software as a Service (SaaS), the marginal cost of reproducing and distributing the product is near zero. Consequently, once a SaaS product secures a foothold - often targeting price-sensitive small and medium-sized businesses (SMBs) or individual consumers with affordable subscription models - it can scale globally with unprecedented speed 3829.

The shift from monolithic, on-premises software to cloud-native applications allows disruptors to iterate continuously without requiring clients to install updates 2930. While traditional enterprise software companies relied on massive upfront licensing fees and long implementation cycles, SaaS disruptors utilized "freemium" or low-cost monthly models to reduce friction, proving value rapidly to non-consumers who previously could not afford enterprise marketing or CRM tools 29.

As these SaaS platforms captured footholds, they moved steadily upmarket. They added enterprise-grade features, guaranteed 99.99% uptime availability, and integrated advanced security protocols, eventually displacing legacy software vendors who were too slow to adapt their core profit formulas 2942. Industry data highlights this shift; by 2018, SaaS commanded 29% of enterprise-software revenues, a figure that climbed significantly when factoring in the transition to broader "as-a-service" and Platform-as-a-Service (PaaS) models .

Generative AI as a Disruptive Catalyst

Generative Artificial Intelligence (GenAI) currently exhibits the classic hallmarks of a disruptive technology evolving at hyper-speed. GenAI entered the market via low-end and new-market footholds. Initially, the technology was dismissed by subject matter experts as hallucination-prone, superficial, and inadequate for professional, enterprise-grade applications 16. It gained a foothold by serving non-consumers - small businesses, solo entrepreneurs, and students - who could not afford professional copywriters, junior coders, or legal consultants 16. For these users, a slightly imperfect AI-generated draft was "good enough" because the alternative was entirely unaffordable 16.

However, due to the scaling laws of machine learning and massive data integration, the rate of technological improvement in GenAI vastly outpaces the gradual increase in mainstream market demands 16. What began as a tool for low-stakes ideation and drafting is rapidly advancing upmarket, demonstrating proficiency in writing production-grade code, conducting advanced data analysis, and generating complex legal documentation 163132. Organizations are now sequencing their strategic AI implementations, moving from isolated, low-risk workflow automations to fundamental business model reimagination 3132.

Network Effects and the Platform Economy

When applying foothold strategy to modern digital ecosystems, strategists must account for the profound impact of network effects. A network effect occurs when the value of a product or service increases exponentially as more people use it, a principle formalized as Metcalfe's Law 4533.

Winner-Take-All Dynamics

In traditional disruptive innovation (e.g., steel mini-mills or disk drives), the market can support multiple competitors at various tiers. In the platform economy, the convergence of disruptive innovation and strong network effects often leads to "winner-take-all" or "winner-take-most" market structures 45343536.

Once a digital platform - such as a social network, ride-hailing app, or digital marketplace - secures a firm foothold, the utility for each subsequent user compounds. Direct network effects (users valuing the presence of other users) and indirect network effects (users valuing the presence of complementary developers or sellers) create massive barriers to entry for latecomers 4533.

Compounding Advantages in Platform Disruption

As a platform scales out of its foothold, it accumulates vast troves of user data, enabling superior algorithmic targeting and personalization 3336. This data advantage allows the platform to move horizontally, leveraging its massive user base to disrupt adjacent industries 36.

For example, Amazon began with a highly focused foothold in online bookselling - serving customers who valued infinite selection over immediate physical possession 37. As it secured this foothold, it leveraged its expanding logistical network and customer data to disrupt broad retail. Eventually, it utilized its internal server infrastructure to disrupt the enterprise computing market via Amazon Web Services (AWS), providing basic computing and storage to startups who could not afford enterprise infrastructure 3738. Similarly, Canva disrupted the design software market dominated by Adobe. Adobe relied on selling expensive, professional-grade software to skilled users. Canva secured a new-market foothold by offering a freemium platform to non-experts, tapping into mass non-consumption before adding premium tiers and moving upmarket 37.

Critics and antitrust economists, including New Brandeisians like Federal Trade Commission Chair Lina Khan, note that in winner-take-all markets, the traditional vulnerability of the incumbent is inverted. Once an incumbent platform establishes absolute dominance, the high switching costs and network lock-in make it extraordinarily difficult for a new entrant to gain a foothold, even if the entrant possesses a technologically superior product 45333539.

Case Studies in Sequential Expansion from Foothold Markets

The theoretical principles of foothold entry and sequential expansion are vividly demonstrated in the strategies of modern technology firms across global emerging markets, particularly in regions where traditional incumbents have left massive populations underserved.

Transsion in Africa: Low-End Hardware Foothold

Transsion Holdings provides one of the most exhaustive examples of geographic and technological foothold sequencing. Founded in 2006, Transsion entered the mobile phone market in Africa at a time when global incumbents like Samsung and Nokia viewed the continent as an afterthought, primarily selling late-model, low-end devices designed for Western or Asian consumers 404142.

Transsion identified a vast new-market and low-end foothold: African consumers who required extreme affordability but also specific localized functionalities. Transsion did not introduce cutting-edge, breakthrough technology; instead, it achieved disruptive innovation through tailored integration to cater to local conditions 43. The company introduced sub-$100 feature phones and smartphones equipped with multiple SIM card slots (crucial for users navigating fragmented telecom networks to avoid out-of-network charges), extended battery life (essential in regions with unreliable electricity grids), and camera algorithms calibrated specifically to capture darker skin tones more accurately 404143.

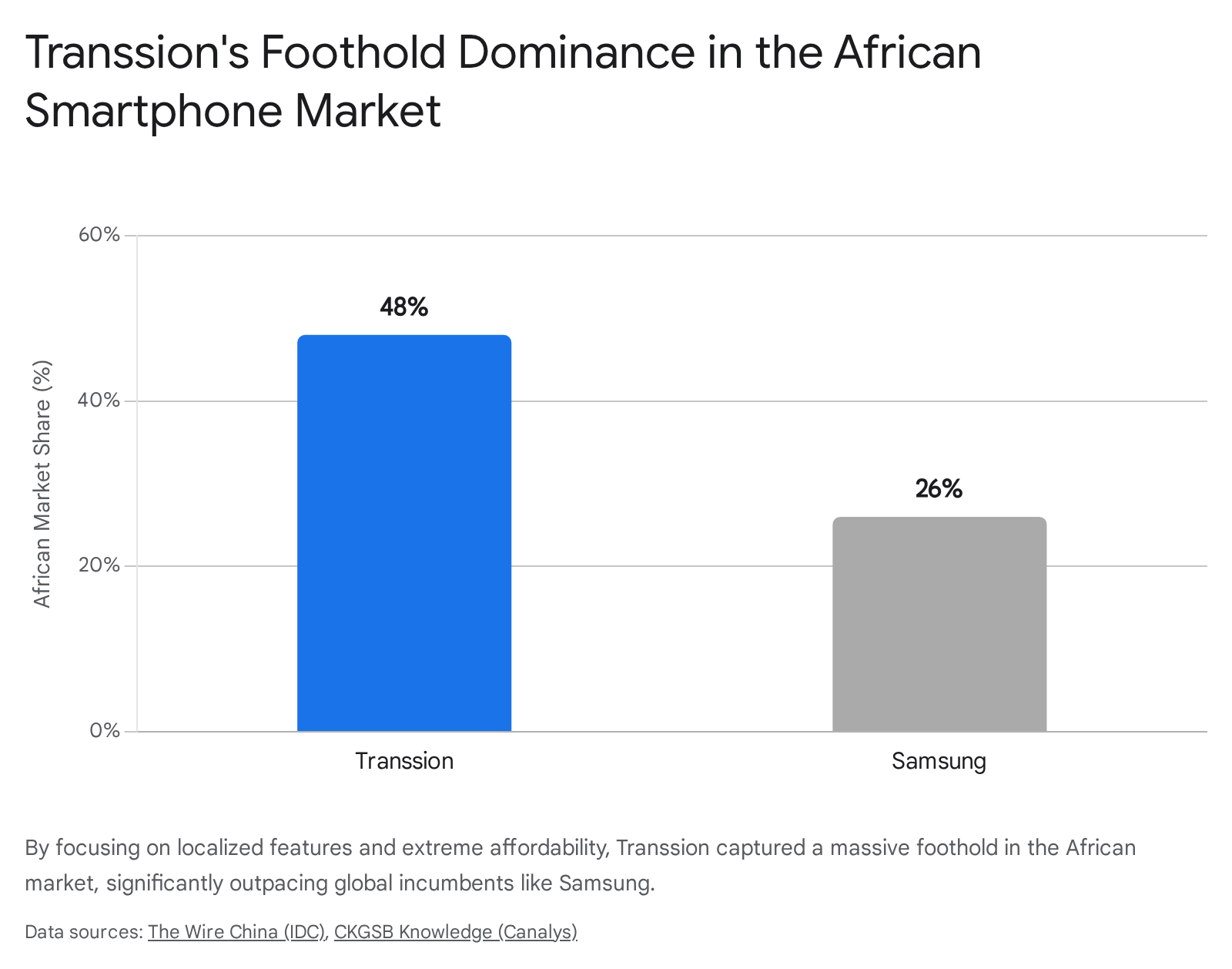

By operating in a market segment deemed unprofitable or overly complex by global giants, Transsion enjoyed a decade of relatively uncontested growth 4042. They utilized this time to build asymmetric skills, heavily investing in local distribution networks in countries like Nigeria and Ghana, and establishing "Carlcare" repair centers that fostered intense brand loyalty 40424445. By 2023, Transsion's brands (Tecno, Infinix, and itel) commanded nearly 48% of the African smartphone market, vastly outperforming Samsung's 26% share 4546.

Having secured this massive foothold, Transsion executed a sequential geographic expansion. Leveraging its low-cost manufacturing capabilities, it entered Indonesia in 2015, followed by India, Bangladesh, and Pakistan, where it captured over 40% of the market share 42. It subsequently replicated its playbook in Latin America, partnering with local electronics firm Positivo Tecnologia to manufacture and sell Infinix phones in Brazil 4246. Despite its monumental success, Transsion now faces the vulnerabilities of an incumbent, as challengers like Xiaomi and Realme deploy aggressive pricing strategies to erode Transsion's African market share 4247.

Xiaomi in Asia: Agility and Ecosystem Disruption

Xiaomi's rise in the smartphone and IoT (Internet of Things) markets demonstrates how a disruptive entrant can use value innovation to capture a low-end foothold and rapidly scale globally. Unlike traditional incumbents that pushed incremental technology improvements at premium prices, Xiaomi designed products specifically to solve the unmet needs of dissatisfied or price-sensitive Apple and Samsung customers in China and India 4849.

Xiaomi's foothold strategy relied on offering superior core specifications - such as extended battery life and high-end processors - while stripping away non-essential features, allowing them to sell devices at a fraction of incumbent prices 49. In India, they localized production to aggressively cut manufacturing costs, systematically chipping away at Samsung's market leadership 485051. Rather than engaging in traditional, expensive marketing campaigns, Xiaomi relied on viral digital marketing, direct-to-consumer online sales, and intense community engagement to capture market share, effectively changing the profit formula of the industry 4950.

The company also executed a sophisticated segmentation strategy, creating sub-brands like Redmi and POCO for mid-market and low-end customers, while maintaining the flagship Xiaomi brand for the high end 49. By mid-2021, Xiaomi had briefly surpassed both Apple and Samsung to become the world's top smartphone brand by global sales volume, executing a flawless upmarket trajectory from its initial budget-friendly foothold without even entering the United States market due to geopolitical risks 49.

Nubank in Latin America: Disruption of Financial Incumbents

The financial services sector in Latin America provided a highly fertile environment for new-market and low-end disruption. Historically, the Brazilian banking sector was highly concentrated, dominated by five large incumbents that charged exorbitant fees, offered poor customer service, and largely ignored the lower-income segments of the population, leaving nearly 30% of Brazilians unbanked 5253.

Nubank entered this market in 2013, founded by David Vélez. Rather than attempting to build a full-service, regulatory-heavy traditional bank, Nubank established a highly focused foothold: a no-fee, digital-only credit card managed entirely via a smartphone app 5267. This targeted approach addressed the extreme friction and bureaucracy of traditional Latin American banking, appealing directly to a younger, digitally native demographic and the financially excluded who lacked long credit histories 6754.

Because Nubank operated without the massive overhead costs of physical branch networks or legacy IT systems, its cost-to-serve was a fraction of traditional banks - reportedly around 80 cents per customer compared to double-digit dollars for incumbents 53. This asymmetric cost structure allowed Nubank to remain highly profitable while offering zero-fee products. The incumbent banks could not replicate this model without severely cannibalizing their own massive revenue streams derived from overdraft fees and account maintenance charges 5269.

Once the foothold was secure and the brand trusted, Nubank sequenced its expansion. Product expansion included digital savings accounts, personal loans, life insurance, and investment platforms 5367. By establishing a "low and grow" business strategy, Nubank helped poorer customers build credit histories, meeting their needs at every stage of their financial journey 53. Geographic expansion followed, with Nubank moving from Brazil into Mexico and Colombia, proving the regional applicability of their disruptive model 525367. Today, Nubank serves over 110 million customers, fundamentally altering the competitive landscape of Latin American finance and forcing traditional banks to accelerate their own digital transformation efforts 5354.

DiDi Global in Latin America: Platform Localization

The ride-hailing industry demonstrates how platform businesses utilize geographic footholds. Chinese ride-hailing giant DiDi Global Inc. targeted Latin America in 2018 as a strategic expansion zone. The region presented a massive addressable market of over 600 million people, rapid urbanization, increasing smartphone penetration, and heavily congested, inefficient public transportation systems 55.

DiDi did not simply copy its Chinese operations; it localized its offerings to address the unique cultural, safety, and economic realities of markets like Mexico, Brazil, Argentina, and Chile 55. By tailoring its global playbook to fit regional dynamics, DiDi gained a foothold in a market that lacked adequate digital mobility solutions. Despite intense competition, regulatory hurdles, and economic volatility, DiDi completed 2.66 billion rides in international markets by 2023, with Latin America serving as its second most important market globally 55.

Academic Critiques and Limitations of Foothold Theory

Despite its ubiquity in corporate strategy and executive planning, the theory of disruptive innovation and the concept of foothold market sequencing have faced severe academic and empirical scrutiny over the past decade. Critics argue that the theory is often misapplied as a universal catch-all explanation for any fast-growing business or industry failure, heavily diluting its analytical rigor 41118.

Empirical Weaknesses and the 9 Percent Fit

A prominent critique was leveled by Harvard historian Jill Lepore in 2014, who argued that Christensen relied on circular logic and hand-picked case studies that favored his conclusions while conveniently ignoring counter-examples that did not fit the narrative 5657. She argued that disruption is merely a theory of why businesses fail, not a predictive law of nature 57.

More devastatingly, empirical research conducted by academics Andrew King and Bajjir Baatartogtokh systematically tested the 77 foundational case studies cited in Christensen's original texts. Consulting with 82 independent industry experts, historians, and financial analysts, they sought to determine if the historical facts of those 77 cases actually matched the theoretical premises of Disruptive Innovation 73. The results revealed massive discrepancies between the theory and historical reality: * In roughly 30% of the cases, the incumbent leaders were not actually on a trajectory of sustaining innovation 73. * In nearly 80% of the cases, the incumbent's innovations had never "overshot" the needs of mainstream customers 73. * In almost 40% of the cases, incumbent firms lacked the actual technological or organizational capability to respond to the threat, rather than merely lacking the financial motivation to do so 73. * In almost 40% of the cases, the incumbents were never actually displaced by the disruptive entrant 73.

Ultimately, the researchers concluded that only seven of the 77 cases - a mere 9 percent - fully matched both the premises and the eventual predictions of Disruptive Innovation Theory 1773. This suggests that while foothold disruption is a real and observable phenomenon, the exact conditions required for it to execute flawlessly are exceptionally rare. Furthermore, the failures of incumbent firms are frequently better explained by standard market dynamics such as the laws of probability, shifting scale economies, macroeconomic burdens, or basic executive mismanagement 73.

Incumbent Resilience and Theoretical Boundaries

Further academic research indicates that disruption is not an inevitable death sentence for incumbents. Dominant players can survive, adapt, and even extend their dominance by forming strategic partnerships with challengers, aggressively acquiring promising startups, or leveraging complementary assets important for the new technology's deployment 1158.

Furthermore, the model's single-minded focus on bottom-up disruption ignores top-down disruptions. Top-down disruptions occur when a premium, high-priced product is introduced to the highest end of the market - initially purchased only by the most discriminating buyers - and eventually moves downward into the mainstream as manufacturing costs fall 1. The original iPod and the iPhone are classic examples of premium innovations that disrupted markets from the top down, a trajectory that traditional foothold theory fails to predict 158. Therefore, while establishing a low-end or new-market foothold is a viable strategy to bypass initial incumbent retaliation, it does not guarantee a successful upmarket trajectory, nor does it guarantee long-term market leadership.

Conclusion

The concept of the foothold market remains one of the most vital strategic heuristics for new entrants seeking to sequence their expansion into competitive industries. By targeting overserved low-end customers or previously excluded non-consumers, entrants can establish operations behind a shield of asymmetric motivation. Incumbents, structurally bound to the pursuit of high-margin sustaining innovations, frequently cede these footholds voluntarily, providing the entrant with the necessary runway to refine its technology and perfect its business model.

As demonstrated by Transsion in Africa, Xiaomi in Asia, and Nubank in Latin America, securing a localized or demographic foothold allows a company to build asymmetric skills and cost structures that are highly toxic to legacy incumbents. Once the product crosses the threshold of "good enough" for the mainstream, the entrant can leverage its operational agility to capture vast market share. Furthermore, the advent of SaaS platforms, Generative AI, and digital networks has drastically compressed the time required to move from an initial foothold to mainstream dominance, while simultaneously raising the stakes through winner-take-all network effects.

However, the application of foothold strategy requires calibrated expectations. Rigorous empirical critiques highlight that true disruptive innovation is rare, and establishing a foothold does not guarantee that incumbents will remain passive or that the entrant will successfully manage the complex transition across market tiers. Ultimately, foothold strategy provides entrants not with an absolute guarantee of victory, but with a highly structured methodology for avoiding premature, fatal conflicts with entrenched industry leaders during the most vulnerable phases of enterprise growth.