What Happens Behind the Scenes of Mortgage Approval

When a mortgage application is submitted, it enters a rigorous forensic audit where a lending professional evaluates a borrower's capacity to repay, credit history, and the property's collateral value. Modern underwriting blends algorithmic automated systems with human detective work to ensure the loan meets strict investor guidelines and federal regulations. Ultimately, lenders want to guarantee the financial stability of the borrower remains intact from the initial application right up to the closing table.

For most homebuyers, the period between submitting a loan application and receiving the final clearance to close feels like a mysterious black box 12. You upload tax returns, pay stubs, and bank statements into a portal, and then wait in anxious silence. Behind the scenes, however, the mortgage underwriting process is a highly choreographed sequence of risk assessment. The primary goal of the lender is to answer a single, fundamental question: Does extending this specific amount of credit make sense from a risk perspective? 2. To answer this, the modern mortgage industry relies on a complex ecosystem of specialized personnel, advanced algorithms, and strict regulatory frameworks designed to stress-test your financial life.

The Mortgage Approval Assembly Line

A mortgage application does not sit on a single desk; it moves through a specialized assembly line of financial professionals 3. Understanding the lifecycle of a loan requires identifying the key players who handle the file from inception to funding.

The borrower's primary point of contact is the loan officer. This licensed professional helps select the appropriate mortgage product, locks in the interest rate, and gathers the initial financial profile to issue a preliminary pre-approval 3. Once the borrower finds a property and signs a purchase agreement, the file moves to the loan processor. Acting as the verifier and organizer, the processor ensures all necessary documentation is present, orders the home appraisal, and requests title insurance 34. It is important to note that processors do not make credit decisions; their job is to build a comprehensive, validated file to hand off to the decision-maker 41.

That decision-maker is the underwriter. Operating mostly out of sight, the underwriter evaluates the risk of the loan against strict guidelines set by secondary market investors and the lender's own corporate policies 36. They are the only individuals authorized to officially approve or deny the loan application 3. Finally, once the loan is approved, the closer takes over to prepare the final legal documents, ensure all closing costs are perfectly calculated, and coordinate the actual transfer of funds 3.

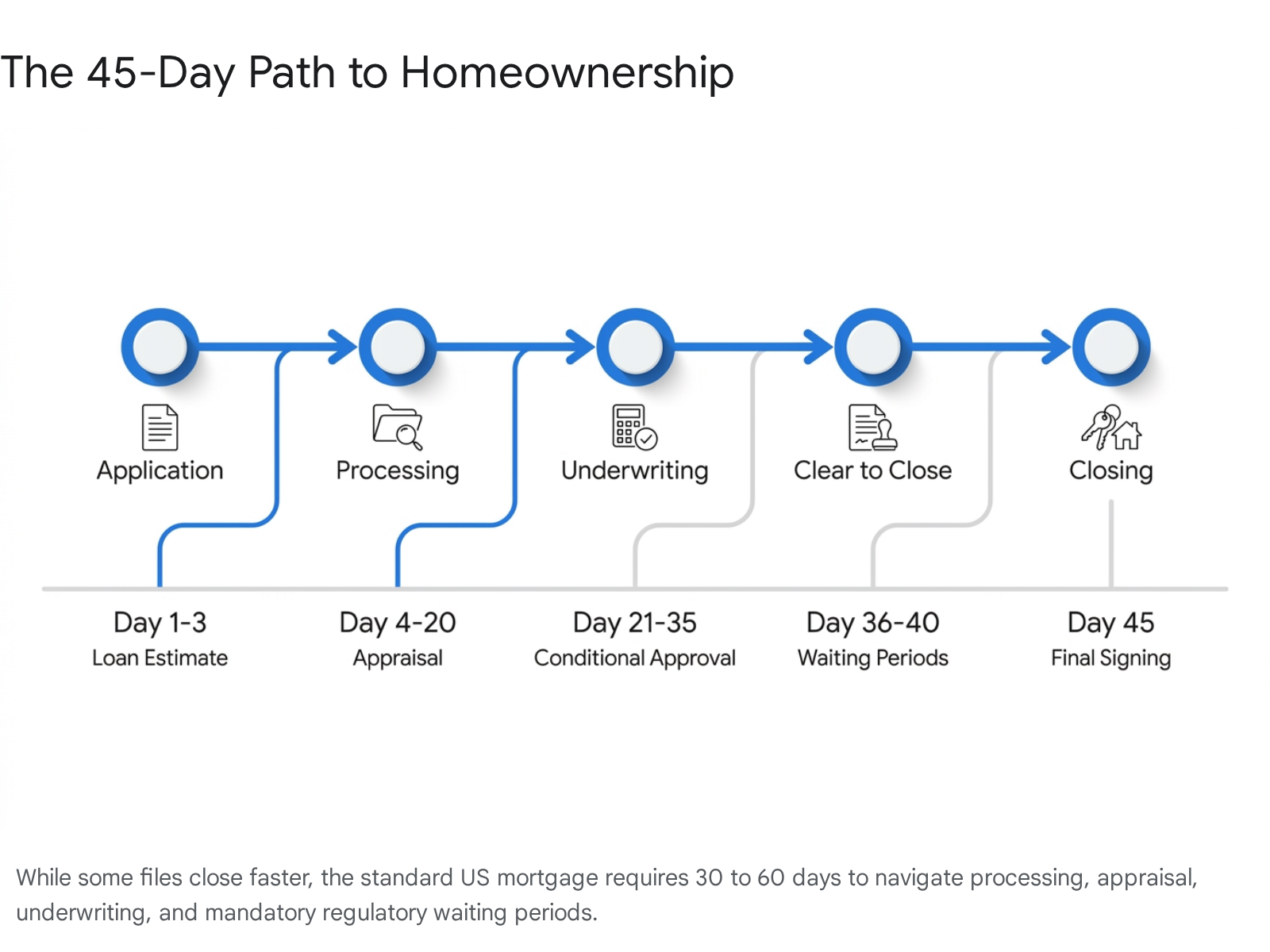

The timeline for a traditional residential mortgage in the United States typically spans 30 to 60 days 178.

The process moves through distinct phases, starting with pre-qualification or pre-approval, which relies on preliminary data and automated systems but does not guarantee funding 89. Once a property is chosen and formal underwriting begins, the borrower will typically receive a conditional approval. This status means the lender agrees to fund the loan, provided the borrower fulfills specific remaining conditions, such as explaining a recent bank deposit or waiting for the property appraisal to clear 348.

When every condition is satisfied, the underwriter issues the ultimate green light: clear to close 238. This milestone triggers the issuance of a Closing Disclosure (CD), a legally mandated document outlining the exact terms, interest rate, and costs of the loan. Under federal rules managed by the Consumer Financial Protection Bureau (CFPB), the borrower must receive this document at least three business days before signing the final paperwork, providing a mandatory cooling-off period to review the math 231.

The Forensic Audit: Evaluating the Three C's

When the processor hands the file to the underwriter, the true forensic audit begins 210. The underwriter's evaluation is universally grounded in the "Three C's" of lending: Capacity, Credit, and Collateral 210. Each pillar represents a different facet of risk that must be verified and documented.

Capacity and the Debt-to-Income Equation

Capacity refers to the borrower's financial ability to comfortably make the monthly mortgage payments alongside all other existing debts. Following the 2008 financial crisis, federal regulations mandated that lenders rigorously verify a borrower's Ability to Repay (ATR) to prevent the issuance of unaffordable loans 11. The primary metric used to measure capacity is the Debt-to-Income (DTI) ratio 213.

DTI is calculated by dividing total monthly debt obligations by gross, pre-tax monthly income. Lenders look at two specific variations of this ratio. The front-end DTI, also known as the housing ratio, considers only housing-related expenses, encompassing principal, interest, taxes, and insurance (PITI) 1314. The back-end DTI is a more comprehensive measure that incorporates PITI plus all other recurring monthly debts, such as auto loans, student loans, minimum credit card payments, and court-ordered alimony or child support 114. While traditional wisdom suggests keeping housing costs below 28% of income and total debt below 36%, modern underwriting guidelines frequently allow back-end DTIs up to 43%, or even 50% if the borrower presents strong compensating factors 1315.

To calculate capacity, a borrower's income must be highly documentable and stable. For traditional employees, this usually means providing the most recent 30 days of pay stubs and two years of W-2 forms 21. However, the underwriter is not just checking to see if the income exists; they are investigating how it behaves over time 3. Overtime, bonuses, and commissions must generally show a consistent two-year history to be counted as qualifying income 4. If a borrower relies on non-employment income, such as rental income or child support, the lender requires proof that this revenue stream can reasonably be expected to continue in the future 5.

For self-employed borrowers, the scrutiny intensifies significantly. Instead of simple W-2s, underwriters require year-to-date profit and loss statements, balance sheets, and two years of both personal and business tax returns 164. Self-employed individuals must demonstrate that their business is financially stable enough to sustain their income for the long term, adding layers of complexity to the capacity calculation 6.

Credit History and Willingness to Repay

While capacity proves a borrower has the financial means to repay the loan, the credit profile suggests whether they actually will. A credit score compresses consumer bureau data into a single number, but the underwriter looks deeper into the full credit report to analyze payment patterns, the age of credit lines, and overall credit utilization 12196. An underwriter evaluates repayment willingness by looking at the borrower's track record of honoring past obligations 6.

In modern lending, the initial credit evaluation is often performed by an Automated Underwriting System (AUS), such as Fannie Mae's Desktop Underwriter (DU) or Freddie Mac's Loan Product Advisor (LPA) 221. These algorithms analyze the credit data and generate rapid risk assessments 21. However, if the automated system flags a file due to a thin credit history, a recent bankruptcy, or an abnormally high DTI, it will return a "Refer with Caution" status 10. This requires the file to be routed to manual underwriting.

In manual underwriting, a human professional conducts a deeper analysis, looking for reasons to approve a loan that a rigid algorithm might reject 10. The underwriter actively seeks "compensating factors" to offset the identified credit risk 1014. These factors might include a substantial down payment, significant cash reserves in the bank equaling several months of mortgage payments, or a spotless alternative credit history demonstrating consistent, on-time payments for rent and utilities 10.

Collateral and Property Appraisals

A mortgage is a secured loan, meaning the property itself acts as collateral. If the borrower defaults, the lender must be able to sell the property to recoup their financial losses. Therefore, the underwriter must ensure the home is actually worth the agreed-upon purchase price 78.

To verify collateral, the lender orders an independent, third-party appraisal. The appraiser performs an on-site inspection of the home and compares it to recent sales of similar properties in the immediate area, adjusting the valuation for differences in amenities 7. If the appraisal comes in lower than the purchase price - a situation known as an appraisal gap - the underwriter will not approve the loan for the full requested amount 224. A lender will never finance more than the property is worth. In these cases, the borrower must either renegotiate the price with the seller, bring extra cash to the closing table to cover the difference, or walk away from the transaction 29.

Beyond raw financial valuation, the underwriter also reviews the appraisal for habitability and safety issues. If the appraiser notes significant problems, such as missing handrails, peeling paint, or broken windows, the underwriter may issue a denial or mandate that repairs be completed before the loan can close 26. Furthermore, a title search is scrutinized during this phase to ensure there are no hidden liens, ownership disputes, or legal encumbrances that would jeopardize the lender's claim to the property 927.

Commercial vs. Residential Underwriting

While residential underwriting focuses heavily on the personal income and credit of the homebuyer, commercial real estate underwriting operates on entirely different principles. A residential mortgage evaluates whether a person can afford a home; a commercial loan evaluates whether a property can function as a profitable business 8.

In commercial underwriting, the financial detective work centers on the property's ability to generate cash flow 8. The critical metric is the Debt Service Coverage Ratio (DSCR), which measures whether the property brings in enough income to pay its own operational bills and the mortgage 8. Lenders calculate this by dividing the property's Net Operating Income (NOI) by the total annual loan payments. A DSCR of 1.0 means the building generates exactly enough to cover the debt, which leaves no margin for error 8. Commercial underwriters typically demand a DSCR of 1.25 or higher, ensuring a 25% cash flow cushion 8.

To verify this income, commercial underwriters analyze complex property documents rather than personal W-2s. They scrutinize the Rent Roll, which provides a snapshot of current leases, tenant stability, and potential future income 28. They compare this against the T12 (Trailing 12 Months) operating statement, which acts as a historical video playback of the property's actual revenue and expenses over the past year 28. By cross-referencing these documents, commercial underwriters determine the true financial health and value of the investment asset 28.

Navigating the Danger Zone: Denials After Pre-Approval

Receiving a pre-approval letter often gives homebuyers a false sense of security, leading to critical mistakes. Mortgages are frequently denied in the final stages of underwriting because the borrower's financial snapshot changed during the quiet period between application and closing 1926. Lenders continually monitor credit and employment status right up to the day of funding, and any deviation from the original application can trigger a denial 26.

Taking on new debt is one of the most common reasons a pre-approved loan falls through. Financing a new car, opening new credit lines, or buying thousands of dollars of furniture on credit fundamentally alters the borrower's debt-to-income ratio 1992627. If this new debt pushes the DTI past the loan program's maximum allowable limit, the underwriter has no choice but to deny the loan 926. Similarly, negative changes to a credit profile, such as missing a payment on an existing student loan or allowing a medical bill to go to collections during the escrow period, can drop a credit score below the program's minimum threshold 926.

Employment stability is equally critical. Changing employers, moving from a salaried position to a commissioned role, or quitting a job entirely disrupts the calculation of sustainable income, immediately halting the approval process 9926.

The Scrutiny of Bank Deposits

Underwriters operate like financial detectives, constantly searching for undisclosed risks 68. One of the most intense points of scrutiny involves a borrower's bank accounts. If a borrower transfers large sums of money between banks or makes large, unexplained cash deposits, the underwriter will demand a meticulous paper trail 952627.

This scrutiny is required under federal anti-money laundering regulations and strict investor guidelines 529. Lenders must verify the source of all down payment funds to ensure the money is not a secret, undisclosed loan that would alter the borrower's true debt load 526. If the deposited money was a gift from a family member, the underwriter will require a formal, signed gift letter confirming that the funds do not need to be repaid 29. The golden rule of the underwriting period is to freeze all financial behavior: keep paying bills on time, avoid moving money without documentation, and maintain open communication with the loan officer before making any changes 2927.

How Federal Rules Shape the Underwriting Process

Underwriters do not invent the rules they enforce; they apply guidelines established by government agencies and secondary market investors who purchase the loans after they are originated 1121. The vast majority of standard mortgages in the United States conform to rules set by Fannie Mae and Freddie Mac.

Fannie Mae, Freddie Mac, and Loan Limits

Fannie Mae and Freddie Mac are government-sponsored enterprises (GSEs) that provide vital liquidity to the housing market by purchasing mortgages from lenders 2. While their underwriting guidelines are broadly similar, lenders must navigate subtle but impactful differences between the two entities 30.

For example, both GSEs allow up to a 97% Loan-to-Value (LTV) ratio on a single-unit primary residence 30. However, their treatment of specific financial hurdles diverges. Fannie Mae allows for the verification of extenuating circumstances to shorten waiting periods after a foreclosure or short sale, and it may recognize divorce as a financial hardship 30. Freddie Mac, conversely, does not accept extenuating circumstances for reduced waiting periods and handles divorce-related hardships differently 30. Additionally, Fannie Mae may offer more flexibility in how student loan repayment plans are calculated into a borrower's DTI, while Freddie Mac applies its own strict calculation methods 30.

The Federal Housing Finance Agency (FHFA) oversees these GSEs and adjusts the maximum size of a conforming loan annually based on national housing price indexes 10. Because home prices rose by an average of 5.21% between late 2023 and 2024, the baseline conforming loan limit for a standard one-unit property was increased to $806,500 for the 2025 calendar year 1011.

In designated high-cost areas, such as major metropolitan centers, Fannie Mae and Freddie Mac are authorized to purchase single-unit loans as large as $1,209,750 1011.

Government-Backed Mortgages

Borrowers who fall outside the strict parameters of conventional lending often turn to government-backed loan programs. Because federal agencies insure these loans against default, lenders are willing to accept higher risk profiles, allowing underwriters to utilize more flexible guidelines 1315.

| Loan Type | Backing Agency | Standard Maximum DTI | Minimum Down Payment | Key Underwriting Nuance |

|---|---|---|---|---|

| Conventional | Fannie Mae / Freddie Mac | Up to 50% (requires strong AUS approval) 12 | 3% to 5% | Emphasizes strong credit history and strict compliance with GSE automated guidelines 234. |

| FHA | Federal Housing Administration | 43% back-end (up to 50% with robust compensating factors) 1335 | 3.5% | Highly forgiving of lower credit scores; borrowers can qualify with scores down to 580 for maximum financing 133436. |

| VA | Department of Veterans Affairs | No strict cap (but scrutinized heavily if over 41%) 37 | 0% | Focuses on "residual income" - the exact cash left over each month after major expenses - rather than just a flat DTI ratio 3637. |

| USDA | U.S. Department of Agriculture | 41% back-end (waivers available for compensating factors) 1415 | 0% | Property must be located in an eligible rural area, and household income must fall below specific regional limits 141536. |

CFPB Regulations and Fair Lending

The regulatory environment also dictates how lenders interact with borrowers and process data. The Consumer Financial Protection Bureau (CFPB) enforces the Equal Credit Opportunity Act (ECOA) and the Fair Housing Act, which strictly prohibit lending discrimination based on race, color, religion, national origin, sex, marital status, or age 38.

Historically, lenders faced regulatory action under ECOA based on "disparate impact" - a legal doctrine where a lender could be penalized if their neutral underwriting policies unintentionally produced statistically worse outcomes for minority borrowers 38. However, a significant finalized rule change by the CFPB, taking effect in July 2026, removed disparate impact liability specifically from ECOA enforcement 38. While intentional discrimination remains unequivocally illegal, and disparate impact claims are still viable under the separate Fair Housing Act, this adjustment narrows the specific enforcement mechanisms regulators use to evaluate lending algorithms 38.

The CFPB also oversees loan originator compensation rules to prevent predatory practices. Following the Great Recession, rules were implemented to stop originators from steering borrowers into unfavorable loans just to earn higher commissions 39. Underwriters and compliance officers must constantly ensure that their company's compensation structures do not inadvertently reward originators differently based on the terms of the specific transaction, ensuring a fair and transparent process for the consumer 40.

The Rise of Artificial Intelligence in Underwriting

Traditionally, mortgage underwriting has been a painstaking, manual process requiring professionals to comb through hundreds of pages of documentation 41. However, the industry is currently undergoing a massive transformation driven by Artificial Intelligence (AI) and intelligent automation 2941.

AI is not replacing the human underwriter; rather, it functions as a high-speed analytical assistant 2141. Modern systems utilize natural language processing and smart document recognition to instantly read tax forms, pay stubs, and bank statements, extracting the exact data points underwriters need while drastically reducing human data-entry errors 212941. This automation allows multi-day document reviews to be completed in seconds 2941.

Beyond speed, AI is revolutionizing risk modeling. Legacy underwriting models relied heavily on static variables like credit scores and basic DTI ratios. Today, machine learning models analyze hundreds of alternative data points - including spending patterns, gig-economy income streams, and regional economic indicators - to produce a highly accurate, holistic view of borrower risk 29. This shift enables "cash-flow underwriting," where algorithms observe deposit frequency and liquidity buffers directly from bank integrations, providing a clearer picture of how a borrower's income behaves under real-world conditions 3.

However, the integration of AI introduces complex compliance challenges. If an AI underwriting algorithm operates as an unexplainable black box, it creates immense legal exposure 106. Under federal adverse action requirements, a lender must be able to explicitly explain the specific factors that led to a loan denial; they cannot simply provide a generic algorithmic rejection 6. Consequently, responsible AI underwriting models are rigorously built to maintain complete explainability, ensuring that every decision can be justified and audited for fair lending compliance 62941.

How Economic Volatility Impacts Loan Approvals

Macroeconomic conditions heavily influence the leniency and strictness of the underwriting process. During periods of economic volatility and rapidly shifting interest rates, lenders tend to become more cautious, tightening their approval standards and demanding deeper income verification and higher cash reserves 24.

The most profound impact of rising interest rates, however, is mathematical disqualification. A study by the Federal Reserve Bank of St. Louis, analyzing over 30 million mortgage applications from 2018 to 2024, revealed a direct and striking correlation between surging interest rates and soaring mortgage denial rates .

When interest rates rise, the projected monthly mortgage payment rises proportionally. For borrowers sitting near the edge of the maximum allowable DTI threshold, a rate increase can instantly push their DTI over the hard regulatory limit . The Federal Reserve's analysis found that during the aggressive 2022-2023 tightening cycle, the surge in loan rejections was almost entirely driven by the cost of capital pushing otherwise stable borrowers past underwriting thresholds . It was not a deterioration in the actual creditworthiness of the applicants that caused the denials, but simply the arithmetic of higher borrowing costs hitting the regulatory wall .

In this way, the mortgage underwriting process acts as a stress-tester for the consumer, analogous to how central banks conduct macroeconomic stress tests on commercial banking institutions 4313. Just as a bank must prove it has sufficient capital to survive an adverse economic scenario, a borrower must prove they have the capacity to absorb the debt obligation under prevailing market rates 113.

International Underwriting: How the U.S. Compares

The exhaustive, heavily regulated 30 to 60-day underwriting process is distinctively American. Mortgage markets in other developed nations operate under vastly different regulatory frameworks, resulting in different timelines and standards 4546.

| Feature | United States | Canada | United Kingdom |

|---|---|---|---|

| Typical Approval Timeline | 45 to 60 days on average due to heavy documentation and regulatory waiting periods 74546. | 2 to 10 days, driven by a highly centralized banking system 464748. | 2 to 6 weeks, depending heavily on the speed of the property valuation and legal conveyancing 4950. |

| Mortgage Term Structure | Commonly fixed for the entire 15 or 30-year life of the loan 51. | Terms are short (e.g., 5 years) and must be re-negotiated over a standard 25-year amortization period 4551. | Initial fixed terms often last 2 to 5 years before reverting to the lender's standard variable rate. |

| Tax Deductibility | Mortgage interest is often tax-deductible for a primary residence 344551. | Not tax-deductible for primary residences 4751. | Not tax-deductible for primary residences. |

| Underwriting Philosophy | Heavy emphasis on historical documentation, specific DTI ratios, and credit bureau scores 346. | Strict federal oversight by OSFI; strong focus on domestic credit history and rigorous stress-testing against future rate hikes 4851. | Focuses on "contextual lending," scrutinizing true net disposable income against lifestyle commitments rather than simple gross salary multiples 5052. |

In Canada, the banking system is highly centralized and regulated federally by the Office of the Superintendent of Financial Institutions (OSFI), which allows major banks to process approvals much faster than the fragmented U.S. system 4851. However, Canadian borrowers face stricter early repayment penalties and must re-qualify for their mortgage rates every few years at the end of their term 4551.

In the United Kingdom, underwriters have recently pivoted heavily toward contextual lending and true affordability 52. UK underwriters deeply scrutinize net disposable income against committed lifestyle costs - such as childcare or private school fees - rather than relying strictly on gross salary multiples 52. Furthermore, aligning with broader sustainability goals, UK underwriters are increasingly factoring in the Energy Performance Certificate (EPC) of a property, potentially reducing loan amounts or increasing rates for homes with poor energy efficiency ratings 52.

Debunking Common Mortgage Myths

Because the underwriting process is multifaceted and often opaque, widespread misconceptions frequently deter otherwise qualified buyers from entering the housing market.

A prevalent myth is the belief that a 20% down payment is an absolute requirement to purchase a home 1914. While putting 20% down is ideal because it eliminates the need for Private Mortgage Insurance (PMI) and lowers the monthly payment, it is not an underwriting mandate 3614. Conventional loan programs allow for down payments as low as 3%, FHA loans require only 3.5%, and specialized programs like VA and USDA loans offer 0% down options for qualified borrowers 3436.

Similarly, many prospective buyers believe they need a flawless credit score to secure an approval 19. While excellent credit certainly yields the most favorable interest rates, underwriters routinely approve borrowers with average or even below-average credit histories 19. Government-backed FHA loans, for instance, are specifically designed to be accessible and can approve borrowers with credit scores down to 580, or even 500 if the borrower provides a 10% down payment 3436.

Another common misconception is that having existing consumer debt completely disqualifies an applicant 19. Underwriters do not expect borrowers to be completely debt-free. Instead, they analyze the ratio of your debt compared to your income 19. As long as the total monthly debt payments, including the new mortgage obligation, fall below the loan program's maximum DTI limit, carrying auto loans or student debt will not prevent a successful approval 19.

Finally, many consumers confuse pre-qualification with a guaranteed loan 1934. A pre-qualification is merely a non-binding estimate based on unverified, self-reported information 36. It is only when the borrower submits formal documentation and the file undergoes the rigorous scrutiny of an underwriter that a true, reliable approval is generated 1936.

Bottom line

The mortgage approval process is a highly structured risk-assessment operation designed to protect both the financial institution and the borrower from the severe consequences of default. By meticulously verifying a borrower's capacity to repay, analyzing their credit history, and confirming the property's value, underwriters ensure that the loans they originate are mathematically sustainable. While the integration of artificial intelligence is accelerating the mechanical aspects of document processing, the core requirement for borrowers remains unchanged: you must maintain absolute financial stability during the entire application period. Buyers who protect their credit, preserve their cash reserves, and avoid taking on new debt will find the complex journey from pre-approval to the closing table far more predictable.