Why the Stock Market Moves on News Everyone Already Knows

The stock market acts as a forward-looking discounting engine, setting asset prices based on future expectations rather than current events. When highly anticipated news finally breaks, its financial impact has usually already been priced in by early investors who bought the asset in advance. The actual announcement simply acts as a catalyst for these early buyers to take profits, while automated options hedging mechanically accelerates the price reversal.

The Forward-Looking Machine: Understanding Market Efficiency

To understand why markets frequently react negatively to positive news - or positively to negative news - one must first abandon the intuitive idea that stock prices reflect the present moment. Financial markets are anticipatory. They act as massive discounting engines, constantly vacuuming up publicly available information, rumors, geopolitical shifts, and economic forecasts to calculate the future value of an asset 11.

At the heart of this dynamic is a concept known as the Efficient Market Hypothesis (EMH). In its most practical form, the EMH suggests that all public information, as soon as it becomes available, is immediately reflected in the price of an asset 2. By the time a retail investor reads a headline about a company securing a massive new government contract, or a central bank hinting at cutting interest rates, institutional trading desks, algorithmic bots, and hedge funds have already bid the price up to reflect that new reality 2.

When the actual news event officially occurs, it rarely contains information that the collective market has not already debated, mathematically modeled, and traded upon for weeks or even months prior. If the news merely confirms what the market already suspected, there is no new upward "catalyst" to drive the price higher. Without a fresh influx of buyers stepping in, early investors who bought the asset in anticipation of the news will sell their positions to lock in their profits, creating downward pressure on the stock 13.

The Sports Betting Analogy: Pricing the Spread

One of the most accurate ways to conceptualize market expectations is to look at the mechanics of sports betting. The betting lines set by oddsmakers function almost identically to the prices set by buyers and sellers in public securities markets 5.

Imagine a hypothetical hockey game between a professional NHL team and a top-tier junior team. The talent gap is massive, and the NHL team's victory is almost a complete certainty 6. If sportsbooks only offered a simple win/lose bet, every single bettor would wager on the NHL team, which would quickly bankrupt the casino. To balance the market and manage risk, oddsmakers introduce a goal spread - requiring the NHL team to win by, for example, 20 goals for a bet on them to actually pay out 6.

The goal spread is the direct equivalent of a stock's valuation. It reflects all known information: the talent disparity, recent injuries, historical performance, home-ice advantage, and public betting sentiment 56. If the NHL team wins the game by 15 goals, they have overwhelmingly won the real-world physical contest, but they have failed to cover the spread. Anyone who bet on them loses money.

The stock market operates on this exact same logic. A company can announce record-breaking, multi-billion-dollar profits (winning the game), but if Wall Street had collectively "priced in" even higher profits (the spread), the stock will fall 17. Just as the final score of a sporting event only matters relative to the point spread, a corporate earnings report or an economic data release only matters relative to established market expectations 1.

Recent academic research reinforces this parallel. Tobias Moskowitz, a Professor of Finance at the Yale School of Management, has studied the intersection of sports and economics extensively. His research indicates that sports betting markets exhibit the same pricing patterns seen in the stock market, including distinct "momentum" and "value" effects 4. In both arenas, participants tend to overprice teams (or companies) that have done well recently, pushing the "spread" to unsustainable levels where even a victory feels like a disappointment 4.

"Buy the Rumor, Sell the News": The Psychology of Anticipation

The phrase "buy the rumor, sell the news" has circulated among Wall Street trading floors and European trading houses for well over a century 1. Its persistence across generations, through multiple market structures, and past massive technological revolutions suggests that it describes a fundamental truth about how human beings collectively process information and manage risk under uncertainty 1.

The strategy is deeply rooted in the capitalization of sentiment. When rumors circulate about a potentially positive development - such as an impending corporate merger, a medical trial breakthrough, or a favorable central bank policy change - traders begin buying the asset immediately to get ahead of the crowd 13. As the price begins to rise, a psychological feedback loop takes hold. Other market participants, experiencing the fear of missing out (FOMO), rush in to buy the asset, which magnifies aggregate demand and drives prices even higher 3.

During this "rumor" phase, the asset's price often becomes detached from its current fundamental reality. The valuation is no longer based on the cash the company is generating today, but rather on the wave of enthusiasm surrounding the expected future value creation 3.

The Catalyst for the Reversal

When the highly anticipated day arrives and the news is officially released, the psychological environment undergoes an immediate transformation. The uncertainty that fueled the speculative buying is gone. The potential future is now the concrete present.

For the institutional traders who bought the asset weeks or months in advance, the official announcement represents the perfect opportunity for exit liquidity. Because retail investors and latecomers are often buying right as the news breaks on television or social media, the early speculative buyers can easily sell their large positions into this fresh demand to lock in their profits 1. If enough institutional traders sell simultaneously, this wave of supply overwhelms the new demand, causing the price to fall rapidly 19.

The news itself may be objectively excellent, but because the market is forward-looking, the financial benefit of that news was already extracted during the run-up 1. The announcement merely serves as the trigger for mechanical profit-taking rather than a reason for fresh investment 1.

The Expectations Game: Official Consensus vs. Whisper Numbers

Understanding why a stock drops after a good earnings report requires looking beyond the official estimates published by Wall Street analysts. In modern financial markets, there is the "official consensus" and then there is the "whisper number."

Publicly traded companies are legally required to provide timely updates on their performance, usually through quarterly earnings reports 710. In the weeks leading up to these reports, equity analysts publish their forecasts for the company's revenue and earnings per share (EPS). The average of these forecasts becomes the official consensus 7.

However, savvy institutional investors know that corporate management teams are adept at playing the "expectations game." Companies frequently guide analysts toward slightly lower, easily beatable targets, ensuring that they can announce an "earnings beat" when the actual data is released 10. Because the market is well aware of this tactic, the true expectation of buy-side investors (hedge funds, mutual funds) is often much higher than the official consensus. This higher, unofficial bar is known as the whisper number.

If a company reports earnings that beat the official consensus but fail to reach the whisper number, the stock will likely be punished. The market views this not as a victory, but as a disappointment relative to the true expectations that were priced into the stock. Furthermore, high expectations can lead to extreme valuations, where a stock is "priced for perfection." When a stock is priced for perfection, any slight flaw in the report - such as a minor deceleration in growth, a dip in profit margins, or cautious forward guidance - can trigger a massive sell-off 1112.

Case Study: Nvidia's Paradoxical Earnings Drops

The mechanics of the expectations game have been perfectly illustrated by Nvidia, the undisputed leader in artificial intelligence infrastructure, across multiple earnings cycles in 2024 and 2025.

In August 2024, Nvidia released its earnings for the second quarter of its 2025 fiscal year. Going into the report, the official Wall Street consensus expected Nvidia to report revenues of $28.42 billion and fully diluted earnings per share of 64 cents 710. When the report was released, the numbers were staggering. Nvidia posted a record-breaking $30 billion in revenue and 68 cents in earnings per share, easily beating the official estimates 10.

Yet, in the immediate aftermath of this seemingly spectacular news, Nvidia's stock plunged 8% in the following day's trading session, wiping out more than $200 billion in market capitalization 710.

| Earnings Period | Wall Street Revenue Consensus | Actual Revenue Reported | Wall Street EPS Consensus | Actual EPS Reported | Immediate Stock Reaction |

|---|---|---|---|---|---|

| Q2 FY 2025 (Aug '24) | $28.42 Billion | $30.00 Billion | $0.64 | $0.68 | -8.0% Drop |

| Q4 FY 2025 (Feb '25) | $38.10 Billion | $39.30 Billion | N/A | $22.1B (Net Income) | -8.5% Drop |

Note: Data derived from Nvidia's August 2024 and February 2025 earnings cycles 710115.

Why did the market react so negatively to objective success? The answer lies in the nuances of expectations, forward guidance, and the "whisper number":

- The Magnitude of the Beat: While Nvidia beat the estimates, the percentage by which it beat expectations was smaller than in its previous blowout quarters 10. The market had grown accustomed to Nvidia shattering records by massive margins. When the company merely beat expectations by a standard amount, it failed the unofficial whisper number test.

- Margin Compression: Investors looked past the top-line revenue and noticed underlying pressures. In its Q4 report in early 2025, Nvidia's gross profit margin fell to 71%, down from 73.5% previously 11. This compression suggested that the cost of transitioning to its complex, next-generation Blackwell AI chips was cutting into profitability 11.

- The DeepSeek and Hyperscaler Threats: While revenue was high, forward-looking investors were increasingly concerned about competition. The emergence of the DeepSeek AI model raised concerns that powerful artificial intelligence could be built with fewer high-performance GPUs, potentially cooling demand 11. Furthermore, hyperscalers (like Amazon and Microsoft) were aggressively looking to design their own in-house chips to reduce reliance on Nvidia 514.

- The Buyback Signal: During the August 2024 call, Nvidia announced a $50 billion authorization for stock buybacks 10. While normally a positive sign, some investors interpreted this massive capital return as a signal that Nvidia was transitioning from a hyper-growth startup into a mature cash cow. It conflicted directly with the narrative of "unlimited growth" that speculative investors had priced into the stock 10.

Nvidia's drop was not a reflection of a failing company; it was a textbook example of a stock priced so high that reality simply could not clear the astronomical hurdle set by market anticipation.

Case Study: TSMC, AI Dominance, and Geopolitics

A similar dynamic occurs when robust corporate fundamentals are overshadowed by broader macroeconomic or geopolitical fears. Taiwan Semiconductor Manufacturing Company (TSMC), the world's dominant semiconductor foundry, experienced this repeatedly.

In April 2024, TSMC reported incredibly strong Q1 results. The company posted 839.25 billion New Taiwan dollars (NT$) in revenue - beating expectations of NT$ 835.13 billion - and a net income of NT$ 361.56 billion against an expected NT$ 354.14 billion 15. TSMC's revenue in March 2024 alone rose 34% year-over-year 16. Despite these solid numbers, the stock showed a near-constant underperformance relative to the broader S&P 500 in the leadup to and immediately after the earnings release 15.

The market's lack of enthusiasm was rooted in factors not found on the balance sheet: * The AI Premium was Exhausted: The market had already aggressively priced in the AI boom. While analysts noted that AI spending could reach $400 billion by 2027, this long-term optimism was already reflected in TSMC's multi-year run-up 16. When forward growth trends suggested slower expansion than in previous fiscal years, the stock stalled 15. * Geopolitical Overhang: TSMC sits at the epicenter of the semiconductor trade war between the United States and China. Export restrictions imposed by the US cut off TSMC's revenue from advanced chips destined for restricted Chinese entities 17. * Costly Diversification: To mitigate geopolitical risks and appease Western governments, TSMC was forced into rapid geographic diversification, breaking ground on fabrication plants in Arizona and Dresden, Germany. These projects were plagued by construction delays, specialized labor shortages, and extraordinarily high costs, which investors feared would weigh heavily on future operating margins 1517.

Even though the immediate "news" (the earnings report) was excellent, the market sold the stock because the longer-term structural and geopolitical risks outweighed the quarterly financial triumph.

How Central Banks Move Markets: It's All About the Future

The "priced in" phenomenon is perhaps most visible and consequential in the realm of macroeconomic policy, specifically the actions of global central banks. Interest rates serve as the foundational gravity for all asset valuations. When central banks announce rate decisions, the market's reaction is almost never based on the rate cut or hike itself - it is based entirely on the forward guidance regarding future actions.

The Federal Reserve's "Soft Landing" Dance

In November and December of 2023, both the US stock and bond markets rallied aggressively. The primary narrative driving this immense surge was a firm belief that the US Federal Reserve would aggressively cut interest rates in 2024 to engineer a perfect "soft landing" for the economy 6. Traders essentially "priced in" a near-certainty of a dovish pivot, with futures markets predicting as many as six quarter-point rate cuts (amounting to 150 basis points) for the upcoming year 6.

However, when the Federal Open Market Committee (FOMC) met in January and March of 2024, they held rates steady at a decades-high range of 5.25% to 5.5% 78. On the day of the January announcement, US equities moved notably lower in the afternoon 7.

The market had eagerly bought the rumor of rapid rate cuts, but was forced to sell the reality of Federal Reserve Chairman Jerome Powell's press conferences. Powell emphasized that while progress was being made, the path forward was "uncertain" and that the committee needed "more data" to ensure inflation was sustainably moving toward their 2% target 78. Because the market had already priced in absolute perfection, the mere introduction of caution and delayed timelines was enough to trigger a rapid sell-off across equities 78.

The ECB and the Bank of Japan

This dynamic played out globally throughout 2024, highlighting that forward guidance overrides current action: * The European Central Bank (ECB): In June 2024, the ECB delivered a highly anticipated rate cut of 25 basis points, lowering its deposit rate to 3.75% 910. The cut was explicitly designed to moderate the degree of monetary policy restriction 10. However, the market reaction was heavily muted. Why? Because the cut was primarily driven by earlier pre-commitments, not a dovish outlook 11. During the announcement, the ECB explicitly refused to pre-commit to a particular rate path moving forward, citing stubbornly high domestic inflation and elevated wage growth that pushed their inflation projections for 2025 up to 2.2% 910. The news of the cut was already fully in the price; the hawkish hesitation about the future was the new information the market had to aggressively digest. * The Bank of Japan (BoJ): In March 2024, the BoJ made a historic monetary policy shift. After years of fighting deflation, they ended their controversial negative interest rate policy (NIRP), moving the benchmark rate to a range of 0% to 0.1%, and simultaneously ended their Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control (YCC) program 121326. The move was bolstered by robust wage increases secured during the ongoing Shunto wage negotiations 14. Normally, raising interest rates significantly strengthens a nation's currency. Yet, following the announcement, the Japanese Yen actually weakened initially. The market had spent weeks anticipating the move, fully pricing it into currency exchange rates. When the BoJ finally acted, it was accompanied by commentary suggesting that financial conditions would remain broadly accommodative for the time being, prompting currency traders to take profits on their long Yen positions rather than doubling down 1213.

The Hidden Plumbers: How Options Dealers Drive the Action

While human psychology and macroeconomic expectations explain the fundamental reasons why markets move counterintuitively, they do not fully explain the violent, mechanical speed of these reversals. To understand the intraday volatility that occurs exactly at the moment a news event drops, one must look at the hidden plumbing of modern financial markets: the options market.

In recent years, the sheer volume of options trading has grown so large that the derivatives tail is often wagging the equity dog. Options are no longer just a side bet; they are a primary driver of liquidity. The mechanics of how options market makers hedge their immense risk creates structural liquidity flows that force the buying and selling of stocks completely independently of human sentiment or fundamental news 15.

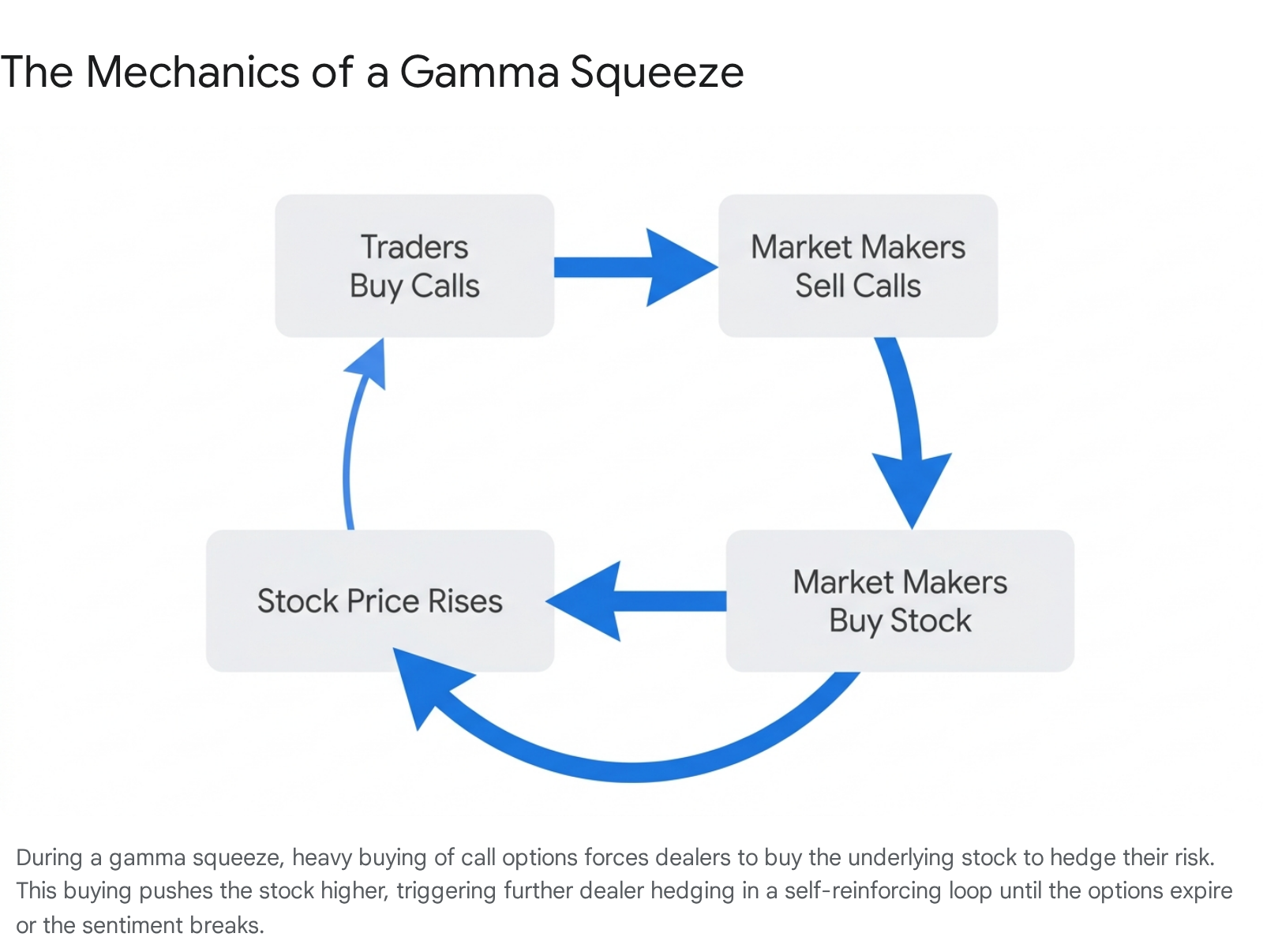

Delta Hedging and the Gamma Squeeze

When a retail or institutional trader buys a call option (a bet that a stock will go up), there must be a counterparty on the exact opposite side of that trade. Usually, this counterparty is a specialized market maker or options dealer 1617. Crucially, market makers are not in the business of directional gambling; they simply want to provide liquidity and collect the spread between the bid and ask prices 17.

To eliminate their directional risk when they sell a call option, the market maker will immediately buy a certain amount of the underlying stock. This practice is known as "delta hedging" 1731. Delta represents how much the option's price is expected to move for every $1 change in the underlying stock 1617. If the stock price rises, the option's delta increases, forcing the market maker to buy more shares of the stock to remain properly hedged 1731.

This mechanical hedging process can create a self-reinforcing feedback loop known as a "gamma squeeze." Gamma is the rate of change of an option's delta 1617.

If positive news is rumored and speculators aggressively buy call options, dealers are forced to buy the underlying stock to hedge their short call positions 3233. The dealers' buying pushes the stock price higher. As the stock price climbs, the gamma of the options increases exponentially, causing the delta to rise, which forces the dealers to buy even more stock to stay neutral 1733. This creates an explosive, mechanical rally driven entirely by options plumbing rather than fundamental valuation 33. This mechanism was a primary driver in the meteoric rise of GameStop in 2021, where the gamma squeeze provided massive additional fuel to an underlying short squeeze 1732.

Vanna and the Post-Earnings Volatility Crush

While gamma explains why stocks run up before an event, an options greek known as vanna is the primary culprit explaining why stocks immediately crash after earnings reports.

Vanna measures the change in an option's delta with respect to a change in implied volatility (IV) 163435. Before a major, binary news event like a quarterly earnings report or a highly anticipated Fed meeting, uncertainty is at its absolute maximum. Because the outcome is entirely unknown, the options market prices in heavy risk, causing implied volatility to skyrocket to a premium 1536.

The moment the earnings report is published to the wire, the uncertainty instantly vanishes. The news is out, the numbers are known. As a direct mathematical result, the implied volatility in the options market collapses instantly - a phenomenon universally known among traders as a "volatility crush" 3336.

Here is where the plumbing takes over: when implied volatility drops, the delta of out-of-the-money options shrinks rapidly toward zero, thanks to the mechanics of vanna 16. For the market makers who were holding millions of shares of the underlying stock to hedge against those highly volatile options, this sudden drop in delta means they are suddenly holding too much stock. To rebalance their portfolios and remain delta-neutral, the market makers are forced to indiscriminately dump millions of shares onto the open market within seconds of the news release 1635.

This massive, automated selling by options dealers can cause a stock to gap down violently, regardless of whether the CEO just announced record revenue or increased dividends. The drop is not a referendum on the company's fundamentals; it is simply the mechanical unwinding of options hedges triggered by a collapse in volatility 1634.

Gamma Pinning and the Charm Effect

Furthermore, as options contracts approach their monthly or weekly expiration dates, two powerful forces combine to paralyze the stock price: gamma pinning and charm.

- Gamma Pinning: When there is a massive amount of open interest concentrated at a specific options strike price, dealers' hedging behavior becomes strictly mean-reverting. If the stock price moves slightly above the strike, they are forced to sell the underlying. If it dips below, they must buy. This relentless two-sided hedging acts as a heavy shock absorber, "pinning" the stock to a specific price and severely frustrating directional traders who are waiting for a fundamental news release to spark a breakout 18.

- Charm: Charm measures how an option's delta changes as time passes 1634. As the clock ticks down toward the expiration Friday, the delta of out-of-the-money options naturally bleeds away. This time decay forces dealers to slowly unwind their hedges over the week, bleeding liquidity out of the market and leaving the stock highly vulnerable to massive, unhedged swings once the options finally expire and the stabilizing "shock absorbers" are completely removed 1634.

Algorithmic Trading and the Speed of Information

Compounding these mechanical market forces is the sheer speed at which information is digested in the modern financial era. The traditional paradigm of a human analyst reading a press release, building an Excel model, contemplating the data, and manually placing a trade is entirely obsolete.

Today, High-Frequency Trading (HFT) firms and algorithmic trading bots dominate global market liquidity 1920. These algorithms are programmed to ingest vast amounts of data - including live news feeds, social media sentiment, and economic calendars - and execute highly complex trades in fractions of a second 1920. When a scheduled data release occurs, algorithms instantaneously parse the headlines for keywords and numerical deviations from the consensus estimate. If a metric misses the whisper number by a fraction of a percent, the algorithms will initiate a massive, coordinated sell-off before a human trader has even finished reading the headline 1920.

Social Churning and the Echo Chamber Effect

Recent academic research sheds light on how the modern information ecosystem alters market reactions to news. A working paper from the National Bureau of Economic Research (NBER) investigated the precise role of social networks in the diffusion of public financial news 40.

The researchers hypothesized that social transmission (such as localized investor networks or internet platforms like StockTwits) heavily influences how fast news is priced in. Their findings confirmed that companies located in "high-centrality" networks experience approximately 29% stronger immediate price reactions and significantly higher immediate trading volume reactions to earnings news 40. Because the social network is dense and highly connected, the information diffuses almost instantaneously, aggressively accelerating the timeline over which the news is "priced in" to the stock 40.

However, the NBER researchers also identified a fascinating phenomenon they termed the "social churning hypothesis" 40. While high connectivity allows the stock price to find its new equilibrium very quickly (drastically reducing post-earnings drift), the subsequent social discussions trigger massive opinion divergence among retail investors 40. This leads to persistent, elevated trading volume and excessive churning long after the news event has passed, as retail investors furiously debate the nuances of the report while institutional algorithms have already moved on 40.

Diagnostic Expectations and Market Stability

Another crucial NBER study utilized structural asset pricing models combined with advanced machine learning to measure exactly how the stock market reacts to hundreds of macroeconomic data releases and central bank communications 214243.

Traditional economic theory relies on "rational expectations" - the idea that investors perfectly and unemotionally process information to determine a stock's true fundamental value 21. However, the NBER data revealed that investors suffer from "diagnostic expectations"; they systematically overreact to news about fundamental shocks 214243.

Paradoxically, the researchers found that this behavioral overreaction can sometimes act as a stabilizing force that actually dampens overall market volatility 2143. Because real-world news events are immensely complex, they often produce conflicting signals with counteracting market implications. For example, a blowout earnings report might contain fantastic short-term cash-flow news, but also hint at rising inflation which would increase discount rates 214243.

When investors overreact to multiple, contradictory shocks simultaneously based on a single news event, the overreactions frequently cancel each other out. The result is a shock composition effect where the overall aggregate market appears to underreact to a major news event. This provides an academic solution to the puzzle of "excess stability," leaving lay observers baffled as to why a seemingly monumental headline caused the broader market to barely register a blip 2143.

Broader Market Shocks: Tariffs, Layoffs, and Unexpected Data

To fully understand why the market shrugs off expected news, it is highly instructive to look at how the market reacts to unexpected news. When a true macroeconomic shock occurs that was not priced into the options market or algorithmic models, the ensuing volatility is devastating, driven by genuine panic rather than mechanical unwinding.

A prime example occurred in April 2025, when sweeping US tariff policies were announced unexpectedly. Because the breadth and severity of the tariffs were not widely anticipated, there was no "buy the rumor" phase. The announcement triggered immediate, widespread panic selling across global stock markets, marking the largest global market decline since the 2020 pandemic crash 22. The S&P 500 lost 5.97% over two consecutive days of heavy losses, and the tech-heavy Nasdaq Composite entered bear market territory as algorithms and humans alike scrambled to reprice the fundamental reality of global trade 22.

Similarly, in late 2025, a report by Challenger, Gray & Christmas revealed a staggering 153,074 job cuts in October, highlighting severe weakness in the labor market at a time when official government data was delayed 23. The tech sector led the private-sector layoffs, completely catching a market that was heavily invested in the AI boom off guard 23. Because this depth of economic slowing was not priced into the lofty valuations of major tech firms, Wall Street tumbled, with the Nasdaq dropping 1.9% in response to the unmodeled data 23.

When the market is hit with a genuine surprise, it resets violently. When it is hit with scheduled, heavily modeled news, it simply unwinds its bets.

Bottom line

The stock market rarely moves in direct, logical correlation with the tone of a breaking news headline because the financial value of that news was likely extracted weeks prior by anticipatory investors. When an expected event finally occurs, a complex combination of psychological profit-taking, the disappointment of missing unofficial "whisper numbers", and the rapid mechanical unwinding of options hedges (volatility crush) frequently forces asset prices downward. Ultimately, investors should remember that markets do not trade on the reality of today; they trade on the shifting probabilities of tomorrow, constantly seeking equilibrium between algorithmic speed and human expectation.