How Anthropic Makes Money and Whether It Is Profitable

Anthropic recently reported its first-ever operating profit of $559 million for the second quarter of 2026, driven by a surge in enterprise revenue that propelled its annualized run-rate past $47 billion. However, this "profitability" milestone controversially excludes the massive, multi-billion-dollar capital expenditures required to train its frontier AI models. While the company generates staggering revenue from its enterprise API and developer subscriptions, its true free cash flow remains deeply negative as it funds the most expensive computing infrastructure in history ahead of a highly anticipated initial public offering.

The Unprecedented Ascent of Anthropic

To understand Anthropic's financial trajectory, one must first contextualize the sheer speed of its revenue growth, which currently represents one of the most extreme expansion curves ever recorded in the software industry. Founded by former OpenAI researchers Dario and Daniela Amodei, the company was essentially pre-revenue at the start of the decade but has since outpaced the growth metrics of virtually every legacy technology giant 12.

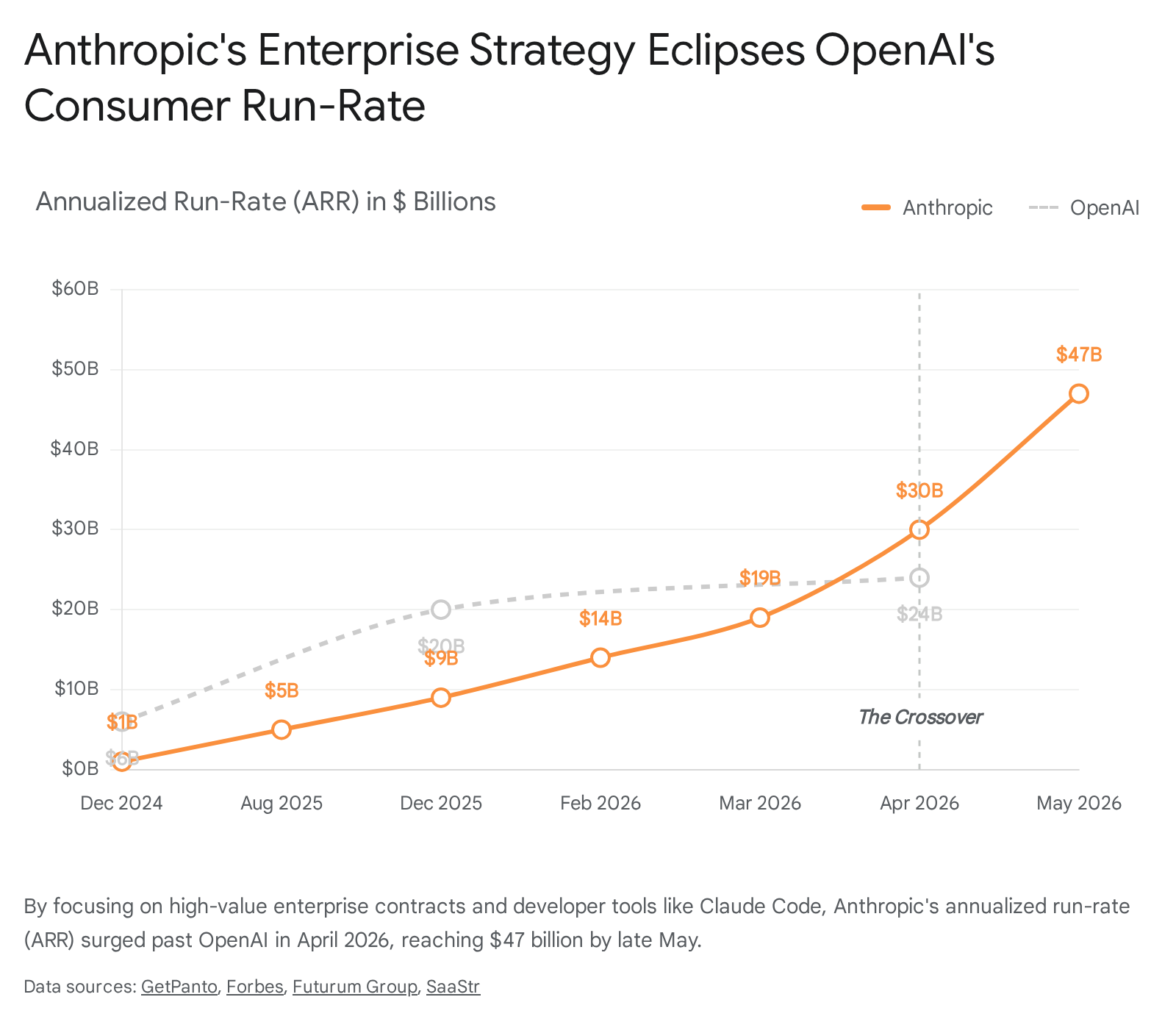

The historical data demonstrates a breathtaking escalation in annualized recurring revenue (ARR). The company reportedly generated around $10 million in 2022, which grew to $100 million in 2023 3. By the end of 2024, Anthropic exited the year at roughly $1 billion in ARR 344. What followed was a period of hyper-growth that stunned private market investors: the company exited 2025 at $9 billion, hit $13 billion in January 2026, reached $19 billion in March, and crossed the $30 billion threshold by April 2026 236.

By late May 2026, following the wildly successful rollout of its autonomous coding tools, CEO Dario Amodei publicly cited 80x year-over-year revenue growth, pushing the company's annualized run-rate past $47 billion 56710. To place this in perspective, enterprise software giant Salesforce required approximately two decades to reach $30 billion in annual revenue; Anthropic achieved the same milestone from a standing start in under three years 7. The company is now projected to reach up to $70 billion in sales by 2028, instantly placing it among the highest-earning software entities on the planet 411.

How Does Anthropic Actually Make Money?

Unlike the consumer-first approach popularized by OpenAI's viral ChatGPT application, Anthropic has architected a business model fundamentally geared toward enterprise clients, developers, and autonomous software engineering. Approximately 80% to 85% of Anthropic's revenue is derived directly from business-to-business (B2B) enterprise clients 4678.

The enterprise focus has proven economically superior in the AI sector. Over 1,000 businesses currently spend more than $1 million annually on the Claude platform, including eight of the Fortune 10 companies 678. Public references confirm massive production deployments at corporations like Netflix, Spotify, KPMG, and L'Oréal 3. Anthropic monetizes this demand through three primary channels: enterprise API consumption, corporate team deployments, and high-tier individual developer subscriptions.

The Enterprise API Ecosystem

The backbone of Anthropic's revenue is its Application Programming Interface (API), which allows businesses to integrate Claude directly into their proprietary software, customer service platforms, and internal data analysis tools. Companies pay for API access based on the volume of data processed, measured in "tokens" (fragments of words or code).

This usage-based model scales effortlessly with corporate adoption. Anthropic offers a tiered model lineup to balance cost and capability 1139: * Claude Opus (e.g., Opus 4.8): The flagship model for highly complex reasoning, mathematics, and advanced coding. A massive pricing overhaul in early 2026 cut Opus token costs by 67%, bringing the price down from $15 per million input tokens to $5 per million, and output tokens from $75 to $25 15. * Claude Sonnet (e.g., Sonnet 4.6): The primary workhorse model, balancing speed and intelligence, priced at $3 per million input tokens and $15 per million output tokens 1. * Claude Haiku (e.g., Haiku 4.5): The fastest and cheapest model for lightweight tasks like topic detection, costing just $1 per million input tokens and $5 per million output tokens 1.

To lock in enterprise customers and incentivize massive scale, Anthropic introduced features that dramatically alter the cost-benefit analysis for corporate buyers. The "Batch API" offers a flat 50% discount for asynchronous workloads processed within a 24-hour window, encouraging companies to run massive overnight data analysis jobs 116. More importantly, "Prompt Caching" allows companies to store frequently used context (such as large codebases, system instructions, or corporate rulebooks) and retrieve it at a 90% discount compared to standard input rates 116. While these features lower the unit cost for the buyer, they dramatically increase the total volume of tokens processed, driving up overall contract values and deepening vendor lock-in.

The "Claude Code" Phenomenon

While the API handles backend enterprise integration, Anthropic captures the frontend developer market through a specialized autonomous programming tool called Claude Code. Launched in mid-2025, Claude Code became a breakout monetization engine and the fastest-growing product in the company's history 56.

Claude Code is an agentic tool that operates directly within a software engineer's terminal and development environment (like VSCode). It is capable of reading entire codebases, autonomously writing new features, and debugging complex errors 410. Within six months of its launch, the product's ARR topped $1 billion, and by February 2026, it had quintupled to $2.5 billion in run-rate revenue 4656.

The success of Claude Code fundamentally altered market share dynamics in the AI sector. By the end of 2025, Anthropic's share of the enterprise AI coding segment grew to 54%, more than doubling OpenAI's 21% share in that specific vertical 45. The nature of autonomous coding - where AI agents continuously read, write, and debug code in iterative loops - burns through context tokens at an incredible rate, making it a highly lucrative revenue stream for Anthropic.

Subscription Tiers and Pricing Psychology

To monetize individual professionals and corporate teams who do not want to manage raw API costs, Anthropic implemented a strict, multi-tiered subscription model. This structure is heavily designed to push professional developers into higher-priced brackets by utilizing strict usage limits 1311.

| Subscription Tier | Monthly Cost | Target Audience | Usage Limits & Key Features |

|---|---|---|---|

| Free | $0 | Casual consumers | Basic web chat. Excludes Claude Code and Opus access. |

| Claude Pro | $20 | Solo developers | Limited to ~44,000 tokens per 5-hour window. Good for light usage. |

| Claude Max 5x | $100 | Daily professionals | 5x Pro usage. Priority access; designed for 2-3 hours of daily coding. |

| Claude Max 20x | $200 | Heavy enterprise users | 20x Pro usage. Built for full-time developers using Claude as a primary IDE. |

| Team Standard | $25 / seat | Small businesses | Shared workspaces and admin controls (drops to $20/seat if billed annually). |

| Team Premium | $125 / seat | Engineering teams | Full Claude Code access, Opus models, high usage limits, SSO. |

The introduction of the $100 and $200 "Max" tiers in 2026 proved to be a masterstroke in behavioral economics 131912. Developers quickly found that the standard $20 Pro plan's 5-hour rolling token limit was entirely insufficient for continuous agentic coding. Hitting a usage wall mid-session forced developers to either stop working or switch to the raw API. However, heavy API users discovered that full-time agentic coding could easily rack up variable bills of $800 to $1,500 a month 1112.

Faced with this volatile expense, developers and their employers flocked to the $200 Max 20x plan. For the developer, it effectively capped their monthly costs while providing enough headroom to work uninterrupted all day; for Anthropic, it locked in highly predictable, high-margin recurring revenue at ten times the price of a standard SaaS subscription 111912.

Anthropic vs. OpenAI: The Enterprise Divergence

The defining business story of 2026 has been the financial decoupling of the world's two most valuable private AI labs. While both Anthropic and OpenAI build frontier large language models, their go-to-market strategies and monetization philosophies have diverged completely.

OpenAI is largely structured as a consumer-first software company. Approximately 85% of OpenAI's revenue is tied to ChatGPT consumer subscriptions 8. While OpenAI boasts over 900 million weekly active users, roughly 95% of those users utilize the free tier 821. This creates a massive computational burden; OpenAI effectively subsidizes inference (the cost of generating answers) for hundreds of millions of non-paying users in a bid for ubiquitous consumer distribution and brand dominance 813.

Anthropic, conversely, operates as an enterprise infrastructure company. Because 85% of its revenue originates from B2B customers, the company rarely pays for "free" usage at scale 4813. Furthermore, enterprise queries are generally more deterministic, easier to cache, and yield three to five times more revenue per token than unpredictable consumer queries 8.

This structural difference manifested violently in the companies' 2026 financials. In April 2026, Anthropic's ARR crossed the $30 billion mark, officially surpassing OpenAI's reported $24 billion run-rate for the first time 2823.

The gap was closed through enterprise dominance rather than consumer virality. Anthropic captured 40% of all enterprise LLM spending (up from 24% in 2024), while OpenAI's share of that specific pie shrank from 50% in 2023 to 27% in 2024 45. According to Ramp's AI Index, which tracks verified U.S. business spending, Claude accounted for 34.4% of business AI adoption versus ChatGPT's 32.3% by mid-2026 1014.

Comparing the Pre-IPO Financial Profiles

The contrast between the two firms becomes starkest when viewing their leaked pre-IPO internal projections. While Anthropic has built a highly efficient monetization engine, OpenAI remains locked in a high-burn battle for generalized artificial general intelligence (AGI).

| Metric | Anthropic (2026 estimates) | OpenAI (2026 estimates) |

|---|---|---|

| Annualized Run-Rate (mid-2026) | ~$47 Billion 256 | ~$24 Billion 2 |

| Client Revenue Mix | ~85% Enterprise / B2B 48 | ~85% Consumer / B2C 8 |

| Projected 2026 Operating Loss | Claiming Q2 Op. Profit ($559M) 2315 | ~$14 Billion Loss 48 |

| Target Free Cash Flow Breakeven | 2027-2028 46 | 2029-2030 8 |

| Estimated 2028 Compute Training Spend | ~$30 Billion 21326 | ~$121 Billion 2813 |

The most glaring discrepancy lies in future training costs. OpenAI's leaked projections indicate an intent to spend an unfathomable $121 billion on compute in 2028 alone, resulting in a projected operating loss of $74 billion that year despite expected revenue growth 2827. OpenAI is on course to accumulate hundreds of billions in losses before reaching positive cash flow near 2030 8. Anthropic's estimated training spend peaks much lower, near $30 billion in the same period, providing a clearer, software-like path to positive free cash flow by 2027 or 2028 2413.

Is Anthropic Profitable? The "Community-Adjusted" Illusion

In May 2026, the financial press erupted with leaks from Anthropic's pre-IPO investor documents indicating the company was on track to report its first-ever quarterly operating profit. The projections claimed that in Q2 2026, Anthropic would generate $10.9 billion in revenue (up 130% from $4.8 billion in Q1) and post an operating profit of $559 million 68231528.

If taken at face value, this would make Anthropic the first frontier AI lab to break into the black, signaling to Wall Street that generative AI is a sustainable business model 15. However, a deeper analysis of AI accounting mechanics reveals that this "profitability" comes with a massive, multi-billion-dollar asterisk.

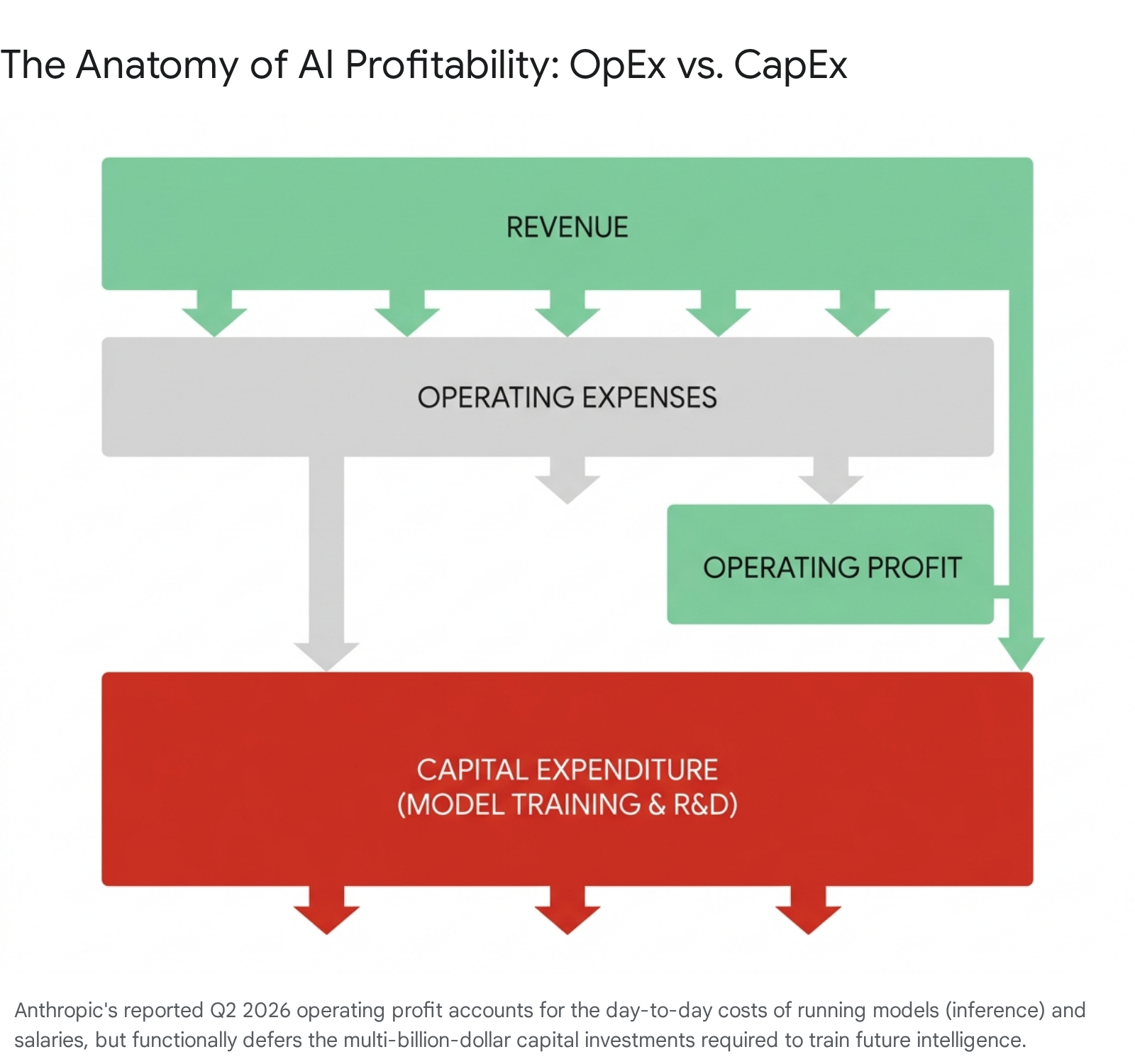

OpEx vs. CapEx: The Accounting Maneuver

The debate centers on how AI companies classify their expenses: specifically, the difference between inference (the operational cost to run the model for a user) and training (the capital cost to build the model in the first place).

Anthropic's claimed $559 million operating profit relies heavily on accounting methods that functionally exclude the multi-billion-dollar capital expenditures (CapEx) required for pre-training runs 1329. Critics, including technology analysts and financial journalists, have compared this accounting maneuver to WeWork's infamous "Community-Adjusted EBITDA," which removed essential real estate costs to create the illusion of a profitable core business 2930.

In an AI context, training a frontier model is astronomically expensive. Anthropic CEO Dario Amodei has publicly explained the underlying economics: a model trained in 2023 might cost $100 million, while the next-generation model in 2024 might cost $1 billion to train before it ever generates a single dollar of revenue 29. Because these massive pre-training runs are treated as amortizable long-term assets (CapEx) rather than immediate operational expenses (OpEx), they do not hit the quarterly operating profit margin directly 313233.

Therefore, Anthropic's Q2 2026 "operating profit" simply means that the revenue collected from customers finally exceeded the server costs of daily inference, employee salaries, and corporate overhead 3116. The reality below the line is entirely different. The company is actively drawing down billions in cash to purchase chips and secure energy contracts for its next-generation models. Anthropic itself warned investors that the Q2 profit was fragile and that subsequent quarters could easily dip back into the red as new data center investments come online 6.

The Crushing Reality of AI Unit Economics

While overall net profitability remains clouded by training CapEx, Anthropic's unit economics - represented by its gross margin - have undeniably improved, though they still lag behind traditional tech companies.

In 2024, Anthropic operated with a staggering negative 94% gross margin. This meant the company lost ninety-four cents in cloud compute costs for every single dollar of inference it sold to customers 41736. By 2025, that figure improved dramatically to approximately 40% 41737.

Though a massive absolute leap, 40% actually fell short of the company's internal 50% target 41737. The miss occurred because inference costs on Amazon Web Services (AWS) and Google Cloud proved 23% higher than management anticipated as enterprise usage scaled unexpectedly 4173738. This highlights the fundamental vulnerability of the AI business model: AI labs are small tenants in an infrastructure market they do not control and cannot entirely price against 27.

At 40% margins, an AI company operates with the financial profile of an infrastructure-heavy industrial business or a semiconductor foundry, not a high-margin software-as-a-service (SaaS) company, which typically enjoys 70% to 80% margins 4. To achieve its massive valuation targets, Anthropic promised investors it will close this gap. The company's internal projections guide toward gross margins of 50% to 63% by the end of 2026, scaling up to an aggressive 75% to 77% by 2028 34.

Achieving a 77% gross margin relies on three highly specific operational shifts becoming reality 34: 1. Algorithmic Efficiency: The models must become computationally cheaper to run by a factor of 3x to 4x each year. 2. Silicon Independence: Anthropic must successfully shift the bulk of its inference workloads away from premium, expensive Nvidia GPUs (like the H-class and B-class) toward cheaper custom silicon, specifically Google's Tensor Processing Units (TPUs) and Amazon's Trainium chips. 3. Economies of Scale: Revenue growth from enterprise clients must continually outpace the baseline infrastructure cost declines.

The Trillion-Dollar Compute Bill and the Energy Crisis

The overarching reality for Anthropic, OpenAI, and their peers is that they are capital-intensive intelligence factories converting electricity and compute into cognition 13. The structural tension in this model is that training costs scale super-linearly. Each new generational jump in AI capability does not cost marginally more; it costs an order of magnitude more 13.

The Grid Constraint

The sheer scale of this infrastructure is beginning to collide with the physical limits of global energy grids. AI data centers are uniquely power-hungry. A generative AI query requires exponentially more electricity than a traditional Google search; processing one million tokens emits carbon roughly equivalent to driving a gas-powered car five to 20 miles 18.

Globally, data center electricity demand was estimated at 415 Terawatt-hours (TWh) in 2024 and is projected to more than double to 945 TWh by 2030, driven almost entirely by AI workloads 40. To put this into perspective, a hypothetical 5-gigawatt (GW) continuous AI data center consumes more electricity in a year than the entire island of Manhattan (between 57% and 68% of Manhattan's total annual use) 41.

Anthropic is securing infrastructure at precisely this macroeconomic scale. In April 2026, the company signed landmark agreements with Google and Broadcom for multiple gigawatts of next-generation TPU capacity, expected to come online starting in 2027 3036. Broadcom's Anthropic-linked TPU capacity is projected to expand from 1 GW in 2026 to an astounding 3 GW by 2027, with the potential to reach 20 GW by 2028 under a massive $35 billion private credit financing deal backed by asset managers Apollo and Blackstone 3642. In this arrangement, the credit finances the purchase of Google TPUs from Broadcom, which Google then installs in data centers and rents back to Anthropic 42.

The necessity of managing volatile power demands has fundamentally altered how these data centers operate. Modern AI training is bulk-synchronous: thousands of chips perform computations in parallel, then pause briefly to exchange data 19. At hyperscale, these synchronized idle periods create sharp, rapid drops in power demand that can stress grid transformers and risk outages 19. To prevent this grid stress, data centers are forced to run secondary "filler" workloads simply to keep power consumption artificially stable during these micro-pauses 19. This practice inflates operational costs, accelerates hardware wear, and significantly drives up the ultimate cost of AI compute that Anthropic must bear 1920.

Global Expansion and Macroeconomic Ripples

To justify these immense infrastructure liabilities and sustain its $47 billion run-rate, Anthropic cannot rely solely on the North American market. The company views international expansion as a critical growth lever, projecting that the Asia-Pacific and European markets could contribute 30% to 40% of its total revenue by 2028 4.

In Europe, Anthropic recently expanded its footprint by opening a major operational office in Milan, Italy. This move initiated a hiring surge designed to capture regional enterprise contracts and navigate the deep complexities of the European Union's evolving AI regulatory frameworks 45. While this geographic diversification mitigates reliance on US corporate spending, the upfront costs of office setup, recruitment, and legal compliance will likely weigh on near-term European margins 45.

The impact of AI's financial explosion is profoundly visible in Asian markets, particularly in Japan. In early to mid-2026, Japan's Nikkei 225 stock index surged to record highs, frequently crossing the 66,000 to 68,000 yen marks 212248. This rally was driven largely by global AI optimism and the performance of Japanese semiconductor equipment manufacturers that are deeply integrated into the AI hardware supply chain 2148.

Financial institutions like BofA Securities explicitly linked the booming performance of Japanese firms - such as Tokyo Electron, Advantest, and Kioxia Holdings - to the rapid capital expenditures of Western AI leaders like Anthropic and OpenAI 2148. For instance, memory-chip maker Kioxia saw its market capitalization increase to 44 trillion yen, surpassing legacy giants like Toyota and symbolically shifting the leading sector of the Japanese stock market from automobiles to AI and semiconductors 21. Market analysts noted that the impending blockbuster IPOs of Anthropic and OpenAI were directly influencing supply and demand pressures within Japanese equities, as institutional investors repositioned capital to secure funds for the AI gold rush 21.

Recognizing that artificial intelligence is now a macroeconomic force rather than just a software tool, Anthropic has uniquely begun hiring teams of elite economists. A group of ten economists convened by the company - mirroring similar hires at Google DeepMind and OpenAI - are tasked with analyzing the structural changes AI brings to labor, wealth reallocation, and the global economy 14. The company understands that its technology is displacing jobs and shifting capital markets, treating these macroeconomic shifts as engineering-relevant constraints rather than just policy talking points 14.

The $965 Billion IPO and the AI Valuation Paradox

Anthropic's rapid revenue acceleration has triggered a frenzy in private capital markets, culminating in a highly anticipated transition to the public sphere.

In February 2026, Anthropic closed a $30 billion Series G funding round that valued the company at $380 billion 3611. The pace of investment was so aggressive that the deal was reportedly arranged in a matter of weeks, driven by venture capital firms pushing their way into the capitalization table 7. Just three months later, in late May 2026, the company secured an additional $65 billion Series H round - co-led by Sequoia Capital, Dragoneer Investment Group, Altimeter Capital, and Greenoaks Capital Partners - at a staggering pre-money valuation of $965 billion 567. This officially crowned Anthropic as the most valuable private AI company in the world 7.

Following this massive capital injection, on June 1, 2026, Anthropic confidentially filed its S-1 paperwork with the SEC, initiating the regulatory review window for an Initial Public Offering (IPO) that investment bankers expect could arrive as early as October 2026 636.

Why Traditional Valuations Break

A near-trillion-dollar valuation for a company barely four years old defies traditional financial logic. However, institutional investors have adapted to the "AI Valuation Paradox," prioritizing technological breakthroughs, intangible assets (like proprietary datasets and model architectures), and future market dominance over present-day cash flows 49.

Venture firm Coatue, in a leaked early 2026 presentation, modeled the long-term justification for these prices. Coatue estimated that by 2031, Anthropic would generate $200 billion in revenue and $48 billion in EBITDA profits 50. Applying a 41x forward EBITDA multiple, Coatue pitched investors that Anthropic could be worth $2.4 trillion by the early 2030s 50.

Yet, traditional financial analysts warn that applying software-as-a-service (SaaS) revenue multiples to AI companies is fundamentally flawed 5152. Standard SaaS companies enjoy predictable recurring revenue where the marginal cost of adding a new user approaches zero. AI companies, conversely, face compute costs that scale linearly - or even super-linearly - with every API call and user interaction 51.

As venture capitalist Bill Gurley and other critics have noted, revenue multiples are "crude and procyclical" 51. If Anthropic achieves $100 billion in revenue but requires $120 billion in compute to service it, a high revenue multiple is a dangerous illusion 5153. The true value of an AI startup lies in its capital efficiency: how much enterprise value it can generate per dollar of funding 54. The upcoming public S-1 filing will force a reckoning on these dynamics, specifically revealing whether Anthropic's "principal-versus-agent" revenue classification practices artificially inflate top-line figures relative to its net-reporting peers 6.

Systemic Risks: What Could Break the Model?

Despite the extraordinary momentum, Anthropic faces several critical headwinds that could disrupt its path to sustainable profitability:

- The Impending Price War: As OpenAI feels the pressure of losing enterprise market share to Anthropic, CEO Sam Altman has publicly acknowledged that AI costs are a "huge issue" for corporate clients . OpenAI is reportedly weighing drastic cuts to its token pricing in a direct attack on Anthropic's B2B dominance . Because enterprise clients face high switching costs, a brutal price war could severely erode Anthropic's hard-won gross margins just as it attempts to demonstrate public market profitability .

- Circular Financing and Cloud Dependency: Anthropic is highly dependent on Amazon and Google for the physical servers required to run its models. These companies are simultaneously Anthropic's primary investors, its infrastructure landlords, and builders of competing AI models (like Google's Gemini) 456. This complex circular entanglement will face intense SEC scrutiny regarding governance and conflict-of-interest disclosures during the IPO process 6.

- Safety Incidents and Regulatory Backlash: Anthropic's entire brand value and premium pricing are predicated on its "Constitutional AI" and safety-first methodology, which appeals deeply to risk-averse corporate clients like banks and healthcare providers 5. A single high-profile safety failure - such as autonomous agent misuse or a massive data privacy violation - would damage its brand asymmetrically compared to competitors 3. Additionally, the company faces ongoing legal disputes regarding military use policies that could jeopardize billions of dollars in government revenue 37.

Bottom line

Anthropic is not traditionally profitable, but its financial trajectory is unmatched in the history of enterprise software. By aggressively capturing the corporate and developer markets - particularly through its $2.5 billion autonomous coding segment - the company surged to an astonishing $47 billion annualized run-rate by mid-2026, officially overtaking OpenAI's revenue scale. While the company projects a $559 million operating profit in Q2 2026, this figure strategically relies on accounting methods that defer the tens of billions in capital expenditures required to train future intelligence. For prospective investors ahead of its anticipated $1 trillion IPO, the ultimate question is whether Anthropic can achieve true hardware independence and algorithmic efficiency fast enough to permanently break the crushing cost of AI compute.