Swing Trading Myths That Cost Beginners Money

Beginner swing traders consistently lose money not because they lack the right technical indicators, but because they misunderstand mathematical risk and succumb to powerful behavioral biases. Believing that averaging down rescues bad trades, or that a high win rate guarantees profitability, mathematically ensures eventual portfolio ruin. To survive the financial markets, traders must abandon these psychological traps and prioritize strict downside protection over the illusion of predictive certainty.

The Brutal Reality of Retail Trading

Swing trading occupies a highly appealing middle ground between the frantic, hyper-active pace of day trading and the passive, multi-year horizon of traditional investing. By holding assets for several days or weeks, swing traders attempt to capture structural price trends and momentum shifts without having to monitor charts on a minute-by-minute basis. Over the past decade, and particularly following the pandemic, the accessibility of modern, zero-commission brokerage applications has democratized this practice, bringing a massive flood of retail capital into the financial markets.

However, the empirical outcomes for these retail participants remain overwhelmingly negative. While financial influencers often promote trading as a straightforward path to independent wealth, regulatory disclosures, academic behavioral finance studies, and platform data paint a starkly different, heavily documented reality: the vast majority of non-professional traders systematically lose their capital.

A pervasive rumor in retail financial circles suggests that "90% of traders lose money." While beginners often dismiss this as an exaggerated myth designed to scare off the uncommitted, global regulatory data confirms that the actual failure rate sits uncomfortably close to this benchmark 1. Data from financial watchdogs across different continents consistently demonstrate massive retail failure rates, particularly in leveraged instruments like Contracts for Difference (CFDs), foreign exchange (Forex), and futures contracts.

For example, the European Securities and Markets Authority (ESMA) requires legally mandated broker disclosures, which reveal that between 74% and 89% of retail accounts lose money trading CFDs and Forex 23. The United States Commodity Futures Trading Commission (CFTC) reports remarkably similar numbers, consistently noting the unprofitability of retail forex traders sitting between 70% and 80% 2. In Australia, the Australian Securities and Investments Commission (ASIC) found that in the 2024 financial year alone, 68% of retail CFD investors lost money, totaling a staggering $458 million (AUD) in collective losses, which included $73 million simply in platform fees 45.

The statistics are even more brutal in emerging markets and complex derivatives. A comprehensive three-year study published in 2024 by the Securities and Exchange Board of India (SEBI) documented that 93% of retail investors trading futures and options (F&O) lost money 2. Across the three-year study period, the average loss for each retail trader was approximately Rs 2 lakh (roughly $2,400 USD) 2. Conversely, on the other side of these trades, proprietary trading firms generated Rs 33,000 crore in the 2024 financial year alone, with 97% of those institutional profits generated by algorithmic trading systems 2.

Even in traditional, unleveraged equity markets, the performance gap between retail participants and institutional benchmarks is devastating. Dalbar's Quantitative Analysis of Investor Behavior study found that over a 20-year period ending in 2024, the average equity fund investor returned 9.24% per annum against the S&P 500 index's 10.35% 3. While a 111-basis-point gap may sound minor, it compounds over two decades to roughly 22% less wealth 3.

A Post-Pandemic Surge Meets Hard Data

The scope of this underperformance is expanding as market participation grows younger. A decade-long study by JPMorgan Chase Institute revealed that young adults are entering the market much earlier than previous generations; by 2024, the share of 25-year-olds using investment accounts was 37%, compared to just 6% for 25-year-olds in 2015 1. Between 2023 and early 2025, retail investing flows rose by about 50%, rivaling the peak of the pandemic savings surge 1.

Despite better charting platforms, sophisticated analytical tools, and endless educational content, the retail trader failure rate has not materially improved in nearly three decades of recorded data 2. A 2020 peer-reviewed study analyzing futures day traders over a timeline of 300 days found that a staggering 97% of them lost money, with only 0.4% earning more than the equivalent of $54 per day 7. The data confirms undeniably that the default outcome for a retail trader is financial loss 1. This consistent underperformance is not an accident of bad luck; it is driven by specific, identifiable misconceptions about how trading mechanics and human psychology interact.

Myth 1: A High Win Rate Guarantees Profitability

Perhaps the most intuitive, and ultimately dangerous, assumption that beginner swing traders make is that predicting the market correctly most of the time will naturally lead to a growing account balance. Human beings are conditioned by traditional education and employment systems to believe that being "right" more than half the time equates to a passing grade or a successful outcome. In the realm of financial trading, however, a trader's win rate is largely irrelevant if their position sizing and risk-to-reward ratios are asymmetrical.

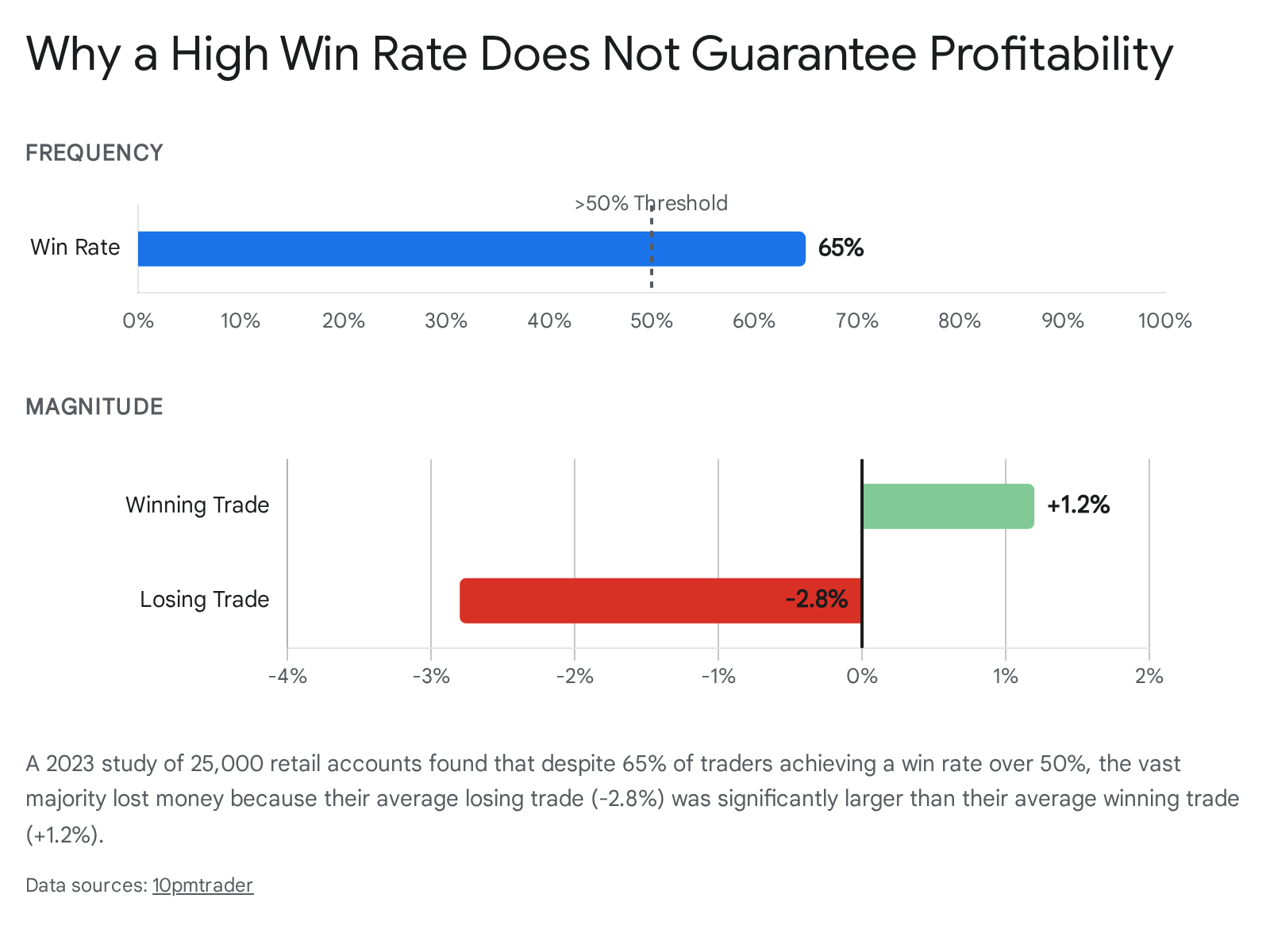

A highly revealing 2023 study analyzed the performance of 25,000 retail traders across more than 4 million individual trades. The researchers uncovered a fascinating paradox: approximately 65% of the traders analyzed actually maintained a win rate above 50% 2. By any normal societal standard, they were picking the right direction more often than they were picking the wrong one. Yet, 82% of those exact same traders lost money overall 2.

The mathematical culprit behind this collapse is asymmetric trade sizing. The study found that the traders' average winning trade gained approximately 1.2% in value, while their average losing trade cost them a devastating 2.8% 2. Because the losses were significantly larger in magnitude than the gains, the high win rate was entirely negated. They were right more than half the time, but every instance of being wrong hurt the portfolio more than twice as much as being right helped it 2.

In quantitative trading terms, a strategy's viability is measured by its "expectancy," which calculates the average amount a trader can expect to win or lose per trade executed. The formula is expressed mathematically as $Expectancy = (Win Rate \times Average Reward) - (Loss Rate \times Average Risk)$ 8. A strategy that wins 60% of the time but loses three times as much capital on a bad trade as it makes on a good one yields a negative expectancy. Consequently, it is mathematically guaranteed to drain the account over a large enough sample size, regardless of how accurate the trader feels their market predictions are.

This destructive asymmetry is rarely a conscious mathematical choice. Instead, it is deeply rooted in human psychology, manifesting as the instinctual urge to close winning trades early out of fear that the market will reverse and take away the unrealized profit, while simultaneously holding onto losing trades in the blind hope that the price will eventually recover to the break-even point 2.

Myth 2: The "Disposition Effect" is Just Academic Theory

The tendency to cut winners short and let losers run is not merely a sign of poor discipline; it is the direct manifestation of a heavily documented cognitive bias known in behavioral finance as the "Disposition Effect." First identified and named by researchers Hersh Shefrin and Meir Statman in a seminal 1985 paper, the disposition effect describes the irrational but universal tendency of investors to sell assets that have increased in value to lock in a sure gain, while holding onto assets that have dropped in value to avoid the finality of realizing a loss 23.

The underlying psychological mechanism of the disposition effect is rooted in Prospect Theory, formulated by Nobel laureates Daniel Kahneman and Amos Tversky. Prospect theory dictates that humans exhibit a greater aversion to losses than a preference for gains; effectively, we experience the psychological pain of a financial loss much more intensely than the pleasure of an equivalent financial gain 211.

To avoid the emotional discomfort of admitting a trade thesis was wrong - which creates cognitive dissonance against a trader's self-image as a rational actor - a swing trader will stubbornly allow a small, manageable loss to spiral into a catastrophic portfolio drawdown 12. Conversely, to secure a psychological "win" and avoid the regret of watching a profitable trade turn negative, they will sell a winning position prematurely, artificially capping their upside potential 13.

The Staggering Cost of Psychological Biases

The financial toll of the disposition effect on retail portfolios is massive. A comprehensive study conducted by researchers at the Stanford Graduate School of Business analyzed an incredible dataset of 2.1 million retail brokerage accounts between January 2019 and December 2024. The researchers established robust statistical benchmarks, finding that the disposition effect was actively present in 71.3% of the active trading accounts 14.

Collectively, this bias - along with associated errors like overtrading, home bias, and return-chasing behavior - reduced the average annual portfolio return of these retail traders by 3.7 percentage points relative to a passive benchmark index 14. The researchers noted that the performance drag was largest for investors who traded most frequently and those who maintained highly concentrated portfolios. The disposition effect alone accounted for an estimated annual return cost of 1.2 percentage points 14.

The impact of this bias extends beyond retail accounts; it is a structural flaw in human cognition that also damages professional funds. Research examining over 2,300 active mutual funds found that institutional managers are also susceptible to the disposition effect. "Disposition-prone" mutual funds systematically fall behind non-disposition-prone funds by 4% to 6% each year, demonstrating that even professionals struggle to override their biological wiring when managing drawdowns 124.

How Algorithms Exploit Human Psychology

One of the clearest proofs that the disposition effect is an emotional flaw rather than a rational market strategy is the behavior of artificial intelligence and algorithmic trading systems. AI-driven systems do not feel regret, fear, pride, or cognitive dissonance; they execute logical strategies based strictly on historical data and real-time probabilistic thresholds 12.

A study conducted by researchers at the Norges Bank in Norway investigated whether algorithmic traders exhibit the disposition effect similarly to their human counterparts. The findings were stark: human traders in the study realized their gains at a rate 43% higher than they realized their losses, actively displaying the disposition effect. In contrast, the algorithmic traders realized 34% of their gains and 33% of their losses, a statistically insignificant gap of just 1.5 percentage points 12.

This symmetrical execution means that algorithms do not systematically sell winners more than losers. By avoiding the bias driven by human emotions, algorithms maintain positive expectancy, essentially profiting off the predictable, irrational behaviors of retail traders who serve as liquidity providers while trapped in emotional trading loops 12. Behavioral interventions, such as broad framing (viewing decisions as a bundle rather than isolated events) and pre-set algorithmic stop-losses, have been shown to mitigate the disposition effect by up to 34% among treated users, further proving that removing emotion is key to profitability 1214.

Myth 3: "Averaging Down" Rescues Losing Trades

When a swing trade immediately moves into negative territory, beginners frequently deploy a strategy they believe will easily rescue the position: "averaging down." This technique involves purchasing additional shares of a declining asset at a price lower than the initial entry. Mathematically, this reduces the average cost basis per share of the entire position, meaning the stock requires a significantly smaller upward price rebound for the overall trade to break even 517.

Because averaging down lowers the break-even point, it provides an immediate cognitive cushion. It reduces the psychological pressure and the emotional urge to sell out of a losing position, allowing the trader to feel as though they are actively "managing" the problem rather than simply accepting a defeat 5. However, applying this technique in short-to-medium-term swing trading is universally considered by institutional analysts and behavioral economists as one of the most dangerous, account-destroying myths for beginners 1819.

The core flaw in averaging down is that it bases an active investment decision on a single, arbitrary factor: the asset's price has dropped 18. While long-term value investors might successfully use this tactic over multi-year horizons to accumulate fundamentally undervalued assets, swing traders operate on much tighter timelines where momentum, market structure, and liquidity matter deeply. A lower price does not inherently equate to better value; more often than not, it indicates severe structural weakness, institutional distribution, or impending negative fundamental news 17.

Averaging Down vs. Dollar-Cost Averaging

Retail traders frequently conflate the toxic habit of averaging down a bad swing trade with the legitimate, passive investment strategy known as Dollar-Cost Averaging (DCA). Understanding the distinction is critical for portfolio survival.

| Strategy Metric | Averaging Down (Swing Trading) | Dollar-Cost Averaging (Long-Term Investing) |

|---|---|---|

| Trigger for Purchase | Reactionary: Buying because the asset price dropped 18. | Proactive: Buying on a strict, predetermined calendar schedule 20. |

| Asset Class Focus | Often single, concentrated, aggressive individual equities 18. | Broadly diversified index funds or established ETFs 20. |

| Primary Goal | To lower the immediate break-even point and escape a losing trade 5. | To steadily build wealth over decades by smoothing out market volatility 20. |

| Risk Profile | Extremely high: Leads to over-concentration in underperforming assets 19. | Low to Moderate: Mechanically builds diversified market exposure 20. |

By systematically averaging down on a losing swing trade, a beginner achieves three disastrous outcomes. First, they suffer from capital concentration. They tie up an increasing percentage of their limited portfolio in their worst-performing asset, reducing essential diversification and destroying opportunity cost, as those funds could have been allocated to stronger-performing assets showing positive momentum 171819.

Second, they dramatically increase their compounded downside. Averaging down increases absolute downside exposure to a declining asset. If the anticipated market rebound never materializes, the financial losses are multiplied by the larger position size 1721. Good stocks can drop and stay down for lengthy periods, but fundamentally bad stocks are more likely to go down and stay down permanently 18.

Third, averaging down bypassing vital risk management protocols. It often replaces disciplined, predetermined exit strategies, such as hard stop-losses 17. What should have been a minor, managed 1% paper cut to the portfolio transforms into a catastrophic, unrecoverable drain. As one market analysis correctly notes, averaging down without structural confirmation is merely speculation disguised as strategy; it is the definition of throwing good money after bad 19.

Myth 4: Technical Indicators Are Crystal Balls

Because swing traders hold positions for days or weeks, they cannot rely solely on the decade-long horizons of fundamental analysis (like reading balance sheets), nor can they rely purely on the order-flow tape reading of day traders. Therefore, they rely heavily on technical analysis - the study of historical price and volume data - to make decisions.

Indicators such as the Moving Average Convergence Divergence (MACD), the Relative Strength Index (RSI), Bollinger Bands, and the Stochastic Oscillator are standard, default tools on virtually every retail trading platform globally 22. A pervasive myth among beginners is that these mathematical overlays possess inherent predictive power, capable of forecasting exactly where a stock will move next.

The mathematical reality is that nearly all standard technical indicators are strictly lagging, not predictive. They are derivative calculations of past price action, designed merely to confirm trends that are already underway or to highlight historical deviations from a mean average 24. They do not, and cannot, predict future buying or selling volume.

The RSI and MACD Debate in Academia

Academic studies evaluating the empirical effectiveness of technical indicators present a highly nuanced picture that rarely aligns with the "guaranteed" strategies sold by online trading gurus. Research has shown that combining multiple indicators can occasionally improve forecasting accuracy slightly better than a simple buy-and-hold strategy, but only under very specific, historical market conditions 246.

For example, a 2025 study assessing the effectiveness of the RSI and MACD indicators on the Indonesian banking sector (specifically the LQ45 index) found sharply diverging levels of accuracy. The researchers evaluated the indicators over a one-year period. The RSI demonstrated an impressive 97% accuracy level in correctly identifying overbought and oversold conditions, successfully calling 31 out of 32 signals 2226. In contrast, the MACD generated 166 signals, but was only successful on 86 of them, resulting in a coin-flip accuracy rate of 52% 22.

However, despite the RSI's high accuracy in identifying short-term extremes, the study noted that the MACD was actually superior in generating long-term trend returns due to its sensitivity to small momentum shifts 22. Furthermore, statistical testing across a broader dataset showed no significant difference in ultimate profitability between the two indicators 22. Another academic study testing weak-form efficiency in cryptocurrency markets analyzed 99 different assets using technical indicators. The authors concluded that trading strategies based on single indicators, or even combinations of two indicators, completely failed to generate higher returns than a simple, passive buy-and-hold strategy, indicating that retail traders over-rely on these tools to their detriment 7.

Institutional vs. Retail Strategy Complexity

The danger arises when beginners assume simple indicators function as automated profit machines. In modern financial markets dominated by high-frequency trading (HFT) environments and institutional algorithms, simple indicator crossovers frequently generate "false signals" due to massive market noise and artificial, machine-driven volatility 28.

A groundbreaking academic study analyzing comprehensive transaction data in the options market highlighted exactly how retail traders misuse technical analysis compared to institutions. The study found that 66% of active retail investors predominantly relied on simple, one-sided strategies (such as buying basic long calls or long puts) triggered by rudimentary technical signals 8. The study concluded that retail investors using these simple, indicator-driven strategies consistently lost money to the rest of the market. Conversely, institutional players profited immensely by employing complex strategies, particularly spread trading and volatility selling, which capitalize on the decay of options premiums rather than trying to perfectly predict directional price movement 8.

When retail traders optimize for "screen time" and stare intensely at lagging indicators on a one-minute or five-minute chart, they are not uncovering a secret algorithmic edge; rather, they are significantly increasing their likelihood of falling into the trap of overtrading 3031. In fact, recent research by NYU Stern found that the median retail investor spends just six minutes conducting research before executing a trade, overwhelmingly focusing entirely on price charts with a lookback period of a single day, ignoring both broader macro fundamentals and long-term technical context 31.

Myth 5: You Only Need an Edge, Not Risk Management

Perhaps the most lethal blind spot for beginner swing traders is the failure to understand the mathematics of the "Risk of Ruin." Risk of ruin refers to the mathematical probability that an individual's trading account will suffer a drawdown so severe that they lose enough capital to cease trading entirely, making recovery practically impossible 2132.

Many beginners focus 95% of their energy entirely on finding the perfect trading setup, indicator crossover, or entry signal, drastically neglecting position sizing. However, financial modeling proves that edge is not enough to survive the markets. Monte Carlo simulations - computational tools that run thousands of randomized scenarios based on a trader's specific win rate and risk-to-reward ratio - prove definitively that even a highly profitable, mathematically sound strategy will completely blow up an account if the risk allocated per trade is too high 833.

Sequence Risk and the Mathematics of Drawdowns

The hidden danger that Monte Carlo simulations reveal is known as "sequence risk," which is the statistical inevitability that a cluster of losing trades will occur in a row at some point in a trader's career 33. Financial markets are messy, dynamic, and full of unknown variables; therefore, winning and losing trades do not alternate perfectly 34.

Consider a swing trader utilizing a genuinely excellent strategy with a 55% win rate and a risk-to-reward ratio of 1:1.5 (meaning they win $1.50 for every $1.00 risked). According to the Kelly Criterion - a mathematical formula used to determine the optimal size of a series of bets - the trader has a massive mathematical edge 33. However, if that trader risks 25% of their capital per trade to maximize growth, a Monte Carlo simulator will show that they are mathematically guaranteed to experience drawdowns exceeding 80%, eventually leading to total psychological or financial ruin 33.

If a trader risks 5% of their capital per trade, a string of just 20 consecutive losses will wipe them out entirely. If they risk 10%, a streak of merely 10 losers zeroes the account 35.

The mathematics of drawdowns are deeply unforgiving and highly non-linear. Because financial losses compound geometrically, recovering from a severe drawdown requires a disproportionately larger percentage gain just to return the account to its initial break-even point 21.

| Account Drawdown (Capital Lost) | Required Gain Simply to Break Even | Consequence on Trading Psychology and Viability |

|---|---|---|

| 10% | 11% | Normal market volatility; relatively easy to recover with standard strategy 21. |

| 25% | 33.3% | Requires significant market outperformance; emotional stress and doubt begin 21. |

| 50% | 100% | Account is severely damaged; requires doubling the remaining capital just to reach zero 21. |

| 75% | 300% | Mathematical ruin; recovery depends more on extreme luck than skill. The account is effectively dead 21. |

When a swing trader suffers a 25% drawdown and immediately increases their position size in a desperate bid to "make up for" previous losses, they accelerate their trajectory toward the 75% ruin threshold. The deeper the drawdown, the harder it becomes to recover, because the remaining capital simply cannot absorb normal market volatility anymore 21.

This non-linear math is precisely why institutional risk management protocols typically cap risk at an absolute maximum of 1% to 2% of total equity per trade. At a 1% risk level, an account can theoretically survive over 100 consecutive losses. Keeping risk this small serves as capital insurance; it ensures the trader stays in the game long enough for their genuine statistical edge to finally play out over thousands of trades 213536.

The Biological Hijack: Gamification and the Emotional Cycle

The raw mechanics of losing money - asymmetric trade sizing, ignoring the disposition effect, averaging down, and ignoring risk of ruin - are often drastically accelerated by the environment in which modern retail trading takes place. During the post-pandemic surge in retail market participation, mobile brokerage platforms introduced controversial "digital engagement practices" (DEPs) meticulously designed to mimic the addictive feedback loops of video games and social media 938.

These platform features include aggressive push notifications, celebratory confetti animations upon executing a trade, digital badges, competitive leaderboards, and prize draws. While marketed as tools to democratize finance and increase user engagement, these features deliberately trigger dopamine responses identical to casino gambling, fostering a highly reactive, short-term mindset and encouraging severe overtrading among novices 1040.

The UK's Financial Conduct Authority (FCA) recently conducted a massive online experiment with over 9,000 consumers to test these features. In an FCA first, the regulator built an experimental trading platform and concluded that gamified apps pushed users to invest in complex products far beyond their actual risk appetite, increasing the frequency of impulsive trading, particularly among younger participants and those with lower financial literacy 941.

Academic research analyzing 142 distinct app updates from 17 major US brokers further demonstrated the financial toll of gamification. The researchers found that as platforms introduced more game-like features, retail traders took on significantly more risk. Each gamified update systematically harmed the retail user, decreasing their average return by 0.19% and increasing their return volatility by 0.13%, while simultaneously making their order flow more predictable and profitable for institutional liquidity providers on the other side of the trade 38.

Revenge Trading and the Threat Response

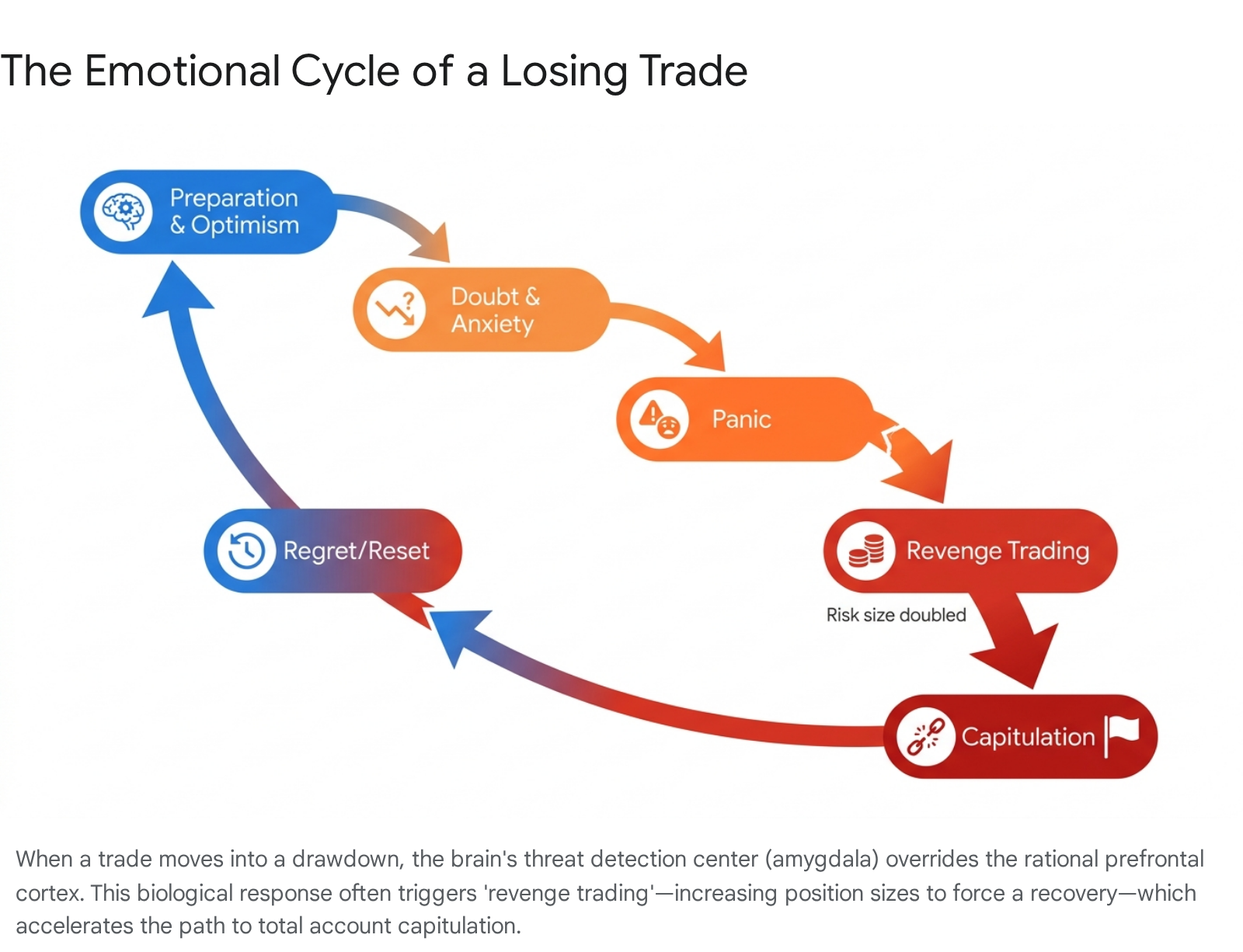

This gamified, high-stimulation environment directly exacerbates what professional traders refer to as the "Emotional Cycle." Every trader experiences emotional swings, but beginners are entirely ruled by them.

When a retail trader is down heavily on the day, their brain does not process the red numbers on the screen as abstract data. Because the human brain evolved for physical survival in probabilistic environments, it cannot distinguish between a severe financial threat and a literal physical threat 4243. The amygdala - the brain's threat detection center - fires with massive intensity, triggering a cascade of stress hormones including cortisol, adrenaline, and norepinephrine 43.

During this biological hijack, cognitive processing forcibly shifts away from the rational, analytical prefrontal cortex and directly into the emotional limbic system 43. The trader enters a predictable psychological loop that transitions from optimism, to anxiety, to denial, and finally to panic 44.

Rather than accepting a small, mathematically sound 1% loss, the hijacked brain demands immediate relief and control, pushing the trader into the "revenge trading" stage 4345. In this state, the beginner will double their position size, abandon their technical indicators, ignore stop-losses entirely, and frantically execute sub-optimal setups simply to win the money back 4346. The combination of a highly gamified mobile interface and an emotionally hijacked brain is the final, lethal catalyst that translates a standard, expected market drawdown into total account capitulation 4344. Data from proprietary trading firms indicates that a staggering 82% of traders fail their evaluations within the first week entirely due to these easily predictable psychological and behavioral errors 43.

Bottom line

The widespread belief that swing trading serves as an accessible pathway to outperforming the broader market is thoroughly debunked by vast quantities of regulatory data, which demonstrate that upwards of 80% to 90% of retail participants systematically lose their capital. The root cause of this massive failure rate is rarely a lack of screen time, inadequate charting software, or a failure to find the "perfect" technical indicator. Rather, the destruction of retail accounts is driven by an inability to overcome deeply ingrained biological biases like the disposition effect, leading traders to mathematically ruin their expectancy by cutting winners early and riding losers to the bottom. Ultimately, long-term survival and profitability in swing trading relies entirely on overriding human emotion with strict mathematical risk management, fractional position sizing, and accepting that avoiding the risk of ruin is far more important than predicting the next price swing.