Databricks financial performance and index inclusion timing

Architectural Evolution of Data Platforms

The transition of enterprise data architecture from passive storage repositories to active artificial intelligence ecosystems represents a fundamental structural shift. As organizations move beyond experimental deployments of generative artificial intelligence and large language models (LLMs), the software infrastructure required to sustain these workloads has converged into a distinct "AI middleware" layer 12. At the center of this transformation is the architectural debate between traditional cloud data warehouses and decoupled data lakehouses.

Traditional Warehouses versus Data Lakehouses

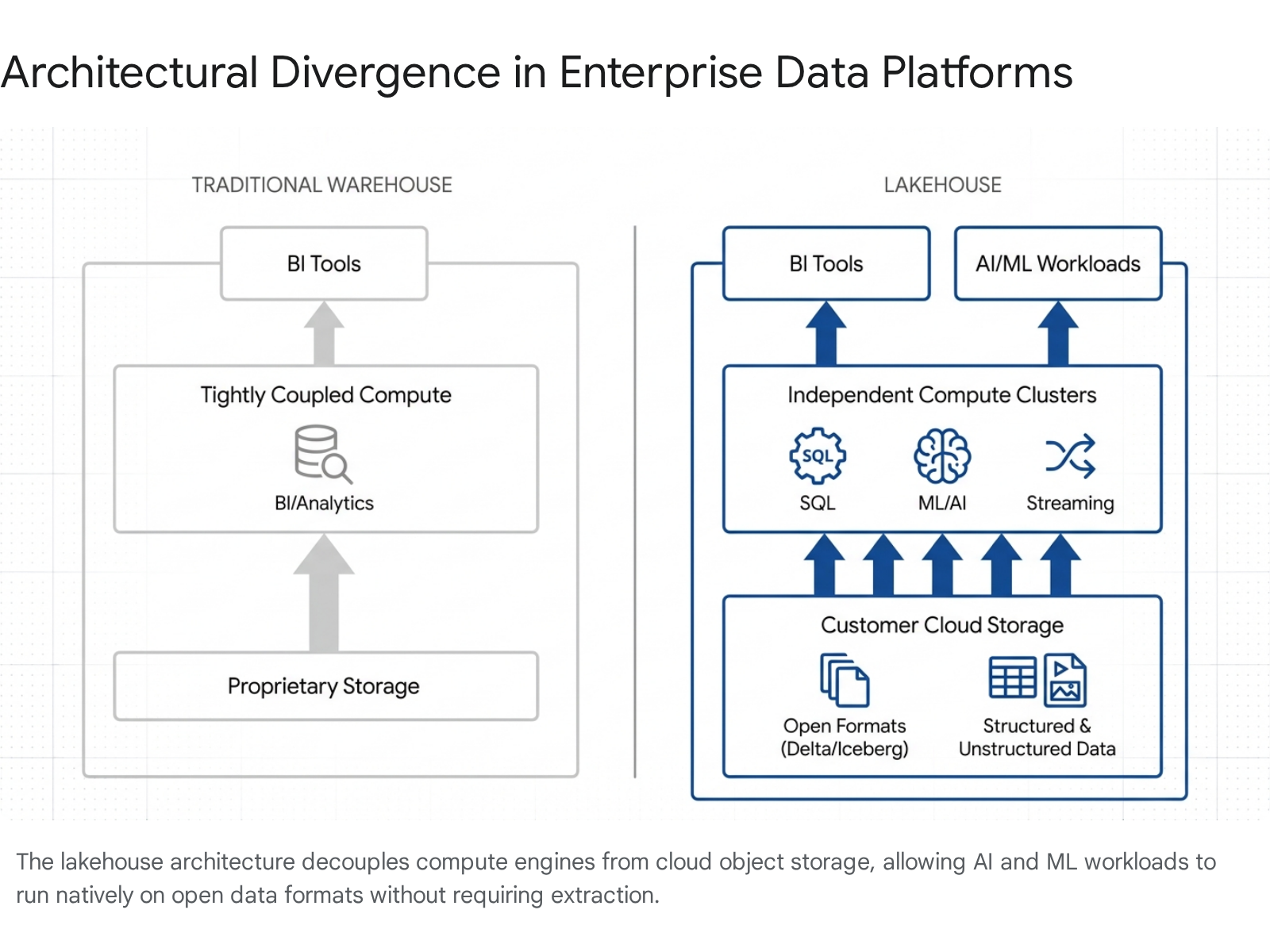

Historically, enterprise data infrastructure relied on tightly coupled cloud data warehouses. In this model, championed by platforms like Snowflake, compute and storage operate within a proprietary, integrated environment 142. This architecture excels at executing structured SQL queries, business intelligence (BI) reporting, and delivering operational simplicity, but it inherently limits flexibility when handling massive volumes of unstructured or semi-structured data required for machine learning 42.

Conversely, the data lakehouse architecture decouples the compute engine from the underlying storage layer. Pioneered by Databricks, the lakehouse allows proprietary enterprise data to reside in the customer's own cloud object storage - such as Amazon S3, Google Cloud Storage, or Azure Data Lake Storage - using open table formats like Delta Lake and Apache Iceberg 1237. Independent analysts indicate that this separation mitigates vendor lock-in, avoids punitive data egress fees, and provides the flexibility of a data lake combined with the structural reliability of a warehouse 1.

The physical requirements of machine learning workloads dictate this architectural preference. Training an AI model or conducting large-scale feature engineering is not a discrete analytical query; it is a highly iterative loop that computes gradients and updates weights millions of times 8. A traditional virtual warehouse was not designed for this distributed processing loop. In tightly coupled systems, unstructured data must often be extracted and moved to a separate compute environment for ML training, creating a governance seam and increasing latency 8. By contrast, the lakehouse allows distributed engines like Apache Spark to process data natively where it resides, maintaining uniform governance and lineage tracking 78.

The Medallion Architecture Framework

To operationalize the lakehouse, leading vendors utilize a standardized design pattern known as the Medallion Architecture. This methodology logically organizes data into three distinct layers - Bronze, Silver, and Gold - to progressively improve data quality and structure as it flows through the platform 74.

The Bronze layer serves as an immutable historical archive, ingesting and storing raw data in its original format from various source systems without alteration 74. The intermediate Silver layer represents the core integration engine, where raw data is cleansed, filtered, and integrated into a unified enterprise view 4. Finally, the Gold layer contains highly curated, aggregated data optimized for specific consumption use cases, such as business intelligence dashboards or machine learning feature stores 74.

By standardizing this pipeline within a single platform, enterprises eliminate the need to maintain redundant, siloed repositories. Data scientists can train models on raw or cleansed data in the Bronze and Silver layers, while analysts query the Gold layer, all without moving the data across distinct physical systems 75. Market surveys conducted in late 2025 demonstrate that 82.6% of enterprises are actively implementing these architectures, with nearly half of all data infrastructure investments driven explicitly by the need to enable generative AI 11.

Competitive Market Positioning

The competition to serve as the default enterprise data substrate features specialized AI platforms competing directly against hyperscaler ecosystems 1213. While the architectural divide between warehouses and lakehouses was distinct in the early 2020s, by 2026, the market has undergone substantial convergence. Snowflake has introduced native support for Apache Iceberg and integrated AI capabilities via Snowflake Cortex, moving toward lakehouse-style flexibility 46. Simultaneously, Databricks has heavily invested in SQL warehouse performance, transactional consistency, and business intelligence ergonomics, crossing a $1 billion revenue run-rate for its Data Warehousing product 47.

| Platform | Architectural Center of Gravity | Primary Differentiators | Target AI/ML Workload Characteristics |

|---|---|---|---|

| Databricks | Decoupled Lakehouse | Spark-native, Unity Catalog, open table formats (Delta Lake, Iceberg) | ML engineering, custom model training, complex RAG pipelines, code-heavy environments 26. |

| Snowflake | Managed Data Cloud / Warehouse | SQL-first, zero infrastructure management, Cortex AI functions | SQL-native AI operations, analytics-heavy use cases, managed environment governance 268. |

| Google BigQuery | Serverless Data Warehouse | Petabyte-scale serverless execution, Gemini AI integrations | High-volume event and ad analytics, seamless Vertex AI ML workflows via SQL 17910. |

| Amazon Redshift | Cluster-Based Data Warehouse | Deep AWS ecosystem integration, predictable pricing via reserved instances | Traditional warehouse patterns tightly coupled with AWS Sagemaker and Glue 101121. |

Despite this convergence, deployment patterns remain specialized. Analysts note that Snowflake and Google BigQuery continue to dominate high-concurrency dashboards, commercial analytics, and SQL-first operational reporting 21710. Conversely, Databricks commands a significant moat in data engineering, machine learning lifecycle management (via MLflow), and custom AI agent development 12129.

Emergence of the AI Middleware Control Plane

Integration of Large Language Models

As AI adoption scales, the enterprise data platform has functionally evolved into an AI middleware layer. The complexity of enterprise AI extends beyond accessing a foundation model; it requires retrieval-augmented generation (RAG) infrastructure, vector databases, and agent orchestration frameworks 21213.

Data platforms have responded by embedding these capabilities directly into their environments, mitigating the need to export data to external machine learning infrastructure 12. For example, Databricks Mosaic AI enables developers to build, fine-tune, and serve models directly on existing lakehouse data 68. By integrating vector search natively into the data architecture, organizations can connect foundation models to proprietary knowledge graphs without establishing separate, insecure pipelines 812. This in-platform approach allows generative AI applications to inherit the existing security and access controls already defined for the underlying data 8.

Agentic Governance and the Unity Catalog

The rapid deployment of agentic AI - autonomous systems executing multi-step tasks across integrated enterprise tools - has introduced unprecedented governance challenges 14. When an AI agent fields a customer inquiry, it may query an LLM, extract order history from a customer relationship management (CRM) database, and check shipping APIs before formulating a response 14. Traditional governance frameworks, which operate in static silos, lack the capacity to track, authorize, and audit these dynamic, cross-system interactions 14.

Databricks has addressed this deficiency by expanding its Unity Catalog from a static data governance tool into an active agent governance platform 1415. Originally deployed to govern structured tables through a unified permissions model, Unity Catalog now encompasses unstructured data, machine learning models, and autonomous agents 815. Because the catalog already manages the identity and access management (IAM) protocols for the underlying data, it can natively enforce policies dictating which AI agents are permitted to access specific external application programming interfaces (APIs) or data stores 1415.

The Unity AI Gateway Architecture

To operationalize this governance, Databricks introduced the Unity AI Gateway as the central routing and enforcement fabric for the agentic ecosystem 1516. The gateway acts as a unified proxy through which every model call, tool invocation, and agent interaction flows, regardless of whether the underlying model is hosted locally or provided externally by OpenAI, Anthropic, or AWS Bedrock 1517.

The implementation of the AI Gateway addresses four critical pillars of enterprise AI deployment: 1. Observability and Payload Logging: The gateway captures the complete payload of every model interaction, including the exact prompt sent, the raw response generated, and precise latency metrics. This data is automatically written to inference tables within the lakehouse, establishing an immutable audit trail required for emerging regulatory compliance 141516. 2. Model Context Protocol (MCP) Governance: Agents increasingly rely on external tools. The gateway manages MCP servers, enforcing identity-aware policies that dictate exactly which agents can invoke specific tools based on runtime context 141516. 3. Cost Attribution: As inference volume scales, unpredictable computing expenses present a severe operational risk. The gateway logs precise token consumption and dollar costs, attributing them dynamically to specific endpoint tags, environments, or internal user identities, thereby preventing token sprawl 141617. 4. Real-Time Guardrails: Instead of relying on static filters, the gateway evaluates customizable safety and compliance policies on inputs and outputs in real-time, preventing data exfiltration and enforcing business-specific logic without breaking agent workflows 1617.

By centralizing these functions, the AI middleware layer ensures that governance travels with the resources, solidifying the data platform as the unavoidable control room for enterprise AI 915.

Capital Intensity and Cost Structures

CapEx Heavy Foundation Models versus OpEx Middleware

The financial profile of the AI ecosystem is deeply bifurcated by capital intensity. Foundation model developers, such as OpenAI and Anthropic, face staggering capital expenditures (CapEx) required to procure, cool, and power immense clusters of specialized graphics processing units (GPUs) 2818. Global investment in AI data center infrastructure is projected to reach $5.2 trillion by 2030, driven by the sheer computational density required for model training and inference 18. As a result, frontier AI labs operate with high cash burn rates; OpenAI's computing expenditures could exceed $120 billion by 2028, rendering the company deeply unprofitable despite generating tens of billions in annualized revenue 1920.

In contrast, AI middleware and data platforms like Databricks function on an operating expenditure (OpEx) model 21. Databricks monetizes the software application layer - organizing data and orchestrating AI workflows - rather than bearing the physical hardware costs of the AI buildout 34. By relying on public cloud hyperscalers (AWS, Azure, Google Cloud) for the underlying compute and storage hardware, Databricks passes the infrastructure capital requirements to the cloud providers, insulating its own balance sheet from the infrastructure arms race 3422.

The Dual-Bill Pricing Mechanism

To facilitate this asset-light software model, Databricks employs a complex "two-bill" pricing structure that heavily impacts enterprise FinOps. Organizations do not pay Databricks a single, bundled infrastructure fee 2324. Instead, costs are bifurcated: * Platform Fees (Databricks DBUs): Databricks charges for its management layer, orchestration, and software capabilities using a normalized metric called Databricks Units (DBUs), billed per second of consumption 2324. * Cloud Infrastructure Pass-Through: Simultaneously, the customer's cloud provider bills directly for the virtual machines (VMs), block storage, and network egress required to execute the Databricks clusters in the data plane 2224.

This dual structure frequently causes budget overruns for inexperienced teams, as cloud infrastructure costs typically account for 55% to 60% of the total cost of ownership (TCO) for a standard mid-size deployment, effectively doubling or tripling the visible DBU platform fee 2224. The lack of native, unified billing visibility forces data teams to manually reconcile Databricks DBU reports with complex cloud provider Cost and Usage Reports (CUR), a fragmented process that obfuscates true workload costs 2539.

Workload Optimization and Total Cost of Ownership

Optimizing costs within this dual-bill paradigm requires strict architectural hygiene. Databricks compute costs fluctuate dramatically - often by a factor of three or four - depending on the cluster type selected for execution 2324.

"All-Purpose Compute" clusters, designed for interactive, human-driven data science and collaborative notebook environments, carry a premium DBU rate (historically $0.40 to $0.55 per DBU) 2223. Conversely, "Jobs Compute" clusters, optimized for automated, scheduled production pipelines (ETL workflows), are priced at a steep discount (approximately $0.15 per DBU) 22. Financial optimization relies heavily on enforcing organizational policies that transition mature, scheduled workloads off interactive clusters and onto automated Jobs clusters, coupled with aggressive auto-termination rules to prevent billing for idle virtual machines 22232426.

Financial Trajectory and Growth Dynamics

Revenue Acceleration at Scale

Enterprise business-to-business (B2B) software companies historically experience a deceleration in growth rates as their baseline revenue scales. Databricks has defied this convention, exhibiting rare revenue acceleration as it crossed the multi-billion-dollar threshold 27.

In the fiscal year ending January 2024, Databricks reported approximately $1.6 billion in annualized revenue, growing at 50% year-over-year 27. Over the subsequent 24 months, propelled by the widespread adoption of enterprise AI and the successful launch of serverless warehousing products, both scale and velocity increased.

| Reporting Period | Annualized Revenue Run-Rate | Year-Over-Year Growth | Key Milestones & Context |

|---|---|---|---|

| Jan 2024 | $1.6 Billion | ~50% | Core lakehouse expansion and initial data intelligence positioning. 27 |

| Jun 2024 | $2.4 Billion | ~60% | Rapid acceleration indicating platform consolidation by enterprises. 2728 |

| Jul 2025 | $3.7 Billion | ~50% | Sustained high growth amid general B2B software market slowdown. 27 |

| Sep 2025 (Q2) | $4.0 Billion | >50% | Closure of $1B Series K valuing the company over $100B. 2729 |

| Dec 2025 (Q3) | $4.8 Billion | >55% | AI products and Data Warehousing each cross $1B run-rates. 727 |

| Feb 2026 (Q4) | $5.4 Billion | >65% | Accelerated growth to 65%; closing of >$4B Series L at $134B valuation. 273045 |

This exponential trajectory is underpinned by top-decile expansion metrics. Databricks reports a net revenue retention (NRR) rate exceeding 140%, indicating that existing customers consistently increase their consumption by more than 40% annually 273031. In a consumption-based pricing model, NRR is a critical proxy for product stickiness; as enterprises ingest more data and deploy more AI agents, token consumption compounds automatically without requiring incremental sales motions 3147. Databricks' AI products alone reached a $1.4 billion revenue run-rate in Q4 2026, comprising roughly 26% of total revenue and growing substantially faster than the core business 273048.

By comparison, Snowflake, its closest public market competitor, reached a similar revenue scale of approximately $4.4 billion by early 2026 but experienced a deceleration in growth to approximately 27% to 29%, with NRR stabilizing near 125% 27493233. This divergence in growth velocity explains the severe disparity in enterprise value: Snowflake commands a public market capitalization near $79 billion (trading at roughly 18x forward revenue), while Databricks secured a private valuation of $134 billion (commanding a premium 25x multiple) 273233.

Profitability Metrics and Free Cash Flow

Databricks' capital-light business model results in highly favorable cash generation. The company reported positive free cash flow (FCF) over the trailing twelve months ending in early 2026 343048. Free cash flow margin is widely viewed by institutional analysts as a superior indicator of sustainable profitability compared to unadjusted earnings, as it strips away non-cash accruals and reflects the actual capital available for reinvestment 343536. The platform maintains strong gross margins, generally ranging from 75% to 80%, which is consistent with the upper echelons of cloud-native enterprise software 4748.

However, positive FCF does not equate to Generally Accepted Accounting Principles (GAAP) net income 49. A critical divergence in modern technology valuation is the treatment of employee equity compensation.

The Impact of Stock-Based Compensation

To attract and retain elite engineering talent in the highly competitive AI sector, Databricks relies heavily on Stock-Based Compensation (SBC) 55. Median total compensation for software engineers at Databricks exceeds $500,000 annually, with Principal Engineers earning over $1.65 million, the vast majority of which is issued as pre-IPO Restricted Stock Units (RSUs) 55.

Under U.S. GAAP, SBC is recorded as a non-cash operating expense, allocated across research and development, sales and marketing, and administrative line items 37. Because this expense dilutes shareholder equity, GAAP mandates its deduction from net income 37. Conversely, when calculating free cash flow, analysts and companies add SBC back to operating cash flow, as no actual cash leaves the corporate treasury 3757.

The magnitude of SBC at high-growth software firms is substantial. While Databricks is generating positive cash flow, the inclusion of its massive SBC liabilities results in significant GAAP operating losses, with estimates pointing to negative operating margins exceeding $400 million in 2024, a deficit that likely persists into 2026 due to increasing headcount and a rising private valuation 4938. Consequently, despite its operational efficiency and cash generation, Databricks remains deeply unprofitable on a strict GAAP basis 4959.

Mega-Cap Initial Public Offerings and Benchmark Mechanics

The convergence of AI hype and unprecedented private market valuations has created a pipeline of "mega-cap" Initial Public Offerings slated for 2026 and 2027. This cohort - primarily consisting of SpaceX, OpenAI, Anthropic, and Databricks - is too massive to be seamlessly absorbed by public markets without structurally impacting passive index funds 603962.

The 2026 Technology Initial Public Offering Cohort

A comparative analysis of the leading pre-IPO candidates reveals vast disparities in business quality and financial viability, despite their similarly massive valuations.

| Entity | Estimated Valuation | Est. Annualized Revenue | Gross Margin | Capital Efficiency / FCF | Core Monetization Strategy |

|---|---|---|---|---|---|

| Databricks | $134 Billion | $5.4 Billion | ~75% - 80% | Positive FCF | B2B Consumption Software 3430 |

| SpaceX | $1.75 - $2.0 Trillion | ~$18.7 Billion (2025) | N/A (Heavy Ind.) | Negative | Aerospace / Satellite Internet 6039 |

| Anthropic | $50 - $900+ Billion | ~$3.0 - $30.0+ Billion | ~40% (2026 Est.) | Deeply Negative | Foundation Model APIs / Enterprise 196240 |

| OpenAI | $100 - $852+ Billion | ~$13.0 - $25.0 Billion | ~40% - 46% | Deeply Negative | Foundation Model APIs / Consumer 316264 |

(Data derived from reported mid-2026 private financing and S-1 leak estimates. 19303160624064)

While OpenAI and Anthropic generate staggering top-line revenue, their business models are hampered by the exorbitant cost of compute. Anthropic aims to reach a 40% gross margin in 2026, still far below software standards, while OpenAI is projected to post operating losses as high as $14 billion due to inference costs 19316240. Databricks stands alone in this cohort as a highly capital-efficient, free-cash-flow-positive enterprise software entity insulated from the GPU infrastructure race 3431. However, public market index methodology treats all of these entities with similar skepticism based on their lack of GAAP profitability.

Nasdaq Fast Entry Inclusion Rules

Inclusion in benchmark indices triggers automatic, price-agnostic buying from passive exchange-traded funds (ETFs) and mutual funds tracking those indices 603941. Anticipating the liquidity strain of absorbing companies valued over $100 billion, index providers faced immense pressure from investment banks to relax eligibility rules 6039.

Nasdaq capitulated to this pressure. Effective May 1, 2026, Nasdaq implemented a "Fast Entry" rule for the Nasdaq-100 index 60394142. Under this updated methodology, any newly listed company whose total market capitalization ranks within the top 40 current constituents (historically requiring a valuation over $100 billion) is exempt from traditional seasoning requirements 4243. These mega-caps can be added to the Nasdaq-100 just 15 trading days after their IPO 4142. Furthermore, Nasdaq eliminated its strict 10% minimum public float rule, utilizing a float multiplier to accommodate companies that only list a small fraction of their outstanding shares 3943.

For Databricks, which easily clears the $100 billion market capitalization threshold, this ensures that shortly following its S-1 filing and subsequent IPO, passive funds tracking the Nasdaq-100 (such as the Invesco QQQ ETF) will be forced to algorithmically purchase its shares 603944.

Standard and Poor 500 Eligibility Constraints

Conversely, the S&P 500 benchmark maintains an exceptionally rigid methodology. In May 2026, S&P Dow Jones Indices opened a consultation proposing to reduce the standard 12-month seasoning window to six months and waive the strict GAAP profitability test for mega-cap IPOs 6045.

On June 4, 2026, S&P issued a definitive rejection of its own proposal. The index provider announced that no exceptions to financial viability, seasoning periods, or minimum investable weight factors would be granted solely based on market capitalization, asserting that "core index principles" take precedence over rapid inclusion 4546.

To gain inclusion in the S&P 500, a company must satisfy the following criteria: 1. Seasoning: A mandatory 12-month waiting period of public trading on an eligible exchange 6045. 2. Public Float: Adequate liquidity and a minimum public float of at least 10% of shares outstanding 6047. 3. Financial Viability: The company must demonstrate positive GAAP earnings in the most recent quarter, as well as positive cumulative GAAP earnings over the most recent four consecutive quarters 60444647.

Liquidity Implications for Passive Index Funds

The S&P 500's adherence to unadjusted GAAP profitability creates a severe bottleneck for Databricks. While the company is cash-generative, its heavy reliance on stock-based compensation means it will likely continue to report trailing 12-month GAAP net losses immediately following its IPO 49.

Index providers explicitly ignore non-GAAP adjusted earnings and free cash flow metrics that exclude real shareholder dilution caused by SBC 353757. As a result, even after satisfying the 12-month seasoning requirement, Databricks cannot enter the S&P 500 until its revenue scale outpaces its equity compensation liabilities to achieve genuine GAAP net income 6047.

This dynamic bifurcates the passive market. The roughly $1.4 trillion in assets tracking the Nasdaq-100 will aggressively rebalance to absorb Databricks almost immediately post-IPO 60. Meanwhile, the estimated $7.5 trillion in passive capital tracking the S&P 500 will remain entirely unexposed to the dominant AI middleware platform until late 2027 or 2028 at the earliest 6046. Until the firm transitions its employee compensation structure or massively outgrows its RSU dilution, Databricks' valuation will be dictated by active managers and tech-heavy indices, isolated from the broad-market passive inflows that traditionally stabilize mature mega-cap equities.