How Is Grid Battery Storage Changing in 2024

Grid batteries are utility-scale energy storage systems that capture surplus electricity - primarily from intermittent renewable sources like solar and wind - and discharge it during periods of peak demand or grid instability. By utilizing advanced lithium-ion technology to instantly inject power into the electrical grid, these systems fundamentally shift energy from times of abundance to times of scarcity, displacing the need for costly fossil-fuel peaker plants. Ultimately, this technological intervention reduces carbon emissions while simultaneously bolstering grid resilience against extreme demand spikes.

For the everyday consumer, the vast intricacies of wholesale power markets are largely invisible; the electrical grid only demands attention when the lights go out or when monthly utility bills skyrocket. However, battery storage has quietly become the ultimate insurance policy against both of these pain points. During extreme heat waves or deep winter freezes, when millions of air conditioners or space heaters threaten to overwhelm transmission capacity, batteries prevent blackouts by instantly discharging massive amounts of stored, inexpensive power. By absorbing cheap renewable energy when it is abundant and deploying it when wholesale electricity is most scarce and expensive, these systems structurally stabilize power rates and protect consumers from the volatile price spikes traditionally associated with fossil fuels.

To understand the scale and function of this technological shift, it is highly instructive to utilize a water pipe and tank analogy. In grid metrics, Gigawatts (GW) measure capacity, which is analogous to the diameter of a water pipe - it dictates exactly how much power can flow into or out of the grid at any single instant. Gigawatt-hours (GWh) measure stored energy, representing the total volume of the water tank. Therefore, a battery with a 1 GW capacity and a 4 GWh duration is analogous to a pipe that can discharge 1 GW of power continuously for four hours before the tank is completely empty.

This functional distinction is crucial for dispelling a persistent industry and public misconception: the belief that a 100% renewable grid requires batteries capable of discharging energy continuously for weeks at a time to cover seasonal lulls in generation. While ultra-long-duration seasonal storage will eventually play a role in deep, end-stage decarbonization, the most lucrative, urgent, and impactful market today is the two- to four-hour peaking market 122. Grid batteries do not currently need to power a state for a month; they only need to bridge the critical daily transition period - such as the late afternoon hours when solar production drops to zero, but evening household energy demand peaks. By simply shifting midday solar to the evening peak, two- to four-hour batteries effectively neutralize the grid's most precarious hours.

FAQ 1: How Fast is Utility-Scale Battery Storage Growing Globally?

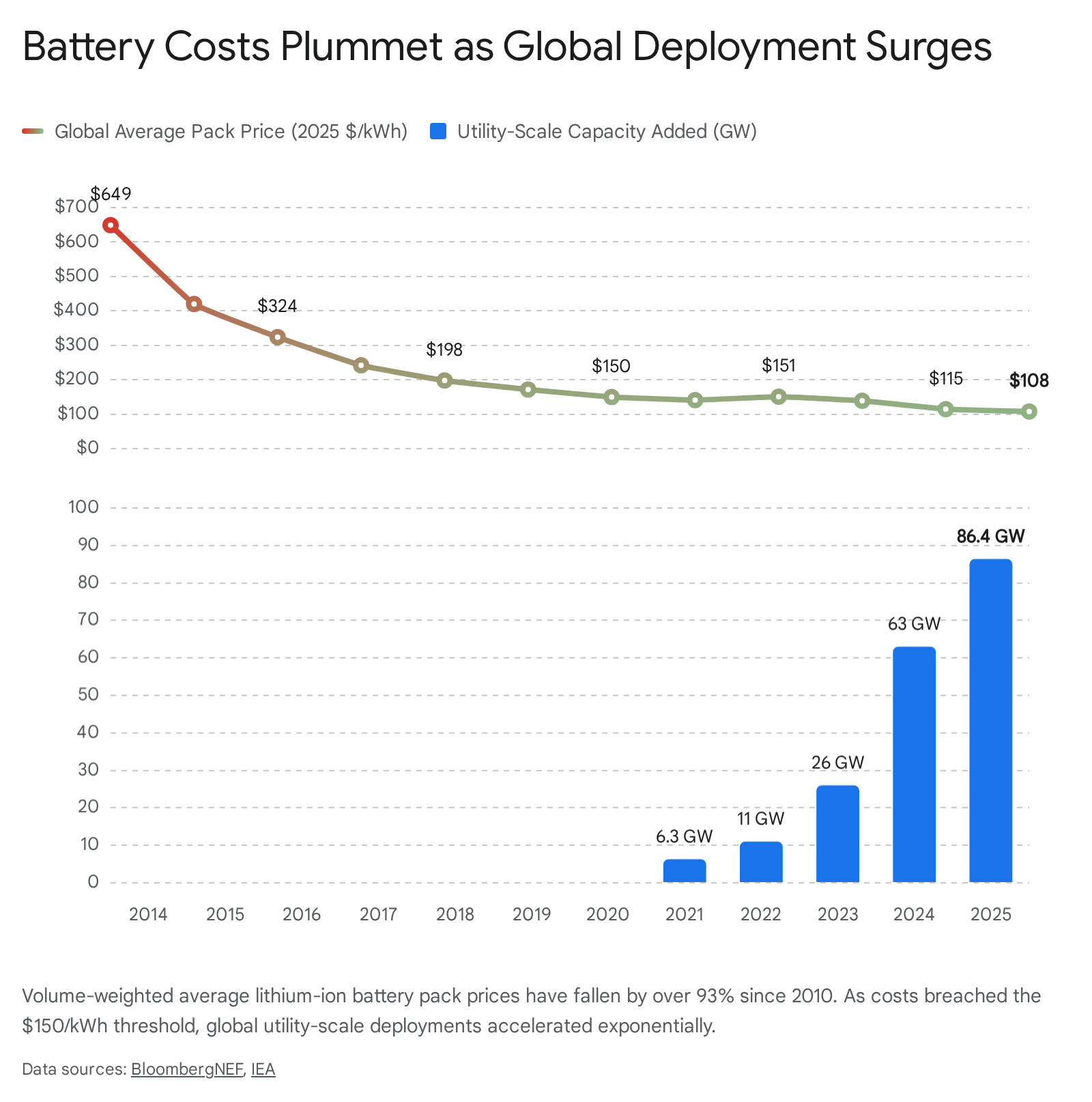

The years 2023 and 2024 marked a decisive inflection point for the global energy storage sector, officially transitioning the technology from a niche, experimental grid-balancing tool to a foundational pillar of global energy infrastructure. The total operational battery storage capacity globally reached an estimated 375 GWh by the end of 2024, following a record 200 GWh of new battery energy storage systems (BESS) coming online in a single year 4. According to the International Energy Agency (IEA), the global power capacity of utility-scale batteries expanded more than twelvefold between 2020 and 2024, surging past 124 GW of total installed capacity 5. In 2025, this momentum accelerated further, with 108 GW of new capacity deployed worldwide, representing a 40% year-over-year growth that exceeded historical peaks for even gas-fired power additions 23.

This explosive, non-linear growth is fundamentally driven by the intersecting macroeconomic forces of plummeting component costs, aggressive state-sponsored decarbonization policies, and the urgent physical necessity to manage grid intermittency as solar and wind penetration increases. Current projections suggest this trajectory will only steepen, with global installed energy storage expected to increase ninefold by 2040 to over 4 Terawatts (TW) 4. However, the deployment of this critical infrastructure is not uniform; it is heavily concentrated among a few global frontrunners that dictate international supply chains.

China's Unprecedented Market Dominance

China has cemented its position as the undisputed global leader in battery storage deployment, driven by strict state mandates and highly centralized infrastructure planning. By the end of 2024, China's cumulative "new energy storage" capacity - a classification that encompasses electrochemical batteries and excludes traditional pumped hydro - reached a staggering 73.76 GW and 168 GWh 78. In 2024 alone, the country added 42.37 GW and 101.13 GWh of new capacity, achieving a year-over-year growth rate exceeding 130% and accounting for roughly 40% of the global total 78.

This expansion is characterized by a distinct and aggressive shift toward massive, centralized projects. In 2024, systems exceeding 100 MW accounted for 74% of the newly added capacity across the nation 910. The geographic distribution is also highly concentrated in the north and northwest, with Inner Mongolia leading at 10.23 GW, followed closely by Xinjiang with 8.57 GW, and Shandong with 7.17 GW 8. Furthermore, the average storage duration in China steadily increased from 2.1 hours in 2023 to 2.3 hours in 2024, reflecting a deliberate effort to optimize peak-shaving capabilities and improve overall grid integration 78.

The primary driver behind this hyper-scaled deployment is a series of strict provincial-level mandates that require renewable energy developers to co-locate a specific ratio of energy storage with any new wind and solar projects 4. This aligns with the broader national target of ensuring a renewable energy utilization rate of no less than 90%, thereby mitigating the curtailment of clean energy 8. Notably, while co-located storage saw significant utilization improvements - averaging 177 full cycles per year - standalone energy storage emerged as the primary growth engine, representing 63% of total new capacity additions and seeing daily charge-discharge cycles rise to 1.5 910. While lithium-ion technology maintains an iron grip on 96.4% of the market, China is also actively diversifying its technological base, having commissioned the world's largest pneumatic energy storage system (300 MW) and a massive 100 MWh sodium-ion facility 712.

The United States and the Impact of the Inflation Reduction Act

The United States represents the second-largest battery storage market, maintaining a rapid momentum fueled by highly favorable free-market economics and aggressive federal policy intervention. The U.S. added approximately 35 GWh of new capacity in 2024 4. A critical, transformative catalyst for this growth was the passage of the Inflation Reduction Act (IRA), which introduced a vital investment tax credit (ITC) specifically for standalone energy storage systems 45. Prior to the IRA, batteries generally only qualified for federal tax credits if they were physically co-located and charged by a solar facility. Decoupling this requirement unleashed a wave of purely grid-optimizing standalone projects 5.

The U.S. grid storage market is overwhelmingly driven by utility-scale projects, which account for roughly 90% of new capacity additions 4. As individual states push forward with aggressive renewable portfolio standards, regional transmission organizations face an accelerating need for flexible capacity, sparking billions in capital investment across the American Sunbelt and the West. This battery boom is intrinsically linked to solar expansion; across the U.S., 1 MW of storage was added for every 3 MW of solar added in 2024 6. The symbiosis is profound: states like California and Nevada became the first to surpass a 30% annual solar generation share in 2024, a feat strictly enabled by the presence of massive battery fleets capable of absorbing midday surpluses and averting disastrous curtailment 6.

Europe's Shift from Residential to Grid-Scale

Europe experienced another record year of battery deployment, though the fundamental pace of expansion showed signs of moderation and structural reorganization. The European market - broadly tracking the European Union, the United Kingdom, and Switzerland - added 21.9 GWh of new battery capacity in 2024, expanding the continent's total fleet to 61.1 GWh 1516. However, the year-over-year growth rate slowed significantly to 15%, a marked deceleration following three consecutive years of near 100% capacity doubling 1617.

This deceleration masks a vital and highly consequential structural shift within the European energy market. Residential behind-the-meter battery deployment - historically the bedrock of European storage growth - declined by 11% in 2024 1516. This contraction was largely due to the stabilization of retail electricity prices following the subsidence of the 2022 geopolitical energy crisis, combined with the reduction or removal of generous state subsidies in key markets 15.

Conversely, the utility-scale segment surged dramatically by 79%, marking a definitive turning point for European grid architecture 1516. Italy serves as the prime example of this pivot; the nation surged ahead with 6 GWh of total additions, driving a 58% year-over-year increase in its domestic market strictly due to the massive expansion of utility-scale projects, even as its residential segment contracted by 19% as the "Superbonus" policy phased out 1718. Germany maintained its overall volume lead with 6.2 GWh installed, while Spain experienced a 41% decline, though it is projected to rebound sharply into the top five by 2025 as large-scale projects revive 1516. Despite this progress, industry advocates warn that Europe's trajectory falls well short of the estimated 780 GWh needed by 2030 to fully support the renewable transition, urging the European Commission to implement a comprehensive, EU-wide flexibility action plan to harmonize fragmented member-state policies 1617. The economic imperative is clear: independent analysis suggests that if Germany had possessed just 2 GW more of battery capacity in June 2024, it could have displaced 36 GWh of expensive fossil fuel power during evening peaks, saving millions in fuel costs 7.

Australia's Breakneck Renewable Transition

Australia has rocketed up the global ranks to become the third-largest utility-scale battery market in the world by capacity added, an urgent necessity given the country's aging and increasingly unreliable coal generation infrastructure 2021. Over the course of 2025, Australia added a record 2 GW (5.1 GWh) of new large-scale battery capacity, representing a staggering 233% increase over the previous year 2022. This momentum is heavily backed by capital, with another 4.3 GW financially committed over the year, worth nearly $4.8 billion in investment 20.

Australia's National Electricity Market (NEM) faces a unique operational paradox: it deals with some of the highest per-capita rooftop solar penetration rates in the world. By the end of 2024, there were over 4 million rooftop solar systems installed across the country, accounting for a massive 12.4% generation share nationally 23. This distributed generation aggressively hollows out midday utility electricity demand, creating extreme "duck curve" conditions. To manage the subsequent steep, volatile evening ramps when solar fades, developers have rushed to deploy major assets like the 500 MW/1,000 MWh Liddell Battery and the 600 MW/1,600 MWh Melbourne Renewable Energy Hub 20.

Furthermore, a growing share of Australia's new utility-scale battery fleet is being equipped with highly advanced grid-forming inverters. This technology allows solid-state batteries to provide synthetic inertia and system strength - essential physical grid services that maintain frequency stability, which were historically provided solely by the heavy, spinning kinetic mass of synchronous coal and gas turbines 22. With coal-fired power failing at alarming rates - evidenced by 90 unscheduled outages in the 2025/26 summer alone - batteries are stepping in not just as energy reservoirs, but as the fundamental electromechanical stabilizers of the Australian grid 21. Meanwhile, on the residential side, close to 75,000 home battery units were sold in 2024, pushing the national total to over 185,000 units, as consumers increasingly seek energy independence and relief from elevated evening tariffs 23.

FAQ 2: How Do CAISO and ERCOT Compare in Battery Deployment and Market Drivers?

Within the United States, the deployment of battery storage is heavily bifurcated and dominated almost entirely by two massive, independent grid operators: the California Independent System Operator (CAISO) and the Electric Reliability Council of Texas (ERCOT). By the end of 2024, these two regions combined accounted for the vast majority of all U.S. additions. While both grids are aggressively scaling storage to record levels, they operate under vastly different regulatory frameworks, fundamental market designs, and operational philosophies.

Deployment Metrics and Duration Trends

As of December 2024, the CAISO balancing area possessed approximately 13 GW of active battery capacity, with an aggregate maximum energy storage capacity of 47.3 GWh 1. The vast majority of this fleet is uniformly designed, consisting of four-hour duration lithium-ion systems 15.

Conversely, ERCOT has experienced a massive surge in standalone storage investment, driven purely by market forces rather than state climate mandates. ERCOT ended 2024 with approximately 10.5 GW of deployed battery capacity 8. Because ERCOT relies heavily on ancillary services and brief, intense periods of extreme scarcity pricing, shorter-duration batteries have historically been favored. However, as market conditions mature, average durations in Texas are rising, moving from roughly 1 hour in previous years to 1.62 hours by late 2024 225.

| Metric / Characteristic | CAISO (California) | ERCOT (Texas) |

|---|---|---|

| Deployed Capacity (GW) | ~13.0 GW (Dec 2024) 1 | ~10.5 GW (Dec 2024) 8 |

| Aggregate Stored Energy | ~47.3 GWh (Dec 2024) 1 | Variable based on mixed duration fleet |

| Average Fleet Duration | 4 hours 15 | 1.6 hours (trending upward) 225 |

| Primary Revenue Streams | Energy arbitrage (Net peak load serving) & Resource Adequacy contracts 1 | Ancillary services (Regulation, ECRS) & high-volatility Real-Time Energy arbitrage 826 |

| Policy/Regulatory Drivers | State decarbonization targets (100% clean by 2045), mandatory CPUC Resource Adequacy 1 | Free-market nodal pricing, strict market design revisions (NPRRs), lack of a capacity market 89 |

| Typical Asset Model | Paired with solar/wind or standalone, highly contracted via long-term tolling agreements 1 | Mostly standalone, pure merchant risk (uncontracted), reliant on real-time price spreads 99 |

The CAISO Model: Orchestrated Adequacy and the Duck Curve

The expansion of battery storage in California is a highly orchestrated, centralized effort driven by ambitious legislative mandates, most notably the target of achieving 100% zero-carbon retail electricity sales by 2045 1. The physical and operational reality of the CAISO grid is universally defined by the "duck curve" - a massive oversupply of extremely cheap solar power during the midday hours, followed by a precipitous, multi-gigawatt drop in supply just as evening residential consumer demand peaks.

CAISO's battery fleet primarily executes intra-day arbitrage to solve this structural mismatch. Batteries charge heavily from 10:00 AM to 1:00 PM, soaking up excess solar that would otherwise be curtailed or exported at negative prices, and then discharge their massive reservoirs between 5:00 PM and 9:00 PM 1. Crucially, the California Public Utilities Commission (CPUC) enforces strict Resource Adequacy (RA) requirements, mandating that Load Serving Entities (utilities) secure sufficient capacity to ensure reliability during these peak net-load hours. Because RA rules heavily value sustained, reliable output, developers are economically incentivized to build four-hour systems 528. Under these RA contracts, developers often receive fixed monthly capacity payments (tolling agreements), which provide stable, predictable returns that heavily de-risk massive capital investments for financiers.

The ERCOT Model: The Merchant Wild West

The ERCOT market is structurally and philosophically unique; it is an "energy-only" market that explicitly lacks a centralized capacity market or state-level decarbonization mandates 9. Generators in Texas are paid only for the actual electrons they inject or the specific ancillary services they provide. When supply becomes precariously tight relative to demand, wholesale prices can spike from double digits to thousands of dollars per megawatt-hour in a matter of minutes.

This extreme price volatility is the lifeblood of Texas battery developers. Historically, the bulk of ERCOT battery revenue was derived from ancillary services - specifically fast frequency response, regulation, and the Contingency Reserve Service (ECRS) - where batteries excel due to their millisecond reaction times 826. Because ancillary service markets are relatively shallow and only require short-duration bursts of power to stabilize grid frequency, this economic structure led to a fleet heavily dominated by one-hour batteries.

However, market dynamics in ERCOT are currently undergoing a violent shift. As gigawatts of new battery capacity come online, the highly lucrative ancillary service markets are becoming saturated, compressing profit margins 526. Consequently, battery operators are increasingly forced to transition into the broader, deeper energy arbitrage market, structurally shifting power from cheap midday solar hours to expensive sunset hours 2526. Furthermore, aggressive new ERCOT market rules are forcing a shift in physical hardware. Programs like the Dispatchable Reliability Reserve Service (DRRS) require resources to sustain maximum output for at least four hours to qualify for compensation 2. These evolving market designs, coupled with immense, unprecedented load growth from the proliferation of data centers, are steadily and inevitably pulling ERCOT developers toward longer-duration, two-hour and four-hour assets 225.

FAQ 3: Can Battery Storage Prevent Blackouts During Extreme Weather?

The true value of grid batteries - and the justification for their massive capital cost - becomes starkly evident during periods of acute meteorological stress. Historically, extreme weather events forced grid operators to rely entirely on aging thermal power plants - coal and natural gas - that are highly susceptible to mechanical failure, frozen instrumentation, and supply-chain fuel disruptions in extreme temperatures. Recent high-stakes case studies in both California and Texas demonstrate that utility-scale batteries are fundamentally superior crisis-management tools.

California's Heatwave Success (Summer 2024)

California's electrical grid has a long and troubled history with late-summer heatwaves. In August 2020, extreme, prolonged heat forced the state into executing rolling power outages as demand outstripped available generation 10. In September 2022, a severe heatwave brought the grid to the absolute brink of failure, triggering desperate text-message appeals for widespread consumer conservation (Flex Alerts) to shave peak demand 1112.

By the summer of 2024, the CAISO grid architecture looked profoundly different. The battery fleet had expanded aggressively to over 10 GW of operational capacity 32. When consecutive days of triple-digit temperatures struck the state in July and August, driving both gross and net demand to near-record levels, the grid held steady without operators needing to issue a single Flex Alert 1232. During the most critical net-load evening hours, battery discharge routinely topped 7 to 8 GW, seamlessly and instantly replacing the solar generation that faded at sunset 1233.

The scale and efficiency of this intervention is staggering: on peak days in 2024, CAISO's battery fleet met approximately 16% of the state's total peak demand 33. This was particularly crucial during a period when the Line Fire in San Bernardino County severely limited the 500kV Morgan to Dugas transmission line, crippling California's ability to import emergency power from neighboring states 33. By holding back their state of charge until the exact moments of highest local stress, internal batteries not only avoided rolling blackouts but successfully mitigated the need for emergency, high-polluting gas plant dispatches, proving that a high-renewable grid can be remarkably resilient in the face of climate-driven heat 3234.

Texas and the Winter Storm Crucible

The trauma of Winter Storm Uri in February 2021 - which caused catastrophic, statewide grid failure, billions of dollars in economic damage, and tragic loss of life - permanently altered the ERCOT landscape 35. In the immediate aftermath, critics questioned whether a grid increasingly reliant on renewables could survive the winter. However, since Uri, Texas has added immense amounts of solar (roughly 31 GW) and battery storage (17 GW) 3513.

When Winter Storm Heather struck Texas in January 2024, driving unprecedented winter heating demand to a record 78,349 MW, the expanded battery fleet proved its existential worth 13. Across the two coldest days of the storm, battery energy storage systems supplied critical, localized flexibility, discharging rapidly into the grid when thermal plants faltered 37. Analytics firm Aurora Energy Research concluded that during the January freeze, battery units fulfilled essential ancillary services, freeing up roughly 3 GW of natural gas generation that was desperately needed to meet base energy needs 38.

The intervention of batteries during Winter Storm Heather successfully prevented localized grid failures, supplied electricity to roughly 434,000 homes, and saved the Texas market an estimated $750 million in day-ahead market costs by forcefully crushing scarcity pricing spikes 3538. This was not an isolated success. During subsequent winter events like Winter Storm Kingston in 2025 and Winter Storm Fern, the grid held flawlessly, with batteries making up nearly 10% of ERCOT's fuel mix during peak demand periods 3513. Throughout the subsequent summer of 2024, despite near-record load demand from prolonged heatwaves, ERCOT issued zero conservation calls - a stark contrast to 2023, when operators were forced to issue 11 emergency appeals under similar demand conditions but with a smaller storage fleet 939.

FAQ 4: How Are Falling Battery Costs Accelerating the Renewable Transition?

The staggering deployment figures of 2023 and 2024 are not a political anomaly; they are the direct, inevitable consequence of a relentless, decade-long collapse in lithium-ion manufacturing costs. According to BloombergNEF's extensive market analysis, the volume-weighted average price for lithium-ion battery packs across all sectors fell to a record low of $139/kWh in 2023 (a 14% year-over-year drop), and plunged further to a historic $108/kWh in 2025 4014. Overall, battery pack prices have fallen by an astonishing 93% since 2010, effectively rewriting the macroeconomic rules of energy infrastructure and making stationary storage competitive with fossil-fuel peakers without subsidies 40.

This cost reduction is occurring despite periods of extreme volatility in underlying raw metal prices. The resilience of the downward cost curve is largely attributed to massive overcapacity in global cell manufacturing - particularly driven by aggressive industrial policy in China - and intense, margin-crushing industry competition across the supply chain 4014. Furthermore, the technological synergy between the electric vehicle (EV) market and the stationary storage market is driving profound economies of scale. While stationary storage accounts for a smaller total volume than EV batteries, the shared manufacturing infrastructure ensures that grid storage directly benefits from automotive scale 15.

The Triumph of Lithium Iron Phosphate (LFP)

A secondary, critical driver of falling costs and rapid deployment is the global pivot in underlying battery chemistry. Historically, the electric vehicle and early stationary storage markets relied on Nickel Manganese Cobalt (NMC) chemistries due to their superior energy density. However, the stationary grid storage market has aggressively and decisively shifted toward Lithium Iron Phosphate (LFP) technology.

By 2025, LFP batteries accounted for roughly 90% of all global grid storage deployments, up from well below 50% just five years prior 29. While LFP batteries possess lower volumetric energy density - making them slightly heavier and bulkier, which is irrelevant for a stationary facility - they are vastly superior for grid applications. LFP utilizes abundant, highly inexpensive iron and phosphate rather than volatile, expensive, and ethically fraught supply chains of nickel and cobalt 14. In fact, the lowest LFP cell prices tracked by BNEF in 2025 hit an astonishing $36/kWh 40. Furthermore, LFP is exceptionally thermally stable, drastically reducing catastrophic fire risk, and boasts superior cycle life, allowing grid operators to aggressively charge and discharge the batteries daily for decades with minimal degradation 2. The normalization of LFP chemistry ensures that grid storage costs will continue to decline, structurally independent of geopolitical bottlenecks in exotic critical minerals.

FAQ 5: What Are the Practical Takeaways for Consumer Bills and Grid Reliability?

While the physics and engineering of the grid transition are highly technical, the end results resonate directly in the wallets, safety, and daily lives of everyday consumers. Utility-scale batteries act as massive grid-level shock absorbers; they elegantly smooth out the chaotic pricing mechanisms of liberalized wholesale electricity markets.

Crushing Peak Wholesale Prices

In unregulated, free-market power grids like ERCOT, consumer retail power bills are ultimately heavily influenced by the wholesale price of electricity, which skyrockets during periods of peak demand when expensive natural gas peaker plants are forcefully dispatched to prevent blackouts.

Batteries inherently destroy this economic model. By charging with solar power when prices are rock-bottom (or even negative) and flooding the grid with cheap, stored energy during the evening peak, batteries aggressively suppress wholesale price spikes. The data from 2024 provides conclusive, undeniable evidence of this phenomenon. In ERCOT, system-wide Real-Time power prices nearly halved in 2024, falling from an annual average of $48/MWh in 2023 to $26/MWh in 2024 43.

The immense success of batteries in lowering consumer costs presents a fascinating, almost punishing economic paradox for the developers who build them: the "cannibalization" effect. Because batteries rely on volatile price spreads (buying low, selling high) to make a merchant profit, deploying thousands of megawatts of batteries flattens the price curve, thereby eroding their own future revenues. In CAISO, net market revenue for batteries decreased by a third in 2024, falling from $78/kW-yr to $53/kW-yr 144. In ERCOT, average battery revenues plummeted by 71% year-over-year in 2024 26. While this severe revenue compression presents a challenge for private investors and underscores the vital need for robust capacity markets or long-term tolling agreements to guarantee continued development, it is an undeniable windfall for everyday ratepayers who are firmly shielded from astronomical scarcity pricing.

Behind-the-Meter Benefits for Commercial and Residential Consumers

Beyond the macroeconomic wholesale market, batteries are shielding commercial and industrial (C&I) consumers from highly targeted, punitive utility tariffs. In California, electricity rates have surged roughly 50% since 2020, largely due to immense transmission and distribution (T&D) charges levied to fund wildfire prevention, vegetation management, and legacy infrastructure upgrades 45.

For massive commercial enterprises, up to 40% of their monthly electric bill is determined by "demand charges" - draconian fees based on the single highest hour of electricity consumption during the month 45. By installing "behind-the-meter" batteries on-site, businesses can perfectly flatten their demand profile. The local battery discharges during the facility's peak operational hour, ensuring that the facility never pulls a massive spike of power from the grid. This simple, automated load-shifting maneuver completely bypasses exorbitant utility demand charges, stabilizing operational expenditures while simultaneously reducing physical strain on the local distribution grid 45.

Similarly, residential customers in California are rapidly adapting. Under the state's revised Net Billing Tariff (NBT/NEM 3.0), the compensation for exporting daytime solar to the grid was severely slashed, strongly incentivizing self-consumption. Consequently, consumers are increasingly pairing solar panels with home batteries. In April 2024, over 50% of new residential solar installations in California were paired with storage - up from just 20% in October 2023 - allowing homeowners to store their midday generation and utilize it during expensive, peak-rate evening hours 47. Furthermore, independent analysis highlights that utilizing batteries to phase out aging natural gas peaker plants - which are disproportionately located in low-income communities and communities of color - drastically reduces localized pollution, yielding massive societal dividends in public health and environmental justice 28.

Bottom line

The comprehensive deployment data from 2023 and 2024 reveals a definitive turning point: grid battery storage has entirely transitioned from an experimental, auxiliary pilot technology to the absolute, indispensable bedrock of modern electrical grid stability. Led by rapid, policy-and-market-driven deployments in China, the United States, Europe, and Australia 45, the global utility-scale storage fleet is expanding at an unprecedented, exponential rate, directly enabled by a historic 93% reduction in lithium-ion pack costs since 2010 40.

Whether operating under the highly regulated, capacity-driven mandates of California's CAISO, or the ruthless, volatile free-market structure of Texas's ERCOT, batteries have proven their superior physical and economic ability to manage modern grid dynamics. By systematically replacing brittle fossil-fuel peaker plants, batteries absorb massive surpluses of cheap midday solar power and instantly inject that exact energy during critical evening demand spikes. In doing so, they have definitively demonstrated their ability to prevent rolling blackouts during extreme climate-driven heat waves and winter storms, while simultaneously crushing the wholesale price spikes that ultimately inflate consumer utility bills. As the energy transition accelerates, the electrical grid of the future will not simply be defined by how much clean power it can predictably generate, but by its capacity to intelligently store, manage, and dispatch that power exactly when humanity needs it most.