Databricks Valuation and Data Lakehouse Market Dynamics

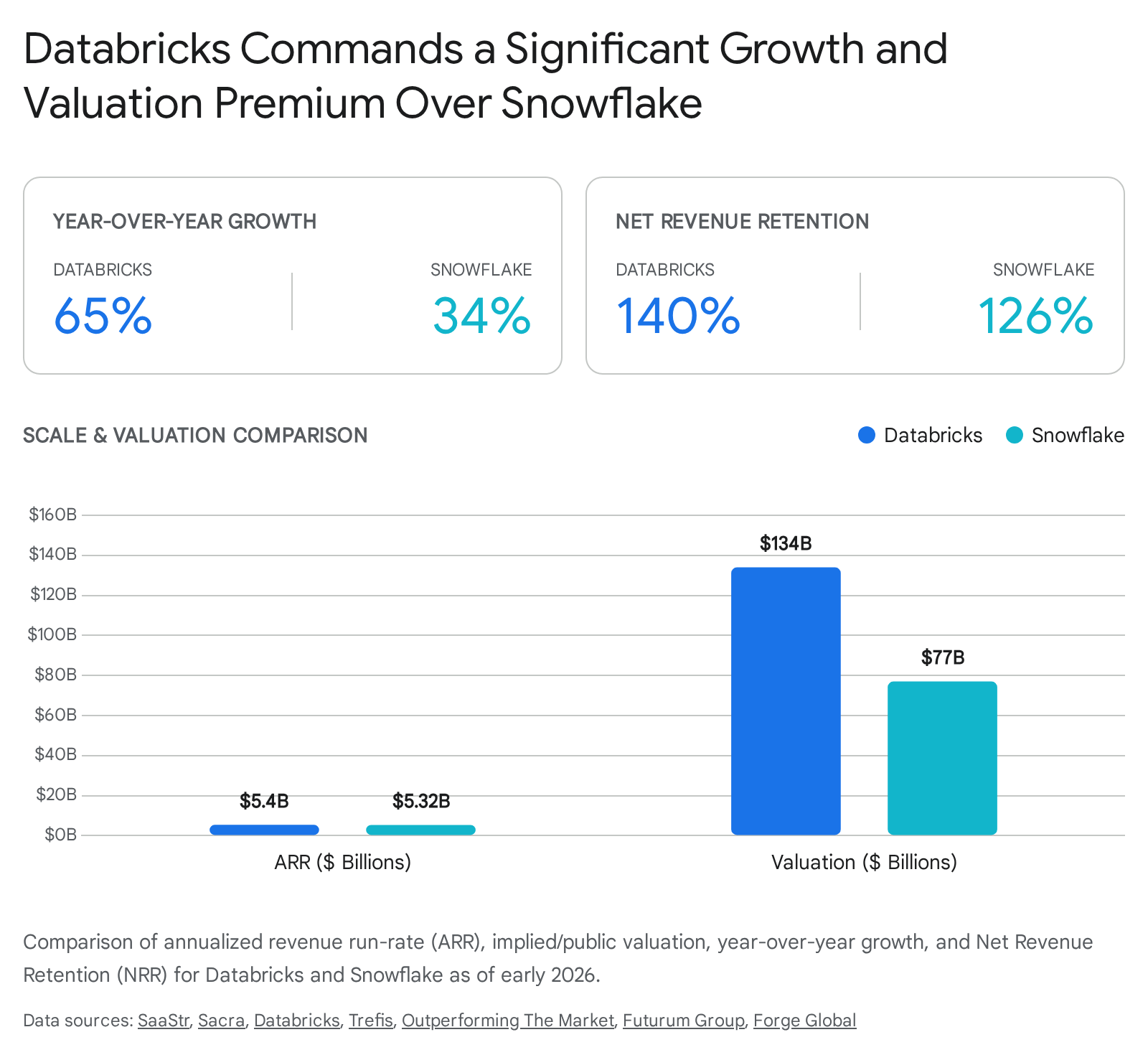

The enterprise data infrastructure sector has undergone a profound architectural and financial realignment, driven by the rapid scaling of artificial intelligence workloads and the convergence of data warehousing and data lake architectures. At the center of this transformation is the competitive dynamic between Databricks and Snowflake. As of 2026, Databricks has achieved a $134 billion valuation in the private markets following a $4 billion Series L funding round, effectively bypassing Snowflake's public market capitalization 123. Generating $5.4 billion in annualized revenue run-rate (ARR) while accelerating growth to 65% year-over-year, Databricks has established a formidable competitive moat through open-source table formats, unified machine learning engineering ecosystems, and anomalous net revenue retention metrics 234.

This report examines the underlying financial trajectories, technical architecture evolutions, artificial intelligence monetization strategies, and comparative valuation multiples defining the rivalry between Databricks and Snowflake. Furthermore, it contextualizes these operational dynamics within broader macroeconomic trends, including the impact of regional data sovereignty mandates currently reshaping European and global cloud consumption architectures.

Valuation Dynamics and Market Capitalization

The valuation spread between Databricks and Snowflake illustrates a divergence in how financial markets price growth, profitability, and artificial intelligence infrastructure positioning. While both entities operate consumption-based revenue models aligned with enterprise compute usage, their respective capital structures and profitability profiles command distinct multiples.

Databricks Series L and Private Market Premium

Databricks' ascent to a $134 billion valuation in December 2025 represents a defining milestone in late-stage private equity. The Series L financing, led by Insight Partners, Fidelity Management & Research Company, and J.P. Morgan Asset Management, brought the company's total raised capital to over $18 billion across equity and debt, including approximately $2 billion in new debt capacity 134. This valuation reflects a 34% step-up from its $100 billion Series K valuation in August 2025 and is more than double its $62 billion Series J valuation from December 2024 35.

The institutional appetite for Databricks equity extends into the secondary markets. Market data from mid-2026 indicates that Databricks shares were clearing at an 11.56% premium to the Series L post-money valuation on secondary platforms, implying a derived valuation closer to $149.49 billion 6. Major mutual funds and institutional asset managers reflect this premium in their net asset value (NAV) calculations. BlackRock's Private Investments Fund, for example, disclosed Databricks as a core holding alongside structured credit assets, while Fidelity integrates Databricks within its broader Blue Chip Growth Fund strategy, reflecting confidence in sustained private market markups prior to an initial public offering (IPO) 7811.

This private market premium is fundamentally anchored by operational execution. By February 2026, marking the end of its fiscal fourth quarter, Databricks reported crossing the $5.4 billion ARR threshold 23. Software enterprises operating above $5 billion in revenue historically exhibit growth deceleration as the law of large numbers takes effect. Databricks, however, demonstrated acceleration, moving from 50% year-over-year growth in mid-2025 to 65% by early 2026 2311. Management attributes this leverage heavily to enterprise adoption of generative AI tools and robust platform consolidation 512.

Snowflake Public Market Multiples and Compression

Snowflake, operating as the defining public comparable in the cloud data platform space, navigated a period of multiple compression before initiating an AI-driven resurgence in 2026. Despite highly robust execution by public market standards, Snowflake's market capitalization of approximately $77 billion sits at roughly half of Databricks' implied private valuation 23.

In the first quarter of fiscal 2027 (ended April 2026), Snowflake reported $1.39 billion in total revenue, with product revenue contributing $1.33 billion. This translated to a 34% year-over-year growth rate, representing an acceleration from the 30% growth recorded in the preceding quarter 9101112. Following these results, the company raised its full-year product revenue guidance to $5.84 billion 1112.

However, Snowflake's forward Price-to-Sales (P/S) multiple hovered between 12x and 14x NTM (next twelve months) revenue during early 2026, a sharp compression from its 2021 peak of over 50x 1314. This multiple compression reflects a broader public market rotation that prioritizes Generally Accepted Accounting Principles (GAAP) profitability and penalizes highly dilutive stock-based compensation (SBC) models 1319. While Snowflake generates excellent free cash flow, its GAAP unprofitability remains a structural narrative challenge. Stock-based compensation accounted for approximately 34% of revenue in FY26, which, while declining as a percentage of overall revenue, exerts downward pressure on GAAP operating margins 1516.

Rule of 40 and Financial Performance Trajectories

A rigorous comparison of the financial mechanics underlying both firms relies heavily on the "Rule of 40," a metric indicating that a software company's combined revenue growth rate and profit margin should exceed 40. In the current infrastructure software market, companies clearing this threshold command significantly higher revenue multiples 22.

Databricks has crossed a critical threshold for pre-IPO companies by achieving positive free cash flow (FCF) over the trailing twelve months leading into early 2026 1117. Achieving FCF positivity while sustaining a 65% growth rate yields a Rule of 40 score securely in the top quartile of the software sector, providing Databricks with immense operational flexibility to fund its own acquisitions without relying strictly on external capital 214. Databricks also maintains non-GAAP gross margins in the 80% range, though some internal segments utilizing third-party compute operate closer to the 70-74% band 3111819.

Snowflake maintains high efficiency regarding cash generation, guiding for a 23% adjusted free cash flow margin for FY27, backed by non-GAAP operating margins that expanded to 12% in Q1 FY27 1020. Snowflake's Rule of 40 score in Q1 FY27 stood at approximately 41 (32% adjusted revenue growth plus a 9% non-GAAP operating margin), indicating a healthy balance of growth and profitability 19. However, Databricks' superior growth rate combined with its FCF positivity grants it a commanding lead in aggregate Rule of 40 assessments 14.

The divergence in valuation is further explained by customer expansion metrics. Net revenue retention is the single strongest driver of premium multiples in AI infrastructure 22. By February 2026, Databricks maintained an NRR exceeding 140%, indicating that the average existing customer expands their spend by over 40% annually without factoring in new customer acquisition 2. Databricks also reported over 800 customers consuming more than $1 million annually, and more than 70 customers exceeding $10 million in annual spend 2. By contrast, Snowflake's NRR stabilized at 125% at the end of FY26 and increased slightly to 126% in Q1 FY27, driven by a normalization of enterprise cloud optimization 102021.

| Financial Metric (Early 2026) | Databricks (Private) | Snowflake (Public) |

|---|---|---|

| Annualized Revenue / Run-Rate | $5.4 Billion 23 | ~$5.32 Billion (based on Q1 FY27 $1.33B) 10 |

| YoY Product Revenue Growth | >65% 23 | 34% (Q1 FY27) 1011 |

| Net Revenue Retention (NRR) | >140% 211 | 126% 1120 |

| Implied Valuation / Market Cap | $134 Billion (Series L) 12 | ~$77 Billion 2 |

| Enterprise Value / NTM Revenue | ~25x (Current ARR basis) 222 | ~12.4x - 14x 1314 |

| Gross Margin (Non-GAAP) | ~80% 31118 | 75% 1020 |

| Free Cash Flow (FCF) Margin | Positive (Absolute value undisclosed) 217 | 23% (FY27 Guide) 2022 |

Data Lakehouse Architectural Evolution

The architectural divergence between Databricks and Snowflake historically centered on the ideological debate between the "Data Lakehouse" and the "Cloud Data Warehouse." However, technical developments throughout 2025 and 2026 effectively dissolved the rigid boundaries between these methodologies, forcing both platforms to adapt their underlying storage and governance mechanisms.

Convergence of Cloud Data Warehouses and Lakehouses

Snowflake originated as a highly optimized, fully separated compute-and-storage SQL data warehouse built exclusively for the cloud. Its proprietary architecture historically required data to be ingested into Snowflake's native formats to achieve maximum query performance 2324. Databricks, conversely, pioneered the Data Lakehouse concept, utilizing open-source Apache Spark to execute compute workloads directly over unstructured or semi-structured data lakes stored in inexpensive cloud object storage solutions like AWS S3, Azure Data Lake, and Google Cloud Storage 2526.

The traditional approach to data lakes involved storing massive volumes of raw data in Hadoop Distributed File Systems (HDFS), which offered limited options for ACID (Atomicity, Consistency, Isolation, Durability) transactions 26. Databricks altered this paradigm by introducing Delta Lake, an open-source storage layer that brought transactional reliability and schema enforcement directly to data lakes, preventing bad data from contaminating storage environments during ingestion 26.

Open Table Formats and Interoperability

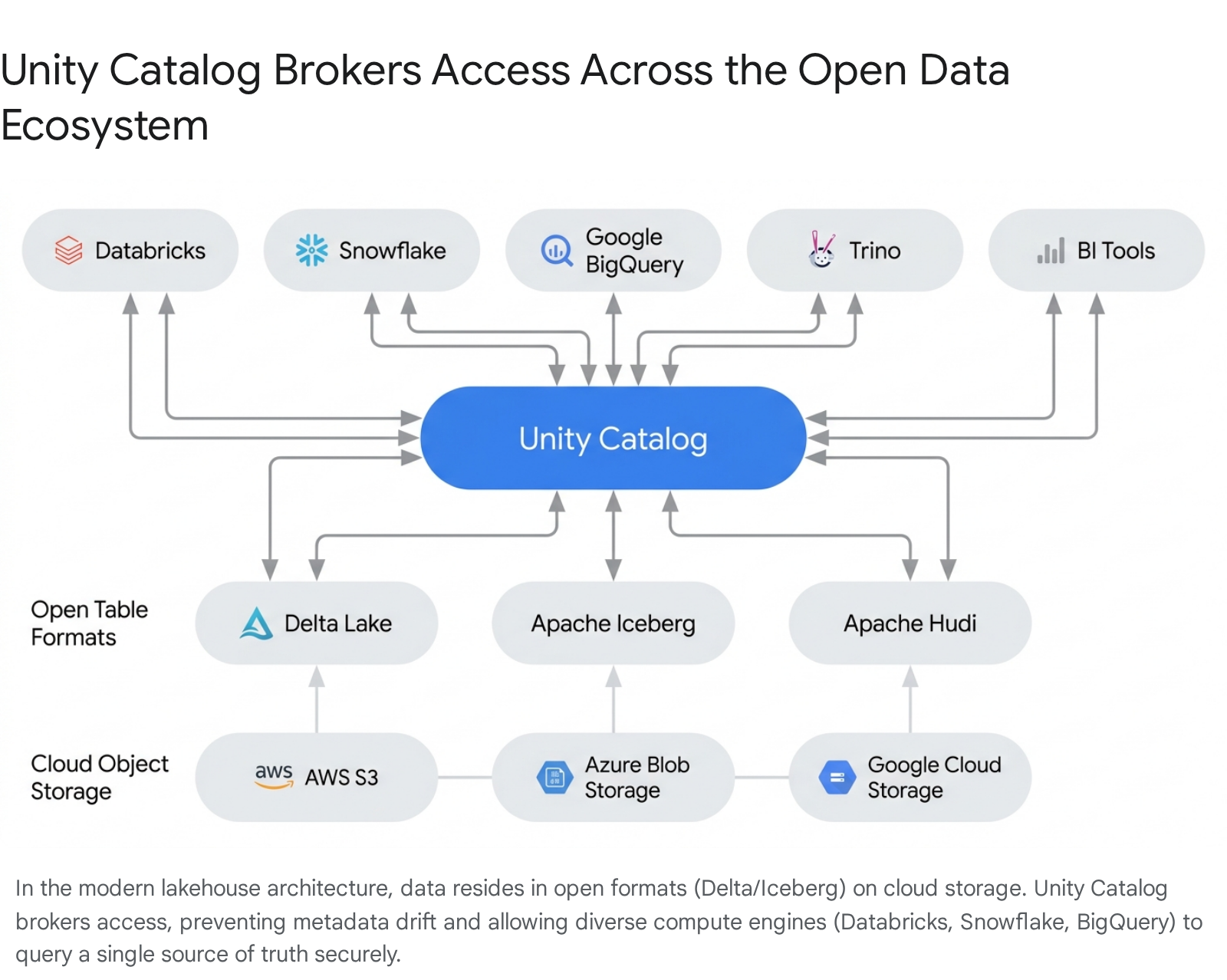

By 2026, the industry consensus concluded that open table formats had decisively won the storage layer architecture war. Enterprise customers overwhelmingly rejected vendor lock-in at the storage layer, demanding the ability to query a single, centralized copy of data using multiple, interoperable compute engines - including Databricks, Snowflake, Google BigQuery, and Trino - without duplicating data or incurring synchronization overhead 232433.

In response to this market demand, Snowflake conceded its strictly proprietary storage stance by adopting Apache Iceberg, an alternative open format 2324. Snowflake expanded its open-source presence by launching Polaris Catalog, a vendor-neutral catalog supporting both Iceberg and Delta Lake formats 24.

Databricks maintained its competitive advantage by introducing Delta Universal Format (UniForm). UniForm technology automatically maintains Iceberg metadata alongside Delta metadata, allowing data written natively as Delta tables to be instantly readable by any Iceberg- or Hudi-compatible engine 2433. The implications of this interoperability fundamentally shift the competitive battleground: if raw data resides in universal open formats accessible by any vendor, the primary differentiator transitions from storage protocols to the overarching governance layer and the speed and cost-efficiency of the compute engines built on top 2333.

Unity Catalog and Managed Storage Dominance

To fortify its open-source position, Databricks invested heavily in Unity Catalog, its unified data governance solution. Within the Databricks ecosystem, engineers must choose between creating "external tables" (where the user manages the storage path) and "managed tables" (where Unity Catalog fully controls data placement and lifecycle management) 2728. Databricks explicitly recommends Unity Catalog managed tables to optimize storage costs, enhance query speeds via AI-powered file size compaction, and enforce fine-grained access controls 272829.

A critical vulnerability in early decentralized data lakes was the "split-brain" problem. When external compute engines wrote directly to Delta tables in object storage, catalog metadata - such as schema definitions - often silently diverged from the actual physical state of the table 30. Databricks resolved this fragmentation in 2026 with the general availability of "Catalog Commits."

By aligning Delta with Iceberg's catalog-oriented model, Unity Catalog now brokers all table accesses and acts as the centralized system of coordination 30. When Catalog Commits are enabled, every read and write operation streams directly through Unity Catalog, creating a consistent discovery and authorization model regardless of which external engine is interacting with the data 30. This architectural maneuver cements Databricks' moat: it champions open storage formats while centralizing operational authority within its proprietary - though open-API supported - governance catalog 2829.

Industry analysts consistently recognize the strength of this architectural convergence. Databricks maintained its position as a Leader in the Gartner Magic Quadrant for Cloud Database Management Systems, scoring highly in the Lakehouse use case, while simultaneously securing top scores in the Forrester Wave for Data Lakehouses 232538. Furthermore, in 2025 benchmarking against Snowflake's generation-two warehouses, Databricks engineering published data indicating their SQL Serverless offering completed ETL benchmarks roughly 2.8x faster at substantially better price-to-performance ratios, widening the performance gap as concurrency and data volume grow 23.

Artificial Intelligence Workload Monetization

The rapid financial acceleration of both platforms in 2025 and 2026 is inextricably linked to generative and agentic artificial intelligence. The transition of AI from an experimental feature to a core driver of infrastructure consumption defines the next phase of competition. However, Databricks and Snowflake target distinctly different user personas and technical paradigms in their AI monetization strategies.

Databricks Machine Learning Engineering Ecosystem

Databricks has transitioned from a data processing engine to an AI-first platform, a pivot significantly accelerated by its $1.3 billion acquisition of MosaicML in 2023 3339. This strategy explicitly targets machine learning engineers and data scientists who require deep, code-first access to infrastructure to train, fine-tune, and deploy custom foundation models 31.

By Q4 of fiscal 2026, Databricks reported its AI products reached a $1.4 billion revenue run-rate, accounting for approximately 26% of its total revenue 31132. The platform's technical moat in AI relies on retaining the entire machine learning lifecycle - from raw data ingestion to fine-tuning domain-specific models like Databricks' open-source DBRX, to production inference - within the governed boundary of Unity Catalog 3331. This end-to-end lineage ensures precise tracking of which enterprise data feeds which models, serving as a critical differentiator against third-party model providers like OpenAI 3931.

Furthermore, Databricks aggressively expanded its addressable market by launching Lakebase, a managed serverless Postgres database engineered specifically to handle transactional (OLTP) workloads and act as the system of record for multi-agent applications 1424. Within its first six months of availability, Lakebase secured thousands of customers and outpaced the early revenue trajectory of Databricks' SQL data warehousing product 1. The tandem rollout of the "Genie" conversational AI assistant and "Agent Bricks" positions Databricks as a foundational operating system for building proprietary, context-aware AI agents directly atop enterprise data lakes 1423.

Snowflake SQL Ergonomics and Agentic Workflows

Snowflake's AI strategy operates on a different axis, prioritizing "SQL-first ergonomics" to target data analysts and business intelligence professionals rather than specialized machine learning engineers 31. Through the Snowflake Cortex suite, the company integrated powerful Large Language Model capabilities directly into SQL statements, allowing analysts to execute complex inference tasks - such as summarization, forecasting, and sentiment analysis - without leaving the familiar data warehouse environment or requiring complex infrastructure orchestration 3142.

The launch of Cortex Code (internally referred to as CoCo), an AI coding agent, served as the primary catalyst for Snowflake's Q1 FY27 revenue acceleration and subsequent upward guidance revision 91012. Reaching general availability in February 2026, Cortex Code rapidly penetrated over 7,100 accounts, shifting the narrative from AI experimentation to tangible revenue generation 91043.

Simultaneously, Snowflake Intelligence - a platform enabling agentic workflows to automate tasks across structured and unstructured enterprise data - more than doubled its adoption quarter-over-quarter, reaching over 2,500 accounts 933. Driven by consumption-based billing where every AI agent query directly increases compute expenditure, Snowflake reached a $100 million AI revenue run-rate a full quarter ahead of analyst expectations 133435. While Databricks commands a substantially larger absolute AI revenue base, Snowflake's successful integration of AI inference into its consumption model proves that analytical workloads are rapidly adopting generative capabilities 1020.

Ecosystem Consolidation and Mergers and Acquisitions

The competitive friction between Databricks and Snowflake has accelerated consolidation across the data infrastructure stack, as both platforms execute aggressive mergers and acquisitions to expand their capabilities and capture adjacent total addressable markets (TAM).

Snowflake Strategic Acquisitions

Snowflake has deployed capital strategically to enhance its platform functionality and defend against specialized point solutions. In January 2026, Snowflake completed the $596 million acquisition of Observe, bringing AI-powered observability for site reliability engineering directly into the Data Cloud 3637. This acquisition moves Snowflake into the multi-billion dollar observability market, structurally acknowledging that tracking data health and pipeline reliability is fundamentally a data processing problem 37.

Snowflake also acquired Crunchy Data for $165 million to integrate PostgreSQL capabilities, expanding its appeal to developers requiring robust transactional database support, and purchased Datavolo for $170 million to enhance multimodal and unstructured data pipelines - critical plumbing for advanced AI workloads 37. To further strengthen its Cortex Code offering, Snowflake acquired TensorStax, bolstering AI-driven data engineering capabilities within its developer environment 2136. Most recently, Snowflake announced a definitive agreement to acquire Natoma, an enterprise Model Context Protocol platform designed to extend governed agent actions across everyday business tools 1012.

Databricks Inorganic Growth

Databricks has matched Snowflake's acquisition velocity, focusing heavily on open-source format control and specialized AI infrastructure. Beyond the transformative $1.3 billion MosaicML acquisition, Databricks spent a reported $2 billion in 2024 to acquire Tabular, a data management company founded by the creators of Apache Iceberg 239. This acquisition was widely viewed as a defensive maneuver designed to maintain influence over the Iceberg ecosystem and outflank Snowflake's growing reliance on the format 2.

In 2025, Databricks acquired Neon, a serverless database company, to support emerging demands for agentic AI database provisioning, accelerating the technical foundation for the Lakebase product launch 2. The $4 billion Series L capital injection ensures Databricks retains substantial dry powder to pursue further strategic acquisitions, advance fundamental AI research, and aggressively expand its international go-to-market operations without requiring access to public markets 2418.

Regional Cloud Sovereignty and Data Residency

A critical macroeconomic variable increasingly dictating the architecture and consumption of cloud data platforms is the tightening regulatory landscape surrounding digital sovereignty, particularly within the European Union.

European Market Demand and Regulatory Pressures

According to Gartner projections, worldwide spending on sovereign cloud infrastructure is expected to reach $80.4 billion in 2026 385039. European sovereign cloud spending, in particular, is forecast to grow 83% year-over-year to $12.6 billion, driven by intense regulatory pressures, geopolitical volatility, and compounding enforcement of the General Data Protection Regulation (GDPR) 3850.

European enterprises, government agencies, and highly regulated industries are systematically reevaluating their reliance on US-based hyperscalers (AWS, Microsoft Azure, and Google Cloud) due to fundamental legal conflicts 38. The US CLOUD Act compels American companies to produce data upon valid US government demand regardless of where that data is physically stored, directly colliding with GDPR Article 48 regulations prohibiting unauthorized data transfers to non-EU authorities 38. As cumulative GDPR fines surpassed €7.1 billion by January 2026 and the EU Data Act intensified requirements for cloud provider switching, "geopatriation" shifted from a policy aspiration to a critical operational mandate 3839.

Vendor Approaches to Geopatriation

Both Databricks and Snowflake operate as higher-level abstraction layers atop the underlying hyperscaler infrastructure, offering unique mechanisms to help clients navigate sovereignty mandates and avoid vendor lock-in.

Snowflake addresses data residency through strict at-rest commitments, explicitly restricting customer data from leaving the deployed geographic region unless the client opts to leverage replication features 40. Snowflake's SnowGrid technology enables governed cross-cloud and cross-region data sharing, allowing multinational organizations to architect highly customized sovereign boundaries while maintaining a unified analytical interface 4041. Furthermore, Snowflake maintains dedicated government regions to satisfy rigorous public sector compliance standards 41.

Databricks leverages its deep open-source DNA to provide a different form of sovereignty defense. By utilizing Delta Lake formats and supporting deployment across all three major public clouds, Databricks inherently prevents lock-in to a single hyperscaler 342. Databricks aggressively expanded its physical footprint, managing 14 specific cloud regions across Europe by late 2025 42. The company heavily promotes Unity Catalog not just as a technical tool, but as a localized governance mechanism that provides transparency and predictability regarding where data is processed, enabling European enterprises to satisfy residency requirements without sacrificing access to advanced AI models 42.

Despite these vendor-level capabilities, a vast scale gap persists. US hyperscalers are collectively projected to invest roughly $600 billion in AI and cloud infrastructure globally in 2026, dwarfing independent European sovereign cloud initiatives like the European Commission's €180 million procurement tender 38. Consequently, data platforms like Databricks and Snowflake that can effectively broker security, unified governance, and AI compute while maintaining strict regulatory compliance across fragmented regional infrastructure will command significant and enduring market premiums.