How to Start Investing With Little Money

You can begin investing with as little as a single dollar by opening a zero-commission brokerage account and purchasing fractional shares of broad-market index funds. The most critical steps for beginners with small balances are to automate consistent contributions, avoid platforms that charge flat monthly subscription fees, and embrace a passive, long-term strategy rather than attempting to time the market. This approach shields your growing wealth from the erosive forces of inflation and high management costs.

The Invisible Battle: Compounding Versus Inflation

If you are diligently saving money in a traditional bank account but choosing not to invest it, you are quietly losing wealth every single day. This steady erosion is caused by inflation, an economic headwind that steadily increases the cost of goods and services, thereby reducing the purchasing power of your cash over time 12. Over a period of just a few months, this reduction in purchasing power is barely noticeable. Over several decades, however, inflation acts as a decisive force that can mean the difference between a comfortable retirement and permanent financial insecurity 12.

Historically, keeping cash tucked away at home - or even in a standard checking account earning near-zero interest - virtually guarantees a negative "real return." The real return is the actual mathematical growth of your money after subtracting the prevailing rate of inflation 23. For example, if you place your money in a high-yield savings account that pays an annual interest rate of 5%, but the broader economic inflation averages 3% that year, your real rate of return is only 2% 24. In certain global markets where retail inflation hovers around 5% to 6%, any investment returning below that threshold actually makes you poorer in real terms, despite the nominal number in your bank account slowly climbing 1.

To build sustainable, long-term wealth, your money must be deployed into assets that grow at a rate significantly outpacing inflation 12. The primary engine for this exponential growth is compounding. Compounding occurs when your initial investments generate earnings, and those new earnings are subsequently reinvested to generate their own additional earnings 12. Financial educators often liken compounding to a snowball rolling down a snow-covered hill; it starts small, but it gathers mass and momentum at an accelerating rate the further it travels 2. Over long periods, the mathematical force of compounding physically bends your wealth's growth curve upward. Assuming a theoretical average annual return of 12%, an initial investment can grow exponentially over twenty years, while that same money left idle in an environment with 6% inflation would see its purchasing power shrink to less than a third of its original value 1.

The Democratization of the Stock Market

One of the most pervasive and damaging myths in personal finance is the belief that you must already be wealthy to start investing 567. Decades ago, this assertion carried a degree of truth. Traditional brokerages required hefty minimum deposits to open an account, and they charged substantial commission fees for every single trade 89. Under that old model, it was mathematically impractical to invest $10 or $20 at a time, because a $10 commission fee would instantly consume the entire investment 9.

Today, the global financial industry has undergone a massive structural democratization, integrating individual retail investors into an ecosystem that was once reserved strictly for institutional giants 1011. The rapid proliferation of financial technology has introduced two monumental changes to the retail landscape: the permanent elimination of trading commissions and the invention of fractional shares 81012.

How Fractional Shares Transformed Access

In the past, if a single share of a major technology company or a popular index fund traded at $500, an investor needed exactly $500 to participate. Fractional shares flipped this dynamic entirely by allowing investors to buy a "slice" of a company's stock based on a specific dollar amount, rather than the full share price 1013. If a premium stock costs $1,000 per share, but you only have $10 to invest, modern brokerages allow you to purchase exactly 1% of a share 8.

Major brokerages and financial platforms - including Fidelity, Charles Schwab, and Robinhood - now fully support fractional trading, allowing entry points as incredibly low as $1 to $5 10. Under the hood, this works through internal brokerage ledgers. If multiple users want to buy fractions of a specific stock, the brokerage goes out and buys whole shares, holding those shares in the brokerage's name. The brokerage then internally assigns the corresponding percentage of ownership - and the proportional dividends - to the individual retail investors 15. This technological shift allows beginners to immediately build a widely diversified, blue-chip portfolio without needing tens of thousands of dollars in upfront capital 81016.

The Danger of Flat Fees on Small Balances

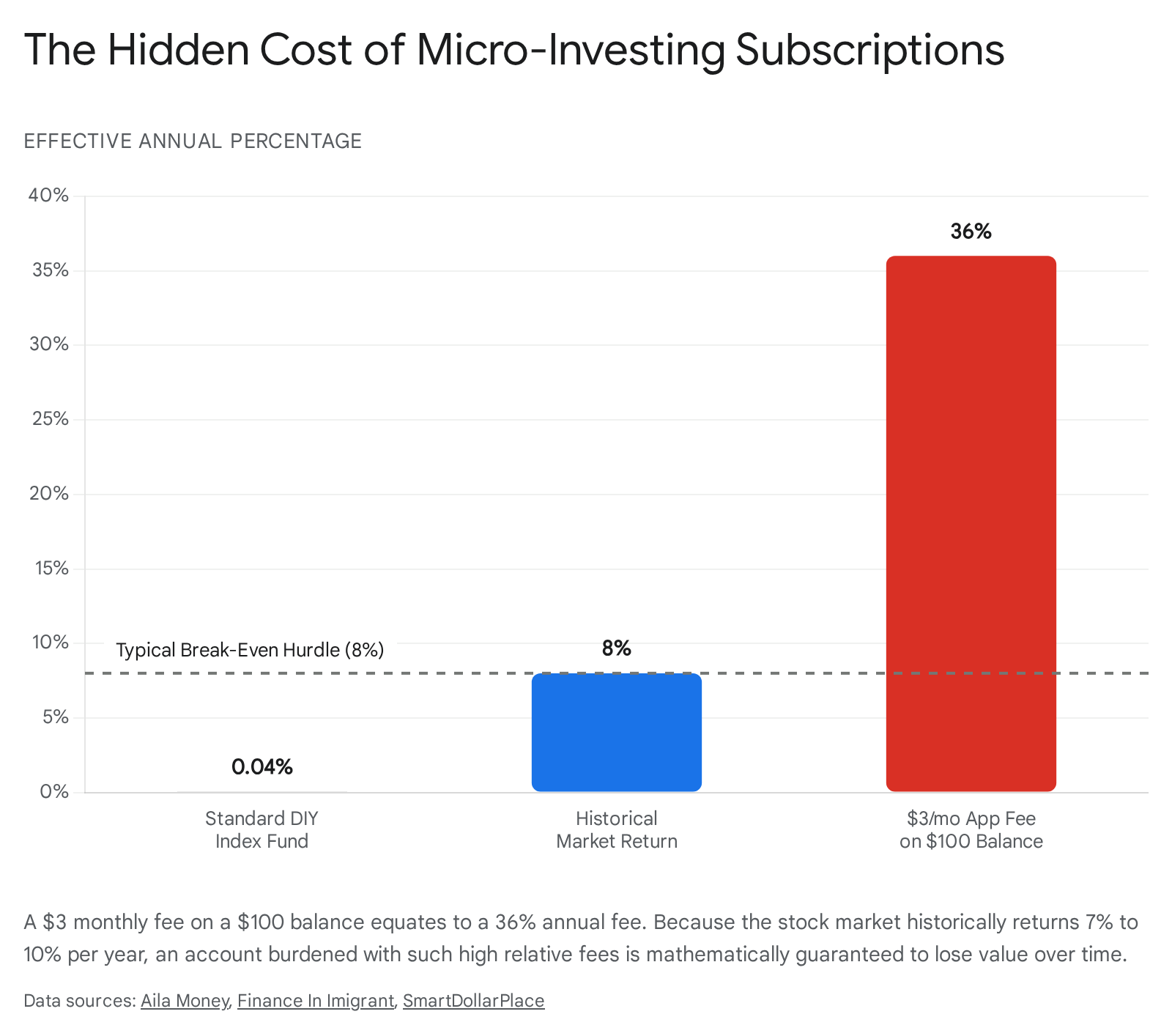

While market accessibility is currently at a historic high, beginner investors starting with very small balances must be highly vigilant regarding fee structures 1718. A new sub-industry of "micro-investing" applications has emerged over the last decade, aggressively marketing themselves to novices. Apps like Acorns and Stash offer highly appealing automated features, such as rounding up your daily debit card purchases to the nearest dollar and automatically investing the spare change into curated portfolios 919.

However, the hidden danger of these platforms lies in their subscription models. Rather than charging a traditional percentage of your assets, these apps charge a flat monthly fee - typically ranging from $3 to $12 per month, depending on the tier of service 202114.

While $3 a month sounds trivial - roughly the cost of a cup of coffee - it represents a mathematically catastrophic percentage drag on a small account balance. If you only have $100 invested, a $3 monthly fee equals $36 a year. That is an astonishing 36% effective annual management fee 919. Given that the broader stock market historically returns an average of 7% to 10% annually before inflation, a 36% fee guarantees that your account is losing value over time 29.

Even if you double your balance to $200, the fee is still 18%, which remains an impossible hurdle to overcome.

For these automated, subscription-based micro-investing apps to make financial sense, an investor generally needs to rapidly build an account balance well over $10,000 to bring the fee percentage down to a competitive industry level (around 0.25% or lower) 19. For individuals who are starting from scratch and can only afford to invest tiny amounts, zero-fee, self-directed brokerages present a far superior mathematical pathway 1920.

Comparison of Beginner-Friendly Micro-Investing Platforms

When choosing an initial platform, beginners should closely evaluate the pricing models relative to the level of guidance they require.

| App / Platform | Monthly Fee Structure | Commission Fees | Investment Approach | Best Suited For |

|---|---|---|---|---|

| Robinhood | $0 ($5 for optional Gold tier) | $0 | Completely self-directed | Self-directed investors wanting zero-cost entry 1920. |

| Acorns | $3 to $12 per month | $0 | Fully automated portfolios | Passive users with larger balances who rely on spare-change automation 1914. |

| Stash | $3 to $9 per month | $0 | Guided ETF & stock picking | Beginners desiring educational guardrails, provided they quickly build larger balances 192021. |

What Are Index Funds and Why Do They Work?

Once an investor has selected a low-cost platform, the next step is determining what exactly to buy. For the vast majority of retail investors, the most effective vehicle for building wealth is the broad-market index fund 1524.

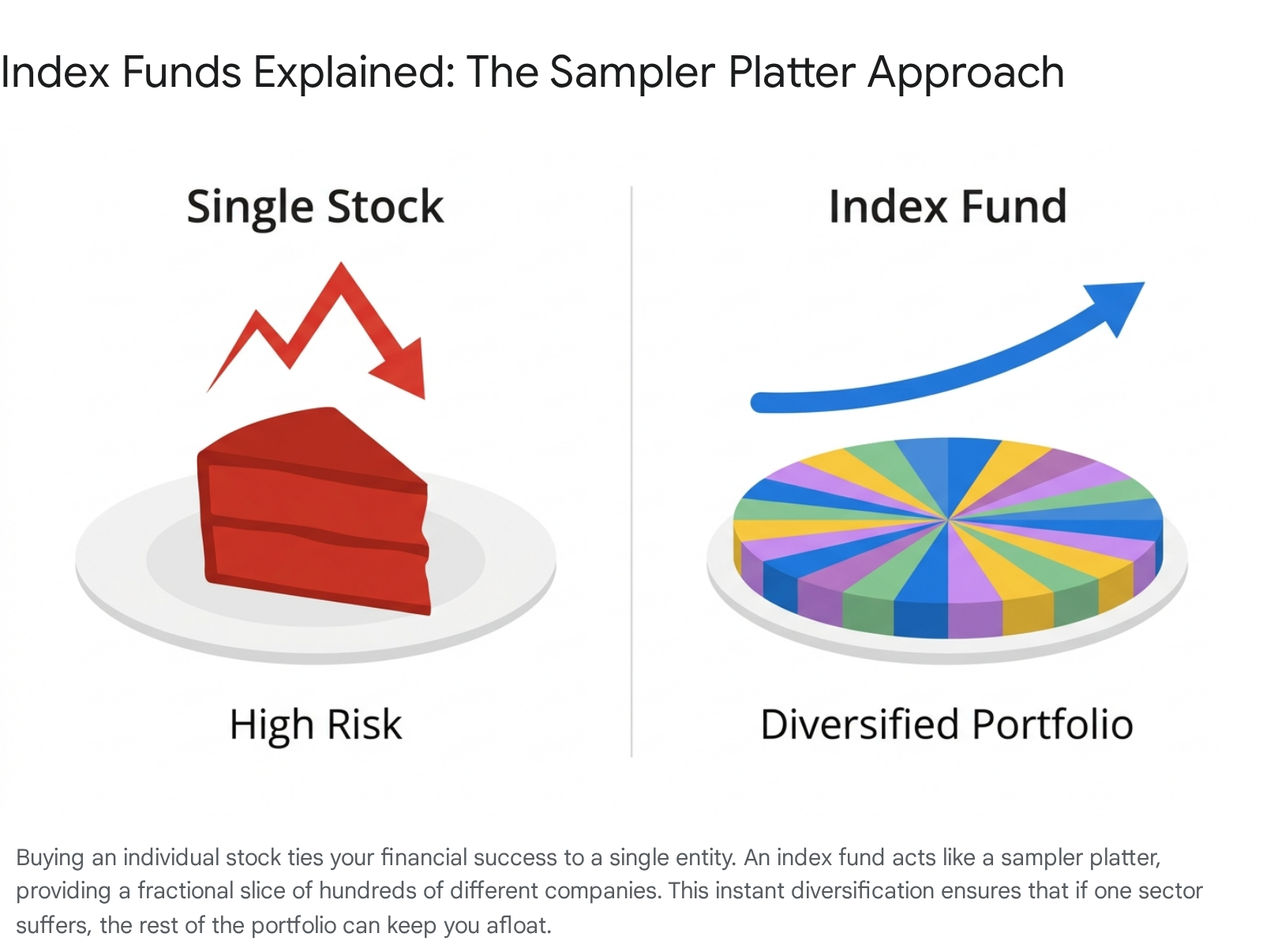

When you purchase an individual stock, you are tying a portion of your financial success directly to the fate of a single corporate entity. If that specific company suffers from poor management decisions, regulatory crackdowns, or technological disruption, you can lose your entire investment 7. This is known as concentrated risk.

An index fund solves this problem through the mechanism of instant, massive diversification. Instead of attempting to research and pick the single "winning" stock out of thousands of options, an index fund buys a tiny, weighted piece of every single stock within a specific market benchmark 1524. The most famous benchmark is the S&P 500, which tracks the performance of the 500 largest publicly traded companies in the United States 1524. When you buy one share of an S&P 500 index fund, you inherently own a microscopic sliver of Apple, Microsoft, Amazon, and 497 other corporate giants simultaneously.

The Sampler Platter Analogy

Financial educators frequently rely on culinary or nautical analogies to explain the mechanics of index funds to absolute beginners. You can think of an index fund as ordering a massive "sampler platter" at a diverse restaurant.

Rather than risking your entire dining budget on one main dish that you might fundamentally dislike, you receive a small taste of everything on the menu 132526. If the fries are cold, it hardly matters because the rest of the meal sustains you.

Another highly effective analogy involves imagining individual stocks as single boats in a massive marina. Each boat makes a profit or loss according to the skill of its captain and the durability of its hull. Buying an individual stock means placing yourself on just one boat; if it encounters a bad storm, it sinks, taking your money with it. Buying a broad-market index fund is the equivalent of buying a tiny piece of every single boat in the marina. You are still fully susceptible to the macroeconomic "tides" that lift or lower the entire harbor, and broad market crashes do happen. However, your individual risk is spread so widely across multiple industries, leadership teams, and business models that a single corporate bankruptcy barely registers in your portfolio 24.

The Bogle Effect and the Critical Role of Expense Ratios

The shift from picking individual stocks to holding broad index funds is largely credited to John Bogle, the founder of Vanguard. This paradigm shift, often referred to as "The Bogle Effect," proved that passively tracking an entire market is mathematically far more effective than paying an expert mutual fund manager to actively attempt to beat the market 2728.

When you evaluate index funds, the single most critical metric to analyze is the expense ratio. The expense ratio represents the percentage of your total investment that the financial institution deducts annually to cover its operational, administrative, and management costs 17. Because pure index funds simply run on passive algorithms designed to mirror an external list of companies, they require very little human intervention 1528. Consequently, their expense ratios are phenomenally low.

Decades of independent research from institutions like Morningstar consistently demonstrate that a mutual fund or ETF's expense ratio is the single most reliable predictor of its future returns. Funds with low expense ratios reliably outperform their highly managed, expensive counterparts because far less capital is siphoned away from the investor's principal balance over time 29. The three largest retail brokerages - Vanguard, Fidelity, and Charles Schwab - have spent the last decade in a fierce price war, driving the expense ratios of their flagship Total Stock Market funds down to near zero 29.

Comparison of Flagship Total Stock Market Funds

Rather than tracking just the top 500 companies, total stock market funds track thousands of large, mid, and small-cap companies, effectively allowing an investor to own a tiny piece of the entire investable U.S. stock market.

| Provider | Fund Name / Ticker Symbol | Expense Ratio | Number of Holdings | 10-Year Avg Annual Return |

|---|---|---|---|---|

| Fidelity | Fidelity Total Market Index (FSKAX) | 0.015% | ~3,860 | 12.52% 29 |

| Charles Schwab | Schwab Total Stock Market (SWTSX) | 0.03% | ~3,310 | 12.50% 29 |

| Vanguard | Vanguard Total Stock Market (VTSAX)* | 0.04% | ~3,670 | 12.50% 29 |

(Note: While Vanguard's traditional mutual fund VTSAX requires a $3,000 initial minimum investment, beginners can easily bypass this by purchasing its Exchange-Traded Fund (ETF) equivalent, VTI, which trades exactly like a stock and can be purchased as a fractional share for as little as $1 on modern brokerage platforms 13293016. All historical return data represents past performance across specific trailing benchmark periods and does not guarantee future results 2916.)

Robo-Advisors Versus Do-It-Yourself (DIY) Investing

Once a beginner understands the power of index funds, they must decide exactly how to acquire and manage them. In the modern retail landscape, there are two dominant paths to building a portfolio: Do-It-Yourself (DIY) investing through a standard discount brokerage, or utilizing an automated algorithmic service known as a "robo-advisor" 3032.

The DIY Index Fund Approach

DIY investing requires opening a standard account with a broker (such as Vanguard, Schwab, Interactive Brokers, or Fidelity), manually selecting your own mix of index ETFs (such as a total US stock market fund combined with an international fund), and physically executing the buy orders on the platform's interface 3033. * The Strategic Advantage: DIY provides absolute control and represents the lowest possible cost ceiling in the industry. By cutting out all middlemen, you pay absolutely nothing except the microscopic expense ratios (typically between 0.03% and 0.10%) of the underlying funds themselves 17. * The Strategic Drawback: DIY investing demands strict emotional discipline and ongoing logistical maintenance. You must remember to log in and make trades when you have extra cash, you must perform your own mathematical rebalancing when your asset allocations drift off target, and crucially, you must rely entirely on your own willpower to avoid panic-selling your portfolio during a terrifying market crash 301718.

The Robo-Advisor Approach

A robo-advisor (such as Betterment, Wealthfront, or Fidelity Go) acts as a highly efficient digital portfolio manager. Upon signing up, the user completes a brief risk-assessment questionnaire regarding their age, financial goals, and comfort with market volatility. Based on these answers, the platform's algorithm automatically constructs and maintains a globally diversified portfolio of index funds 283317. * The Strategic Advantage: Robo-advisors are the ultimate "set it and forget it" solution. Once a recurring bank transfer is established, the robo-advisor invisibly handles everything. It automatically routes your deposits into fractional shares, reinvests your dividends immediately, and continuously rebalances your portfolio to maintain your exact risk profile 3317. For taxable accounts, advanced robo-advisors also execute "tax-loss harvesting" - a complex strategy of selling losing assets to offset capital gains taxes, which is incredibly tedious for a DIY investor to perform manually 1719. * The Strategic Drawback: Convenience comes at a cost. Robo-advisors charge a platform management fee, typically ranging between 0.25% and 0.50% of your total assets annually. This is charged entirely on top of the underlying ETF expense ratios 171819.

The Long-Term Mathematical Impact of Fee Drag

The decision between a robo-advisor and a DIY approach often boils down to your current account balance and your long-term trajectory.

On a small portfolio of $5,000, a standard 0.25% robo-advisor fee equates to roughly $12.50 per year. For a beginner, paying $12.50 annually to have an algorithm perfectly manage, balance, and shield their investments from their own emotional mistakes is a spectacular bargain 321719.

However, because management fees are calculated as a percentage of assets, the dollar cost scales directly alongside your wealth. Fast forward a few decades: on a retirement portfolio that has grown to $500,000, that exact same 0.25% fee now removes $1,250 from your account every single year 1719. Because fees degrade your balance, they also eliminate the future compounding growth that those lost dollars would have otherwise generated 202139.

Many investors adopt a hybrid evolutionary approach: they utilize the safety and automation of a robo-advisor while they are learning the basics and building their first $50,000. Once their portfolio grows large enough that the percentage fee translates into a painful dollar amount, they port their assets over to a DIY brokerage and manage a simplified three-fund portfolio themselves 3317.

| Management Style | Typical Annual Fee | Estimated Cost on $10K Portfolio | Estimated Cost on $250K Portfolio | Core Benefit |

|---|---|---|---|---|

| DIY Indexing | ~0.04% | $4 / year | $100 / year | Absolute lowest cost; maximum control 17. |

| Robo-Advisor | ~0.25% to 0.40% | $25 - $40 / year | $625 - $1,000 / year | Hands-off automation; behavioral guardrails; tax-loss harvesting 17. |

| Human Advisor | ~1.00% | $100 / year | $2,500 / year | Deep, personalized financial and estate planning; emotional coaching 1819. |

Optimizing Growth Through Global Tax-Advantaged Accounts

Before a beginner deposits money into a standard, taxable brokerage account, it is critical that they first utilize government-sponsored, tax-advantaged accounts. While the specific acronyms change depending on your country of residence, the core mechanism remains identical globally: these accounts act as a legal "tax wrapper" around your investments, shielding your compounding growth, dividends, and capital gains from being heavily taxed by the government 4022.

United States: The IRA and 401(k)

In the United States, the primary vehicles for retail investors are the Individual Retirement Account (IRA) and the employer-sponsored 401(k) or 403(b) 2324. * The IRA: A Traditional IRA allows you to contribute pre-tax dollars, providing an immediate tax deduction, while the Roth IRA requires you to invest after-tax dollars. The massive benefit of the Roth IRA is that all future growth and withdrawals in retirement are completely tax-free. The IRS places strict limits on these accounts; for 2024 and 2025, the contribution limit was $7,000, with an additional $1,000 catch-up allowance for individuals aged 50 and older 2425. For the 2026 tax year, the IRS increased the IRA contribution limit to $7,500, with the catch-up increasing the total to $8,600 25. * The 401(k): Workplace plans have significantly higher limits, allowing up to $23,500 in 2025 24. The most critical aspect of a 401(k) for a beginner is the employer match. If a company offers to match your contributions up to 3% or 4% of your salary, it represents a 100% instant, guaranteed return on your investment. Failing to contribute enough to capture the full employer match is universally considered a massive financial mistake 152425.

United Kingdom: The ISA

The UK equivalent of the tax wrapper is the Individual Savings Account (ISA). Unlike the US IRA, which is rigidly structured around retirement age, the British ISA is incredibly flexible; it imposes no age-based restrictions or penalties for withdrawals, making it a true multi-purpose savings vehicle that can be used for mid-term goals or long-term wealth building 402223. The UK government has established a highly generous annual ISA contribution allowance of £20,000, and current policy dictates that this threshold will remain frozen until 2030 2226.

A major shift for beginner investors in the UK occurred recently. Following extensive industry consultation, His Majesty's Revenue and Customs (HMRC) implemented new regulations, effective in late 2024, that officially recognized and permitted fractional shares to be held legally within a Stocks and Shares ISA 222728. This regulatory modernization closed a confusing loophole and ensured that British investors starting with small amounts of money can fully utilize tax-free wrappers while buying slices of expensive global equities.

Canada: The TFSA

The Canadian Tax-Free Savings Account (TFSA) operates in a manner very similar to the US Roth IRA and the UK ISA: contributions are made with money that has already been taxed, and in return, all subsequent capital gains, dividends, and interest compound completely tax-free 29.

However, the TFSA holds a unique mechanical advantage regarding its flexibility. If a Canadian investor faces an emergency and must withdraw funds from their TFSA, they do not permanently lose that contribution space. The exact dollar amount withdrawn is automatically added back to their available contribution limit on January 1st of the following calendar year, a highly forgiving feature that neither the UK ISA nor the US Roth IRA can match 403050.

Behavioral Finance: The Psychology of Losing Money

The actual mechanics of investing are simple mathematics; however, the successful execution of an investing strategy relies entirely on human psychology. The academic field of behavioral finance - popularized by Nobel laureate Richard Thaler - studies how our deep-seated cognitive biases and emotional instincts cause us to make predictably irrational financial decisions, particularly during periods of intense market stress 315253.

The Illusion of Timing the Market

A pervasive and dangerous myth among beginners is the belief that successful investing requires "buying low and selling high" by accurately predicting when the market will crash and when it will recover 632. Attempting to actively time the market is arguably the single most destructive mistake a retail investor can make 6733.

Financial data routinely proves that even seasoned professionals backed by supercomputers cannot reliably or consistently predict short-term market movements 656. The stock market experiences its best-performing days in highly unpredictable bursts, and these massive upward swings often occur immediately following periods of severe market panic. Missing just a handful of the market's best-performing days over a multi-decade period can permanently cripple your overall long-term returns 756.

The primary mathematical antidote to the temptation of market timing is a strategy called dollar-cost averaging 63256. This involves committing to investing a fixed dollar amount at regular intervals (for example, $100 on the 1st of every month), completely ignoring the daily financial news or the current price of the stock 632. When the market is booming and prices are high, your $100 buys fewer fractional shares. When the market is crashing and everyone else is panicking, your $100 automatically buys significantly more shares while they are "on sale" 656. This mechanical consistency removes emotion from the equation entirely.

Common Cognitive Biases to Avoid

To survive decades in the market, an investor must recognize the internal psychological traps that naturally trigger poor decisions:

- Overconfidence Bias: This occurs when an investor vastly overestimates their own financial acumen, often because a few speculative stock picks happened to go up during a broad bull market. Research from the Financial Industry Regulatory Authority (FINRA) notes that 64% of investors believe they possess high investment knowledge, much like how 78% of people believe they are better-than-average drivers 3152. This illusion of control leads beginners to take massive, concentrated risks rather than relying on boring, safe diversification 31525734.

- Loss Aversion (Prospect Theory): Human beings are neurologically hardwired to feel the psychological pain of losing $100 roughly twice as intensely as the joy experienced from gaining $100 5257. This emotional asymmetry is disastrous in finance. It causes terrified investors to panic-sell their assets during temporary market downturns, thereby permanently locking in their paper losses instead of waiting patiently for the market's historical eventual recovery 535734.

- Herd Mentality (FOMO): The overwhelming biological urge to follow the crowd. Herd mentality drives novice investors to abandon their disciplined, low-cost index fund strategies to chase "hot" speculative assets, trendy tech stocks, or volatile cryptocurrencies simply because their peers appear to be getting rich quickly. This bias actively fuels asset bubbles and ensures investors buy at the absolute peak of the market right before a crash 523257.

- Anchoring Bias: The tendency to fixate on irrelevant or obsolete data points. An investor might refuse to sell a failing stock simply because they are "anchored" to the high price they originally paid for it, ignoring the fact that the company's underlying fundamentals have completely deteriorated 525357.

Institutional Risk Versus Investment Risk

When entering the financial markets, beginners frequently confuse two very different types of hazard: investment risk and institutional risk.

Investment risk is the natural, unavoidable volatility of the stock market. Asset prices go up and down daily based on corporate earnings, global geopolitical events, and economic data 6759. If you buy an index fund and the global economy enters a severe recession, the value of your portfolio will drop. It is paramount to understand that no government body, insurance scheme, or regulatory agency will protect you or reimburse you for making a bad investment or losing money due to normal market fluctuations 3536.

Institutional risk, however, relates to the safety of the specific financial platform or brokerage holding your assets. A common fear among beginners is: What happens to my money if the app or brokerage firm I use suddenly goes bankrupt?

State-Backed Protections Against Brokerage Failure

To prevent panic and ensure the integrity of the financial system, governments maintain robust insurance mechanisms designed specifically to step in if a brokerage fails and customer assets go missing due to fraud or insolvency.

In the United States, the Securities Investor Protection Corporation (SIPC) serves as the primary safeguard for investment accounts 353738. The SIPC is a federally mandated, private nonprofit organization that protects investors up to a limit of $500,000 per account capacity, which includes a maximum sub-limit of $250,000 specifically for uninvested cash held within the brokerage 373839.

It is vital to understand exactly how SIPC operates. It only protects the custody function of the broker. If your broker goes under, SIPC's primary goal is not to hand you a check; rather, it works to locate your missing stocks and securely transfer your exact number of shares to a new, healthy brokerage firm, regardless of whether the market value of those specific shares has gone up or down 3540. (It is worth noting that standard cash deposits held at commercial banks are protected by a completely separate entity, the Federal Deposit Insurance Corporation (FDIC), which also covers up to $250,000 363739).

In the United Kingdom, parallel protections are provided by the Financial Services Compensation Scheme (FSCS). In a move to strengthen consumer confidence and keep pace with inflation, the Prudential Regulation Authority (PRA) mandated a significant increase to the FSCS deposit protection limits. As of December 1, 2025, the FSCS limit rose to £120,000 per eligible person, per authorized firm 414243.

The Nuance of Fractional Shares During Liquidation

While standard whole shares of stock are easily transferable between brokerages during an insolvency crisis, a highly specific technical nuance exists regarding fractional shares.

Because fractional shares do not technically exist on public stock exchanges - they are internal accounting mechanisms facilitated entirely by the specific brokerage's ledger - they generally cannot be transferred directly to a different financial institution 15. In the rare event of a severe brokerage collapse where SIPC or the FSCS must step in, the regulatory liquidator will typically be forced to sell the fractional share portions at current market value and return the resulting cash to the investor, rather than transferring the fraction "in kind" 15.

While the underlying economic value of the fraction remains strictly protected against institutional fraud, investors should be aware that their fractional holdings might trigger an involuntary cash liquidation during a severe institutional failure.

Bottom line

Starting to invest with very little money is highly achievable in the modern era thanks to the elimination of trading commissions and the advent of fractional shares. By setting up automated, recurring investments into low-cost, broad-market index funds, beginners can effectively harness the mathematical power of compounding to safely outpace the silent wealth-erosion of inflation. The greatest realistic risks to retail investors are not sudden market crashes, but rather the hidden mathematical drag of high-fee micro-investing platforms on small balances, and the psychological impulses that lead to disastrous market-timing. While robust institutional protections like SIPC and the FSCS secure your assets from outright fraud or platform bankruptcy, the ultimate safety of your wealth relies entirely on boring, highly diversified, long-term discipline.