How Reinforcement Learning Teaches AI to Trade

Reinforcement learning is an artificial intelligence paradigm where an algorithm learns to make optimal decisions by interacting with a simulated market, receiving mathematical rewards for profitable actions and facing penalties for losses. By mastering sequential decision-making through millions of trial-and-error simulations, these autonomous agents learn to balance risk, execution timing, and capital allocation without relying on predefined trading rules.

From Prediction to Action: Why Trading Needs a New Approach

For decades, quantitative trading relied heavily on predictive modeling. Traditional machine learning and classical statistics focused predominantly on forecasting: attempting to predict the future price of an asset, estimating upcoming volatility, or classifying a market regime as bullish or bearish. While generating a highly accurate forecast is valuable, it leaves a critical operational gap. Knowing what the market is likely to do does not automatically tell a portfolio manager what specific actions to take regarding capital allocation, execution speed, transaction costs, and portfolio impact 1.

Reinforcement learning (RL) fills this gap by shifting the mathematical focus from pure prediction to optimal policy generation. Rooted in behavioral psychology, reinforcement learning trains agents to make sequences of decisions by interacting with an environment and learning directly from feedback 23. It is the same underlying computational approach that allowed artificial intelligence to master complex, multi-step environments ranging from board games like Chess and Go to the physical navigation required by autonomous vehicles 4567.

Instead of feeding a model historical data packed with labeled, "correct" answers - the standard approach in supervised machine learning - reinforcement learning places an agent in a dynamic environment 38. The agent observes the current state of the market, takes a specific action such as buying, selling, or holding an asset, and then receives a delayed reward based on the eventual financial outcome of that action 52. The core philosophy of applying reinforcement learning to finance is the transition from forecasting to action - teaching an algorithm how to operate under uncertainty to optimize long-term outcomes, rather than just generating a one-step price prediction 1.

The Limitations of Traditional Algorithms

To understand why quantitative funds have aggressively integrated reinforcement learning, it is helpful to examine the limitations of traditional rules-based algorithms and standard machine learning approaches. Traditional algorithmic trading generally operates on preset rules and conditions 1011. A quantitative researcher might define specific parameters, instructing the software to execute a buy order when an asset's price crosses above a moving average, or to sell when a momentum indicator drops below a specific threshold 1012.

While these traditional algorithms effectively remove human emotional decision-making and drastically enhance execution speed, they remain rigid. They execute fixed, hand-coded logic that struggles to adapt when unpredictable market environments emerge 1011. If a market enters a regime that the human programmer did not anticipate, the static rules will continue to execute, often leading to severe losses until the algorithm is manually updated 1013. Furthermore, traditional rules-based systems cannot efficiently process the hundreds of interconnected factors - such as options pricing, liquidity regimes, alternative data, and macroeconomic indicators - that drive modern financial markets 1213.

How Machine Learning Paradigms Compare

While the financial industry recognized the limitations of static rules, early attempts to apply machine learning to trading heavily favored supervised and unsupervised learning, which presented their own challenges.

Supervised learning requires large amounts of labeled data to train a predictive model 1415. For instance, a supervised algorithm might analyze a decade of financial metrics to predict whether a stock will outperform the market over the next quarter 6. However, financial markets are highly volatile and non-stationary. A supervised model seeks to minimize its prediction error based entirely on historical patterns, essentially assuming that future data will behave similarly to past data 1516. When new, unprecedented variables arise - such as a sudden geopolitical conflict or a global pandemic - supervised models often fail because they lack the capacity to adjust their behavior to novel, unlabeled situations 1516. Moreover, supervised models typically optimize for return maximization while ignoring exogenous constraints like execution slippage, lack of liquidity, and transaction costs 16.

Unsupervised learning, conversely, involves training a model on unlabeled data to identify hidden structures, such as clustering similar stocks together based on their price movements or identifying anomalies in trading volume 141517. While highly useful for exploratory data analysis and risk classification, unsupervised learning does not output a definitive trading strategy.

Reinforcement learning bridges these gaps by directly learning a trading strategy that integrates forecasting, risk management, and portfolio construction into a single, continuous step 16.

| Feature | Traditional Rules-Based Trading | Supervised Machine Learning | Unsupervised Machine Learning | Reinforcement Learning |

|---|---|---|---|---|

| Core Mechanism | Executes fixed, hand-coded logic based on human hypotheses. | Maps inputs to known outputs to predict future values. | Identifies hidden patterns or clusters within unlabeled data. | Learns sequential decision-making via trial and error. |

| Data Requirements | Requires explicitly programmed rules and historical price series. | Requires massive datasets with clear, static input-output labels. | Requires large volumes of unlabeled market data. | Requires an interactive environment or high-fidelity simulator. |

| Adaptability | Rigid. Fails when market regimes shift outside programmed parameters. | Prone to overfitting. Struggles with market regime shifts (concept drift). | Adapts to structural data changes, but does not execute decisions. | Highly adaptable. Learns to dynamically update policy as markets change. |

| Treatment of Risk | Relies on static, hard-coded stop-loss levels and position sizes. | Often ignores operational risk, optimizing solely for prediction accuracy. | Used to classify risk profiles, but requires secondary systems for action. | Bakes risk, tail-events, and transaction costs directly into the reward function. |

| Primary Output | Binary execution signals (e.g., execute trade when condition X is met). | A point forecast (e.g., predicted price) or classification. | Segmented data clusters or anomaly alerts. | A dynamic policy mapping market states to optimal actions. |

Data synthesized from industry analyses of algorithmic and machine learning methodologies in finance. 3101114151617

The Anatomy of an RL Trading Agent

To build a reinforcement learning system capable of navigating financial markets, engineers must define five fundamental pillars. If any of these foundational elements are poorly constructed, the agent will inevitably learn destructive behaviors or fail to generalize to live, unpredictable markets. The core of this system is a continuous cyclic flow between the trading agent and the market environment. The agent, driven by a neural network policy, constantly observes the current market state. Based on that state, it executes an action, which the environment processes. The environment then returns an updated state and a mathematical reward reflecting the profit or loss of that action, closing the loop and allowing the agent to refine its strategy.

1. The Environment

The environment is the simulated world in which the agent operates. In the context of quantitative trading, this is a highly complex simulated financial exchange that processes the agent's actions, calculates the resulting financial outcome, and transitions the market to the next chronological time step 2. A robust environment enforces all the structural rules of the actual market, including margin requirements, fractional position limits, borrowing costs, trading hours, and capital constraints 8319. Without a realistic environment, the agent cannot learn practical trading mechanics.

2. The State (Observation Space)

The state represents the totality of information the agent observes at any given moment before making a decision. This observation space is highly customizable and typically includes a massive vector of features 25820. A state might encompass traditional technical indicators like moving averages, relative strength index (RSI) values, and rolling volatility estimates. It can also include raw order book depth, macroeconomic indicators, and alternative data feeds 81320. Crucially, the state must also include the agent's internal status, such as its current cash allocation and existing long or short positions, so the agent understands its own exposure to the market at all times 8.

3. The Action Space

The action space defines exactly what the agent is permitted to do within the environment. The simplest reinforcement learning trading environments utilize a discrete action space limited to basic commands: Buy, Hold, or Sell 5204. However, modern institutional applications demand much more nuance, leading to the use of continuous action spaces. Rather than a simple binary "Buy" command, an agent operating in a continuous action space might output a fractional number to dictate position sizing. For example, an output of +0.5 might instruct the system to allocate exactly 50% of the portfolio to an asset, while an output of -1.0 would signal an aggressive short position using borrowed capital 34. More advanced agents can also decide on the specific limit price at which to place an order, or determine the exact routing path to use across multiple fragmented exchanges 45.

4. The Reward Function

The reward signal is the ultimate objective the agent is attempting to maximize over time. In a closed-system game like chess, the reward is straightforward and binary: win or lose. In the noise-filled domain of finance, reward engineering is notoriously difficult and critical to success. If a financial agent is rewarded solely for generating raw, absolute profit, it will almost certainly learn highly risky, over-leveraged strategies that eventually result in catastrophic account blow-ups during inevitable market downturns 81620.

Consequently, quantitative developers rely on a technique called "reward shaping" to mathematically penalize excessive risk and encourage stable growth. Modern agents are rarely rewarded for raw profit alone. Instead, they are rewarded based on risk-adjusted metrics like the Sharpe ratio, or penalized heavily for experiencing large peak-to-trough drawdowns 262023. Furthermore, an agent will typically be docked points for exhibiting high portfolio turnover to simulate the drag of transaction costs and exchange fees, forcing it to learn that excessive trading is counterproductive 2023.

5. The Policy

The policy is the operational "brain" of the agent. It is the complex logic - typically represented by a deep neural network - that maps the observed state of the market to the most optimal action. During the training phase, the agent must constantly balance two competing forces: exploration and exploitation 232. Early in its training, the agent's policy heavily favors exploration, executing random actions to discover how the environment reacts and to uncover potentially hidden, highly profitable strategies 23. As the agent accumulates experience and maps out the consequences of its actions, the policy mathematically decays its exploration rate and shifts toward exploitation - relying on the best-known strategies it has discovered to secure reliable, long-term rewards 22.

The "Crystal Ball" Challenge: Why Prediction Is Insufficient

A pervasive misconception among retail investors and novice quantitative developers is that achieving outsized returns in financial markets simply requires a highly accurate predictive model. They assume that if an algorithm can accurately forecast whether an asset will go up or down, immense profitability will naturally follow. This fallacy was brilliantly exposed in an experiment dubbed "The Crystal Ball Challenge," conducted by researchers Victor Haghani, a founding partner of the famed hedge fund Long-Term Capital Management, and James White, CEO of Elm Partners 242526.

Inspired by the theories of quantitative analyst and author Nassim Nicholas Taleb, the researchers sought to test how traders would perform if they possessed actual foresight 242627. In late 2023 and early 2024, they conducted a proctored experiment involving 118 financially trained young adults and seasoned macro traders. Participants were given a simulated $1 million in capital and a seemingly unbeatable edge: they were shown the actual front pages of the Wall Street Journal a full day in advance of major historical market moves spanning a 15-year period 2627. They possessed perfect, guaranteed foresight of major economic news, such as exact Federal Reserve interest rate decisions and geopolitical shocks, though the specific magnitude of the resulting market price action was redacted 2427.

Despite possessing an overwhelming informational advantage that effectively removed the need for prediction, the participants performed abysmally. The empirical data revealed that knowing the news in advance did not translate to wealth generation.

The Cost of Poor Position Sizing

The results of the Crystal Ball Challenge demonstrated a severe gap between possessing theoretical knowledge and successfully executing practical application 25. Approximately half of the participants lost money over the course of the simulation, and roughly 16% went completely bankrupt 26. The average payout across the board represented a mere 3.2% gain, a figure statistically indistinguishable from simply breaking even 26.

Even among the most elite cohort of participants - professional, seasoned macro traders - the results were startling. While these top-tier investors accurately guessed the direction of the market's movement 63% of the time, their median ending wealth after the 15 rounds of trading represented a loss of 31% 2427.

The primary catalyst for this widespread failure was a lack of rigorous risk management and catastrophic errors in position sizing. When participants believed they had a "sure thing" based on the future news, they routinely over-leveraged their accounts to maximize gains 2425. Because the exact magnitude of the market's reaction was unknown, interim volatility or slight miscalculations resulted in margin calls and total account ruin 2425. Conversely, other participants fell victim to cognitive biases such as loss aversion, severely under-betting on highly favorable outcomes and failing to compound their wealth optimally 25. The experiment unequivocally proved that informational advantages and accurate predictions do not guarantee wealth preservation without disciplined, mathematically sound capital allocation 2526.

How Reinforcement Learning Solves the Execution Problem

The conclusions drawn from the Crystal Ball Challenge perfectly illustrate why institutional quantitative funds are transitioning away from standard supervised machine learning toward reinforcement learning architectures.

A supervised learning model functions much like the crystal ball in the experiment: it ingests historical data and outputs a prediction regarding the probability that a specific asset will rise or fall. However, as the human participants demonstrated, a prediction is operationally useless without a surrounding framework for execution 126.

A reinforcement learning agent, by contrast, operates as an autonomous, disciplined portfolio manager. It does not merely predict a price movement; it mathematically determines the optimal sequence of actions required to capitalize on that movement. The RL policy continuously calculates exactly how much capital to allocate to a specific trade, determines the optimal threshold for a dynamic stop-loss, and dictates how to strategically scale into or out of a position over time 1. By integrating prediction, risk assessment, and position sizing into a unified mathematical objective, the agent maximizes expected returns while strictly capping the statistical risk of ruin 1.

Practicing in the Sandbox: How Agents Learn Without Losing Money

One of the most significant hurdles in developing robust machine learning systems is the inherent cost of failure during the learning phase. An autonomous vehicle cannot be permitted to learn how to navigate intersections by crashing real cars on public highways. Similarly, an untrained artificial intelligence trading agent cannot be unleashed on live brokerage accounts while its neural network is still making random, exploratory decisions that would obliterate real capital 84.

To solve this problem, quantitative researchers rely on high-fidelity market simulators. Frameworks like Gymnasium - an open-source Python library maintained by the Farama Foundation that serves as a fork of the widely used OpenAI Gym - provide standardized environments for developers to build and benchmark reinforcement learning algorithms 192829. Within the financial domain, highly specialized environments like TradingGym and ABIDES (Agent-Based Interactive Discrete Event Simulation) allow agents to train on vast repositories of historical tick data 2330.

Through these simulators, an agent can step through decades of historical price action, executing millions of simulated trades in a highly compressed timeframe 3132. This rapid iteration cycle allows the agent to continuously update its policy, learning which specific combinations of technical indicators and macroeconomic data point toward profitable trades, and precisely when a strategy ceases to function 43132.

Avoiding Simulator Traps: Slippage, Latency, and Impact

While simulated training is absolutely mandatory, it carries a severe and pervasive risk: the simulator might not accurately reflect the harsh realities of live financial markets. If a simulated training environment is too simplistic, the reinforcement learning agent will inevitably exploit unrealistic loopholes in the code rather than discovering genuine, deployable market alpha 4. Several specific traps consistently plague novice quantitative developers:

- The Illusion of Zero Slippage: In a rudimentary simulator, the environment assumes an agent can execute an order of any size at the exact historical closing price recorded in the dataset. In live markets, particularly when dealing with large institutional order sizes, trades experience slippage 820. A massive market order will eat through the available liquidity in the order book, resulting in an average execution price that is significantly worse than the initial quoted price 20. If a simulator ignores slippage, the agent will learn a hyper-active, high-frequency trading strategy that exploits microscopic price variations - a strategy that will immediately generate massive losses when deployed live due to execution costs.

- Ignoring Network Latency: If a simulation assumes trades are executed instantaneously, the agent will learn to front-run data without accounting for the actual milliseconds it takes for a digital order to travel from a server to an exchange's matching engine 4.

- The Absence of Market Impact: When an institutional agent buys millions of dollars of a specific equity, its own aggressive purchasing action drives the price of the asset upward. Traditional backtesting models frequently ignore this phenomenon, assuming the agent's actions occur in a vacuum 14. Sophisticated reinforcement learning environments must endogenously simulate how other market participants will react to the agent's own presence in the market 14.

To counter these simulation traps, advanced financial researchers now construct complex, highly realistic simulators that mathematically enforce latency penalties, model dynamic transaction costs based on historical spreads, and simulate transient market impact 20423.

Backtesting Rigor and Synthetic Data

Even with a highly realistic simulator, an agent trained exclusively on a single set of historical data is highly susceptible to overfitting - memorizing the specific noise of the past rather than learning generalizable market principles 111520. To ensure an agent's strategy is actually robust, developers employ rigorous out-of-sample testing methodologies.

A standard practice is walk-forward optimization, where an algorithm is trained on a specific segment of data (e.g., 2015 to 2018) and then tested on an entirely unseen, subsequent segment of data (e.g., 2019) to observe how it performs in novel market conditions 33. To further stress-test agents, researchers are increasingly utilizing synthetic data generation. By mathematically creating artificial, yet statistically plausible, price histories, researchers can subject an agent to hypothetical market scenarios - such as unprecedented volatility spikes, prolonged liquidity droughts, or flash crashes - that did not explicitly occur in the available historical dataset 34. This ensures the agent learns adaptive behaviors rather than simply memorizing the timeline of past events 34.

Navigating Volatility: Black Swans and Market Regimes

Despite its vast advantages over static rules-based systems, reinforcement learning is not a flawless solution. One of its most significant vulnerabilities is its performance during "Black Swan" events - highly improbable, catastrophic market shocks that carry massive consequences and lie far outside the scope of historical patterns 3536.

Because reinforcement learning algorithms learn inductively by optimizing for average errors and standard distributions within past environments, they perform brilliantly during stable, recognizable market regimes 36. However, they can fail catastrophically when those regimes shift abruptly and the fundamental mechanics of the market change 36. In academic experiments evaluating the efficacy of reinforcement learning algorithms during the sudden, unprecedented market crash of March 2020, researchers found that standard value-based models, such as basic Q-Learning architectures, struggled immensely to adapt 35. These agents suffered severe drawdowns because their neural networks had never "experienced" such a rapid evaporation of liquidity and simultaneous cross-asset correlation 35.

Advanced Risk Mitigation Strategies

To mitigate the existential risks posed by Black Swan events and sudden volatility, modern quantitative research has shifted focus toward highly advanced, risk-aware architectures designed to manage extreme tail events:

- Distributional Reinforcement Learning: Standard reinforcement learning models calculate the expected, average mathematical reward for a given action. Distributional models, however, learn to predict the entire probability distribution of possible outcomes 1. This nuanced understanding of variance allows the agent to recognize and actively avoid actions that might have a profitable average outcome but carry a small, unacceptable probability of catastrophic failure 1.

- Risk-Sensitive Reward Shaping: Instead of optimizing purely for average returns, modern agents incorporate advanced risk metrics directly into their reward functions. By utilizing metrics like Conditional Value at Risk (CVaR), the mathematical penalty heavily weights the worst-case scenarios 123. This forces the agent to optimize its strategy specifically to minimize tail-risk exposures during catastrophic market days 23.

- Queue-Reactive Simulators: To prepare agents for the reality of vanishing liquidity during crashes, researchers are moving away from static historical data toward Queue-Reactive Models 23. These sophisticated simulators dynamically adjust the arrival times of orders based on the depth of the simulated order book, producing the transient impact and nonlinear flow responses seen in real, highly volatile markets. This forces the agent to learn tactical execution strategies in environments where liquidity is scarce and unpredictable 23.

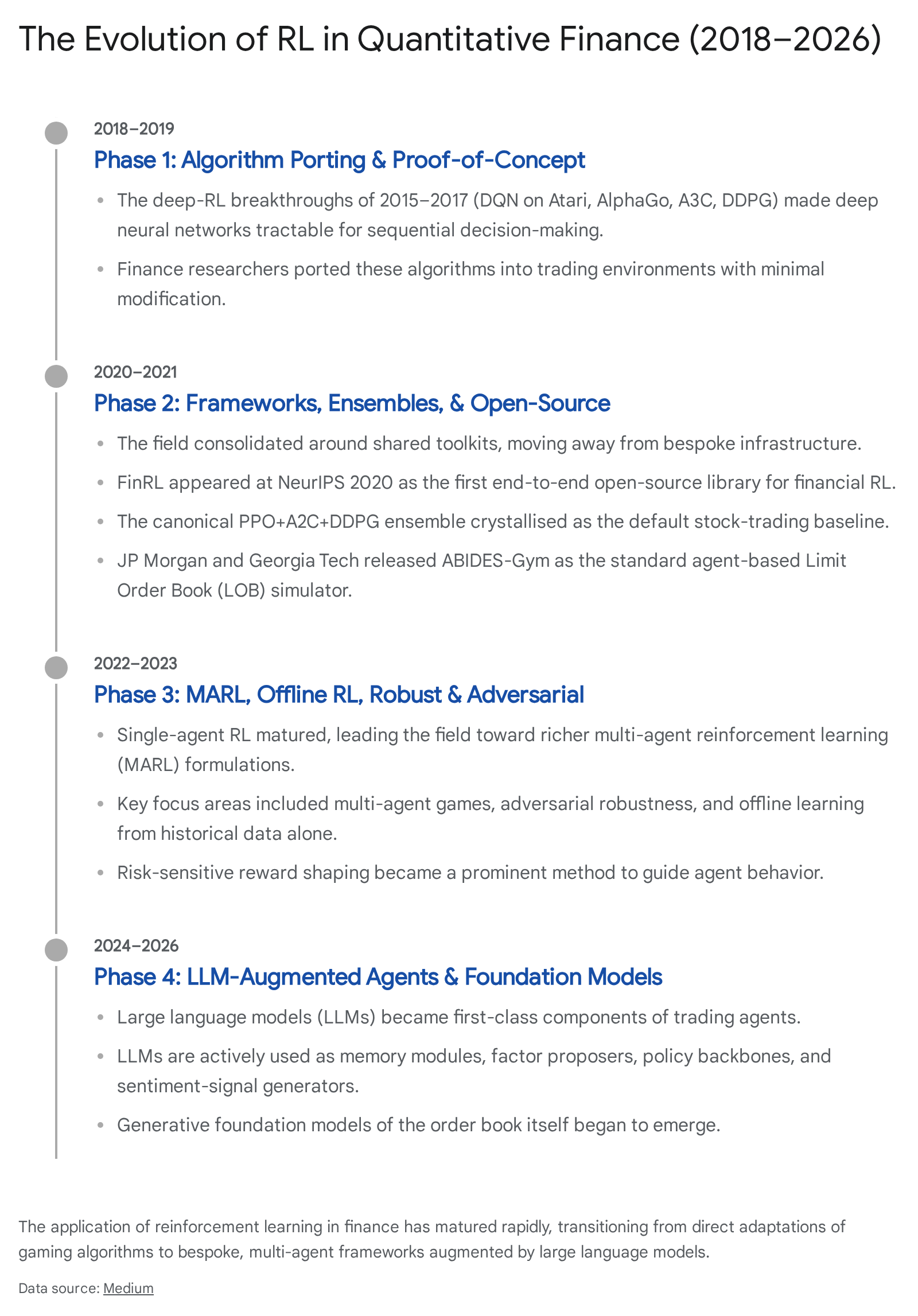

The Evolution of Reinforcement Learning in Finance (2018 - 2026)

The integration of reinforcement learning into quantitative finance has not been a slow, gradual process; it has evolved rapidly through four distinct phases of academic and industrial development over less than a decade.

In the initial phase (roughly 2018 to 2019), quantitative researchers focused on direct algorithm porting and proof-of-concept models 23. During this era, deep reinforcement learning breakthroughs that had conquered video games - such as Deep Q-Networks (DQN) on Atari systems or AlphaGo - were adapted to financial time series data with minimal modification 723. These early systems proved that neural networks were tractable for sequential financial decision-making, though they relied on idiosyncratic benchmarks and bespoke infrastructure 23.

The second phase (2020 to 2021) brought much-needed standardization to the field. Researchers consolidated their efforts around shared, open-source toolkits 23. The release of FinRL at the NeurIPS 2020 conference marked a turning point, providing the first end-to-end open-source library specifically designed for financial reinforcement learning 23. Concurrently, frameworks like ABIDES-Gym established standardized agent-based limit order book simulators, allowing researchers globally to reproduce results and benchmark canonical ensemble algorithms, such as Proximal Policy Optimization (PPO) combined with Advantage Actor-Critic (A2C) architectures 2337.

By phase three (2022 to 2023), single-agent reinforcement learning had matured, and researchers began tackling significantly richer, more complex formulations. The focus shifted toward Multi-Agent Reinforcement Learning (MARL), adversarial robustness, and offline learning from historical data alone 23. This era explored how individual algorithms behaved when thrust into a market teeming with other learning agents. Notably, research demonstrated the concept of "tacit collusion," revealing that independent reinforcement learning market makers could mathematically converge to maintain wide spreads above competitive levels without any explicit, programmatic coordination, thereby maximizing collective dealer profits 23. Researchers also made strides in addressing time-varying liquidity and latent market regimes, training agents to aggressively deploy capital when liquidity was abundant and to intuitively scale back when order books thinned out 23.

The Fourth Phase: LLM-Augmented Agentic Architectures

The most profound paradigm shift in financial reinforcement learning has emerged recently (2024 to 2026), characterized by the seamless integration of Large Language Models (LLMs) directly into agent architectures 23.

Historically, reinforcement learning agents in finance were highly specialized calculators, ingesting purely numerical streams of price data, moving averages, and volume statistics. Today, cutting-edge systems deploy multi-agent collaborative frameworks where LLMs serve as the cognitive sensory organs for the RL execution engine 383940. In these hybrid frameworks, an LLM acts as a high-speed feature extractor. It might simultaneously ingest real-time news articles, dense SEC 10-K filings, and live earnings call transcripts, using semantic processing to map complex narratives into quantified market sentiment probabilities 384142.

These LLM-derived sentiment scores and regime predictions are then fed directly into the reinforcement learning agent's observation state alongside traditional numerical data 4142. The RL agent synthesizes this holistic view of the market to make the final, optimized trading decision 4041. Beyond sentiment extraction, leading institutions are now utilizing LLMs as generative "factor proposers" - suggesting novel mathematical trading signals and formulaic alphas that the RL agent then evaluates, scores, and weights based on real-time backtesting, effectively automating portions of the quantitative research process 23.

Institutional Dominance vs. Retail Access

The deployment of these advanced algorithmic systems currently spans a wide spectrum, from the proprietary servers of the world's largest asset managers to increasingly accessible retail trading platforms.

Wall Street's AI Arms Race

Major financial institutions have fully embraced systematic, AI-driven operations to maintain a competitive edge. JPMorgan Chase continues to invest heavily in its technological modernization, with an $18 billion technology budget in 2025 aimed at deploying AI capabilities across trading and customer service operations 6. The firm's internal E-trading surveys reveal that 65% of institutional traders now view artificial intelligence and machine learning as the most influential technology shaping the future of market liquidity and execution 44.

Similarly, BlackRock, the world's largest asset manager, has publicly emphasized its transition toward highly systematic strategies. The firm actively leverages artificial intelligence, foundation models, and immense datasets to identify new sources of "alpha" - investment outperformance - in an era marked by heightened macroeconomic volatility and the conclusion of the Great Moderation 457478.

The Democratization of Algorithmic Infrastructure

For decades, institutional-grade quantitative trading was an exclusive domain, restricted to Wall Street firms possessing vast data centers, direct market access, and armies of PhD researchers. Today, the landscape is shifting as open-source frameworks and specialized brokerage platforms democratize access to advanced algorithmic tools 49.

| Platform | Primary Target Audience | Key Features & Architecture |

|---|---|---|

| QuantConnect | Serious Retail Quants & Systematic Investors | Open-source LEAN engine (Python/C#). Cloud deployment, institutional-grade backtesting, multi-asset coverage, and extensive historical data libraries. |

| Interactive Brokers | Professional Retail & Multi-Asset Traders | Provides the API backbone for algorithmic execution. Offers extensive global market access across equities, futures, options, and forex. |

| TradeStation | Active Automated Traders | Integrated broker and automation platform utilizing EasyLanguage scripting, designed to lower the technical barrier for strategy development. |

| TradingView | Charting & Community Strategy Developers | Renowned charting capabilities utilizing Pine Script for custom indicator creation, backtesting, and massive community strategy sharing. |

| MetaTrader 5 (MT5) | Forex & CFD Algorithmic Traders | Industry-standard stability utilizing the MQL5 programming language, highly favored for its extensive global broker compatibility. |

Summary of prominent retail and professional algorithmic trading platforms in 2026. 495095210

Platforms like QuantConnect allow independent developers to write sophisticated trading logic in Python, backtest strategies on high-resolution tick data, and deploy those algorithms directly to live markets through API integrations with brokers like Interactive Brokers 49910. This infrastructure dramatically lowers the barrier to entry, allowing sophisticated retail quants to experiment with the same deep reinforcement learning methodologies previously isolated to hedge funds 49.

The Evolution of Robo-Advisors

While fully autonomous, reinforcement learning-driven portfolio management is currently confined to institutional use and advanced independent developers, the retail "robo-advisor" space is undergoing its own evolution 11.

Currently, the vast majority of retail robo-advisors - including industry leaders like Vanguard Digital Advisor, Betterment, Fidelity Go, and Wealthfront - do not utilize reinforcement learning 371112. Instead, they manage hundreds of billions of dollars using automated, static algorithms based on Modern Portfolio Theory 3713. These platforms rely on rule-of-thumb optimization, assessing a user's risk tolerance questionnaire to construct a fixed allocation of low-cost exchange-traded funds (ETFs) and adjusting them along a predetermined glide path as the investor ages 37111415.

However, the boundaries are beginning to blur as artificial intelligence permeates the sector. In mid-2024, the retail trading platform Robinhood acquired Pluto Capital, an AI-powered investment research startup designed to offer highly customized investment strategies using large language models and real-time data analytics 591661. While Robinhood indicated that its initial proprietary robo-advisor rollout would rely on traditional, plain-vanilla allocation mechanics rather than fully autonomous AI management - likely a result of intense regulatory scrutiny regarding the deployment of unexplainable AI models at scale - it has concurrently rolled out AI agents to assist users with research and decision-making 1763.

The academic literature demonstrates that reinforcement learning is highly capable of providing personalized, adaptive, real-time financial advice that significantly outperforms static Modern Portfolio Theory allocations in dynamic markets 3764. As reinforcement learning technology matures, interpretability improves, and regulatory frameworks adapt to ensure consumer safety, the current gap between rigid retail robo-advisors and fully autonomous, institutional AI agents is likely to close.

Bottom line

Reinforcement learning represents a fundamental paradigm shift in algorithmic trading, moving the financial industry beyond static, rules-based predictive models toward dynamic, autonomous decision-making. By continuously interacting with high-fidelity market simulators, these AI agents learn to mathematically balance risk, transaction costs, and optimal capital allocation to formulate robust trading policies. While significant challenges remain - particularly in managing unprecedented Black Swan events and the inherent complexities of live market impact - the ongoing integration of reinforcement learning with large language models indicates that these autonomous systems will become increasingly resilient and prevalent across both institutional and retail finance.