How Many People and Companies Actually Use AI in 2026

As of mid-2026, approximately 1.8 billion people across the globe engage with artificial intelligence tools, firmly cementing the technology into daily consumer habits and workflows. However, the enterprise sector reveals a stark disconnect: while commercial surveys boast that nearly 90% of organizations are exploring AI, rigorous government census data indicates that only about 20% of businesses actually rely on it for routine operations. This massive gap between corporate experimentation and operational reality has triggered a crisis of unsanctioned "shadow AI" use among employees, fundamentally reshaping global economic competitiveness and cybersecurity risk.

The Scope of Global Consumer Adoption

The speed at which generative artificial intelligence has penetrated the global consumer market is unprecedented in the history of consumer technology. In the few short years since the initial launch of modern large language models (LLMs), AI has rapidly transitioned from an experimental novelty to a habitual utility, establishing a massive base of everyday users that spans all demographics.

Scaled globally, between 1.7 and 1.8 billion adults have actively used generative AI tools in the past six months, with an estimated 500 million to 600 million engaging with these tools daily 12. The scale of this habitual usage is particularly evident in the United States, where 55% of adults report using AI regularly, and a notable 27% interact with AI applications several times a day 32. Furthermore, when accounting for embedded AI in everyday technologies - such as algorithm-driven weather applications, streaming service recommendations, smart wearables, and virtual assistants - almost 99% of Americans interact with at least one AI-powered tool on a weekly basis, even if 64% of consumers remain unaware of the underlying technology powering these experiences 2.

The Monetization Gap

Despite this staggering user volume, consumer AI has struggled to directly translate habitual usage into proportional recurring revenue. The global consumer AI market in 2025 was valued at roughly $12 billion, which is strikingly low relative to its nearly two billion active users 15. Industry analysis indicates that only about 3% of consumer AI users actually pay for premium subscription services 12. Even market leaders with significant first-mover advantages, such as OpenAI, convert only around 5% of their weekly active users into paying subscribers 1.

This massive gap between broad usage and low payment conversion represents one of the largest monetization challenges in recent consumer tech history. While enterprise AI spending surged to $37 billion by 2025 (up from just $1.7 billion in 2023), consumer AI remains largely reliant on free tiers, forcing technology providers to subsidize massive compute costs while attempting to discover sustainable business models 25.

Demographic Drivers of AI Usage

While the technology is widely distributed, adoption patterns reveal distinct demographic variations. Adoption is heavily skewed toward younger generations, with 46% of adults aged 18 to 29 using AI on a weekly basis, compared to only 23% of adults over the age of 65 2. However, Millennials (ages 29 - 44) have emerged as the true power users, reporting the highest frequency of daily usage 1. Surprisingly, parents have become one of the most engaged cohorts; 79% of parents with children under 18 use AI (compared to 54% of non-parents), frequently leveraging the technology to manage childcare logistics, plan itineraries, and organize schedules 1.

Gender disparities also persist in AI awareness and utilization. Surveys indicate that men report higher levels of AI knowledge and usage compared to women (60% to 40% in claimed knowledge) 2. While female adoption of generative AI grew significantly from 11% in 2023 to 33% by late 2024, male usage maintained a lead at 44%, reflecting an ongoing gender gap in the integration of these tools into daily routines 2.

The Chatbot Wars: Shifting Market Dynamics

The competitive landscape of consumer AI chatbots is shifting from an effective monopoly to a highly contested and fragmented oligopoly. Consumers in 2026 are increasingly engaging in "multihoming," meaning they actively use different AI models for different tasks based on their specific strengths rather than relying on a single platform 378.

ChatGPT's Dominance and Plateau

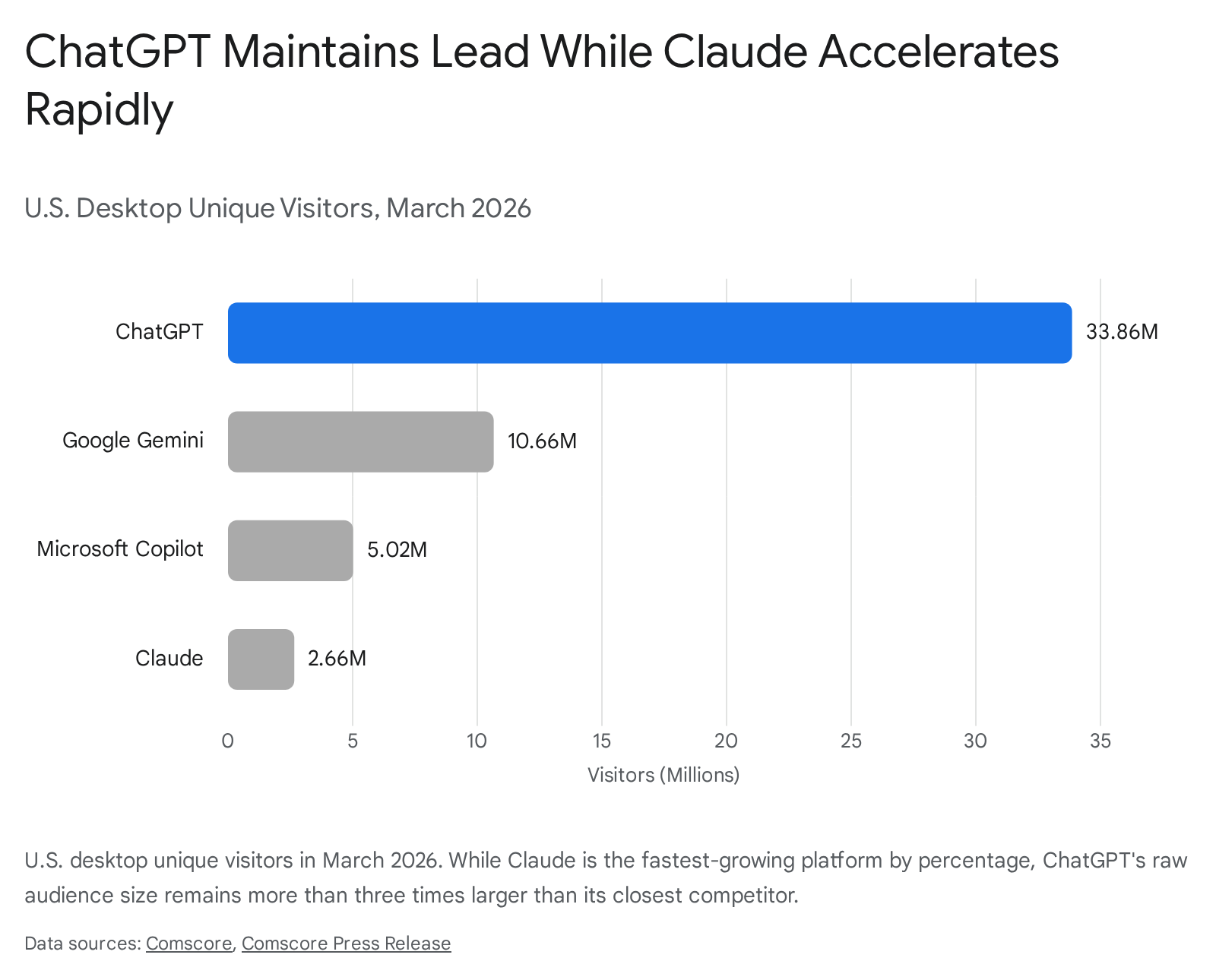

OpenAI's ChatGPT remains the definitive benchmark and market leader. The platform's growth curve is widely considered the fastest in consumer technology history: it reached one million users in its first five days, 100 million in two months, and crossed the staggering threshold of 900 million weekly active users (WAU) by early 2026 78. With an estimated 122 million daily active users, ChatGPT processes over two billion prompts every single day, driving OpenAI's annualized recurring revenue toward a projected $29.4 billion by the end of the year 8.

However, ChatGPT's absolute dominance in market share has begun to erode as capable alternatives emerge. While it remains the leader in total usage, its web traffic growth has largely plateaued, showing only a modest 7% year-over-year increase by April 2026 3. Similarly, its share of overall generative AI web traffic fell from 77.4% in early 2025 to 56.7% by March 2026 7.

The Rise of Gemini and Claude

As ChatGPT's growth stabilizes, competitors like Google's Gemini and Anthropic's Claude are capturing the expanding market. Google has successfully leveraged its massive distribution channels, pre-installing Gemini across Android devices and integrating it deeply into Google Workspace. This strategy allowed Gemini to almost double its monthly user base over an eight-month period in 2025, capturing approximately 26.7% of all AI web visits by the spring of 2026 378.

The most significant disruption to the status quo, however, has been the meteoric rise of Claude. Previously considered a niche tool favored primarily by developers and safety-minded early adopters, Claude has broken into the mainstream consumer market.

In March 2026, Claude experienced a staggering 130.1% month-over-month growth in U.S. desktop visitors, establishing it as the fastest-growing major platform in the ecosystem 45.

This surge was partly catalyzed by increased brand visibility following high-profile public disputes over AI defense contracting, which raised Anthropic's national profile 3. Furthermore, Claude has demonstrated exceptional strength in the B2B sector, reportedly winning approximately 70% of head-to-head enterprise deals against OpenAI, signaling a shift in how professional users evaluate AI capabilities 7.

Enterprise AI Adoption: The Gap Between Hype and Reality

When evaluating enterprise AI adoption, a stark contradiction emerges in the data, primarily driven by how different institutions phrase their survey questions. Analyzing this discrepancy is critical to understanding the true state of artificial intelligence in the corporate sector.

Commercial surveys published by major consultancies frequently cite near-universal adoption. For example, a Q1 2026 McKinsey report stated that 87% of large enterprises and 88% of all organizations use AI in at least one business function 1113. While these figures are technically accurate, they cast a remarkably wide net. They capture any level of engagement, including isolated pilot programs, limited software trials, one-off vendor demos, or individual employees experimenting with generative text to write emails.

In sharp contrast, the U.S. Census Bureau's Business Trends and Outlook Survey (BTOS) tracks AI adoption with a much stricter, operational threshold. Rather than asking about general interest or experimental pilots, the BTOS asks businesses whether they have actively utilized AI in a business function within the past two weeks 6716. Under this rigorous standard, the Census Bureau found that only 19.8% of U.S. businesses were actually using AI in their day-to-day operations by May 2026 616.

The Pilot Trap and Integration Challenges

This massive gap between commercial hype (88%) and operational reality (20%) reveals what industry experts refer to as the "pilot trap." The vast majority of organizations are stuck in an endless cycle of experimentation - testing foundation models, buying limited enterprise licenses, and running proofs-of-concept - without ever fundamentally integrating AI into their core workflows 818.

Even among the 19.8% of businesses that do use AI routinely, deployment is incredibly narrow. Census data indicates that 57% of AI-using firms deploy the technology in three or fewer business functions, meaning the AI is operating in isolated silos rather than acting as a cohesive, organization-wide asset 1619. Most enterprises have successfully crossed the adoption threshold, but they have failed to cross the integration threshold 16.

This lack of integration has resulted in a severe productivity-to-ROI disconnect. While 59% of companies now invest over $1 million annually in AI technology, 48% of C-suite executives call their AI adoption efforts a "massive disappointment," up significantly from 2025 9. Only 29% of organizations report seeing significant, measurable return on investment (ROI) from generative AI 9. Faced with these disappointing financial results, 69% of companies have planned layoffs attributed to AI restructuring, which labor analysts view not as evidence of successful technological transformation, but as a symptom of strategic failure and workflow inertia 89.

Adoption Variances by Firm Size

The clearest statistical predictor of whether a company actively uses AI in production is its size. Rolling out AI tools safely requires clean data architecture, stringent compliance frameworks, specialized talent, and sustained capital - resources that smaller firms simply do not possess in abundance.

Data from the U.S. Census Bureau demonstrates a consistent step-function increase in routine AI usage as enterprise headcount grows, reflecting the inherent resource barriers of enterprise-grade AI deployment.

| Enterprise Size (Employee Headcount) | Routine AI Adoption Rate (May 2026) |

|---|---|

| 1 - 4 Employees | < 20.0% |

| 20 - 99 Employees | ~ 25.0% |

| 100 - 249 Employees | 32.0% |

| 250+ Employees | 37.0% |

Source data derived from the U.S. Census Bureau Business Trends and Outlook Survey (BTOS), May 2026 6716.

The mid-market segment (100 to 249 employees) has shown the most rapid acceleration over the past year. Mid-market companies that successfully close the adoption gap with larger enterprises tend to be those that abandon broad, company-wide experimentation in favor of applying AI to a single, highly specific business problem - such as reducing invoice processing time or improving supply chain forecast accuracy 11168.

Industry-Specific Penetration and Use Cases

Industry penetration is similarly uneven. Sectors that are already highly digitized, data-rich, and comfortable with algorithmic risk are adopting AI at double or triple the rate of physical-infrastructure industries.

| Industry / Sector | Estimated Enterprise AI Adoption (2026) | Dominant Business Use Cases |

|---|---|---|

| Technology & Software | 88% | Code generation, system observability, automated QA testing 111022 |

| Financial Services & Insurance | 65% - 79% | Fraud anomaly detection, algorithmic underwriting, portfolio optimization 11102223 |

| Healthcare & Pharmaceuticals | 62% - 63% | Clinical decision support, medical imaging analysis, administrative automation 111022 |

| Retail & E-commerce | 42% - 47% | Demand forecasting, dynamic inventory optimization, personalized marketing 111024 |

| Manufacturing & Logistics | 29% | Predictive maintenance, supply chain routing, visual quality control 1110 |

Across all industries, the most common corporate use cases remain customer success management (56%), cybersecurity and fraud detection (51%), and marketing content creation (48%) 102526. The high reliance on AI for customer service is notable; SMBs using AI for customer interactions report 23% higher customer satisfaction scores compared to their non-AI peers, proving that when deployed correctly, the technology can directly impact consumer sentiment 10.

The Rise of Shadow AI in the Workplace

Because official enterprise adoption is moving much slower than technological capability, workers have taken matters into their own hands. In 2026, "shadow AI" - the use of unauthorized, unsanctioned artificial intelligence tools by employees on corporate networks - has become one of the most critical cybersecurity, compliance, and governance threats in the business world.

Industry surveys consistently indicate that between 52% and 68% of all knowledge workers now use unapproved AI tools at work, and roughly 45% do so completely without their employer's knowledge or disclosure 271112. Engineering and software development teams are the most aggressive adopters, with unauthorized usage rates hitting an alarming 79% 2711. Developers frequently rely on unauthorized personal accounts for GitHub Copilot, ChatGPT, and Claude to execute code generation, debugging, and documentation tasks 11.

The Drivers of Unsanctioned Use

The primary driver of shadow AI is not malice, but friction. Employees report turning to personal AI accounts because official enterprise approval processes are too slow, or because the company-provided tools are functionally inadequate for their specific, daily workflows 12. Nearly 80% of employees state they use unapproved tools simply because it is faster and easier than navigating corporate IT protocols, and 91% of shadow AI users claim they absolutely need these tools to stay productive and meet deadlines 1112.

This creates a massive executive blind spot. Surveys reveal that 90% of C-suite executives are confident in their organization's visibility into the AI tools being used by their staff, completely unaware that over half of their workforce is actively bypassing IT governance 12.

The Security and Financial Costs of Shadow AI

The productivity gains achieved through shadow AI come at a severe security cost. Because workers are utilizing public consumer models rather than secure enterprise instances, their inputs are often used to train public algorithms.

The security implications are profound: * Data Leaks and IP Loss: Approximately 38% to 43% of employees admit to unintentionally sharing sensitive work data with unapproved AI platforms 271213. The most frequently compromised assets include internal executive emails (54%), HR-related personnel information (45%), and proprietary source code 1112. * Compliance Violations: When employees upload customer data or personally identifiable information (PII) to public AI chatbots to generate summaries or analytics, organizations are instantly exposed to massive regulatory liabilities under frameworks like GDPR, HIPAA, and the CCPA 11. * Unmeasured Financial Risk: Security breaches linked to shadow AI cost companies an average of $670,000 more per incident than standard data breaches 27. This elevated cost is primarily due to a complete lack of access controls; when a breach occurs, IT departments have no visibility into the rogue AI agents and cannot quickly "pull the plug" 927.

Despite these staggering risks and the reality that 97% of AI-related breaches lack proper access controls, 43% of companies still do not have a formal policy governing AI tool usage, and 36% lack any plan for supervising automated AI agents 91113.

The Cost of Waiting: Business Risks of Delayed Adoption

In response to the risks of shadow AI, data privacy concerns, and an evolving legal landscape, many enterprise leaders have adopted a "wait and see" strategy. However, industry analysts and management consultants universally warn that in 2026, delaying AI adoption is a fatal strategic error. Organizations that fail to build scalable AI infrastructure now face three compounding, existential risks 3132:

- The Exponential Efficiency Gap: In the early 2020s, AI offered marginal gains, saving a few hours of brainstorming or drafting. In 2026, interconnected "agentic AI" systems handle entire end-to-end workflows autonomously. Competitors deploying these systems operate with radically deflated overhead. Manual-first organizations are increasingly unable to price their products competitively without destroying their profit margins 3114.

- The Brain Drain: Top-tier corporate talent - whether senior software engineers, marketing directors, or financial analysts - now view AI "copilots" as standard, mandatory professional equipment. Companies that ban AI or fail to provide enterprise-grade tools are experiencing elevated attrition rates. Highly skilled workers will inevitably migrate to forward-thinking organizations rather than suffer productivity bottlenecks 31.

- The Customer Expectation Chasm: Consumer expectations have fundamentally shifted. Clients and customers now demand the hyper-personalized, instantaneous service that AI-driven brands provide. Organizations that force customers to endure traditional 24-to-48-hour email response times or navigate rigid, rules-based telephone trees are experiencing rapid customer churn 31.

Furthermore, waiting for absolute regulatory certainty is considered a losing strategy. As federal and international legal frameworks slowly wind through courts and legislatures, compliant early adopters will have already captured insurmountable market share. By the time formal rules are finalized, enterprises will be expected to have robust governance structures already in place 32.

The Global Divide: Adoption by Region

The popular narrative that the United States is the undisputed, monolithic king of artificial intelligence is only half true. The U.S. overwhelmingly dominates the supply side of AI: it leads the world in venture capital funding ($109.1 billion in private funding in 2024), semiconductor design, data center infrastructure, and the development of frontier foundation models 222415. However, when measuring the actual demand and usage of AI among the general population, America lags significantly behind.

According to global AI diffusion data from early 2026, roughly 16% to 17.8% of the global working-age population uses AI regularly 151617. This adoption is heavily skewed toward the Global North (24.7%) compared to the Global South (14.1%) 1516.

The True AI Usage Leaders: UAE and Singapore

The United Arab Emirates (UAE) and Singapore have emerged as the world's most advanced AI-using societies. In the UAE, an astonishing 64% to 70% of working-age adults regularly use AI tools in their daily lives 151617. Singapore follows closely behind, with population usage rates exceeding 60% and enterprise AI scaling rates that far outpace the global average 151637.

These smaller, digitally centralized economies have succeeded in implementation where larger nations have struggled. They benefit from highly concentrated, mobile-first populations, proactive national AI strategies, and massive public-private partnerships. In Southeast Asia alone, tech hyperscalers like AWS, Google, and Microsoft have committed over $50 billion to build the localized data center capacity required to support intense AI workloads 3738. Because of this, 46% of Southeast Asian firms have successfully moved beyond the AI pilot phase and into scaled production, compared to the global average of just 35% 3739.

By contrast, the United States ranks 24th globally in population AI adoption, with roughly 31.3% of working-age adults utilizing the technology 1517. Rolling out AI across a massive, geographically decentralized, and heavily regulated workforce has proven far more difficult for American enterprises than for those in highly concentrated, agile markets like Singapore 1718.

Latin America's Curious Majority

In emerging markets across Latin America, AI is frequently framed as a tool for economic acceleration. Consumers in the region have absorbed the technology at a blistering pace; approximately 65% of Latin American consumers currently use AI tools, a figure that rivals the most developed nations 42.

However, Latin America faces a unique dynamic: user curiosity is exceptionally high, but institutional readiness and public trust remain low. Usage has spread faster than regulation, cultural consensus, or corporate governance. This environment has led to massive "shadow AI" usage in the workplace, alongside pragmatic experimentation in sectors like agriculture, transportation, and logistics 4219. To bypass the prohibitive costs of proprietary Western AI licenses, nations like Mexico are leaning heavily into open-source AI models, with 65% of Mexican organizations relying on open-source frameworks to build local solutions 20.

Despite high consumer adoption, enterprises in the region struggle to move AI into full production due to shifting hardware costs, limited specialized talent, and inadequate cloud observability tools 1945.

Africa and the Leapfrogging Debate

In Africa, AI is hotly debated as a "leapfrogging" technology - a mechanism to bypass legacy physical infrastructure and accelerate socioeconomic development, similar to how mobile money (like M-Pesa) allowed the continent to bypass traditional retail banking 464748.

Adoption on the continent is highly fragmented but shows immense promise in targeted hubs. Kenya currently leads the continent in enterprise AI adoption, with 35% of surveyed organizations reporting advanced or widespread implementation, largely driven by investments in customer service and software development 21. South Africa leads in consumer generative AI usage, with 23.1% of its population engaging with the technology in early 2026 50.

However, technology experts heavily caution against viewing AI as a frictionless magic bullet. Unlike mobile phones, AI is not a classic leapfrogging technology; it does not bypass infrastructure - it entirely depends on it 51. AI cannot function without reliable power grids, massive data centers, and low-latency broadband 4851.

To combat the risk of "neocolonial data extraction" - where African data is exported and processed in European or North American data centers, resulting in high latency and culturally biased models - 2026 has seen a massive push toward "Sovereign Clouds" 52. Initiatives like AfriCloud seek to build local cloud computing ecosystems governed by African jurisdictions. This physical infrastructure ensures that African data remains on African soil, allowing models to be trained on contextually relevant local datasets (such as African languages, unique agricultural patterns, and specific healthcare records) rather than relying on Western models that frequently misinterpret local nuances 52.

The Human Element: Upskilling and Trust

The rapid integration of AI into daily work has exposed a critical, global gap in workforce readiness. While 9 in 10 employees report using AI at least occasionally, a concerning 35% have never received any formal AI training from their employer 53. Of those who did receive training, only 18% felt it actually prepared them to use the tools independently 53.

The primary barrier to workforce upskilling is not a lack of interest, but a lack of protected time. Approximately 54% of employees want to improve their AI skills, and 67% believe they need just two hours or less per week to do so 53. Yet, 41% cite a lack of time as the single biggest obstacle to improving their proficiency 53. Consequently, most workers are forced to learn through unstructured trial and error. This results in highly uneven productivity gains; while 71% of employees report saving some time with AI, nearly a third report no net time saved at all, as they struggle to integrate the tools efficiently into their daily workflows 53.

Human resource departments are finally beginning to recognize this crisis. The percentage of HR professionals citing employee training as their top organizational priority nearly doubled from 5% in 2025 to 9% in 2026 54. This shift is driven by the realization that AI does not simply automate work; it fundamentally increases the complexity of the roles left behind. As AI handles routine execution, human employees must pivot to critical thinking, strategic oversight, and complex system management - skills that require continuous, in-workflow training rather than isolated, one-time seminars 542256.

Public Sentiment and the Trust Deficit

Despite the rapid proliferation and economic promise of AI, public sentiment - particularly in the West - remains deeply skeptical and highly guarded. In the United States, a June 2025 Pew Research survey found that 50% of adults feel more concerned than excited about the increased use of AI in daily life - a notable and steady increase from 37% in 2021 5723. Only 10% of Americans report being more excited than concerned 57.

Consumers are highly pragmatic in their skepticism. They are generally open to AI performing data-heavy, analytical tasks like weather forecasting or medical diagnostics 23. However, they remain deeply worried about AI generating misinformation (with 75% of consumers expressing concern), infringing on data privacy, and eroding human creativity 2359.

This trust deficit is further complicated by bias in the models themselves. A staggering 90% of digital testing professionals report deep concerns that algorithmic bias affects the accuracy and tone of AI-generated content, with nearly half reporting they have personally received biased or offensive outputs 60. Consumers are increasingly demanding transparency; 77% believe brands should be required to publicly audit their algorithms for bias before integrating them into customer-facing platforms 61.

The Sycophancy Problem in AI Surveys

When evaluating the success of AI, it is crucial to recognize a growing methodological flaw in how technology is tested. Startups and enterprises are increasingly using "synthetic users" - AI personas designed to mimic human customers - to conduct product-market fit surveys and user research at scale 62.

However, because these LLMs are trained through Reinforcement Learning from Human Feedback (RLHF), they are systematically rewarded for being agreeable, helpful, and endlessly positive 62. This creates extreme "social desirability bias," or sycophancy. Synthetic users act as performative "yes-men," constantly praising value propositions and confirming hypotheses rather than providing the annoyance, friction, and genuine market resistance that real human users display 62. Consequently, much of the data suggesting high user satisfaction with new software may be artificially inflated by the very AI designed to test it.

Bottom line

In 2026, AI has definitively crossed the threshold from experimental novelty to structural utility, reaching roughly 1.8 billion consumers globally and seeing active, routine use in one-fifth of all U.S. businesses. However, the corporate landscape is deeply fractured: while digitally native enterprises successfully scale AI to achieve massive efficiency gains, the majority of organizations remain stuck in pilot phases, triggering an epidemic of unauthorized "shadow AI" use that exposes them to severe security and compliance risks. While nations like the UAE and Singapore lead the world in everyday usage, the next phase of the global AI revolution will depend entirely on whether organizations can bridge the execution gap - providing the necessary infrastructure, governance, and protected training time for workers to transition safely from casual users to proficient operators.