Neural mechanisms of financial decision making and risk

For decades, the foundational paradigm of classical economics rested upon the assumption that human beings function as perfectly rational agents. Under Rational Choice Theory, the Homo economicus consistently maximizes utility, evaluating decisions through a lens of perfect logic, stable preferences, and comprehensive information processing 12. However, empirical observations of real-world financial markets consistently revealed phenomena that defied these mathematical abstractions. From speculative asset bubbles and manic herd behavior to panic selling and individual debt accumulation, human financial behavior frequently deviated from optimal utility maximization 3.

To bridge the gap between theoretical models and observed human behavior, behavioral economics introduced the concept of bounded rationality, demonstrating how cognitive biases, heuristics, and emotional states systematically influence economic choices 235. Yet, while behavioral economics successfully cataloged these deviations, it remained largely descriptive, unable to explain the underlying physical architecture generating these behaviors.

Neuroeconomics emerged at the intersection of neuroscience, psychology, and economics to open the "black box" of human decision-making 364. By leveraging advanced neuroimaging techniques - primarily functional magnetic resonance imaging (fMRI) and electroencephalography (EEG) - researchers began to map the biological mechanisms that drive economic behavior in real time 36. This interdisciplinary field has moved beyond observing psychological biases to identifying the precise neuroanatomical networks that dictate risk assessment, subjective valuation, and temporal discounting. From the physiological drivers of credit card debt to the neural prediction of aggregate stock market trends, brain imaging is fundamentally altering the understanding of financial decisions and risk 85.

Theoretical Evolution of Decision Models

The transition from classical economic theory to neuroeconomics represents a profound shift from abstract prescriptive models to biologically grounded, descriptive computational models of human choice. This evolution has required reconciling the mathematical elegance of classical economics with the biological reality of the human brain.

From Expected Utility to Subjective Value

Traditional Rational Choice Theory posits that individuals evaluate the expected utility of all available options and select the one yielding the highest personal benefit 12. When experimental evidence demonstrated that humans systematically violate these assumptions - displaying phenomena such as loss aversion and present bias - the field adapted by introducing dual-process models 23. Dual-process theories distinguish between a fast, intuitive, emotionally driven system and a slow, deliberative, analytical system 2.

Neuroeconomics provides the physiological foundation for these dual-process models by identifying the specific brain structures that instantiate them 10. It demonstrates that rationality is not a default state but a dynamic, context-dependent process resulting from the continuous interaction of distinct neural networks 2. Instead of calculating a static "expected utility," neuroeconomic models suggest the brain computes a dynamic "subjective value." This subjective value is a composite metric, continuously updated by the brain, that integrates reward magnitude, probability, temporal delay, and the individual's current affective state 16.

Recent theoretical advancements in neuroeconomics have introduced models such as Expected Subjective Value Theory (ESVT) and divisive normalization 7. Divisive normalization, a computational principle observed across sensory systems, has been applied to value coding to explain how the brain scales value representations dynamically based on the surrounding choice context 7. Because neurons have a bounded maximum firing rate, the brain must normalize the subjective value of a financial option relative to the other options currently available, leading to context-dependent choices that often appear irrational under classical absolute-valuation models 7.

Integration of Reinforcement Learning

Neuroeconomics has also heavily integrated machine learning and algorithmic science, specifically reinforcement learning architectures 89. Computational models of decision-making reveal an impressive correspondence between the firing of dopamine neurons in the mammalian midbrain and the reward prediction errors of reinforcement learning algorithms 10. These algorithms express the difference between an actual received reward and the predicted mean reward 10.

Recent developments in distributional reinforcement learning suggest that the mesolimbic dopamine system does not merely update a representation of mean value; it encodes the entire probability distribution of potential rewards 10. This biological capacity to learn full reward distributions helps explain how humans navigate complex, probabilistic financial environments where both the mean return and the variance of an asset must be evaluated simultaneously.

| Feature | Rational Choice Theory | Behavioral Economics | Neuroeconomics |

|---|---|---|---|

| Core Assumption | Utility maximization based on perfect logic, stable preferences, and complete information. | Bounded rationality; humans rely on heuristics and suffer from predictable cognitive biases. | Decisions arise from the biological integration of cognitive, affective, and valuation neural circuits. |

| Primary Methodology | Mathematical modeling and axiomatic deduction. | Psychological experiments, surveys, and observational economic data. | Functional neuroimaging (fMRI, EEG), biometrics, and computational modeling. |

| View of Emotion | Irrelevant or treated as external noise to be ignored. | A significant driver of irrational decision-making and systemic bias. | A central, quantifiable input essential to the brain's valuation and decision process. |

| Decision Mechanism | Unitary mathematical process calculating absolute expected utility. | Dual-process interaction (System 1 intuition vs. System 2 deliberation). | Interacting neural networks tracking subjective value via divisive normalization and prediction errors. |

The Neural Architecture of Valuation and Risk

Neuroimaging studies have consistently identified a specific network of brain regions that govern financial choices, forming what researchers term a neural risk matrix 11. The continuous, dynamic interplay between these localized regions dictates an individual's financial risk tolerance, reward anticipation, and response to uncertainty.

Reward Processing and the Striatum

The striatum, and specifically its ventral region encompassing the nucleus accumbens (NAcc), is heavily implicated in the processing of reward, positive arousal, and value representation. Activity in the NAcc correlates robustly with the anticipation of financial gain 312. When evaluating financial options, quantitative meta-analyses of fMRI experiments reveal that assets with high expected values and positive statistical skewness (the potential for outsized positive returns, akin to lottery tickets) have the highest probability of increasing ventral striatal activity 12.

This dopaminergic reward center is the identical neural pathway exploited by addictive substances such as cocaine and amphetamines 13. In financial contexts, elevated NAcc activity shifts preferences toward riskier assets, driving speculative investments, impulsive trading, and a prioritization of immediate gratification 311.

Threat Detection and the Amygdala

While the striatum drives approach behaviors and reward-seeking, the amygdala acts as the brain's primary threat detection and fear-processing center. In financial decision-making, the amygdala processes uncertainty, loss anticipation, and ambiguity. Neuroeconomic studies demonstrate that ambiguity aversion - the strong preference for known risks over unknown risks - triggers significantly stronger amygdala activation than standard, quantifiable risk assessment 14.

During market crashes or periods of high portfolio volatility, hyperactivation of the amygdala is associated with the sudden onset of loss aversion. This subcortical fear response can override executive planning, triggering panic selling as investors instinctively act to eliminate the source of the perceived threat, prioritizing immediate emotional relief over long-term strategic holding 320.

Arousal, Variance, and the Anterior Insula

The anterior insula is critical for interoception - the perception of internal bodily states - and is closely linked to negative arousal, anxiety, and the processing of aversive stimuli. Meta-analyses indicate that exposure to financial options with high variance (high volatility) reliably increases anterior insula activity 12. The insula acts as a biological warning system for uncertainty and potential loss.

Furthermore, the insula is activated by perceived social and financial unfairness. For instance, when participants receive severely unbalanced, low offers in the Ultimatum Game, the anterior insula exhibits pronounced activation, triggering a response akin to physical or moral disgust 14. In the specific context of financial risk, increased anterior insula activity reliably predicts a subsequent decrease in financial risk-taking, functioning as a physiological brake against potential capital losses 1112.

Executive Control and the Prefrontal Cortex

The prefrontal cortex (PFC), particularly the dorsolateral prefrontal cortex (dlPFC) and the ventromedial prefrontal cortex (vmPFC), provides top-down cognitive control over the deeper, affective subcortical regions. The PFC is responsible for rational analysis, long-term strategic planning, and the final computation of subjective value 36.

The vmPFC acts as the brain's ultimate integrative hub during economic choice. It weighs the anticipatory reward signals originating from the striatum against the risk and aversion signals generated by the insula and amygdala to compute a final, unified subjective value for a given financial option 106. Dysfunction, immaturity, or reduced functional connectivity in the PFC is frequently linked to impulsive trading, an inability to delay financial gratification, and heightened susceptibility to behavioral biases 33.

Consumer Spending and the Medium of Exchange

The practical application of neuroeconomics has profoundly altered the understanding of everyday consumer spending, particularly regarding the psychological and physiological impact of different payment methods. Historically, behavioral economists theorized that credit cards facilitated overspending primarily by "anesthetizing the pain of paying" 815. Because credit cards decouple the acquisition of goods from the immediate, tangible depletion of physical resources, they were thought to release the psychological brakes that normally hold consumer expenditure in check 8.

Recent fMRI research has refined this hypothesis, revealing a more active, stimulatory mechanism underlying debt accumulation. When consumers make purchases using credit cards within simulated fMRI shopping tasks, neural scans show strong, specific activation in the striatum 813. This suggests that credit cards do not merely reduce the pain of payment; they actively "step on the gas" by sensitizing the brain's reward networks 813.

The physical act of swiping a card provides immediate pleasure associated with product acquisition, while the financial cost is deferred to a bill realized weeks later 13. This temporal decoupling creates an anticipatory reward loop highly similar to conditioning processes seen in addiction, increasing motivation to spend and leading individuals to pay significantly higher prices for the same items compared to cash transactions 816.

Conversely, purchasing with physical cash elicits a distinctly different neural signature. Cash transactions are associated with significantly greater activation in the right parietal cortex and the right insula 17. The parietal cortex processes the perceived utility of motor behavior, while the insula processes emotional involvement and negative affective valence 17. This heightened neural activity indicates that the physical friction of parting with cash enhances the salience of the transaction. The brain perceives the loss of physical currency as a highly salient, aversive stimulus, effectively triggering the "pain of paying" and acting as a robust self-regulating tool against impulsive consumption 17.

Investor Behavior in Market Downturns

Neuroeconomics provides a biological lens through which to examine broad market dynamics and the behavior of distinct investor cohorts. Financial markets are fundamentally driven by aggregate human psychology, and understanding the neural correlates of retail investors clarifies why markets frequently deviate from efficient pricing models.

Retail Investor Psychology and Vulnerabilities

Recent demographic shifts and the proliferation of accessible fintech applications have introduced millions of new retail investors to the equity markets. In 2024, retail investors accounted for more than 45% of cash market turnover globally, bringing with them unique behavioral vulnerabilities 18. Survey data from the FINRA Investor Education Foundation indicates that younger retail investors (under 35) are significantly more likely to engage in high-risk behaviors compared to older cohorts, including the trading of complex options (43% versus 10%) and utilizing margin debt (22% versus 4%) 19.

These retail behaviors are frequently driven by social media influence, viral trends, and the "Fear Of Missing Out" (FOMO) regarding meme stocks and unproven assets 1819. From a neuroeconomic perspective, FOMO is mediated by intense striatal reward anticipation conflicting with social conformity pressures, a combination that can easily override the prefrontal cortex's more deliberate risk assessment systems 1018. The result is a tendency toward herd mentality and an overreliance on fast, System 1 cognitive heuristics 2.

Emotional Instability and Panic Selling

Market downturns ruthlessly expose the biological limits of rational investing. Panic selling - the impulsive, widespread divestment of assets during a crash - is driven heavily by an individual's inherent personality traits and emotional regulation capacities 2026. A comprehensive 2023 - 2024 empirical study encompassing over 189,000 investors demonstrated a robust, positive correlation between the personality trait of neuroticism and the likelihood of panic selling 2620.

Neuroticism, characterized by emotional instability, anxiety, and heightened reactivity to stress, biologically amplifies loss aversion and regret aversion 2620. In highly neurotic individuals, negative market information likely triggers disproportionate amygdala and anterior insula activation, leading to overwhelming negative physiological arousal. The 2024 study further revealed that overconfident investors were more prone to panic selling during crises, even when controlling for baseline financial literacy 21. This suggests that sudden negative market shocks easily shatter cognitive illusions of control, leaving the overconfident investor at the mercy of subcortical fear circuits, prioritizing immediate emotional relief over long-term strategic holding 2021.

The Disposition Effect and Realization Utility

Individual investors also suffer from the disposition effect - the pervasive tendency to sell assets that have increased in value too early, while holding onto depreciating assets for too long. Traditional economic models struggle to explain this phenomenon, as it runs counter to standard risk-aversion assumptions 22.

Neuroeconomic research has tested the "realization utility" model, which posits that individuals receive a direct, hedonic burst of utility at the exact moment an asset is sold at a gain 22. Using fMRI, researchers observed that selling a stock at a profit triggers a distinct spike in striatal activity at the moment of execution 22. This neural evidence supports the realization utility model, demonstrating that investors act to harvest immediate, biologically coded utility bursts, rather than maximizing the long-term mathematical yield of their portfolio 22.

Neural Profiles of Professional Traders

Sustained exposure to the extreme pressures of financial markets can structurally and functionally alter an individual's neural response to risk. Neuroimaging of professional stock traders engaging in simulated financial decision-making reveals a unique neural profile compared to untrained retail investors 23.

When faced with high-stakes, high-risk financial decisions, professional traders exhibit significantly heightened activation in both the ventromedial prefrontal cortex (vmPFC) and the nucleus accumbens, alongside notably reduced activation in the amygdala 23. This specific neural configuration suggests that professional experience heavily modulates brain pathways to prioritize potential reward and objective value calculations, while systematically suppressing the panic and fear responses typical of the amygdala 23.

Conversely, when navigating lower-risk scenarios, professional traders show increased activity in the dorsolateral prefrontal cortex (dlPFC) 23. This indicates a shift toward highly deliberate, rule-based cognitive control when profit margins are narrow and require precise, emotionless calculation 23. The ability to decouple risk from fear - relying on the vmPFC to integrate risk objectively rather than emotionally - separates the neural architecture of the professional from that of the amateur.

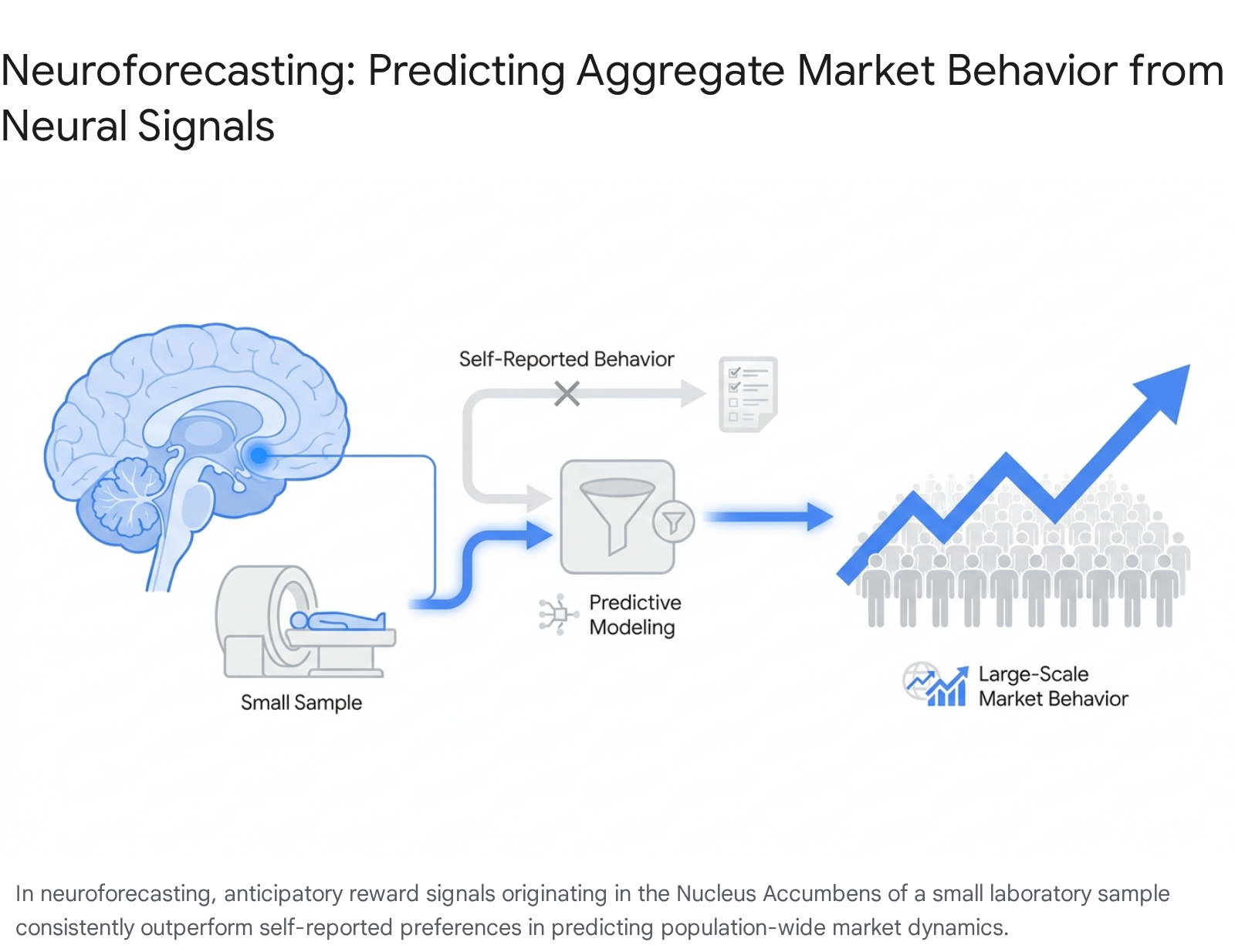

Neuroforecasting Aggregate Market Dynamics

Perhaps the most revolutionary application of neuroeconomics is the emerging sub-field of neuroforecasting. Historically, economic models relied on historical data sets, sentiment polling, and stated behavioral preferences to predict market trends. However, stated preferences are notoriously poor predictors of actual future behavior; what individuals report they value frequently diverges from their actual purchasing or investment choices 531.

Neuroforecasting bypasses self-reported behavioral data entirely. Instead, it utilizes the functional brain activity of a small sample of individuals to predict out-of-sample, population-level aggregate behavior 3124.

The foundational premise is that certain deep, affective neural processes - such as basic reward anticipation computed in the ventral striatum - are more universally shared across human populations than the highly idiosyncratic, socially mediated conscious choices recorded in behavioral surveys 25.

Predicting Stock Market Performance

In a landmark 2024 neuroimaging experiment published in the Proceedings of the National Academy of Sciences (PNAS), researchers tested whether the brain activity of 34 professional investors could forecast long-term stock market performance 526. The expert investors were asked to evaluate complex, real-world investment cases while undergoing fMRI scanning.

The behavioral results confirmed traditional economic skepticism: the investors' conscious, stated predictions regarding future stock performance were highly inaccurate, failing to predict market realities above chance 526. However, neuroimaging data revealed a hidden predictive signal. Activity in the nucleus accumbens (NAcc) while evaluating the stocks successfully predicted which assets would overperform the broader market one year later 526.

This predictive capability remains robust even when controlling for traditional stock metrics 526. In related studies, average brain activity in the anterior insula of a small sample has been shown to forecast stock price inflections, leveraging the insula's sensitivity to variance and impending risk 527.

The success of neuroforecasting extends well beyond the financial sector. Similar neuroimaging methodologies have proven that NAcc activity in a small group of 20 to 30 unrepresentative subjects can reliably forecast the funding success of crowdfunding campaigns, the virality of online videos, and national music sales 3127. The profound implication is that while conscious decision-making is heavily clouded by cognitive biases, overthinking, and social desirability effects, the raw, anticipatory reward signals generated by the brain's subcortical structures offer a relatively unfiltered, highly generalizable predictor of mass human economic behavior 3125.

Cross-Cultural Neuroeconomics

As the discipline matures, researchers are increasingly acknowledging that the neural mechanisms of financial decision-making do not operate in a biological vacuum; they are profoundly modulated by socio-cultural environments. Classical economics traditionally operated under the assumption that the basic cognitive and logical processes underlying economic choice were universal and invariant across all human populations 2829. However, cross-cultural neuroeconomics has demonstrated that cultural norms physically shape how the brain perceives and processes financial risk.

A prominent framework in this area is the "cushion hypothesis." This theory posits that individuals originating from collectivist societies (such as many East Asian cultures) exhibit structurally lower financial risk aversion compared to individuals from highly individualistic societies (such as the United States or Western Europe) 28. The hypothesis suggests that collectivist cultures provide a robust, tightly knit social support network - a financial and emotional "cushion" - that mitigates the catastrophic, isolating consequences of severe financial loss, thereby fundamentally altering the biological perception of risk 28.

Neuroimaging and electroencephalography (EEG) support this hypothesis by revealing distinct temporal processing differences during risky financial tasks across cultures. In comparative EEG studies between East Asians and European Americans engaged in gambling tasks designed to test gain-maximizing versus loss-minimizing strategies, European Americans behaviorally exhibited significantly higher loss aversion 28.

At the neural level, Event-Related Potentials (ERPs) demonstrated stark contrasts during the post-decisional evaluation of financial outcomes. East Asian participants displayed strong modulation of the P2 component - an ERP wave associated with spontaneous emotional arousal - specifically in response to financial gains 28. In contrast, European Americans showed strong modulation of the P3 component - a wave associated with effortful, conscious attentional allocation - specifically in response to financial losses 28. These findings indicate that deep-seated cultural backgrounds dictate whether the brain automatically prioritizes the emotional reward of an economic gain or the cognitive, self-reliant mitigation of an economic loss 28. This concept of "conation" - the neurocognitive capacity for goal-directed action amid contextual complexity - underscores the social embeddedness of economic behavior 2.

Methodological Advancements in Brain Imaging

The rapid evolution of neuroeconomic theory is inextricably linked to continuous advancements in fMRI and computational methodology. In its early years, neuroeconomics relied heavily on univariate General Linear Models (GLM). This approach mapped decision-making processes by looking for isolated regions of the brain that exhibited localized spikes in blood-oxygen-level-dependent (BOLD) signals during a specific task 30. Today, the field is undergoing a paradigm shift toward more sophisticated, data-dense methodologies that treat the brain as a highly complex, integrated network.

Multivariate Pattern Analysis (MVPA)

Introduced as an evolutionary alternative to univariate analysis, Multivariate Pattern Analysis (MVPA) applies machine learning algorithms to fMRI data to analyze distributed patterns of neural activity across thousands of voxels simultaneously 3031. Rather than simply asking where a physiological function occurs, MVPA allows researchers to decode what specific information or subjective value is being represented within a cortical field 30.

By training decoder models to recognize specific mental states, researchers can generate highly reliable "neural signatures" that distinguish between subtle gradations in cognitive load, intertemporal discounting preferences, or subjective valuations during financial decisions 3032. This provides a vastly more nuanced understanding of economic behavior than earlier global-activation models 3033.

Precision Functional Mapping (PFM)

Historically, fMRI studies averaged data across large groups of participants to find common neural denominators. While useful for establishing baseline neuroanatomy, this practice severely obscured vital individual idiosyncrasies in brain network topography 34. The emerging movement of Precision Functional Mapping (PFM) addresses this limitation by collecting massive amounts of longitudinal data - often accumulating hours of scanning over several days - on single individuals 343544.

PFM has definitively revealed that functional brain networks are highly individualized, much like fingerprints 3435. For example, PFM studies have shown that the lateral prefrontal cortex, a region critical for financial executive control, contains finely interwoven, highly distinct brain networks whose exact anatomical positioning varies significantly from person to person 3435. Recognizing these unique spatial network configurations is crucial for understanding individual biological variations in financial risk tolerance and cognitive flexibility.

Artificial Intelligence and Brain Foundation Models

The integration of artificial intelligence is solving the severe "curse of dimensionality" inherent in fMRI data, which requires the processing of millions of spatiotemporal features per scan 36. Advanced machine learning models, including neural networks, transformers, and self-attention mechanisms, are now being utilized to construct overarching foundational models of the human brain 37.

These sophisticated models capture both the broad regularity and the minute variability of brain activity across time and populations, allowing for highly accurate predictions of brain states during complex financial tasks 3637. By overcoming the limitations of standard linear regression analysis, neural networks can extract non-linear relationships between physiological arousal, market prediction, and economic choice, driving the next generation of algorithmic trading and behavioral modeling 3747.

The Reproducibility Crisis and the Shift to Large-Scale Data

Despite its rapid growth and theoretical successes, neuroeconomics - like the broader disciplines of psychology and neuroscience - has recently faced a severe reproducibility crisis. In recent years, independent research groups have frequently failed to replicate the findings of seminal fMRI experiments, casting doubt on foundational assumptions regarding brain-behavior correlations 383940.

The Reverse Inference Fallacy

A major, systematic contributor to this crisis is the "reverse inference fallacy" 4142. This logical error occurs when researchers observe activation in a specific brain region during a task and incorrectly infer the presence of a specific cognitive or emotional state based on prior, unrelated literature, rather than direct behavioral testing 41.

For instance, inferring that an investor is experiencing financial anxiety simply because their anterior insula is active ignores the physiological reality that the insula is a highly multi-functional region involved in everything from physical pain and nausea to general somatic arousal 41. This epidemic of backward reasoning, combined with the extreme methodological flexibility of fMRI processing pipelines - where independent analysis teams utilizing the exact same raw dataset can reach entirely different conclusions based on arbitrary software and preprocessing choices - has historically led to unacceptably high rates of false positives 3841.

The severity of these methodological flaws was dramatically highlighted in 2025 when a highly publicized, paradigm-shifting 2022 Science paper on a novel fMRI method (DIANA), which purported to directly image neuronal activity at the millisecond scale, was retracted 43. Independent laboratories proved that the observed "neuronal signals" were merely systemic electrical artifacts resulting from a 10-microsecond data-collection timing error, demonstrating the extreme fragility of highly complex neuroimaging methodologies 43.

The UK Biobank and Brain-Wide Association Studies

To systematically combat the reproducibility crisis, the field of neuroeconomics is abandoning traditional, small-sample laboratory studies (which historically relied on groups of n=20 to 30 university students) that lack adequate statistical power 40. The vanguard of this methodological shift is the UK Biobank, a massive prospective cohort study that reached a historic scientific milestone in July 2025 by completing 100,000 whole-body and brain scans of the general population 4445.

By providing researchers worldwide with open access to an unprecedented volume of standardized, high-quality multimodal imaging data - linked directly to participant genetic information, continuous cognitive assessments, real-world lifestyle questionnaires, and longitudinal electronic health records - the UK Biobank effectively eliminates the sample-size limitations that severely constrained early neuroeconomic research 464748.

Recent theoretical derivations utilizing datasets of this immense magnitude have finally clarified the exact statistical tradeoff between sample size and individual scan time required for reliable Brain-Wide Association Studies (BWAS) 49. The integration of these massive, population-representative datasets with advanced MVPA and machine learning ensures that future neuroeconomic models will be highly robust. This scale of data allows for powerful causal inferences regarding how individual neuroanatomical structures and functional connectivity networks influence a lifetime of financial accumulation, economic risk-taking, and cognitive decline 4649.

Conclusion

Neuroeconomics has fundamentally transformed the study of financial decision-making, providing a rigorous, physiological foundation for behaviors previously dismissed as irrational anomalies. By discarding the outdated assumption of the perfectly logical Homo economicus, the field has provided a biologically accurate map of how humans actually evaluate risk, process reward, and make choices in the face of profound uncertainty.

The precise identification of the neural risk matrix - anchored by the continuous interaction of the striatum, insula, amygdala, and prefrontal cortex - explains why consumers spend more aggressively when shielded by the psychological abstraction of credit cards, why highly neurotic investors succumb to panic during volatile market downturns, and why professional traders must develop distinct, highly controlled neurological profiles to manage financial stress.

Furthermore, the advent of neuroforecasting has proven that deep, subcortical affective signals can predict global market behavior with significantly greater accuracy than conscious, self-reported preferences. As the discipline actively overcomes its historical reproducibility challenges through the adoption of Multivariate Pattern Analysis, individualized Precision Functional Mapping, and the utilization of massive data repositories like the UK Biobank, neuroeconomics is poised to move far beyond academic observation. In the near future, these biological insights will drive the design of more effective financial regulatory policies, highly personalized wealth management interfaces, and targeted interventions designed to protect vulnerable populations from systemic financial risk.