Macroeconomic implications of a 120-year lifespan

Introduction

The prospect of a 120-year human lifespan, once relegated to the periphery of speculative biology and science fiction, has increasingly become a critical boundary condition for rigorous macroeconomic forecasting and demographic modeling 12. As advancements in molecular biology, artificial intelligence-driven drug discovery, and multiomics fundamentally alter the trajectory of human aging, economists and central banks are compelled to re-evaluate the foundational assumptions of the modern welfare state, global labor markets, and aggregate capital accumulation 13. The global population has more than tripled since the 1950s, reaching over 8.2 billion in 2024, but the primary driver of demographic shifts has definitively transitioned from high fertility rates to unprecedented longevity gains 21. Globally, life expectancy has risen dramatically, and while the United States has experienced localized stagnation due to chronic diseases and healthcare inefficiencies, comparable advanced economies continue to push the upper limits of the human lifespan 26.

A radical shift toward a 120-year lifespan requires a structural reimagining of macroeconomic theory. The prevailing models of fiscal sustainability, sovereign pension solvency, and lifecycle savings were calibrated during the mid-twentieth century, anchored to an average lifespan of roughly 80 years and a statutory retirement age of 65 34. Extending the human lifespan by four decades shatters the mathematical equilibrium of these interlocking systems. If individuals continue to exit the labor force in their early sixties, a 120-year lifespan implies an unprecedented 55-year retirement phase, a scenario that would necessitate mathematically impossible savings rates, trigger catastrophic old-age dependency ratios, and systematically bankrupt sovereign balance sheets 29.

Consequently, the macroeconomic analysis of extreme longevity cannot be treated as a simple linear extrapolation of current demographic trends. It demands a rigorous examination of the morbidity compression debate, the behavioral shifts in aggregate savings and intertemporal substitution, the evolution of consumption patterns within the emerging "Silver Economy," and the profound wealth inequality generated by delayed intergenerational capital transfers 56127. By examining contrasting geographic responses - from China's rapid structural reforms to Denmark's automatic longevity indexing - this report comprehensively maps the fiscal, theoretical, and societal implications of radical life extension 815.

The Morbidity Compression Debate: Lifespan Extension Versus Healthspan Extension

The economic viability of a 120-year lifespan hinges entirely on the biological nature of the extended years. Macroeconomic projections must explicitly distinguish between the extension of frail, dependent years and the extension of healthy, productive years. This paradigm, known in demographic and health economics literature as morbidity compression, operates as the core driver of long-term fiscal outcomes 169.

If breakthroughs in medical technology merely prolong the final stages of biological decline, the resulting expansion of the frail lifespan would exert an unsustainable drag on global economic growth. Under this scenario, health systems would be overwhelmed by the compounding costs of chronic diseases, long-term care, and intensive geriatric interventions. In the United States, healthcare expenditure already consumes approximately 18 percent of the Gross Domestic Product (GDP), a figure significantly higher than peer nations due to a combination of systemic inefficiencies, high administrative overhead, and reliance on expensive late-stage interventions 210. Extending the frail period by several decades would disproportionately inflate this figure, crowding out essential public investments in infrastructure, education, and technological innovation. The marginal welfare value of each additional unhealthy life year becomes a severe economic liability, forcing governments to allocate an ever-increasing share of national wealth to biological maintenance rather than productive growth 919.

Conversely, the morbidity compression model posits that advancements in senolytic therapies, cellular reprogramming, mTOR inhibitors, and CRISPR gene editing will actively delay the onset of age-related diseases, thereby extending the healthspan proportionally to the lifespan 1316. There is already empirical precedent for this shift. According to the World Health Organization, 83 percent of the increase in global life expectancy between 2000 and 2021 reflects years expected to be lived in good health, free from debilitating chronic conditions 9. If radical longevity is fundamentally characterized by morbidity compression, the macroeconomic narrative shifts away from fiscal catastrophe and toward a highly lucrative "longevity dividend" 2021.

Healthy aging fundamentally alters the macroeconomic equation. It enables older cohorts to remain active in the labor market for significantly longer durations, maintaining high levels of labor productivity and consumption while deferring the drawdown of public pension systems and private retirement accounts 919. Rigorous health-economics modeling indicates that premature death and functional decline currently claim tens of millions of life-years annually in major economies, costing the United States alone an estimated $4.6 trillion per year in lost human capital and productivity 1. By extending the period of physiological vitality, societies can amortize their initial investments in early-life education and human capital over a much longer economic horizon. Furthermore, a highly compressed period of morbidity at the very end of a 120-year life would mean that lifetime healthcare costs, when annualized over a century, could actually represent a smaller, more manageable percentage of total GDP than they do in the current 80-year demographic paradigm 1019.

Dispelling the Lump of Labor Fallacy in an Era of Extreme Longevity

As structural reforms and biological advancements inevitably push older cohorts to remain in the workforce into their seventies and eighties, a persistent political and economic anxiety arises: the fear that older workers delaying retirement will "crowd out" younger entrants from the labor market. This zero-sum view of employment is rooted in the "lump of labor" fallacy, which erroneously assumes that an economy possesses a fixed, finite number of jobs that must be rationed among the population 11121314.

Extensive empirical evidence from major economic bureaus and rigorous cross-country panel data systematically refutes this fallacy 111516. Time-series analyses demonstrate that the employment rates of younger and older workers are positively correlated, not negatively correlated, across both advanced and emerging economies 111428. In the long run, macroeconomic models show that younger and older cohorts act as complements rather than substitutes within the broader economic ecosystem.

When older workers delay retirement, they continue to generate labor income, which in turn sustains higher levels of aggregate demand through their ongoing consumption 1113. This sustained consumption directly stimulates job creation across the broader economy, which ultimately absorbs the labor of younger workers 13. Furthermore, younger and older workers typically occupy entirely different segments of the labor market and possess highly differentiated skill sets. Older workers leverage decades of accumulated human capital, specialized institutional knowledge, and deep relationship networks, whereas younger workers bring updated technical skills, geographical mobility, and adaptability 1315. Research by Goldin and Katz (2007) and recent empirical studies highlight that skill complementarity between these generations drives overall productivity higher, making the labor force more dynamic rather than stagnant 15.

Historical policy experiments confirm this complementary dynamic and highlight the dangers of misunderstanding labor markets. In the late twentieth century, several European nations, including France, Denmark, Belgium, and the Netherlands, implemented early retirement schemes that were explicitly designed to open up vacancies for unemployed youth 11151628. These programs, such as the UK's Redundancy Payments Act of 1965 and the Dutch Gradual Retirement Programs, universally failed to reduce youth unemployment 1415. In reality, incentivizing the early exit of older workers reduced overall economic output, shrank the national tax base, and depressed aggregate demand, which ultimately harmed the job prospects of the very younger generations these policies were intended to help 111528.

A comprehensive 2024 World Bank analysis of the Indonesian labor market - a rapidly aging society with a high youth population - reaffirmed these historical findings. The empirical analysis concluded that an increase in the employment of older persons robustly increases employment opportunities for younger persons across all genders, education levels, and economic sectors 13. Therefore, in a 120-year lifespan scenario, policies that successfully keep octogenarians engaged in productive labor will be essential drivers of macroeconomic expansion and youth prosperity, rather than obstacles to intergenerational equity.

Demographic Divergences: Geographic Case Studies in Aging

The macroeconomic shock of radical longevity will not be distributed evenly across the global economy. Different nations are entering this demographic transition at different stages of economic development and with vastly different policy frameworks, creating a highly heterogeneous global landscape that requires tailored fiscal strategies.

Japan serves as the vanguard of the global aging phenomenon, boasting the highest life expectancy among major economies (averaging 85 years) and serving as a real-time laboratory for structural demographic adjustments 617. The transition to a high old-age dependency ratio took only 19 years in Japan, during which the nation faced significant headwinds in GDP growth, a phenomenon often categorized by macroeconomists as secular stagnation 818. Japan's high savings rate peaked at 34.1 percent in 1991, reflecting a population bracing for prolonged retirements. This savings glut subsequently drove down real interest rates and contributed to decades of deflationary pressure 1819. To counter the shrinking workforce, Japan has heavily subsidized the retention and re-employment of older workers. Since 2003, the government has provided direct financial grants to employers who hire or retain workers aged 45 to 64, and variable financial aid to medium enterprises that provide opportunities for employees to work until age 70, demonstrating that an economy can adapt to extreme aging through aggressive labor market interventions 20.

China, by contrast, is experiencing rapid demographic aging before reaching the high-income status enjoyed by Japan or Western Europe. The legacy of the one-child policy has artificially accelerated the demographic transition, with the working-age population (ages 20 - 60) projected to contract from 840 million to roughly 614 million by 2050, representing an average annual decline of 1.2 percent 8. Recognizing the acute threat to its state pension budgets and overall economic growth, China enacted historic structural reforms in late 2024. For the first time since the 1950s, the Chinese government legislated a gradual increase in the statutory retirement age. Over a 15-year period starting in 2025, the retirement age for men will rise from 60 to 63, while the age for women will rise from 50 to 53 for blue-collar workers and from 55 to 58 for white-collar workers 821. Additionally, the minimum pension contribution period required to receive benefits will be extended from 15 to 20 years by 2030 821. While this centralized, top-down intervention is designed to stabilize the pension system, the rapid contraction of the youth labor force alongside radical longevity gains will require China to pivot heavily toward artificial intelligence, automation, and industrial upgrading to maintain global productivity 18.

European nations offer a different model, characterized by decentralized, varied responses to state welfare pressures. Denmark represents the most mathematically rigorous and forward-looking approach to longevity. Since a landmark 2006 welfare agreement, Denmark has structurally linked its statutory retirement age to national life expectancy, ensuring that the retirement age automatically adjusts upward without requiring highly politicized legislative battles every few years 1522. In 2025, the Danish Parliament passed legislation by a decisive 81 to 21 vote that will gradually raise the retirement age to 70 by 2040 for anyone born after 1970 1522. Models suggest the Danish retirement age could theoretically exceed 74 if longevity trends accelerate toward the 120-year mark 35. Italy, conversely, represents the political friction of aging. Despite facing a rapidly shrinking population and severe fiscal pressures, intense political resistance from labor unions has led to proposals to freeze the retirement age at 67, exacerbating long-term solvency risks and guaranteeing a heavy future tax burden on younger cohorts 635.

Nations like the United States and Canada rely on a fundamentally different mechanism to offset demographic drag: high rates of inward immigration 2324. The U.S. currently suffers from a notably lower life expectancy (79.0 years in 2024) relative to its OECD peers (averaging 82.7 years) due to systemic healthcare inefficiencies, high obesity rates, and elevated mortality from chronic diseases and overdoses, despite spending nearly $14,885 per person on healthcare 26. However, its demographic pyramid is continually stabilized by the influx of working-age immigrants, which acts as a demographic shock absorber, ensuring a steady supply of labor and taxpayers to fund current-generation liabilities 2324. Nevertheless, if radical life extension biotechnology becomes widely accessible, even high-immigration nations will eventually be forced to restructure their Social Security and Medicare systems. The mathematical burden of financing 50-year retirements would easily surpass the fiscal capacity of any reasonably sized youth labor force, eventually requiring the U.S. to adopt structural indexing similar to the Danish model 15.

Updates to the Life-Cycle Hypothesis: Savings, Capital Accumulation, and Interest Rates

Franco Modigliani's foundational Life-Cycle Hypothesis (LCH) posits that individuals systematically manage consumption over their lifetimes by accumulating wealth during their peak earning years and subsequently dissaving during retirement to maintain a smoothed standard of living 525. The advent of a 120-year lifespan fundamentally fractures the standard calibration of this model, necessitating profound adjustments to aggregate savings behavior, wealth accumulation curves, and macroeconomic capital formation 2627.

Under the standard LCH assumptions anchored to an 80-year lifespan, an individual accumulates wealth steadily until reaching a peak at the traditional retirement age of 65. Following retirement, this accumulated capital is gradually drawn down to zero over a 15-year decumulation phase. However, modeling a 120-year lifespan reveals a drastic divergence in this trajectory. To fund a 55-year post-work period, the accumulation phase must be far steeper, and the ultimate peak wealth target at retirement must scale exponentially higher than historical baselines. Rather than a modest hump, the wealth curve for a 120-year life requires an aggressive, sustained upward trajectory, culminating in a massive capital reserve that is then very slowly decumulated over half a century.

If individuals expect to live to 120, the target level of wealth required to finance retirement scales to unprecedented levels 7. Under a classic 80-year lifespan model, a savings rate of 10 to 15 percent of gross income might be sufficient to achieve a reasonable replacement rate for a 15-year retirement 28. However, if the retirement phase expands to 40 or 50 years, the mathematics of capital accumulation become brutally unforgiving. Actuarial models indicate that funding a multi-decade retirement without proportional extensions in working years would require required savings rates to surge to an untenable 35 percent of gross income - or potentially 60 to 80 percent higher than historical norms for high earners in low-return environments 928.

This microeconomic behavioral shift translates into a massive macroeconomic distortion. As entire populations simultaneously increase their age-specific savings rates to prepare for century-long lifespans, the aggregate supply of loanable funds in the global economy expands drastically 2642. According to standard Ramsey frameworks, this hyper-accumulation of capital drives the capital-to-output ratio to historical highs, sequentially forcing down the marginal product of capital 27.

The inevitable consequence of this demographic-induced savings glut is a secular decline in the natural equilibrium real interest rate ($r^*$) 72729. Recent working papers from NBER and CEPR, including studies by Beaudry et al. (2024) and Greenwald et al. (2023), demonstrate that life-cycle forces and longevity expectations exert a far stronger downward pull on real rates than previously modeled 7. Central banks across advanced economies have already observed long-term real interest rates falling by over 400 basis points over recent decades, a trend heavily influenced by the aging of populations 2742. In a world characterized by extreme longevity, natural interest rates may become structurally anchored near or below the zero lower bound, establishing a persistent state of "secular stagnation" 2742. This dynamic severely restricts the traditional monetary policy transmission mechanism, as central banks lose the conventional capacity to stimulate aggregate demand during cyclical downturns without resorting to permanent, aggressive quantitative easing 72542.

Furthermore, contemporary empirical data challenges the expected rapid decumulation phase of the LCH. Economists have identified a "Wealth Decumulation Puzzle," wherein retirees, paralyzed by the uncertainty of their ultimate lifespan and terrified of escalating end-of-life healthcare costs, maintain or even aggressively increase their net wealth well into their final decades 525. In a 120-year lifespan environment, this intense risk aversion - compounded by the inability of the elderly to recuperate from financial setbacks - would lock vast reserves of global capital in highly conservative, low-yield safe-haven assets, such as government bonds, starving productive, high-risk entrepreneurial ventures of essential liquidity 529.

The Silver Economy: Aggregate Demand and the Transformation of Consumption

The extension of the human lifespan will not merely shift the volume of macroeconomic variables; it will fundamentally restructure the composition of aggregate demand. The emergence of the "Silver Economy" - a sprawling market ecosystem geared toward the consumption preferences, healthcare needs, and lifestyle aspirations of older cohorts - is projected to become one of the primary engines of global GDP over the coming decades 1244. In China alone, the Silver Economy is forecast to reach 30 trillion CNY (approximately $4.3 trillion USD), representing roughly 10 percent of the country's GDP by 2035, signaling a transition from a niche sector to a foundational economic pillar 1245.

Historically, economic models assumed that consumption patterns for the elderly were dominated almost entirely by non-discretionary healthcare expenditures, basic housing, and conservative staple goods. However, the advent of morbidity compression and the rise of a demographic group identified in recent market research as "savvy silvers" are rewriting this narrative 129. A 2025 consumer survey by Accenture focusing on 55 - 65-year-olds in China revealed a dramatic shift in behavior: multi-generational co-living dropped from 75 percent in 2021 to just 38 percent in 2025, with older consumers increasingly choosing to live alone or with spouses 12. This reflects a broader psychological pivot. Individuals who retain high physical and cognitive function into their advanced years are actively transitioning their capital away from traditional family-first preservation toward self-actualization, experiential spending, and proactive vitality management 1244.

Over a 120-year lifecycle, the traditional three-stage model of existence (education, continuous work, brief retirement) becomes structurally obsolete. Aggregate demand will increasingly rotate toward lifelong learning, continuous professional retraining, and recurrent sabbaticals 44. As centenarians seek to maintain social visibility, agency, and dignity, capital will flood into new sectors: advanced preventative biotechnology, smart co-housing developments designed to mitigate the health risks of social isolation, artificial intelligence-assisted personal logistics, and extensive leisure travel 122044. The transition of the Silver Economy from a peripheral, healthcare-dominated niche into a technology-driven, multi-trillion-dollar engine of discretionary spending will require corporations to entirely recalibrate their product development cycles and marketing architectures. They must address a consumer base that prioritizes emotional resonance, longevity dividends, and sustained independence over pure functional utility 1245.

Intergenerational Wealth Inequality and Compounding Capital

Perhaps the most destabilizing macroeconomic consequence of a 120-year lifespan is the radical distortion of intergenerational wealth transfers. In historical demographic regimes, inheritances typically passed to the next generation when the heirs were in their forties or early fifties - a critical life-cycle juncture where capital injections could be deployed to eliminate mortgage debt, finance entrepreneurial ventures, or fund the higher education of the subsequent generation 6.

Under a radical longevity paradigm, the velocity of capital transfer grinds to a halt. If the accumulator lives to 120, their heirs will not receive inheritance distributions until they are in their eighties or nineties. This decades-long delay structurally neutralizes the historical equalizing function of inheritances, preventing younger generations from utilizing inherited capital during their peak productive years 630. Demographic aging and delayed capital transfer systematically sever the liquidity lifelines that historically allowed credit-constrained younger cohorts to build wealth.

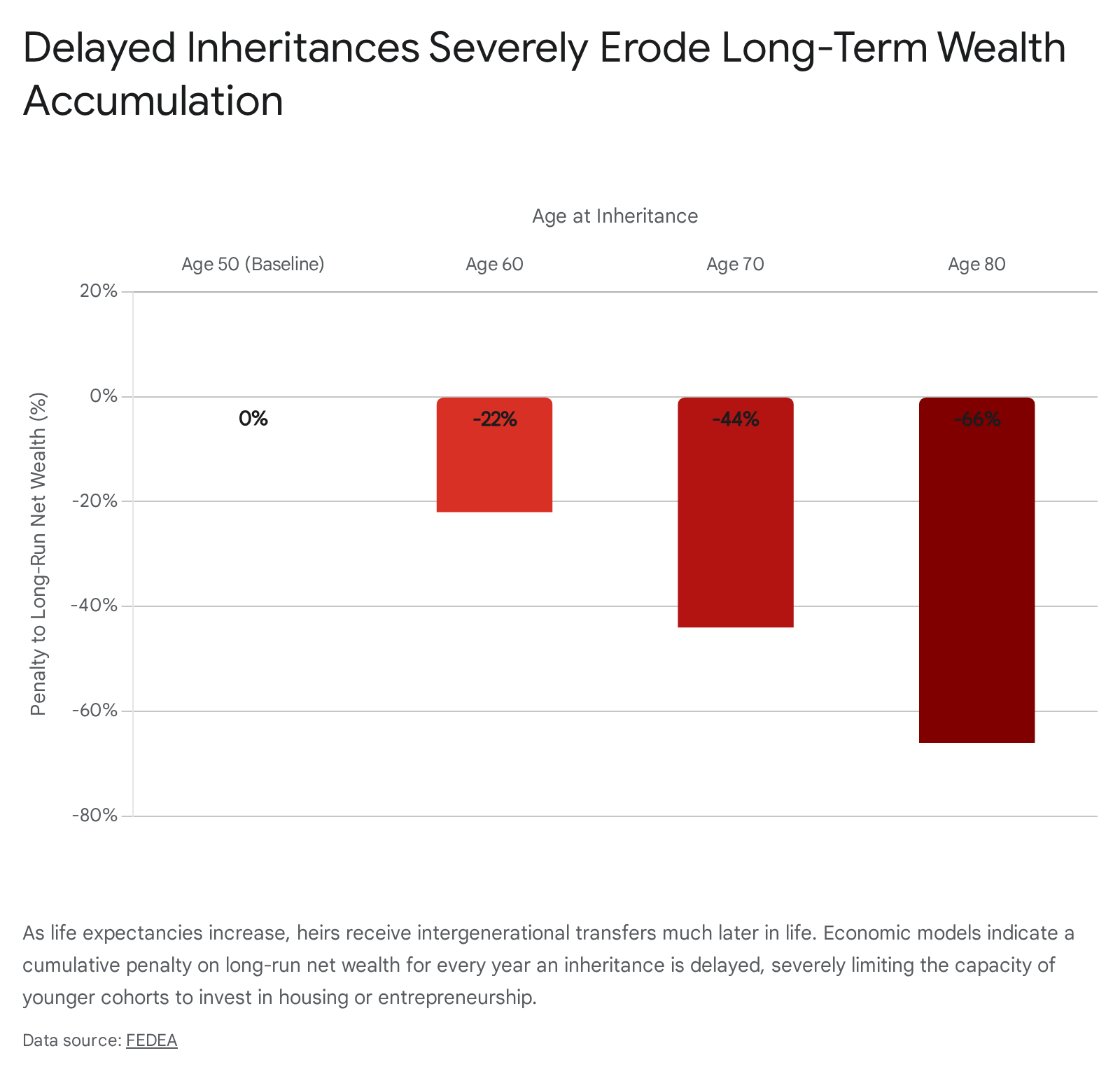

The exact mechanism of this inequality is rooted in the mathematics of compound interest and collateralization. Wealth accumulation is heavily dependent on the duration of exposure to compounding returns. An inheritance received at age 50 provides 30 years of capital compounding and acts as immediate collateral to unlock credit markets 6. Conversely, economic research demonstrates a severe "timing penalty" for delayed transfers. Each additional year of delay in receiving an inheritance is associated with a reduction in long-run net wealth of approximately 2.0 to 2.25 percent 6. A delay of just ten years (receiving inheritance at 60 rather than 50) is associated with a net wealth reduction of roughly 22 percent 6.

By the time an heir reaches 80, the marginal utility of the inheritance is vastly diminished; it can no longer be leveraged to shape key economic life-cycle decisions, such as homeownership or starting a business 6.

Crucially, this timing penalty is highly asymmetric across socioeconomic and racial strata, serving as an accelerant for systemic inequality. Highly educated, high-income households possess robust self-financing capacities and generate substantial labor income; their long-run wealth trajectories are largely insulated from the exact timing of external inheritances 6. Furthermore, wealthy patriarchs and matriarchs can bypass the timing penalty entirely through strategic inter vivos transfers (living gifts), systematically shifting resources forward in time to advantage their descendants 6. Because these early transfers are disproportionately received by already wealthy families, the mechanism reinforces wealth concentration rather than offsetting it 6.

Recent historical analyses by Derenoncourt et al. (2022, 2024) on long-run wealth gaps emphasize that delayed capital access drastically alters convergence paths 2431. When initial capital disparities exist, identical savings rates fail to close the wealth gap; capital must be actively deployed early in the life cycle to achieve parity 2431. Conversely, households with lower educational attainment and constrained credit access depend heavily on the timing of inheritances to alter their socioeconomic trajectory. Because these constrained households are the least likely to receive early inter vivos interventions, radical longevity will act as a permanent compounding engine for systemic wealth inequality, entrenching capital within dynastic structures for over a century while younger, working-class cohorts remain starved of liquidity 63031.

Fiscal Projections: 80-Year vs. 120-Year Lifespan Scenarios

To quantify the macroeconomic divergence between the current demographic paradigm and a radically extended lifecycle, standard fiscal models must be recalibrated. The following table models the theoretical divergence across three scenarios: the historical baseline (anchored to an 80-year lifespan), a "Frail Extension" scenario where the lifespan reaches 120 without equivalent healthspan gains, and a "Morbidity Compression" scenario where individuals work proportionally longer in good health.

| Macroeconomic Metric | Baseline (80-Year Lifespan) | 120-Year Lifespan (Frail Extension) | 120-Year Lifespan (Morbidity Compression) |

|---|---|---|---|

| Statutory Retirement Age | 65 Years | 65 Years | 95 Years |

| Years in Retirement | 15 Years | 55 Years | 25 Years |

| Old-Age Dependency Ratio | ~30% (3 workers per retiree) | ~110% (< 1 worker per retiree) | ~40% (2.5 workers per retiree) |

| Required Savings Rate | 10% - 15% | 35%+ (Mathematically Untenable) | 12% - 18% |

| Healthcare % of GDP (U.S.) | ~18% | 35%+ (Systemic Insolvency) | ~20% (Amortized over longer timeline) |

| Natural Interest Rate ($r^*$) | Moderately Positive | Deeply Negative (Severe ELB Constraint) | Stable to Slightly Depressed |

Note: Projections synthesized from actuarial life-cycle accumulation models, historical OECD baseline data, and demographic compression theories 91610272832.

The projections validate the absolute necessity of tying statutory retirement ages to life expectancy, mirroring the structural mechanisms pioneered by Denmark 1522. Under the "Frail Extension" scenario, keeping the retirement age static at 65 produces an apocalyptic old-age dependency ratio where retirees outnumber active workers. The resulting required savings rate breaches 35 percent of gross income, a threshold that is effectively impossible for median earners, which would obliterate current consumption and crash aggregate demand 949. Furthermore, financing five decades of intensive end-of-life care would push healthcare expenditure to consume over a third of global GDP, effectively bankrupting sovereign state budgets and eliminating public investment in other sectors 1033.

The "Morbidity Compression" scenario, however, demonstrates a sustainable macroeconomic equilibrium. By proportionately extending the working life to 95, the old-age dependency ratio remains manageable, and the required savings rate stabilizes near historical norms. The integration of advanced senolytics and preventative biotechnology curbs the explosion of healthcare costs, allowing the economy to harness a century of compounded human capital, fuel the innovative Silver Economy, and preserve the fiscal integrity of the state 1621.

Conclusion

The transition toward a 120-year human lifespan constitutes the most profound structural shock to macroeconomic theory since the Industrial Revolution. The evidence clearly dictates that radical longevity cannot be treated as a purely medical breakthrough; it is a fundamental reconfiguration of capital, labor, and time.

If this demographic shift manifests as an extension of frail, dependent years, it threatens to trigger unprecedented sovereign debt crises, collapse natural interest rates into permanent secular stagnation, and suffocate global economic dynamism beneath the weight of insurmountable healthcare liabilities. However, if radical longevity is achieved through morbidity compression - extending the period of vigorous, productive health alongside chronological age - it offers the potential for a massive, multi-trillion-dollar longevity dividend.

Realizing this dividend requires aggressive, preemptive policy architecture. Governments must permanently dispel the lump of labor fallacy and actively integrate octogenarians into the workforce, recognizing that older labor expands aggregate demand rather than crowding out youth employment. Furthermore, sovereign states must immediately explore structural mechanisms to link retirement ages dynamically to life expectancy, following the Danish model, while simultaneously addressing the severe intergenerational inequalities bred by century-long delays in capital transfer through reformed tax and inter vivos transfer policies. Ultimately, the macroeconomics of a 120-year lifespan demand a transition away from rigid, age-based financial milestones toward fluid, probability-weighted lifecycles, ensuring that the greatest triumph of human science does not precipitate the collapse of the global economy.