Disruptive innovation theory and distributed energy markets

The application of disruptive innovation theory to global energy markets provides a vital and comprehensive framework for understanding the structural friction between distributed energy resources (DERs) and the traditional centralized utility model. For over a century, electric utilities have operated as natural monopolies, relying on massive economies of scale, heavy capital infrastructure, and centralized generation to deliver power across a unidirectional transmission and distribution grid 12. Under standard cost-of-service regulatory paradigms, these utilities earn a guaranteed, state-authorized rate of return on their capital infrastructure investments, recovering those extensive fixed costs through volumetric, per-kilowatt-hour (kWh) charges levied on captive residential and commercial ratepayers 234.

However, the rapid commercialization and subsequent cost deflation of distributed energy resources - primarily rooftop solar photovoltaics (PV), behind-the-meter battery energy storage systems (BESS), and smart home energy management software - have introduced a fundamentally different technological and economic paradigm. Because these technologies sit at the grid edge and allow consumers to generate, store, and manage their own electricity, they directly attack the volumetric revenue model of the incumbent electric utilities 566. The ongoing collision between these decentralized assets and the legacy regulatory framework is reshaping grid architecture, utility business models, and electricity rate design on a global scale, presenting one of the most significant industrial transformations of the twenty-first century.

The Theory of Utility Disruption

To understand the mechanics of this market shift, it is necessary to frame it within the context of disruptive innovation. First popularized in the broader business context, disruptive innovation describes a process whereby a smaller, initially inferior or niche technology enters a market, steadily improves, and eventually displaces established incumbent systems. In the context of electricity markets, distributed solar PV and battery storage were initially viewed as expensive, niche applications reserved for off-grid counter-cultures or highly subsidized environmental pilot programs 78.

However, as manufacturing scaled and technological efficiencies improved, the levelized cost of energy (LCOE) for distributed solar began to achieve grid parity in numerous markets 89. The disruptive nature of these technologies does not merely stem from their ability to generate clean electrons; it stems from their unique capacity to decouple consumer electricity demand from utility revenue generation 310. Traditional utilities make money by deploying massive amounts of capital into large-scale infrastructure (power plants, high-voltage transmission lines, substations) and then slowly recovering those costs over decades through the volumetric consumption of their customers 24. When a consumer installs a solar panel, they reduce their volumetric consumption from the grid, striking at the heart of the utility cost-recovery mechanism while simultaneously still relying on the grid for backup power and evening load requirements 611.

The Utility Death Spiral Hypothesis

At the core of the disruptive innovation narrative in energy markets is the concept of the "utility death spiral," a term that gained immense traction in utility planning and regulatory circles throughout the 2010s 512. The hypothesis outlines a severe, self-reinforcing economic feedback loop that theoretically threatens the absolute financial viability of traditional investor-owned utilities (IOUs) and public power entities 510.

The mechanics of the spiral are straightforward. As early adopters install rooftop solar panels, their volumetric grid electricity consumption drops. Because the utility's high fixed costs for maintaining distribution infrastructure, managing vegetation, and servicing debt remain entirely unchanged, the utility is forced to spread these identical fixed costs over a progressively smaller volume of total electricity sales 61012. To maintain their state-authorized revenue requirements, utilities must petition regulatory commissions to increase the per-kWh electricity rate for all remaining consumers 710.

This subsequent rate increase creates an unintended consequence: it shortens the payback period for solar and storage installations, making self-generation economically attractive to an even broader demographic of customers 51012. As this cycle repeats and accelerates, the customer base relying solely on the grid shrinks, rates escalate uncontrollably, and the utility business model theoretically collapses under the weight of stranded assets and unrecoverable capital expenditures 5813.

The Threat of Economic Grid Defection

The ultimate and most extreme endpoint of the utility death spiral is complete grid defection. This represents a scenario where a commercial entity or residential customer severs their physical connection to the macro-distribution network entirely, relying exclusively on a hybridized system of solar PV, deep-cycle battery storage, and perhaps a backup diesel or natural gas generator 714. Historically, grid defection was dismissed by utility planners and economists as a technically challenging, highly uneconomical pursuit limited to remote cabins or islanded communities.

However, continuous and precipitous cost declines in lithium-ion batteries and solar PV have fundamentally altered this calculus. By 2024, empirical academic studies indicated that pure grid defection had become economically advantageous for certain consumer segments in at least five high-rate U.S. states: California, Connecticut, Hawaii, Massachusetts, and New York 714. Furthermore, research evaluating grid defection potential at 18 locations across 13 states found that communities on the margin included Los Angeles, Boston, Concord, and Hartford 7.

The parity point for solar-plus-battery systems acting as a "utility in a box" is increasingly falling within the 30-year planned economic life of central power plants and transmission infrastructure, creating a severe risk of asset stranding 8. High utility base rates, the systematic reduction of net energy metering (NEM) compensation by public utility commissions, and the declining costs of hybrid generation systems create powerful, near-term incentives for commercial and residential defection 714. Emerging distributed business models that offer "grid defection as a service" - where third-party companies finance, install, and operate off-grid systems in exchange for a share of the energy savings - further lower the barrier to entry for consumers who are unwilling or unable to manage complex hybrid power systems themselves 7.

Real-World Friction and Load Displacement

Despite the theoretical soundness of the utility death spiral and the rising economic viability of grid defection, empirical evidence suggests the phenomenon is highly nuanced and far from an inevitable terminal event for the utility sector. Market data indicates that true, physical grid defection remains exceedingly rare 715. Instead, customers primarily engage in load displacement, a strategy where they optimize behind-the-meter generation to offset expensive peak grid pricing while maintaining their grid connection for reliability, backup power, and operational flexibility 1516.

For example, regulatory filings from LUMA Energy in Puerto Rico - a grid characterized by high rates and historic reliability challenges - demonstrate that while industrial usage of the macro-grid has declined due to the adoption of combined heat and power (CHP) and solar-plus-storage, actual physical disconnections remain near zero 15. Out of 43 large industrial customers displacing approximately 34 GWh per month through private generation, fewer than five fully disconnected from the grid 15. This indicates that while the volumetric revenue model is deeply threatened, the fundamental value of the grid as an interconnected network of backup reliability remains intact 115.

Furthermore, the death spiral framework implicitly assumes that utilities and their regulators will remain passive as the disruption unfolds. In reality, the utility industry is aggressively adapting to the threat through rate restructuring, deep infrastructure modernization, and the active co-optation of grid-edge technologies into their own rate bases 121817.

Structural Vulnerabilities of Centralized Architectures

The vulnerability of the traditional utility model extends significantly beyond the pure economics of volumetric revenue loss; it is deeply rooted in the physical architecture of the grid and the evolving physics of power flows.

Centralized Systems and Single Points of Failure

The legacy power grid was engineered over a century ago for unidirectional power flow from centralized, highly dispatchable baseload generation facilities (coal, nuclear, large hydro) to passive residential and commercial endpoints 116. While this hub-and-spoke model successfully exploited economies of scale to electrify nations during the twentieth century, it inherently possesses a "single point of failure" (SPOF) architecture 161819. Disruptions at a central generation plant, a high-voltage transmission corridor, or a primary substation - whether caused by extreme weather, equipment fatigue, or cyberattack - can cascade into catastrophic, widespread blackouts 1619.

Conversely, decentralized grid architectures, empowered by disruptive DERs, rely on distributed nodes of generation and storage. When a decentralized network experiences a local macro-grid failure, smart inverters and microgrid controllers allow specific segments, neighborhoods, or critical facilities to physically isolate themselves ("island") and maintain critical power delivery 162021. As climate change increases the frequency and severity of extreme weather events - from wildfires in California to winter storms in Texas - commercial and residential consumers are increasingly prioritizing physical resilience 2223. This search for autonomous reliability, rather than pure economic cost avoidance, has become a primary, non-price driver for the deployment of DERs at the grid edge, further eroding the traditional utility's monopoly on reliability 152022.

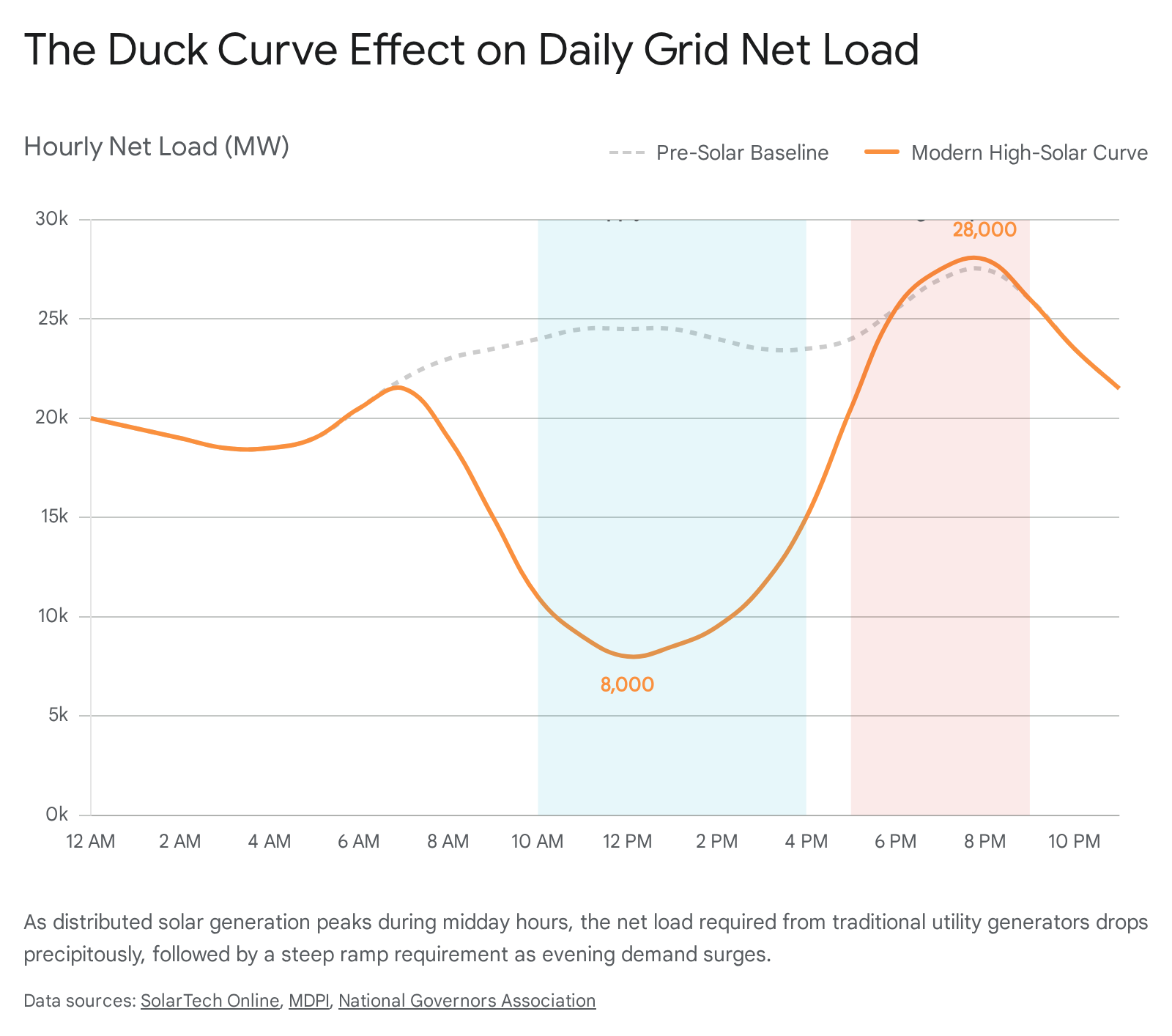

The Duck Curve and Grid Load Management

The proliferation of grid-tied, unmanaged distributed solar generation has introduced severe operational strains for centralized utilities and independent system operators, most notably illustrated by the phenomenon known as the "duck curve" 242526.

Because solar PV generation peaks during the midday hours, it radically depresses the net load (total demand minus solar and wind generation) required from traditional utility generators. However, as the sun sets and solar output predictably drops to zero, residential demand spikes concurrently due to evening activities (lighting, cooking, cooling, and increasingly, electric vehicle charging) 52425.

This dynamic forces grid operators to manage an incredibly steep evening ramp rate, requiring dispatchable thermal plants (typically natural gas) to rapidly spin up to replace the lost solar capacity within a matter of two to three hours 2526. To manage this severe imbalance, utilities are forced to retain and maintain expensive, fast-ramping fossil fuel "peaker" plants that sit idle for most of the day, escalating system-wide capacity costs and undermining the environmental benefits of the solar generation 2426. In high-solar-penetration markets like California and South Australia, the duck curve frequently results in negative wholesale electricity prices during midday oversupply, necessitating the economic curtailment (shutting down) of clean energy assets because the grid cannot physically absorb the power 242728.

Emergence of the Prosumer Paradigm

The convergence of digitalization, localized distributed generation, and advanced battery energy storage has facilitated the transition of the traditional ratepayer into a "prosumer" - an active entity that both produces and consumes electricity 2930. The prosumer business model fundamentally alters the transactional nature of retail energy markets. Rather than acting as passive endpoints at the end of a distribution feeder, prosumers engage in self-consumption to avoid high retail utility tariffs, export surplus generation back to the grid for financial compensation, and provide flexibility services 130.

In advanced market designs and pilot programs, peer-to-peer (P2P) energy trading allows prosumers to sell excess electricity directly to their neighbors via digital platforms, effectively bypassing the traditional utility as the mandatory middleman 2131. This disintermediation represents a profound attack on the traditional utility's historic monopoly over retail electricity supply. Utilities must now contend with an environment where their former customers act as competitors, supplying low-marginal-cost energy back into the distribution network during the day and drawing heavily from it during the evening peak.

The structural and economic differences between the legacy model and the emerging decentralized paradigm are stark, touching every aspect of how electricity is financed, generated, and consumed.

| Design Dimension | Traditional Utility Model | Prosumer Energy Model |

|---|---|---|

| Generation Architecture | Centralized, large-scale utility power plants (coal, nuclear, combined cycle gas) 132. | Distributed, behind-the-meter, customer-sited assets (rooftop PV, micro-turbines) 2122. |

| Revenue Generation | Volumetric electricity sales and guaranteed regulatory returns on infrastructure capital expenditures 24. | Self-consumption savings, grid export compensation (net metering), and localized energy arbitrage 30. |

| Capital Deployment | Slow deployment of massive capital into highly regulated mega-projects (e.g., transmission corridors) 1733. | Rapid, granular capital deployment driven by private households, third-party developers, and commercial entities 34. |

| System Resilience | Reliant on robust but vulnerable central nodes (single points of failure); focus on post-fault reaction 1621. | Decentralized nodes capable of autonomous islanding, prevention, and automated self-healing 162021. |

| Consumer Role | Passive ratepayer generating inelastic, predictable load profiles 1. | Active market participant enabling demand flexibility, capacity support, and two-way power flows 3135. |

Regulatory Adaptation and Rate Restructuring

Faced with the existential economic pressures of the death spiral, the operational headaches of the duck curve, and the proliferation of prosumer models, utilities and public utility commissions (PUCs) are rapidly evolving their regulatory frameworks. The transition necessitates moving away from 20th-century business models that inadvertently penalize utilities for energy efficiency and decentralized generation, toward sophisticated frameworks that reward system optimization, resilience, and equity 3436.

Revenue Decoupling and Performance Incentives

To directly neutralize the financial threat of the death spiral, numerous regulatory jurisdictions have implemented a mechanism known as revenue decoupling. Decoupling severs the strict link between a utility's volumetric energy sales and its authorized profit margin 337. Under this regulatory mechanism, if electricity sales fall due to high rooftop solar adoption, favorable weather, or widespread energy efficiency measures, retail rates are automatically adjusted upward in subsequent periods to ensure the utility recovers its fixed revenue requirement 3. Conversely, if sales exceed projections, customers receive a surcharge refund 3.

While decoupling successfully removes the utility's financial disincentive to support energy efficiency and DERs, it is fundamentally a blunt instrument. It does not solve the underlying issue of cross-subsidization and cost-shifting between wealthy solar adopters and lower-income non-adopters, as the rising decoupled rates fall heavily on those who cannot afford to self-generate 3238.

Time-of-Use Pricing and Demand Flexibility

To specifically combat the operational realities of the duck curve, utilities have widely deployed Time-of-Use (TOU) pricing. Unlike traditional flat volumetric rates, TOU rates charge significantly more for electricity consumed during system peak demand hours 24. As solar penetration pushes the net peak load later into the day, TOU pricing windows have shifted uniformly to the evening, typically capturing the 4:00 PM to 9:00 PM window across various regions 24.

During these critical evening hours, summer peak rates can reach exorbitant levels. For example, in Southern California Edison (SCE) territory, peak rates can reach $0.74 per kWh during summer weekday evenings, while off-peak rates drop to $0.21-$0.25 24. TOU structures weaponize price signals to force prosumers to align their consumption with grid conditions. By making evening grid consumption punitively expensive, TOU rates incentivize consumers to invest in smart home automation and behind-the-meter batteries, essentially transforming autonomous disruptive technologies into grid-responsive assets that actively flatten the duck curve 2425.

The Shift to Income-Graduated Fixed Charges

The most aggressive and controversial counter-attack against the volumetric disruption is the structural redesign of retail electricity rates to heavily feature fixed monthly charges. Utilities argue that because the underlying costs of maintaining the physical distribution grid, upgrading transformers, managing vegetation, and mitigating wildfire risks do not decrease when a customer installs rooftop solar, these non-incremental fixed costs must be stripped out of the volumetric per-kWh rate and charged as a flat, unavoidable baseline fee 61139.

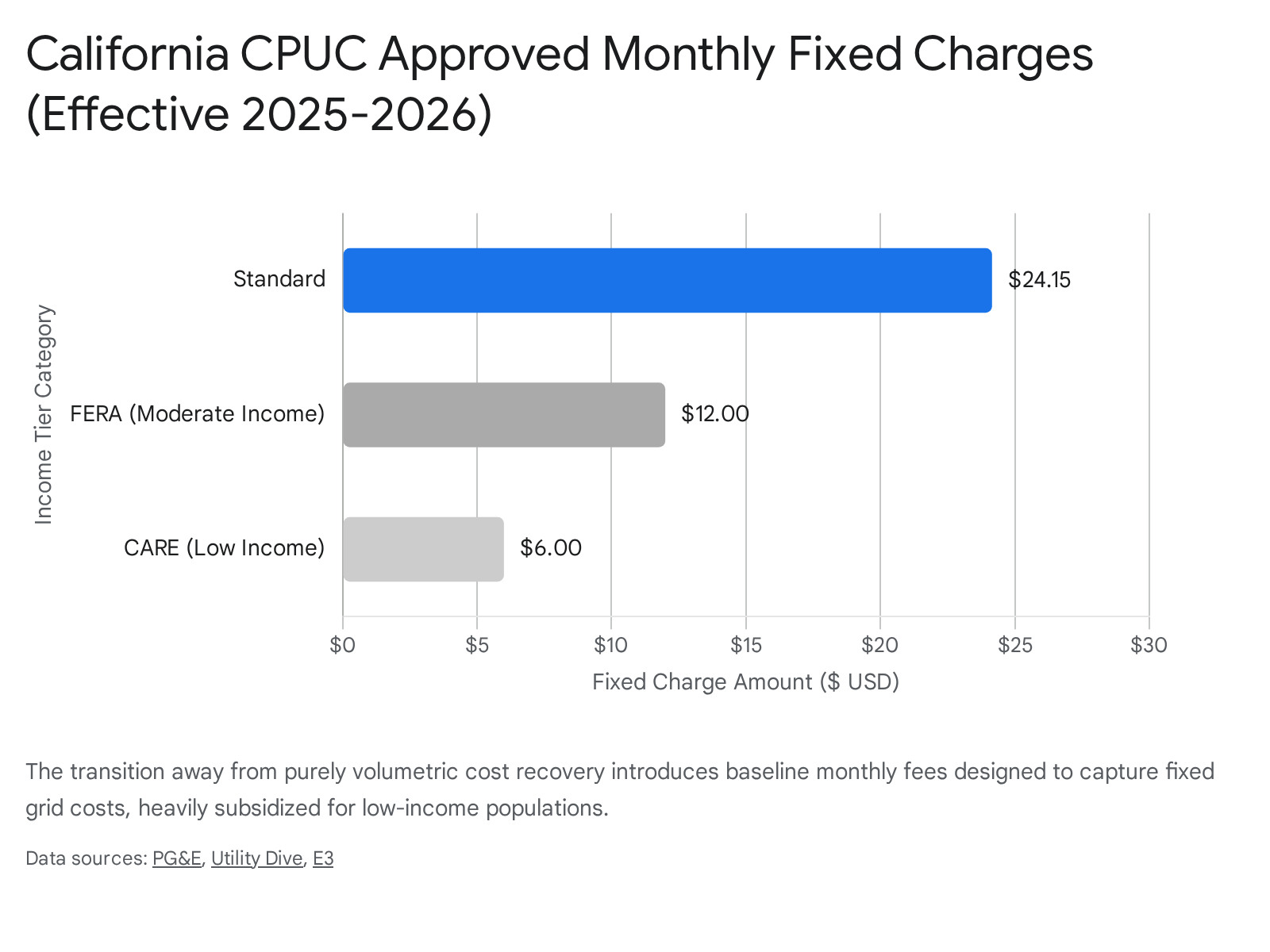

In 2022, the state of California passed Assembly Bill 205, a landmark piece of legislation mandating the implementation of an Income-Graduated Fixed Charge (IGFC) for the state's massive investor-owned utilities (Pacific Gas & Electric, Southern California Edison, and San Diego Gas & Electric) 4041. Set to take effect between late 2025 and early 2026, the California Public Utilities Commission (CPUC) approved a tiered fixed charge structure based on verifiable household income 414243.

The new billing structure mandates a standard fixed charge set at $24.15 per month for the majority of customers. However, to address energy burden and equity, the CPUC established discounted rates of $12 per month for moderate-income households (those enrolled in the Family Electric Rate Assistance, or FERA, program) and $6 per month for low-income households (those enrolled in the California Alternate Rates for Energy, or CARE, program) 114244.

The primary regulatory objective of the IGFC is twofold. First, it ensures that all ratepayers, regardless of their behind-the-meter solar generation capacity, contribute equitably to the fixed costs of maintaining the macro-grid infrastructure 4045. Second, by moving a substantial portion of fixed costs out of the volumetric rate, the CPUC expects the per-kWh price of electricity to drop by 5 to 7 cents 394144. This reduction in the marginal cost of electricity is critical for achieving state climate goals, as it significantly improves the economic payback period for beneficial electrification technologies, such as electric vehicles and residential heat pumps, which rely heavily on high volumetric grid consumption 404446.

However, the policy remains fiercely contested. Critics argue that introducing high fixed charges reduces the financial incentive for basic energy conservation and fundamentally undermines the return on investment for existing rooftop solar adopters, effectively penalizing past investments in clean energy 384146. Opposing legislators introduced Assembly Bill 1999 to repeal or severely limit the fixed charge, reflecting deep political divisions over how grid costs should be allocated 46. Fundamentally, by insulating utility revenues from the impacts of reduced volumetric demand, fixed charges neutralize the disruptive economic threat of prosumerism, securely entrenching the traditional utility's capital recovery mechanism regardless of how efficiently the customer manages their own load 64349.

Grid Edge Technologies and Artificial Intelligence

While distributed generation initially acted as an unmitigated disruptive force against incumbent utilities, the introduction of advanced digitalization and artificial intelligence (AI) at the grid edge is providing grid operators with the sophisticated tools necessary to assimilate these rogue assets.

Distributed Intelligence and Virtual Power Plants

The modern electric grid is undergoing a massive transformation from a physical system engineered merely to transport electrons into a software-defined network engineered to process massive datasets, automate decisions, and optimize distributed resources 2050. Edge AI involves deploying machine learning algorithms locally on smart meters, battery inverters, EV chargers, and distribution transformers. This allows individual nodes to process data, predict local load, and react to grid voltage conditions in real-time without relying on centralized communication latency or a single centralized command center 2347. The market for Edge AI in smart grids is expanding rapidly; global projections suggest the broader edge AI market could surge to $143 billion by 2034 50.

This distributed, autonomous intelligence is the foundational enabling technology for Virtual Power Plants (VPPs). A VPP aggregates thousands of disparate, customer-owned DERs - such as smart thermostats, home battery systems, commercial microgrids, and electric vehicles - and coordinates their charging and discharging behavior via cloud-based software to mimic the dispatchable capabilities of a traditional centralized power plant 484950.

When the duck curve dictates a steep evening ramp, or when extreme weather threatens a macro-grid failure, an AI-driven VPP can autonomously signal thousands of residential batteries to discharge simultaneously, effectively flattening the peak load and providing critical capacity to the grid 2027. The U.S. Department of Energy estimates that to meet rising demand and maintain reliability, the domestic grid will require between 80 to 160 GW of virtual power plant capacity by 2030, representing roughly 10 to 20 percent of total peak load 50.

Massive federal investments are accelerating this transition. Projects like Sunnova's "Project Hestia," backed by a $3 billion loan guarantee from the Department of Energy, aim to install 568 MW of rooftop solar, battery storage, and VPP software across up to 115,000 households, specifically targeting disadvantaged communities 55. By formally compensating prosumers for participating in VPPs and providing capacity back to the network, utilities and regulators are successfully transforming a disruptive threat into an orchestrated, highly valuable grid service 4955.

The AI Load Paradox and the Resurgence of Centralized Capital

The relationship between artificial intelligence and the utility sector presents a profound and highly consequential paradox. While edge AI algorithms enable the efficient integration of DERs and support decentralized resilience, the centralized training and deployment of massive Large Language Models (LLMs) has triggered explosive growth in hyperscale data centers 5152.

Data centers are exceptionally energy-intensive operations, consuming 10 to 50 times more power per square foot than standard commercial real estate 51. Projections indicate that electricity demand from data centers will multiply exponentially over the coming decade. In the United States alone, data center consumption could account for up to 12 percent of total national electricity demand by 2028 51. Meeting this projected 600 TWh of additional electricity demand would necessitate building the equivalent of approximately 77 new 1,000-megawatt nuclear reactors operating at peak capacity 51. The International Energy Agency warns that 15 to 27 GW of onsite natural gas generation could end up powering US data centers by 2030, highlighting the sheer scale of the required firm capacity 50.

This staggering, exogenous load growth effectively counteracts the central premise of the utility death spiral. The death spiral theory relies entirely on the assumption of shrinking overall volumetric demand. However, the AI revolution, coupled with the macro-trends of industrial reshoring and the electrification of transportation (EVs), ensures that overall grid demand will reach unprecedented highs 5152.

For traditional utilities, this represents a historic opportunity. Utilities are now faced with an unprecedented mandate for capital deployment to build the massive firm generation, high-voltage transmission lines, and distribution upgrades required by these hyperscale facilities 525354. By deploying capital at this scale, utilities are guaranteeing decades of rate-base growth, effectively cementing the long-term viability of the centralized utility business model and rendering the death spiral threat largely obsolete 175253.

Utility-Scale Storage: The Incumbent Counter-Offensive

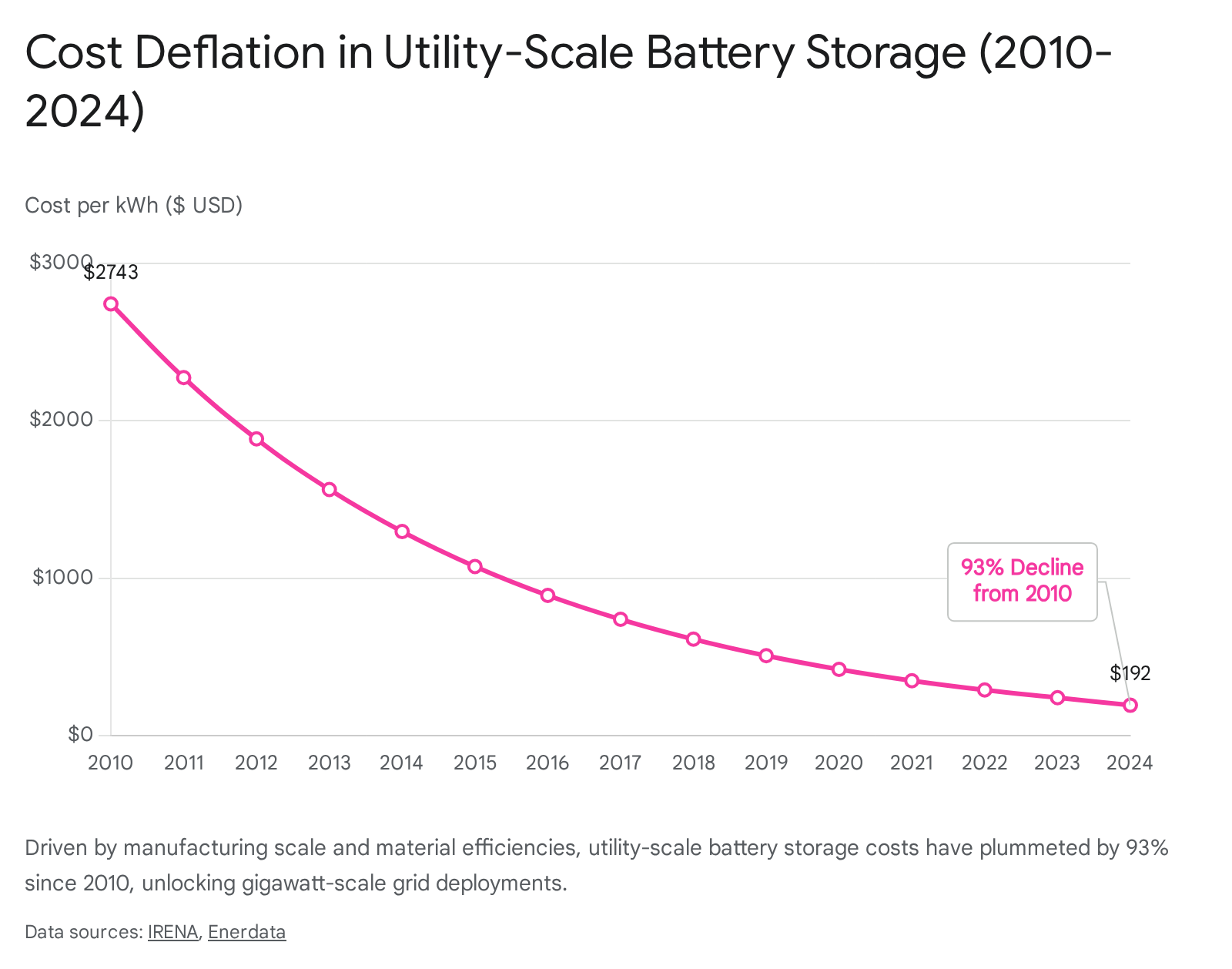

To survive the intermittency of utility-scale renewables and actively manage the severe economic strain of the duck curve, the centralized utility model is executing a massive, capital-intensive deployment of utility-scale battery energy storage systems (BESS). Benefiting heavily from the rapid scaling of the global electric vehicle supply chain and advancements in material science, the cost of utility-scale lithium-ion battery storage plummeted by an astonishing 93 percent between 2010 and 2024, falling to approximately $192/kWh 955.

This unprecedented cost deflation has catalyzed massive market growth, allowing traditional utilities to deploy storage assets on a scale that dwarfs decentralized residential batteries. In 2024 alone, the United States installed over 12.3 gigawatts (GW) of energy storage, with the utility-scale segment accounting for the vast majority of that capacity and driving 32% year-over-year growth 56.

The global expansion is equally staggering. The utility-scale energy storage development pipeline across Europe has surged to over 130 GW across more than 3,000 projects, driven by the critical need for grid stability and the integration of massive offshore wind and solar assets 57. Similarly, Australia has rapidly ascended to become the third-largest utility-scale battery market globally, trailing only China and the United States 58. Australian utilities and developers are commissioning gigawatt-scale projects to tame extreme price volatility and seamlessly displace retiring coal assets within the National Electricity Market 2758.

Utility-scale storage functions as the ultimate architectural defense against the disruption of solar PV. By absorbing vast quantities of excess solar generation during the midday duck curve trough and discharging it forcefully during the steep evening peak, BESS directly neutralizes grid instability without requiring utilities to forfeit control to decentralized, peer-to-peer prosumer networks 2527.

Furthermore, the economic competitiveness of these centralized green assets is now undeniable. Data from 2024 indicates that 91 percent of all newly commissioned utility-scale renewable projects globally delivered electricity at a lower cost than the cheapest fossil fuel alternatives 95559. This proves conclusively that centralized capital deployment into clean energy and storage can effectively compete with distributed models on strict levelized cost of electricity (LCOE) metrics, reinforcing the utility's position as the primary engine of the energy transition 955.

Conclusions

The application of disruptive innovation theory to the energy sector accurately predicted that distributed energy resources would attack the structural and economic vulnerabilities of the centralized, volumetric utility model. The proliferation of rooftop solar PV and behind-the-meter storage forced an unprecedented decoupling of consumer energy consumption from utility revenue generation, manifesting physically in the operational strains of the duck curve and sparking highly credible concerns regarding an impending utility death spiral.

However, the assumption that incumbent utilities would simply collapse under this decentralized pressure fundamentally underestimated the protective power of regulatory restructuring and the sheer adaptability of capital-intensive monopolies. By proactively transitioning away from pure volumetric pricing toward sophisticated time-of-use rates and income-graduated fixed charges, utilities and their regulators are systematically insulating utility revenue recovery from the threat of grid-edge efficiency and self-generation.

Concurrently, the rapid deployment of artificial intelligence, virtual power plants, and gigawatt-scale battery energy storage allows utilities to co-opt distributed assets, transforming rogue disruptive threats into orchestrated, valuable network services. Finally, the massive, exogenous load growth driven by hyperscale AI data centers and the electrification of the broader economy has completely reversed the narrative of shrinking volumetric demand. Ultimately, the centralized utility model is not facing extinction; rather, it has successfully leveraged regulatory frameworks and advanced technology to undergo a forceful evolution, transitioning from a pure commodity provider into a highly secure, digitally orchestrated network manager.