How the GENIUS Act Affects Stablecoin Yields in 2026

The Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act and its sweeping 2026 federal rulemakings fundamentally transform payment stablecoins from lightly regulated cryptographic assets into strictly supervised, fully reserved financial instruments overseen by federal banking agencies. Under this new regulatory regime, stablecoin issuers are legally mandated to maintain 1-to-1 backing in high-quality liquid assets, and they are explicitly prohibited by statute from paying any form of interest or yield directly to token holders. Furthermore, proposed regulations aim to aggressively sever the indirect pipelines through which third-party exchanges currently pass yield to retail consumers, creating a stringent framework that seeks to integrate digital dollars into the traditional payment rail system while neutralizing their potential to act as competitive, yield-bearing investment vehicles.

If you rely on digital dollars to hedge against inflation, remit funds across international borders, or generate passive income on your holdings, your financial reality is about to fundamentally change.

How do yield-bearing stablecoins compare to standard savings accounts and money market funds?

To fully grasp the magnitude of the regulatory battle unfolding in 2026, it is necessary to demystify the core financial mechanics that separate stablecoins from legacy banking products. The most common real-world analogy for a yield-bearing stablecoin is a traditional money market fund. When a retail investor allocates cash into a money market fund, the fund manager pools that capital to purchase low-risk, short-duration government debt, such as United States Treasury bills. As those Treasury bills generate interest, the fund passes the yield back to the investor, minus a management fee. A yield-bearing stablecoin operation functions on an almost identical financial premise: the issuer accepts user fiat, mints digital tokens on a 1-to-1 basis, invests the fiat reserves into Treasury-backed instruments or reverse repurchase agreements, and historically distributes the resulting yield to the token holders. The paramount difference lies in the technological wrapper, as stablecoins settle instantaneously on a decentralized blockchain ledger, operating twenty-four hours a day without reliance on the clearinghouses that govern traditional mutual funds 12.

Conversely, traditional bank savings accounts operate on a completely different premise known as fractional reserve banking. When a consumer deposits money into a standard checking or savings account, the bank does not lock that specific dollar in a vault, nor does it hold a 1-to-1 reserve. Instead, the bank leverages those deposits to extend credit, lending the capital out as mortgages, automotive loans, and corporate credit lines. The bank then pays the depositor a fraction of the interest it earns from those long-term lending activities 12. Because stablecoin reserves under the new federal rules must be held on a strict 1-to-1 basis and cannot be fractionally lent out to consumers or businesses, traditional banking institutions argue that any large-scale migration of consumer funds from bank savings accounts to yield-bearing stablecoins directly drains the core deposit funding that banks require to generate credit and fuel the broader economy 133.

This structural divergence leads directly to one of the most pervasive and dangerous misconceptions in the digital asset market: the assumption that heavily regulated, dollar-pegged stablecoins carry government backing. Despite their strict 1-to-1 dollar peg, their new designation as "payment stablecoins," and the severe bank-like oversight imposed by the GENIUS Act, digital stablecoins are completely uninsured by the Federal Deposit Insurance Corporation (FDIC) 245. If a traditional commercial bank becomes insolvent, the FDIC steps in to protect standard retail deposits up to $250,000. If a stablecoin issuer fails, suffers a catastrophic smart contract vulnerability, or falls victim to a cyberattack, the federal government will not deploy a taxpayer-funded backstop to make token holders whole 57. The new legislation addresses this risk not through insurance, but through strict reserve composition rules and bankruptcy remoteness, ensuring that the underlying assets are segregated and protected rather than guaranteed by the state.

What is the GENIUS Act and how does it overhaul U.S. stablecoin regulation?

Signed into law by President Donald Trump on July 18, 2025, the GENIUS Act represents the first comprehensive federal legislative framework for digital assets in United States history, effectively ending a decade-long era defined by regulatory ambiguity, agency turf wars, and a fragmented patchwork of state-level money transmitter licenses 67811. The statute fundamentally alters the classification of stablecoins. By explicitly amending federal securities laws and the Commodity Exchange Act, the legislation dictates that a compliant "payment stablecoin" is neither a security nor a commodity, officially carving these assets out from the aggressive enforcement jurisdictions of the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) 79.

Instead, the GENIUS Act establishes a tailored, prudential regulatory perimeter overseen entirely by federal and state banking regulators 71011. The legislation restricts the issuance of payment stablecoins within the United States strictly to entities classified as a "permitted payment stablecoin issuer" (PPSI) 6. To operate legally, an entity must secure authorization through one of three highly regulated pathways. The first pathway allows subsidiaries of insured depository institutions, such as traditional banks and credit unions, to issue stablecoins under the oversight of their primary federal regulator, typically the FDIC or the Federal Reserve 681512. The second pathway establishes the "Federal qualified payment stablecoin issuer" (FQPSI), allowing nonbank entities, uninsured national trust banks, and federal branches of foreign banks to obtain a specialized charter and operate under the direct supervision of the Office of the Comptroller of the Currency (OCC) 61314. The third pathway preserves a role for state regulators, allowing nonbank entities to operate as "State qualified payment stablecoin issuers" (SQPSI) under certified state-level frameworks, provided their total outstanding stablecoin issuance remains below a strict $10 billion threshold 6151219.

The architectural foundation of the GENIUS Act is its stringent reserve requirements, designed to eliminate the systemic risks that led to historical algorithmic stablecoin collapses. Every permitted payment stablecoin must be backed by segregated, high-quality liquid assets on at least a 1-to-1 basis, meaning the total fair value of the reserves must continually equal or exceed the outstanding token issuance 61315. Under the statute and the subsequent implementing rules proposed by the OCC in early 2026, the definition of permissible reserve assets is deliberately narrow. Issuers are legally restricted to holding reserves in U.S. currency, demand deposits at federally insured institutions, balances held in Federal Reserve master accounts, U.S. Treasury securities with a remaining maturity of 93 days or less, and overnight repurchase agreements fully collateralized by short-term Treasuries 1151319.

Crucially, these reserves are subject to strict anti-rehypothecation mandates. Issuers are prohibited from pledging, lending, or commingling these assets to fund alternative investments or chase higher yields, ensuring the reserves remain highly liquid and exclusively available to satisfy customer redemptions at par 152116. The legislation pairs these financial constraints with sweeping consumer protections, notably amending the U.S. Bankruptcy Code to grant stablecoin holders priority claims over all other creditors in the event of an issuer's insolvency, effectively ring-fencing the reserve assets from the issuer's general corporate estate 576.

Can I still earn yield on my stablecoins, or is it banned?

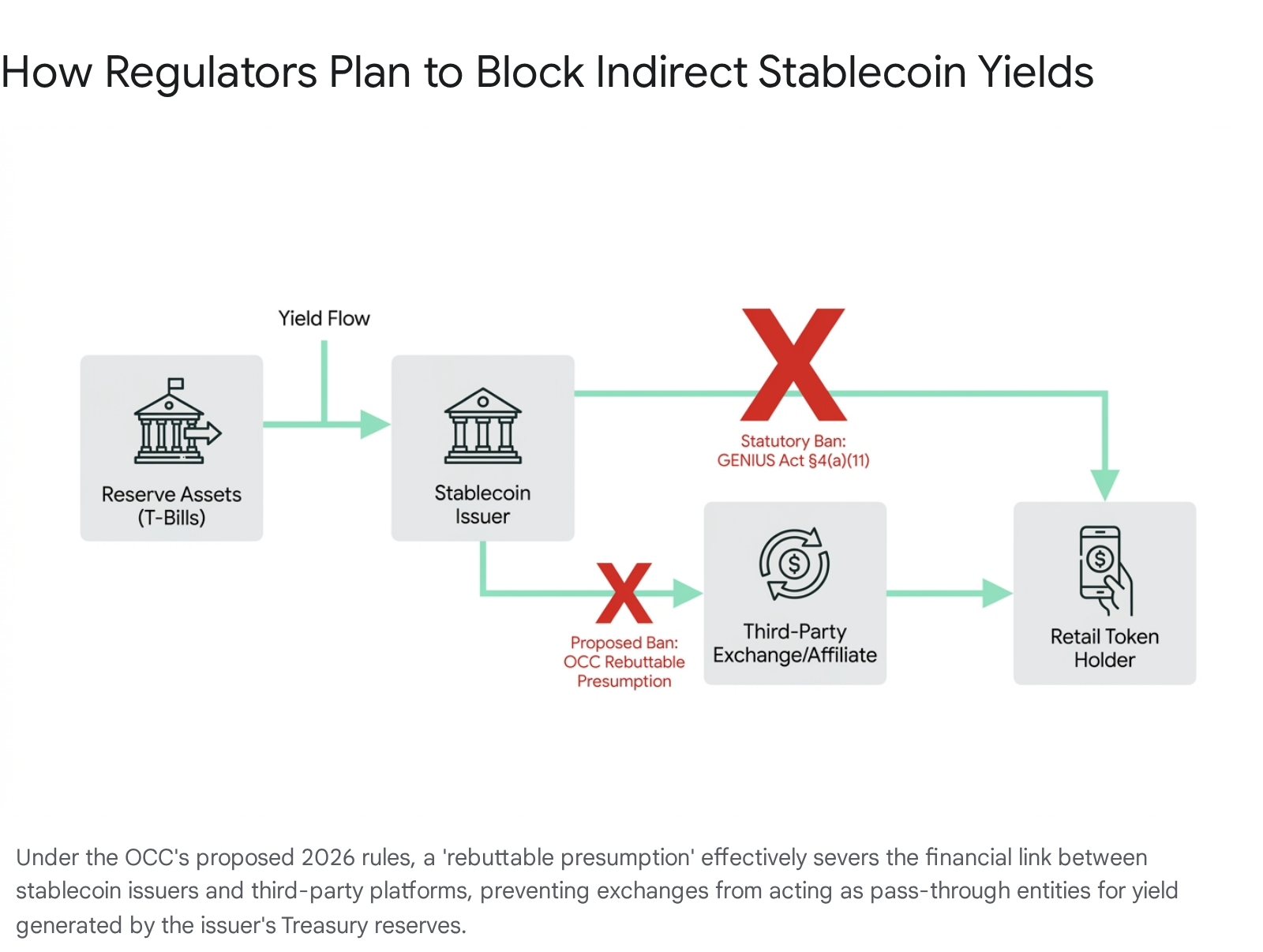

The most consequential, disruptive, and fiercely contested provision within the entire GENIUS Act framework is Section 4(a)(11), which dictates the absolute prohibition of direct yield. The statute explicitly states that no permitted payment stablecoin issuer shall pay a token holder any form of interest or yield - whether distributed in cash, additional tokens, or other consideration - solely in connection with the holding, use, or retention of the asset 13172418. This prohibition was strategically designed to cement the legal classification of stablecoins as non-security payment instruments. By eliminating the expectation of profit derived from holding the asset, regulators successfully engineered a legislative bypass of the SEC's Howey Test, legally transforming stablecoins from speculative investment contracts into sterile mediums of exchange 7102119. Consequently, primary token issuers like Circle (USDC) and Tether (USDT) are legally barred from distributing the billions of dollars in interest they harvest from their massive Treasury reserves directly to their retail user base 32427.

However, while the statutory language of the GENIUS Act explicitly handcuffed the primary token issuers, it left open a critical structural ambiguity regarding the broader cryptocurrency ecosystem. The statute did not explicitly prohibit third-party cryptocurrency exchanges, decentralized finance (DeFi) distribution platforms, or affiliated lending intermediaries from offering proprietary rewards, staking yields, or interest-bearing products to users who custody their stablecoins on those secondary platforms 1728. This perceived "yield loophole" quickly escalated into a massive lobbying war between the traditional banking sector and the digital asset industry in early 2026, completely dominating the regulatory discourse.

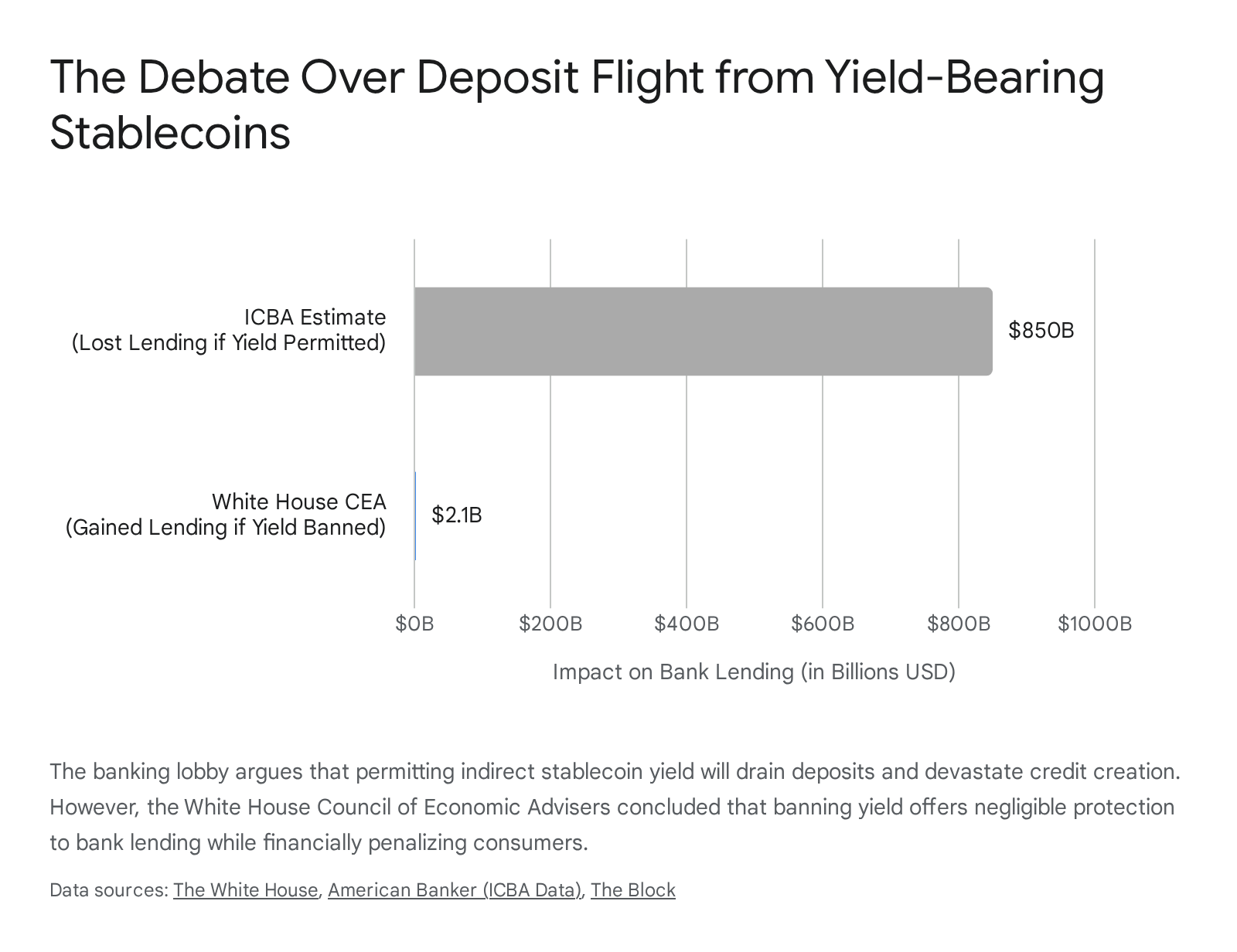

The traditional banking lobby, orchestrated primarily by the American Bankers Association (ABA) and the Independent Community Bankers of America (ICBA), argued vehemently that allowing third-party platforms to pay yield on stablecoin holdings would create a structurally superior alternative to zero-yield commercial bank checking accounts. Bank of America CEO Brian Moynihan publicly warned that if regulators permit yield payments on stablecoins, up to $6 trillion in traditional deposits - roughly one-third of all commercial bank deposits in the United States - could eventually migrate to digital tokens 20. The ICBA released detailed economic modeling in early 2026 projecting that if indirect stablecoin yields were permitted, the global stablecoin market could rapidly expand from its baseline of $300 billion to over $2 trillion 328. According to the banking lobby, this massive deposit flight would severely restrict credit creation, reducing aggregate community bank lending capacity by up to $850 billion and devastating local agricultural and small business credit lines 3328.

In direct response to these macroeconomic stability concerns, the OCC utilized its February 2026 Notice of Proposed Rulemaking to take an exceptionally aggressive regulatory posture. The OCC proposed a sweeping "rebuttable presumption" that treats any financial arrangement where a stablecoin issuer coordinates with an affiliate or a "related third party" to pass yield to token holders as an intentional violation of the statutory interest ban 1318.

Under the proposed OCC regulations, a related third party is broadly defined to include any person paying interest to holders as a service on behalf of the issuer, as well as entities engaged in white-label branding arrangements where the issuer mints stablecoins under the partner's brand 131821. Unless the stablecoin issuer can present written materials definitively proving to the OCC's satisfaction that the third-party arrangement is not an evasion of the law, the yield payouts are categorically prohibited 151822.

Crypto industry advocates, led by massive digital asset exchanges like Coinbase, strongly opposed this expansive interpretation. They argued that the OCC's rebuttable presumption severely oversteps the explicit statutory text of the GENIUS Act, which was specifically negotiated in Congress to limit only the primary issuer from paying yield, intentionally preserving the ability of intermediaries to offer activity-based rewards to incentivize network participation 331922. This fierce industry pushback found highly unexpected and empirical support from the White House Council of Economic Advisers (CEA). In April 2026, the CEA published an extensive economic report titled "Effects of Stablecoin Yield Prohibition on Bank Lending," which systematically dismantled the banking lobby's catastrophic deposit flight narrative.

The White House macroeconomic analysis concluded that completely eliminating stablecoin yield to protect banks would result in negligible gains for the credit system. According to the CEA's baseline calibration, enforcing a total yield prohibition would only increase aggregate bank lending by a trivial $2.1 billion - representing a microscopic 0.02% increase in total lending - while simultaneously imposing a net welfare cost of $800 million on everyday consumers by depriving them of competitive returns on their digital asset holdings 13.

The CEA report noted that large banks would absorb 76% of this minor lending increase, leaving community banks with an almost imperceptible $500 million bump, or a 0.026% increase in their localized lending portfolios 1. Furthermore, the White House economists pointed out that to reach the apocalyptic figures cited by the banking lobby, one would have to assume the implausible scenario that the stablecoin market grows to six times its current size, that all reserves are locked in unlendable physical cash rather than Treasury securities, and that the Federal Reserve completely abandons its established monetary framework 1. The report bluntly concluded that a yield prohibition does very little to protect bank lending, while heavily penalizing the consumer 13.

This ideological friction inevitably spilled back into Congress, severely complicating parallel legislative efforts. Lawmakers attempted to address the stablecoin yield controversy within the broader Digital Asset Market Clarity Act (CLARITY Act), an accompanying piece of market structure legislation working its way through the Senate 319. Driven by the ABA's emergency lobbying campaign, early drafts of the CLARITY Act included specific provisions that legally restricted cryptocurrency intermediaries from paying rewards that were economically or functionally equivalent to the payment of interest on bank deposits, effectively attempting to codify the OCC's aggressive regulatory stance into federal law 319. This inclusion prompted immediate retaliation from the crypto sector. Coinbase CEO Brian Armstrong publicly announced that his exchange could not support the legislation under those conditions, and the resulting political deadlock indefinitely stalled the CLARITY Act's markup in the Senate Banking Committee 1932. As of mid-2026, the question of whether indirect yield payouts will survive the final regulatory sweep remains the market's most significant and legally contested unresolved variable.

How do the OCC and FDIC banking rules reshape stablecoin operations?

Beyond the contentious battle over yield, the federal banking agencies are utilizing their 2026 rulemaking sprint to impose a highly sophisticated, bank-like prudential architecture upon stablecoin operations. The speed of this regulatory overhaul is unprecedented; driven by the statutory deadlines embedded in the GENIUS Act, five major federal rulemakings were introduced in a span of just ten weeks during the spring of 2026 2324.

The Office of the Comptroller of the Currency issued its massive 376-page Notice of Proposed Rulemaking in late February 2026, setting the baseline for the entire federal stablecoin framework 1523. The OCC proposal meticulously details the diversification and liquidity standards required to maintain a stablecoin's dollar peg during periods of severe market stress. The agency requires issuers to adhere to strict quantitative maturity standards that are conceptually identical to those applied to regulated money market funds 13. Specifically, stablecoin issuers must maintain at least 10% of their total reserves in highly liquid daily assets, such as demand deposits or Federal Reserve balances, and at least 30% of their reserves in assets that mature within five business days 13. To prevent systemic vulnerability due to institutional collapse, the OCC mandates concentration limits, capping exposure so that no more than 50% of an issuer's daily liquidity reserves and no more than 40% of its total portfolio can be held at any single eligible financial institution 1315. The total reserve portfolio must also maintain a weighted average maturity of no more than 20 days 13.

The Federal Deposit Insurance Corporation (FDIC) followed shortly after, issuing its own Notice of Proposed Rulemaking in April 2026. The FDIC explicitly aligned its rule with the OCC's framework to prevent regulatory arbitrage, targeting the application procedures and capital adequacy standards for state nonmember banks and state savings associations that intend to issue stablecoins through subsidiaries 122526. The FDIC proposal also tackles the critical, highly technical issue of pass-through deposit insurance for stablecoin reserves held at traditional banks, while clarifying the regulatory treatment of tokenized deposits - blockchain-based representations of commercial bank money that function similarly to stablecoins but remain fully integrated into the fractional reserve banking system 1225.

Crucially, the regulatory transformation extends deeply into the realm of national security and illicit finance. In coordination with the banking agencies, the Treasury Department, FinCEN, and OFAC issued joint proposed rules that formally classify permitted payment stablecoin issuers as "financial institutions" for the purposes of the Bank Secrecy Act 72627. This integration requires stablecoin operators to abandon the permissionless ethos of early cryptocurrency in favor of establishing robust, traditional AML and CFT compliance programs. Issuers must conduct comprehensive risk assessments, implement strict Know Your Customer (KYC) identity verification protocols, actively screen against international sanctions lists, and maintain the technical capability to unilaterally freeze, seize, or burn payment stablecoins when served with lawful orders from federal authorities 51938. Violations of these BSA obligations carry severe criminal exposure, with penalties including millions of dollars in fines and substantial prison sentences for corporate officers who facilitate sanctions evasion 5710.

The rulemakings also meticulously define the transition process for large stablecoin issuers currently operating under state-level licenses. Recognizing that massive token issuance poses systemic national risks, the OCC rules stipulate that if a state-qualified nonbank issuer exceeds $10 billion in circulating payment stablecoins, it must notify the OCC within five business days 151821. The issuer is then granted a strict 360-day window to complete a comprehensive capital analysis and transition its operations under direct federal OCC oversight, or alternatively secure a rare waiver 1821. Failure to transition forces the issuer to immediately cease all net new stablecoin issuance until its circulation falls back below the $10 billion threshold 1321.

What is the timeline, and what happens if regulators miss the July 2026 deadline?

The GENIUS Act established an extraordinarily aggressive implementation schedule that has placed immense operational pressure on both government regulators and private industry participants. The statute explicitly requires the primary federal payment stablecoin regulators - including the OCC, FDIC, Federal Reserve, and NCUA - as well as the Treasury Department and certified state agencies, to issue their final implementing regulations no later than one year after the legislation's enactment, establishing a hard statutory deadline of July 18, 2026 15132328.

However, the rapid succession of massive proposed rules in the spring of 2026 has resulted in thousands of pages of complex commentary from traditional banks, crypto exchanges, and public policy groups, particularly regarding the fiercely contested rebuttable presumption on indirect yields 32429. This heavy volume of industry feedback has raised the distinct possibility of interagency gridlock, prompting legal experts to analyze the looming enforcement uncertainty regarding the statute's effective dates 41.

The text of the GENIUS Act dictates that the law officially takes effect on the earlier of two specified dates: 18 months from the date of enactment, which falls on January 18, 2027, or 120 days after the primary federal payment stablecoin regulators issue their final rules 6132830. The July 18, 2026 deadline for the agencies to finalize those rules is a strict statutory mandate, not a mere advisory target 41. If the federal banking agencies fail to finalize the capital, liquidity, and supervisory frameworks by mid-year due to political disagreements over the yield prohibition, the foundational requirements of the GENIUS Act will still activate by default on January 18, 2027 1241.

This scenario would plunge the digital asset industry into a perilous regulatory vacuum. Without finalized technical guidelines regarding reserve calculations, state-level equivalency certifications, and custody standards, neither the prospective stablecoin issuers nor the regulatory examiners would possess the necessary implementation guidance 4143. Compliant stablecoin issuance by institutional players - including the major Wall Street banks preparing to enter the market - would be effectively frozen, as multibillion-dollar financial entities cannot construct enduring compliance infrastructure against unfinished, hypothetical rules 4143. Existing digital asset service providers and crypto exchanges are granted a slightly longer statutory grace period to adjust their operations; they face a final, immutable deadline of July 18, 2028, which marks exactly three years from enactment. After that date, it becomes a federal crime for any exchange to offer, list, or sell a payment stablecoin in the United States that is not issued by a fully compliant, permitted issuer 1015.

How does the U.S. approach compare to the EU's MiCA and other global frameworks?

While the United States engages in bitter domestic debates over the technicalities of the GENIUS Act, other major global jurisdictions have already activated comprehensive stablecoin regimes. An analysis of these disparate international frameworks reveals profound philosophical differences regarding monetary sovereignty, the protection of legacy banking institutions, and the management of systemic financial risk.

The European Union's Markets in Crypto-Assets (MiCA) regulation, which came into full legal effect for stablecoins in 2024, is structurally far more rigid and protectionist than the American approach. MiCA creates a unified, top-down framework across all 27 EU member states, categorizing stablecoins primarily into "e-money tokens" (EMTs), which reference a single official currency, and "asset-referenced tokens" (ARTs), which may reference baskets of currencies or commodities 314532.

The most striking divergence between the European and American models is their handling of the yield controversy. Unlike the U.S. GENIUS Act - which relies on a complex, litigious "rebuttable presumption" by the OCC to curb indirect yield payouts through affiliates - MiCA imposes a categorical, airtight prohibition. Article 22(4) of the MiCA framework explicitly forbids all issuers and licensed Crypto-Asset Service Providers (CASPs) from granting interest, or any other benefit related to the length of time a token is held, to stablecoin users 1733. This deliberate policy choice completely prevents stablecoins from functioning as savings instruments, cleanly insulating the European banking sector from digital deposit flight without the need for case-by-case agency enforcement 33.

Furthermore, the rules dictating reserve composition highlight a massive geopolitical divergence. The GENIUS Act takes a narrow view of eligible reserves, allowing U.S. issuers the operational flexibility to hold up to 100% of their backing in short-term U.S. Treasury bills 194849. This strategically ensures that the $300 billion global stablecoin market continues to act as a massive, reliable buyer of United States government debt, reinforcing the U.S. dollar's status as the global reserve currency 53451. In stark contrast, MiCA prioritizes the health of local credit markets over sovereign debt funding. To prevent runs and ensure instant liquidity, the EU mandates that a significant portion of stablecoin reserves - specifically a 30% absolute floor for standard tokens, escalating to 60% for systemically significant tokens - must be held as unencumbered cash deposits within European credit institutions 31483553. The EU framework also implements strict daily transaction volume caps on non-euro denominated stablecoins - such as the dominant dollar-pegged USDT and USDC - if they exceed 1 million transactions and EUR 200 million per day, a blatant safeguard aimed entirely at protecting European monetary sovereignty from dollarization 1148. The U.S. GENIUS Act contains no analogous foreign-currency caps 48.

In Asia, emerging regulatory frameworks similarly prioritize intense capitalization requirements and localized oversight to maintain financial stability. Hong Kong's Stablecoins Ordinance, which takes effect on August 1, 2025, requires all fiat-referenced stablecoin issuers to be locally incorporated entities. Issuers must maintain a minimum paid-up share capital of HK$25 million (approximately $3.2 million USD), and they are legally mandated to hold 100% of their reserve backing in highly liquid assets stored within segregated trust accounts operated by local Hong Kong custodians 34365537. Singapore's Monetary Authority (MAS) finalized its highly anticipated framework in late 2023. Singapore allows only single-currency stablecoins that are explicitly pegged to either the Singapore Dollar or recognized G10 currencies to achieve the official "MAS-Regulated" label 3858. To qualify for this label, issuers must meet strict monthly auditing standards, guarantee token redemption at par value within a tight five-business-day window, maintain a base capital of at least S$1 million, and are strictly prohibited from engaging in any other business activities such as lending or staking 3858. Meanwhile, the United Kingdom's Financial Conduct Authority (FCA) is pursuing a phased approach. Rather than creating entirely new asset categories, the UK is integrating stablecoins into existing electronic money and payment services regulations, heavily emphasizing operational resilience, mandatory par redemption, and strict safeguarding of customer funds, with new issuance authorization rules opening in early 2025 11485939.

Direct Comparison: Stablecoin Frameworks

| Regulatory Feature | Pre-2026 Status Quo (U.S.) | Post-GENIUS Act Rules (U.S.) | EU MiCA Framework |

|---|---|---|---|

| Primary Regulatory Authority | Fragmented state money transmitter licenses (e.g., NYDFS BitLicense); unclear federal oversight. | Federal banking regulators (OCC, FDIC, Fed) with a limited state opt-in for issuers under $10 billion. | National Competent Authorities passported automatically across all 27 EU Member States. |

| Reserve Composition | Varies significantly by state; historically opaque, leading to severe de-pegging risks. | Strictly 1-to-1 backing in U.S. cash, short-term Treasuries (<93 days), or Fed deposits. | Strictly 1-to-1; mandates 30% to 60% of reserves must be held as cash in EU credit institutions. |

| Yield Legality (Issuers) | Unregulated; though major issuers actively avoided it to bypass SEC securities classification. | Strictly prohibited by statute. Permitted issuers cannot pay yield directly. | Categorically banned for all asset-referenced and e-money token issuers. |

| Yield Legality (Exchanges/DeFi) | Generally permitted; widely utilized by exchanges as marketing incentives. | Highly uncertain. OCC's "rebuttable presumption" proposes to block affiliated/third-party yield. | Strictly prohibited for any licensed Crypto-Asset Service Provider (CASP). |

| Consumer Insolvency Protection | Weak; token holders generally treated as unsecured general creditors in bankruptcy. | Strong; GENIUS Act amends bankruptcy code to give token holders priority claims over reserve assets. | Strong; mandates strict segregation of reserve assets entirely remote from issuer bankruptcy. |

| Foreign Issuer Access | Unrestricted; offshore entities freely serviced U.S. retail and institutional customers. | Restricted; requires Treasury equivalency determination and OCC registration to operate onshore. | Restricted; non-EU issuers must establish a locally authorized and regulated entity within the EU. |

What are the practical takeaways for everyday retail crypto investors?

For retail investors, decentralized finance participants, and everyday digital asset traders, the transition from an unregulated, frontier ecosystem to the rigorously supervised GENIUS Act era requires immediate strategic recalibration. The era of assuming all dollar-pegged stablecoins are functionally identical, bearer-asset equivalents is ending.

First and foremost, retail investors must prepare for the likely restructuring, degradation, or outright suspension of popular exchange-based "Earn" programs. While decentralized finance lending protocols governed purely by permissionless smart contracts - such as Aave or Compound - currently remain largely outside the direct jurisdictional reach of the OCC's issuer-focused regulations, centralized entities face massive, immediate regulatory pressure 2761. Given the calibrated uncertainty regarding exactly how strictly the OCC will enforce its "related third party" presumption by the impending July 2026 deadline, investors should anticipate that U.S.-regulated centralized exchanges will act defensively. To avoid crippling compliance violations and potential enforcement actions, exchanges may proactively halt yield payouts on simple stablecoin balances 32722. Investors relying heavily on centralized stablecoin custody for passive income generation will likely need to shift capital entirely into complex on-chain DeFi mechanisms or simply accept holding zero-yield digital payment tokens.

Second, the market is poised for a violent bifurcation between "compliant" onshore stablecoins and "non-compliant" offshore assets. The operational gap between the two major market leaders - Circle's USDC and Tether's USDT - is widening rapidly. While USDC is rapidly aligning its corporate infrastructure, auditing practices, and reserve composition to meet the incoming OCC and FDIC mandates, the legal status of USDT remains highly precarious within the formalized U.S. market 4362. Under the GENIUS Act provisions, a foreign-issued stablecoin can only be offered by U.S. digital asset service providers if the Treasury Department grants a formal equivalency determination, proving that the foreign jurisdiction's rules are comparable to the U.S. framework 144340. If Tether fails to secure this rare Treasury recognition, U.S. exchanges will be legally compelled to delist USDT entirely by the July 2028 statutory deadline 1015. Retail traders must actively monitor this compliance gap and should consider gradually rotating their portfolios toward GENIUS-compliant stablecoins to avoid being trapped in severe liquidity crunches resulting from sudden, forced exchange delistings.

Finally, while the new regulations may stifle passive yield generation, everyday users will benefit immensely from unprecedented, bank-grade consumer protections. The GENIUS Act definitively strips away the opaque, proprietary reserve practices that defined the crypto industry over the past decade. With the implementation of mandatory monthly audits conducted by registered public accounting firms, strict prohibitions against risky asset rehypothecation, and new federal bankruptcy code amendments ensuring that token holders possess priority claims over the underlying reserve assets, the existential risks of the asset class have been mitigated 576. For the everyday user, the threat of a catastrophic, Terra-style algorithmic collapse or a run-on-the-bank liquidity crisis for compliant tokens is fundamentally neutralized, transforming stablecoins into a genuinely reliable digital medium of exchange.

Bottom Line

- Federal Legitimacy and Reserve Integrity: The GENIUS Act successfully elevates payment stablecoins from speculative, unregulated crypto assets to federally supervised financial instruments. By mandating strict 1-to-1 backing in high-quality liquid assets like short-term U.S. Treasuries and cash, and placing issuers under rigorous BSA/AML oversight, the law ensures digital dollars are safe, auditable, and bankruptcy-remote.

- The Contentious Yield Ban: While the statute clearly forbids stablecoin issuers from paying yield directly to users, the OCC is aggressively utilizing proposed rulemakings to close the loopholes that allow third-party exchanges to pay out rewards. This regulatory overreach is heavily lobbied for by traditional banks terrified of a $2 trillion deposit flight, despite White House economic reports concluding that such bans harm consumers while offering negligible protection to bank lending.

- Global Regulatory Divergence: The U.S. regulatory approach focuses on integrating stablecoins into the banking perimeter while strategically ensuring that the $300 billion market continues to purchase U.S. Treasury debt, thereby reinforcing dollar dominance. In stark contrast, the EU's MiCA framework adopts a highly protectionist stance, mandating heavy local bank-deposit quotas and enforcing absolute, categorical bans on all forms of stablecoin yield to protect European credit institutions.

- Actionable Impact for Retail Investors: Retail investors face immediate uncertainty regarding the future of centralized exchange "Earn" programs, which may be heavily restricted or suspended by late 2026. However, users must balance the loss of effortless yield against massive upgrades in systemic safety, as the new laws enforce radical transparency and provide priority bankruptcy claims that severely reduce the risk of a stablecoin de-pegging.