Why Is OpenAI Losing Billions Despite Having So Many Users

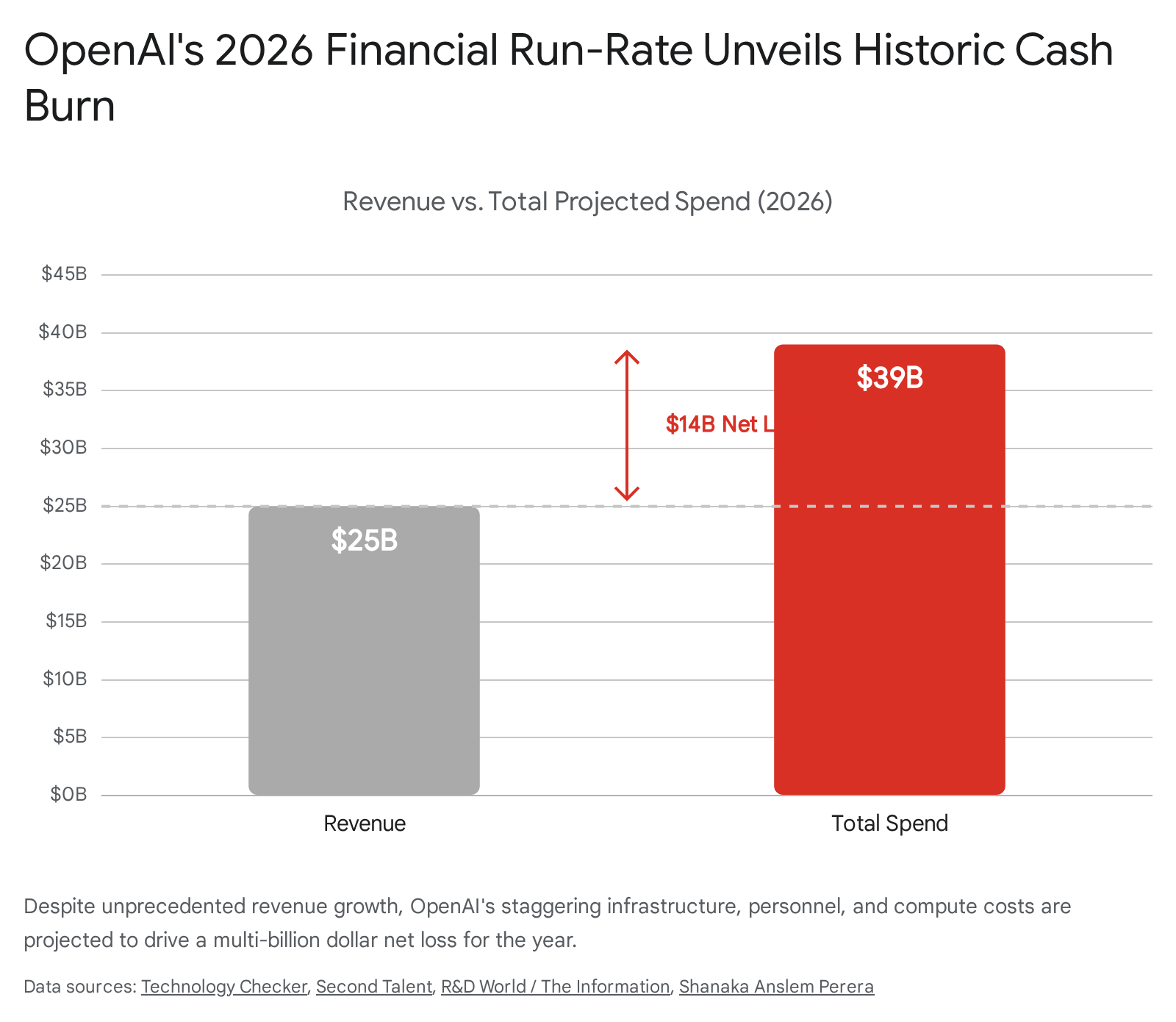

OpenAI projects a staggering $14 billion net loss for 2026 because the underlying economics of generative artificial intelligence fundamentally break the highly profitable business model of traditional software. While classic digital platforms can serve an additional user for practically zero marginal cost, every single query processed for OpenAI's 900 million weekly active users requires relentless, expensive computing power and massive physical infrastructure. As the company scales its user base, the compounding costs of model training, cloud inference, and severe hardware supply shortages are dramatically outpacing its rapidly growing $25 billion annualized revenue.

The Core Problem: The Broken Economics of Intelligence

For the past three decades, the technology industry has been built on a single, highly lucrative economic premise: the zero marginal cost of digital goods. Once a traditional software-as-a-service (SaaS) company spends the upfront capital to develop a product, duplicating and distributing that software to millions of users costs virtually nothing 12. Scale becomes the ultimate driver of profit. As user numbers grow, fixed costs are seamlessly amortized, and margins expand into the 80% to 90% range, heavily rewarding rapid, viral consumer adoption 23.

Artificial intelligence obliterates this established economic advantage. Generative AI models do not sit passively on a server waiting to be downloaded. They are active computing engines that must "infer" or calculate every single response in real-time, token by token 124. This continuous process, known as inference, requires immense ongoing processing power, electricity, and hardware utilization. Consequently, AI applications face relentless direct variable costs for every user interaction that never decrease with scale 2.

This dynamic creates a structural margin inversion that is currently causing deep anxiety across enterprise boardrooms. While a casual consumer asking a simple trivia question might cost OpenAI fractions of a cent, a power user deeply engaged in multi-turn conversations, massive document analysis, or agentic coding workflows can cost orders of magnitude more to serve 2. With over 900 million weekly active users - the vast majority of whom are utilizing the free tier - growth directly increases OpenAI's largest expense category 567. The classic venture capital playbook of "grow now, monetize later" is incredibly dangerous in the AI sector; the faster an AI company grows an unmonetized or heavily subsidized user base, the faster it accelerates its cash burn 2.

Furthermore, as models advance, their cost structures change unpredictably. Scaling laws for AI models demonstrate that increasing compute creates diminishing returns on capability while exponentially increasing costs. A next-generation reasoning model may cost ten times more to train and operate than its predecessor, yet only deliver marginal improvements in user-facing utility 2. For enterprise buyers evaluating these tools against traditional human labor, the mathematics are tightening. Industry analysts note that companies are now frequently investing more in the computing power required for AI workloads than in the human personnel running them, a historic shift in IT budget allocation 89.

OpenAI's Historic Revenue Velocity

To understand the sheer scale of OpenAI's financial situation, one must juxtapose the unprecedented velocity of its revenue growth against its astronomical spending. The company has evolved from a non-profit research laboratory into the fastest-growing enterprise revenue engine in the history of the technology sector.

By early 2026, OpenAI's revenue trajectory had broken every historical precedent. The company reached an annualized revenue run-rate of over $25 billion, generating approximately $2 billion per month 56710. This represents a stunning 12.5x expansion in just three years, climbing from a $2 billion run-rate in 2023, to $6 billion in 2024, to $20 billion by the end of 2025, and pushing toward an internal target of $29.4 billion by the end of 2026 5101112.

This revenue is sustained by an enormous user ecosystem. ChatGPT boasts 900 million weekly active users, 193 million daily active users, and processes over 2.5 billion prompts per day 6. Approximately 1 in 8 people on Earth interact with the platform weekly 10. To monetize this massive footprint, OpenAI has developed a highly stratified, complex pricing structure spanning consumer subscriptions, enterprise contracts, and developer APIs.

The Subscription and Enterprise Revenue Mix

The $25 billion revenue base is heavily diversified, shifting rapidly away from pure consumer subscriptions toward enterprise lock-in. As of early 2026, the revenue mix is roughly divided into three core pillars: 24% from ChatGPT Plus consumer subscriptions, 50% from Team and Enterprise business deployments, and roughly 26% from developer API usage 6.

The consumer side of the business is anchored by the ChatGPT Plus tier. At $20 per month, this tier generates an estimated $2.4 billion in annual recurring revenue (ARR) from roughly 10 million paying subscribers 6. To capture extreme power users and professionals who consistently hit messaging caps, OpenAI introduced specialized higher-tier plans. The $100-per-month Pro tier and the $200-per-month Pro tier unlock advanced capabilities, massive 1-million-token context windows, exclusive reasoning models (like o1 Pro mode), and extensive deep research tools 131415. Despite its high price point, the $200 ChatGPT Pro tier quickly captured nearly 5.8% of consumer B2C sales 11.

However, the enterprise sector is the true growth engine. With 92% of Fortune 500 companies using the platform, over 7 million enterprise workplace seats deployed, and 9 million paying business users, B2B contracts form the backbone of OpenAI's monetization strategy 67. These Enterprise and Team tiers, priced between $20 and $30 per user per month, provide crucial data compliance, single sign-on (SSO), and shared workspaces 1314. The company reports that enterprise revenue is on track to reach absolute parity with consumer revenue by late 2026 710.

| Pricing Tier | Cost (2026) | Target Audience | Key Feature Limits |

|---|---|---|---|

| Free | $0/month | Casual / Occasional | ~10 messages per 5 hours (GPT-5.3 Instant), US Ads |

| Go | $8/month | Light Daily Use | Unlimited GPT-5.3, US Ads, Image Generation |

| Plus | $20/month | Professionals | GPT-5.5 access, 160 messages/3 hrs, 32K context |

| Pro $100 | $100/month | Heavy Developers | 5x Plus limits, o1 Pro mode, 50 Deep Research/mo |

| Pro $200 | $200/month | Power Researchers | 20x Plus limits, 1M context, 250 Deep Research/mo |

| Business / Team | ~$25/user/month | SMBs / Workgroups | Pooled team quotas, SSO, no internal data training |

| Enterprise | Custom Pricing | Large Organizations | Negotiable SLA, custom limits, SCIM provisioning |

Table 1: OpenAI's fragmented 2026 ChatGPT subscription tiers, reflecting a transition from simple consumer pricing to aggressive usage-based segmentation 13141516.

The Financial Abyss: Deconstructing the $14 Billion Loss

Despite taking in roughly $25 billion a year, OpenAI is profoundly unprofitable. Its cash consumption is among the fastest of any startup or public enterprise in global financial history. Internal financial documents analyzed by major publications in early 2026 revealed projections of a staggering $14 billion net loss for the year 17181920. This represents a near tripling of the operational losses experienced in 2025.

To put this cash burn into perspective, historical analogues pale in comparison. Amazon accumulated roughly $3 billion in cumulative net losses over a six-year period before turning its first annual profit in 2003 1721. Tesla burned through approximately $10 billion over 17 years before stabilizing its cash flow in 2020 17. WeWork, infamous for its spectacular collapse, lost roughly $20.7 billion through its bankruptcy 17. Uber, long considered the poster child for subsidized consumer growth, burned through $31.7 billion over a decade before reaching profitability in 2023 17.

OpenAI, however, is operating on an entirely different scale. The company projects cumulative net losses of $115 billion through 2029, with some models forecasting cumulative negative free cash flow extending to $143 billion if capital expenditures remain elevated 172223. Independent financial analysts calculate that when factoring in aggressive capital expenditures and the substantial revenue sharing owed to infrastructure partners like Microsoft, OpenAI is hemorrhaging approximately $11.5 billion per quarter. In essence, the company spends an estimated $3.30 for every single dollar it earns 23.

| Company | Time Period to Profitability | Cumulative Cash Burn / Net Losses | Core Business Model Driver |

|---|---|---|---|

| Amazon | 1997 - 2003 (6 Years) | ~$3 Billion | E-commerce / Retail Infrastructure |

| Tesla | 2003 - 2020 (17 Years) | ~$10 Billion | Automotive Manufacturing R&D |

| WeWork | Pre-Bankruptcy | ~$20.7 Billion | Commercial Real Estate Arbitrage |

| Uber | Through 2023 | ~$31.7 Billion | Two-Sided Marketplace Subsidy |

| OpenAI | 2023 - 2029 (Projected) | $115 Billion+ | AI Compute & Datacenter Infrastructure |

Table 2: Comparing startup cash consumption at scale. OpenAI's projected cumulative losses dwarf the most capital-intensive startups in modern history 17212223.

This deficit calculation also obscures another massive expense: employee retention. To keep elite artificial intelligence researchers from defecting to rivals like Google, Meta, or Anthropic, OpenAI relies heavily on equity compensation. The company projected $6 billion in stock-based compensation for 2025, and recorded $1.5 billion in equity compensation in the first half of 2024 alone - a figure nearly equivalent to its cash revenue for that period 171819. Because this does not strictly hit the cash flow statement immediately, it obscures the true cost of operating the business.

Yet, the private equity and venture capital markets continue to fund this deficit without hesitation. In March 2026, OpenAI closed a $122 billion funding round led by major institutional and sovereign wealth investors, reaching an unprecedented post-money valuation of $852 billion 6724. Investors are effectively betting that OpenAI can survive the multi-year "AI J-curve," enduring deep initial losses to establish an insurmountable, monopolistic position in artificial general intelligence (AGI) 3.

Where exactly is $39 billion in annual spending going?

The deficit is driven by three interconnected black holes: the relentless toll of cloud inference, spiraling compute and model training budgets, and an increasingly hostile global hardware supply chain.

Black Hole 1: The Inference Cost of 2.5 Billion Prompts

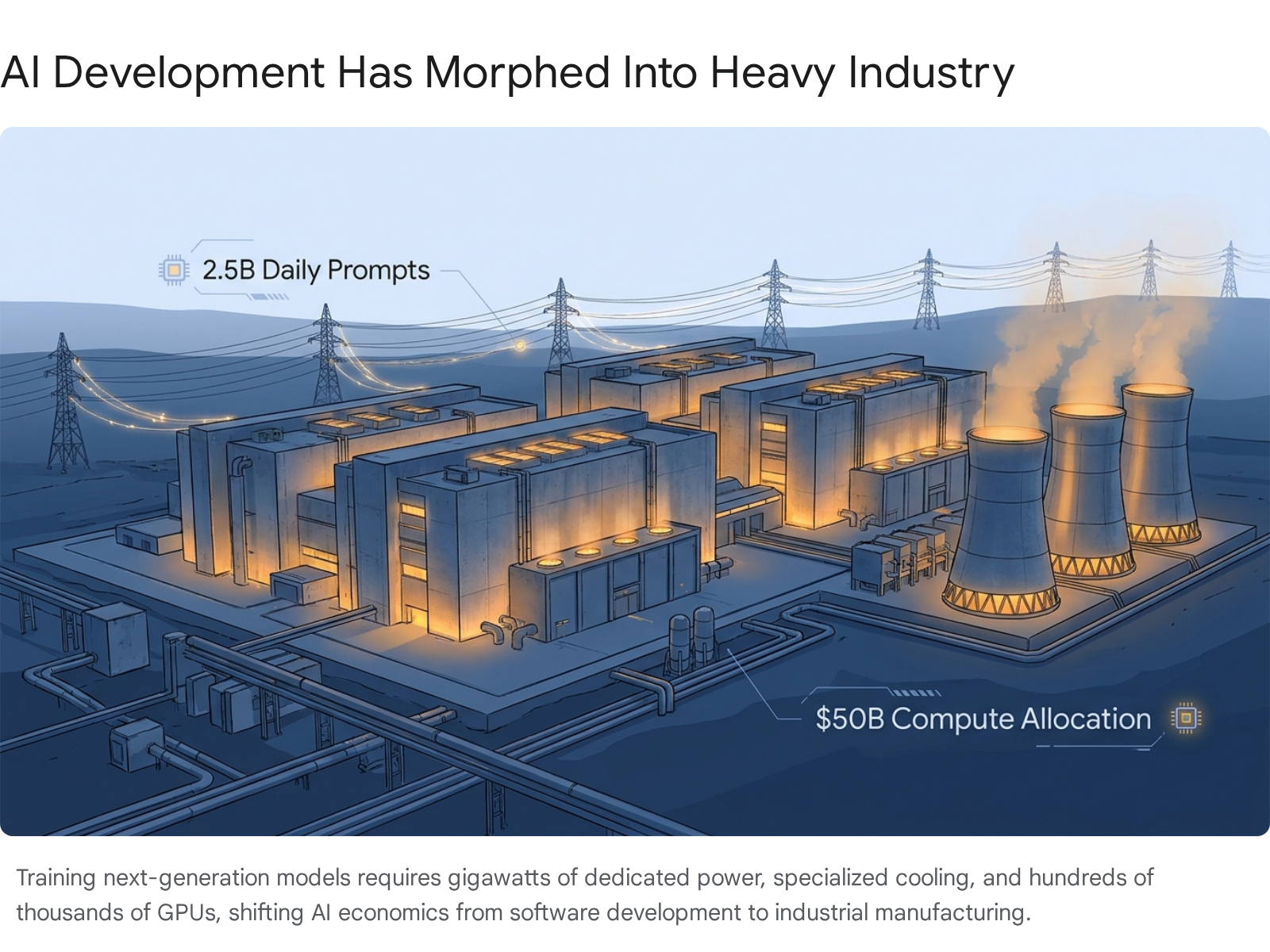

If software is eating the world, AI inference is eating the power grid. Every time a user inputs a prompt into ChatGPT, the model must mathematically process the text, retrieve context across vast neural parameters, and generate a response token by token. OpenAI confirmed that users now send roughly 2.5 billion prompts per day to the platform 25.

This scale of inference carries severe financial and environmental costs. Research indicates that a single standard ChatGPT prompt consumes an estimated 0.0029 kilowatt-hours (kWh) of electricity, which is roughly the amount of energy needed to run a standard LED lightbulb for two continuous minutes 2526. Visual and multimodal generation tools are even more intensive; generating an image via DALL-E consumes roughly 0.005 kWh per prompt 26.

While a fraction of a watt-hour seems insignificant on an individual basis, the math becomes staggering at planetary scale. Scaling 0.0029 kWh across 2.5 billion daily prompts equals roughly 7.25 million kilowatt-hours consumed every single day just to process user queries. This is equivalent to the daily electricity consumption of hundreds of thousands of residential households 25. In regions with high electricity rates, such as Hawaii, one dollar of commercial electricity buys only about 800 ChatGPT prompts, compared to nearly 3,000 in energy-abundant states like Louisiana 26.

At the data center level, this electricity, combined with the massive water requirements for server cooling and physical infrastructure maintenance, forms an inescapable baseline operating cost. OpenAI must lease this cloud inference capacity primarily from Microsoft Azure. Even with preferential pricing, the sheer volume of 900 million weekly active users - again, mostly on free tiers - acts as a continuous, massive cash drain. Analysts estimate OpenAI's daily inference and operational costs hover around $17 million, or $47 million a day when fully accounting for total platform delivery 1227.

The Threat of "Tokenmaxxing"

The financial strain is exacerbated by enterprise behavior. In traditional SaaS models, a corporate client pays a flat monthly fee for an application regardless of how much an employee clicks around the interface. With AI, usage is metered by "tokens" (fragments of words). As corporate employees integrate AI into complex, automated workflows - such as analyzing massive Excel datasets, debugging thousands of lines of code, or deploying autonomous agents - they consume millions of tokens per hour.

This has led to a phenomenon colloquially known in the industry as "tokenmaxxing." Corporate clients are utilizing AI so heavily that they are exhausting their annual budgets in a matter of months. Uber's Chief Technology Officer reported that the company's entire 2026 AI token budget was entirely consumed by April 8272829. Similarly, Swan AI exhausted its corporate tooling budget in just two months 8.

For OpenAI, this is a double-edged sword. While it indicates massive product-market fit, it means their enterprise clients are highly sensitive to price and volume. If clients hit their budgets too quickly, they will demand volume discounts or switch to smaller, cheaper open-source models for routine tasks, aggressively compressing OpenAI's already razor-thin gross margins on inference 27.

Black Hole 2: The $50 Billion Training Expenditure

If inference is the variable cost of operating the AI, training is the fixed capital expenditure of building it. In 2024, training a frontier model like GPT-4 was estimated to cost roughly $78 million to $100 million in direct cloud compute expenses 30313233. However, the AI industry operates on strict scaling laws: capabilities reliably increase with the infusion of more compute, more data, and more parameters.

Consequently, the cost of training next-generation models has skyrocketed. A single six-month training run for a frontier model (such as the iteration leading up to GPT-5 or internal projects codenamed "Orion") can now consume upwards of $500 million in computing costs alone 32.

In a federal court testimony in early 2026, OpenAI President Greg Brockman formally disclosed that the company plans to spend an astonishing $50 billion on computing power in 2026 343536. This figure transcends standard capital expenditure; it is a global demand signal that reshapes the entire tech landscape. It transitions the AI race from a battle of algorithmic cleverness to a war of brute-force industrial capital allocation 34.

Model training is also an inherently risky and volatile process. If a training run fails to produce the desired emergent capabilities, or if the model hallucinates uncontrollably - which reportedly occurred in early trials of newer models - the entire compute investment is effectively incinerated 32. Industry insiders frequently compare large-scale training runs to aerospace engineering: a failed run is financially equivalent to a rocket exploding shortly after launch 32.

To secure the physical resources required to maintain dominance over the next decade, OpenAI and its CEO Sam Altman have made unprecedented infrastructure commitments. The company has secured over $600 billion in long-term compute and data center capacity through partnerships with Microsoft, Oracle, CoreWeave, and Cerebras, ensuring access to gigawatts of power spanning into the 2030s 3637. This includes projects like the rumored $100 billion "Stargate" data center initiative 17.

Black Hole 3: The Hostile Hardware Supply Chain

OpenAI does not exist in a vacuum; it is a captive buyer entirely dependent on a highly constrained global hardware supply chain. At the very foundation of this chain is Taiwan Semiconductor Manufacturing Company (TSMC), which singlehandedly controls over 90% of the world's advanced chip manufacturing, including the silicon used by Nvidia, AMD, and Apple 38140.

By mid-2026, the artificial intelligence boom resulted in a systemic, multi-year supply chain crisis. TSMC's fabrication plants were running at absolute maximum capacity. The primary bottleneck was not just printing the silicon logic, but the highly complex Chip-on-Wafer-on-Substrate (CoWoS) advanced packaging required to assemble AI accelerators 41. Because demand far outstripped TSMC's ability to build new packaging facilities, the foundry flexed its pricing power. TSMC initiated a 15% price increase on 3nm wafers in the second half of 2026, with further compounded price hikes mapped out continuously through 2029 3812.

This foundry price hike at the base of the supply chain ripples upward, directly inflating the cost of Nvidia's hardware. Leading data-center GPUs remain exorbitantly expensive. The Nvidia H100 continues to command prices in the $25,000 to $40,000 range per chip on the open market, while fully equipped DGX server systems housing the newer H200 architectures cost nearly half a million dollars each 4344. The rollout of the next-generation B200 (Blackwell) architecture pushed prices even higher, with individual chips exceeding $40,000 41.

The Memory Squeeze and Consumer Spillover

The cost crisis extends beyond the processor itself into the memory chips necessary to run large models. Global shortages of High-Bandwidth Memory (HBM3e) and GDDR7 memory caused prices to surge between 40% and 60% in late 2025 and 2026 4445.

The demand from hyperscalers like OpenAI is so ravenous that it has actively cannibalized the broader consumer electronics market. Because Nvidia prioritizes high-margin datacenter chips (where an H100 can sell for $30,000) over lower-margin gaming chips (which sell for $1,000), consumer GPU production was slashed by 30% to 40% 45. This resulted in dramatic "demand spillover," where desperate AI startups unable to secure data center allocation began buying up high-end consumer cards, causing the secondary market price of the consumer RTX 5090 GPU to nearly double to $3,700 4145.

The macroeconomic result is that AI infrastructure has become a genuine driver of technological inflation 146. For OpenAI, this means the fundamental building blocks of its business are getting systematically more expensive precisely when it needs to buy millions of them.

The Anthropic Threat: A Tale of Two Margins

OpenAI's strategy of massive cash burn might be mathematically viable if it were an unchallenged monopoly. However, 2026 marked a devastating shift in the competitive landscape. Anthropic, a rival AI lab founded by former OpenAI researchers, quietly surpassed OpenAI in annualized revenue run-rate, hitting $30 billion by April 2026 122148.

Anthropic achieved this milestone by playing an entirely different economic game. While OpenAI boasts 900 million weekly active users, roughly 85% to 95% of its traffic comes from consumers, the vast majority of whom pay nothing 212249. OpenAI is heavily burdened by the monumental inference costs of answering billions of casual queries.

Anthropic, conversely, largely eschewed the viral consumer market to focus almost exclusively on business-to-business (B2B) enterprise adoption. Approximately 80% to 85% of Anthropic's revenue is derived from enterprise and developer customers, with more than 1,000 organizations paying over $1 million annually, and eight of the Fortune 10 actively running its Claude models in production 2122483.

Because enterprise clients use structured API calls, require lower latency, and pay heavy premiums for reliability, security, and massive context windows, Anthropic's unit economics are vastly superior. By mid-2026, Anthropic was operating with gross margins of roughly 40% to 44%, with a projected trajectory toward 77% gross margins by 2028 21483. The company projects reaching positive cash flow by 2027 - two to three years ahead of OpenAI 2249.

| Metric (Mid-2026) | OpenAI | Anthropic |

|---|---|---|

| Annualized Revenue Run-Rate | ~$25 Billion | ~$30 Billion |

| Projected 2026 Cash Burn | $14 Billion Loss | ~$5.2 Billion Loss |

| Revenue Mix | ~85% Consumer / 15% Enterprise | ~15% Consumer / 85% Enterprise |

| Gross Margin Profile | Highly Compressed / Subsidized | 40% - 44% (Targeting 77% by 2028) |

| Target Profitability Date | ~2029 - 2030 | ~2027 |

| Developer API Pricing (per 1M tokens) | GPT-5.5: $5 Input / $30 Output | Claude equivalents tightly matched |

| Valuation Estimates | $852 Billion | $380B - $965B (Pre-IPO targets) |

Table 3: The growing economic divide between the consumer-scale model of OpenAI and the enterprise-focused model of Anthropic 12214849351.

In the enterprise programming tool segment, Anthropic's flagship product, Claude Code, captured a commanding 54% market share, generating over $2.5 billion in annual revenue and surpassing incumbent tools like GitHub Copilot 1248. This B2B dominance is critical because enterprise software has historically commanded the highest valuation multiples on Wall Street. PitchBook's AI business quality framework scored Anthropic an 8.2 out of 10.0, significantly outperforming OpenAI's 4.8, highlighting a massive gap in underlying business sustainability 3.

Desperate Measures: The API Price War

In response to Anthropic's enterprise dominance, OpenAI has been forced into a highly precarious strategic position. Despite projecting a $14 billion operational loss, reports in mid-2026 indicated that OpenAI was evaluating major reductions in its API token pricing to win back developers and stem the market share bleed to Anthropic 295253.

This pricing battle is fought at the micro-transaction level of the API. For developers integrating AI into their applications, cost is paramount. OpenAI's flagship GPT-5.5 model, launched in April 2026, charges $5.00 per million input tokens and $30.00 per million output tokens 15163054. For less intensive tasks, developers can route queries to GPT-5.4 Mini at a much cheaper $0.75 input and $4.50 output rate, or utilize the Batch API for a 50% discount on delayed asynchronous processing 151654.

| Model Tier | Input Price (per 1M tokens) | Output Price (per 1M tokens) | Optimal Use Case |

|---|---|---|---|

| GPT-5.5 Pro | $30.00 | $180.00 | Maximum reasoning, complex autonomous agents |

| GPT-5.5 | $5.00 | $30.00 | High-level coding, professional workflows |

| GPT-5.4 Standard | $2.50 | $15.00 | Balanced capability and daily application cost |

| GPT-5.4 Mini | $0.75 | $4.50 | Routine web scraping, simple chatbot routing |

| GPT-5.4 Nano | $0.20 | $1.25 | Massive volume, low-complexity programmatic tasks |

Table 4: OpenAI's 2026 API token pricing structure, illustrating the severe cost variance based on reasoning requirements 151654.

If OpenAI slashes these API prices to undercut Anthropic, it is executing a dangerous volume play. The strategic hope is that cheaper tokens will drive such immense developer adoption that sheer scale compensates for thinner margins. However, as noted by industry analysts, deliberately slashing prices while already projecting a $14 billion loss - and while hardware costs from TSMC and Nvidia are rising - is a high-wire act that could drastically accelerate the company's cash burn 5253.

Concurrently, to offset these losses and increase the average revenue per user (ARPU) on the consumer side, internal financial documents reviewed by major media outlets suggest OpenAI is exploring gradual, multi-year price hikes to the standard ChatGPT Plus subscription. Current projections indicate intentions to push the baseline consumer cost from $20 up to $22 in the near term, with targets reaching $44 per month within five years 2955. This risks alienating the casual consumer base that currently defines OpenAI's cultural dominance.

Bottom line

OpenAI is losing $14 billion a year because it is operating an industrial-scale computing utility masquerading as a high-margin consumer software app. The relentless variable costs of processing 2.5 billion daily queries, combined with a $50 billion mandate for training compute and a heavily constrained hardware market, have created an economic reality where massive consumer scale actively accelerates cash burn. Whether OpenAI can flip its margins and achieve profitability by 2030 depends entirely on its ability to command premium enterprise pricing against rivals like Anthropic, while simultaneously out-engineering the staggering physical costs of intelligence.