What Is Stripe and How Does It Make Money

Stripe is a financial infrastructure platform that enables businesses to accept payments, manage subscriptions, and navigate global commerce online and in person. The company generates the majority of its revenue by taking a small percentage - typically 2.9% plus a 30-cent fixed fee - on every successful transaction it processes, alongside a growing ecosystem of high-margin software products for billing, automated tax compliance, and fraud prevention.

The Invisible Engine of Internet Commerce

When a consumer purchases a physical good from an online retailer, subscribes to a software service, or hails a rideshare, they rarely consider the complex financial choreography occurring behind the screen. For a digital transaction to succeed, sensitive data must securely travel from a website checkout page through payment gateways, fraud detection algorithms, card networks, and banking institutions within milliseconds. Stripe provides the foundational software code that orchestrates this entire process 1.

Founded in 2010 by brothers Patrick and John Collison, Stripe emerged to solve a glaring vulnerability in the early internet economy: writing code to accept credit cards was famously difficult and resource-intensive 234. Historically, businesses seeking to operate online had to establish separate merchant accounts with acquiring banks, integrate cumbersome payment gateway software, and navigate dense regulatory and security compliance frameworks 35. The process could take weeks of negotiations and significant engineering overhead.

Stripe collapsed this complexity into an Application Programming Interface (API) that developers could integrate into a website with just seven lines of code 67. By acting as a single intermediary that aggregates millions of businesses underneath its own master merchant account, Stripe removed the bureaucratic hurdles of digital commerce 58.

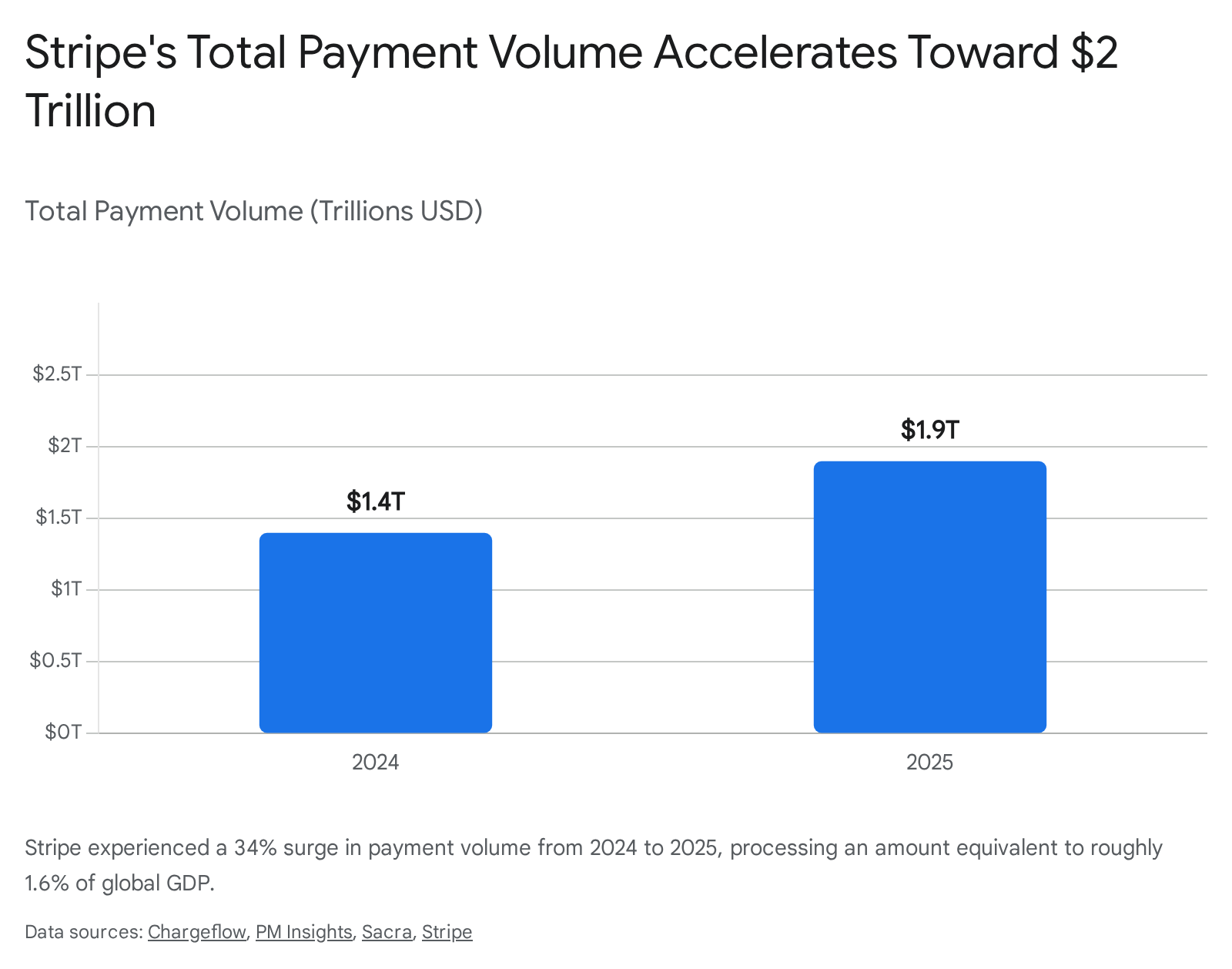

This developer-first philosophy transformed the company from a simple payment gateway into the default financial operating system for the modern internet. As of 2026, Stripe powers payments for 90% of the Dow Jones Industrial Average and 80% of the Nasdaq 100, including massive technology conglomerates like Amazon, Microsoft, and OpenAI, alongside traditional brands such as Ford and Starbucks 295. In 2025 alone, the platform processed $1.9 trillion in total payment volume - a figure equivalent to roughly 1.6% of the global gross domestic product (GDP) 56.

The scale of this adoption demonstrates that Stripe is no longer just a vendor; it is a structural pillar of global macroeconomic movement.

The Anatomy of a Stripe Transaction

To understand how Stripe monetizes its platform, it is necessary to examine the mechanics of the transaction lifecycle. Every electronic payment triggers a highly coordinated sequence of steps across disparate financial institutions 1.

When a customer submits their payment information on a Stripe-powered checkout page, the data is instantly encrypted and securely transmitted to Stripe's servers 1213. Stripe, acting as the payment processor, routes this authorization request through a card network - such as Visa, Mastercard, or American Express - directly to the customer's credit card issuing bank 113. The issuing bank runs instantaneous algorithms to verify available funds and check for fraud signals 1.

If the transaction is approved, the decision flows back through the network infrastructure to Stripe, which immediately communicates the successful capture to both the customer and the business 113. Following this authorization, the actual funds enter the clearing and settlement phase. The money moves from the issuing bank to Stripe's acquiring bank partners, and is finally deposited into the merchant's business bank account. This payout timeline is typically completed within two business days, though instant payouts are available for a premium fee 1814. Stripe makes its money by exacting a toll for facilitating, routing, and securing this rapid data exchange.

The Pricing Engine: How Stripe Charges for Payments

Stripe's foundational business model relies on usage-based transaction fees. For standard merchant accounts, the company employs a "blended" or flat-rate pricing model. This means that instead of charging businesses varying rates based on the specific type of credit card used - such as a premium travel rewards card versus a basic debit card - Stripe charges a single, predictable percentage alongside a flat per-transaction fee 115.

Standard Domestic Card Processing

As of 2026, the baseline fee for a successful domestic online card payment in the United States remains at 2.9% of the transaction amount, plus 30 cents 15167. For a theoretical $100 purchase, the merchant pays a total processing fee of $3.20, resulting in a net business deposit of $96.80 1518.

This baseline rate adjusts depending on the exact method the consumer uses to present the card. If a retail business utilizes Stripe Terminal hardware to accept a physical card in-person - via a modern dip, tap, or swipe - the inherent risk of digital fraud is considerably lower. Recognizing this, Stripe charges a reduced rate of 2.7% plus 5 cents for domestic in-person transactions 15167. Conversely, if a merchant bypasses security hardware or secure digital checkouts and manually types a customer's credit card number into their Stripe dashboard, the fraud risk spikes dramatically. To offset this risk, Stripe adds a 0.5% premium, bringing the total cost to 3.4% plus 30 cents 12157.

International Commerce and Currency Conversion

When internet businesses expand their operations globally, payment processing becomes vastly more expensive and complex. If a merchant based in the United States processes a card issued by a bank in Europe or Asia, Stripe applies an additional 1.5% cross-border fee to cover the increased international network routing costs 15719. Furthermore, if that specific transaction requires converting the customer's local currency into the merchant's home settlement currency, an additional 1% currency conversion fee is levied 1516. Therefore, a $100 international transaction requiring currency conversion could cost an American merchant $5.20 in processing fees (2.9% base + 1.5% international + 1% conversion + 30 cents) 18.

Alternative Payment Methods and Financing

Stripe has systematically expanded its infrastructure to support more than 100 global payment methods, allowing online merchants to cater to hyper-local consumer preferences 89. These alternative methods carry distinct pricing architectures: * ACH and Bank Transfers: Processing payments directly from a customer's bank account via the Automated Clearing House (ACH) network bypasses the traditional credit card networks entirely. Stripe charges just 0.8% for ACH Direct Debit transactions, capped at a maximum fee of $5.00 15167. This makes ACH highly attractive for businesses handling massive invoice amounts, such as B2B wholesalers or enterprise software vendors, who can save hundreds of dollars per transaction compared to card processing 18. * Buy Now, Pay Later (BNPL): Integrating consumer financing options like Klarna, Affirm, or Afterpay significantly increases checkout conversion rates and average order values for retailers. However, the merchant absorbs the cost of offering this unsecured credit. Stripe charges between 5.99% and 6.00% plus 30 cents for these BNPL transactions 157. * Stablecoins: For businesses accepting digital dollar cryptocurrencies, Stripe applies a flat 1.5% fee on the transaction amount in USD to settle the digital assets into fiat currency 157.

Core Processing Fees at a Glance

The following table outlines the core transaction fees a standard US-based merchant encounters on Stripe's pay-as-you-go pricing plan as of 2026 15167.

| Transaction Type | 2026 Processing Rate | Operational Context |

|---|---|---|

| Online Card (Domestic) | 2.9% + 30¢ | Applies to standard Visa, Mastercard, Amex, Discover, Apple Pay, and Google Pay digital wallets. |

| In-Person Card (Terminal) | 2.7% + 5¢ | Requires a physical card to be present (tap, dip, swipe) using certified hardware. |

| ACH Direct Debit | 0.8% (Capped at $5) | Highly cost-effective alternative for B2B and high-value wholesale transactions. |

| Manually Keyed Card | +0.5% Surcharge | Applied when physical cards or secure online checkouts are bypassed by the merchant. |

| International Card | +1.5% Surcharge | Applied to cards issued by a bank outside the merchant's home country. |

| Currency Conversion | +1.0% Surcharge | Applied if funds must be dynamically converted to the merchant's settlement currency. |

| Stablecoin Payments | 1.5% Flat Fee | The cost of settling digital asset transactions (like USDC) into fiat currency. |

| Dispute / Chargeback | $15.00 Flat Fee | Charged per dispute filed by a customer; returned only if the merchant wins the case. |

Following the Money: Interchange, Networks, and Take Rates

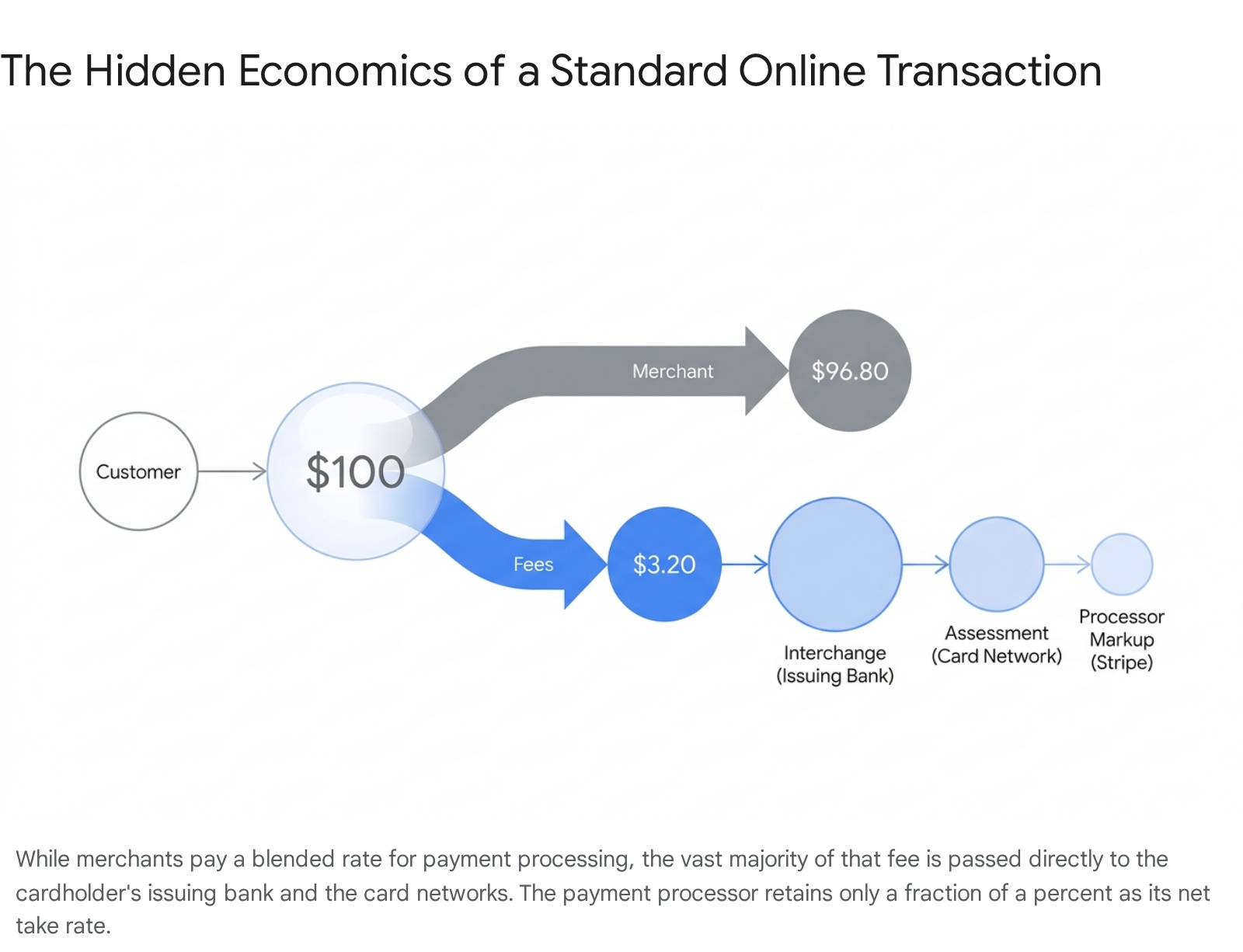

A pervasive misconception among business owners is that Stripe retains the entirety of the 2.9% processing fee for its own corporate profits. In reality, the payment processing industry operates on exceedingly tight margins, and the gross fee acts as a bundle that must pay several different financial stakeholders 1.

When a merchant pays $3.20 on a $100 transaction, the money is distributed across three primary channels:

- Interchange Fees (The Issuing Bank): The largest portion of the fee goes directly to the bank that issued the customer's credit card 1. This fee compensates the bank for the risk of extending unsecured credit and funds the lucrative rewards programs (cash back, travel points) that consumers demand. Interchange rates vary wildly depending on the card; a basic debit card costs pennies to process, while a premium corporate travel card commands a massive percentage 110.

- Assessment Fees (The Card Network): A smaller percentage is paid to the card networks - such as Visa, Mastercard, Discover, or American Express - for the privilege of routing authorization data across their proprietary global infrastructure 1.

- The Processor Markup (The Net Take Rate): Stripe only keeps what remains after the interchange and network assessment fees have been satisfied. This remainder covers Stripe's operational costs, security infrastructure, and corporate profit 1.

Because Stripe charges a flat 2.9% rate regardless of what card the customer uses, its actual profit margin fluctuates on every single transaction. If a customer uses a cheap-to-process debit card, Stripe enjoys a healthy margin. If a customer uses an ultra-premium rewards card, the underlying interchange fee eats up almost the entire 2.9%, leaving Stripe with practically nothing.

While Stripe operates as a private company and does not publish precise margin data, financial analysts estimate that across its multi-trillion-dollar portfolio, Stripe's gross fees convert into a net take rate of approximately 0.40% after clearing interchange, network, and partner costs 23. This dynamic reveals why sheer volume is paramount to Stripe's business model. Capturing just a fraction of a percent requires processing trillions of dollars to generate meaningful enterprise value 3.

Expanding the Revenue Model: The "Software Stack"

If payment processing is fundamentally a low-margin commodity bound by the unyielding math of interchange fees, how did Stripe achieve a valuation of $159 billion? The answer lies in the company's aggressive, decade-long expansion into enterprise software 37.

Over time, Stripe shifted its strategic positioning from being a mere payment gateway to becoming a comprehensive "Revenue and Finance Automation Suite" 2311. By building auxiliary software products that sit natively on top of its payment rails, Stripe unlocked high-margin, sticky revenue streams that are not subjected to the toll roads of the card networks 712. Because the marginal cost to deliver cloud software is minimal compared to the cost of moving money, these products radically improve Stripe's unit economics.

Stripe Billing and Subscription Management

Subscription-based businesses - ranging from software-as-a-service (SaaS) providers to monthly physical delivery boxes - require complex accounting infrastructure. These businesses must manage recurring charges, handle failed payments via automated dunning, and prorate upgrades or downgrades perfectly mid-billing cycle 2613. Furthermore, software pricing models have become increasingly sophisticated, shifting from simple flat-rate subscriptions to tiered pricing, freemium models, and pay-as-you-go usage-based structures 1314.

Stripe Billing handles this complex logic. In 2024, Stripe consolidated its billing tiers and increased the price of its standard billing product to 0.7% of recurring volume 712. Crucially, this 0.7% is charged in addition to the baseline 2.9% payment processing fee 1229. By early 2026, Stripe's automation suite was on track to hit an annual revenue run rate of $1 billion, managing nearly 200 million active subscriptions worldwide for clients ranging from small creators to AI giants 223.

Stripe Tax and Automated Compliance

Global digital commerce requires navigating a labyrinth of international tax codes, European Value-Added Tax (VAT) laws, and state-by-state sales tax thresholds in the United States. Instead of merchants hiring dedicated accounting compliance teams, Stripe Tax automates calculations, threshold monitoring, and collections directly within the checkout flow 15.

Stripe monetizes this compliance through two primary pricing structures. For standard users who want a no-code integration, Stripe charges a pay-as-you-go fee of 0.5% on the total volume processed in jurisdictions where the merchant is registered to collect tax 716. For enterprise users who integrate directly via the API, Stripe charges $0.50 per transaction call (which includes 10 free calculation calls), and $0.05 for each subsequent calculation 16. Over 67,000 companies now utilize this infrastructure rather than building proprietary tax software 15.

Stripe Radar and Fraud Prevention

As an aggregator of global payment data across millions of merchants, Stripe possesses immense visibility into fraudulent purchasing patterns 7. It leverages this vast data pool to train machine learning models for its proprietary fraud detection tool, Stripe Radar 717.

While basic Radar protection is included in the standard 2.9% pricing tier, larger enterprise customers operating on negotiated custom processing rates must pay for this security separately. These custom accounts pay between $0.02 and $0.07 per screened transaction for access to advanced fraud control panels and AI interventions 719. The return on investment for merchants is substantial; internal data indicates that Radar reduces fraud by an average of 71% across alternative payment methods like Klarna and Cash App Pay 15.

Financial Services: Connect, Capital, and Atlas

Stripe has systematically built tools that position it as the holistic financial operating system for digital businesses, expanding far beyond the checkout page.

- Stripe Connect: Designed specifically for multi-sided marketplaces (like Uber or Shopify), Connect facilitates complex money routing, split payments, and seller payouts to independent contractors 2918. Stripe monetizes this infrastructure with per-active-account fees (e.g., $2 per month) and payout transaction fees, capturing revenue on both sides of the marketplace transaction 19.

- Stripe Capital: Acting as a modern fintech lender, Stripe utilizes algorithmic models based on a merchant's real-time cash flow to offer immediate working capital loans 6. The loan is automatically repaid through a fixed percentage of the merchant's daily sales, drawing future working capital forward 6. This product fills a crucial macroeconomic gap; following the 2008 Global Financial Crisis and subsequent Basel III and Dodd-Frank reforms, traditional bank lending to small businesses contracted severely 6. In 2025, Stripe Capital funding volume grew by 45%, providing liquidity to over 81,000 businesses 6.

- Stripe Atlas: This unique tool allows global entrepreneurs to form a US-based Delaware corporation, issue stock, and open a bank account in minutes. While it generates some upfront fee revenue, its true purpose is strategic customer acquisition. By helping a startup incorporate, Stripe ensures it acts as the default payment processor from the company's first day of existence. In 2025, Atlas saw a 41% increase in company formations, with one in six new Delaware corporations now incorporating via the platform 76.

Security and PCI Compliance as a Service

A highly technical yet critical mechanism driving business adoption - and justifying Stripe's fees - is how the platform handles regulatory security burdens. Any business worldwide that accepts, processes, or transmits credit card data is legally obligated to comply with the Payment Card Industry Data Security Standard (PCI DSS) 2036. This rigorous framework contains over 300 security controls, including firewall configuration, data encryption, and vulnerability management, designed to prevent devastating data breaches 2122.

For a small merchant or even a mid-sized technology firm, auditing internal servers for PCI compliance is incredibly expensive, requiring dedicated security software, hardware, and external auditors 2022. Failure to comply can result in catastrophic fines and the revocation of payment processing privileges 36.

Stripe solves this massive headache through an architectural design called tokenization. When a customer enters their credit card into a Stripe Checkout form or mobile SDK, the sensitive PAN (Primary Account Number) data bypasses the merchant's servers entirely 2122. Instead, the data routes directly to Stripe's heavily encrypted, PCI Level 1 certified vaults 2223. Stripe then hands the merchant a secure, randomized digital "token" representing the card, which the merchant can safely store in their own database to trigger future charges without ever actually touching the raw credit card data 3621.

This structural design drastically reduces the merchant's legal and security liabilities. By utilizing Stripe's hosted elements, a merchant can reduce their compliance scope from a highly complex SAQ D (Self-Assessment Questionnaire) to a simplified SAQ A 36. Furthermore, Stripe maintains rigorous internal security postures, operating under a zero-trust approach for employee access, regular SOC 1/2/3 audits, and EMVCo Level 1 and 2 certifications for its hardware terminals 23. This security-as-a-service acts as a massive value-add that deters businesses from seeking cheaper, bare-bones payment processors 36.

The Competitive Ecosystem: Stripe vs. The Market

As of 2026, the payment processing market is fiercely contested. While Stripe is the undisputed dominant player among developers and high-growth technology companies, holding roughly 20.8% to 29% of the global online payment processing sector, it competes against several specialized giants 4041.

Stripe vs. PayPal and Braintree

PayPal is the oldest heavyweight in the digital payments arena. Globally, PayPal commands a larger overall market share (roughly 43.4%) than Stripe 40. However, the companies serve fundamentally different core needs. PayPal's greatest asset is its legacy consumer trust; millions of shoppers prefer the friction-free experience of logging into a consumer-facing PayPal wallet rather than hunting for a physical credit card 184243.

However, PayPal traditionally operates as a closed ecosystem. Stripe, conversely, was built as an invisible, "white-label" infrastructure meant to blend seamlessly into a brand's own website architecture 318. While PayPal remains highly relevant for small e-commerce merchants and peer-to-peer transfers, Stripe's enterprise adoption has radically altered the growth dynamics between the two firms. In 2025, Stripe's total payment volume grew by 34% to $1.9 trillion, far outpacing PayPal's 7% growth on $1.79 trillion 43. The trajectory gap has widened so significantly that in early 2026, major financial outlets reported that Stripe was actively weighing an acquisition of all or parts of PayPal 4344.

Stripe vs. Adyen

Adyen is Stripe's primary competitor in the global enterprise sector. Operating out of the Netherlands, Adyen bypasses traditional third-party acquiring banks because it holds its own banking licenses 18. This end-to-end control allows Adyen to offer "Interchange++" pricing - a highly transparent model where merchants pay the exact raw interchange and network costs, plus a fixed per-transaction markup (e.g., $0.13) rather than a blended percentage 1845.

For startups and small businesses, Stripe's flat 2.9% rate is simpler, easier to predict, and requires no monthly minimums 45. But for massive multinational corporations processing hundreds of millions of dollars, Adyen's Interchange++ model is mathematically cheaper 184524. Financial analysts suggest the break-even point where Adyen's fixed-fee model becomes more cost-effective than Stripe's percentage markup typically occurs between $750,000 and $1.2 million in monthly processing volume 45. Furthermore, Adyen boasts stronger direct local acquiring relationships in Europe, which can improve authorization rates by several percentage points - a metric that translates to millions in recovered revenue at enterprise scale 24. Consequently, Adyen remains the processor of choice for mature global giants like Spotify and Uber, while Stripe dominates the high-growth software and AI sectors 1847.

Stripe vs. Square

Square (owned by Block, Inc.) dominates the physical retail space. Its business model relies heavily on integrating payment processing directly into specialized point-of-sale (POS) hardware tailored for cafes, salons, and brick-and-mortar shops 264248.

Historically competitive on price, Square alienated many digital merchants in 2026 by quietly raising its standard free-tier online processing rates to a steep 3.3% plus 30 cents, making Stripe the clearly more economical choice for purely digital businesses 484950. Furthermore, manually keyed transactions on Square cost a punitive 3.5% plus 15 cents 4950. Conversely, businesses heavily reliant on physical locations generally find Square's cohesive hardware-software ecosystem superior to Stripe's developer-centric Terminal offerings 4225.

Financial Scale and the 2026 Valuation

Because Stripe remains a privately held company - steadfastly resisting immense market pressure to execute an Initial Public Offering (IPO) - it does not publish traditional quarterly earnings reports 252. However, detailed financial metrics routinely surface during private equity events and annual letters.

In February 2026, Stripe executed a major tender offer - a liquidity event allowing current and former employees to sell their private shares to institutional investors 5253. The majority of funds for this offer were provided by heavyweights including Thrive Capital, Coatue Management, and Andreessen Horowitz (a16z), while Stripe also utilized a portion of its own corporate cash to repurchase shares 525354.

This transaction valued Stripe at an astronomical $159 billion 5354. This represented a massive 70% jump from its $91.5 billion valuation established in early 2025, firmly cementing it as the most valuable privately owned financial technology company in the world 525426.

The valuation is underpinned by extraordinary financial scale. In 2024, Stripe reported approximately $5.1 billion in net revenue 256. For 2025, financial analysts estimate net revenue reached between $5.8 billion and $6.9 billion, supported by the $1.9 trillion flowing through its servers 22356. Furthermore, leadership has officially confirmed that the company remains "robustly profitable," allowing it to fund aggressive research and development - and execute billion-dollar acquisitions - entirely through its own cash flow without relying on external venture capital injections 62354.

The Next Era: Bridge, Stablecoins, and Agentic Commerce

While Stripe achieved its $159 billion valuation by mastering and optimizing the legacy credit card system, the company is actively preparing to disrupt the very rails it relies upon. The current global banking network is fundamentally slow, expensive, and constrained by international borders and weekend operating hours 3857.

To solve this, Stripe has made a massive strategic pivot toward stablecoins - cryptocurrencies whose values are directly pegged 1:1 to traditional fiat currencies like the US Dollar 5827. In 2025, global stablecoin payment volume doubled to roughly $400 billion, diverging entirely from the volatility of broader crypto assets 6. Stripe estimates that 60% of this volume represents legitimate cross-border business-to-business settlements rather than retail speculation 628.

The $1.1 Billion Bridge Acquisition and Bank Charter

In late 2024, Stripe spent $1.1 billion to acquire Bridge, a startup specializing in stablecoin payment orchestration 535729. Bridge provides a developer-friendly API that allows businesses to seamlessly convert between traditional fiat currencies and digital dollars without needing extensive blockchain expertise 2730. Prior to the acquisition, Bridge was already processing an annualized volume of $5 billion, facilitating everything from cross-border aid in Latin America to global treasury management for SpaceX 5729.

Following the acquisition, Stripe sought deep regulatory legitimacy. In February 2026, the Office of the Comptroller of the Currency (OCC) granted Bridge conditional approval for a national trust bank charter 313265. This charter is a watershed moment for the fintech industry. Once fully finalized, it allows Stripe's subsidiary to legally custody digital assets, manage stablecoin reserves, and issue stablecoins under unified federal oversight, aligning with the new GENIUS Act regulations 653334.

This move allows Stripe to bypass the fragmented system of applying for individual state-by-state money transmitter licenses 6533. However, the charter application has faced pushback. The National Community Reinvestment Coalition (NCRC) and various banking trade groups urged the OCC to reject the application, arguing that granting limited-purpose trust charters to fintechs allows them to operate as shadow banks with a lighter regulatory touch, heightening systemic risk 653368. Despite this friction, by owning the infrastructure that issues and settles stablecoins, Stripe positions itself to facilitate instantaneous, near-zero-cost global transactions, entirely bypassing the legacy toll roads owned by Visa, Mastercard, and traditional acquiring banks 85730.

Powering the AI Economy

Stripe's evolution into programmable money is inextricably linked to the artificial intelligence boom. The company currently processes payments for virtually all top-tier AI developers, including OpenAI, Anthropic, and Perplexity 9669.

As AI evolves from conversational chatbots into autonomous agents capable of executing complex tasks across the web, Stripe is building the economic layer for "agentic commerce" 326. Through initiatives like the Agentic Commerce Protocol (co-developed with OpenAI) and machine payments, Stripe is enabling AI agents to autonomously negotiate, purchase API credits, and instantly settle micro-transactions using stablecoins 3626. By combining automated subscription billing, native stablecoin settlement, and robust fraud prevention, Stripe is transitioning from a tool used to process credit cards into the foundational monetary protocol for the automated internet.

Bottom line

Stripe is an indispensable pillar of modern internet commerce, operating as the primary interface between millions of digital businesses and the complex, legacy banking system. It generates vast revenue by charging percentage fees on trillions of dollars in transaction volume, while systematically expanding its profit margins through a highly integrated ecosystem of automated billing, tax, and security software. While its $159 billion valuation relies heavily on its current dominance in the traditional credit card space, Stripe's aggressive expansion into federally regulated stablecoin infrastructure and agentic commerce signals its ambition to rewrite the fundamental rules of global money movement over the next decade.