What Replaced IEEPA for Section 122 Tariffs in 2026

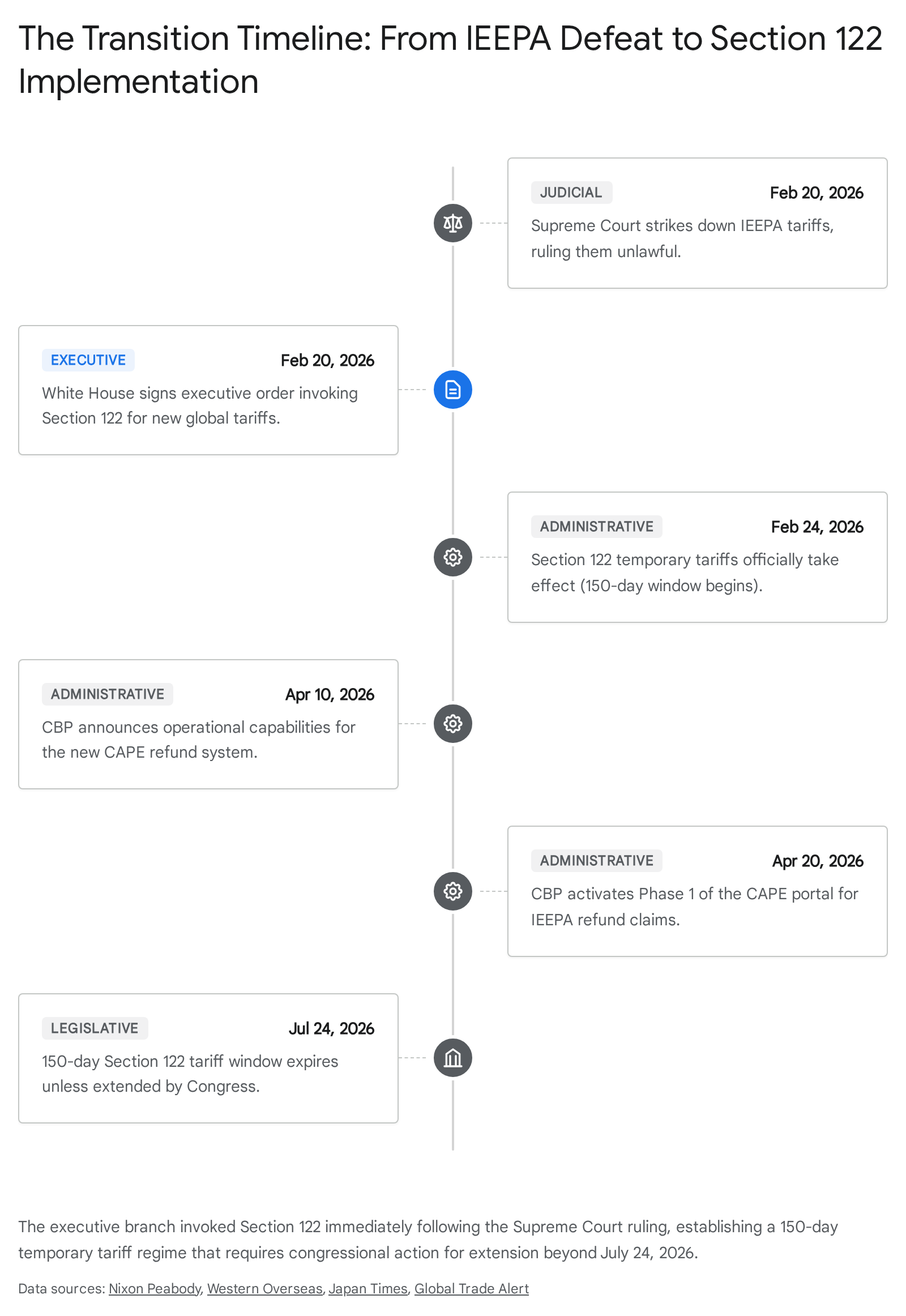

Bottom Line Up Front: The United States Supreme Court's landmark 6-3 decision on February 20, 2026, struck down the International Emergency Economic Powers Act (IEEPA) tariffs, prompting the executive branch to immediately implement a temporary 15% global import duty under Section 122 of the Trade Act of 1974. While the global supply chain scrambles to adjust to this standardized tax - which will expire in July 2026 without a highly uncertain congressional extension - domestic importers must urgently utilize the new Customs and Border Protection (CBP) CAPE portal to file e233 companion claims and recover an estimated $166 billion in unlawfully collected duties.

For the general reader, the arcane mechanics of executive trade authority might seem disconnected from daily life, but this abrupt policy shift has immediate consequences for the cost and availability of everyday goods. Tariffs act as hidden, indirect taxes embedded in the retail price of physical products. Whether it is a smartphone assembled in Asia, specialty groceries imported from Europe, or an automobile manufactured in the United Kingdom, the cost of clearing these items through U.S. customs fundamentally dictates their final price tag on store shelves. The overnight transition from targeted, country-specific tariffs to a blanket 15% global surcharge forces retailers to rapidly absorb or pass down these compliance costs. If supply chains cannot pivot quickly to source from newly advantaged regions, everyday consumers will bear the brunt of this geopolitical turbulence at the checkout counter.

What Exactly Replaced IEEPA?

To understand the current trade environment, one must first define the framework that governed U.S. imports until early 2026. The International Emergency Economic Powers Act (IEEPA) of 1977 was originally designed to grant the President broad authority to regulate commerce after declaring a national emergency in response to an unusual and extraordinary foreign threat 123. In previous years, the executive branch aggressively expanded its interpretation of IEEPA to unilaterally impose varying, punitive, country-specific tariffs on foreign trading partners, sidestepping traditional legislative trade mechanisms 345.

This legal architecture collapsed on February 20, 2026. In a definitive 6-3 ruling concerning consolidated cases (such as Learning Resources, Inc. v. Trump), the Supreme Court held that IEEPA did not authorize the executive branch to impose tariffs of unlimited amount and duration across arbitrary products and countries, declaring the collection of these duties fundamentally unlawful 1567. The ruling immediately terminated the collection of IEEPA tariffs and severely restricted the President's ability to utilize emergency powers as a permanent taxation tool, reaffirming that the power of the purse rests primarily with Congress 45.

However, utilizing an accessible analogy, the administration did not abandon trade barriers; instead, it shifted from a complex, unpredictable matrix of "emergency presidential trade powers" to a "standardized temporary tax." Within hours of the Supreme Court's ruling, the administration issued an executive proclamation invoking Section 122 of the Trade Act of 1974 235. This obscure, never-before-used statute allows the President to impose a temporary import surcharge of up to 15% ad valorem on all countries to address "fundamental international payments problems," specifically citing a $1.2 trillion goods trade deficit and deteriorating net international investment positions 235. Initially announced as a 10% global tariff on February 21, the rate was aggressively raised to the statutory maximum of 15% the very next day, taking formal effect on February 24, 2026 467.

When addressing the exact legal status of this current framework, it is vital to express calibrated uncertainty regarding its future. The Section 122 tariff is currently an active executive order, not a proposed bill 25. However, the statutory language of Section 122 explicitly limits this authority to a maximum duration of 150 days. Consequently, without an affirmative act of Congress to extend the measure, the 15% global tariff will automatically expire on July 24, 2026 356. Because congressional authorization is notoriously difficult to secure during polarized political climates, the administration is highly likely to face legal and procedural hurdles maintaining these rates. Anticipating this expiration, the executive branch has simultaneously ordered the fast-tracking of extensive investigations under Section 301 (Unfair Trade Practices) and Section 232 (National Security), seeking to utilize these separate, more durable legal authorities to replicate the current tariff levels before the summer deadline 235.

| Framework Attribute | Old IEEPA Regime (Terminated Feb 2026) | New Section 122 Regime (Active Feb 2026) |

|---|---|---|

| Legal Authority | International Emergency Economic Powers Act (1977) | Trade Act of 1974, Section 122 |

| Justification | National emergencies and foreign threats | "Large and serious" balance of payments deficits |

| Rate Structure | Highly variable, country-specific (e.g., 10% to 50%) | Flat, standardized 15% global ad valorem surcharge |

| Duration & Expiration | Indefinite (until constrained by judicial intervention) | Strictly temporary; expires in 150 days (July 24, 2026) |

| Target Scope | Specifically targeted at adversarial nations or trade disputes | Universal application to all countries |

| Exemptions Mechanism | Complex bilateral negotiations and floor deals | Narrow statutory carve-outs (e.g., USMCA, Section 232 items) |

Who Really Pays For These Tariffs?

Before analyzing the geopolitical and financial impacts of the new rate structures, it is necessary to address a pervasive common misconception that routinely distorts discussions of global trade. Political rhetoric often suggests that tariffs are punitive levies paid directly by foreign governments or overseas exporting corporations to the U.S. Treasury. This is fundamentally inaccurate. A tariff is a domestic tax assessed on imports, and the invoice is handed exclusively to the domestic Importer of Record 10.

When a shipment of textiles from Malaysia or machinery from the United Kingdom arrives at a U.S. port of entry, the foreign manufacturer has already been paid for the goods. It is the American business - the importer - that must calculate the landed cost, file the entry summary with CBP, and physically transfer the required funds to the federal government to clear customs 10. While the foreign exporter may suffer secondary effects if the U.S. buyer demands price concessions or shifts their purchasing to a different country, the primary, immediate financial hemorrhage is absorbed entirely by the domestic corporate balance sheet. As these American businesses incur higher import costs, they inevitably protect their operating margins by passing the tax down the supply chain, ultimately resulting in inflationary pressures and higher retail prices for the everyday consumer 410.

Understanding this mechanism is crucial for comprehending the scale of the ongoing tariff refund crisis. Because IEEPA tariffs were paid by U.S. companies, the Supreme Court's ruling invalidating those tariffs means the U.S. government unlawfully extracted domestic capital. Analysts estimate that between $166 billion and $175 billion was collected under the now-defunct IEEPA mandates across more than 53 million entry lines 478. The resulting e233 refunds, therefore, are not international reparations to foreign states; they represent a massive, $175 billion capital injection directly back into the American private sector. This refund mechanism serves to offset the enormous capital drain importers experienced over the past several years, providing them with the necessary liquidity to navigate the current chaotic transition to the Section 122 framework 4.

How Much Do Importers Pay Under Section 122?

The transition from the customized, punitive rates of IEEPA to the standardized 15% flat rate under Section 122 has drastically reordered the global trade landscape, creating distinct geographic winners and losers based entirely on their previous baseline rates 37. While the 15% surcharge applies broadly, there are limited exceptions. Roughly 1,100 specific product codes are exempt, including essential pharmaceuticals, certain critical minerals, and aerospace components 27. Furthermore, goods imported under the U.S.-Mexico-Canada Agreement (USMCA) remain compliant with their specific treaties, and products already subjected to Section 232 tariffs (such as the 25% duties on specific steel and aluminum imports) are generally excluded from the overlapping Section 122 surcharge 712. For everything else, the new reality is a rigid 15% tax.

This sudden standardization has provided a massive, albeit potentially temporary, windfall for Asian exporters. Under the previous IEEPA regime, members of the Association of Southeast Asian Nations (ASEAN) were subjected to crippling retaliatory tariffs. Myanmar and Laos faced rates as high as 40%, while the Philippines, Cambodia, Indonesia, and Thailand were burdened with 19% tariffs 9. By standardizing the global rate at 15%, Section 122 effectively slashed the import tax burden on Southeast Asian goods, instantly making these markets highly competitive alternatives for U.S. buyers 79. Recognizing this sudden advantage, Malaysia formally declared its previous bilateral Agreement on Reciprocal Trade (ART) with Washington - which had locked in a 19% rate - as "null and void," opting instead to operate under the lighter 15% global baseline 14. Similarly, major manufacturing hubs like China and India have experienced effective tariff reductions of 7.1 and 5.6 percentage points, respectively, restoring a degree of cost competitiveness to their exports 7. Economies heavily reliant on high-tech exports, such as Taiwan and South Korea, remain relatively insulated; their advanced semiconductor and AI server components largely bypassed both the harshest IEEPA penalties and the new 15% regime due to strategic technological exemptions, allowing their export volumes to surge continuously 67.

Conversely, the shift to a 15% global tariff has shocked traditional U.S. allies in Europe and the United Kingdom, who had previously negotiated preferential floors. The UK had successfully secured a favorable 10% rate under its Economic Prosperity Deal with the United States 1012. The overnight imposition of the 15% Section 122 tariff eradicated that competitive advantage, immediately threatening the margins of approximately 40,000 UK exporters and forcing rapid contract renegotiations across the Atlantic 1012.

The European Union's reaction has been equally turbulent. In July 2025, the U.S. and the EU brokered the "Turnberry Agreement," a highly controversial pact designed to cap U.S. tariffs on European goods at 15% in exchange for the elimination of EU tariffs on American products and a massive, $250 billion annual commitment by the EU to purchase U.S. energy (LNG, oil, and coal) 15161018. The agreement was fundamentally flawed from inception, with actual EU energy purchases in 2025 totaling a mere $73.7 billion, failing entirely to meet the political targets 18. Following the Supreme Court's dismantling of IEEPA and the unilateral executive imposition of the Section 122 global tariff, the European Parliament formally froze the ratification of the Turnberry Agreement, declaring that the underlying logic of the pact had been rendered obsolete by Washington's erratic trade posturing 151011. Similarly, Japan's Ministry of Economy, Trade and Industry (METI) has engaged in aggressive diplomatic consultations, leveraging its massive $550 billion capital commitment to U.S. investments to demand that Japanese exports remain capped at their previous 10% rate rather than face the new 15% universal levy, highlighting the intense friction the new policy has generated among long-standing allies 212.

How Do e233 Refunds Work?

While managing the fallout of the new 15% tariff, U.S. importers are simultaneously racing to reclaim the estimated $166 billion in funds unlawfully collected under IEEPA 48. Following sweeping orders from the U.S. Court of International Trade in cases such as Atmus Filtration v. United States and Euro-Notions Florida Inc. v. United States, CBP was legally compelled to architect a system capable of refunding millions of entry lines at unprecedented speed 1713. The result of this 45-day judicial mandate is the Consolidated Administration and Processing of Entries (CAPE) portal, which officially went live within the Automated Commercial Environment (ACE) on April 20, 2026 1781314.

To initiate the recovery process, an importer or their licensed customs broker must file a companion customs claim - commonly known within trade compliance circles as the e233 refund declaration. This electronic submission acts as the precise legal request for the return of funds, triggering a highly automated administrative sequence.

The CAPE system was designed for mass processing, but it is rolling out in distinct operational phases. Phase 1, which represents approximately 63% of the total affected entries, targets the most administratively straightforward claims 7813. Once an importer uploads a precisely formatted CSV file detailing their entry summary numbers and the specific IEEPA duty lines, the CAPE system automatically cross-references the data against CBP's internal ledgers 18. If validated, the software digitally removes the unlawful IEEPA Harmonized Tariff Schedule (HTS) codes, recalculates the baseline duty obligation as if IEEPA had never applied, and calculates the statutory interest owed to the importer 713. The interest payments are significant; under 19 U.S.C. Section 1505(c), CBP must pay a 7% interest rate for non-corporate entities and a 6% rate for corporate entities, calculated from the original date of duty payment through the date of liquidation 13.

The timeline for these e233 refunds requires strategic patience. Upon filing, CBP generally takes 10 days to officially accept the CAPE declaration 13. For unliquidated entries, the system schedules a final liquidation 45 days after acceptance 13. Ultimately, CBP is projecting that single, consolidated lump-sum refunds will be distributed electronically via the Automated Clearing House (ACH) directly to the importer's designated bank account within 60 to 90 days of the initial filing 81314.

| Importer Entry Status | CAPE Phase 1 Eligibility | Estimated Refund Timeline | Action Required by Importer |

|---|---|---|---|

| Unliquidated Entries | Eligible. | 60 to 90 days after e233 submission. | File CSV declaration in CAPE. |

| Recently Liquidated (≤ 80 Days) | Eligible. (Will be reliquidated). | 60 to 90 days after e233 submission. | File CSV declaration in CAPE. |

| Old Liquidated (> 80 Days) | Not Eligible in Phase 1. | Unknown. Pending future CAPE phases. | Consult counsel to preserve judicial remedies. |

| Suspended / Under Review | Standard Course. | Follows standard administrative timelines. | Monitor ACE status closely. |

It is critical to note that entries liquidated more than 80 days prior to the CAPE launch (i.e., before January 30, 2026) are currently excluded from Phase 1. The Court of International Trade has acknowledged that these older, finalized liquidations present complex legal and technical challenges, and importers possessing these entries must rely on alternative legal remedies or await subsequent, currently unscheduled phases of the CAPE rollout 813.

What This Means for Small Businesses

For small to medium-sized importers, the simultaneous implementation of the Section 122 tariffs and the launch of the CAPE refund portal presents a dual challenge of aggressive cost mitigation and rigorous compliance management. The following practical takeaways outline the necessary steps to navigate this complex environment.

First, small businesses must adopt a disciplined, zero-defect approach when filing the e233 companion customs claims. CBP has restricted access to the CAPE portal to the actual Importer of Record or the specific customs broker who filed the original entries 17. Small businesses must immediately coordinate with their brokers to compile their data. The automated nature of the CAPE mass processing script means that any discrepancy between the CSV upload and CBP's historical data will result in outright rejection. Importers must ensure that all refund data precisely matches the original entry summary at the line level, and that IEEPA duty lines are accurately linked to the underlying HTS classifications 14. Maintaining clear, auditable documentation supporting the duty paid and the calculation methodology is essential to avoid lengthy administrative delays.

Second, small businesses operating as Non-Resident Importers (NRIs) must urgently verify their financial infrastructure. CBP's refund mechanism is exclusively electronic, issuing payments via ACH directly to the U.S. bank account linked to the importer's ACE profile 1314. While domestic businesses typically have this integration natively configured, NRIs frequently lack valid U.S. banking infrastructure 14. Without a properly configured ACH setup, even fully approved e233 claims will face indefinite delays at the point of payment. NRIs must resolve these banking technicalities concurrently with their data compilation efforts to ensure liquidity flows unobstructed 14.

Finally, small businesses must ruthlessly audit their global supply chains to mitigate the cost impacts of the new 15% Section 122 tariff. Because this rate applies universally, the comparative advantage of various international suppliers has fundamentally shifted. For instance, continuing to source components from the United Kingdom - which saw its tariff rate increase from 10% to 15% - may no longer be economically viable when competing manufacturers in Southeast Asia just experienced a drastic reduction from 19% or 40% down to the 15% baseline 10129. Small businesses should actively explore diversifying their supplier base to leverage these new geopolitical realities. Furthermore, because the Section 122 authority is strictly temporary and set to expire in 150 days (July 24, 2026), importers should aggressively utilize Foreign Trade Zones (FTZs) or bonded customs warehouses 3612. By storing goods in these designated areas, businesses can legally delay formally entering their products into U.S. commerce, effectively deferring the payment of the 15% surcharge until the political and legal landscape stabilizes later in the year, potentially avoiding the tariff altogether if Congress fails to extend the measure.

Bottom Line

The U.S. trade environment in 2026 is defined by rapid legal upheaval and immense financial stakes. The Supreme Court's invalidation of the IEEPA framework forced an emergency pivot to Section 122 of the Trade Act of 1974, establishing a temporary, 150-day flat global tariff of 15% that will require a difficult congressional extension to survive beyond July. Concurrently, U.S. importers - who directly bear the financial burden of these taxes, not foreign governments - are navigating the complexities of the newly launched CAPE portal. By meticulously filing e233 companion claims, domestic businesses have a historic opportunity to reclaim billions in unlawfully collected funds, requiring precise data compliance and agile supply chain strategies to weather the ongoing geopolitical volatility.