7 Ways to Lower the Cost of College

College affordability is largely driven by understanding the gap between published sticker prices and the actual net price your family will pay. By leveraging regional tuition reciprocity agreements, maximizing federal aid early, earning pre-college credits, and negotiating competitive financial aid packages, you can dramatically reduce your out-of-pocket expenses. The key is to shift your focus from the advertised cost to customized, data-driven financial planning.

The Illusion of the Sticker Price

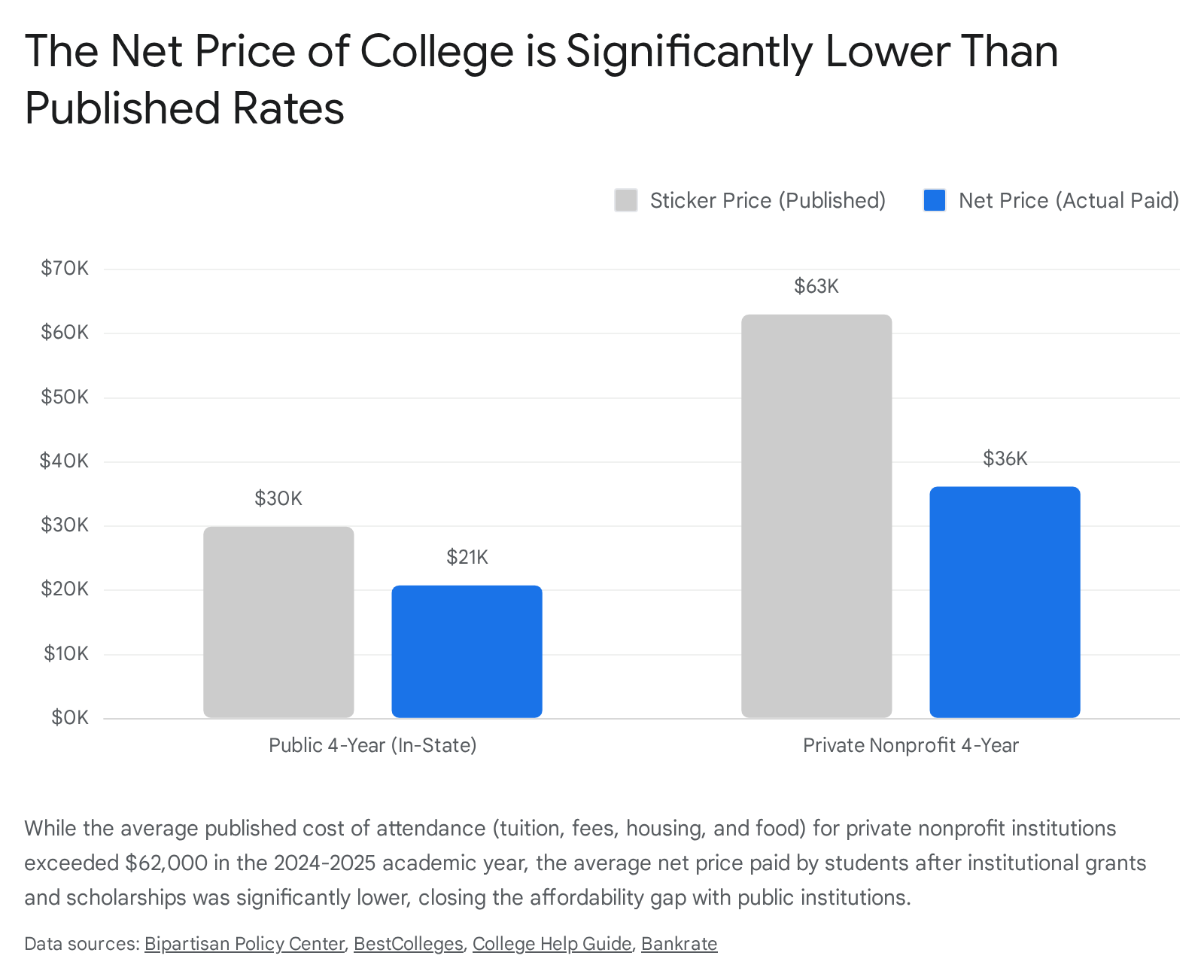

As the cost of higher education continues its upward trajectory, many prospective students and their families experience intense sticker shock. For the 2024-2025 academic year, the average published sticker price for tuition, fees, room, and board was roughly $29,910 at in-state public universities, and approached $63,000 at private nonprofit institutions 11.

At elite Ivy League institutions, the total cost of attendance routinely exceeds $80,000 to $90,000 per year 1. These published college costs are often terrifying, but that reaction stems from a misunderstanding of how higher education pricing works.

Published prices are a remarkably poor metric for understanding what most students actually pay 2. Decades of tuition discounting - a practice where institutions use their own endowment funds to offer grants and scholarships to offset the advertised price - have created a massive gap between the sticker price and the net price. Understanding the variables that dictate this net price is the most critical financial literacy skill a family can develop during the college application process 4. The following comprehensive guide breaks down the seven most effective, research-backed strategies to lower the cost of college, ranging from optimizing federal aid forms to negotiating final offers with university administrators.

1. Target Net Price Instead of Sticker Price

The most foundational strategy to reduce college costs is to shift the search focus entirely from published tuition rates to the anticipated net price. The net price is defined by the National Center for Education Statistics (NCES) as the total cost of attendance - which includes tuition, required fees, books, supplies, and a weighted average for room, board, and personal expenses - minus any federal, state, and institutional grant or scholarship aid that does not need to be repaid 3456. When it comes to paying for higher education, the net price is the only number that dictates true affordability.

Private nonprofit institutions heavily utilize tuition discounting as an enrollment management tool to attract desirable students. In the 2019-2020 academic year, 57% of all undergraduates at private nonprofit four-year colleges received institutional aid, and the average tuition discount per student had grown to $20,800 7. By the 2024-2025 academic year, the average net tuition and fees (excluding room and board) for first-time, full-time students at private nonprofit institutions dropped to $16,510, despite sticker tuitions easily exceeding $43,000 2108. For the average student receiving grant aid at a four-year private nonprofit institution, the net price frequently represents only about 30% of the published sticker price 4.

This institutional discounting takes two primary forms. Need-based aid is distributed based on a family's financial situation, calculated via forms like the FAFSA or CSS Profile. At private colleges, nearly 31% of students receive need-based tuition discounts, averaging over $17,200 7. Merit-based aid, conversely, is distributed based on academic achievements, athletic prowess, or other institutional priorities regardless of household income. Notably, private university students are significantly more likely to receive merit scholarships - approximately 18% of the student body - compared to only 10% of students at public universities 12.

Because the disparity between the sticker price and net price is so vast, evaluating affordability requires personalized data early in the process. Since 2011, the federal government has mandated that all postsecondary institutions participating in Title IV federal student aid programs feature a Net Price Calculator on their websites 1314. These calculators allow families to input their specific financial data and the student's academic profile to generate an estimated, customized aid package. If a family utilizes these calculators during a student's junior year of high school, they can build a college list comprised of institutions historically generous with their specific demographic or academic bracket, rather than blindly hoping for aid after applications are submitted 14.

| Institution Type (4-Year) | 2024-2025 Average Published Tuition & Fees | 2024-2025 Average Net Tuition & Fees | 2024-2025 Total Net Cost of Attendance (Including Living Expenses) |

|---|---|---|---|

| Public (In-State) | $11,610 108 | $2,480 28 | $20,780 28 |

| Public (Out-of-State) | $30,780 1 | Data varies by state | $49,080 1 |

| Private Nonprofit | $43,350 10 | $16,510 28 | $36,150 28 |

Data averages represent historical figures provided by the College Board. Actual costs vary significantly by state and individual institution endowments.

2. Capitalize on Regional Tuition Reciprocity Agreements

For students looking to attend a public college out of state, the tuition multiplier can be devastating. Out-of-state students can pay as much as 300% more than in-state students at public universities, adding tens of thousands of dollars to the final bill 9. However, a highly effective and historically underutilized method to bypass these punitive fees is through regional tuition reciprocity agreements.

Reciprocity agreements are formal compacts between states - administered by regional higher education boards - that allow residents to attend participating out-of-state public colleges at steeply discounted rates 10. Depending on the specific program, students pay either the standard resident tuition rate or a capped multiplier, which is most commonly 150% of the in-state rate. Because these programs represent massive structural savings, often equating to $15,000 to $25,000 annually, they can be highly competitive. Some universities implement strict enrollment caps for reciprocity students, meaning applications must be submitted months before regular college deadlines to secure the discount before funds are depleted 10.

The Four Major Regional Agreements

The higher education landscape in the United States is divided into four primary reciprocity consortiums, each governed by unique rules regarding eligibility, major selection, and participating institutions.

| Reciprocity Program | Managing Region & States | Average Annual Savings | Key Rules and Limitations |

|---|---|---|---|

| Western Undergraduate Exchange (WUE) | 16 Western states/territories via WICHE (e.g., CA, CO, WA, AZ) 917. | $12,517 per student 1112. | Caps tuition at 150% of in-state rate. High-demand majors like Nursing or Engineering are frequently excluded by selective campuses 91711. |

| Midwest Student Exchange Program (MSEP) | 8 Midwestern states via MHEC (e.g., IN, KS, MN, OH, WI) 1314. | $7,000 per student 14. | Caps public tuition at 150% of in-state rate; offers a 10% discount at participating private institutions. Some regional states like IL and MI do not participate 131516. |

| Academic Common Market (ACM) | 15 Southern states via SREB (e.g., AL, GA, MD, TX) 1718. | Varies heavily by specialized program. | Grants pure in-state tuition rates, but only for specific degree programs that are not offered in the student's home state 1718. Texas restricts this to graduate programs only 19. |

| New England Tuition Break (RSP) | 6 New England states via NEBHE (e.g., MA, CT, VT, ME) 2021. | $8,500 per student 2021. | Applies to over 3,000 approved academic programs. At certain institutions, the regional discount does not apply until the student's junior year 212223. |

Navigating these programs requires careful academic planning. For instance, in the Western Undergraduate Exchange and the Academic Common Market, the discount is strictly tied to the student's approved major. If a student enrolls under an eligible major to secure the discount but later decides to change to an ineligible discipline, the university may immediately revoke the reciprocity status and charge full non-resident tuition for the remainder of their degree 9. Students must verify availability and specific GPA requirements directly with the admission office of their target school, as the regional boards only set the framework, leaving final admission decisions entirely to the individual campuses 91324.

3. Master the FAFSA, CSS Profile, and Pell Grant Timelines

Missing financial aid deadlines or fundamentally misunderstanding application requirements results in billions of dollars of unclaimed aid annually 25. Managing the intricate logistics of the Free Application for Federal Student Aid (FAFSA) and the College Scholarship Service (CSS) Profile is paramount for any family attempting to lower the cost of a college education.

Navigating the FAFSA Overhaul and Processing Delays

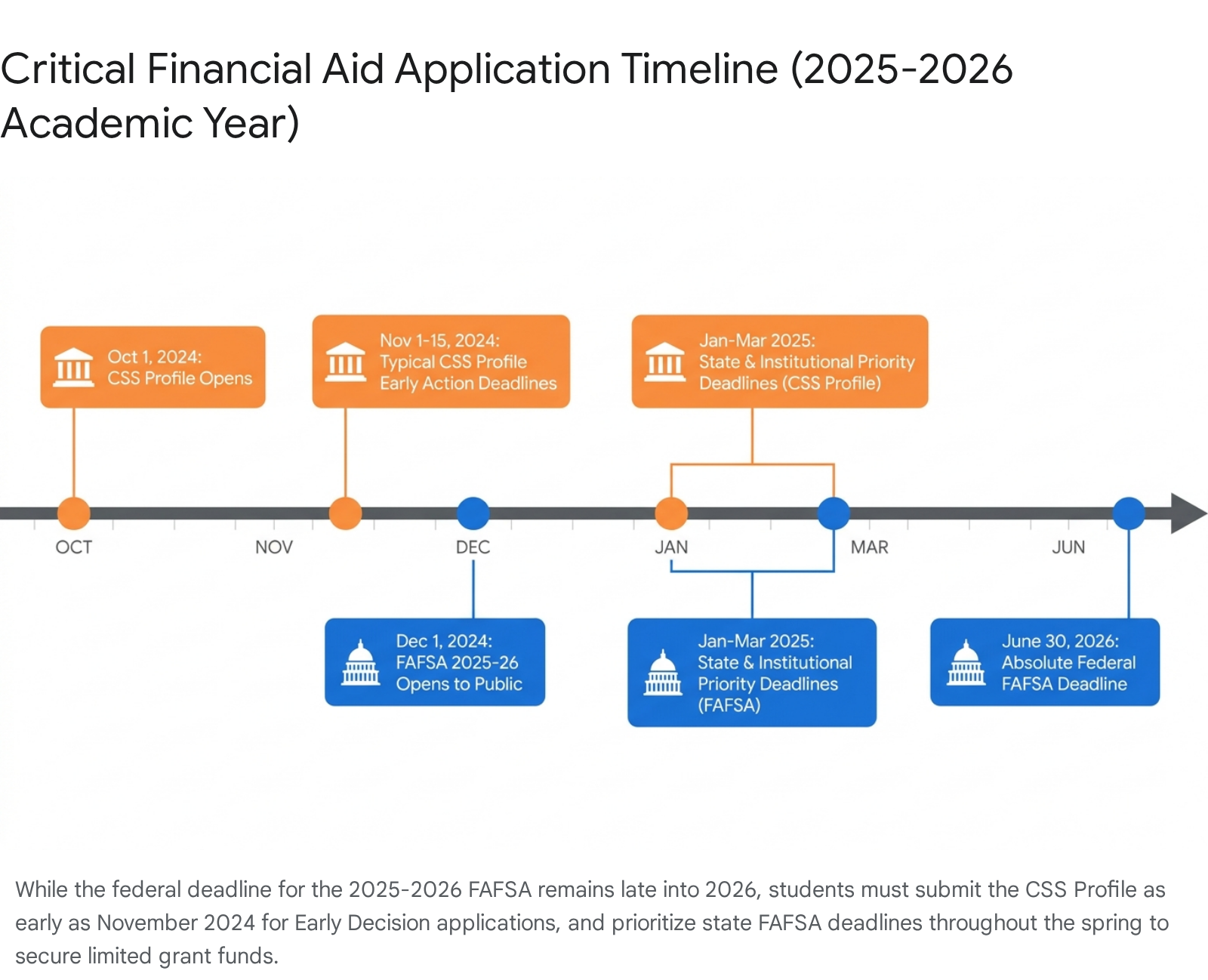

The federal financial aid landscape has experienced massive turbulence due to the FAFSA Simplification Act, which completely overhauled the underlying formulas used to award federal student aid starting in the 2024-2025 award year 2627. Historically available on October 1 every year, the launch of the revised application was heavily delayed and plagued by technical glitches, dropping completion rates significantly nationwide 262728.

For the 2025-2026 academic year, the Department of Education announced a phased beta rollout beginning in October 2024, with the form becoming fully available to the public by December 1, 2024 29. While the absolute federal deadline to submit the 2025-2026 FAFSA is June 30, 2026, students must submit their applications much earlier to meet individual state and college deadlines. Many state higher education agencies and individual colleges award their limited grant funds on a strict first-come, first-served basis, meaning a delay in filing can result in thousands of dollars in lost opportunity 303132.

The new FAFSA introduces several critical changes. The traditional metric known as the "Expected Family Contribution (EFC)" has been entirely replaced by a new formula called the "Student Aid Index (SAI)" 28. The application itself has been drastically shortened, reduced from over 100 questions to roughly 36 dynamic questions, requiring an automated transfer of tax data directly from the IRS 2641. However, the new methodology also removes the "sibling discount." Previously, the formula provided a significant reduction to the expected family contribution if a household had multiple children in college simultaneously; the removal of this factor means larger families may see a reduction in their federal aid eligibility unless individual colleges choose to adjust their institutional offers 26.

Maximizing Pell Grant Eligibility

The Federal Pell Grant is the foundational need-based award that does not require repayment. The FAFSA Simplification Act explicitly tied Pell Grant eligibility to federal poverty guidelines and family size, aiming to expand access for lower and middle-income students 2533. For the 2024-2025 and 2025-2026 award years, the maximum Pell Grant is fixed at $7,395, with a minimum award of $740 3334.

Under the new system, students can automatically qualify for the Maximum Pell Grant, regardless of their calculated SAI, if they meet specific income thresholds tied to their tax filing. A dependent student whose parent is a single parent automatically qualifies for the maximum grant if their Adjusted Gross Income (AGI) is at or below 225% of the federal poverty guideline 2544. If the parents are married and not single, the AGI threshold for maximum eligibility is 175% of the poverty guideline 2544.

The CSS Profile: Unlocking Private Institutional Aid

While the FAFSA is the universal key to unlocking federal and state aid, approximately 400 highly selective and private institutions - along with select competitive public schools like the University of Michigan and the University of North Carolina at Chapel Hill - require the CSS Profile to distribute their own institutional endowments 353647.

Administered by the College Board, the CSS Profile is vastly more invasive and comprehensive than the FAFSA. It scrutinizes assets that the federal government historically ignores, such as the equity built up in a primary home, the value of small family businesses and farms, medical expenses not covered by insurance, and retirement account contributions 354737. Furthermore, for students with divorced or separated parents, the CSS Profile frequently requires the non-custodial parent to create their own account and submit their full financial information, whereas the FAFSA generally only considers the finances of the custodial parent 4737.

Unlike the FAFSA, which is mandated by law to be free, the CSS Profile requires a fee. As of the 2024-2025 cycle, it costs $25 for the initial application and $16 for each additional school report, though fee waivers are granted for families earning under $100,000 annually 35364737. Because CSS Profile deadlines are often tied to early action or early decision admission rounds, families must prepare these detailed financial documents as early as November of the student's senior year, months before the traditional regular decision timeline 364738.

4. Accumulate College Credit During High School

For a motivated student, the core requirements of the first two years of college - typically encompassing general education courses in English, math, science, and history - can often be completed before ever stepping foot on a university campus. By earning college credits during high school, students can shave semesters or even full academic years off their degree timeline, saving tens of thousands of dollars in tuition and living expenses while arriving on campus with the flexibility to pursue double majors or lighter course loads 3940.

There are three primary pedagogical avenues to secure early credit, each carrying distinct costs, academic structures, and differing levels of university acceptance.

| Program Type | Pedagogical Structure | Approximate Cost | Credit Acceptance & Reality |

|---|---|---|---|

| Advanced Placement (AP) | A year-long, college-level class taught in a traditional high school setting by a high school teacher, culminating in a standardized exam 3941. | ~$98 per exam 3942. | Exams are scored 1 to 5. While 3 is technically passing, highly selective colleges increasingly require scores of 4 or 5 to grant actual college credit 4143. |

| CLEP Exams | Purely an assessment model with no prerequisite course. Students self-study existing knowledge and sit for an exam at a testing center 39404243. | ~$93 per exam, plus administrative fees 394243. | Scored 20 to 80, with 50 indicating a pass. Accepted by ~3,000 schools, but frequently rejected by elite, top-tier, or highly selective universities 404243. |

| Dual Enrollment | Students take actual college courses at a local community college or online, earning high school and college credit simultaneously 4143. | Varies heavily; often subsidized or completely free through public school districts 4043. | Credit is based on the final course grade from a college professor, not a single exam. In-state public universities readily accept these, but private or out-of-state schools may not 41. |

Navigating these credit transfers requires preemptive research. Because colleges have ultimate authority over what credits they accept, a student might score a 3 on an AP Calculus exam and receive full credit at a regional state school, but receive zero credit at a highly selective private institution that demands a 5 41. Families must research the specific transfer policies of their target universities before committing time and financial resources to exam fees.

5. Execute a 2+2 Transfer Strategy

If enrolling directly into a four-year university is financially out of reach, the "2+2 transfer strategy" offers a highly economical, well-trodden alternative. In this model, a student attends a local community college or two-year institution to complete their general education requirements and earn an associate degree, and subsequently transfers to a four-year university to complete the final two years of their bachelor's degree 4445.

The financial arithmetic of this strategy heavily favors the student. In the 2024-2025 academic year, the average published tuition and fees for an in-district community college student were approximately $3,990 to $4,050 per year 1410. After factoring in grants and scholarships, the net tuition for many community college students falls below zero (averaging -$710 nationally), meaning federal and state aid entirely covers tuition and leaves leftover funds for books, supplies, or living expenses 2. Compared to paying $30,000 to $60,000 annually at a university for identical introductory courses, the savings are transformative 11.

Navigating Articulation Agreements to Prevent Credit Creep

The greatest systemic risk in the 2+2 strategy is known as "credit creep." This occurs when a student takes classes at the community college that the destination university ultimately refuses to accept for credit toward their specific major, forcing the student to retake courses, spend more money, and delay graduation 444557.

To neutralize this risk, students must build their academic schedules strictly around articulation agreements. These are formal, legally binding partnerships between community colleges and universities that explicitly map out exactly which course credits will transfer seamlessly between the two institutions 444557. Many regions have elevated these agreements into formal transfer pathways featuring guaranteed admission parameters. For example, the Transfer Admission Guarantee (TAG) program in California offers guaranteed admission to specific University of California campuses for community college students who meet strict coursework and GPA requirements 57. Similarly, the ACComplish program connects Austin Community College students with St. Edward's University, offering a seamless pathway combined with dedicated merit scholarships, while the Bats to Cats program guarantees transfer paths to Texas State University 44.

Students executing this strategy must engage with dedicated transfer specialists immediately upon enrolling in community college 4445. Utilizing digital platforms like Transferology can help verify course equivalencies, and maintaining an organized record of all syllabi, transcripts, and advisor communications ensures the student can successfully advocate for their credits upon transferring 4457. Importantly, regardless of where the first two years were spent, when a transfer student graduates, the diploma only bears the name and prestige of the four-year university where they finished their degree 45.

6. Systematize the Search for Micro-Scholarships and Private Grants

While the vast majority of non-loan financial aid comes directly from the federal government and institutional university endowments, private sources still award over $8.2 billion in scholarship money annually 58. Despite this massive volume of available capital, statistics indicate that only about 11% of college students receive a private scholarship, meaning a tremendous amount of funding goes unclaimed 5859.

To capture this aid, students must treat the scholarship search methodically, looking beyond highly competitive national awards to target local grants, major-specific funds, and innovative micro-scholarship platforms.

Optimizing Scholarship Databases

Instead of searching blindly on standard web engines, students should create comprehensive profiles on vetted scholarship aggregators. Modern platforms utilize algorithms to match students with high-probability awards based on their academic background, demographic data, and unique family situations. Legacy platforms like Fastweb and Scholarships.com maintain massive, daily-updated databases covering over 1.5 million opportunities, pushing personalized recommendations directly to users 4661.

More modern application platforms, such as Going Merry (operated by the student lender Earnest), allow students to filter heavily for local scholarships, which often have significantly smaller applicant pools and higher win rates. Going Merry streamlines the process by automatically filling out application forms with the student's saved personal data and allowing for bundled applications to multiple funds simultaneously 4647. Additionally, the College Board's BigFuture database catalogs over 6,000 scholarships and is particularly strong for students seeking merit-based awards or filtering by highly specific criteria, such as parent marital status, specific medical conditions, or community organization affiliations 464748.

The Rise of Micro-Scholarships

The traditional scholarship model usually requires high school seniors to write exhaustive essays just months before graduation. However, platforms like RaiseMe have revolutionized this paradigm by allowing students to earn micro-scholarships starting as early as the 9th grade 49.

Rather than competing in a winner-take-all essay contest, students build an ongoing digital portfolio on the platform and earn incremental dollar amounts for specific, routine achievements. Partnering colleges pledge varying amounts of money for accomplishments such as getting an 'A' in a core academic class, participating in extracurricular sports, holding a part-time job, or even taking on responsibilities caring for family members 49. While this money is not paid out in liquid cash immediately, it accumulates as guaranteed institutional aid that the student will receive as a discount if they apply, are accepted, and enroll at that specific participating college 49. This model shifts the financial aid process from a stressful senior-year scramble to a transparent, multi-year incentive structure.

7. Appeal and Negotiate Financial Aid Offers

One of the best-kept secrets in higher education finance is that an initial financial aid award letter is merely an opening offer, not a final verdict 6566. Especially at private and out-of-state universities where enrollment managers control highly discretionary endowment funds, there is often substantial room to negotiate a better deal 1450. Successful appeals generally fall into two distinct strategic categories: Special Circumstances reviews and Competitive Merit appeals.

Strategy A: The Professional Judgment (Need-Based Aid)

Because the FAFSA relies on tax data that is effectively two years old ("prior-prior year" taxes), it cannot capture real-time financial disasters. If a family's financial situation has materially degraded since that original tax return was filed, they have the right to request a Professional Judgment review from the college's financial aid administrator 66515270. Financial aid offices have the federal authority to manually adjust data elements on a student's FAFSA, generating a new Student Aid Index (SAI) that unlocks more need-based federal and institutional aid 52.

A successful appeal requires proof of an uncontrollable event that impacts the ability to pay. Valid reasons include recent job loss, furlough, or significant reduction in salary; unreimbursed extraordinary medical or dental expenses; the death, divorce, or separation of parents since filing; or the termination of child support and alimony 5152705372. Conversely, financial aid administrators will almost universally reject appeals based on high discretionary consumer debt, the cost of funding lifestyle choices or vacation homes, or vague assertions that the family simply cannot afford the bill without specific numerical data backing the claim 657053.

To execute this strategy, families must bypass verbal requests and formally submit rigid documentation - such as termination letters, medical receipts, or divorce decrees - to build an undeniable paper trail for the financial aid office 6551525373.

Strategy B: The Competitive Appeal (Merit-Based Aid)

If a family does not qualify for need-based aid due to high income, they can still negotiate their merit-based tuition discounts using market leverage 1466. Colleges operate as businesses competing for the best students to fill out their freshman class metrics and achieve enrollment goals. If a student receives a superior financial offer from a peer institution - defined as a college with highly similar academic rankings, selectivity, and regional prestige - they can use that competing offer as direct leverage 14656673.

| Elements of a Successful Competitive Appeal | Actions to Avoid |

|---|---|

| Provide Proof: Attach the competitor's award letter as a PDF to demonstrate the exact financial gap 507374. | Paying the Deposit: Never pay the enrollment deposit before negotiating. Once the school secures your enrollment, they have zero incentive to increase aid 66. |

| Compare Peer Schools: Only compare similar tiers. A highly selective university will not match a less selective regional school's offer 656673. | Being Demanding: Do not treat it like haggling for a car. Approach the staff with a professional, collaborative tone 65667374. |

| Show Commitment: Explicitly state that if the college matches the financial gap, the student will immediately commit to enrolling 6550737475. | Focusing on "Need": If appealing purely for merit aid based on peer offers, focus on the student's value, not household expenses 66. |

| Highlight New Data: Provide updated senior year grades, new test scores, or recent awards to justify an increase in merit funds 737475. | Accepting Front-Loaded Offers: Ensure any new money is renewable for all four years, not just a one-time freshman discount 66. |

When writing the appeal, the student should address the financial aid or admissions office directly, expressing deep gratitude for the initial offer and reiterating that the institution remains their absolute top choice 65667374. By combining a polite tone with hard data from competing institutions, families force the university to make a distinct business decision on whether they want to purchase that specific student's enrollment for the upcoming year.

Bottom line

Lowering the cost of college requires aggressive, data-driven financial strategy that begins long before the first tuition bill arrives. Families must look beyond terrifying sticker prices to identify schools with generous net-price discounting, leverage regional reciprocity agreements to bypass out-of-state fees, and systematically build pre-college credits through AP or Dual Enrollment programs. By preparing for the strict, early timelines of the FAFSA and CSS Profile, and utilizing competing peer offers to professionally negotiate final merit packages, students can effectively protect themselves from debilitating long-term debt. What remains uncertain going forward is how ongoing software updates to the FAFSA platform and shifting congressional appropriations may alter the speed and distribution of federal grant aid in future academic cycles.