Gender differences in risk tolerance and consumer financial behaviors

The Paradigm Shift in Behavioral Finance

Historically, the foundational premise within both academic behavioral finance and applied wealth management has been that women are inherently more risk-averse than men 123. This dominant narrative dictated everything from the design of retail financial products to the heuristics utilized by wealth advisors, effectively shaping the macroeconomic participation of half the global population. However, recent rigorous reviews of early empirical data - such as the reassessment of Charness and Gneezy's influential findings on gender disparities in risk-taking - demonstrate that the statistical case for innate, immutable gender differences is considerably less substantial than traditionally portrayed 145. Contemporary research indicates that differences observed at the aggregate level are often modest, highly context-dependent, and heavily influenced by structural constraints, shifting macroeconomic environments, and the systemic disparities inherent in financial advisory services 136.

As the global economy approaches the "Great Wealth Transfer" - an estimated $84 trillion expected to pass to younger generations, and predominantly to women who outlive their male counterparts, by 2030 - understanding the nuanced reality of female consumer financial behavior is a macroeconomic imperative 779. Women currently control about one-third of all retail financial assets in the United States and Europe, a share projected to rise to 45% by the end of the decade 9. Evidence suggests that female investors engage in strategic, calculated risk-taking that diverges significantly from the impulsive or overconfident risk-taking frequently observed in male cohorts 710.

Furthermore, the modernization of financial platforms, the rapid proliferation of retail trading applications, and significant macroeconomic events such as the 2022 - 2025 global inflation shocks have catalyzed profound shifts in how diverse demographics interact with capital markets 89. This report provides an exhaustive, multi-disciplinary examination of gender differences in consumer financial behaviors, prioritizing recent literature from leading economic and sociological sources. By explicitly disentangling the concepts of risk tolerance, risk perception, and risk capacity, the analysis deconstructs the mechanisms driving observed behavioral divergence. It moves beyond Western-centric datasets to include cross-cultural phenomena and integrates a critical intersectional lens to evaluate how variables such as age, marital status, and baseline wealth interact with structural mechanisms to dictate long-term financial outcomes.

Disentangling the Risk Triad: Capacity, Perception, and Tolerance

To accurately evaluate financial behavior, the academic literature insists on a strict taxonomic differentiation between three frequently conflated variables: risk capacity, risk perception, and risk tolerance 1011. A historical failure to differentiate these elements led to the blanket assumption of female "risk aversion," when in reality, women were often responding rationally to suppressed financial capacities or heightened, accurate perceptions of systemic risk 310.

Risk Capacity: The Objective Constraint

Risk capacity is an objective, mathematical metric that defines the extent to which an individual or household can absorb financial losses without suffering adverse, ruinous outcomes to their standard of living 10. It is entirely dependent on structural variables such as baseline wealth, liquid assets, income stability, time horizon, and the number of dependents 1012. The data systematically demonstrates that women, on average, possess significantly lower risk capacity than men 3. This diminished capacity is driven by lower lifetime earnings, higher rates of part-time work, career interruptions due to disproportionate caregiving responsibilities, and longer life expectancies that stretch limited retirement pools over a broader time horizon 3.

If an individual's risk capacity is low, engaging in high-variance, high-risk investment strategies exacerbates their financial precarity 10. Thus, a lower allocation to equities by a female investor may not reflect a psychological aversion to risk, but rather a highly rational alignment of her portfolio with her objective, structurally constrained risk capacity. For instance, single women are significantly less likely to engage in financial behaviors compared to men, yet studies demonstrate that this disparity is fundamentally linked to lower income and larger household sizes rather than inherent psychological differences 13.

Risk Perception: The Cognitive Assessment

Risk perception refers to the subjective cognitive assessment of the danger or uncertainty inherent in a specific financial decision 10. It evaluates how an individual interprets the probability of a negative outcome. Research highlights that macroeconomic conditions, trust in institutions, and objective financial literacy heavily modulate risk perception 1415. Women often display higher risk perception, viewing certain financial instruments - such as direct stock purchases or cryptocurrency - as more perilous than men do 101516.

This elevated perception of danger is partially attributed to a well-documented confidence gap. Surveys, such as the barometer issued by France's Autorité des marchés financiers (AMF), reveal that women are far less likely to be confident in their financial knowledge compared to men (28% versus 51%) 16. However, when tested with technical questions, the AMF found that women accurately assess their knowledge, whereas men systematically overestimate theirs 16. When an individual perceives a market as highly volatile, opaque, or overly complex, their willingness to engage diminishes independently of their inherent tolerance for volatility 141517.

Risk Tolerance: The Psychological Baseline

Risk tolerance is the psychological and emotional ability to withstand fluctuations, uncertainty, and potential losses in the pursuit of future growth 1018. It is an attitudinal trait related to personality, biological predispositions, and deeply ingrained socialization 11. While older studies posited massive gender gaps in risk tolerance, modern analyses reveal a converging reality. Data from the 2022 Survey of Consumer Finances (SCF) demonstrates that when controlling for education, wealth, and human capital among never-married individuals, both single men and single women exhibit decreasing relative risk aversion as wealth increases, with no statistically significant gender difference in this behavioral trait 319.

Where psychological differences in risk tolerance do appear, they are frequently mediated by the "Big Five" personality traits. Individuals displaying higher openness to experience and extraversion tend to exhibit higher risk tolerance, while higher neuroticism correlates heavily with risk aversion 311. Furthermore, loss aversion - the psychological phenomenon where losses loom larger than equivalent gains - has been shown to account for roughly 53% of the observed gap in the willingness to take risks between men and women, supplemented by an additional 3% attributed to lower levels of generalized financial optimism among females 20. Interestingly, neurological studies utilizing electroencephalogram (EEG) methodologies have found that individuals displaying higher alpha and theta wave activity engage in more risk-taking behaviors, whereas women, on average, exhibit distinct wave patterns that may biologically predispose them to take fewer impulsive financial risks 21.

Stated Preferences vs. Revealed Preferences: The Risk Discrepancy

A critical challenge in behavioral finance is the frequent misalignment between an individual's stated preferences (how much risk they claim they are willing to take in surveys, questionnaires, or hypothetical lotteries) and their revealed preferences (the actual risk profile of their investment portfolio based on their capital allocation) 4222324.

The "risk discrepancy" phenomenon occurs when nonprofessional investors hold portfolios with risk levels that significantly diverge from their elicited tolerances 2225. In a study analyzing Canadian retail investors, researchers utilized Value-at-Risk (VaR) modeling to mathematically compare elicited risk against revealed risk. The findings demonstrated that elicited risk is consistently higher than revealed risk, often because financial advisors build safety buffers into their recommendations or because investors fail to execute on their stated psychological thresholds 22.

When applying this framework to gender, a complex narrative emerges. Stated preferences often capture societal scripting and confidence levels, while revealed preferences capture actual economic action. Table 1 synthesizes the empirical divergence between stated and revealed risk preferences across genders based on recent (2022 - 2025) datasets.

| Behavioral Metric | Male Tendencies | Female Tendencies | Implications & Findings |

|---|---|---|---|

| Stated Risk Tolerance (Self-Reported Surveys) | Consistently reports a higher willingness to accept financial volatility for superior returns. Prone to overestimating personal risk tolerance 1329. | Frequently underestimates personal risk tolerance. Reports lower willingness to take risks, often selecting "no risk" or "below-average risk" on financial surveys 161929. | Surveys predominantly capture gendered confidence gaps and societal expectations rather than true psychological thresholds for risk absorption 29. |

| Revealed Preferences (Actual Portfolio Allocation) | Portfolios show higher initial equity allocations. Prone to impulsive, high-frequency trading and speculative assets (e.g., direct stocks, cryptocurrency) 10162631. | Actual portfolio allocations closely resemble male portfolios when controlling for age and income. Adopts steady buy-and-hold strategies, and trades less frequently 3726. | The gender gap in actual portfolio risk has narrowed substantially. Lower trading frequency in female portfolios consistently generates higher risk-adjusted alpha 713. |

| Reaction to Financial Shocks (Crisis/Loss) | More likely to view market dips as buying opportunities due to higher baseline financial optimism and overconfidence in forecasting abilities 2031. | Exhibits higher loss aversion. More apt to sell declining stocks and prioritize financial security over speculative growth during severe macroeconomic downturns 71320. | Loss aversion drives a significant portion of the behavioral gap during crises. Women prioritize long-term wealth preservation over short-term speculative recovery 1320. |

| Variance in Preferences (Distribution Patterns) | Exhibits "Greater Male Variability" (GMV); males dominate the absolute extreme ends of both the risk-taking and risk-averse spectrums 27. | Preferences cluster near the statistical median; women are significantly less likely to adopt extreme risk-seeking or extreme risk-averse behavioral outliers 27. | Simple mean comparisons underestimate reality; extreme male risk-takers skew aggregate data sets, creating an illusion of uniform male risk-seeking 27. |

This dynamic extends far beyond financial portfolios. Experimental data on ideal partner preference matching across 43 countries reveals a universal psychological tendency where women's stated preferences frequently underestimate their revealed preferences, highlighting a broad behavioral phenomenon where societal conditioning influences self-reported survey data, making revealed actions a far more reliable metric for economic analysis 282930.

Competing Hypotheses for Behavioral Divergence

To understand why these behavioral and perceptual gaps persist, the academic community has developed several competing theoretical frameworks. These hypotheses range from deeply ingrained biological and evolutionary arguments to complex sociological critiques regarding household bargaining and institutional discrimination. Table 2 summarizes the dominant paradigms.

| Hypothesis | Core Mechanism | Supporting Evidence & Context |

|---|---|---|

| The Biological / Evolutionary Hypothesis | Risk-taking is linked to hormonal markers (testosterone, cortisol), genetic predispositions, and historical evolutionary roles (hunter vs. gatherer dynamics) 331. | Physical markers such as the 2D:4D digit ratio have been correlated with managerial ability and masculine traits, suggesting a biological underpinning for extreme risk-taking 332. |

| The Socialization & Gender Norms Hypothesis | Risk aversion is a learned behavior. Patriarchal norms and societal scripting dictate that women should be cautious, nurturing, and financially conservative 33133. | In matrilineal societies (e.g., the Mosuo in China), girls exhibit higher economic risk tolerance than boys. This reverses only when children integrate into patriarchal school systems 31. |

| The Overconfidence & Loss Aversion Hypothesis | Men systematically overestimate their financial literacy and forecasting abilities. Women possess higher loss aversion, weighing the psychological pain of financial loss heavier than equivalent gains 32031. | Surveys of MBA students demonstrate that overconfident males predict impossible 30-50% annual returns, while empirical analysis attributes 53% of the gender risk gap to female loss aversion 2031. |

| The Endowment Effect & Ownership Hypothesis | Willingness to Pay (WTP) vs. Willingness to Accept (WTA) discrepancies. Women may require larger premiums to part with owned assets due to stronger self-association with possessions, increasing apparent risk aversion 2. | In gambling-framed decisions, women appear highly risk-averse, but this gap narrows significantly in differently framed contextual decisions (e.g., insurance or household purchasing) 2. |

| The Statistical Discrimination Hypothesis | Institutions and advisors assume women have lower financial literacy and tailor their services accordingly, leading to self-fulfilling prophecies of lower market engagement 3435. | Real-world audit studies reveal advisors recommend lower-risk, higher-fee products to women even when the women present identical risk profiles and wealth levels as male clients 3435. |

| The Risk Mitigation / Ethics Hypothesis | Female leadership and individual decision-making prioritize steady, ethical growth over volatile, high-stakes expansion, often viewed inaccurately as pure risk aversion 3637. | Female CFOs at firms with excess cash reduce holdings to distribute dividends, mitigating agency conflicts. This reflects ethical, stakeholder-aligned governance rather than fear of risk 36. |

These hypotheses are not mutually exclusive. The modern academic consensus points toward a synthesis where minor biological or evolutionary predispositions are vastly amplified by lifelong socialization, parental influence, and cultural stereotype beliefs, which ultimately crystallize as structural barriers in the labor and capital markets 363143. For instance, an analysis of applications to elite universities in China revealed that gender gaps in pursuing prestigious, high-risk educational paths were heavily driven by parental expectations and students' internalized stereotype beliefs (e.g., "Girls should stay near family"), completely overriding the students' inherent risk preferences 43.

Structural Mechanisms: The Intersectional Wealth Gap

To analyze consumer financial behavior without addressing the underlying macroeconomic and structural constraints is to observe symptoms while ignoring the pathogen. Risk capacity is inextricably linked to income and wealth, and gendered disparities in these areas are profound, particularly when viewed through an intersectional lens encompassing race, age, and marital status 3845.

The Racial and Gender Wage Gap

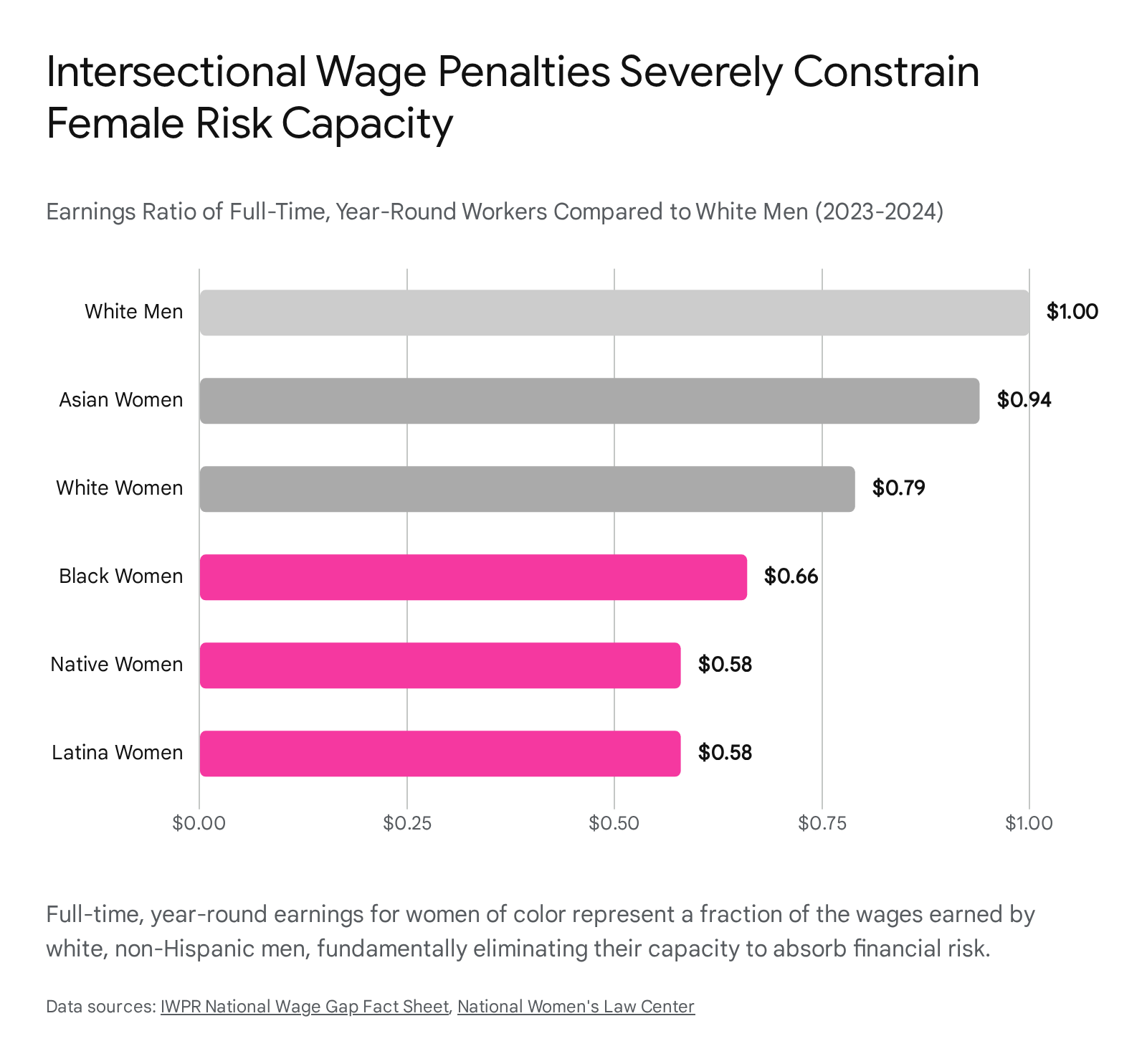

The United States labor market continues to perpetuate severe wage penalties for women, which dramatically restrict their ability to accumulate investable capital. In 2023 and 2024, data from the U.S. Census Bureau and the Department of Labor revealed that women working full-time, year-round received roughly 81 to 84 cents for every dollar paid to men 4639. However, analyzing the gap strictly along gender lines obscures the catastrophic impact of racial intersectionality.

When comparing earnings to the benchmark of white, non-Hispanic men, the disparities widen significantly. Black women working full-time, year-round earned just 65 to 66.5 cents on the dollar, translating to over $25,000 in lost wages annually 3846. Latina women faced an even steeper penalty, earning approximately 54 to 58 cents on the dollar, representing a deficit of over $32,000 per year 3846. Native women similarly earned 53 to 58 cents 46.

These wage deficits are driven almost entirely by occupational segregation, where Black and Hispanic women are disproportionately concentrated in service and production industries that historically offer lower wages, limited benefits, and virtually no avenues for wealth compounding 4539.

The Compounding Effect on Wealth and Risk Capacity

Income disparities compound exponentially over time, resulting in staggering wealth gaps that permanently alter financial behavior. According to Asset Funders Network data, while the median wealth of single white women stood at approximately $15,640, the median wealth for single Black women and Latina women was recorded at a devastating $200 and $100, respectively 45. This translates to minority women holding literally pennies on the dollar compared to white demographics 45.

From a behavioral finance perspective, these numbers dictate financial action. A Black or Latina woman with $200 in liquid wealth possesses a risk capacity approaching absolute zero. In such a scenario, participating in high-risk equity markets or speculative assets is not an option; wealth preservation and liquidity management become matters of basic survival 45. The structural inability to absorb a financial shock perfectly explains why minority and single women report higher levels of financial stress and exhibit behaviors that traditional finance mistakenly labels as generically "risk-averse" 4548.

Age, Marital Status, and Household Bargaining

Intersectional analysis further reveals that age and marital status significantly skew risk profiles. Generational convergence is occurring; while the gender gap in self-reported risk tolerance remains wide among older cohorts, it has narrowed substantially among Generation X and Millennials (Generation Y), only to modestly reappear in Generation Z, likely due to acute, short-term macroeconomic anxieties rather than a reversal of the long-term narrowing trend 13.

Marital status introduces the complex dynamics of household bargaining and asset management. Research mapping the life-cycle portfolio choices of households reveals that married women face a higher cost of financial literacy accumulation due to labor divisions within the home 49. Within marriage, women predominantly manage liquid, short-term accounts (holding 43% and 80% of household checking and savings balances, respectively), while the management of long-term, high-risk equity investments overwhelmingly falls to their husbands 49. This specialization limits women's experiential learning in equity markets. Furthermore, cross-cultural studies, such as those analyzing household decision-making in Malaysia, confirm that while both men and women practice autonomy in financial investments, earning share dictates bargaining power; women with lower relative incomes exhibit mechanically lower risk tolerance due to their diminished financial leverage within the household 40.

The Advice Gap: Systemic Disparities in Financial Services

While structural constraints limit capacity and macro-shifts test expectations, the financial services industry itself actively perpetuates behavioral gaps through discriminatory practices. A growing body of empirical literature confirms that women receive objectively worse financial advice than men, an inequality driven heavily by statistical discrimination rather than benign oversight 34355141.

Real-World Audit Studies and Advisor Bias

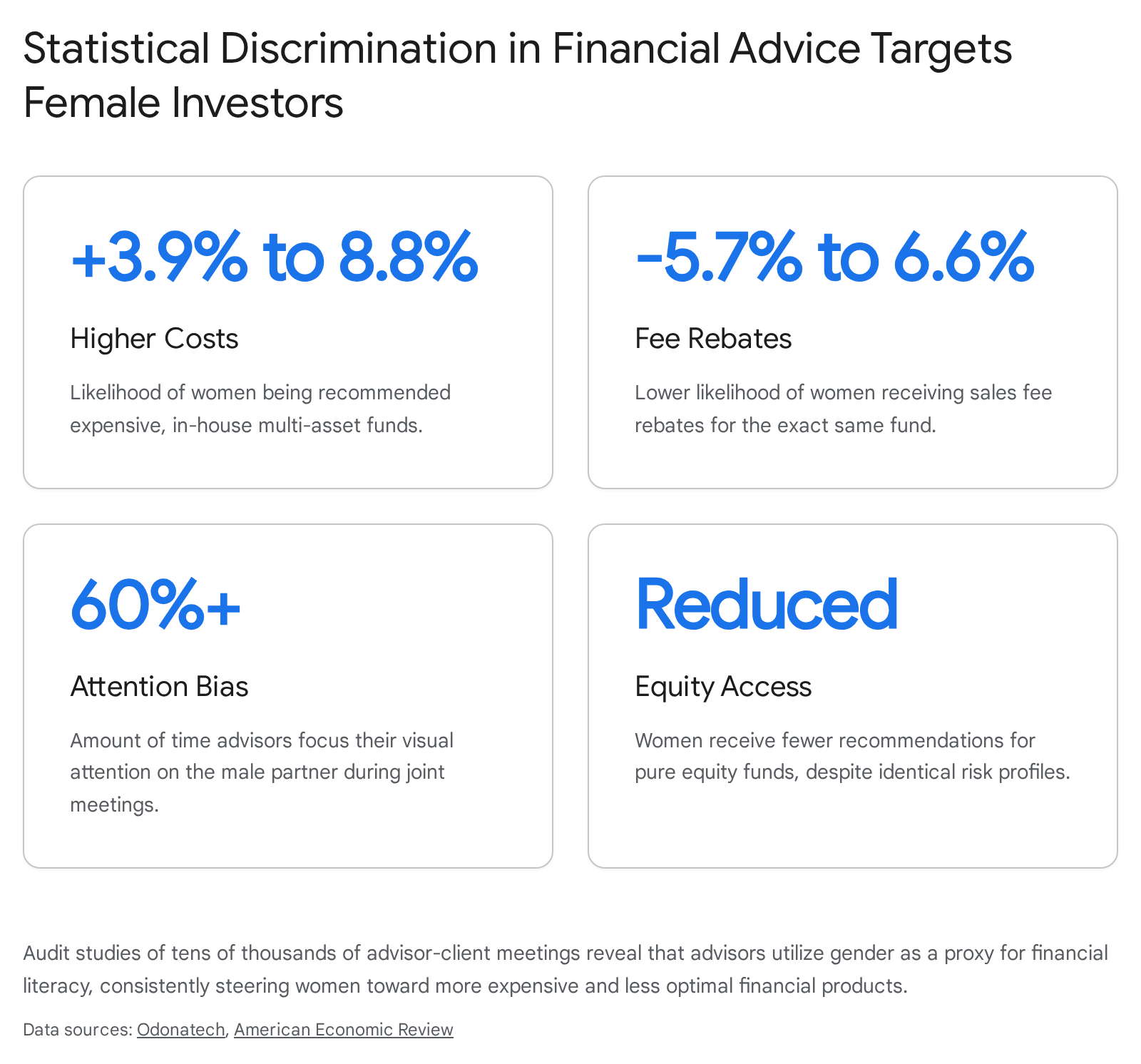

A landmark 2023 study by Bucher-Koenen et al. analyzed administrative data from over 27,000 real-world meetings between financial advisors and retail clients at a large German bank. The findings provided robust, quantitative evidence of systemic gender bias: female clients were 3.9% to 8.8% more likely to be recommended higher-cost, actively managed multi-asset funds issued by the banking group, and were 5.7% to 6.6% less likely to receive sales fee rebates compared to male clients dealing with the exact same advisor for the exact same fund 3451. Consequently, recommendations to women resulted in significantly higher annual costs and lower equity shares, potentially limiting long-term growth even when controlling for fund risk categories and client characteristics 3451.

Similarly, an exhaustive audit study conducted in Hong Kong by Bhattacharya et al. (2024) deployed trained undercover men and women to pose as potential clients across 65 local financial advisory firms 35. The results confirmed that at financial planning firms (where advisors have a fiduciary-like role but face inherent conflicts of interest regarding product promotion), women were far more likely than men to receive suboptimal advice, such as recommendations to purchase solely local or individual securities 35. Notably, this suboptimal advice was most frequently directed at women who signaled high confidence and high risk tolerance, penalizing female investors who defied traditional gender expectations 35.

The Mechanism: Statistical Discrimination

The theoretical models underpinning these global studies attribute this phenomenon to "statistical discrimination" rather than pure "taste-based discrimination" or overt malice 3435. Advisors interact with retail clients under conditions of profound asymmetric information. Because women, on an aggregate level, test lower on objective financial literacy quizzes and project lower financial confidence during interactions, advisors utilize client gender as a highly visible proxy for financial sophistication 3435. Operating under the assumption that the female client is less financially literate and less price-sensitive, the advisor steers her toward expensive, self-serving in-house products, confident she lacks the technical expertise to challenge the recommendation, identify the fee drag, or seek alternative markets 3451.

Furthermore, unconscious biases actively dictate interaction dynamics. Eye-tracking analyses conducted by major institutions during appointments with heterosexual couples reveal that both male and female advisors spend over 60% of their visual attention focused on the male partner, operating under the deeply rooted presumption that men are the primary financial decision-makers 51.

The "Gender Threat" and Trust Deficits

The gender dynamics of the advisor-client relationship also trigger psychological responses that alter revealed risk. Research on the "gender threat hypothesis" among UK investors demonstrates that individuals exhibit hyper-stereotypical risk attitudes when advised by a financial professional of the opposite gender 42. Men advised by a woman tend to take significantly more risk than when advised by a man, while women advised by a man adopt a far more cautious, risk-averse approach, likely due to ego-depletion and anxiety stemming from perceived low status regarding financial skills 42. When this gender threat is alleviated (e.g., women advising women, men advising men), the gender gap in portfolio risk-taking effectively vanishes 42.

Simultaneously, the broader market actively discounts female financial expertise. An extensive analysis of over 7 million comments on the financial platform Seeking Alpha found that articles authored by women received 40% less engagement, lower trust, and faced significantly higher levels of user disagreement than male-authored articles, despite researchers finding absolutely zero gender differences in stock forecasting accuracy 43. This indicates a pervasive, systemic distrust of female financial acumen, further isolating women from peer-based financial integration and independent stock analysis 4143.

Macroeconomic Shifts: Inflation Expectations and Market Volatility

Macroeconomic volatility acts as a real-time stress test for consumer financial behavior. The unprecedented inflation levels observed globally between 2022 and 2025 provided a unique laboratory to study how men and women process macroeconomic shifts differently, revealing disparities in both expectation formation and behavioral adjustment 4844.

The Gender Gap in Inflation Expectations

A well-established phenomenon in consumer surveys across numerous geographies is that women systematically report higher inflation expectations and perceive current inflation to be higher than men do 454647. Traditionally, this gap was attributed almost exclusively to the "grocery shopping" hypothesis - the sociological assumption that women, acting as primary household purchasers, are disproportionately exposed to highly volatile food prices, which biases their overall macroeconomic inflation predictions through a heuristic of availability 4547.

However, recent empirical analysis utilizing Bayesian learning frameworks has fundamentally updated this understanding 47. Reiche (2024) demonstrated that frequent grocery shopping only increases inflation expectations for individuals who possess a "low confidence" sample 47. In a Bayesian framework, low financial confidence equates to a "flat prior" (a higher prior variance). When an individual with a flat prior encounters a volatile, high-frequency price signal (like an increasingly expensive weekly grocery bill), they adjust their overall macroeconomic expectations much more aggressively than someone with a strong, confident prior 47. Because women systematically report lower financial confidence than men, the local price signals they receive at the consumer level are drastically amplified. When researchers control strictly for financial confidence and remove extreme outliers, the gender gap in inflation expectations completely closes, proving the disparity is cognitive and confidence-based rather than purely experiential 47.

Behavioral Responses to Inflation and Crisis

Inflation does not merely skew economic expectations; it radically alters consumer behavior and mental health. During times of heightened inflation, research indicates that men and women pivot their behaviors differently. While male retail investors often look to change their capital investment strategies - such as proactively reallocating portfolios from stocks and bonds to cash to mitigate market downturns - women tend to focus on adjusting immediate household cash flow 848. Surveys tracking the 2022 - 2023 inflation surge reveal that women cut costs across personal products, delay necessary healthcare, and cancel subscription services at rates 20% higher than their male counterparts of the same age and education level 48.

Furthermore, the cumulative burden of inflation-related hardships directly impacts psychological distress levels. Interestingly, while women report higher baseline anxiety regarding economic impacts, exposure to severe, compounded inflation hardships (defined as experiencing five or more concurrent hardships, such as working multiple jobs while delaying medical care) is more strongly associated with acute distress among men, highlighting complex, gendered psychological responses to perceived financial failure and breadwinner pressures 4844.

Retail Trading Apps and the Democratization of Investing

Despite systemic headwinds, the rapid proliferation of retail trading applications and digital wealth managers (Fintech) has fostered a democratization of financial access that is currently accelerating the closure of the gender investment gap 948. By removing the human advisor from the equation, Fintech platforms and algorithmic portfolio generators neutralize statistical discrimination and the psychological "gender threat," providing a sterile, objective environment where women can engage with capital markets without facing unconscious bias 4248.

Surging Engagement and Generational Shifts

Recent data points to an aggressive paradigm shift in female market participation. A comprehensive 2024 study by Fidelity Investments revealed that 71% of women now own investments in the stock market, representing an almost 20% increase compared to 2023 949. While younger generations lead the charge - with 77% of Gen Z women currently holding stock market investments - the most striking year-over-year growth occurred among older cohorts 9. Gen X and Boomer women increased their active market participation by 18% and 23%, respectively, signaling a broadening of investment involvement that transcends age barriers 949.

Similarly, data from the UK-based digital wealth manager Nutmeg illustrates a profound evolution. Female representation on their platform grew from just 24% in 2013 to 41% by 2025 48. More importantly, the actual risk profiles of these female digital investors have evolved dramatically. As of 2025, 89% of female Nutmeg clients actively select medium-to-high risk managed portfolios, achieving near-parity with the 92% rate of male clients 48. Furthermore, 58% of millennial women plan to actively increase their investment risk in the coming year, compared to only 36% of men in the same demographic, shattering the illusion of perpetual female risk aversion 48.

Behavioral Advantages in Portfolio Management

When women do overcome structural barriers and allocate capital to equities, their unique behavioral tendencies frequently yield superior financial outcomes 77. Longitudinal studies, including extensive data from Warwick Business School and the Wells Fargo Investment Institute, consistently demonstrate that female investment portfolios outperform male portfolios by 1.2% to 1.8% annually on a risk-adjusted basis 77.

This outperformance is entirely behavioral. Female investors trade far less frequently, rarely attempting to time the market, thereby incurring significantly fewer transaction costs and tax drags 7726. They are less susceptible to the overconfidence bias that plagues male retail traders, maintain strict discipline during market downturns rather than panic-selling, and allocate capital toward highly diversified, steady-compounding assets like low-cost index funds rather than highly speculative direct stocks or volatile cryptoassets 71626. Therefore, while the traditional finance apparatus historically labeled women as "risk-averse" in a pejorative sense, a vastly more accurate descriptor is that female investors are highly "risk-aware," disciplined, and strategically oriented 7.

Cross-Cultural Contexts: Beyond the WEIRD Demographics

The vast majority of classical behavioral finance literature relies heavily on Western, Educated, Industrialized, Rich, and Democratic (WEIRD) datasets. To determine if gender differences in risk tolerance are biologically innate or socially constructed, modern economics turns to cross-cultural evaluations and emerging market data 631.

Global South and Indigenous Studies

Studies examining children's risk preferences in non-Western settings provide critical insights. In Namibian foraging societies (the Hai||om) and rural agropastoralists (the Ovambo), researchers found that while both groups are generally risk-averse, boys across both distinct cultures exhibited higher risk-taking tendencies than girls, particularly when observed by peers 31. This suggests some evolutionary or universal baseline for male, peer-driven risk-seeking in early childhood 31.

However, studies in China provide a compelling and total counter-narrative regarding the immense power of socialization. When comparing Han children (raised in a traditional patriarchal society) with Mosuo children (raised in a matrilineal society where women primarily control economic decisions, inherit wealth, and hold household authority), researchers observed a complete reversal of the standard dynamic 31. Among the Mosuo, young boys were actually more risk-averse than girls 31. This unique behavioral inversion only normalized to the global standard (boys becoming more risk-prone) when Mosuo children integrated into regional, patriarchal school systems alongside their Han peers 31. This provides profound evidence that economic risk tolerance is highly malleable and heavily programmed by local cultural norms regarding gendered power and wealth control 3150.

Emerging Markets and Asymmetrical Conduct

In emerging markets, female financial integration is rapidly accelerating, though not without unique challenges. In India, the Association of Mutual Funds (AMFI) reported that the share of industry assets owned directly by female investors surged from 15% in 2017 to nearly 21% by the end of 2023 49. This growth in a rapidly developing economy mirrors the democratization trends seen in the West and highlights how expanding digital access circumvents traditional cultural barriers that historically kept women entirely out of the financial system 49.

However, emerging market structures also reveal unique gendered behaviors regarding financial misconduct. An experimental study analyzing the mobile money (Fintech) market in Ghana tested vendors for financial misconduct and price transparency 51. The findings challenged traditional theories of discrimination, revealing that female vendors were actually more likely to engage in financial misconduct (cheating customers) when interacting with customers of their own gender, demonstrating "within-group" discrimination 51. When tested, these female vendors did not display higher risk tolerance than males; rather, the misconduct was driven by localized market concentration effects and differing beliefs about the costs of misconduct, proving that as women enter novel financial markets, their behaviors adapt rapidly to local incentive structures 51. Similarly, empirical data from Chinese Stock Connect structures confirms that as urbanization and market access expand, the decision-making autonomy of women regarding portfolio allocation and regulatory arbitrage evolves, progressively neutralizing traditional gender roles in emerging economies 4352.

Conclusion

The extensive empirical evidence synthesized in this report definitively refutes the archaic paradigm that women are biologically, universally, or immutably "risk-averse." The observed gender gaps in consumer financial behaviors are not the result of inherent psychological timidity; rather, they are the highly complex output of severe systemic constraints, discriminatory institutional practices, and intense, lifelong socialization.

Women exhibit systematically lower risk capacity due to severe intersectional wage penalties, a lack of baseline wealth, and career interruptions that structurally prohibit high-variance investing 3845. Women exhibit higher risk perception because they operate in a financial system characterized by a profound lack of trustworthy advice, where advisors actively engage in statistical discrimination by offering expensive, suboptimal products based on flawed heuristics regarding female financial literacy 3435.

However, the data clearly indicates that when these structural barriers are removed - as seen in the anonymity of retail trading apps, the shifting demographics of digital wealth management, and the evolution of cross-cultural market access - the revealed risk portfolios of women rapidly align with those of men 748. Furthermore, their highly disciplined, low-frequency trading strategies consistently yield superior long-term, risk-adjusted returns, highlighting the profound difference between "risk aversion" and "risk awareness" 748.

As the global financial ecosystem prepares for the unprecedented $84 trillion transfer of wealth to female control, institutions must fundamentally overhaul their engagement models 79. Wealth management firms and macroeconomic policymakers must abandon patronizing assumptions of inherent risk aversion and transition toward objective capacity analysis, bias-free algorithmic advising, and systemic efforts to close the intersectional wealth gap 753. Recognizing that female investors are highly rational, structurally constrained but increasingly empowered actors will ultimately dictate the future flow, allocation, and success of global capital.