Why August Is the Worst Month for Funding and How to Plan

While venture capital transactions certainly close during the summer, August remains a notoriously difficult time to initiate a new round of funding due to the vacation schedules of key decision-makers. The absence of even a single senior partner can break the strict quorum rules required for investment committees to issue term sheets. To avoid this bottleneck and maintain deal momentum, savvy founders reverse-engineer their fundraising timelines, choosing to either pitch aggressively in May or wait to launch their roadshows until September.

The Paradox of the Summer Slump

A pervasive piece of conventional wisdom in the startup ecosystem is that venture capital (VC) grinds to a complete halt during the summer. For first-time founders, the advice is almost uniformly to avoid sending pitch decks between the Fourth of July and Labor Day.

However, looking at global venture capital market data presents a paradox. According to equity management platforms and market intelligence firms, venture deals are signed consistently throughout the year, and summer months often approach or exceed baseline averages 1. In a perfectly even distribution, each month would account for roughly 8.3% of total annual deals; surprisingly, June and August consistently demonstrate strong deal activity that mirrors other busy periods, with July experiencing only a slight dip 1.

This trend has been corroborated by recent market data. In the third quarter of 2025, VC firms deployed a massive $80.9 billion across an estimated 4,208 deals 2. Similarly, in the second quarter of 2024, startups closed 1,287 new funding rounds totaling $20.9 billion, representing the highest amount of VC cash invested in a single quarter over the preceding year 3. If tens of billions of dollars are flowing and thousands of deals are closing in the late summer, why is August widely considered the absolute worst time to raise capital?

The answer lies in the fundamental difference between closing a deal and initiating one. Venture capital transactions operate on a prolonged enterprise sales cycle subject to a significant time lag. The deals that are announced, finalized, or wired in August are almost never the result of a pitch that happened in late July. A standard timeline illustrates a 90-day lag: an initial pitch in May leads to due diligence and partner meetings in June, term sheets and legal processing in July, and finally, a deal close and wire transfer in August 14.

The historical data demonstrates a consistent upward trend in summer closings, but these figures represent the tail-end of processes initiated months prior. Attempting to begin the fundraising cycle in August traps founders in a vacation dead-zone where initial meetings cannot be scheduled, and early momentum cannot be established. Therefore, the "August slump" does not describe a lack of capital being wired; it describes the near-impossibility of getting a new deal approved.

The Mechanics of Venture Capital Decision-Making

To understand why the August bottleneck is so lethal to a fundraising campaign, founders must understand the internal governance and mechanics of a venture capital fund. Venture capital is not distributed unilaterally; it is a highly structured process governed by legal agreements and consensus.

The Investment Committee (IC) Bottleneck

A startup pitch typically begins with a junior team member - an associate or a principal - and eventually moves up to a sponsoring partner. If the sponsoring partner has conviction about the startup, they invite the founder to a formal "Partner Meeting" to pitch the broader partnership 5.

However, capital deployment is ultimately governed by an Investment Committee (IC). The IC reviews all investment-related policies, performance metrics, due diligence, valuations, and final deal terms 56. Because venture investments carry immense risk and require millions of dollars in capital, the fund's limited partnership agreements (LPAs) dictate strict quorum and voting rules for the IC to function.

Depending on the specific fund's bylaws, the IC generally requires a minimum number of partners to be present to constitute a quorum. In many institutional funds, unanimous approval from all committee members present is mandatory to approve the investment 6. Other funds stipulate that any resolution at a partner meeting must be agreed upon by all partners unanimously, or by a cohort of partners holding a specific, dominant percentage of the paid-up capital interest 78.

This is the mechanical failure point of the summer slump. If a venture firm requires a quorum of its senior partners to issue a term sheet, and just one or two key partners are out of the office on a two-week vacation, the IC cannot formally convene or vote. No matter how much the sponsoring partner loves the startup, their hands are tied until their colleagues return from holiday.

The Lead Investor Domino Effect

The absence of a single partner does not just stall one firm; it can stall an entire funding round due to the mechanics of venture syndication.

In priced equity rounds, securing a lead investor is the most critical and challenging hurdle 5. The lead investor conducts the deepest due diligence, negotiates the valuation, issues the term sheet, and typically contributes the largest single check to the round 5. Their presence acts as an internal champion and a market catalyst, setting off a "domino effect" that validates the startup's prospects and attracts the remaining capital from follower funds 5.

Many follower investors will explicitly withhold commitment until a reputable lead is confirmed, operating on a fear of missing out (FOMO) 5. If a founder reaches the final stages with a potential lead investor in early August, but that firm's IC cannot meet due to absent partners, no term sheet is issued. Without that anchoring term sheet, the follower investors continue to wait on the sidelines. The entire momentum of the fundraise evaporates. A startup that was a highly competitive, fast-moving deal in July suddenly becomes a stagnant deal in August, leaving the founder burning through precious cash runway while waiting for September.

The Macroeconomic Context: Why Delays Are Deadlier Today

The risks associated with the August slump are magnified significantly by the current macroeconomic climate. Following the record-breaking, zero-interest-rate policy (ZIRP) highs of 2021 and 2022, the venture market entered a period of severe correction 911. While capital is still available, the bar for securing it has risen dramatically, and the speed at which deals are processed has slowed for the vast majority of startups.

The Bifurcation of the Market

The contemporary venture landscape is characterized by extreme bifurcation. There is a clear divide between elite, often AI-driven startups that experience seemingly unquenchable private investor demand, and the broader market of startups that are struggling to attract capital amid a persistent liquidity crunch 2.

In 2024 and 2025, artificial intelligence dominated global venture activity. AI-related ventures accounted for roughly 37% of global venture funding and 17% of deals, representing an all-time high for sector concentration 1112. In the US, AI captured nearly 46% of total deal value, bolstered by massive mega-rounds 1210. For instance, a single $40 billion AI deal in Q1 2025 effectively doubled VC activity for the quarter; without it, funding would have declined by 36% 11. Similarly, in Q3 2025, unicorns (companies valued at over $1 billion) captured 56.8% of venture dollars while representing just 2.7% of the deal count 2.

For these high-momentum companies, the August slump is less of a barrier. Investors will interrupt their vacations to secure an allocation in highly competitive AI mega-deals. However, for the other 97% of startups, the reality is starkly different.

Increased Scrutiny and Extended Timelines

For non-AI startups, or those operating in traditional SaaS, consumer, or hardware sectors, investors are deploying capital much more cautiously 1216. The focus has shifted heavily away from "growth at all costs" toward unit economics, capital efficiency, and clear paths to profitability 1617.

This shift means that due diligence takes significantly longer than it did in previous years. Investors are demanding clearer proof of product-market fit and deeper audits of revenue metrics before committing capital 17. The extended diligence phase means that a fundraising process initiated in June is highly likely to bleed into August. If the diligence drags, the startup crashes directly into the vacation bottleneck.

Furthermore, the consequences of a stalled round are severe. The rate of down rounds (raising capital at a lower valuation than the previous round) and flat rounds represented 30% of deals in 2024, as startups that relied on cheap money were forced to face a capital crunch 1016. If a founder runs out of cash because an IC could not meet in August, they may be forced to accept highly punitive bridge financing terms or face insolvency.

Table 1: US Venture Capital Activity by Stage (2024 Summary)

The following table highlights the distribution of capital, illustrating that while late-stage and mega-deals receive the lion's share of funding, early-stage deals face intense competition and extended timelines.

| Funding Stage | Deal Count Share (2024) | Deal Value Share (2024) | Market Commentary |

|---|---|---|---|

| Pre-Seed / Seed | High (majority of volume) | ~7% of total value | Seed deals accounted for 92% of early transactions, but valuations face downward pressure in non-AI sectors 1314. |

| Early Stage (Series A/B) | Moderate | Moderate | Deal counts declined YoY; bridge rounds remain common as startups struggle to reach Series B metrics 313. |

| Late Stage / Growth | Low | High (47%+ of total value) | Capital is highly concentrated in proven winners and AI mega-rounds; median round sizes are swelling 1315. |

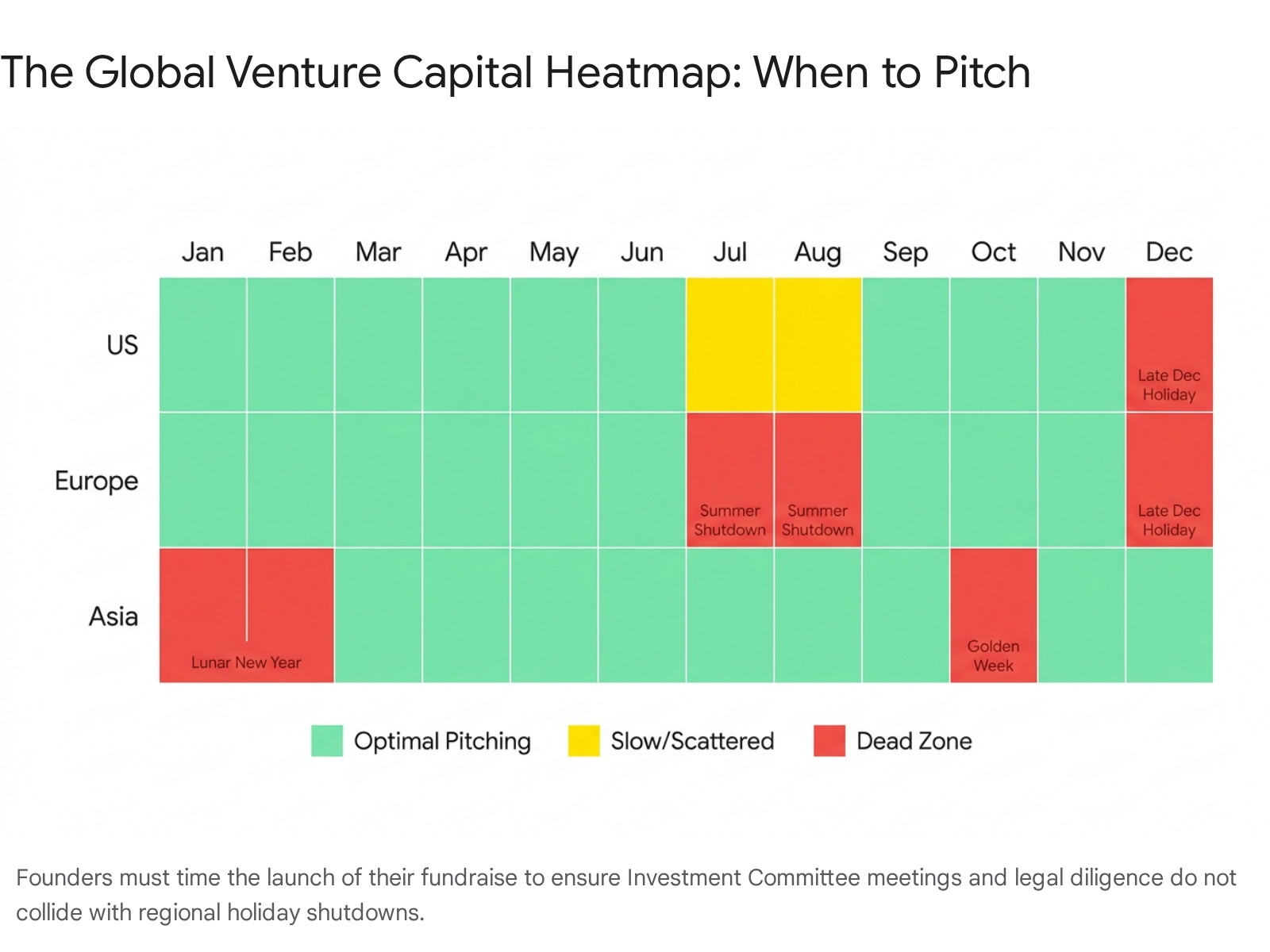

Global Seasonality: The European Shutdown vs. The US Summer

The severity of the summer slump depends heavily on the geographic location of the targeted investors. Venture capital is increasingly a borderless asset class, but cultural attitudes toward summer holidays remain deeply entrenched. Founders raising cross-border rounds must navigate these overlapping global schedules.

The United States: Fragmented Absences

In the United States, business leaders rarely take more than two consecutive weeks off, and summer vacations are generally scattered across the months of late June, July, and early August 16. The US venture market rarely experiences a total, systemic shutdown. Even around the July 4th holiday, the pause in operations is brief 16.

A founder raising exclusively from Silicon Valley, New York, or Boston funds might still secure a partner meeting in August, provided they can successfully navigate the fragmented vacation schedules of individual partners. However, because ICs require quorums, the scattered nature of US vacations can still stall deals; it is simply less predictable than in Europe.

Europe: The Institutional August Shutdown

If a startup is raising capital from European funds, or from US funds with significant European operations, August is an absolute dead zone.

Southern Europe operates on a systemic August shutdown. In France, Italy, Spain, and Portugal, it is culturally standard for businesses, professional services, and industrial operations to close for weeks at a time 161723. Italy observes Ferragosto starting August 15, while French businesses famously place closure notices in their windows for the entire month 161724. In the manufacturing sector, up to 80% of Portuguese textile factories close for two to three weeks between mid-August and early September 18. During this time, emails are answered slowly, meetings are pushed, and executive decisions are explicitly delayed until September 16.

In Northern Europe, the timing shifts slightly earlier. Countries like Sweden, Germany, and the Netherlands often take their extended "industrial holidays" in July, meaning their quietest month hits before the Southern European shutdown even begins 1617. For instance, Swedish businesses historically observe an industrial break from weeks 28 to 31, taking the majority of July off 17.

When trying to close a cross-border deal or secure a European lead investor during these windows, founders will simply be asked to wait. Legal processing, term sheet issuance, and IC quorums are virtually impossible to achieve.

Asia-Pacific: Alternative Rhythms and Golden Weeks

For startups operating in or raising from the Asia-Pacific (APAC) region, August is relatively insulated from the summer slump. In China and surrounding markets, summer is not a traditional season of rest, making July and August highly productive times to engage with Asian investors while European counterparts are away 16.

However, the Asian market is not without its own severe venture capital dead zones. The true shutdown occurs during the Lunar New Year (also known as the Spring Festival), which typically falls in late January or February 2627. This festival triggers the largest annual human migration on the planet and halts business operations, manufacturing, and financial transactions across China, Singapore, South Korea, Vietnam, and Malaysia for up to two weeks 262719. In 2026, for example, the Lunar New Year provides a 9-day statutory window that will effectively shut down factories and financial institutions for 12 to 14 calendar days 26.

A secondary, albeit shorter, slump occurs during China's "Golden Week" in early October 2629. Chinese markets close entirely during this seven-day national holiday, significantly reducing trading volumes, stalling cross-border wire transfers, and depressing global commodity prices like gold 2629.

Table 2: The Global VC Sourcing Calendar

To effectively plan a fundraise, founders must map their roadshows against regional downtime.

| Region | Primary "Dead Zone" | Secondary "Dead Zone" | Business Culture Impact |

|---|---|---|---|

| United States | Late December | Fragmented July & August | Short, scattered vacations; ICs may struggle for quorum, but there is no systemic national shutdown 16. |

| Northern Europe | July | Late December | Widespread "industrial holidays"; skeletal office staffing in July limits deal progression 1617. |

| Southern Europe | August | Late December | Near-total business shutdown; term sheets, legal processing, and partner meetings halt completely 1623. |

| Asia-Pacific | Lunar New Year (Jan/Feb) | Golden Week (October) | Massive domestic travel; markets close, halting due diligence, wire transfers, and regulatory processing 2629. |

How Founders Reverse-Engineer the Fundraising Timeline

Because the venture capital market relies heavily on momentum and market signaling, founders cannot afford to have their deal stall in the final stages. A stalled deal loses its aura of competitiveness, giving investors leverage to negotiate lower valuations, demand more onerous terms, or simply walk away entirely.

To prevent this, experienced founders reverse-engineer their fundraising timelines based on the exact month they need the capital deposited in their bank account. Knowing that a standard priced equity round takes three to six months from the first pitch to the final wire, founders generally opt for one of two distinct fundraising campaigns.

The Spring Sprint (Targeting a July Close)

If a startup requires capital by the end of the summer, they must launch their fundraise in the early spring. To generate a sense of urgency and close by July, proactive founders begin scheduling and taking first meetings in late April or early May 4.

This timeline allows May and June to serve as the intensive discovery and due diligence phases. By the time late June arrives, the startup is presenting at partner meetings before the general partners begin to leave for vacation. Once the IC approves the deal and the term sheet is signed in early July, the legal paperwork can commence. Crucially, the final legal drafting and wire transfers are handled by lawyers and finance teams, who are less subject to IC quorum rules, allowing the deal to successfully close in late July or August.

The Fall Campaign (Targeting a November Close)

If a startup is not fully prepared to launch its roadshow by early June, the prevailing advice from seasoned venture capitalists is to wait. Launching a fundraise in July virtually guarantees that the startup will hit the IC quorum bottleneck in August, stalling the deal and burning the startup's momentum.

Instead, intelligent founders use the quiet weeks of July and August to meticulously prepare their materials behind the scenes. They use the summer slump to refine their financial models, clean up their data rooms, build extensive target investor lists, and conduct mock pitches with advisors 5. They may also engage in "soft networking," reaching out to junior associates to get on the radar without formally opening a round.

When September arrives - widely considered the month when the global business engine restarts - the founder is ready to hit the ground running 16. A post-Labor Day launch provides a clear, uninterrupted 10-to-12-week runway to pitch, undergo diligence, secure term sheets, and close the round before the next major dead zone hits: the mid-December holiday freeze.

Bottom line

While macroeconomic data indicates that venture deals are finalized and vast amounts of capital are deployed during the summer, August remains effectively a dead zone for starting new fundraising conversations or securing term sheets. Because venture capital funds rely on strict Investment Committee quorum rules to deploy capital, the overlapping vacations of key partners - particularly in Europe - frequently halt the decision-making process. Founders seeking to maintain deal momentum and avoid punitive bridge rounds must actively reverse-engineer their timelines, ensuring they either pitch aggressively in May to close by July, or utilize the summer to prepare for a targeted September launch.