What Is the GENIUS Act 2026 Stablecoin Deadline

The GENIUS Act establishes the first comprehensive federal framework for U.S. dollar-backed payment stablecoins, mandating 1:1 liquid reserves and strict anti-money laundering controls to protect consumers and the broader financial system. With a critical statutory deadline of July 18, 2026, federal regulators are currently finalizing the rules that will permanently dictate how traditional banks, fintech startups, and foreign issuers compete in the emerging digital payments economy.

The Genesis of Federal Stablecoin Regulation

For years, the U.S. digital asset market operated in a regulatory gray area. Stablecoin issuers navigated a fragmented, inefficient patchwork of state-by-state money transmitter licenses while operating outside the traditional federal banking perimeter 11. Economists and policymakers frequently compared this environment to the chaotic "free banking era" of 1837 - 1862, warning that without federal guardrails, the rapid growth of privately issued digital money posed systemic risks 2.

To address this, Senator Bill Hagerty introduced the Guiding and Establishing National Innovation for U.S. Stablecoins (GENIUS) Act in May 2025 2. Recognizing the necessity of regulatory clarity, the legislation garnered massive bipartisan support, passing the U.S. Senate with a 68 - 30 vote and the House of Representatives by a 308 - 122 margin 234. President Donald Trump signed the bill into law on July 18, 2025, declaring it a crucial step in cementing the U.S. dollar's status as the global reserve currency and securing American leadership in digital financial technology 256.

The Casino Chip Analogy

To grasp the regulatory philosophy underlying the GENIUS Act, it is helpful to understand how stablecoins actually function in the broader economy. Industry experts frequently compare stablecoins to casino chips 8. Inside a casino, a chip is a widely recognized and trusted medium of exchange. Players, dealers, and cashiers accept it seamlessly, accelerating the velocity of transactions. However, the chip itself is not money; it is a bearer instrument representing a promise. Its value is entirely derived from the underlying belief that it can be redeemed for actual fiat currency at the cashier's cage at any moment 8.

Stablecoins operate on a similar Layer 2 payment architecture. Within the digital economy, they change hands rapidly, facilitating global trade, decentralized finance, and instant remittances. However, the underlying Layer 1 currency - the actual U.S. dollars backing the tokens - never actually leaves the issuer's bank account 8. Prior to the GENIUS Act, the "cashier's cage" was largely unregulated at the federal level. The new legislation serves to aggressively regulate that underlying reserve pool, ensuring that the institutions issuing these digital chips actually possess the cash they claim to hold, thus transforming the illusion of money in motion into a legally guaranteed reality 89.

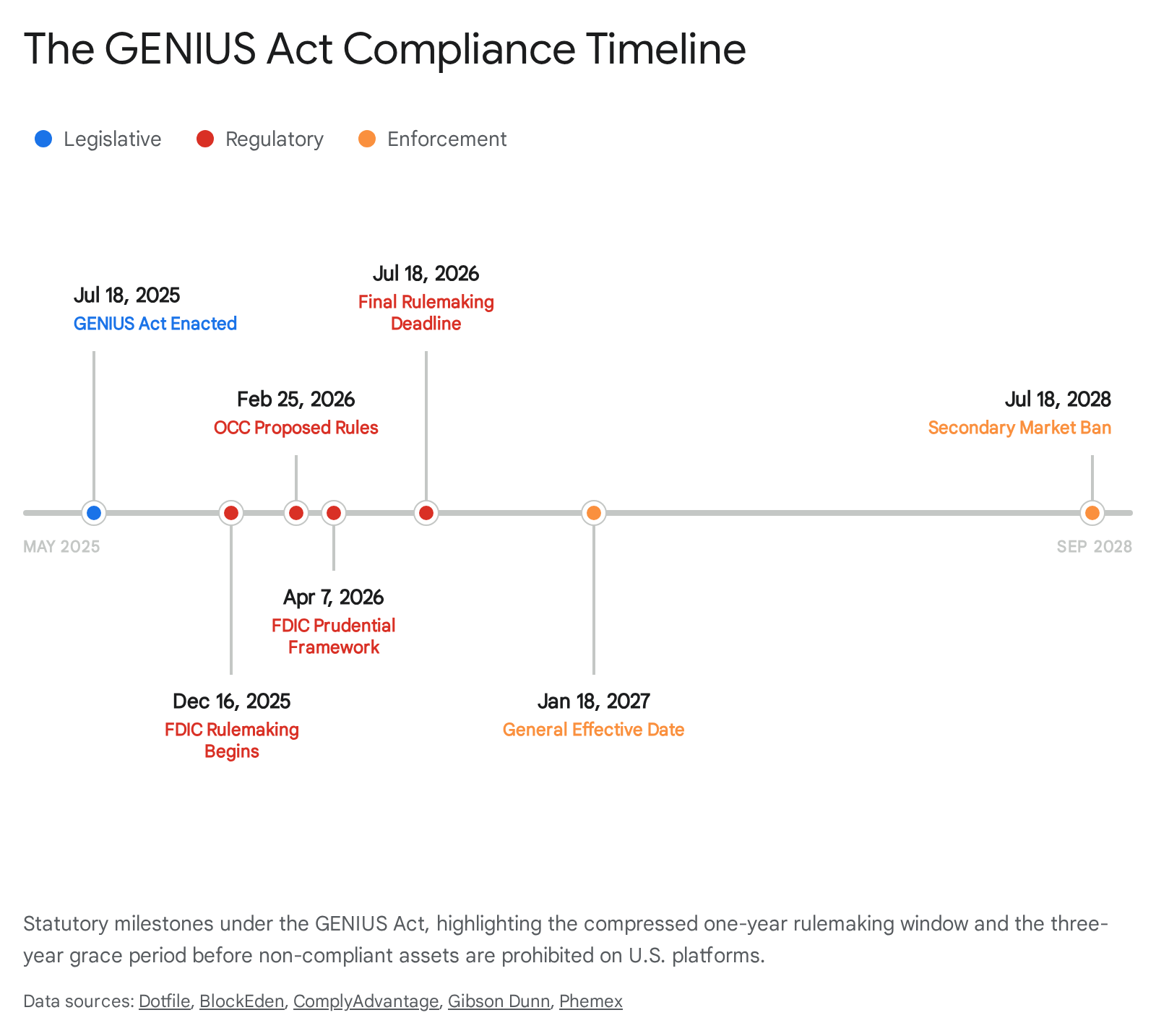

The 2026 Compliance Timeline and Looming Deadlines

The passage of the GENIUS Act effectively started a high-stakes ticking clock for federal agencies, traditional banks, and native cryptocurrency operators. The legislation mandates that primary federal regulators - specifically the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation (FDIC), and the Department of the Treasury - must finalize their implementing regulations within exactly one year of the bill's signing 147.

This creates a highly compressed rulemaking window. As illustrated in the timeline below, the regulatory rollout dictates when the market transitions from proposed frameworks to hard enforcement.

The sequence of milestones is unforgiving. Federal regulators began pushing out Notices of Proposed Rulemaking (NPRMs) in early 2026, with the FDIC acting in December 2025 and April 2026, the OCC in February 2026, and the Treasury following in April 2026 3789.

The critical threshold is July 18, 2026, the statutory deadline for all primary federal agencies to issue their final rules 11014. The law formally takes effect on the earlier of two dates: 120 days after these final regulations are issued, or January 18, 2027 (exactly 18 months post-enactment) 1710. If regulators somehow miss the July 2026 deadline, the statutory framework activates automatically in January 2027, which could create a chaotic regulatory vacuum where the law is enforceable but operational implementation guidelines remain undefined 7.

Finally, the Act provides a three-year safe harbor for secondary markets. By July 18, 2028, a "hard delisting cliff" occurs, legally prohibiting any digital asset service provider (like cryptocurrency exchanges or wallet hosts) from offering non-compliant stablecoins to individuals in the United States 1101116.

Core Requirements of a Permitted Payment Stablecoin Issuer

The GENIUS Act establishes a bespoke supervisory regime by creating a new category of regulated entity: the Permitted Payment Stablecoin Issuer (PPSI) 71213. To qualify for and maintain this status, an entity must adhere to a strict set of operational, financial, and compliance pillars that completely redesign the architecture of privately issued digital dollars.

The 1:1 Reserve Mandate

Historically, the term "reserves" in the crypto industry was applied loosely. Some major issuers backed their tokens with commercial paper, corporate debt, or other relatively illiquid assets that resembled business loans more than actual cash reserves 9. The GENIUS Act entirely eliminates this ambiguity.

A PPSI is now legally required to maintain identifiable reserves backing its outstanding payment stablecoins on at least a 1:1 basis 11213. The statute severely restricts the composition of these reserves to highly liquid, low-risk instruments. Permissible assets are limited to U.S. currency, demand deposits at federally insured depository institutions, U.S. Treasury securities with a strict maturity limit of 93 days or less, and overnight repurchase agreements backed by those short-term Treasuries 11213. The Act strictly forbids issuers from rehypothecating, lending out, or commingling these reserve assets with the company's general corporate funds 119.

To prevent systemic contagion and bank runs, the FDIC has proposed concentration limits. Under the FDIC's April 2026 proposed rule, an issuer cannot hold more than 40% of its reserve assets at any single eligible financial institution, mitigating the risk of an issuer becoming overly exposed to a single banking partner's failure 10.

Consumer Protection and Superpriority

To guarantee the safety of the public's funds, the GENIUS Act mandates radical transparency. PPSIs must publish monthly reports detailing the exact composition of their reserves, and these reports must be verified by independent third-party audits 3513. Executives are held personally liable; chief executive and financial officers must certify the accuracy of these reports under penalty of perjury, with false certifications triggering potential criminal fines of up to $5,000,000 and 20 years imprisonment 113.

Crucially, the legislation amends the U.S. Bankruptcy Code to grant stablecoin holders priority - and potentially superpriority - claims over the reserve assets in the event of an issuer's insolvency 51314. This ensures that the 1:1 reserve pool is completely ring-fenced from the issuer's general creditors, creating a formidable consumer protection backstop 315.

Anti-Money Laundering (AML) and Sanctions Integration

Prior to the GENIUS Act, stablecoin issuers operated under state-level money transmission laws that varied wildly in their enforcement of financial crime controls 11. The new legislation definitively integrates stablecoins into the federal Bank Secrecy Act (BSA) framework 15.

Under the joint proposed rules issued by the Financial Crimes Enforcement Network (FinCEN) and the Office of Foreign Assets Control (OFAC) in April 2026, PPSIs are formally classified as financial institutions 69. They must implement rigorous, risk-based AML and Countering the Financing of Terrorism (CFT) programs 616. This places the same burden on stablecoin operators as commercial banks, requiring continuous customer identification, suspicious activity reporting, and sanctions list verification 5. Furthermore, the law mandates that issuers possess the technical ledger capability to freeze, seize, or burn tokens when legally required by enforcement orders 15.

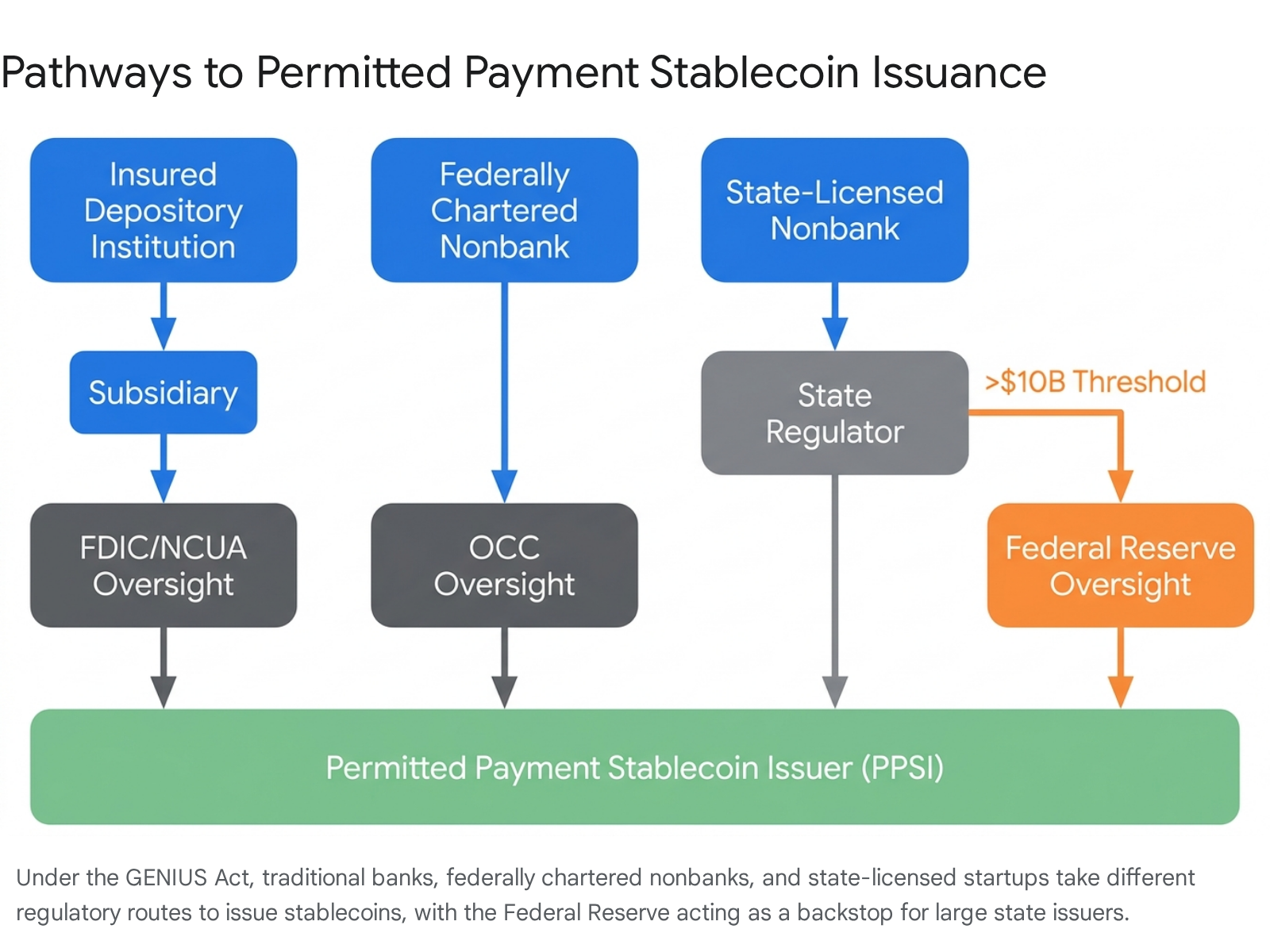

The Three Regulatory Pathways to Issuance

The GENIUS Act rejects a monolithic federal monopoly on regulation, instead establishing a dual federal-state supervisory architecture 131623. This architecture, mapped in the schematic below, ensures rigorous standards while preserving multiple avenues for both incumbent financial giants and native technology startups to enter the market.

1. The Bank Subsidiary Route

Traditional federally insured depository institutions - banks and credit unions - can legally issue stablecoins 1623. However, they cannot do so directly off their primary balance sheets. To protect core banking operations and FDIC-insured deposits from potential crypto-asset volatility, banks must establish specific, ring-fenced subsidiaries to serve as the PPSI 11323. The FDIC and the National Credit Union Administration (NCUA) advanced application procedures for this pathway in late 2025 and early 2026, creating an on-ramp for traditional finance to enter the digital asset space safely 71012.

2. The Federal Nonbank Charter

For fintech companies, uninsured national banks, and digital asset native firms that want a streamlined national presence, the Act establishes a direct federal pathway 1623. These entities can apply to the OCC for a specialized federal charter 113. If approved as a "Federal Qualified Payment Stablecoin Issuer," the firm can operate nationwide without needing to secure fifty individual state money transmission licenses 1. In February 2026, the OCC issued a massive 376-page NPRM detailing the full supervisory lifecycle for these firms, establishing rigorous standards for capital, liquidity, and risk management 161217.

3. The State Certification Pathway

To ensure that states retain their historical role as laboratories for financial innovation, nonbank entities can choose to remain under the supervision of state regulators 11316. This path is particularly viable for smaller or emerging issuers. However, this pathway carries a strict volume constraint: if a state-regulated issuer's outstanding stablecoin circulation exceeds $10 billion, it automatically triggers joint supervisory oversight and backup enforcement authority from the Federal Reserve Board 1162317.

Furthermore, state regulatory frameworks cannot be lax. States must submit their local stablecoin regulations to a federal Stablecoin Certification Review Committee, comprised of the Treasury Secretary, the Federal Reserve Chair, and the FDIC Chair 313. This committee must unanimously certify that the state's regime is "substantially similar" to the federal standards 314. The Treasury formally proposed the guiding principles for this substantial similarity test in April 2026, with states facing a deadline to update their laws to secure certification 3913.

The $6.6 Trillion Question: Stablecoins vs. Tokenized Deposits

One of the most intensely debated aspects of the GENIUS Act involves the treatment of yield. The statute explicitly prohibits payment stablecoin issuers from paying interest or yield directly to token holders 71318.

This hardline stance was heavily influenced by traditional banking lobbyists, including the Independent Community Bankers of America (ICBA), who warned that allowing stablecoins to pay interest could trigger a catastrophic migration of deposits out of the commercial banking system. Early industry estimates suggested that up to $6.6 trillion in traditional deposits could be siphoned into digital assets if stablecoins functioned essentially as unregulated, high-yield digital savings accounts 7.

By legally banning yield on payment stablecoins, the GENIUS Act clarifies that these tokens are instruments of settlement, not instruments of credit creation or savings 726. However, this prohibition has inadvertently accelerated the development of a competing product: tokenized bank deposits 1827.

| Feature Comparison | Payment Stablecoins (Under GENIUS Act) | Tokenized Bank Deposits |

|---|---|---|

| Issuer Type | Nonbanks, or specifically ring-fenced bank subsidiaries 113 | Commercial banks directly from their primary balance sheet 27 |

| Legal Classification | Not a security, not a bank deposit; specialized payment instrument 1418 | Legally recognized as traditional bank deposits 27 |

| Yield / Interest | Prohibited by law from the issuer 713 | Permitted, as they rely on established banking regimes 27 |

| Asset Backing | 1:1 backing with highly liquid, safe assets (e.g., Treasuries) 113 | Fractional-reserve banking (backed by bank loan portfolios) 26 |

| Consumer Insurance | Bankruptcy superpriority; No FDIC pass-through insurance 913 | Fully backed by standard FDIC deposit insurance 927 |

This regulatory bifurcation suggests a coming market split. Because stablecoin issuers cannot pay yield, these tokens will likely dominate the retail payments space, cross-border remittances, and decentralized finance networks 1628. Conversely, tokenized bank deposits - which are exempt from the yield ban due to their status under banking laws - are poised to dominate the institutional B2B market, corporate treasury management, and large-scale wholesale settlement where earning interest on idle capital is non-negotiable 162728. It is worth noting, however, that while stablecoin issuers cannot pay yield, users can still generate returns by deploying their stablecoins into third-party decentralized lending protocols 78.

The Battle for the Settlement Layer

While the FDIC, OCC, and Treasury moved swiftly in early 2026 to propose rules governing who can issue stablecoins, a massive operational question remained unresolved: how would these nonbank fintechs actually clear and settle their digital dollars? Without direct access to the Federal Reserve's payment rails, fintechs would be forced into dependent, expensive partnerships with traditional sponsor banks 1930.

The Federal Reserve had been historically hesitant to grant nonbanks direct access to the nation's core payment infrastructure, citing systemic risks and money laundering concerns 3020. However, the landscape shifted dramatically on March 4, 2026, when the Federal Reserve Bank of Kansas City broke protocol and granted a limited-purpose master account to Kraken Financial, making it the first digital asset bank to gain direct access 302032.

The May 19 Executive Order

To break the regulatory bottleneck and support the intent of the GENIUS Act, President Trump signed an Executive Order on May 19, 2026, titled "Integrating Financial Technology Innovation into Regulatory Frameworks" 213422. The Order explicitly criticized fragmented and burdensome supervisory practices that protect incumbent banks from competition 213422.

The directive was aggressive. It required all federal financial regulators to conduct a 90-day review of existing regulations impeding fintech integration, and ordered them to implement steps to encourage innovation within 180 days 2123. Most significantly, Section 4 of the Order specifically requested the Federal Reserve to evaluate options for expanding direct payment account access to non-bank digital asset firms, demanding a report back to the President within 120 days 342223. The timing coincided with the Senate confirmation of a new, potentially more crypto-friendly Federal Reserve Chair, Kevin Warsh, further pressuring the central bank's traditional posture 3738.

The Fed's Payment Account Proposal

Responding immediately to the political and industry pressure, the Federal Reserve Board voted 6-1 the very next day, May 20, 2026, to publish a formal proposal establishing a new "payment account" prototype specifically tailored for fintech and nonbank institutions 303224.

This "skinny" master account is heavily restricted to manage risk: * No Credit Access: Account holders cannot access the discount window or intraday credit 322425. * No Interest: Balances held at the Reserve Bank do not earn interest 3224. * Overdraft Controls: Access is limited to payment services with automated controls to prevent overdrafts (such as FedNow and Fedwire) 3224. * Dynamic Balance Limits: Closing balance limits are capped based on an institution's expected payment activity, not to exceed a hard limit of $1 billion 3224.

The proposal faced internal pushback. Federal Reserve Governor Michael Barr delivered a dissenting vote, arguing that the framework lacked robust safeguards to protect against illicit finance by institutions the Fed does not directly supervise 20. The outcome of the 60-day comment period on this proposal will effectively determine whether GENIUS Act stablecoin issuers become independent financial powerhouses or remain reliant on legacy banking infrastructure 3032.

The Global Arena: The GENIUS Act vs. Europe's MiCA

The U.S. framework does not exist in a vacuum. The European Union's Markets in Crypto-Assets (MiCA) regulation became fully active in 2024. Together, MiCA and the GENIUS Act govern jurisdictions responsible for over 60% of global stablecoin transaction volume 26. For businesses operating internationally, navigating the divergence between these two frameworks is the single largest operational variable they face in 2026 26.

While both laws mandate 1:1 reserve backing and guarantee the redemption of tokens at par, their underlying regulatory philosophies are starkly opposed 152627. The EU's MiCA operates on the Precautionary Principle, assuming stablecoins pose systemic risks to the banking sector until proven otherwise. Consequently, MiCA heavily restricts stablecoin issuance to established credit institutions and electronic money institutions, essentially functioning as a banking license requirement 32643.

In contrast, the U.S. GENIUS Act operates on the Innovation Principle. While it sets rigid structural guardrails regarding asset quality, it is designed to allow nonbank startups to compete aggressively with traditional finance 2643.

The technical divergence is most evident in reserve composition. MiCA mandates that issuers of e-money tokens must hold at least 30% of their reserves in European commercial bank deposits, rising to 60% for tokens deemed "significant" 315. The GENIUS Act takes the exact opposite approach. Seeking to insulate stablecoins from the leverage risks of commercial banking, the U.S. law caps single-bank deposit concentration and pushes issuers toward holding short-term U.S. Treasury securities and central bank cash 101315.

Furthermore, to protect monetary sovereignty, MiCA's Article 23 imposes a harsh €200 million daily transaction cap on stablecoins denominated in non-euro currencies when used as a medium of exchange 16. The GENIUS Act, conversely, contains no such caps and is actively intended to promote the global proliferation of USD-denominated stablecoins to reinforce the dollar's international dominance 515. Crucially, there is no equivalence framework between the two regimes; a MiCA-licensed issuer cannot operate in the U.S. without securing separate GENIUS Act compliance, forcing global operators to maintain dual licensing and disparate reserve structures 2627.

Macroeconomic Impact and Market Reality

As the July 2026 regulatory deadline approaches, the macroeconomic impact of the GENIUS Act is becoming increasingly apparent. By the end of 2025, global stablecoin circulation had surpassed $200 billion 819. Because the Act legally forces all compliant USD stablecoins to be backed 1:1 by cash or short-term U.S. Treasuries, the stablecoin ecosystem is transitioning into a massive, inelastic buyer of U.S. government debt 519.

Financial analysts predict that if compliant stablecoin volumes approach $500 billion, this mandatory, structural buying pressure will begin to substantially compress short-term Treasury yields 19. The White House has explicitly championed this dynamic, viewing stablecoin proliferation as a strategic mechanism to ensure continued global demand for U.S. Treasuries amidst a ballooning national deficit 537.

The Diverging Fates of USDC and USDT

The stringent new rules are forcing immediate strategic realignments for the two dominant market players: Circle's USDC and Tether's USDT, which together account for nearly 87% of the total stablecoin market 1928.

Circle (USDC) is heavily favored by the new landscape. The company proactively built its operational model around the transparency and asset-quality standards now codified by the GENIUS Act. By holding reserves in cash and short-dated Treasuries and providing regular attestations, USDC became the first major stablecoin to achieve compliance with MiCA in Europe, and it seamlessly aligns with the impending U.S. rules 84344.

Tether (USDT), however, faces severe compliance headwinds in regulated Western markets. Tether has historically prioritized deep liquidity in emerging markets over proactive regulatory alignment, operating offshore with less transparent reserve compositions 843. As a result of MiCA enforcement, USDT has already faced widespread delistings across European exchanges, including Coinbase Europe, Bitstamp, and Kraken EEA 16. Under the GENIUS Act, if the OCC rules that Tether does not meet the strict criteria for a "Foreign Payment Stablecoin Issuer," U.S. digital asset platforms will be legally forced to delist USDT entirely by the July 18, 2028 enforcement cliff 1101619. Such an event would trigger a massive restructuring of global cryptocurrency liquidity 19.

Bottom line

The GENIUS Act represents the permanent transition of digital dollars from an unregulated crypto experiment into foundational U.S. financial infrastructure. By July 18, 2026, the final implementation of 1:1 safe-asset backing, the prohibition of issuer-paid yield, and the enforcement of bank-grade AML standards will fundamentally reshape the competitive landscape. While the path is now clear for nonbank fintechs and traditional banks to battle for market share via dedicated payment accounts and tokenized deposits, immense uncertainty remains regarding how foreign giants like Tether will navigate the new, unforgiving compliance reality before the 2028 delisting cliff.