How a Bank Run Unfolds Day by Day

When a bank faces a sudden crisis of confidence, panicked depositors race to withdraw their funds, rapidly depleting the institution's liquid cash reserves. This triggers a frantic, highly choreographed timeline where regulators covertly seize the insolvent bank - typically on a Friday evening - and spend the weekend restructuring it so customers can access their insured money by Monday morning.

The Anatomy of a Banking Panic

A bank run is a fundamental risk embedded deeply in the architecture of the modern financial system. Because commercial banks operate on a fractional-reserve basis, they only keep a small percentage of their total customer deposits on hand as liquid cash. The vast majority of the money is lent out to borrowers - such as homebuyers and small businesses - or invested in longer-term securities like government bonds to generate a yield 12.

When economic conditions are stable, this mechanism, known as maturity transformation, functions smoothly. The bank borrows money on a short-term basis from its depositors and lends it out on a long-term basis. However, if depositors suddenly lose faith in the bank's solvency, they will attempt to pull their money out simultaneously. Because the bank's assets are tied up in long-term loans and bonds, it physically does not have the liquid cash in its vaults or central bank reserves to satisfy all withdrawal requests at once.

Financial historians and economists often compare the psychology of a bank run to someone yelling "fire!" in a crowded theater 343. Even if the threat of a fire is merely an unfounded rumor, the most rational action for any single individual in that theater is to rush for the exit immediately. If a person waits to verify the rumor, they risk being trampled or trapped. In the context of banking, this translates to the fear that if you are not the first in line to withdraw your funds, the institution will run out of cash before it processes your account 6. Once this psychological threshold is crossed, the panic becomes a self-fulfilling prophecy.

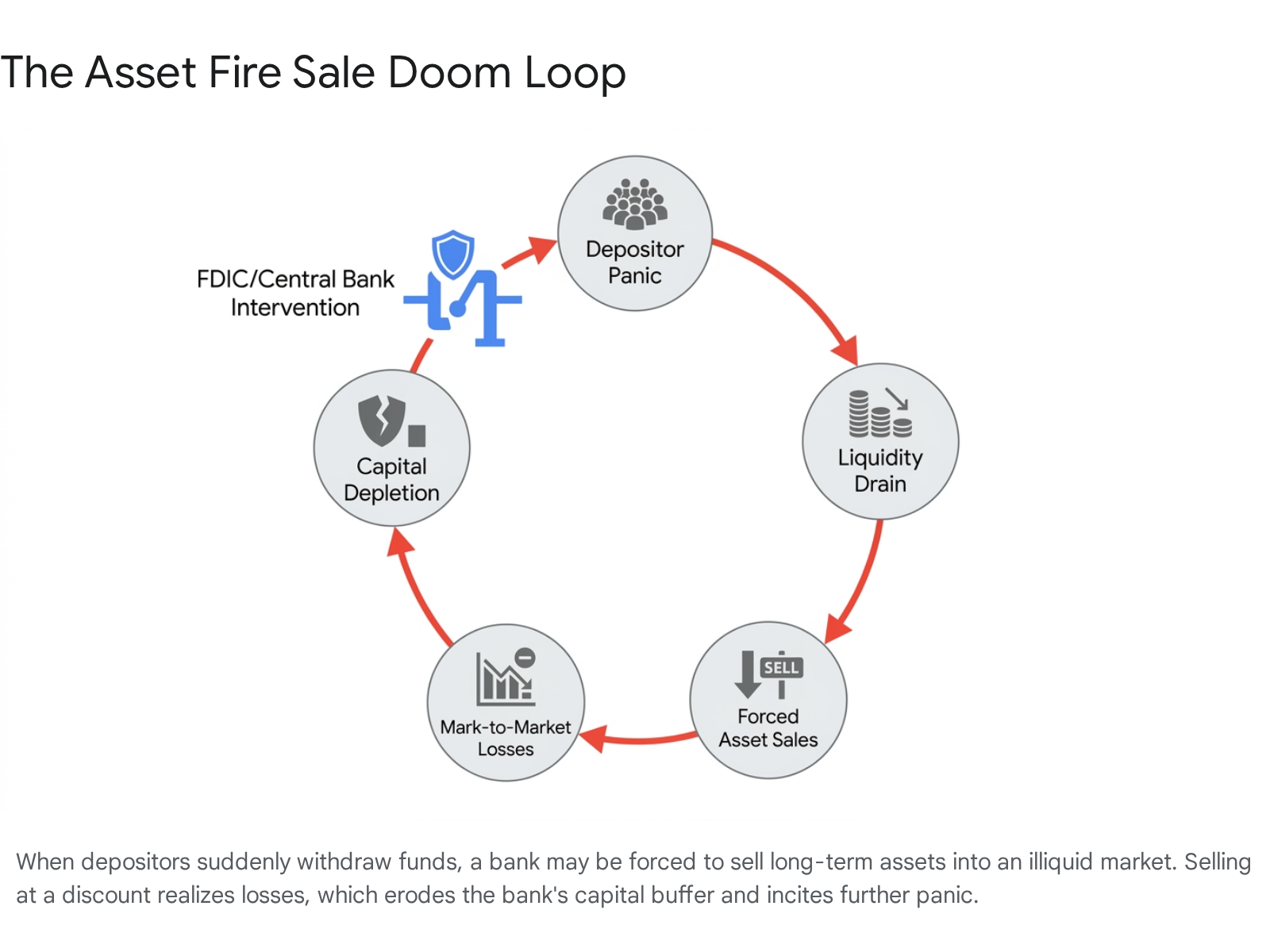

The Contagion of Asset Fire Sales

When a bank begins bleeding deposits rapidly, it must find cash immediately. If its highly liquid cash reserves are exhausted, the bank is forced to sell its longer-term investments - such as government Treasury bonds or mortgage-backed securities - on the open market.

If this forced liquidation happens during a period of broad economic stress or rising interest rates, the market value of those bonds may be significantly lower than the price the bank originally paid for them. Selling these assets under extreme duress is known as an "asset fire sale" 74. Fire sales create a vicious, destabilizing cycle: selling assets at a steep discount forces the bank to realize massive financial losses, which eats directly into its equity capital 49. As word spreads that the bank's equity is evaporating and its solvency is threatened, even more depositors panic and demand their money, accelerating the doom loop.

Furthermore, fire sales create what macroeconomists refer to as a "pecuniary externality" 795. When one massive financial institution floods the market with distressed assets, the overall market supply surges, driving the price for those specific assets down for everyone else. Other, entirely healthy banks holding those identical securities suddenly see the value of their own portfolios decline, putting their balance sheets under pressure 96. This mechanism is a primary driver of systemic risk; it explains how a localized problem at a single regional bank can rapidly contaminate the entire global financial system.

Day by Day: The Timeline of a Bank Run

While the underlying vulnerabilities that cause a bank to fail - such as poor risk management, toxic asset accumulation, or unhedged interest rate exposure - often fester in the dark for months or years, the actual run that kills the institution usually plays out in the public eye over a matter of days.

Using historical regulatory protocols and the documented progression of recent events, such as the March 2023 collapse of Silicon Valley Bank (SVB), we can accurately map out the typical day-by-day timeline of a modern banking crisis.

The Incubation Period: Accumulating Risk

Long before the panic begins, the foundation for a bank run is laid by structural imbalances. In the years leading up to the 2023 crisis, many institutions benefited from a period of exceptionally low interest rates and a boom in the technology sector 7. Deposits surged, and banks invested heavily in long-term securities.

The fatal flaw emerges when macroeconomic conditions shift. As central banks begin to raise interest rates to combat inflation, the value of older, lower-yielding bonds falls. Banks carrying large portfolios of these bonds begin to accumulate massive unrealized losses 78. Concurrently, if a bank relies heavily on uninsured deposits - accounts holding more than the Federal Deposit Insurance Corporation (FDIC) protected limit of $250,000 - it becomes acutely vulnerable. Uninsured depositors know they will take losses if the bank fails, making them highly sensitive to bad news 910.

Day 1: The Wednesday Whisper

Most modern bank runs are triggered by a distinct catalyst event that inadvertently exposes the bank's hidden vulnerabilities to the broader market. This often happens mid-week, frequently on a Wednesday, when banks release unexpected financial disclosures.

The catalyst is usually an attempt by bank management to fix a worsening balance sheet. For instance, on Wednesday, March 8, 2023, SVB announced a massive restructuring 7. The bank revealed it had sold $21 billion in available-for-sale (AFS) securities to generate liquidity, taking a devastating $1.8 billion after-tax loss in the process 7. To plug this massive hole in its capital, the bank announced a desperate intention to raise $2.25 billion by selling new shares to investors 7.

Simultaneously, the bank disclosed that major credit rating agencies, such as Moody's and S&P, were considering negative downgrades to the bank's debt 7. To institutional depositors and sophisticated venture capital investors paying close attention to financial filings, this Wednesday announcement was the equivalent of smelling smoke in the theater. It signaled that the bank was bleeding cash and struggling to survive.

Day 2: The Thursday Stampede

Historically, bank runs required customers to line up physically outside branch doors, which placed a natural, physical limit on how fast money could leave the institution. Today, panic moves at the speed of social media, and money moves at the speed of digital wire transfers 1112.

By Thursday morning, rumors of insolvency tear through private messaging networks, Slack channels, and investor group chats. Because commercial clients and high-net-worth individuals hold uninsured funds, they recognize that staying loyal to the bank carries catastrophic financial risk 910. A coordinated exodus begins.

The ensuing digital run can be historically unprecedented in its velocity. On Thursday, March 9, 2023, SVB depositors withdrew more than $40 billion in a single business day 713. By the close of business that Thursday evening, bank management informed federal supervisors that their liquidity was completely exhausted and they expected an additional $100 billion in withdrawal requests the following morning 713. The stampede effectively kills the bank before the week is over.

Day 3: The "Friday Night" Closure

When a bank crosses the threshold of insolvency - meaning it cannot meet its obligations or pay out requested withdrawals - state and federal regulators must step in. In the United States, the FDIC is the primary agency tasked with resolving failed depository institutions 2014.

To prevent widespread, uncontrollable panic in the financial markets, the FDIC almost exclusively executes bank closures on Friday evenings 141523. This "Friday night" playbook is a deliberate strategy. It allows the agency to utilize the weekend, when markets are closed and transaction volumes drop, to secure the bank's assets, process complex data, and arrange a transition before Monday morning 1524.

The operation is highly orchestrated and fiercely confidential. FDIC closing teams - consisting of specialized accountants, asset managers, and financial investigators - will travel to the failing bank's headquarters. To avoid alerting the local media or spooking depositors, they often check into nearby hotels under fictitious corporate names, such as "CB and Associates" 14.

The moment the chartering authority (either a state regulator or the Office of the Comptroller of the Currency) officially revokes the bank's charter on Friday afternoon, the FDIC steps in as the legal receiver 2024. The transition of power is instantaneous and absolute.

According to internal FDIC closing procedures, several immediate actions occur: * Securing the Premises: FDIC agents walk into the bank's branches at the close of business, taking immediate physical custody of the premises, the vaults, all financial records, and physical assets 1424. * Freezing the Ledger: All deposit accounts are temporarily frozen at the exact moment of failure. This is critical so the FDIC can accurately calculate insured balances without numbers shifting. Any checks or electronic payment requests presented after the closure are returned unpaid 16. * Staff Briefings: The FDIC's newly appointed Receiver-in-Charge holds an immediate meeting with the failed bank's employees. They explain the strict weekend protocols, mandate overtime, and reveal the name of the assuming institution if a buyer has already been secured 26. * Contract Review: Legal specialists immediately begin reviewing qualified financial contracts and unfunded loan commitments, deciding which agreements the FDIC will honor and which it will disaffirm 2326.

Days 4 & 5: The Resolution Weekend

Behind the locked doors of the failed bank, the FDIC works through the weekend under a strict legal mandate to resolve the institution using a "least-cost analysis" 23. This federal requirement dictates that the agency must choose the resolution path that results in the smallest possible financial loss to the Deposit Insurance Fund (DIF) 2324.

During the weekend, the FDIC essentially acts as an investment banker, evaluating bids and pursuing two primary options:

| Resolution Method | Description | Typical Outcome for Depositors |

|---|---|---|

| Purchase and Assumption (P&A) | A healthy, open bank acquires the failed bank, assuming its insured deposits and purchasing a portion of its assets. | Seamless transition. Depositors become customers of the acquiring bank with uninterrupted access to insured funds. |

| Deposit Payoff | No buyer is found. The FDIC acts as liquidator, paying depositors directly for their insured balances via check. | Access to insured funds within a few days. Uninsured funds become a claim against the liquidated assets. |

| Bridge Bank | The FDIC creates a temporary, government-run national bank to maintain critical operations while seeking a permanent buyer. | Uninterrupted access to funds, but under temporary government management until a sale is finalized. |

The Purchase and Assumption (P&A) transaction is the overwhelmingly preferred method 1516. Between 2007 and 2017, the FDIC successfully used this method in 97% of all bank failures 15. The primary advantage of a P&A is that it is virtually invisible to the retail customer; the failed bank's branches simply reopen on Monday under the branding of the acquiring institution 14.

If the FDIC cannot find a willing buyer who submits an acceptable bid over the weekend, it must execute a Deposit Payoff 1516. The agency cuts checks directly to depositors for their insured balances up to $250,000 16. For amounts exceeding the insurance limit, the FDIC issues a "receivership certificate" to the depositor 2024. This certificate acts as an unsecured legal claim on the failed bank's remaining assets. As the FDIC slowly sells off the bank's loan portfolio, real estate, and office equipment over the coming months and years, these uninsured depositors receive periodic dividend payments, eventually recovering a percentage of their lost funds 1527.

Day 6: Monday Morning Reopening

Regardless of the resolution method chosen over the weekend, federal law dictates that the FDIC must make insured funds available to depositors "as soon as possible" 28.

Despite a persistent, anxiety-inducing internet myth that the FDIC has up to 99 years to return insured money, there is no such timeline in reality. The FDIC's explicitly stated goal - which it routinely meets with high efficiency - is to provide access to insured deposits within one business day if the bank fails on a Friday, or two business days if the failure occurs mid-week 16281718.

When Monday morning arrives, the outcomes for the public diverge based on the weekend's events: * If a buyer was found (P&A): Depositors wake up as customers of the acquiring bank. They can log into their accounts, use their existing debit cards, write checks, and access their full insured balances immediately as if nothing happened 201416. * If a bridge bank was formed: In the case of massive, complex failures, the FDIC may establish a bridge bank. Customers can access their funds and conduct business as usual on Monday while the FDIC takes extra time to market the institution 81031. * If a direct payoff occurred: Checks for the insured balances are typically mailed within a few days of the Friday closing 1516. Customers who held items in safe deposit boxes are contacted on Monday with instructions on how to physically retrieve their belongings 16.

A Tale of Three Crises: How Bank Runs Are Changing

The fundamental psychology of a bank run - fear, contagion, and the rush for liquidity - has remained unchanged for centuries. However, the mechanics, the speed of capital flight, and the regulatory responses have evolved dramatically in the digital age. Comparing three high-profile bank runs illustrates this profound shift.

The Analog Run: Northern Rock (2007)

In August 2007, the UK-based mortgage lender Northern Rock found itself in severe distress. The bank's business model relied heavily on short-term wholesale funding to finance aggressive, long-term mortgage lending 1933. When the global credit markets began to freeze due to early subprime mortgage fears, Northern Rock was unable to roll over its short-term debt 193320.

On September 13, news leaked via the BBC that Northern Rock had requested emergency liquidity support from the Bank of England 2021. This public confirmation of distress triggered the UK's first major bank run in over a century 33. But because this was 2007, the run was decidedly analog. Panicked retail customers physically queued outside branch doors across the country 192122. The bank's website crashed under the traffic, and its phone lines jammed 20.

Despite the intense, highly televised visual of people lining up around city blocks, the actual pace of the capital withdrawal was relatively slow by modern standards. Over several days of intense panic, depositors withdrew £4.6 billion - roughly 5% of the bank's total deposit base 192022. The UK government eventually had to step in and guarantee all retail deposits to stem the tide, ultimately leading to the bank's formal nationalization in early 2008 332122.

The Digital Flash Run: Silicon Valley Bank (2023)

By stark contrast, the collapse of Silicon Valley Bank sixteen years later demonstrated the terrifying velocity of a modern digital bank run.

SVB's clientele was highly concentrated, consisting largely of venture capitalists, tech startup founders, and crypto-asset firms. These individuals were highly networked, communicated constantly on social media, and utilized sophisticated online banking tools 12. When the bank announced its balance sheet restructuring on March 8, 2023, there were no physical lines. Instead, a coordinated group of institutional depositors utilized corporate treasury software to wire money out simultaneously .

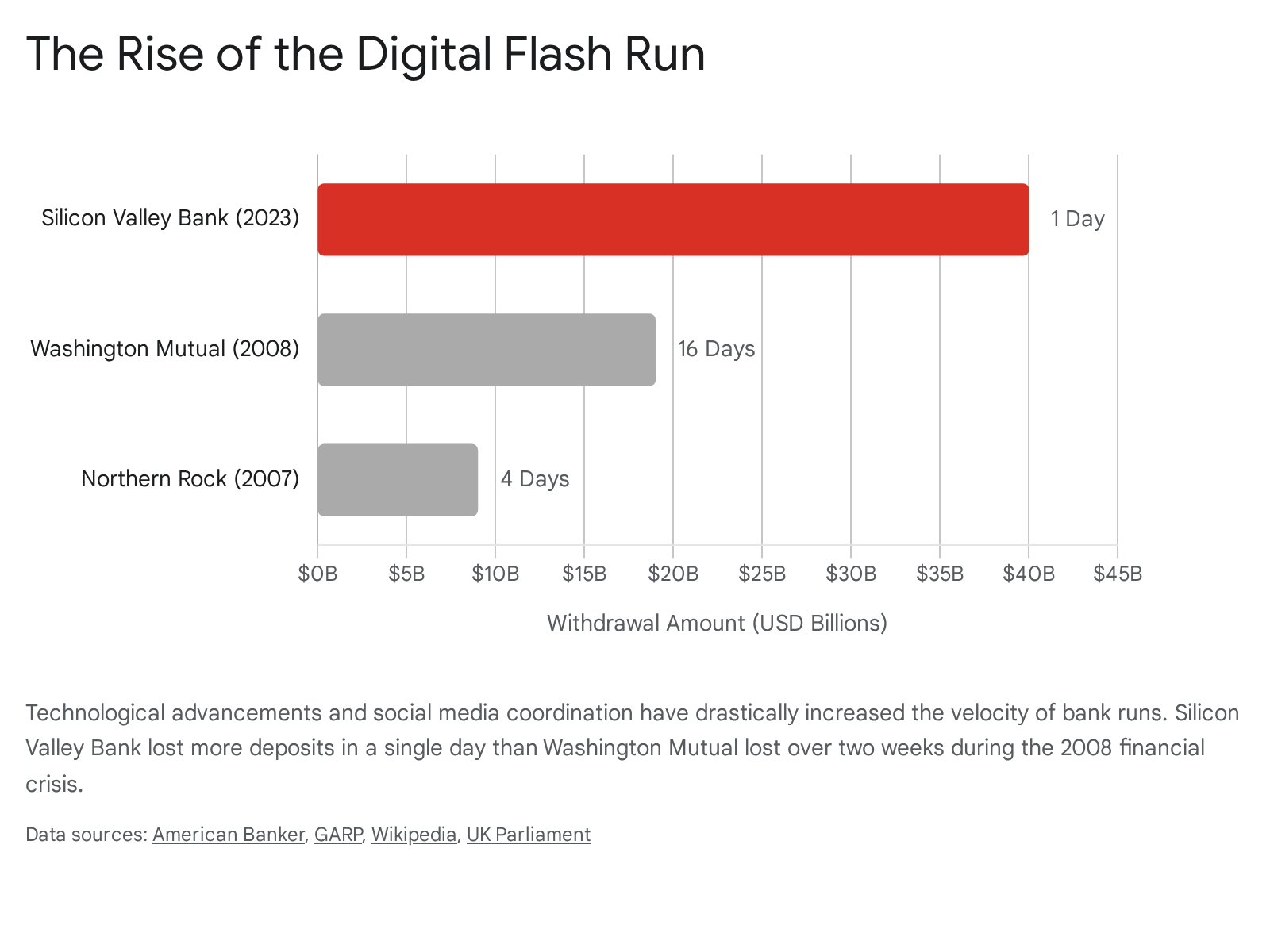

The capital flight was instantaneous. $40 billion evaporated from the bank's digital ledgers in a matter of hours 713. To contextualize this speed: during the 2008 collapse of Washington Mutual (the largest bank failure in US history prior to 2023), it took 16 agonizing days for depositors to withdraw $19 billion 11. SVB lost more than double that amount in less than 24 hours.

The Global Bail-In: Credit Suisse (2023)

While SVB was a massive regional bank, the run on Credit Suisse that same month presented a profoundly more dangerous scenario: the potential failure of a Global Systemically Important Bank (G-SIB) 2324.

Credit Suisse had suffered years of reputational damage, executive turnover, and staggering financial losses stemming from scandals, notably the collapse of the Archegos Capital family office 2339. Despite holding a massive regulatory liquidity buffer of CHF 230 billion in high-quality liquid assets in late 2022, investor confidence was incredibly fragile 2526. When SVB failed in the US, the panic immediately jumped the Atlantic 25. Following a delayed financial report and a highly publicized statement by its largest shareholder refusing further capital injections, Credit Suisse faced an unstoppable, global wave of withdrawals 2526.

Because Credit Suisse was globally systemic, a traditional FDIC-style closure was considered wildly dangerous; allowing it to collapse into disorganized bankruptcy could have triggered a global depression 2427. Swiss regulators (FINMA) had spent over a decade preparing a "bail-in" resolution plan for exactly this scenario. Under a bail-in framework, the bank remains open, but its unsecured bondholders and shareholders are wiped out. Their debt is converted into new equity, instantly recapitalizing the bank without requiring taxpayer funds 2526.

However, as the run reached its peak over the weekend of March 18-19, 2023, the firm hit the point of non-viability (PONV) 2526. Swiss authorities determined that executing a full bail-in was too risky amidst the panicked global environment, fearing unpredictable market impacts 27. Instead, the Swiss government bypassed its own meticulously crafted resolution playbook. Utilizing emergency legislation and a CHF 200 billion liquidity backstop from the Swiss National Bank (SNB), they brokered an emergency commercial merger, forcing the rival bank UBS to acquire Credit Suisse 2427.

To make the financial math of the acquisition work for UBS, FINMA controversially ordered the complete, contractual write-down of CHF 16 billion in Additional Tier 1 (AT1) capital bonds 2527. This action effectively wiped out those specific institutional investors entirely, preserving the broader stability of the global financial system while highlighting the unpredictable nature of crisis management.

Historical Comparison of Banking Crises

| Feature | Northern Rock (2007) | Silicon Valley Bank (2023) | Credit Suisse (2023) |

|---|---|---|---|

| Systemic Status | Domestic UK Mortgage Lender | Large US Regional Bank | Global Systemically Important Bank (G-SIB) |

| Primary Catalyst | Freezing of wholesale funding markets due to US subprime exposure | Unrealized losses on government bonds exacerbated by rising interest rates | Years of reputational damage and scandals compounded by the SVB panic |

| Velocity of the Run | Slow; £4.6 billion withdrawn over several days | Flash; $40 billion withdrawn in hours via digital transfers | Severe; required $50 billion+ in emergency central bank liquidity |

| Resolution Strategy | Temporary public ownership (Nationalization) | FDIC Receivership, Bridge Bank, and ultimate sale | State-brokered emergency commercial merger with UBS |

| Investor Impact | Shareholders wiped out; bank eventually returned to private sector | Shareholders and executives wiped out | Shareholders diluted; AT1 bondholders wiped out completely (CHF 16bn) |

How Regulators Protect the Financial System

When a bank run threatens to spill over into the broader economy, regulatory bodies have several powerful tools at their disposal to halt the contagion and restore market confidence.

Expanding Deposit Insurance and Systemic Risk Exceptions

In the United States, the baseline defense against bank runs is the FDIC, which guarantees deposits up to $250,000 per depositor, per institution, per ownership category 2728. This elevated limit was made permanent by the Dodd-Frank Act following the 2008 crisis specifically to foster unshakeable confidence among retail depositors 28.

However, during the SVB collapse, it became immediately apparent that strictly enforcing the $250,000 cap would lead to the financial destruction of thousands of technology startups and venture capital firms. Regulators feared this would trigger secondary runs on dozens of other regional banks holding similarly high concentrations of uninsured corporate deposits 810.

Consequently, the Secretary of the Treasury, the Federal Reserve, and the FDIC jointly invoked a rare "systemic risk exception." They announced on Sunday night that all depositors at SVB and the similarly afflicted Signature Bank - even those holding tens of millions of dollars - would be made entirely whole and have full access to their funds by Monday morning 82844. Crucially, the authorities stated that the funds to cover these massive uninsured deposits would come from a special assessment levied on the banking industry, ensuring that direct taxpayer funds were not used for the bailout 844.

The Central Bank as Lender of Last Resort

To prevent the devastating cycle of asset fire sales, central banks are designed to act as a "lender of last resort" 13. If a solvent bank needs cash to pay panicked depositors, it can borrow directly from the Federal Reserve by pledging its assets as collateral, rather than being forced to sell those assets at a steep loss in the open market 2.

Following SVB's failure, the Federal Reserve created a novel emergency facility called the Bank Term Funding Program (BTFP) 2. This facility allowed banks to pledge their high-quality government bonds as collateral and receive cash loans equal to the original face value of those bonds, rather than their severely depressed market value 2. By doing so, the Fed essentially neutralized the threat of asset fire sales. It reassured the public and the markets that banks had access to enough immediate cash to meet all withdrawal demands without destroying their equity capital 228.

Resolution Planning: The "Living Wills"

To ensure that even the largest, most complex banks can be dismantled without crashing the global economy, regulatory frameworks enacted since 2008 require major institutions to draft comprehensive "Resolution Plans," colloquially known as living wills 182329.

The FDIC periodically updates the rules surrounding these plans, known as the IDI (Insured Depository Institution) Rule 2930. Under these guidelines, banks with over $50 billion or $100 billion in total assets are required to submit highly detailed operational roadmaps outlining how they could be safely sold or liquidated over a single weekend 183147. The frequency of these filings is tightly managed; the largest institutions, or Group A CIDIs (Covered Insured Depository Institutions), file triennially, while affiliates of U.S. G-SIBs file biennially 3047.

The ultimate goal of resolution planning is to ensure the FDIC possesses the architectural blueprints, IT system maps, and financial data necessary to execute a Friday night takeover smoothly 183129. By forcing banks to prove their "resolvability" during peacetime, regulators aim to avoid the ad-hoc chaos, taxpayer bailouts, and systemic panic that have historically characterized weekend banking crises 1831.

Bottom line

A bank run is a devastating crisis of confidence where depositors collectively attempt to withdraw more cash than a financial institution physically holds. While the underlying psychology remains the same, modern digital runs happen with terrifying speed, forcing regulators to execute complex, covert takeovers over a single weekend to prevent systemic contagion. While investors, bondholders, and executives frequently lose their capital when a bank fails, aggressive interventions by the FDIC and central banks are designed to ensure that the broader financial system survives and that everyday depositors retain uninterrupted access to their insured funds.