Factors in startup pitch deck success and investor decision-making

The startup pitch deck serves as the primary artifact of persuasion in the global venture capital ecosystem. Functioning as a strategic bridge between entrepreneurial vision and institutional capital, the pitch deck is subjected to intense scrutiny by investors operating under conditions of extreme uncertainty and information asymmetry. Over the past decade, the evaluation of these presentations has shifted from subjective, relationship-based appraisals to highly empirical, data-driven filtering processes. Recent macroeconomic tightening, the rapid proliferation of artificial intelligence, and evolving geopolitical paradigms have further altered the criteria by which venture capitalists assess pitch decks.

By synthesizing behavioral finance research, platform-derived engagement metrics, and geographic venture trends, this analysis identifies the structural, psychological, and macroeconomic factors that determine whether a pitch deck successfully secures capital. The data reveals that the efficacy of a pitch deck is not merely a function of graphic design, but rather a complex interplay of cognitive management, empirical validation, and precise market timing.

Pitch Deck Engagement Metrics

The volume of capital seeking allocation and the supply of startups seeking funding create a highly competitive marketplace where investor attention is a scarce commodity. Data aggregated from document-sharing platforms and presentation software provides a granular view of how venture capitalists consume pitch decks, revealing a consistent trend toward accelerated, highly critical evaluations 12.

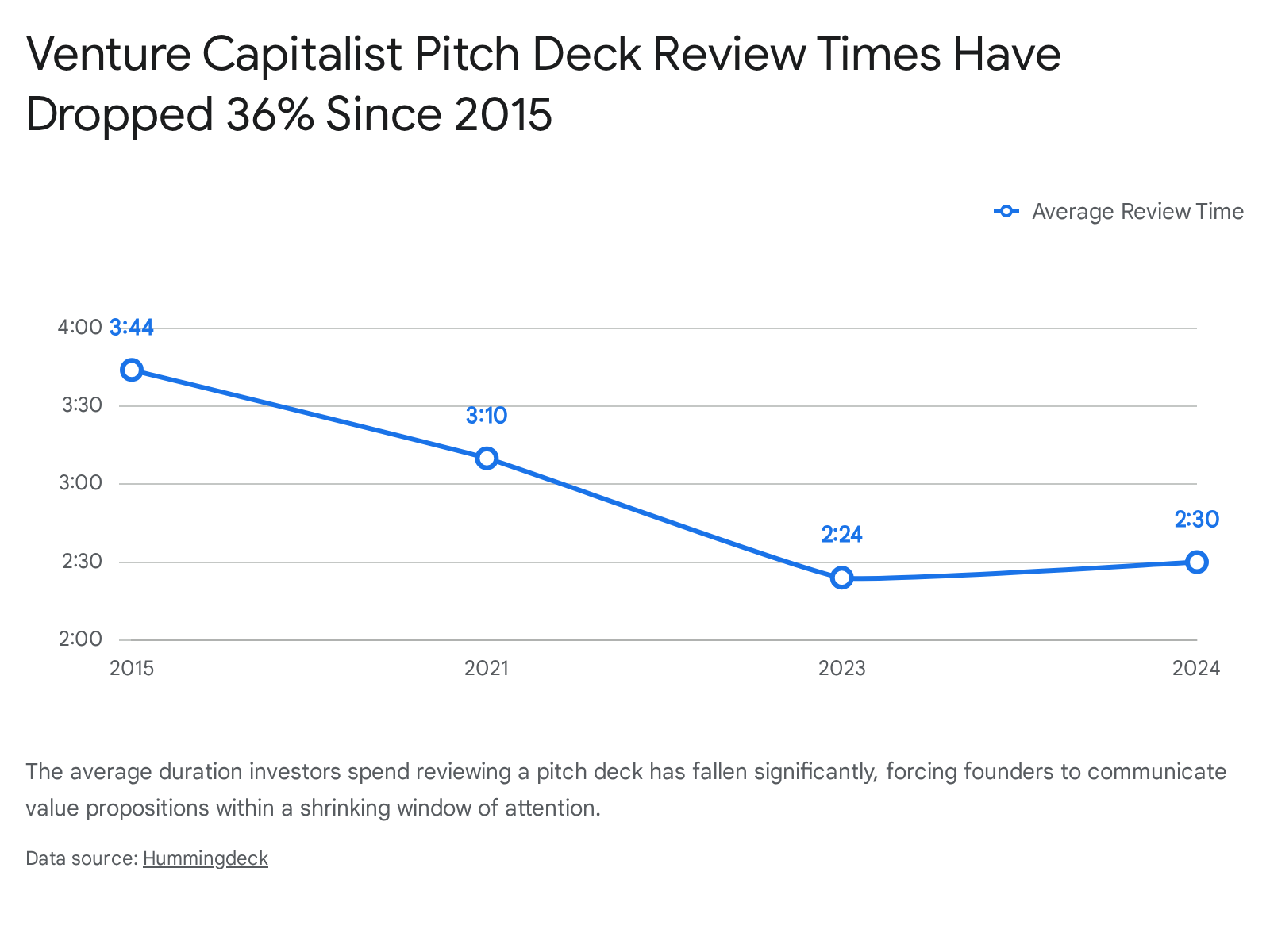

Viewing Time Attrition

The duration of time investors spend evaluating a single pitch deck has steadily declined over the past decade. An analysis of over 1.3 million presentation sessions demonstrates that the window to capture investor interest is shrinking rapidly 3. In 2015, the average investor spent 3 minutes and 44 seconds reviewing a deck 4. By 2021, this average had fallen to approximately 3 minutes and 10 seconds, and by late 2023, the metric hit an all-time low of 2 minutes and 24 seconds, with seed-stage decks dipping under the two-minute mark for the first time 145. While 2024 saw a marginal stabilization around 2 minutes and 30 seconds, the broader trend indicates that founders have less time than ever to convey their business case 46.

This attrition in viewing time is heavily influenced by the context of the deck's delivery. Pitch decks introduced via warm introductions average 4 minutes and 18 seconds of viewing time, whereas cold submissions average only 2 minutes and 31 seconds 4. Consequently, cold submissions convert to subsequent meetings at a rate of just 3% to 5%, compared to a 40% to 50% conversion rate for warm introductions 4. An engagement time exceeding four minutes is currently interpreted as a strong positive signal, while times under two minutes generally indicate rapid screening and rejection 4. Furthermore, timing optimization is critical; 35% of investor meetings are booked within the first 48 hours of opening a deck, and 96% happen within the first week, after which interest drops off completely 3.

Sectional Scrutiny and Attention Distribution

The distribution of investor attention across different sections of a pitch deck reveals a clear prioritization of empirical evidence over theoretical vision. As macroeconomic conditions tightened between 2022 and 2023, focus shifted dramatically from top-line growth to long-term profitability and unit economics 5. Data indicates that investors allocate the most time to the Financials and Traction slides, with the Team slide following closely behind 57.

In 2023, venture capitalists spent 48% more time evaluating business model slides and 25% more time analyzing traction slides compared to the previous year 5. Conversely, attention allocated to market size and competition slides decreased by 19% and 48% respectively, suggesting that investors prioritize proven, internal operational metrics over external, abstract market data 89. Unsuccessful decks experienced an even higher degree of scrutiny on empirical slides; investors spent 110% more time analyzing the traction slides and 233% more time on the business model sections of rejected decks, searching for validation that was ultimately absent or logically flawed 510.

The Team Slide Imperative

While financial metrics are heavily scrutinized, the "Team" slide remains the most consistently critical component across all stages of early funding. In 2024, venture capitalists spent 40% more time on seed-stage team slides and 30% more time on pre-seed team slides compared to 2023 810. The team slide appears in 100% of successfully funded decks, making it the only slide with that distinction 4.

Investors use this section not merely to review academic or professional credentials, but to assess "inevitability" - the perception that a specific group of founders possesses an unfair advantage, domain expertise, or unique insight required to execute the business model 71112. Research indicates that omitting technical founders at the pre-seed stage, or failing to connect individual team experiences directly to the problem being solved, serves as a primary catalyst for investor drop-off 713. Investors frequently ask whether the team's cohesion and dynamic can survive the inherent friction of scaling a venture 12.

Structural Architecture and Information Sequencing

The structural architecture of the pitch deck functions as a mechanism through which founders manage investor psychology and deliver empirical data. Standardization of deck architecture has occurred largely because predictable formats reduce cognitive load for investors processing thousands of opportunities annually 1415.

The most widely adopted structural framework originates from guidelines established by Sequoia Capital. While Sequoia never published a rigid "template," their recommended narrative flow has become the industry standard for evaluating opportunities 161718. The framework typically spans 10 to 15 slides and is designed to sequentially answer the investor's core underlying questions regarding purpose, problem, solution, market size, competition, and economics 18. Decks falling within the 10 to 18 slide range exhibit the highest completion rates (32%), whereas engagement drops precipitously for decks exceeding 20 slides, as excessive length signals an inability to prioritize critical information 37.

Observational data reveals structural divergences between decks that successfully secured capital and those that did not. Successfully funded decks typically place their Business Model slide fourth in the presentation sequence, whereas unsuccessful decks often delay this information, placing it tenth or later 4. Investors require an early understanding of the monetization mechanism to contextualize the subsequent product and market claims. Additionally, decks that clearly establish the problem and solution before detailing the product architecture consistently outperform those that lead with product features 10. Successful seed decks frequently insert a "Why Now?" slide immediately following the opening company purpose slide, addressing the specific market timing, technological breakthrough, or regulatory shift that makes the venture viable immediately 457.

| Deck Component | Successful Deck Sequencing | Unsuccessful Deck Sequencing | Underlying Rationale |

|---|---|---|---|

| Business Model | Typically placed 4th | Typically placed 10th | Investors demand early clarity on monetization mechanics before evaluating the product. |

| Problem/Solution | Placed prior to Product slides | Placed after Product slides | Establishes urgent market pain and context before demonstrating features. |

| Why Now? | High prominence, early placement | Often omitted | Validates market timing (e.g., AI breakthroughs, regulatory shifts). |

| Team | Included early, high detail | Placed at the end, vague | Mitigates execution risk and establishes founder inevitability. |

Funding Stage Evaluation Criteria

The expectations placed upon a pitch deck evolve as a startup matures through funding lifecycles. A presentation format that successfully secures pre-seed capital will almost certainly fail in a Series A context, as the evidentiary burden shifts from narrative potential to mathematical execution 1419.

At the pre-seed stage, companies typically seek between $250,000 and $2 million and operate with minimal quantitative traction. Pre-seed investors do not expect detailed, multi-year discounted cash flow models; instead, they fund insight, clarity, and the capacity for execution 72021. Successful pre-seed pitch decks function as narrative artifacts that communicate a compelling problem thesis 1921. Because historical revenue data is absent, traction must be demonstrated through alternative validation signals, such as design partnerships, pilot customers, letters of intent (LOIs), and waitlists with strong conversion metrics 72021. A bottom-up market sizing approach, relying on realistic adoption rates and customer counts rather than broad industry reports, builds the highest credibility at this stage 20.

Seed stage rounds, ranging from $2 million to $5 million, require a transition from narrative potential to empirical proof of product-market fit 720. The pitch deck must demonstrate that the hypothesis presented at the pre-seed stage is yielding tangible results in the market 19. At this juncture, investors expect specific revenue benchmarks, often looking for $10,000 to $50,000 in Monthly Recurring Revenue (MRR) 7. However, the absolute revenue figure is frequently secondary to the growth velocity. Consistent month-over-month (MoM) growth exceeding 15%, strong net revenue retention, and organic customer acquisition are critical indicators 7. The traction slide must present specific, defensible numbers rather than vague assertions of momentum 7.

Series A funding, which routinely exceeds $10 million, represents a definitive shift toward scaling a proven, economically sound business model 22. Investors at this stage demand rigorous financial models, cohort analysis, and predictable unit economics, strictly evaluating Customer Acquisition Cost (CAC) and Lifetime Value (LTV) 2023. Expectations for Series A metrics have increased significantly in the post-2022 macroeconomic environment. For software-as-a-service (SaaS) companies in the 2024 - 2025 period, the preferred Annual Recurring Revenue (ARR) threshold rose to between $2 million and $5 million, accompanied by requirements for sustained 100% year-over-year growth 22. The Series A pitch deck must transition entirely from a story about a product to a deeply analytical plan for aggressive, sustainable expansion 1424.

Cognitive Biases in Investor Psychology

Traditional financial theory posits that investors act as highly rational agents, systematically weighing the risks and projected returns of a venture. However, academic research in entrepreneurial finance and behavioral economics reveals that venture capitalists rely heavily on psychological heuristics, cognitive biases, and emotional responses when evaluating pitch decks under conditions of high uncertainty 2526282927.

Pattern Matching and Visual Dominance

Venture capitalists review thousands of pitch decks annually, necessitating rapid heuristic processing to filter opportunities 25. The decision to pass on an investment is often made within the first 30 seconds 1112. During this initial window, investors engage in "pattern matching," a cognitive shortcut wherein they subconsciously compare the current pitch against mental templates of previously successful or failed startups 111225. Pitch decks that fail to align with recognized patterns of success trigger immediate risk aversion 11. Successful founders actively manage this bias by anchoring their pitch to familiar patterns while introducing a unique differentiator to maintain intrigue 25.

While the substantive text and financial data of a pitch deck are vital for later stages of due diligence, initial screening decisions are heavily influenced by visual and non-verbal information. A comprehensive academic study analyzing 1,855 participants evaluating entrepreneurial pitch competitions found that participants could successfully predict the winning pitches using silent video recordings alone 28. Audio-only recordings or transcribed text of the pitches did not yield the same predictive accuracy 28. This research highlights that dynamic visual cues - such as gestures, facial expressions, and visible passion - often dominate the substantive content of the business proposition in the minds of evaluators 28. Investors frequently do not recognize the extent to which these visual and emotional heuristics factor into their decisions, subsequently rationalizing their choices based on the substantive metrics they explicitly cite as important 2832.

Established Behavioral Finance Biases

A systematic literature review of peer-reviewed behavioral finance research published between 2020 and 2025 confirms that classical cognitive biases continue to heavily influence venture capital decision-making 262930. Loss aversion plays a critical role; investors generally fear financial losses more than they value equivalent gains. In a pitch context, founders must frame their solutions as inevitable and highlight the risks of missing out on a paradigm shift, thereby triggering FOMO (Fear of Missing Out) to leverage loss aversion to their advantage 11122526.

Herding behavior is similarly prevalent. Investors frequently mimic the actions of prominent peers rather than conducting purely independent analysis, mitigating personal reputational risk 2629. Pitch decks that demonstrate social proof - such as commitments from notable angel investors, partnerships with recognized brands, or acceptance into elite accelerators - effectively trigger this herding instinct 112535. Furthermore, the anchoring effect dictates that the first piece of information offered sets the cognitive baseline for the rest of the evaluation 26. Successful decks utilize anchoring by presenting their most impressive metric immediately, framing all subsequent operational data favorably against that anchor 1112.

An emerging trend identified in 2020s literature involves automation bias, wherein investors over-rely on algorithmic recommendations and AI-driven screening tools utilized by fintech platforms 2629. Pitch decks must increasingly be formatted cleanly enough to be parsed seamlessly by the natural language processing (NLP) systems utilized by large venture funds during the initial triage phase.

Trust, Coachability, and Gender Stereotyping

When evaluating the founding team, investor psychology prioritizes perceived trustworthiness and character over pure technical competence 2731. Research conducted at Babson College demonstrated that angel investors' interest in a startup was driven less by judgments of the founder's competence and more by perceptions of their trustworthiness and openness to feedback, defined as coachability 31. Founders who demonstrated receptiveness to investor input during Q&A sessions were significantly more likely to advance to due diligence, as investors seek leaders they can collaborate with during inevitable operational pivots 2731.

These heuristic evaluations are deeply susceptible to systemic biases. Studies analyzing pitch interactions have found that investors often evaluate pitches through the lens of gender stereotypes 31. Research indicates that venture capitalists historically hold a bias against behaviors stereotypically associated with femininity, such as high emotional sensitivity or expressiveness; presenters exhibiting a high degree of these traits were less likely to succeed in pitching, regardless of their actual gender 31. Despite these systemic challenges, recent data from 2024 indicates a slight corrective trend, with mixed-gender teams receiving the highest average pre-seed and seed funding amounts, suggesting a growing investor recognition of the value of cognitive and demographic diversity 8.

Macroeconomic Influences on Capital Allocation

Pitch deck efficacy is highly contextual, governed by the prevailing macroeconomic environment. The transition from the low-interest-rate environment of 2021 to the higher-rate landscape of 2024 - 2026 profoundly altered the lens through which investors evaluate presentations 3233343541.

The Shift to Profitability and Capital Efficiency

In 2021, global venture capital investment reached a record high of approximately $254 billion in the United States alone, driven by near-zero interest rates and pandemic-fueled digital transformation 3536. During this period, pitch decks could succeed largely on the promise of hyper-growth, massive market capture, and visionary product development, even if unit economics were deeply unprofitable.

Following aggressive rate hikes by global central banks, borrowing costs increased dramatically, and institutional investors re-allocated capital toward lower-risk assets. By Q1 2024, venture capital investment had dropped significantly to $76 billion, marking the lowest level since 2019, and distributions from funds plummeted 33. In this environment - where interest rates hovered around 4.25% to 4.5% - the investor mandate shifted sharply from "growth at all costs" to capital efficiency and accelerated paths to profitability 333738.

Consequently, pitch decks evaluated in 2025 and 2026 are scrutinized through a stringent lens of risk mitigation. Founders must demonstrate sustainable operational models and fundamentally sound unit economics 39. High cash burn rates without immediate, measurable return on investment are heavily penalized 40. The statistical increase in viewing time dedicated to Financials and Business Model slides directly correlates with this macroeconomic reality, as investors meticulously verify runway, margin profiles, and cash flow projections 457.

The Artificial Intelligence Concentration Effect

The macroeconomic landscape of the mid-2020s has also been defined by an extreme concentration of capital within the artificial intelligence sector. In February 2026, the venture capital ecosystem shattered records, raising $189 billion in a single month; however, AI-related startups captured 90% of that capital, with just three companies (OpenAI, Anthropic, and Waymo) securing $156 billion 47.

This unprecedented concentration has raised the evidentiary bar for companies operating outside the AI sphere. Non-AI startups face a significantly smaller pool of available capital and must produce pitch decks with exceptional traction metrics to successfully compete for funding 47. For AI startups, expectations have similarly matured. Whereas a generic AI wrapper leveraging third-party APIs might have secured funding in 2023, investors in 2026 require pitch decks to demonstrate "Agentic Readiness" - the capacity for autonomous operational execution - alongside proprietary data moats and inference economics that radically reduce operational costs for clients 39.

Geographic Variances in Venture Expectations

While the Sequoia structure serves as a global baseline, the cultural, regulatory, and economic contexts of different geographic regions dictate specific modifications to the pitch deck narrative. A presentation optimized for Silicon Valley will frequently falter in Tokyo or Berlin due to misaligned expectations regarding risk appetite, scaling logic, and corporate governance 404142.

The United States: The "Adventurer" Model

The US venture ecosystem, epitomized by Silicon Valley, is characterized by a high tolerance for risk, vast domestic markets, and an aggressive pursuit of massive, industry-disrupting outcomes 414344. US investors expect founders to explicitly "sell the dream." Pitch decks must be bold, highly ambitious, and focus heavily on massive Total Addressable Markets (TAMs) 41. There is a pronounced tolerance for prioritizing rapid scaling and user acquisition over immediate profitability, provided the long-term monopoly potential and network effects are clear 41. Decks are typically concise and heavily index on the value proposition, founder conviction, and visionary narrative 4553.

Europe: Pragmatism and Sustainable Growth

The European venture capital landscape is shaped by a highly fragmented regulatory environment and a culturally ingrained preference for risk mitigation and sustainability 4154. European investors demand empirical proof over narrative hype. A successful pitch deck must present solid traction, a highly realistic and proven business model, and clear, near-term paths to profitability 41. Because the European Union consists of distinct national markets with differing regulations, languages, and cultural behaviors, a critical component of the European pitch deck is a meticulously detailed, localized Go-To-Market strategy. Founders must articulate exactly how they plan to navigate cross-border complexities and compliance requirements 4154. Furthermore, B2B buyer logic in Europe relies heavily on case studies, risk reassurance, and relationship-building rather than the high-velocity outbound sales models prevalent in the US 45.

Japan: Trust, Harmony, and Corporate Alignment

The Japanese venture capital ecosystem requires profound adjustments to the western pitch deck model. Japanese business culture places paramount importance on consensus, stability, and institutional trust 405546. Foreign founders entering the market must include a dedicated "Why Japan?" slide, addressing why their solution specifically targets domestic socio-economic issues, such as aging demographics, labor shortages, or the national green transition 40.

Due to tightening Initial Public Offering (IPO) regulations implemented by the Tokyo Stock Exchange - which mandate listed companies maintain a market capitalization of at least ¥10 billion within five years of listing - Japanese VCs are hyper-focused on capital efficiency and steady, predictable growth over high-burn expansion 4046. Investors closely assess "Team Harmony," evaluating not just the capability of the CEO, but the cohesion, stability, and longevity of the entire executive group 40. Furthermore, the pitch deck is rarely the venue where decisions are made. In Japan, the deck must be provided well in advance for private review, facilitating Nemawashi (the quiet pre-pitch alignment and consensus-building process) prior to formal meetings 4057.

China (Shenzhen): The "Architect" Model

The Chinese venture capital ecosystem operates in close alignment with state industrial policy, prioritizing hardware, supply chain integration, and rapid market deployment over software disruption 434458. While a Silicon Valley deck emphasizes proprietary Intellectual Property (IP) as a primary defensive moat, the Shenzhen ecosystem is built on rapid iteration, open collaboration, and component integration. Pitches in this region often focus on speed to market, manufacturing scalability, and supply chain dominance rather than strict IP protection 44.

Pitch decks targeted at Chinese capital - or increasingly, Middle Eastern sovereign wealth funds - must frequently pivot the narrative away from pure financial returns to demonstrate alignment with broader national strategic objectives and technology transfer goals 47. Geopolitical tensions and regulatory mechanisms, such as the Committee on Foreign Investment in the United States (CFIUS), have increasingly walled off these ecosystems, forcing globally ambitious founders to maintain dual-track narratives depending on the origin of the capital they are soliciting 435847.

| Region | Ecosystem Philosophy | Primary Pitch Deck Focus | Key Risk Factor Assessed |

|---|---|---|---|

| Silicon Valley (US) | Visionary / Adventurer | Disruption, massive TAM, hyper-growth | Lack of ambition, small market size |

| Europe | Pragmatic / Sustainable | Measurable traction, path to profitability | Regulatory hurdles, fragmented scaling |

| Japan | Consensus / Stability | Capital efficiency, team harmony, local fit | High cash burn, internal team friction |

| China / Shenzhen | Strategic / Architect | Supply chain leverage, speed, policy alignment | Geopolitical exposure, state regulation |

Prevalent Pitch Deck Failures

Despite the widespread availability of standardized frameworks and extensive advice regarding venture capital expectations, founders consistently commit specific rhetorical and structural errors that trigger rapid rejection. Peer-reviewed studies, investor surveys, and platform analytics highlight several fatal mistakes 13156048.

The most pervasive error is the overloaded slide. Founders frequently attempt to utilize the pitch deck as a comprehensive business plan, packing slides with dense text and complex technical diagrams. The optimal word count is approximately 30 to 50 words per slide 7. Dense text drastically increases cognitive load, obscuring the core value proposition and causing the investor to abandon the document 7131549. This failure in visual rhetoric signals a lack of operational clarity and an inability to prioritize critical information 2139.

Another common pitfall is the reliance on jargon and buzzwords. Substituting clear value propositions with visionary language (e.g., "AI-powered synergistic solutions for scalable disruption") obscures the actual mechanics of the business model and signals amateurism 6050. Investors require plain, descriptive language that directly addresses the problem and solution parameters. Furthermore, the top-down market sizing fallacy remains a frequent point of failure. Claiming a 1% capture of a broadly defined, multi-trillion-dollar industry lacks credibility. Investors demand a bottom-up market sizing approach that realistically calculates potential based on specific, reachable customer segments, sales cycles, and pricing models 206048.

Finally, failing to explicitly state the "Ask" undermines the utility of the deck. Pitch decks that omit the specific amount of capital being raised, the intended use of funds, and the operational milestones that capital will unlock fail to establish a clear call to action 2060. The omission leaves the narrative incomplete, transferring the burden of defining the investment parameters onto the investor, which often results in a passed opportunity. Similarly, burying the team slide at the end of the presentation, or failing to highlight a technical founder for deeply technical products, signals significant execution risk and limits investor confidence from the outset 1315.

Conclusion

The successful startup pitch deck is a highly engineered document that must satisfy competing and complex demands. It must be concise enough to respect diminishing investor attention spans, yet substantive enough to survive rigorous financial and operational due diligence. The empirical data clearly indicates a definitive shift away from the hype-driven narratives of previous economic eras. In the current macroeconomic climate, defined by higher interest rates and extreme capital concentration, investors utilize pitch decks primarily to identify empirical evidence of product-market fit, sustainable unit economics, and founding teams capable of highly capital-efficient execution.

Furthermore, a nuanced understanding of behavioral finance reveals that while quantitative metrics form the foundation of a business case, the ultimate decision to invest is inextricably linked to human psychology and cognitive biases. Founders must design presentations that manage cognitive load, leverage established structural heuristics, and generate trust through clear, visually compelling storytelling. Ultimately, a pitch deck succeeds when it seamlessly aligns the specific problem a startup solves with the distinct regional, financial, and psychological expectations of the institutional investor evaluating it.