Founder Cognitive Biases and Startup Decision-Making Countermeasures

The entrepreneurial ecosystem is characterized by the pursuit of innovation and the allocation of venture capital in environments of extreme uncertainty. Despite the proliferation of startup incubators, refined agile methodologies, and vast influxes of private equity, the statistical reality of startup outcomes remains stark. Across diverse markets and economic conditions, the long-term failure rate for new ventures hovers near 90% over a ten-year horizon, with approximately 75% of venture-backed startups failing to return capital to investors 112. While conventional post-mortems frequently attribute these failures to market timing, competitive displacement, or capital exhaustion, expansive meta-reviews of startup outcomes indicate a deeper underlying mechanism. Cognitive errors - specifically driven by the psychological strain of operating in high-uncertainty environments - account for between 40% and 90% of startup failures 4.

In highly fluid startup environments, founders are required to make continuous strategic choices with incomplete information, limited resources, and intense time pressure. Under these conditions, human cognition naturally relies on heuristics: mental shortcuts designed to accelerate decision-making without exhaustively analyzing every variable 34. While heuristics are evolutionarily efficient, they regularly produce systematic deviations from rational judgment, known as cognitive biases 7. When scaled across a startup's lifecycle - from ideation and product-market fit (PMF) discovery to scaling and corporate governance - these unmitigated biases distort data interpretation, foster the misallocation of capital, and ultimately derail operations 43.

Statistical Prevalence of Startup Mortality

To understand how cognitive biases precipitate failure, it is necessary to examine the primary proximal causes of startup death. Research indicates that successfully building a product and achieving initial product-market fit does not guarantee long-term viability; approximately 78% of companies that reach this milestone subsequently fail to scale, struggling to transition from charismatic founder-led sales to industrialized, scalable processes .

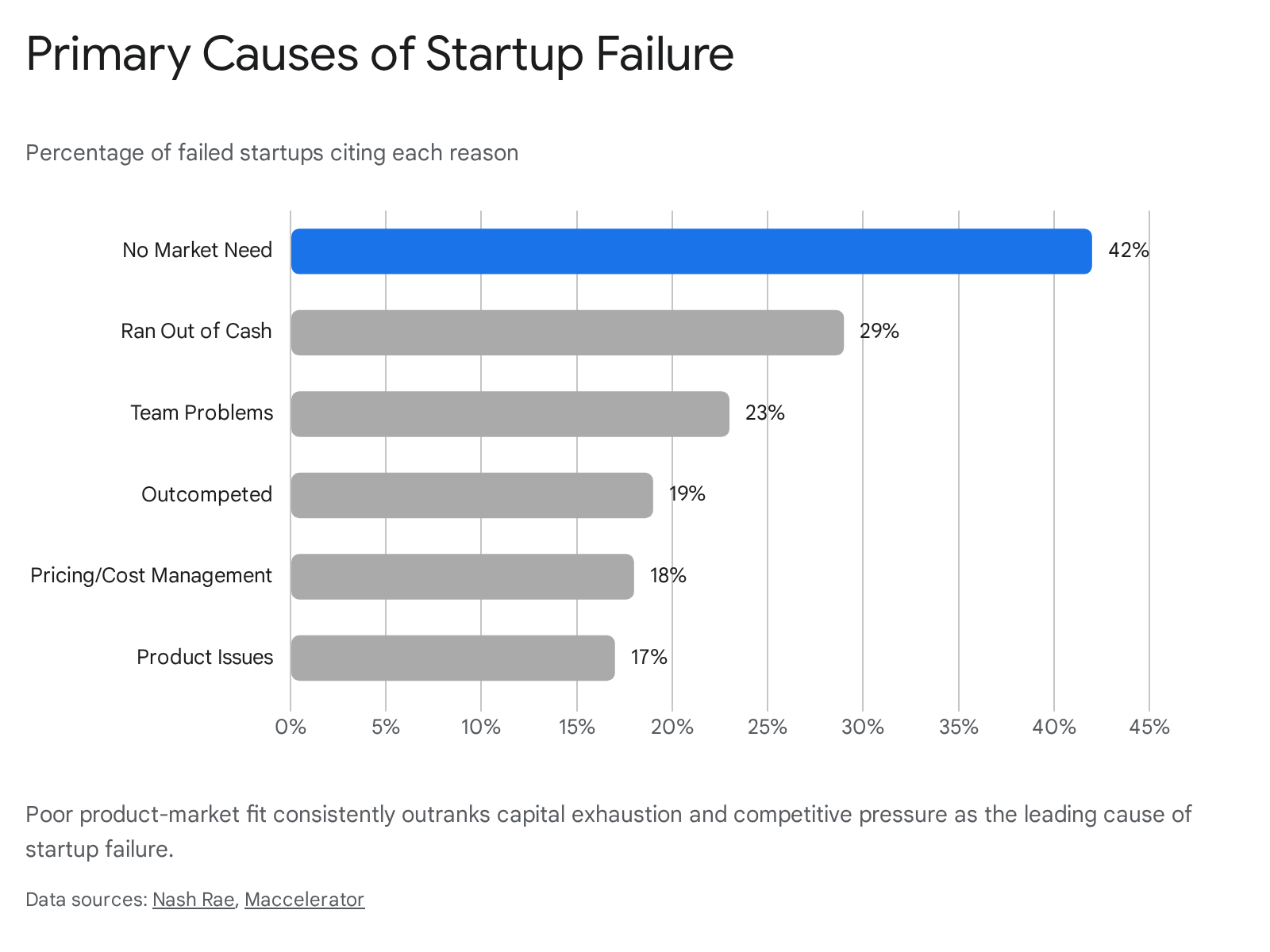

Analyses of failed technology companies consistently highlight an absence of market need as the leading catalyst for collapse. Across datasets spanning over a decade, including the CB Insights post-mortem analysis of 431 failed venture-backed companies, 42% to 43% of startups cite poor product-market fit as their primary cause of failure. This ranks higher than capital depletion (29%), team conflicts (18% to 23%), or being outcompeted (19%) 1156.

The consistency of the product-market fit deficit points directly to a systemic flaw in the discovery and validation phases of product development. Research demonstrates that founders routinely build products optimized for their own cognitive experience rather than the reality of their target users 5. This phenomenon is reflected in product analytics data, which shows that roughly 80% of software features deployed in live products are rarely or never used, with merely 6.4% of features driving 80% of actual user activity 5. Premature scaling - investing heavily in marketing, hiring, and infrastructure before validating core user demand - is heavily linked to these misjudgments, functioning as a primary factor in 70% of startup failures within the Startup Genome dataset 5.

Personality Traits and Lifecycle Performance

The susceptibility to cognitive bias is not uniform; it is heavily mediated by the baseline personality traits of the founding team. A large-scale field study examining 10,541 founder-startup dyads utilized the "Big Five" personality framework to map how specific traits influence outcomes across the venture lifecycle 7. The data reveals that the influence of personality traits shifts dynamically as a startup matures.

| Personality Trait | Early-Stage Impact | Late-Stage Impact | Operational Implication |

|---|---|---|---|

| Openness to Experience | Positive | Neutral | Increases the likelihood of raising initial funding rounds by 5% per standard deviation increase 7. |

| Agreeableness | Positive | Neutral | Correlates with successfully attracting initial seed and angel investments 7. |

| Neuroticism | Negative | Negative | Decreases early funding amounts and lowers the probability of a successful exit (IPO or acquisition) by 16% 7. |

| Conscientiousness | Positive | Negative | Highly organized founders raise more initial capital, but their rigidity reduces late-stage exit likelihood by 15% due to an inability to adapt to fast-moving ecosystems 7. |

| Extraversion | Neutral | Neutral | Shows no significant relationship with startup outcomes, likely offset by the success of introverted technical founders 7. |

The paradox of conscientiousness is particularly notable. While organizational rigor allows founders to execute early-stage business plans and secure funding effectively, excessive conscientiousness creates friction during later stages. The rigid adherence to original operational plans conflicts with the requisite agility and "move-fast-and-break-things" culture required to navigate acquisitions or strategic pivots 7. Similarly, the universally negative impact of neuroticism underscores the critical role of emotional resilience. Founders high in neuroticism struggle to maintain objective decision-making under stress, raising less capital and significantly reducing their chances of returning venture investments 47.

Cognitive Biases in Entrepreneurial Strategy

Cognitive biases function as an invisible operating system, steering resource allocation, hiring, and strategic pivots. Management research categorizes several predominant biases that consistently manifest within the entrepreneurial context, transforming natural psychological tendencies into structural corporate vulnerabilities.

Overconfidence and the Illusion of Control

Entrepreneurs exhibit significantly higher levels of overconfidence compared to corporate managers in established organizations 48. Overconfidence in this context is defined as the tendency to overestimate the correctness of one's initial assessments, personal capabilities, and the likelihood of future success 4. Empirical studies reveal that over 80% of entrepreneurs estimate their chances of success to be 70% or higher, while nearly one-third assess their probability of success at a statistical impossibility of 100% 9.

This extreme optimism is frequently coupled with the illusion of control: the false belief that an individual can dictate or influence outcomes that are objectively governed by external macroeconomic forces or chance 4. By overestimating their control over market dynamics, founders systematically underestimate external risks and forego robust contingency planning 4. Grounded in Behavioral Decision Theory, studies utilizing structural equation modeling indicate that both excessive optimism and the illusion of control exert a statistically significant negative impact on long-term firm performance 10. The boundary between "productive optimism" - the necessary drive to innovate - and destructive hubris is crossed when founders fail to distinguish between the variables they can influence (e.g., product quality) and the variables they cannot (e.g., global economic shifts) 11.

Confirmation Bias and the False-Consensus Effect

Confirmation bias is the human tendency to seek, interpret, favor, and recall information that confirms preexisting beliefs while simultaneously dismissing contradictory data 3712. In new product development, confirmation bias distorts user research, feature prioritization, and data interpretation 37.

Founders affected by confirmation bias will often conduct user interviews that inadvertently validate their assumptions rather than test them. They are prone to cherry-picking metrics that support their strategic vision during board meetings while dismissing rising churn rates or flatlining engagement as anomalies 3. This bias is heavily exacerbated by the "false-consensus effect," an established psychological phenomenon where individuals overestimate the extent to which other people share their choices, values, and judgments 512. Consequently, founders assume their personal pain points represent a broad, monetizable market need. When the product launches, the lack of traction is often met with confusion, as the founder projected their own cognitive reality onto a market that did not share it 5. This is frequently compounded by wording bias during discovery phases, where founders ask leading questions (e.g., "How difficult was it to complete that task?") that prompt users to deliver the answers the founder consciously or subconsciously desires 12.

Escalation of Commitment and Sunk Cost Fallacy

The sunk cost fallacy describes the irrational incorporation of irrecoverable past investments - whether capital, time, or emotional energy - into calculations regarding future actions 71213. In the startup environment, this manifests as an "escalation of commitment" to failing strategies.

When market feedback indicates that a product lacks traction, rational decision-making dictates a cessation of investment or a strategic pivot. However, founders suffering from the sunk cost fallacy often compound the error by injecting additional capital into the failing venture - throwing good money after bad 9. This reluctance to pivot is highly destructive; however, the pivot itself is fraught with cognitive traps. Survey data indicates that 81% of founders pivot from their original idea at least once 2. Yet, up to 10% of startups fail specifically due to an unsuccessful pivot, indicating that a pivot driven by desperation rather than objective market signals often functions merely as a mechanism to stall inevitable failure 13. Founders can become trapped in "pivot hell," continuously exhausting resources on lateral moves without ever establishing core product-market fit 14.

The Availability Heuristic and Survivorship Bias

The availability heuristic causes decision-makers to overweight information that is recent, emotionally salient, or easily recalled 713. In product management, this results in roadmaps dictated by the loudest customer complaints, the most recent bug encountered by the CEO, or an isolated anecdote from an investor, rather than systematic analyses of aggregate user data 37. This correlates closely with anchoring bias, where early prototype estimates or initial revenue projections become immovable targets regardless of emerging market realities 3.

A macro-level manifestation of the availability heuristic in entrepreneurship is survivorship bias. Survivorship bias occurs when individuals mistake a highly visible, successful subgroup for the entire population, ignoring the invisible majority that failed 15. The media disproportionately amplifies the narratives of "unicorn" startups and visionary founders, creating a distorted archetype of success 1. Consequently, novice founders emulate the behaviors of successful outliers without recognizing that thousands of failed founders executed the exact same strategies 15.

This bias deeply infects academic and market research. The Academy of Management Annals notes a "scholarly convenience bias," wherein researchers predominantly study surviving firms and executives because their data is readily accessible, thereby building incomplete theoretical models of organizational behavior 16171819. Studies of "born-global" firms, for example, have historically omitted the massive failure rates of startups that attempted rapid internationalization and collapsed under the complexity of managing divergent value propositions 20. This leads to an ecosystem where both academic literature and popular business guidance fundamentally underestimate the risks associated with entrepreneurial ventures 2021.

Cognitive Biases in Technology Paradigm Shifts

The interplay of cognitive biases and capital markets is particularly visible during technological paradigm shifts. The rapid emergence of Generative Artificial Intelligence (AI) between 2024 and 2026 provides a highly documented case study of cognitive biases - particularly Fear of Missing Out (FOMO) and the bandwagon effect - operating at scale.

Driven by speculative fervor, venture capital poured $67 billion into AI startups in 2024, and $192.7 billion globally by 2025 1422. However, by 2026, 40% of the AI startups launched in 2024 had shut down entirely 22. Furthermore, enterprise adoption experienced massive failure rates; a comprehensive MIT study revealed that over 95% of generative AI pilots in major companies failed to deliver any return on investment, primarily because generic LLMs failed to integrate into existing deterministic workflows 23. The enterprise abandonment rate for AI initiatives spiked from 17% in 2024 to 42% by 2025, driven by security concerns, spiraling costs, and a lack of fundamental strategy .

These failures were largely driven by misaligned executive decision-making frameworks rather than raw algorithmic limitations. The cognitive errors manifested in several predictable patterns: * Category Errors in Application: Organizations attempted to apply non-deterministic AI models (which infer probabilistic answers) to highly deterministic core business problems (which require predictable, rigid logic). This fundamental mismatch resulted in severe operational drift and unrecoverable cost overruns 24. * Lack of Defensibility: Startups raised massive capital based on products that functioned as thin wrappers over existing APIs. Due to overconfidence and a failure to realistically assess competitive moats, these startups were immediately rendered obsolete when foundational model providers integrated identical features natively for free 22. * The Big Bang Fallacy: Companies routinely attempted massive, monolithic AI modernizations rather than focused, iterative deployments. Volkswagen's Cariad software division, for example, attempted to simultaneously replace legacy systems, build custom AI, and design proprietary silicon, resulting in a reported $7.5 billion in operational losses 25. * Data Blindness: Executives suffered from confirmation bias regarding the readiness of their organizational data infrastructure. Industry analysts noted that AI initiatives failed predominantly due to "weak data," yet capital allocation continued to prioritize the procurement of advanced models over fundamental data remediation 23.

Cross-Cultural Dimensions of Cognitive Bias

A critical limitation in understanding entrepreneurial cognitive bias is the geographic and cultural homogeneity of the underlying research. More than 95% of psychological studies draw samples from Western, Educated, Industrialized, Rich, and Democratic (WEIRD) societies, predominantly the United States and Western Europe 2627. This creates a severe ethnocentric bias, where Western cognitive styles are mistakenly treated as human universals 26.

Cultural psychology reveals that cognitive processes, including those impacting entrepreneurial risk and decision-making, vary significantly across different eco-cultural zones. Western societies heavily promote an independent self-construal, resulting in analytical, categorical thinking and a high degree of self-enhancement (the tendency to view oneself as superior to others) 2829. This cultural bedrock supports the hyper-optimism and individualistic overconfidence typical of Silicon Valley entrepreneurship 2830.

In contrast, populations in East Asia, South Asia, Latin America, and Africa predominantly exhibit an interdependent self-construal, emphasizing social harmony and collective context 28. Cognitive styles in these regions are measurably more holistic; individuals distribute attention more broadly across context rather than focusing strictly on an isolated object 29. Notably, the self-enhancement bias is significantly lower in East Asian populations compared to Western samples, suggesting that the precise manifestation of entrepreneurial overconfidence differs dramatically across borders 2831.

Furthermore, risk assessment and interpersonal trust operate differently across regions. Research highlights culturally specific phenomena, such as "enemyship" in West Africa, representing a heightened vigilance against sabotage by ingroup members 28. Non-Western collectivistic societies generally exhibit lower baseline levels of generalized trust compared to individualistic Western societies, fundamentally altering how founders approach team building, delegation, and investor relations 2829.

These cognitive differences fundamentally alter macro-level strategic execution. For instance, theoretical models of cross-border cooperation (CBC) developed in Western Europe emphasize decentralized, multi-level governance 32. However, when these models are applied to Southeast Asia or Africa, they fail to align with reality, as CBC in these regions is overwhelmingly driven by top-down, central government mandates 32. Therefore, scaling operational playbooks directly from Silicon Valley to emerging markets without adjusting for culturally embedded cognitive frameworks often results in friction, misalignment, and organizational failure 30.

Structural Bias Mitigation and Decision Frameworks

While cognitive biases cannot be entirely eradicated from the human brain, their impact on the startup lifecycle can be systematically neutralized through the implementation of rigorous organizational architectures, objective evaluation frameworks, and robust governance 37.

Debiasing versus Choice Architecture

Management research categorizes bias mitigation into two distinct approaches: debiasing and choice architecture 33.

- Debiasing seeks to modify the decision-maker directly. It involves training programs, active feedback loops, and cognitive warnings designed to help individuals recognize and counter their own biases. Debiasing is highly effective during the early, ambiguous stages of the decision-making process (e.g., initial market research and ideation) and in high-uncertainty environments where founders need adaptable, generalizable critical thinking skills 33.

- Choice Architecture modifies the environment in which the decision is made rather than the individual. This involves restructuring how information is presented, altering default options, and imposing structural friction before irreversible actions are taken. Choice architecture requires pre-existing organizational trust and is most effective in stable environments where optimal choices can be engineered into the workflow to reduce cognitive load 33.

Objective Metric Frameworks

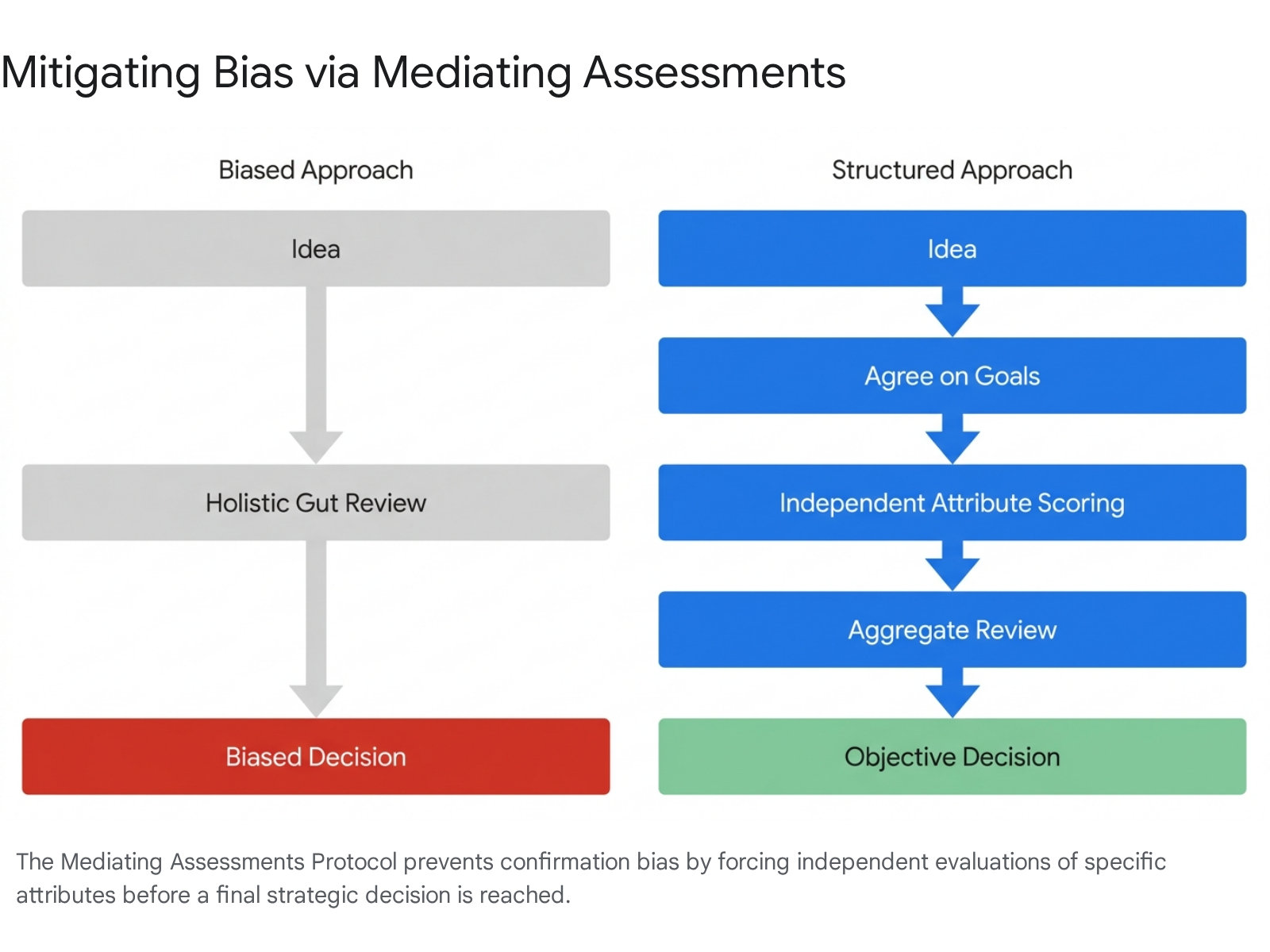

To counter confirmation bias and the reliance on holistic "gut feelings," startups must integrate structured evaluation protocols. Unstructured decision-making allows charismatic leaders to dominate outcomes via the recency effect and anchoring bias 339. The Mediating Assessments Protocol (MAP) is designed to dismantle this by breaking complex decisions into distinct, independent evaluations 39. Rather than judging a product feature comprehensively in one sitting, teams evaluate it sequentially against distinct, pre-agreed goals (e.g., acquisition impact, engineering cost, retention value), scoring each attribute independently before making a final holistic judgment 39.

For product-market fit and growth, standardized metric frameworks force startups to confront objective data rather than vanity metrics. Utilizing established frameworks provides cognitive distance, allowing founders to evaluate operations systematically.

| Framework | Core Focus | Lifecycle Stage | Primary Utility for Bias Mitigation |

|---|---|---|---|

| AARRR (Pirate Metrics) 40 | Acquisition, Activation, Retention, Referral, Revenue | Early to Scaling | Prevents founders from fixating purely on top-of-funnel acquisition while ignoring fundamental flaws in product retention and monetization. |

| HEART 40 | Happiness, Engagement, Adoption, Retention, Task Success | Product iteration | Centers quantitative user experience data, mitigating the founder's false-consensus assumption that the product is intuitively usable. |

| Sean Ellis 40% Rule 634 | Product-Market Fit validation | Post-MVP | Provides a rigid threshold: if fewer than 40% of users would be "very disappointed" to lose the product, PMF is absent, halting premature scaling. |

| OODA Loop 42 | Observe, Orient, Decide, Act | High-competition / Pivots | Forces continuous observation and orientation, reducing the likelihood of falling into the sunk cost fallacy by demanding rapid iteration. |

| Kepner-Tregoe Matrix 42 | Resource Prioritization | Resource Constrained | Introduces a highly structured, data-driven methodology for weighing risks against benefits, countering the availability heuristic. |

Board Governance and Independent Oversight

The ultimate structural safeguard against executive cognitive bias is the formal Board of Directors. An effective board does not simply measure financial outputs; it fundamentally alters the cognitive processing of the executive team. According to the Information Processing Model of Board Decision Synergy, successful boards reduce bias through a three-step process: discovery, deliberation, and decision 35.

When a founder presents a recommendation heavily laden with personal bias, a synergistic board engages in independent discovery to introduce outside data 35. Without this independent injection of facts, boards risk falling into groupthink and acting as an echo chamber that merely amplifies the CEO's original bias 3544.

To achieve this, the composition of the board is critical. Startups that rely exclusively on founding members and early investors face inherent structural imbalances. Investor-affiliated directors are often biased toward aggressive M&A or IPO strategies, while founders may be overly attached to the original product vision 45. Independent directors - those without material relationships to the company or its investors - act as essential mediators 4647. In the early stages, independent directors frequently resolve deadlocks between founders and venture capitalists, providing unbiased oversight and a reality check that interrupts the sunk cost fallacy during high-stakes strategic pivots 45.

Establishing these governance structures early is vital. While early-stage startups often view formal governance as bureaucratic friction, delayed implementation creates severe systemic risks 36. A poorly constructed capitalization table or an unchecked, dominant founder can render a startup uninvestable to later-stage venture capital firms 36. Best practice dictates that founders aim for the compliance and governance standard required for the funding stage ahead of their current level; for instance, a seed-stage business should align its governance structures with those of a Series A company 36. By instituting advisory boards and formal independent director seats prior to massive scaling efforts, startups embed choice architecture directly into their corporate DNA, ensuring that the inevitable cognitive biases of the founding team do not go unchallenged when the financial stakes are highest 464937.