Capital allocation for disruptive internal ventures in incumbent firms

The failure of leading incumbent firms to sustain dominance in the face of technological or market disruption is rarely a consequence of technological incompetence or an inability to generate innovative ideas. Rather, organizational inertia is frequently the byproduct of rational, well-executed capital allocation processes that systematically starve disruptive internal ventures of appropriate funding. The theoretical framework surrounding this phenomenon relies heavily on the dichotomy of "good money" versus "bad money." Adapted from classical monetary theory into the realm of corporate strategy, this paradigm provides a comprehensive lens through which to understand how traditional financial metrics, managerial incentives, and corporate venture structures inadvertently sabotage breakthrough innovations by imposing the wrong expectations at the wrong time.

Historical and Theoretical Foundations of Capital Allocation

To understand the funding constraints on internal corporate ventures, it is necessary to trace the origins of the "good money" versus "bad money" concept and its translation from macroeconomic theory to corporate strategic management. The terminology is not merely colloquial; it represents a fundamental economic law concerning the circulation of value.

The Macroeconomic Origins of Gresham's Law

The conceptual root of good versus bad money lies in Gresham's Law, a monetary principle stating that "bad money drives out good" 2. Named in 1860 by the economist Henry Dunning Macleod after Sir Thomas Gresham, a sixteenth-century English financier, the phenomenon itself has ancient origins 21. Historical records of commodity money manipulation, such as the debasement of the silver Denarius in the Roman Empire and similar practices in ancient Greece referenced by Aristophanes, demonstrate that when a government artificially overvalues one type of currency and undervalues another, public behavior predictably shifts 1.

Under these conditions, the public will systematically hoard the undervalued "good" money - currency possessing high intrinsic commodity value - and aggressively circulate the overvalued "bad" money, such as debased coinage or unbacked fiat 1. As a result, the superior currency is effectively driven out of the open market, leaving the economic system dominated by the inferior medium of exchange. In modern fiat systems, similar dynamics emerge when highly regulated "safe assets" issued by commercial banks compete with novel monetary liabilities issued by unregulated payment platforms or decentralized entities, creating complex regulatory challenges regarding monetary credibility 23.

Application to Corporate Capital and Short-Termism

In the context of organizational behavior, corporate strategy, and financial markets, Gresham's macroeconomic principle serves as a potent operational metaphor for resource allocation and internal investment 24. As noted by central banking authorities, including former Bank of England Executive Director Andrew Haldane, Gresham's Law effectively models the deleterious effects of short-termism in modern financial markets 2. When financial systems disproportionately reward impatient, short-term speculation, these activities drive out patient, long-term capital investment.

Within an established corporation, capital allocated to sustaining innovations - projects that improve existing products for current customers and offer predictable, immediate, high-margin returns - acts as the dominant, overvalued currency. Because the organization's incentive structures and performance metrics heavily reward these immediate, low-risk returns, capital designated for long-term, highly uncertain, exploratory projects is either hoarded, misallocated, or fundamentally altered to mimic the characteristics of short-term sustaining capital 24. Consequently, opportunistic and self-centered organizational behaviors emerge at the managerial level. These behaviors prioritize immediate divisional returns over long-term enterprise renewal, effectively allowing the "bad" short-term money to drive out the "good" exploratory money required for disruptive innovation 4.

The Mechanics of Good Money and Bad Money

The most precise application of the Gresham dynamic to corporate innovation was formulated by researchers studying the innovator's dilemma. In evaluating why incumbent firms struggle to incubate disruptive ventures, the critical variable identified is not the absolute volume of capital provided to the venture, but rather the specific financial expectations attached to that capital 5.

Characteristics of Patient Capital

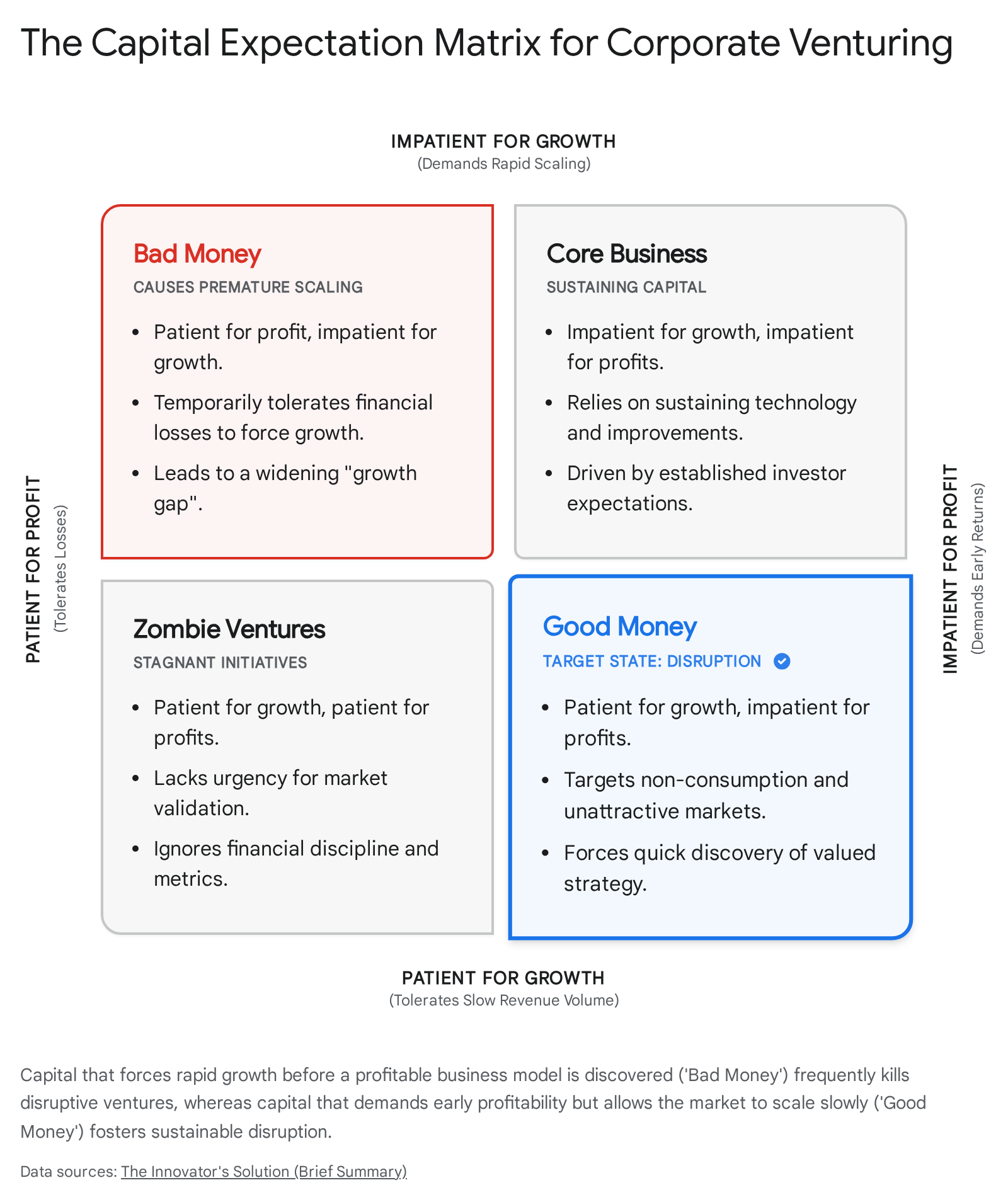

In this specialized framework, "good money" is defined as capital that is strictly patient for growth but highly impatient for profit 5. Disruptive innovations typically begin in small, undefined markets serving non-consumers or low-end customers who find existing solutions too expensive or complex 678. Because the ultimate trajectory of the new market is entirely unknown, the venture must iterate rapidly to discover a viable, profitable business model before exhausting its funding. Good money enforces operational discipline by demanding early profitability - proving that the unit economics function successfully - while allowing the total revenue volume to remain small while the nascent market develops organically 56.

Conversely, "bad money" is defined as capital that is impatient for growth but patient for profit 5. Incumbent firms, driven by the need to satisfy public market expectations and maintain overall corporate growth rates, require new ventures to move the financial needle for the multi-billion-dollar parent company. Consequently, executives force internal ventures to scale prematurely. They tolerate prolonged financial losses and negative unit economics under the flawed assumption that aggressive capital injection will manifest a massive market 59.

The Five-Step Process of Capital Degradation

The transformation of good money into bad money follows a predictable five-step sequence within established organizations 5: 1. Success Leads to Over-Focus: The organization achieves significant success in its core business, leading to an over-concentration of resources on sustaining the existing core product line. The organization ignores nascent, highly uncertain new-growth businesses that appear financially immaterial 5. 2. Failure to Meet Expectations: Because early-stage growth opportunities were systematically ignored during periods of high profitability, the firm eventually faces a growth gap when the core business matures. The firm subsequently fails to meet the expanding growth expectations modeled by market investors 5. 3. Impatience for Growth: Facing intense external pressure to reignite top-line expansion, the capital available for internal ventures abruptly shifts from patient to impatient, demanding immediate, large-scale revenue from nascent projects 5. 4. Tolerating Losses: To achieve this unnatural growth rate in unproven markets, corporate executives begin to temporarily tolerate severe financial losses, subsidizing the venture in a desperate bid to acquire scale and market share rapidly 5. 5. Increasing Losses and Growth Gaps: Attempting to force disruptive ideas through the predictable, rapid trajectory of a sustaining technology proves vastly more difficult and expensive than anticipated. This results in escalating corporate losses, abrupt project termination, and a widening organizational growth gap that leaves the firm vulnerable 5.

Financial Metrics and the Penalty on Disruption

The structural inability of incumbent firms to provide "good money" is deeply embedded in the standard financial accounting metrics used to allocate corporate resources. Traditional valuation methodologies systematically penalize disruptive innovation while overwhelmingly favoring sustaining improvements.

Discounted Cash Flow and Hurdle Rates

Corporate capital allocation relies heavily on quantitative tools such as Discounted Cash Flow (DCF) analysis and Internal Rate of Return (IRR) to evaluate competing internal funding proposals 1011. These specific metrics are inherently biased against disruptive internal ventures.

Disruptive innovations target unproven markets with uncertain adoption curves, meaning their early cash flows are typically minimal or distinctly negative. The bulk of their potential financial return is weighted heavily in the distant future 610. When these distant cash flows are discounted to the present value - incorporating a high discount rate to account for the extreme risk of the unknown market - the net present value (NPV) of a disruptive project consistently calculates to zero or less. By comparison, sustaining innovations target known customers with predictable demand, generating reliable, near-term cash flows that easily survive the mathematical discounting process 11.

Furthermore, corporate finance departments establish rigid hurdle rates for all new investments. A disruptive venture, attempting to serve a low-end market or non-consumers with a cheaper, simpler product architecture, naturally exhibits lower initial gross margins 78. Consequently, internal ventures fail to clear the established corporate hurdle rates. To secure necessary funding, venture leaders are forced to manipulate their business plans, inflating revenue projections or aggressively altering the product architecture to appeal to the organization's existing, high-margin customer base 511. This process - known as "cramming" a disruptive idea into a sustaining business model - strips the venture of its disruptive potential 11.

Return on Assets and Asset-Light Biases

Return on Assets (ROA) creates an additional, highly specific internal force that transforms corporate funding into "bad money." Executives compensated primarily on ROA metrics are heavily incentivized to outsource asset-intensive processes and focus internal capital strictly on high-margin, asset-light stages of the industry value chain 5.

While this financial engineering rapidly improves short-term ratios and satisfies public market analysts, it blinds the organization to emerging layers of the value chain where attractive future profits are migrating. Internal ventures requiring capital-intensive exploration - such as deep technology development or new hardware manufacturing capabilities - are routinely denied funding because their necessary initial expenditures temporarily depress the overall corporate ROA 514. This ensures that the firm remains paralyzed in its legacy operating model, maximizing current asset efficiency at the cost of future survival.

| Financial Metric | Impact on Sustaining Innovation (Core Business) | Impact on Disruptive Internal Venture (Exploratory) | Consequent Capital Allocation Behavior |

|---|---|---|---|

| Discounted Cash Flow (DCF) | Highly favorable; near-term predictable cash flows yield high NPV. | Highly punitive; distant, uncertain cash flows are mathematically zeroed out. | Capital demands near-term certainty, rejecting nascent markets and prolonged R&D. |

| Hurdle Rates / IRR | Easily met through incremental price increases to existing premium clients. | Rarely met; disruptive products initially offer lower margins and target lower-tier clients. | Forces venture teams to alter products to target existing high-end clients ("cramming"). |

| Return on Assets (ROA) | Encourages rapid outsourcing and optimization of existing legacy assets. | Discourages necessary capital-intensive capability building for new technological paradigms. | Starves deep-tech or hardware-heavy ventures of necessary patient capital. |

| Market Sizing (TAM) | Total Addressable Market is known and easily quantifiable by industry analysts. | TAM is zero or unquantifiable because the market does not yet exist. | Funding is strictly withheld until quantitative proof of a large market is fabricated. |

Internal Resource Allocation and the Managerial Filter

The realization of the "bad money" phenomenon occurs at the intersection of executive strategic intent and operational reality, a dynamic thoroughly mapped by the Bower-Burgelman resource allocation model 1213.

The Bower-Burgelman Model of Strategic Behavior

Strategic direction in large, complex corporations is rarely a pure top-down mandate executed perfectly by subordinates. Instead, as the Bower-Burgelman framework outlines, strategy is effectively determined by the actions of middle managers who act as a critical organizational filter 1112. These managers decide which operational-level, autonomous strategic initiatives will be actively championed to the executive suite for funding, and which will be suppressed 121314.

The resource allocation process highlights that strategy-making is an intrinsically intertwined social learning process. Entrepreneurial participants at the product or market level conceive new business opportunities and engage in strategic forcing efforts to create momentum 1214. However, they rely entirely on middle managers to navigate the structural context of the firm to secure necessary capital.

Middle Management Incentives and Asymmetric Risk

Middle managers operate under a strict, often unforgiving incentive structure; their career progression, compensation, and institutional prestige depend on successfully backing winning projects and avoiding high-profile financial failures 41112.

When an operational team develops a genuinely disruptive idea, the middle manager must evaluate its potential against alternative sustaining projects. The sustaining project offers clear historical data, immediate demand from major corporate clients, and high, predictable margins 59. The disruptive project requires "good money" - a willingness to endure low initial revenue, a tolerance for high ambiguity, and patience for growth. Because the overarching corporate incentive structure punishes long-term ambiguity and rewards immediate growth, the middle manager rationally chooses to kill the disruptive project or demands that the venture team rewrite the proposal to promise immediate, massive scale 1118.

Thus, the very architecture of internal resource allocation guarantees that disruptive ventures are subjected to "bad money" constraints before they even reach the executive board for review. Opportunistic behaviors spread, leading to a prioritization of safe, incremental improvements that guarantee quarterly bonuses but leave the firm vulnerable to external disruption 4.

Structural Interventions and Corporate Venturing

Recognizing the innate hostility of the core business environment to disruptive innovation, incumbents frequently attempt structural interventions. The most common approach is the establishment of Internal Corporate Ventures (ICVs) or Corporate Venture Units (CVUs).

The Paradox of Internal Corporate Ventures

ICVs are structurally differentiated, semi-autonomous organizational units designed specifically to incubate new businesses away from the crushing demands of the core's financial metrics 151617. The theoretical goal of an ICV is to create a secure, ring-fenced haven where "good money" can be deployed patiently 1718.

However, ICVs suffer from a fundamental and persistent operational paradox 16. To survive the initial incubation phase, the ICV requires profound structural and operational independence. It must emulate the external entrepreneurial ecosystem to test highly novel, disruptive models without the bureaucratic drag of the parent firm 16. Yet, the greater the separation from the mainstream organization, the more difficult it becomes for the parent company to comprehend, legitimize, and ultimately integrate the venture once it achieves viability 16.

If the ICV remains highly independent, it risks being perceived by mainstream executives as an alien entity consuming resources without contributing to the core's immediate bottom line. This makes the unit highly vulnerable to sudden elimination during corporate budget cuts or shifts in strategic leadership 17. Conversely, if the ICV is integrated too closely to maintain internal legitimacy and secure ongoing funding, it is inevitably forced to adopt the parent's "bad money" metrics. The parent organization demands synergy, immediate scale, and adherence to existing strategic frameworks, which effectively neutralizes the ICV's disruptive capability and turns it into just another sustaining engineering department 1518.

Organizational Ambidexterity Approaches

To manage this paradox, modern management theory emphasizes the necessity of organizational ambidexterity - the ability to simultaneously pursue both exploration (radical innovation) and exploitation (incremental improvement of existing capabilities) 192025.

Achieving ambidexterity requires a delicate balance of structural and contextual elements. Structural ambidexterity formally separates the exploratory units from the exploitative core to protect their distinct operational mandates 19. Contextual ambidexterity relies on specialized leadership and organizational culture, where top management teams (TMT) explicitly support and integrate the divergent activities without forcing uniform financial metrics across the board 1920. Some firms utilize a sequential approach, shifting organizational focus between exploration and exploitation over time, while others attempt a simultaneous approach, requiring intense collaboration and technology transfer between venture managers and middle-level managers 13. Regardless of the approach, without explicit, top-down protection of the distinct accounting and evaluation systems, the dominant logic of the core business will inevitably overwrite the rules of the ICV 131920.

The Role of Corporate Venture Capital

To completely bypass the internal resource allocation sieve and the middle-management filter, corporations increasingly utilize Corporate Venture Capital (CVC) to invest in external startups.

Investment Models and Strategic Alignment

CVC acts as an essential inter-organizational learning mechanism. It allows incumbents to access new technologies, scan the periphery for market disruptions, and expand business activities without the immediate friction of internal development 212722. CVC units are theoretically positioned to provide optimal "patient capital," allowing the parent to explore new markets passively while the external startup efficiently iterates on its business model using lean startup methodologies 2930.

The structural setup of CVCs varies widely, typically falling into three categories: a direct investment arm investing off the parent's balance sheet, a formalized fund structure with the parent as a captive limited partner (LP), or a spun-out fund incorporating various external LPs 30. Furthermore, CVC strategies generally align with four models: driving investments (high collaboration with operational involvement), enabling investments (supporting an ecosystem of complementary products), emergent investments (exploring new markets with capital and advisory support), and passive investments (focused purely on financial returns) 2923.

Corporate Venture Capital Incentive Misalignment

Despite the structural distance from the core business, CVCs frequently fall into the "bad money" trap due to shifting corporate mandates and deeply misaligned incentives. While traditional Venture Capital (VC) is driven purely by financial returns over a dedicated 7-to-10-year fund cycle, CVCs are heavily scrutinized for ongoing strategic alignment with the parent organization 302433.

If the parent company faces a macroeconomic downturn or a core business contraction, CVC units are intensely pressured to abandon exploratory, long-term emergent investments in favor of startups that provide immediate, tangible synergistic value to the existing product lines 2725. This dynamic forces the CVC to withdraw follow-on funding from truly disruptive external ventures, reinforcing the cycle wherein short-term strategic pressures drive out long-term exploratory capital. Furthermore, many corporations fail to establish specialized compensation structures for their venture managers. By tying CVC manager compensation to short-term corporate performance rather than the long-term success of the venture portfolio, parent companies incentivize the premature termination of funding for ventures that are not scaling rapidly enough to satisfy corporate leadership 2125.

Capital Intensity and the Deep Tech Funding Gap

The theoretical tension between good and bad money is currently undergoing a severe real-world stress test in the realm of "deep tech" - a category encompassing climate technology, advanced materials, next-generation hardware, and fundamental scientific breakthroughs.

The Software Scaling Paradigm

Over the last two decades, the venture capital ecosystem has been overwhelmingly dominated by software and Software-as-a-Service (SaaS) business models. These models require relatively low initial capital expenditures and have the capacity to scale revenue exponentially with minimal marginal costs 1426. This dynamic created a hyperscalable paradigm where venture capital firms became highly incentivized to prioritize rapid, short-term markups to justify management fees and raise subsequent funds 26.

This "Startup Industrial Complex" institutionalized "bad money" behavior across both traditional VC and CVC markets 26. Investors began demanding immediate commercial traction and rapid revenue scaling to justify continued funding, optimizing their portfolios for companies that could sprint to an exit or an inflated valuation within a few years 1426.

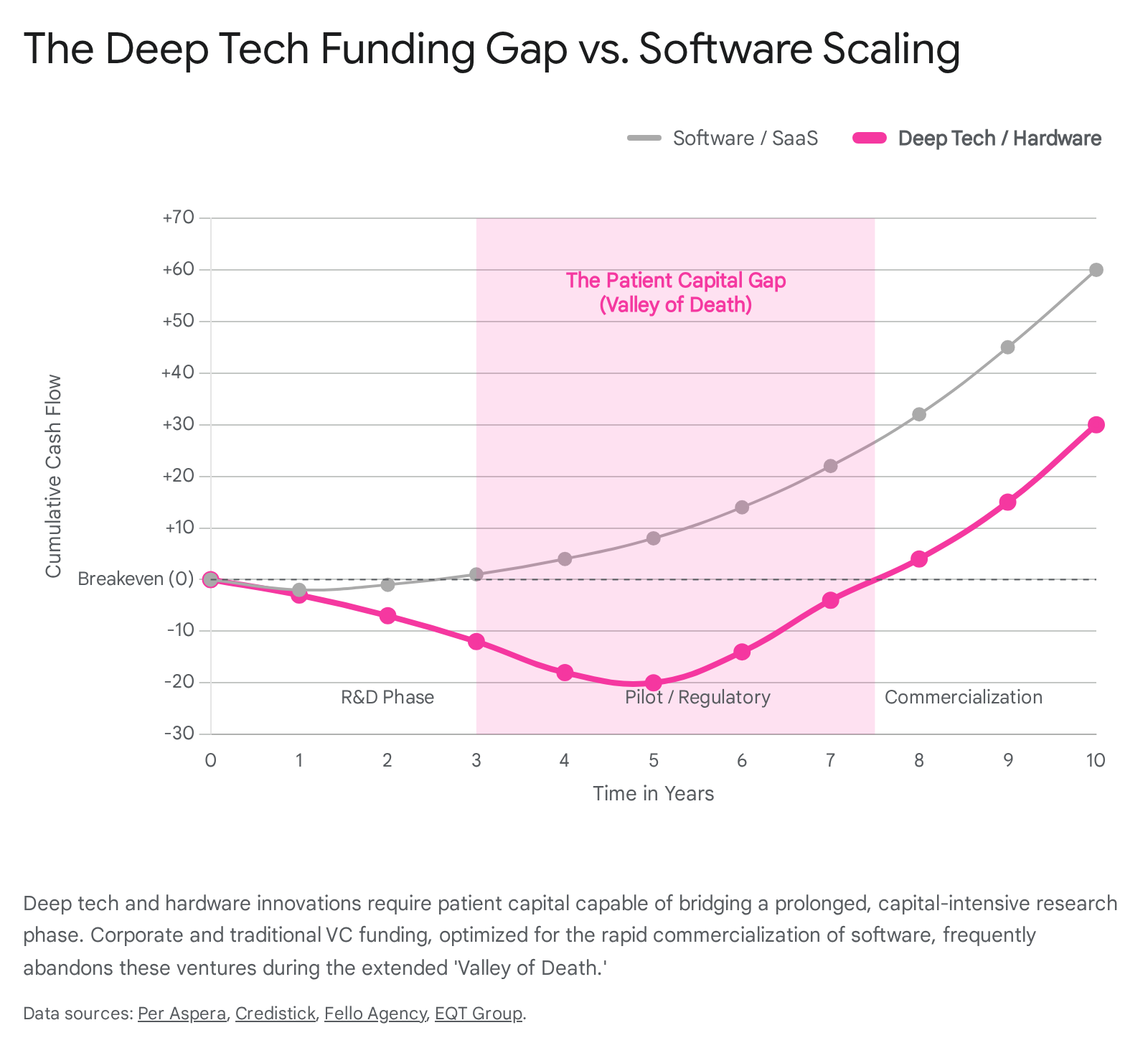

Deep Tech Hardware Timelines and the Valley of Death

Deep tech ventures operate on fundamentally different timelines and economic realities. Unlike software, deep tech requires massive capital intensity, extended research and development horizons, and significant regulatory navigation before commercialization is even possible 143637. For example, training advanced artificial intelligence models incurs direct computing costs between $78 million and $100 million, while developing first-of-their-kind Small Modular Reactors (SMRs) requires between $300 million and $2 billion in capital prior to regulatory approval and initial deployment 14.

The contemporary VC and CVC ecosystem is structurally misaligned with these requirements. Investors accustomed to the rapid feedback loops of software impose "bad money" expectations on deep tech founders, demanding fast paths to revenue and applying pressure for premature scaling 263637. When deep tech ventures inevitably face extended timelines, high cash burn rates, and lengthy technology-market fit validation cycles, impatient capital abandons them 36. This dynamic creates a severe funding gap, sidelining crucial technical advancements simply because they do not match the hyperscalable, low-capex financial models preferred by modern capital allocators 1426.

State-Backed Capital and Geopolitical Implications

The inability of standard corporate and venture capital models to supply patient "good money" for capital-intensive innovation has profound geopolitical ramifications. In economies dominated by state-backed enterprises (SOEs), innovation funding operates on vastly different time horizons and performance metrics 2728.

Subsidies and Patient Capital in State-Backed Enterprises

State capitalism theoretically cushions technological transitions by directing massive investment toward emerging strategic sectors without the immediate demand for quarterly public market returns 2829. Supported by direct government subsidies, heavily discounted state loans, tax rebates, and strategic domestic procurement frameworks, state-backed entities are positioned to deploy genuine "good money" 284142. This capital is deeply patient for commercial growth and heavily capitalized, oriented toward achieving long-term technological hegemony rather than short-term profitability 2942.

For example, China's aggressive industrial strategies, such as "Made in China 2025," rely heavily on SOEs to build dominance in advanced manufacturing, renewable energy, generic active pharmaceutical ingredients (APIs), and lithium-ion battery production 284142. By absorbing initial low-margin, high-capex penalties that Western ROA metrics would strictly prohibit, these state-backed enterprises establish formidable global supply chain dominance 4230.

Western Corporate Disadvantages in Capital-Intensive Sectors

Conversely, Western incumbents in Europe and the United States often struggle to fund disruptive clean energy transitions, advanced nuclear projects, or critical mineral developments due to strict internal capital allocation constraints and public market impatience 4130. The European Union, for instance, faces significant institutional fragmentation; while regions receive funding from structural funds, the lack of centralized, state-backed megaproject financing places European mid-caps and startups at a stark disadvantage against highly subsidized foreign competitors 2830.

This disparity highlights a critical vulnerability: the inability of Western corporate structures to isolate long-term "good money" from the "bad money" demands of quarterly capitalism severely limits their capacity to internalize generation-defining disruptions in heavy industry and hardware 4130.

| Capital Source / Enterprise Type | Primary Funding Mechanism | Time Horizon & Tolerance for Losses | Dominant Sector Success |

|---|---|---|---|

| Western Public Corporations | Internal cash flow, CVC, traditional private equity. | Short-term (Quarterly/Annual). Low tolerance for prolonged capex without rapid ROA improvement. | Asset-light software, incremental sustaining hardware, SaaS. |

| Traditional Venture Capital | 7-10 year closed-end funds driven by management fees and markups. | Medium-term. Tolerates early losses but demands rapid, hyperscalable revenue growth. | Consumer internet, B2B enterprise software, fintech. |

| State-Backed Enterprises (SOEs) | Direct state subsidies, below-market loans, protected domestic procurement. | Ultra Long-term (Decadal). High tolerance for massive capex and negative margins to secure strategic dominance. | Electric vehicle batteries, high-speed rail, generic APIs, clean energy infrastructure. |

Innovation Accounting as an Operational Solution

If traditional financial accounting transforms vital corporate capital into "bad money," resolving the internal venture struggle requires a fundamental restructuring of how progress is measured and funded. The operational antidote to the bad money problem is the adoption of "innovation accounting" within ambidextrous organizational structures 944.

Lagging Versus Leading Financial Indicators

Traditional financial accounting focuses heavily on lagging indicators: historical revenue, gross margin, return on investment (ROI), and EBITDA 44. Applying these mature metrics to a nascent disruptive venture inherently forces the venture into the "impatient for growth" paradigm 44. Because the financial outcomes of an unproven business model cannot be accurately modeled using historical data, demanding traditional pro formas guarantees that venture teams will fabricate data to secure funding, masking critical, untested assumptions as guaranteed facts 931.

Innovation accounting solves this systemic issue by measuring progress through leading indicators and the deliberate, quantified reduction of uncertainty 94446. Instead of asking, "What is the ROI of this venture over five years?", an innovation accounting framework asks, "How much capital is required to validate the core assumption of customer demand?" 4446.

Hypothesis Testing and Metered Funding

This approach closely mimics the metered funding mechanisms utilized in early-stage venture capital and mineral exploration industries. Innovation teams deploy minimal initial resources to test discrete hypotheses utilizing methodologies such as customer discovery interviews, paper prototyping, and rigorous A/B testing 9. Larger tranches of capital are only released as empirical evidence accumulates and confidence levels regarding the business model rise 9.

By explicitly quantifying the uncertain impact of investments in new capabilities and strategies rather than demanding immediate, massive scale, innovation accounting ensures that capital remains "patient for growth" 4447. Simultaneously, it enforces the "impatient for profit" rule by requiring ventures to prove unit economic viability and customer willingness-to-pay at a micro level before any capital is provided for mass commercialization 947. Pioneering models, such as the Amazon Working Backwards (AWB) approach, have proven successful in creating order in the naturally messy innovation process, actively mitigating the risk of early-stage failure by anchoring ventures tightly to validated customer pain points before significant capital is burned 3132.

When integrated within a structurally ambidextrous organization - where the core business relies on traditional accounting for execution, and exploratory units utilize innovation accounting for discovery - firms can successfully insulate their "good money" from the corrosive effects of the legacy business 131946.

Conclusion

The persistent struggle of incumbent firms to fund genuinely disruptive internal ventures is not primarily a symptom of organizational complacency or a lack of technological vision. Rather, it is a mechanical failure in corporate capital allocation. Governed by sophisticated financial metrics - such as DCF, IRR, and ROA - that are mathematically optimized for existing, high-margin markets, corporate funding architectures inherently transform capital into "bad money." This capital demands rapid, massive growth while simultaneously exhibiting an unnatural patience for sustained unprofitability in the pursuit of scale. Consequently, nascent, highly uncertain disruptive ventures are forced to abandon their necessary exploratory trajectories, exposed to premature scaling, and ultimately terminated.

To survive impending market shifts, particularly in capital-intensive deep tech sectors, incumbents must recognize that capital is not uniform; its utility is entirely dependent on the specific expectations attached to it. By creating ambidextrous corporate structures that formally separate exploratory funding from core operations, and by replacing traditional lagging financial metrics with rigorous, milestone-driven innovation accounting, large corporations can preserve the "good money" required to incubate disruption. Until the expectations attached to corporate capital are systematically recalibrated to tolerate the slow, ambiguous scaling of entirely new markets, the mechanics of "bad money" will continue to drive out the good, leaving incumbents highly optimized for the present but structurally defenseless against the future.