5 Scenarios for the Space Economy by 2035

The global space economy is projected to nearly triple from $613 billion in 2024 to $1.8 trillion by 2035, driven primarily by the rapid deployment of low Earth orbit (LEO) satellite constellations. As launch costs plummet and commercial players dominate the market, this technological boom will reshape terrestrial industries, introduce direct-to-device mobile connectivity, and trigger a fierce geopolitical race for sovereign satellite networks. However, this explosive growth faces severe existential threats from orbital debris cascades, regulatory gridlock over spectrum rights, and escalating electronic warfare that could cripple global navigation systems.

The Dawn of a Trillion-Dollar Frontier

Space is no longer a distant, government-dominated frontier. Today, it is deeply woven into the fabric of daily terrestrial life, supporting everything from agricultural supply chains and digital nomadic workforces to disaster mitigation and national defense 12.

The global space economy reached a record $613 billion in 2024, reflecting a strong 7.8% to 8% year-over-year growth from 2023 34. The fundamental driver of this transition is the commercial sector, which now accounts for approximately 78% to 80% of total industry revenue 45. Government budgets, while still growing (reaching $132 billion in 2024), now make up the remaining minority share 47. By the second half of this decade, commercial markets are expected to outspend government programs by a factor of two to one in nearly all end markets, except for specific Earth observation missions .

This commercialization has been catalyzed by a dramatic reduction in launch costs. In 2010, launching one kilogram of payload into LEO cost approximately $18,000 9. Today, thanks to the development of reusable launch technology pioneered by companies like SpaceX, Blue Origin, and Rocket Lab, that figure has plummeted by roughly 90% to between $1,500 and $2,000 per kilogram 5910. This unprecedented drop in overhead has made mega-constellations containing thousands of satellites economically viable, setting the stage for five distinct scenarios that will define the space economy over the next decade.

Scenario 1: A Multi-Trillion Dollar Economic Boom

The space industry is currently approaching a critical inflection point. As satellite internet deployment accelerates, the industry is transitioning from a niche aerospace sector into a foundational backbone for global commerce 111.

Trajectories of Expansion

Joint research from the World Economic Forum and McKinsey & Company estimates that the global space economy will reach $1.8 trillion by 2035 1. Other feasibility models, factoring in deep-space logistics and hypersonic travel, push this valuation as high as $2.7 trillion by 2040 9.

Industry analysts have modeled three potential economic trajectories for the space economy over the next decade, hinging on launch capabilities and regulatory stability 311:

| Economic Scenario | Projected Value (2035) | Key Drivers and Assumptions |

|---|---|---|

| Base Case | $1.1 Trillion to $1.8 Trillion | Steady 9% to 12% compound annual growth rate (CAGR). Reusable launches scale as currently projected, driving heavy adoption of LEO communications. |

| Upside Scenario | $2.2 Trillion to $2.3 Trillion | Accelerated 18% CAGR. Next-generation heavy-lift reusable rockets achieve full reusability early, slashing costs further and expanding in-space manufacturing and tourism. |

| Downside Scenario | $800 Billion to $1.4 Trillion | Capped at 8% CAGR. Growth is stunted by geopolitical tensions, severe orbital debris incidents (Kessler Syndrome), or breakthroughs in terrestrial networks that reduce satellite demand. |

Terrestrial Industries Driving Demand

Crucially, the majority of this economic expansion will not come from traditional aerospace manufacturing. Projections indicate that more than 60% of the revenue growth in the space economy by 2035 will be generated by five terrestrial sectors: supply chain and transportation, food and beverage, state-sponsored defense, retail and consumer goods, and digital communications 2116.

For example, satellite data is already being used to optimize shipping logistics, monitor crop health through Earth observation imagery, and provide high-speed broadband to rural enterprises 78. The enterprise network segment is expected to dominate demand, as energy, maritime, and logistics firms increasingly require secure data transfers, Internet of Things (IoT) support, and cloud access in remote areas where laying fiber-optic cables is physically or economically unfeasible 916.

The Launch Volume Acceleration

To support this demand, the volume of hardware entering orbit is scaling exponentially. In 2023, over 1,500 tons of spacecraft were launched - a 50% increase from the previous year 7. Looking ahead, industry forecasts predict that more than 43,000 satellites will be launched between 2025 and 2035, averaging roughly 12 satellite launches per day 10. This surge is expected to drive a $665 billion satellite manufacturing and launch services market over the next decade 10. By 2035, total orbital launches are projected to exceed 967 annually, with SpaceX and the China Aerospace Science and Technology Corporation (CASC) accounting for a combined 69% of the global total 11.

Scenario 2: The Sovereign Constellation Race

The most visible manifestation of the modern space economy is the race to deploy low Earth orbit (LEO) broadband networks. LEO satellites orbit much closer to the Earth than legacy geostationary (GEO) satellites, dramatically reducing signal latency and enabling speeds capable of supporting modern digital activities like video conferencing and cloud computing 912. However, the LEO landscape is rapidly evolving from a commercial frontier into a strategic geopolitical battleground.

Western Commercial Dominance

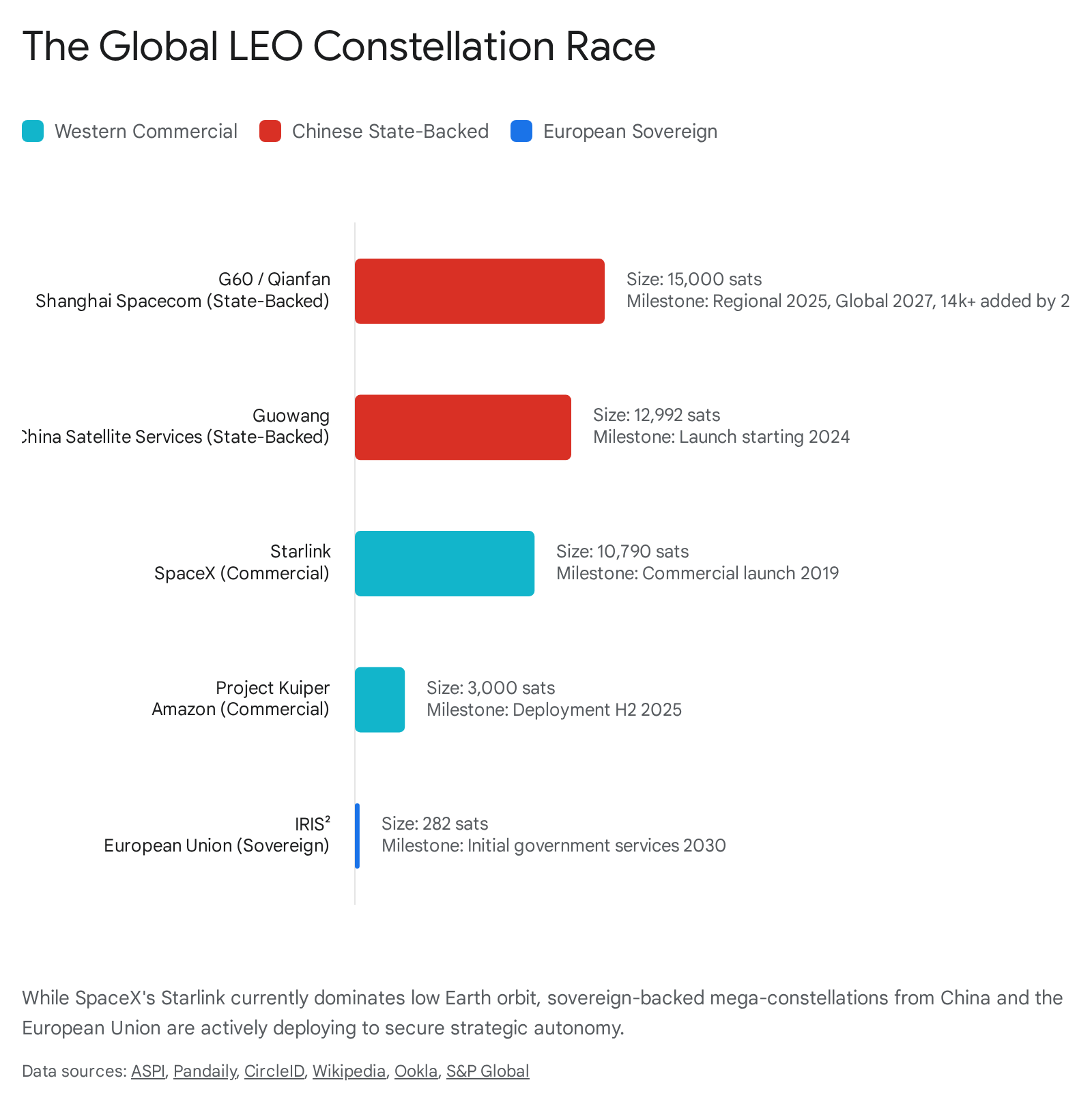

Currently, the LEO internet market is heavily dominated by SpaceX's Starlink, which holds a massive first-mover advantage 20. As of late 2025, SpaceX had launched over 10,790 Starlink satellites, securing 9.2 million active customers worldwide 12. The sheer scale of this deployment is reflected in global performance data; in the third quarter of 2025, Starlink accounted for 97.1% of all global satellite Speedtest samples, with legacy GEO providers Viasat and HughesNet trailing at 1.7% and 1.0%, respectively 12.

Amazon's Project Kuiper is also emerging as a major Western competitor. Backed by extensive cloud and logistics infrastructure, Amazon launched the initial batches of its planned 3,200-satellite constellation in 2025, aiming to integrate space-based connectivity directly with terrestrial data centers 913.

China's "Thousand Sails" and the Digital Iron Curtain

Recognizing the strategic vulnerability of relying on Western-controlled communications networks, foreign powers are aggressively accelerating their own sovereign alternatives 20. China treats dominance in LEO as a critical national security priority and is currently constructing three distinct mega-constellations: the Guowang project (approximately 13,000 satellites), the Honghu-3 constellation (10,000 satellites), and the G60 project, also known as "Qianfan" or "Thousand Sails" 141524.

Led by Shanghai Spacecom Satellite Technology (SSST) and backed by the Shanghai Municipal Government, the G60 constellation successfully launched its first batch of 18 satellites into polar orbit via a Long March 6A rocket in August 2024 142425. The project has aggressive milestones: achieving regional network coverage with 648 satellites by 2025, global coverage by 2027, and deploying a massive fleet of up to 15,000 satellites by 2030 to offer direct-to-mobile services 1415.

Geopolitical analysts warn that China's satellite initiatives are not merely for domestic connectivity. By offering state-backed satellite internet to developing nations - particularly those participating in its Belt and Road Initiative across Southeast Asia and Africa - China aims to export its digital governance model 1424. If widely adopted, this could establish a "digital Iron Curtain" from space, extending state surveillance and controlling the free flow of information on a global scale 14.

Europe's Quest for Autonomy: IRIS2

The European Union is similarly uncomfortable relying on commercial American entities or foreign state actors for its critical infrastructure. In response, Europe is advancing IRIS2 (Infrastructure for Resilience, Interconnectivity and Security by Satellite), its third flagship space program alongside Galileo and Copernicus 1617.

Scheduled for initial government deployment in 2030, IRIS2 is a €10.5 billion multi-orbit initiative consisting of 264 LEO satellites and 18 MEO satellites 18. Managed via a 12-year concession contract with the SpaceRISE consortium - comprising Eutelsat, SES, and Hispasat - IRIS2 is fundamentally different from Starlink 1718. It is not designed as a mass-consumer mega-constellation; rather, it is a highly secure, sovereign network intended to protect European embassies, military theaters, and critical infrastructure from cyber and hybrid threats 1629.

However, IRIS2 faces commercial viability challenges. Telecommunications executives warn that to successfully attract private enterprise customers, the EU-backed system will ultimately have to match the pricing and performance benchmarks set by Starlink and Project Kuiper, an incredibly difficult task in a capital-intensive and price-sensitive market 30.

| Constellation | Origin | Primary Backing | Planned Fleet Size | Strategic Focus |

|---|---|---|---|---|

| Starlink | USA | Commercial (SpaceX) | ~12,000+ | Mass consumer & enterprise broadband dominance. |

| Project Kuiper | USA | Commercial (Amazon) | ~3,200 | Cloud integration; broadband services. |

| G60 (Qianfan) | China | State (Shanghai Govt.) | 14,000 to 15,000 | Sovereign autonomy; digital infrastructure export. |

| Guowang | China | State (China SatNet) | ~13,000 | Secure national communications. |

| IRIS2 | EU | Sovereign (SpaceRISE) | ~290 (Multi-orbit) | Governmental security; cyber resilience. |

Scenario 3: The Direct-to-Device (D2D) Revolution

Historically, connecting to a satellite network required expensive, specialized hardware and dedicated antennas. That dynamic is changing through the advent of Direct-to-Device (D2D) or Direct-to-Cell technology, which enables standard, unmodified smartphones to communicate directly with satellites in orbit 3132. By functioning essentially as cell towers in space, D2D networks promise to eradicate mobile dead zones globally, extending connectivity to remote oceans, deserts, and rural communities 3219.

The Mechanics and Limitations of Space-Based Cellular

Because providing D2D service generally requires the use of established terrestrial radio spectrum, satellite operators have been forced to forge partnerships with mobile network operators (MNOs) 3119. SpaceX has partnered with T-Mobile in the United States, while other firms like AST SpaceMobile and Lynk Global have pursued similar supplementary coverage agreements 919. Apple, conversely, pioneered a "walled garden" approach by utilizing Globalstar's mobile satellite service spectrum to offer emergency SOS messaging built directly into its latest iPhones 19.

Despite the transformative potential, D2D technology currently operates under strict physical limitations: * Low Initial Capacity: A single satellite can only handle a fraction of the simultaneous connections managed by a terrestrial cell tower 31. Early D2D services are strictly limited to text messaging and low-bitrate data. For instance, some initial direct satellite calls operated at just 800 bits per second 31. Voice and high-speed data will require the deployment of thousands of additional, highly advanced satellites 3435. * Line-of-Sight Requirements: Satellite signals struggle to penetrate solid objects. For a standard smartphone to establish a connection, the user typically must be outdoors with a clear, unobstructed view of the sky 31. The service is unreliable indoors, underground, or in dense urban areas with tall buildings 31. * Power Consumption: Pinging a satellite hundreds of miles away requires significantly more transmission power than connecting to a nearby cell tower, which can rapidly drain a smartphone's battery 31.

Market Impact and Consumer Pricing

For the average consumer, D2D will not replace traditional 5G networks. Instead, it is being marketed as a premium, supplementary safety net. Pricing structures revealed during T-Mobile's early integration of Starlink highlight this strategy: the service is offered for free on the highest-tier premium cellular plans, but requires a $10 to $15 monthly add-on fee for standard plans, and up to $20 per month for users roaming from rival carriers 35.

This pricing model is highly advantageous for telecom providers. It acts as a powerful incentive to push customers toward ultra-premium subscriptions, which are a major driver of carrier revenue 35. Consumer appetite is strong; surveys from 2025 indicate that over 70% of respondents are interested in satellite mobile services, and nearly a third are willing to pay a monthly premium to ensure they never lose connectivity 1920. Consequently, D2D capability is expected to become a critical differentiator for mobile carriers seeking to reduce customer churn over the next decade 19.

Scenario 4: The Kessler Syndrome and Orbital Debris

The rapid proliferation of mega-constellations required to sustain a $1.8 trillion space economy carries a catastrophic environmental risk: space debris. Earth's low orbit is currently congested with over 9,000 metric tons of junk, including defunct satellites, spent rocket stages, and fragments from past collisions 21.

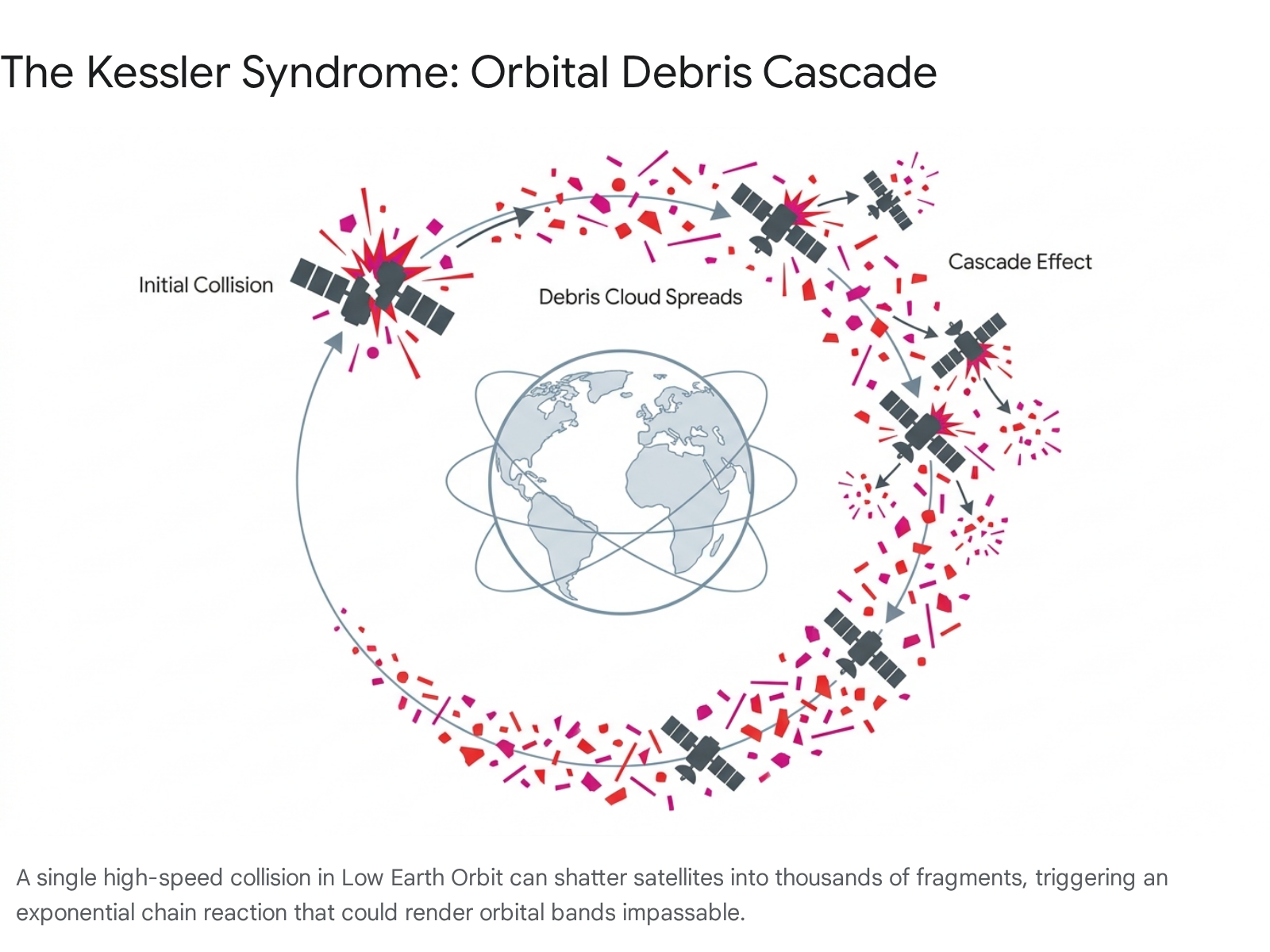

The most severe consequence of this congestion is the Kessler Syndrome. Proposed by NASA scientists Donald J. Kessler and Burton G. Cour-Palais in 1978, the Kessler Syndrome describes a runaway chain reaction of orbital collisions 2223. Because objects in LEO travel at extreme velocities - up to 28,000 km/h - even an impact with a millimeter-sized paint chip carries the kinetic energy of an explosive 2140.

The Highway Pileup Analogy

To visualize the Kessler Syndrome, imagine a busy highway where cars are traveling at 28,000 km/h. If one vehicle crashes, it shatters into thousands of high-speed fragments. These fragments immediately strike surrounding cars, which also explode into debris. In space, this cascading effect creates an exponentially expanding cloud of high-speed shrapnel 21. Over time, this self-sustaining cascade could render entire bands of LEO completely impassable, threatening critical infrastructure like GPS systems, weather forecasting satellites, and the International Space Station 212223.

Many experts fear this process is already slowly underway. In 2009, a defunct Russian Cosmos satellite collided with an active American Iridium satellite, instantly spawning thousands of new debris fragments 2140. Furthermore, intentional anti-satellite (ASAT) missile tests conducted by the United States, Russia, China, and India have exacerbated the crisis. These tests alone generated 6,851 cataloged pieces of trackable debris, of which nearly 3,000 remain hurtling through orbit today 24.

Circular Economies and Market Solutions

Without aggressive mitigation, industry models suggest a 15% to 25% probability of a major cascade event by 2035, which could destroy up to 40% of satellite assets in LEO and trigger tens of billions of dollars in insurance losses 9. Paradoxically, this existential threat is birthing a new sub-industry. The market for active debris removal, orbital sustainability, and in-space satellite servicing is projected to reach an $8 billion to $12 billion valuation by the late 2030s 9. Experts advocate for adopting "circular economy" principles in space - focusing on repairing, refueling, and recycling spacecraft in orbit - though widespread adoption remains stymied by high costs and regulatory ambiguity 25.

Scenario 5: Regulatory Gridlock, Spectrum Wars, and Space Security

As physical space becomes congested, the invisible infrastructure that enables satellite communication - radio frequencies and orbital slots - is also becoming a fiercely contested battleground. The governance of these resources relies on legal frameworks designed for a bygone era.

Who Owns the Sky?

The fundamental legal debate over airspace and outer space dates back to ancient Roman law and the doctrine of cujus est solum ejus est usque ad coelum - "whoever owns the soil, it is theirs up to the sky" 434426. This concept survived until the dawn of commercial aviation, when governments systematically claimed sovereignty over navigable airspace 4326. In the United States, the 1946 Supreme Court case United States v. Causby established that property owners only control the "immediate reaches" of the atmosphere necessary to enjoy their land; everything above is public domain regulated by the federal government 4627.

Moving higher into orbit, the legal landscape changes drastically. The 1967 Outer Space Treaty, signed by over 115 nations, serves as the foundation of international space law 2829. Article II of the treaty explicitly prohibits national appropriation, meaning no country, corporation, or individual can legally claim sovereignty over an orbital slot or celestial body 283051.

Spectrum Scarcity and "Paper Satellites"

Because orbital slots cannot be owned, the right to operate satellites and transmit on specific radio frequencies is coordinated globally by the International Telecommunication Union (ITU) 3132. The ITU historically assigned geostationary slots on a "first-come, first-served" basis. Because these slots are scarce and highly lucrative, a speculative loophole emerged known as "over-filing" 32. Nations and corporations register unneeded "paper satellites" simply to hoard orbital positions, effectively locking out emerging competitors who have genuine, near-term operational needs 32.

While LEO networks do not rely on fixed physical slots in the same way GEO satellites do, the radio spectrum remains a critical bottleneck 31. Decades-old spectrum-sharing regulations are increasingly misaligned with modern technology. Satellite operators are pressuring bodies like the FCC and the ITU to modernize interference frameworks to allow dense LEO mega-constellations to coexist without degrading global signal quality 54.

Electronic Warfare and GPS Interference

Beyond bureaucratic gridlock, deliberate interference is rapidly becoming one of the most pressing threats to the space economy. Global shipping, aviation, and financial infrastructure rely heavily on Global Navigation Satellite Systems (GNSS) such as the American GPS, Europe's Galileo, and Russia's GLONASS 55.

Recent years have witnessed a severe escalation in electronic warfare targeting these systems. In March 2026, maritime tracking agencies reported a 50% surge in satellite jamming (blocking the signal) and spoofing (transmitting false positioning data), heavily concentrated around geopolitical flashpoints 55. During peak disruptions, traffic through vital maritime corridors like the Strait of Hormuz saw massive drops in reliable navigation capability, as civilian cargo ships reported their digital infrastructure being entirely "blinded" by electronic attacks 56.

While jamming and spoofing do not physically destroy space assets, they paralyze the terrestrial economies that depend on them 5533. The lack of a centralized, real-time global detection network for GPS interference leaves critical infrastructure highly vulnerable 33. Moving forward, protecting the space economy will require massive investments not just in physical rockets, but in interference-resistant technologies and secure, encrypted communication links 5556.

Bottom line

The space economy is rapidly transitioning from a government-funded exploratory frontier into a $1.8 trillion commercial engine, driven by the mass deployment of low Earth orbit internet constellations and direct-to-device cellular technology. While these innovations promise to bridge the digital divide and revolutionize terrestrial logistics, they have sparked a tense geopolitical race as nations scramble to build sovereign networks to avoid reliance on Western tech monopolies. Ultimately, the long-term viability of this multi-trillion-dollar industry hinges on humanity's ability to mitigate the physical threat of orbital debris and modernize international laws to prevent devastating electronic warfare.