Will Congress Pass Stablecoin Laws Before the 2026 Midterms

The legislative landscape for digital assets in the United States has reached a critical inflection point as of May 2026, characterized by a bifurcated regulatory reality. The United States Congress has successfully established a definitive framework for dollar-pegged stablecoins through the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act, which was enacted in July 2025 and is currently navigating an intricate, multi-agency rulemaking phase 12. Simultaneously, broader market structure reform - embodied in the Digital Asset Market Clarity (CLARITY) Act - has cleared the Senate Banking Committee but faces a precarious path to secure the 60 votes required for cloture on the Senate floor 24. This immediate legislative reality means that while the issuance, reserve requirements, and compliance obligations for payment stablecoins are now codified in federal law, the broader jurisdictional boundaries between the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) regarding the trading of digital commodities remain unresolved, suspended within a highly congested election-year congressional calendar 56.

For the general reader, the stakes of this legislative maneuvering extend far beyond the esoteric debates of financial technologists. The traditional, legacy financial system currently operates with a massive amount of hidden friction that acts as a silent tax on the broader economy. Everyday consumers and merchants lose tens of billions of dollars annually to credit card interchange fees, foreign exchange markups, and delayed settlement times when executing basic commercial transactions or remitting funds across borders 78. The codification and mainstream adoption of regulated stablecoins pave the way for frictionless, nearly instantaneous digital payments integrated directly into smartphone digital wallets and retail applications. This technological shift possesses the potential to entirely eliminate the standard 2% to 3% transaction fee that legacy card networks impose on merchants - savings that can ultimately be passed down to the consumer at the checkout counter 910.

To fully comprehend the significance of this shift, it is necessary to establish a real-world analogy that corrects common misconceptions regarding the varied forms of digital currency, specifically separating volatile cryptocurrencies and Central Bank Digital Currencies (CBDCs) from payment stablecoins. Volatile cryptocurrencies, such as Bitcoin or Ethereum, operate much like digital gold or speculative commodities; their value fluctuates wildly based on market supply and demand, rendering them wholly unsuitable for pricing everyday goods or paying a monthly mortgage 611. Conversely, Central Bank Digital Currencies function like programmable casino chips issued directly by the house - in this case, the federal government. Because CBDCs are managed on a centralized government ledger, they carry profound implications for privacy and state surveillance, theoretically allowing the issuing monetary authority to monitor, restrict, or program individual spending behaviors 1213.

Payment stablecoins exist in the pragmatic middle ground, functioning much like heavily regulated, digital gift cards or private casino chips issued by vetted private-sector financial institutions. Under the newly established statutory frameworks, every digital stablecoin must be backed on a strict one-to-one basis by a physical U.S. dollar or a highly liquid cash equivalent, such as a short-term Treasury bill, held securely in a regulated bank vault 1415. This mechanism ensures that the token retains a perfectly stable value while simultaneously offering the instantaneous, cross-border transmission speed of a cryptocurrency, entirely avoiding the direct government surveillance apparatus inherent to a CBDC 1617.

FAQ 1: What is the current status of the top competing legislative proposals?

The 119th Congress has produced a complex matrix of interconnected legislation designed to address distinct facets of the digital asset ecosystem. Lawmakers have recognized that a monolithic approach to digital asset regulation is unfeasible, prompting a strategy that addresses stablecoins, market structure, taxation, and central bank powers through separate, targeted bills. The following table outlines the core components, regulatory focus, and specific May 2026 status of the four most consequential proposals shaping U.S. financial policy, utilizing data compiled from congressional committee records, the Congressional Research Service (CRS), and GovTrack.

| Legislative Proposal | Primary Focus & Regulatory Scope | Key Statutory Provisions | Current Status (May 2026) | Lead Regulators |

|---|---|---|---|---|

| GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act) | Federal framework for payment stablecoins; Reserve backing and issuer licensing. | Mandates 1:1 reserves in U.S. dollars/Treasuries; prohibits algorithmic stablecoins; imposes strict AML/OFAC compliance; allows dual federal/state chartering pathways for issuers with specific market cap thresholds. | Enacted (Signed into law July 18, 2025). Currently in the agency rulemaking phase, with compliance deadlines expected by early 2027. | Federal Reserve, OCC, FDIC, Treasury (FinCEN/OFAC), State Regulators. |

| CLARITY Act (Digital Asset Market Clarity Act of 2025) | Broader digital asset market structure; SEC vs. CFTC jurisdictional boundaries. | Establishes the "mature blockchain test" to classify decentralized tokens as commodities; mandates registration for crypto exchanges/dealers; limits stablecoin yield and interest payouts. | Pending Senate Floor Vote. Passed House July 2025 (294-134); advanced by Senate Banking Committee May 14, 2026 (15-9). | CFTC, SEC. |

| Anti-CBDC Surveillance State Act (H.R. 1919) | Prohibition of retail Central Bank Digital Currencies. | Amends the Federal Reserve Act to strictly prohibit the Fed from issuing a CBDC directly to individuals or utilizing a digital currency to conduct monetary policy without express congressional authorization. | Pending Senate Consideration. Passed House July 2025; attached as Title VI of the CLARITY Act and separately attached to the NDAA. | Federal Reserve (Prohibitive). |

| Digital Asset PARITY Act (Protection, Accountability, Regulation, Innovation, Taxation, and Yields Act) | Modernization of digital asset taxation and reporting. | Creates a deemed-basis rule for regulated stablecoins to exempt routine consumer transactions from capital gains taxes (if variance is <1%); establishes safe harbors for foreign investors. | Introduced. Bipartisan introduction in the House Ways and Means Committee on May 19, 2026. | IRS, Department of the Treasury. |

The passage of the GENIUS Act (S. 1582) marked a historical milestone as the first major legislative framework enacted into law in the United States specifically targeting digital assets 23. Originally building upon the foundation laid by former Chair Patrick McHenry's Clarity for Payment Stablecoins Act in the 118th Congress and the subsequent Lummis-Gillibrand Payment Stablecoin Act, the GENIUS Act successfully navigated bipartisan hurdles to pass the Senate 68-30 and the House 308-122 24. As noted by the Congressional Research Service, the legislation definitively answers whether non-bank financial firms and non-financial commercial firms can issue stablecoins, provided they adhere to the same rigorous 1:1 reserve requirements as traditional banks 5.

Meanwhile, the CLARITY Act (H.R. 3633) represents an ambitious attempt to completely overhaul the broader market structure. It passed the House of Representatives in July 2025 with a commanding bipartisan vote of 294-134, seeing 78 Democrats cross the aisle to support the Republican-led initiative 2122. The Senate Banking Committee, under Chairman Tim Scott, advanced a substitute version of the bill on May 14, 2026, through a narrower 15-9 vote, setting the stage for a highly contested floor debate 422.

FAQ 2: How do the GENIUS Act and CLARITY Act differ in scope and federal-state power dynamics?

The GENIUS Act and the CLARITY Act represent two fundamentally distinct philosophical approaches to financial regulation, differing primarily in their scope and their treatment of the traditional federal-state power dynamic. The tension between state-level innovation and federal preemption has been a defining feature of American financial regulation for over a century, and the digital asset space has inherited this exact jurisdictional battle.

The GENIUS Act is narrowly tailored to payment stablecoins and establishes a dual-track licensing regime that delicately balances federal oversight with traditional state banking authority 46. The legislation allows payment stablecoin issuers with a consolidated total outstanding issuance of $10 billion or less to opt for a state-level regulatory regime rather than submitting directly to federal agencies 46. This preserves the authority of state regulators, such as the New York Department of Financial Services (NYDFS), which has long managed its own robust "BitLicense" framework, and the California Department of Financial Protection and Innovation under its forthcoming Digital Financial Assets Law (DFAL) 247.

However, this state autonomy is heavily conditioned and strictly monitored by federal authorities. The Treasury Department, operating alongside the Federal Reserve and the Federal Deposit Insurance Corporation (FDIC), maintains the ultimate authority to determine whether a state's regulatory framework is "substantially similar" to the federal standard 68. To enforce this, the Act relies on a newly established Stablecoin Certification Review Committee (SCRC). This committee must unanimously certify that a state's rules do not materially weaken uniform federal requirements regarding 1:1 reserve backing, anti-money laundering (AML) controls, and bankruptcy protections 68. If a state attempts to initiate a regulatory "race to the bottom" to attract issuers with lax oversight, federal standards automatically preempt the state regime 89. For entities exceeding the $10 billion outstanding issuance threshold, a transition to direct federal regulation under the Office of the Comptroller of the Currency (OCC) or the Federal Reserve is mandatory, effectively centralizing the oversight of all systemically important stablecoin issuers 1011.

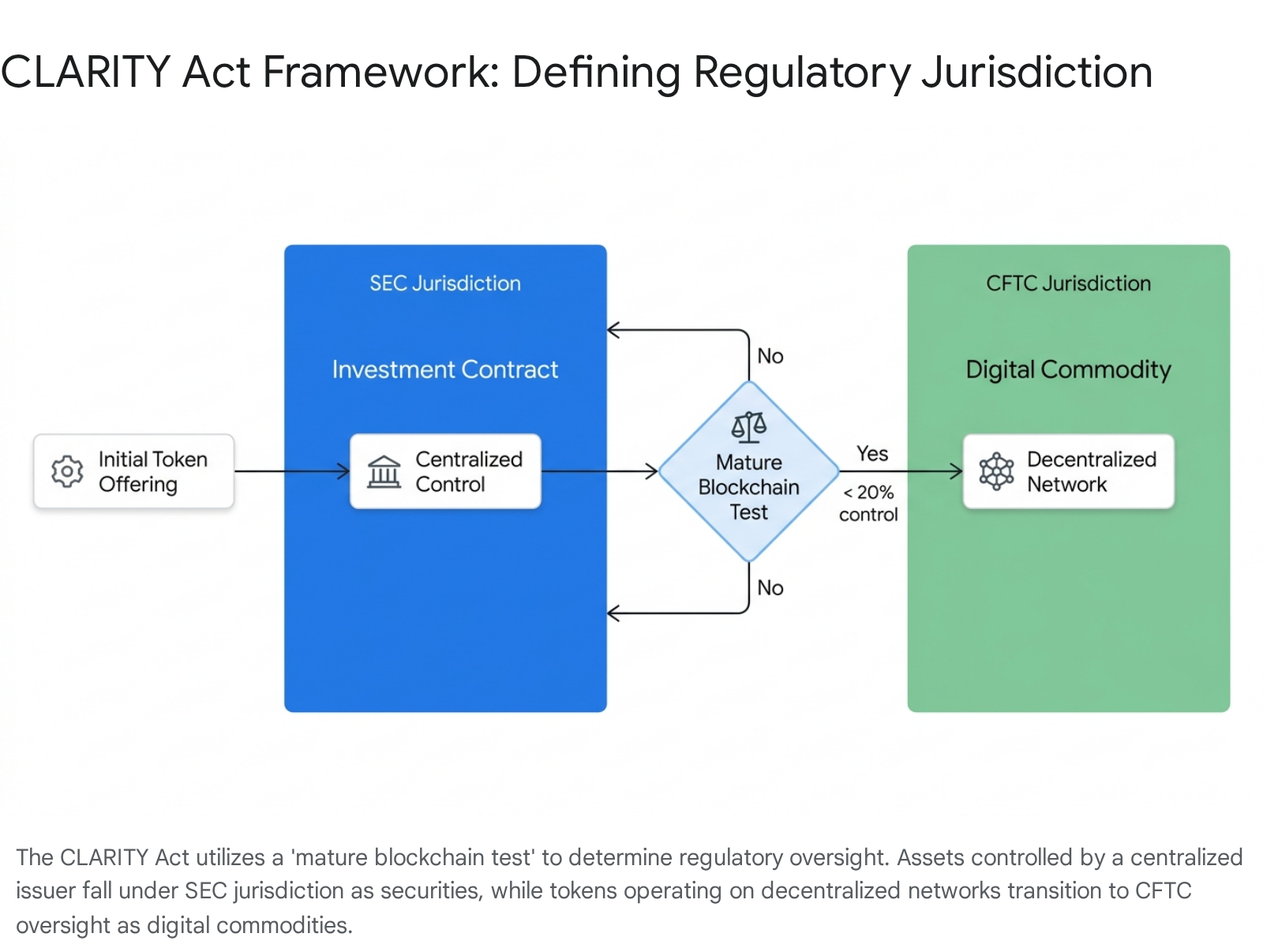

Conversely, the CLARITY Act operates on a much broader canvas, seeking to permanently resolve the jurisdictional turf war between the SEC and the CFTC over the entirety of the digital asset market 530. The cornerstone of the CLARITY Act is the "mature blockchain test," which provides a statutory mechanism for digital assets to transition from being classified as investment contracts - securities subject to SEC oversight - to digital commodities subject to CFTC oversight, provided their underlying networks become sufficiently decentralized 615.

The Senate Banking Committee's substitute draft of the CLARITY Act, advanced in May 2026, utilizes a qualitative "common control" test. This test evaluates whether the network remains meaningfully controlled by the issuer, insiders, or affiliated parties, generally looking for thresholds where no single entity controls 20 percent or more of the token supply or governance rights 1531. Where the GENIUS Act embraces state regulators through its dual-track system, the CLARITY Act leans heavily toward federal preemption. The CLARITY Act explicitly preempts state securities laws concerning digital commodities, aiming to prevent a fragmented patchwork of state-level enforcement actions from disrupting national and international trading platforms 3212. By granting the CFTC exclusive jurisdiction over spot markets for digital commodities and introducing federal registration requirements for all digital asset intermediaries, the CLARITY Act effectively consolidates market structure oversight at the federal level, leaving states with preserved authority only in exceedingly narrow areas such as anti-fraud enforcement 1234.

FAQ 3: What are the primary concerns delaying the implementation of the GENIUS Act and the Senate floor vote for the CLARITY Act?

Despite the immense momentum generated by bipartisan committee votes and the formal enactment of the GENIUS Act, the translation of statutory text into functional, day-to-day market architecture has been severely bogged down by deep ideological divides and complex administrative rulemaking processes.

For the GENIUS Act, which is already the law of the land, the delay stems from the extreme intricacies of interagency coordination. The legislation mandates that the Federal Reserve, the FDIC, the OCC, the National Credit Union Administration (NCUA), and the Treasury Department issue coordinated implementing regulations by July 2026 113. The law is scheduled to take full effect either 18 months after its enactment or 120 days after these final rules are published - pointing toward an effective operational date in early 2027 12. A primary point of friction within this rulemaking phase is the joint proposal issued by the Financial Crimes Enforcement Network (FinCEN) and the Office of Foreign Assets Control (OFAC) in April 2026 36.

These sweeping rules formally classify Permitted Payment Stablecoin Issuers (PPSIs) as financial institutions under the Bank Secrecy Act, requiring them to implement sophisticated, tech-native sanctions screening and transaction monitoring systems capable of tracking illicit funds across decentralized wallet addresses globally 3614. Traditional compliance departments are struggling to map existing, legacy bank-era AML frameworks onto decentralized digital asset infrastructure, causing widespread industry anxiety over the massive operational lift and technical complexity required to achieve compliance 3036. Furthermore, the American Bankers Association (ABA) and allied banking sector groups have aggressively lobbied regulators, officially requesting that the Treasury Department and the FDIC extend their public comment deadlines to align with the OCC's final rule. The banking industry argues that fragmented comment periods across interdependent proposals will undermine regulatory consistency, potentially giving non-bank stablecoin issuers an unfair operational advantage 15.

For the CLARITY Act, the delay in securing a full Senate floor vote is primarily tethered to the highly contentious "stablecoin yield" debate. Initial drafts of stablecoin legislation banned issuers from paying interest directly to stablecoin holders to prevent the assets from competing directly with insured bank deposits 1516. The CLARITY Act attempts to address loopholes in that ban, specifically regarding whether third-party platforms, brokers, and exchanges can offer rewards or yield to users holding passive stablecoin balances. Following intense pushback from the banking lobby - which fears that yield-bearing stablecoins will inevitably function as unregulated, uninsured shadow deposits and drain liquidity from community banks - the Senate Banking Committee incorporated the "Tillis-Alsobrooks compromise text" in May 2026 2240.

This compromise language explicitly prohibits rewards on passive stablecoin holdings that are "economically or functionally equivalent" to bank deposit interest, while carving out exceedingly narrow allowances for rewards tied specifically to active network participation, staking, or promotional activities 1522. This compromise has fractured the crypto industry's support; major entities like Coinbase have publicly voiced concerns that overly broad yield restrictions stifle the fundamental utility of digital dollars and threaten the competitiveness of U.S. stablecoins in the global market against frameworks like Europe's Markets in Crypto-Assets (MiCA) regulation 1141.

Furthermore, Senate Democrats have raised profound objections regarding the efficacy of the Act's illicit finance provisions, arguing that the legislation fails to close glaring loopholes surrounding crypto mixers and decentralized finance (DeFi) protocols 46. Lastly, unresolved ethics provisions, which seek to bar senior government officials and members of Congress from profiting on digital assets they regulate while in office, remain a major sticking point that could cost the bill the crucial Democratic votes required to overcome a filibuster 415.

FAQ 4: What is the legislative window, and what competing political priorities are clogging the 2026 calendar?

The primary threat to the enactment of the CLARITY Act and the advancement of other digital asset initiatives is not substantive policy opposition, but rather the severe temporal constraints imposed by the 2026 congressional calendar. The sheer lack of floor time threatens to derail the industry's progress 2142.

During the second session of the 119th Congress, a midterm election year introduces massive structural impediments to legislative productivity. Members of Congress are required to spend significantly more time in their home states and districts actively campaigning ahead of the November elections, resulting in drastically fewer days in session in Washington, D.C. 4243. The Senate's tentative schedule reflects this stark reality, outlining a non-legislative state work period from June 29 to July 10, followed by an extensive summer recess from August 10 through September 11, and a final pre-election recess beginning October 5 17.

This truncated timeline leaves a minuscule window for floor debate on a bill that requires 60 votes to overcome a filibuster 415. To reach that required 60-vote threshold, the Republican-led Senate (holding 53 seats) requires at least seven Democratic or independent votes, assuming absolute party unity 4. During the Senate Banking Committee markup, the bill only secured two Democratic votes (Senators Ruben Gallego and Angela Alsobrooks), indicating that floor math remains highly precarious 46. This mathematical reality forces the CLARITY Act to compete directly against deeply entrenched, must-pass political priorities that are currently clogging the legislative pipeline 21.

Chief among these competing macro-priorities is the BUILD America 250 Act (H.R. 8870), a comprehensive five-year surface transportation reauthorization bill that advanced out of the House Transportation and Infrastructure Committee following a grueling 14-hour markup session on May 22, 2026 4518. The BUILD America 250 Act authorizes a massive $580 billion in infrastructure spending and introduces highly contested provisions, such as new federal registration fees for electric vehicles ($130 initially) designed to offset declining gas tax revenues 4547. Because current highway and transit program authorities derived from the 2021 Infrastructure Investment and Jobs Act are scheduled to expire on September 30, 2026, the transportation bill will inevitably consume substantial floor time and political capital throughout the summer 4345.

In addition to infrastructure reauthorization, the calendar is heavily burdened by the annual appropriations process. Congress must finalize fiscal year 2027 funding by the end of September to avoid a government shutdown, while simultaneously navigating intense partisan negotiations over "reconciliation 2.0," a Republican-led effort to secure multi-year funding for Immigration and Customs Enforcement (ICE) and Customs and Border Protection (CBP) 4218. Lawmakers must also address the biennial reauthorization of the Water Resources Development Act (WRDA) and upcoming Farm Bill extensions 43. With the White House actively pushing for the CLARITY Act to pass by July 4, the sheer volume of macro-economic, defense, and infrastructure-related legislation threatens to push digital asset market structure reform past the point of political viability before the midterm elections 46.

FAQ 5: What are the practical takeaways detailing how passage or failure affects consumers, tech companies, and the banking industry?

The practical implications of the GENIUS Act's ongoing implementation, combined with the potential passage or failure of the CLARITY, PARITY, and Anti-CBDC Acts, will fundamentally alter the long-term operational strategies of consumers, multinational technology conglomerates, and legacy financial institutions.

Impact on Consumers and Everyday Transactions For the everyday consumer, the primary benefit of the emerging regulatory framework is the seamless integration of digital dollars into routine commerce without the friction of taxation or extreme volatility. Currently, utilizing a standard cryptocurrency to purchase a consumer good triggers a taxable event under IRS rules, requiring the user to painstakingly calculate and report capital gains or losses on minor transactions 4849. The bipartisan Digital Asset PARITY Act, introduced in May 2026 by Representatives Max Miller (R-Ohio) and Steven Horsford (D-Nevada), aims to eliminate this massive barrier by creating a deemed-basis rule specifically for regulated, dollar-pegged payment stablecoins 4919.

Under this draft legislation, if a consumer utilizes a stablecoin for a transaction and the asset's value variance is less than 1% from its peg against the dollar, the transaction is exempt from tax reporting requirements, effectively treating the digital asset exactly like physical cash 20. This tax clarity, combined with the robust consumer protection mandates of the GENIUS Act - which ensure that stablecoins are fully backed by safe assets and legally insulated from issuer bankruptcy proceedings - will likely catalyze widespread mainstream adoption of digital wallets for retail payments and cross-border remittances 1416. A failure to pass the PARITY Act would mean that while the regulatory rails for stablecoins exist, the tax uncertainty would continue to stifle everyday adoption 49. Furthermore, the passage of the Anti-CBDC Surveillance State Act ensures that consumers retain privacy in their digital transactions, blocking the Federal Reserve from establishing a centralized retail ledger capable of monitoring individual financial behavior 1213.

Impact on Technology Companies and the Retail Sector For multinational technology companies and retail behemoths, the GENIUS Act provides the critical legal certainty required to architect proprietary payment networks that entirely circumvent legacy financial infrastructure 79. The Wall Street Journal recently reported that corporations like Amazon and Walmart, which process hundreds of billions of dollars in transaction volume annually, are actively exploring the launch of their own digital currencies or forging deep partnerships with existing stablecoin providers 89.

By launching branded stablecoins or utilizing established networks like Circle's USDC, these retailers can settle payments instantly on blockchain ledgers, effectively reducing processing costs to fractions of a cent and bypassing the $32 billion in total interchange fees collected on prepaid and debit transactions 89. The GENIUS Act's strict requirement that stablecoin reserves be held in high-quality liquid assets, such as short-term U.S. Treasuries, presents a massive secondary revenue vector. In a positive interest rate environment, tech companies issuing their own stablecoins can capture the 4% to 5% yield generated by billions of dollars in Treasury reserves, fundamentally transforming their internal payment infrastructure from a necessary cost center into a highly lucrative profit-generating enterprise 1014.

Impact on the Traditional Banking Industry The traditional banking sector views the rapid proliferation of non-bank stablecoins as an existential threat to deposit stability and systemic liquidity 1652. The American Bankers Association (ABA) has aggressively lobbied regulators and lawmakers, warning in a 2026 letter to the Senate that an estimated $6.6 trillion in bank deposits are at risk of fleeing the traditional system 1321. The industry fears that the emergence of stablecoins - especially if they find loopholes to offer yield - will trigger massive deposit flight, transferring trillions of dollars out of community banks and into the shadow banking sector, thereby constraining local lending 1322. Consequently, banking industry groups have demanded that federal regulators harmonize their public comment periods for GENIUS Act implementation to ensure that nonbank stablecoin issuers do not receive preferential treatment 15.

To adapt and survive this structural shift, banks are increasingly leveraging the Automated Clearing House (ACH) network as the primary fiat on-ramp and off-ramp for digital wallets, ensuring that they maintain a toll-taking foothold in the transaction lifecycle even as payments move on-chain 23. Furthermore, major institutions are fighting back with proprietary innovations; for instance, JPMorgan is actively developing its own blockchain-based deposit token (JPMD) to offer institutional clients the 24/7 settlement capabilities of stablecoins while explicitly retaining those funds within the traditional, FDIC-insured banking perimeter 4956. Finally, groups like the Defense Credit Union Council (DCUC) are closely monitoring how digital asset legislation moves through Congress, specifically watching to ensure that harmful amendments like the Credit Card Competition Act (CCCA) - which would further limit network interchange fees - are not stealthily attached to must-pass defense authorization bills (NDAA) alongside crypto provisions 57.

Bottom Line

The U.S. digital asset landscape in 2026 is defined by an intense race against the political clock. The passage of the GENIUS Act definitively answered the question of stablecoin legitimacy, providing technology giants and financial institutions the regulatory certainty required to embed tokenized dollars into global payment rails and potentially upend the legacy credit card network. However, the broader digital asset economy remains in a state of suspended animation. The CLARITY Act represents the most comprehensive attempt to date to modernize financial market structure and legally define digital commodities, yet its passage remains highly uncertain. As lawmakers navigate severe election-year gridlock, fierce lobbying from a threatened legacy banking sector, and profound debates over illicit finance compliance, the ultimate outcome of the Senate vote will determine whether the United States establishes a cohesive, future-proof digital asset framework, or cedes regulatory leadership to competing international jurisdictions.