Can AI Actually Predict the Stock Market

Artificial intelligence cannot predict the stock market with absolute certainty, but it can identify subtle historical patterns and fleeting market inefficiencies that provide a measurable statistical edge. While massive financial institutions leverage highly complex AI models to exploit microsecond anomalies, everyday investors are increasingly utilizing generative AI to gauge market sentiment and parse complex financial documents. However, the democratized access to these technologies has also sparked a surge in sophisticated investment scams, prompting global regulators to hastily build new frameworks to protect retail traders and ensure systemic market stability.

The Evolution of Empirical Asset Pricing

For decades, the field of empirical asset pricing has sought to understand the drivers of conditional expected returns. Academic finance traditionally views these expected returns as a "risk premium" - the compensation investors demand for bearing systematic, non-diversifiable risk 1. Historically, quantitative analysts relied on linear econometric models, breaking asset returns down into a conditional expectation term and a residual error term, typically utilizing a limited number of factors to measure an asset's exposure to underlying risks 1.

The advent of machine learning has fundamentally disrupted this classical approach. By synthesizing advanced computational methods with canonical problems in asset pricing, researchers have established new standards for predictive accuracy 2. A landmark, comprehensive study evaluating the efficacy of machine learning in forecasting United States stock returns analyzed a broad repertoire of methods, including generalized linear models, dimension reduction techniques, boosted regression trees, random forests, and deep neural networks 12. The empirical results demonstrated that machine learning consistently offers a vastly improved description of expected return behavior compared to traditional forecasting methods 23.

The Mechanics of the Machine Learning Advantage

The predictive gains achieved by machine learning models trace directly to their ability to capture complex, nonlinear interactions between predictor variables - nuances that traditional linear regressions simply miss 12. In highly efficient financial markets, relationships between macroeconomic indicators, firm fundamentals, and price momentum are rarely straightforward. Machine learning algorithms, particularly tree-based models and neural networks, excel at mapping these intricate, high-dimensional data landscapes 24.

Interestingly, within the realm of neural networks applied to financial data, researchers have found that "shallow" learning architectures often outperform "deep" learning models 1. When algorithms process panels of historical data encompassing past returns, moving average trading signals, and dozens of firm fundamentals, the best performing models rely heavily on a small set of dominant predictive signals 24. Regardless of the specific algorithmic architecture utilized, models generally agree that variations on momentum, liquidity, and volatility are the most potent predictors of future price movement 2.

To a layperson, the success metrics of these models might appear underwhelming. The aforementioned studies reported out-of-sample predictability - often measured as an R-squared value - of between 0.33% and 0.40% for neural network architectures containing one to four layers 1. However, in the context of institutional finance, these seemingly minuscule percentages translate into economically massive gains 1. Because financial markets are deeply competitive, even a fractional improvement in predictive accuracy can generate substantial portfolio alpha when applied to billions of dollars in assets under management 56.

Human Expertise vs. Artificial Intelligence

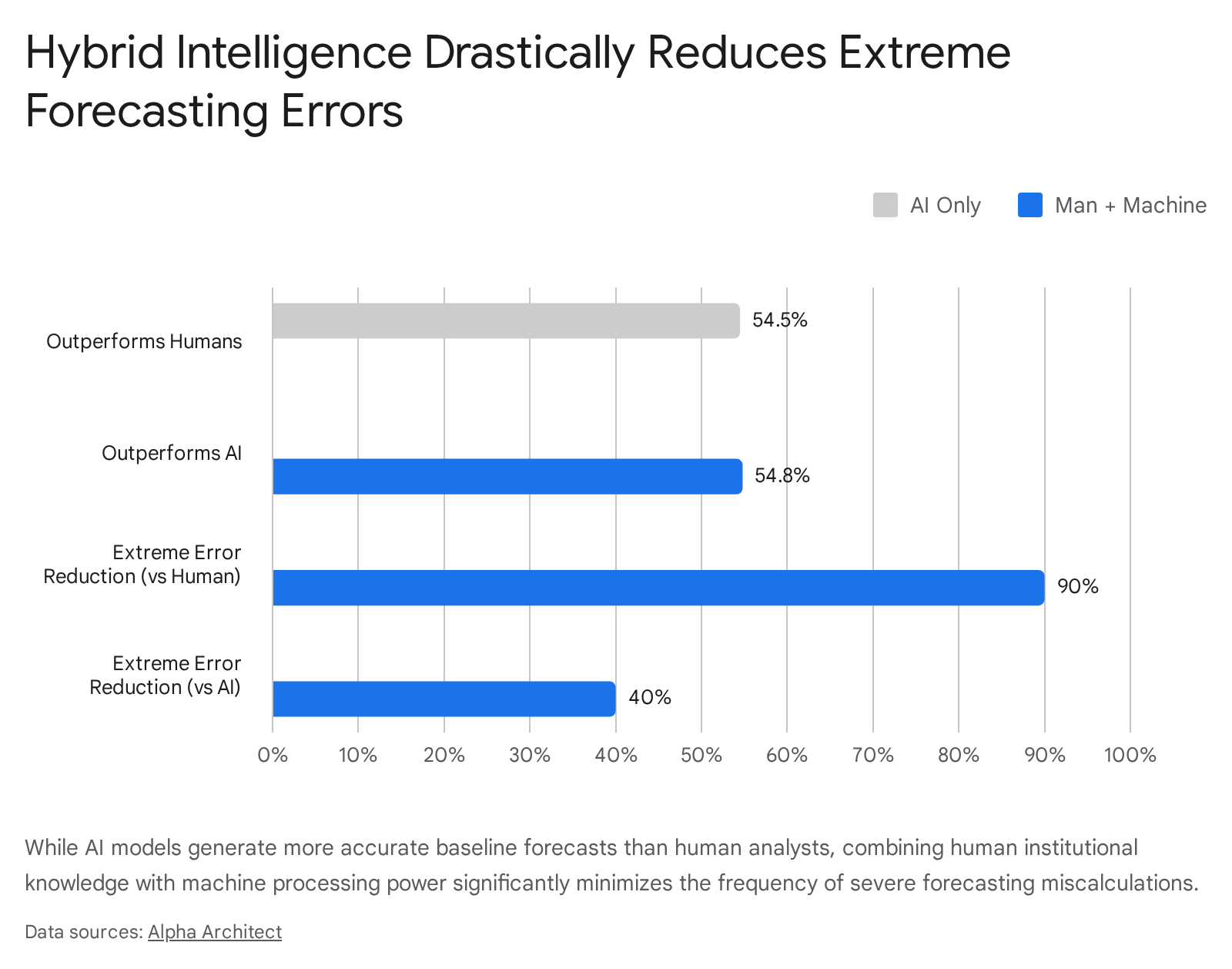

As machine learning algorithms achieve new benchmarks in predictive accuracy, the financial industry faces a critical question regarding the future of human analysts. A comprehensive 2024 study titled "From Man vs. Machine to Man + Machine" investigated this dynamic, analyzing firm-level variables, macroeconomic data, and textual information from corporate disclosures to determine whether algorithms have definitively surpassed human intuition 4.

The findings revealed that a pure artificial intelligence analyst model outperformed human analysts in 54.5% of stock return predictions over a seventeen-year sample period 4. The primary advantage of the machine learning model lies in its sheer processing capacity. Algorithms can instantly digest high-dimensional, unstructured data at a volume and speed that no human can replicate 4. Furthermore, the study adjusted the human forecasts to remove known psychological and cognitive biases, effectively creating a "debiased" human benchmark. Even against this optimized human standard, the artificial intelligence model maintained its superior performance in 54.5% of cases 4.

The Enduring Value of Institutional Knowledge

Despite the statistical edge of machine learning, human analysts retain distinct, irreplaceable advantages in specific market environments. The research indicated that human experts consistently outperform artificial intelligence when evaluating smaller, less liquid firms where clean, structured data is sparse 4. Humans also excel when analyzing companies heavily reliant on intangible assets, or businesses facing high distress risk and significant financial stress 4.

Fundamentally, machine learning models struggle in environments characterized by rapid, unprecedented changes or high competitive dynamics 4. Algorithms require historical patterns to make predictions; when an industry undergoes a structural paradigm shift, the historical data becomes obsolete. In these scenarios, human analysts utilize institutional knowledge, nuanced contextual understanding, and intuitive judgment to formulate accurate forecasts 47.

Because the strengths of algorithms and humans are highly complementary, the most effective approach in modern finance is hybrid. The "Man + Machine" model, which integrates human expertise with algorithmic processing, proved significantly more robust than either system operating in isolation. This combined model outperformed 54.8% of the forecasts made by the standalone artificial intelligence system 4.

Perhaps the most crucial benefit of this hybrid synergy is risk mitigation. The combination of human context and machine precision dramatically curtails severe forecasting miscalculations. The joint model avoided approximately 90% of the extreme errors typically made by human analysts, while simultaneously preventing 40% of the extreme errors generated by the artificial intelligence alone 4.

| Analytical Domain | Primary Advantage | Optimal Use Cases | Vulnerabilities |

|---|---|---|---|

| Traditional Human Analysis | Contextual reasoning and intuition | Micro-caps, distressed firms, intangible asset valuation | Susceptible to cognitive bias; unable to process massive datasets |

| Standalone Artificial Intelligence | High-dimensional data processing | Highly liquid, large-cap equities; identifying complex mathematical patterns | Underperforms during unprecedented market shifts; prone to specific algorithmic errors |

| Hybrid (Man + Machine) | Synthesizing scale with qualitative judgment | Comprehensive portfolio management and risk mitigation | Requires significant infrastructure to maintain seamless integration between quantitative models and human oversight |

Rethinking the Efficient Market Hypothesis

The successful application of artificial intelligence in predicting stock returns has forced economists to re-evaluate the Efficient Market Hypothesis (EMH). Established in its modern form by Eugene Fama in the 1970s, the EMH postulates that financial markets are perfectly efficient in incorporating information 98. In a strongly efficient market, asset prices instantaneously reflect all known public and private information, making it theoretically impossible for any investor or algorithm to consistently achieve excess returns 989.

If the strong form of the EMH were absolute reality, utilizing machine learning to uncover trading signals would be an exercise in futility. Prices would follow a random walk, rendering historical data useless for forecasting future movements 81013. However, professional traders and quantitative analysts generally operate under an adaptive or "semi-strong" interpretation of market efficiency 91011. They acknowledge that while markets are exceptionally efficient over long horizons, they are deeply flawed in the short term.

These short-term inefficiencies arise from human emotional reactions, structural delays in information processing, and asymmetric access to specialized data 9. Artificial intelligence does not invalidate the EMH; rather, it serves to illuminate the theory's practical limitations 99. Machine learning systems are explicitly designed to identify and exploit these fleeting anomalies 1015. Paradoxically, as algorithmic trading becomes ubiquitous and these tools instantly arbitrage away mispricing, they actually accelerate the speed of price discovery. In doing so, the widespread adoption of artificial intelligence may ultimately drive financial markets closer to the perfect efficiency described by the EMH 99.

The Challenge of Signal vs. Noise in a Non-Stationary World

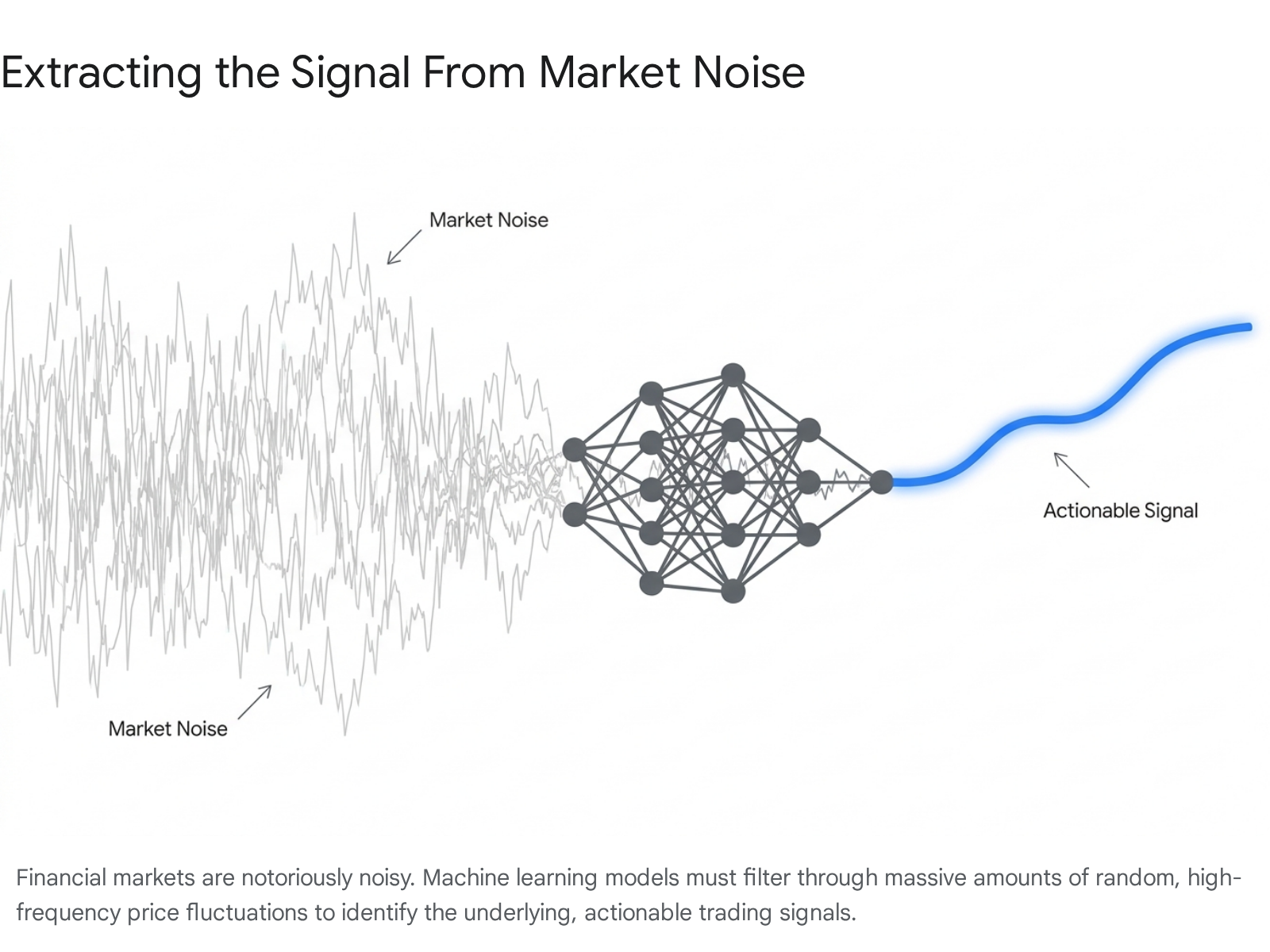

To understand why predicting the stock market is so exceptionally difficult, one must grasp the concepts of signal-to-noise ratios and non-stationarity. In fields like physics or electrical engineering, extracting a mathematical signal is a relatively clean process. In financial markets, the signal is buried under an avalanche of chaotic data 161718.

Defining Financial Noise

Quantitative analysts define the "signal" as the fundamental, meaningful information that dictates an asset's true expected return over time. "Noise," conversely, represents the random, meaningless price fluctuations driven by temporary supply and demand imbalances, market microstructure mechanics (such as bid-ask spreads), and the reactionary behavior of algorithmic trading bots 161718.

The signal-to-noise ratio in financial data is shockingly low. Experts estimate that in high-frequency trading environments, the ratio is frequently 10:1 or worse. This implies that approximately 90% of the tick-by-tick data observed in the market is essentially random noise 17. Filtering out this noise to reveal a persistent, actionable trend requires immense computational power and sophisticated mathematical decomposition, such as wavelet analysis, which separates time series data into different frequency components without losing temporal localization 17.

The Reality of Non-Stationarity

If noise were the only issue, powerful algorithms would eventually solve the market. The insurmountable barrier to perfect prediction is "non-stationarity." In statistics, a stationary process is one whose fundamental properties - like its mean and variance - do not change over time 1220. Traditional probability theory relies heavily on the assumption of stationarity to make reliable forecasts.

Financial markets are profoundly non-stationary 13122021. The underlying rules governing the market are continuously shifting due to macroeconomic policy changes, geopolitical shocks, technological innovations, and evolving regulatory landscapes 1721. A predictive model trained meticulously on data from the low-interest-rate environment of the 2010s will fail spectacularly in the inflationary environment of the 2020s because the fundamental distribution of outcomes has changed 1220.

Because the financial landscape is constantly evolving, algorithmic models that assume stationarity frequently underestimate the probability of extreme tail risks, such as sudden market crashes 12. Successful quantitative finance does not require predicting the exact future; it requires managing this non-stationary uncertainty better than the competition, exploiting small statistical edges while recognizing that the rules of the game will inevitably change 171220.

Institutional Power vs. Retail Democratization

The application of artificial intelligence has dramatically reshaped the competitive dynamics between elite institutional investors - such as hedge funds and investment banks - and independent retail traders. Historically, institutions operated on an entirely different playing field, utilizing sophisticated infrastructure and premium market intelligence that ordinary individuals could not access 222324.

The High-Frequency Institutional Edge

Institutions currently account for an estimated 70% to 90% of daily trading volume, and their dominance is heavily rooted in structural and technological advantages 2225. Elite quantitative trading focuses largely on High-Frequency Trading (HFT). These strategies do not attempt to predict where an asset's price will be next week; rather, they hunt for "micro-anomalies" 1526. These anomalies are brief statistical discrepancies, order book imbalances, and latency arbitrage opportunities that exist for fractions of a second 1526.

To exploit these micro-anomalies, institutions invest millions in specialized infrastructure. They utilize Field-Programmable Gate Array (FPGA) chips and pay exorbitant fees for co-location services - placing their physical servers in the exact same data centers as the exchange matching engines 2226. This allows them to execute trades in microseconds (millionths of a second), creating an unassailable moat that no retail trader can cross 2226. Furthermore, institutional analysts rely on enterprise-grade software. The industry-standard Bloomberg Terminal costs approximately $31,980 per year for a single seat, providing deep access to fixed income data, dark pool activity, and integrated execution workflows 232728.

The Retail AI Revolution

Despite the institutional stranglehold on raw speed, artificial intelligence is democratizing access to sophisticated analytics and strategy automation. Retail investors, once limited to delayed data feeds and basic charting, can now deploy machine learning algorithms that react in milliseconds 222326.

The cost of accessing institutional-grade data has plummeted as a vibrant ecosystem of alternative platforms emerges. Modern retail quantitative analysts construct their technical stacks using a variety of cost-effective tools. Platforms like Koyfin or TIKR provide comprehensive fundamental data and global screening capabilities for a fraction of Bloomberg's cost, often ranging from free tiers to $199 per month 293031. For charting and technical analysis, tools like TradingView offer advanced scripting capabilities 293031. Meanwhile, specialized artificial intelligence platforms, such as NowNews or Hudson Labs, allow retail users to automate the parsing of SEC filings, earnings call transcripts, and global news sentiment 2930. A retail investor can effectively replicate 80% to 90% of the functional utility of a $31,980 Bloomberg Terminal for less than $150 a month 2931.

Furthermore, retail investors possess unique structural advantages that massive institutions cannot replicate. A multi-billion-dollar fund cannot easily invest $50,000 into a promising micro-cap company; to make a meaningful impact on their portfolio, they must deploy tens of millions of dollars, which immediately drives up the asset's price and alerts the market 25. Retail algorithms can quietly exploit these illiquid corners of the market 25. Additionally, individual traders are immune to the career risk that plagues institutional portfolio managers, and they do not face the threat of forced liquidations during market panics caused by sudden client redemption requests 25.

| Feature | Institutional High-Frequency Trading | Retail Algorithmic Trading |

|---|---|---|

| Execution Latency | Microseconds | Milliseconds to seconds |

| Technological Infrastructure | Co-located servers, FPGA chips, Direct Market Access | Standard desktop PCs, Cloud VPS, API integrations |

| Primary Trading Strategies | Arbitrage, market making, exploiting micro-anomalies | Trend following, swing trading, macroeconomic sentiment analysis |

| Core Software Expense | ~$31,980 annually per seat (Bloomberg Terminal) 2728 | < $150 monthly (Koyfin, TradingView, AI plugins) 2931 |

| Market Impact Profile | High risk of slippage; trades heavily influence asset pricing | Nimble execution; orders easily absorbed by market liquidity |

Generative AI and the Sentiment Game

While historical price data and technical indicators form the backbone of quantitative analysis, the stock market is ultimately driven by human psychology. Periods of extreme market volatility are heavily influenced by fear, greed, and shifting public perception 13. Historically, assessing this "market mood" was a manual, subjective process reliant on lagging economic indicators or tedious media analysis 13.

Generative artificial intelligence and Large Language Models (LLMs) have revolutionized sentiment analysis by allowing machines to quantify massive volumes of unstructured qualitative data in real time 131434. These algorithms continuously scrape and process diverse data streams, including dense SEC filings, live earnings call transcripts, financial news publications, and vast social media networks like Twitter 1334.

The algorithms utilize Natural Language Processing (NLP) to dissect the syntax and context of this text, assigning precise polarity scores to determine whether the prevailing narrative surrounding a specific asset is bullish, bearish, or neutral 1336. This data is then fed directly into predictive trading models. Research has demonstrated that hybrid models - which integrate traditional technical indicators with AI-derived sentiment data - consistently outperform models relying solely on numerical price data 6131437. This advantage is particularly pronounced during periods of market stress or sudden geopolitical events, where historical price patterns offer little guidance, and rapid sentiment shifts dictate immediate price action 63437.

The Dark Side: AI Trading Scams and Fraud

As public fascination with artificial intelligence has surged, malicious actors have weaponized the technology to orchestrate sophisticated frauds against retail investors. Global regulatory bodies are battling an explosion of AI-enabled financial scams, issuing urgent warnings regarding the severity of the threat 151617.

A primary tactic is "AI washing," wherein unregistered platforms falsely claim their trading bots utilize proprietary neural networks to generate guaranteed, risk-free returns 151618. These platforms frequently employ aggressive social media marketing and high-pressure sales tactics to target novice investors 1518. In reality, these algorithms either do not exist or are mere facades for traditional theft. Deposited funds are rarely invested in actual markets; instead, they are funneled directly into offshore criminal accounts. When victims attempt to withdraw their fabricated profits, they are hit with demands for fraudulent "release fees" 15184243.

The sophistication of these schemes has escalated due to generative AI. Scammers routinely deploy "deepfake" audio and video technology to clone the voices and likenesses of prominent corporate executives, celebrities, or government officials 15174419. These deepfakes are used to disseminate false market news in order to manipulate micro-cap stock prices in classic pump-and-dump operations, or to artificially endorse fraudulent crypto-asset exchanges 15174244.

The scale of this algorithmic fraud is unprecedented. In Australia, the Australian Securities and Investments Commission (ASIC) coordinated the takedown of 11,964 phishing and investment scam websites in 2025 alone - a staggering 90% increase from the previous year, equating to over 30 site removals every single day 1746. Younger demographics are particularly susceptible to these operations. Studies indicate that nearly a quarter of Generation Z individuals own cryptocurrency, and a significant portion base their financial decisions heavily on advice from social media "finfluencers" and artificial intelligence chatbots 424347. Scammers exploit this trust by infiltrating encrypted messaging apps like WhatsApp to push fraudulent trading tips directly to victims 4243.

Global Regulatory Responses

The rapid integration of artificial intelligence into algorithmic trading, coupled with the exponential rise in digital fraud, has forced financial regulators worldwide to rapidly overhaul their oversight frameworks. Authorities are attempting a delicate balancing act: fostering technological innovation and market efficiency while simultaneously safeguarding consumer protection and mitigating the risk of systemic market failure 2021.

The European Union: MiFID II and the AI Act

In the European Union, the regulatory approach is increasingly comprehensive, bridging existing financial directives with newly enacted digital frameworks. The European Securities and Markets Authority (ESMA) provides oversight based on the Markets in Financial Instruments Directive (MiFID II) 2050. ESMA has issued strict guidance emphasizing that investment firms remain entirely accountable for their algorithmic systems, regardless of whether those systems are developed internally or outsourced to third-party artificial intelligence providers 2051.

The regulatory landscape is further complicated by the implementation of the landmark EU AI Act 5052. While certain financial applications - such as credit scoring or biometric identity verification - are strictly classified as "high-risk" under the AI Act, general algorithmic trading currently faces slightly less stringent categorization 515354. Nevertheless, ESMA requires firms to rigorously test their models to prevent algorithmic bias, ensure data privacy, and maintain transparency to prevent "opaque decision-making" where human operators cannot explain an algorithm's actions 2050. Crucially, under the combined force of the EU AI Act, the Digital Operational Resilience Act (DORA), and the Markets in Crypto-Assets (MiCA) regulation, accountability for technological risk is being elevated directly to the corporate board level, shifting the burden of oversight far beyond basic IT compliance departments 53.

India: The SEBI Algorithmic Framework

Facing a massive surge in retail algorithmic trading participation, the Securities and Exchange Board of India (SEBI) enacted highly stringent rules in 2025 aimed specifically at curbing unregulated, opaque trading bots 555657.

To protect retail investors from untested software, SEBI mandated that no algorithmic strategy can go live in the Indian market without explicit prior approval from the stock exchanges 5859. The regulator strictly differentiates between "white-box" algorithms - which operate on clear, logical rules (e.g., executing a trade when a specific technical indicator reaches a certain threshold) - and complex "black-box" models, which face significantly higher scrutiny 5759. Every approved algorithm is assigned a unique tracking ID that tags every order it generates, ensuring total traceability 5859. Furthermore, brokers are explicitly designated as the ultimate gatekeepers, holding full responsibility for any algorithmic strategy deployed by their clients 5658. To combat cyber threats and unauthorized access, SEBI also mandated rigorous security protocols, including Two-Factor Authentication (2FA) and static IP address requirements for any Application Programming Interface (API) connection to the exchanges 5558.

Contrasting Approaches in China and Japan

Regulatory philosophies across major Asian markets present a stark contrast in their approach to financial technology. In China, the primary focus remains on maintaining absolute market stability and preventing systemic manipulation. The China Securities Regulatory Commission (CSRC) has publicly committed to cracking down on automated program trading, viewing the unchecked proliferation of algorithms as a direct threat to market order 22. Chinese regulations lean heavily toward centralized oversight, stringent cross-border data controls, and comprehensive filing obligations to ensure state visibility into algorithmic operations 2223.

Conversely, Japan has adopted a deliberately "innovation-friendly" posture. Rather than drafting sweeping, restrictive laws specific to artificial intelligence, Japan's Financial Services Agency (FSA) relies on existing, technology-neutral legal frameworks 212324. The FSA actively supports the integration of algorithms into the financial sector to boost global competitiveness 2124. However, Japanese regulators are increasingly focused on consumer protection issues unique to modern technology, specifically the phenomenon of AI "hallucinations" - where generative models confidently present entirely fabricated financial data to users. This poses a significant danger as retail investors increasingly rely on autonomous chatbots for investment advice 24.

Systemic Fragility and the Threat of Feedback Loops

Underpinning all global regulatory efforts is a deep-seated fear of systemic market fragility. Regulators remain haunted by the memory of the 2010 Flash Crash, an event where a single, flawed algorithmic sell order triggered a cascading chain reaction across high-frequency trading systems, erasing nearly $1 trillion in United States market value in a matter of minutes 25.

As modern artificial intelligence models become increasingly interconnected, researchers warn that the risk of a similar event is intensifying. In a market dominated by algorithms, a minor data error or a misinterpreted news headline in one system can trigger aggressive, self-reinforcing feedback loops across thousands of competing bots 25. The speed at which these algorithms operate means that a catastrophic market decline can occur before human circuit breakers have the opportunity to intervene, underscoring the critical need for robust, globally coordinated algorithmic risk management 25.

Bottom line

Artificial intelligence represents a profound leap forward in the ability to process massive datasets, quantify market sentiment, and execute trades with microsecond precision. However, it cannot predict the future with perfect accuracy, largely due to the non-stationary, deeply chaotic nature of financial markets. While institutional investors utilize advanced machine learning to capture fleeting micro-anomalies, retail traders are leveraging accessible generative AI tools to close the analytical gap and manage risk more effectively. Despite these advancements, the democratization of algorithmic trading carries significant dangers; investors must remain highly vigilant against a rising tide of sophisticated, AI-driven financial scams and the ever-present threat of systemic market volatility.