How AI Flags Credit Card Fraud Step by Step

When a consumer initiates a digital payment, a global network of artificial intelligence models analyzes the transaction, scores its risk, and determines whether to approve or decline it in under 300 milliseconds. Rather than examining the specific items purchased, these models evaluate hundreds of contextual metadata points, device fingerprints, and behavioral patterns to accurately spot anomalies. This rapid, probabilistic decision-making prevents billions of dollars in losses while minimizing friction for legitimate shoppers.

The Scale of the Digital Payment Ecosystem

The transition from cash-based economies to digital payments has revolutionized global commerce, but it has simultaneously created an expansive surface area for financial crime. In 2024, nationwide credit card transactions in the United States alone totaled an estimated 56.2 billion, while total global credit card transactions reached an estimated 791 billion 1. This equates to an average of more than 25,000 global transactions occurring every single second 1.

With the average U.S. cardholder making 257 credit card transactions per year, the sheer volume of digital money movement is staggering 1. Major payment processors handle the bulk of this volume; Visa processed roughly 293 billion global payment transactions in the 2024 calendar year, while Mastercard processed an estimated 197 billion 1.

However, this convenience carries a severe financial risk. Global credit card fraud losses reached $32.3 billion in 2023, with projections indicating that the figure could exceed $40 billion by 2026 and reach $41.06 billion by 2030 23. Financial institutions face sophisticated, automated threats ranging from phishing and identity theft to massive enumeration attacks - where botnets rapidly test stolen credentials to exploit vulnerabilities at unprecedented scale 42. In response to these mounting threats, the financial industry has largely abandoned manual reviews and rigid, traditional software in favor of advanced artificial intelligence frameworks capable of rendering real-time, adaptive judgments 6.

The Hidden Architecture of an Authorization

To the modern consumer, tapping a contactless card or clicking a checkout button feels instantaneous. Yet, in the blink of an eye, a complex digital negotiation takes place across global networks. A standard card payment requires seamless collaboration between five core entities: the cardholder, the merchant, the acquirer (the merchant's bank), the card network (such as Visa or Mastercard), and the issuer (the cardholder's bank) 78.

At its core, payment authorization is the process of verifying that a customer has sufficient funds or credit and that the transaction itself is legitimate 9. When a customer presents a card, the merchant's payment gateway captures the sensitive data, encrypts it, and translates the request into an ISO 8583 message 89. ISO 8583 is the universal standard protocol for financial transaction messaging, consisting of a Message Type Indicator (MTI), bitmaps that act as a table of contents, and specific data elements detailing the transaction 89.

The gateway routes this structured message to the acquiring bank, which then forwards it to the appropriate card network 73. The network acts as the central hub, identifying the issuing bank and routing the authorization request to them 93. The issuing bank receives this request and must perform a rapid-fire series of checks, evaluating the validity of the card, the available balance, the cryptographic security (such as the EMV cryptogram or CVV), and the likelihood of fraud 7. Finally, the issuer returns a decision - either approved with an authorization code or declined with an error code - which travels back down the chain to the merchant terminal 4.

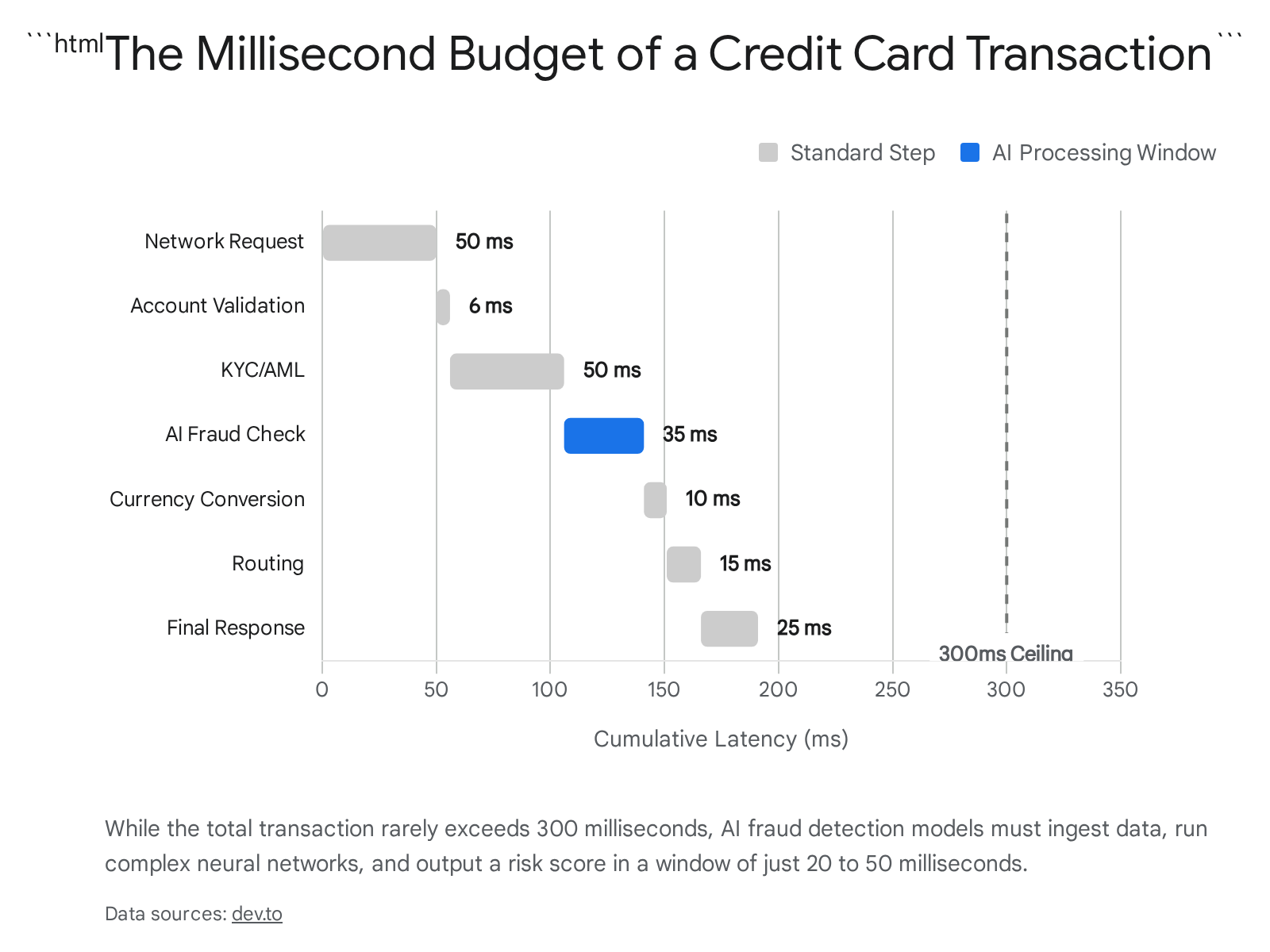

The Strict Latency Budget

This entire digital round trip must complete in milliseconds. For business analysts and systems engineers designing these platforms, latency is the primary concern, as every millisecond of delay dramatically increases the risk of checkout abandonment and degrades the customer experience 912. The industry standard service-level agreement (SLA) for end-to-end payment authorization is typically capped at around 300 milliseconds 125.

Latency in this context breaks down into two distinct components: network latency and processing latency 12. Network latency refers to the physical time it takes for data packets to traverse global fiber-optic cables and bounce between the various institutions' servers. Processing latency, conversely, is the "hidden" computational work that happens while the data is at rest inside a system 12.

During a typical transaction, processing latency consumes the bulk of the timeline. The system must perform account validation, Anti-Money Laundering (AML) and Know Your Customer (KYC) compliance checks, currency conversion calculations, optimal payment rail routing, and sophisticated fraud detection 12. In a modern transaction, the artificial intelligence fraud detection engine is allocated a remarkably narrow window - often between 20 and 50 milliseconds - to ingest a year's worth of historical context, evaluate the current metadata, and render a precise mathematical judgment regarding the transaction's legitimacy 1256.

The Metadata Misconception: What AI Actually Analyzes

When a transaction is inexplicably declined at the point of sale, a common misconception among consumers is that the bank recognized the specific items being purchased and deemed the shopping cart contents suspicious 1516. However, the reality of payment processing is fundamentally different.

The vast majority of consumer credit card transactions operate on "Level 1" or "Level 2" data processing 1516. These levels transmit only basic metadata: the total transaction amount, the date and time, the merchant's name, and standard tax indicators 16. Itemized receipt data - which lists individual products, brands, and prices - is known as "Level 3" data 1516. Level 3 processing is highly specialized, strictly reserved for massive business-to-business (B2B) transactions, corporate procurement cards, and government contractors 1617. Consumer credit card networks generally do not receive, nor do they process, item-level data 1617.

Therefore, AI fraud detection models operate entirely blind to the actual items in a consumer's shopping cart. Instead, the AI must construct a highly accurate profile of intent relying entirely on transaction metadata, device intelligence, and merchant classification 18.

The Critical Function of Merchant Category Codes (MCC)

Because the AI cannot see the items being purchased, it relies heavily on the Merchant Category Code (MCC) to establish the context of a transaction. An MCC is a four-digit numerical identifier assigned to a business by credit card networks to classify the primary type of goods or services it provides 19207. The acquiring bank and payment processors collaborate to assign this code when a business first establishes its payment infrastructure 19.

MCCs are foundational to the payment ecosystem. They dictate the interchange fees merchants pay, influence credit card reward programs (e.g., granting double points for transactions at gas stations or restaurants), and trigger specific regulatory compliance pathways 208. Crucially, MCCs serve as immediate, high-priority signals for fraud detection engines 1920.

Different business models carry inherently different risk profiles. Financial institutions continuously monitor transaction data, comparing real-time events against known behavioral patterns associated with specific MCCs 20.

| Example Merchant Category Code (MCC) | Business Classification | Fraud Risk Profile |

|---|---|---|

| 5411 | Supermarkets and Grocery Stores | Lower risk. High frequency, localized, essential consumer spending. |

| 5942 | Books and Media | Lower risk. Generally lower transaction values and lower resale value on the black market. |

| 5094 | Precious Stones and Jewelry | Higher risk. High transaction values, easily resalable, frequent target for stolen card testing. |

| 6051 | Digital Currency / Crypto Services | Highest risk. Subject to strict compliance monitoring; highly targeted by automated botnets and scammers. |

| 7995 | Gambling and Betting | Highest risk. Strictly regulated, prone to money laundering and high chargeback rates. |

Table data synthesized from industry risk classification models 198.

If a customer's historical spending behavior primarily consists of transactions at local grocery stores (MCC 5411) and bookstores (MCC 5942), and their card suddenly attempts a $5,000 transaction at an overseas digital currency exchange (MCC 6051), the AI's risk models will immediately flag the metadata anomaly 19208.

The stakes for proper MCC categorization are incredibly high. A payment network's risk tolerance is directly tied to these codes. Visa, for example, categorizes specific high-risk merchants into distinct tiers under its Visa Integrity Risk Program (VIRP), carefully monitoring sectors like digital file sharing, card-absent crypto, and adult content 9. If an acquiring bank accidentally or intentionally misclassifies a high-risk merchant with a low-risk MCC to bypass strict fraud filtering or secure lower processing fees, the payment networks can levy severe financial assessments 79. Regulatory risk management firms have reported fines reaching upwards of seven digits against acquiring banks for MCC miscodings 9.

The Evolution of Defense: Rules-Based Logic vs. Machine Learning

To fully comprehend the sophistication of modern AI fraud detection, it is essential to examine the legacy systems it replaced. For decades, enterprise risk management was governed by rules-based software engines 2425.

Rules-based systems function on rigid, deterministic "if-then" logic engineered by human analysts 242526. An analyst reviewing historical fraud patterns might write a rule stating: If a transaction exceeds $10,000, and the shipping address does not match the billing address, block the transaction immediately 242510.

While these deterministic systems were effective during the early days of e-commerce, they suffer from fatal flaws in the modern, high-velocity digital economy. Fraudsters adapt to static rules quickly. If a criminal syndicate discovers that a bank blocks international transfers over $1,000, they will simply program their automated scripts to rapidly process thousands of transactions for $999 2628. Rules-based systems fail to anticipate these new threats, as they require manual human intervention and software updates to recognize novel attack vectors 242629.

Furthermore, static thresholds lack contextual awareness. A rigid rule cannot distinguish between a malicious actor attempting an account takeover and a legitimate customer logging in from a new smartphone while traveling abroad 26. This inherent lack of nuance historically resulted in an unacceptable volume of false positives - legitimate transactions improperly blocked due to overlapping, clumsy rules 252611.

The Probabilistic Revolution

The paradigm shifted with the advent of machine learning (ML). Unlike deterministic rules, machine learning employs a probabilistic approach 31. Instead of checking a transaction against a hard-coded list of conditions, the AI asks, "Based on millions of historical outcomes involving similar contextual parameters, what is the mathematical probability that this specific transaction is fraudulent?" 2631.

Machine learning models ingest massive datasets to uncover hidden patterns, subtle anomalies, and complex, non-linear relationships that are entirely invisible to human analysts 2431. Most importantly, these models leverage adaptive learning 1132. As they process new data, the algorithms continuously self-retrain, independently adjusting their risk parameters to account for evolving fraud tactics without waiting for a human to write a new rule 25113312. This enables the AI to recognize "unknown-unknowns" - brand-new, zero-day fraud patterns that have no established historical precedent 29.

| Defense Mechanism | Traditional Rules-Based Systems | Machine Learning (AI) Systems |

|---|---|---|

| Core Logic | Deterministic (Static If/Then conditions) | Probabilistic (Dynamic risk scoring based on historical outcomes) |

| Adaptability | Reactive; requires manual updates by fraud analysts | Proactive; continuously self-updates through adaptive learning |

| Data Utilization | Limited to predefined, human-selected parameters | Analyzes thousands of aggregate signals and hidden correlations |

| False Positive Rate | Extremely high; rigid rules blindly block anomalous but valid behavior | Significantly lower; understands behavioral nuance and intent |

| Scale | Struggles under high transaction volumes; rules become unmanageable | Scales effortlessly; performance improves as data volume increases |

Comparison based on core architectural differences in enterprise fraud management 24252631.

Inside the AI Engine: The Algorithmic Pipeline

When a consumer's transaction enters the payment gateway, it triggers a highly choreographed sequence of data science operations. To execute a complex risk assessment in a fraction of a second, the AI must undergo extensive preparatory training and utilize optimized real-time infrastructure.

Step 1: Data Preparation and Solving the Imbalance Problem

Before an AI model can identify fraud, it must be trained on vast troves of historical data. However, the nature of financial fraud presents a unique mathematical challenge for data scientists: extreme class imbalance 1336.

In any given financial dataset, fraudulent transactions represent a microscopic fraction of the total volume - often significantly less than 1% 133637. If a neural network is trained on this raw, highly skewed data, it will likely suffer from the accuracy paradox. Because the vast majority of transactions are legitimate, the model can simply learn to guess "Not Fraud" every single time and still achieve an accuracy metric exceeding 99% 13. While highly "accurate," this model is functionally useless because it has failed to learn the minority class - the actual fraudulent behavior 1336.

To force the AI to recognize malicious activity, engineers must manipulate the training data. This is frequently achieved through a technique known as SMOTE (Synthetic Minority Over-sampling Technique) 133738. SMOTE analyzes the existing sparse examples of fraud and uses statistical interpolation to generate new, synthetic examples of fraudulent behavior 3714. By artificially inflating the presence of the minority class, the dataset is balanced, allowing the AI to successfully learn the nuanced boundary lines between legitimate and criminal intent 133738.

Beyond balancing the data, advanced platforms utilize sophisticated feature engineering. Stripe's Radar system, for instance, trains its models to generate "embeddings" for every merchant on its network 15. These embeddings plot merchants into a multi-dimensional coordinate space based on their transaction patterns. The AI quickly learns that ride-sharing apps like Uber and Lyft are statistically similar, while a B2B software company like Slack occupies a different behavioral space 15. By structuring the data this way, if the AI detects a novel fraud attack targeting Uber, it can instantly transfer that defensive knowledge to protect Lyft, leveraging network-scale intelligence 15.

Step 2: Real-Time Inference and Millisecond Execution

With the models trained and deployed into the production environment, the system is ready to evaluate live transactions. Because latency is the enemy of commerce, the AI infrastructure is heavily optimized for speed. When a payment request hits the API, the system instantly retrieves the user's historical state - such as the frequency of specific IP addresses or device identifiers associated with that card - and feeds these features into the machine learning models 41.

Financial institutions do not rely on a single algorithm; rather, they deploy an ensemble of models operating simultaneously. Support Vector Machines (SVM) draw optimal hyperplanes to separate high-dimensional data, while Random Forests leverage decision trees to quickly classify behavioral patterns 43738. For highly complex, non-linear fraud sequences, Deep Neural Networks (DNN) and Recurrent Neural Networks (RNN) are employed 42837.

These models excel at behavioral analytics, moving beyond mere identity verification to evaluate psychometric intent 64243. The AI examines subtle nuances: the typing rhythm of the user, the screen resolution of the device, sudden shifts in geolocation, the velocity of the transaction compared to historical baselines, and network telemetry 6294243.

The speed and scale of these evaluations are immense. Stripe's Radar evaluates over 1,000 distinct signals for every transaction, outputting a highly accurate verdict in under 100 milliseconds 4144. Visa's Advanced Authorization (VAA) operates even faster; trained on more than 15 billion VisaNet transactions, the VAA artificial intelligence model analyzes up to 500 unique risk attributes and generates a real-time risk score in a window of roughly 1 to 20 milliseconds 2616.

Step 3: Risk Scoring and The Final Decision

The final output of this algorithmic pipeline is a precise, contextualized risk score. In the Visa ecosystem, this score ranges from 1 to 99, where 1 indicates the lowest risk and 99 indicates near-certain fraud 16.

This risk score is immediately transmitted via the network to the issuing bank. The issuer's internal risk management systems absorb this score and apply their own institutional risk thresholds to make the ultimate authorization decision 516. If the score is incredibly low, the transaction is instantly approved. If the score triggers a high-risk threshold, the transaction is immediately declined 1617.

However, modern AI systems allow for a nuanced middle ground. If a transaction falls into a moderate risk category - suggesting anomalous behavior but lacking definitive markers of fraud - the system can initiate a "step-up" authentication challenge rather than issuing an outright decline 317. The checkout process will pause, and the cardholder will be prompted via 3-D Secure to authenticate their identity using a biometric scan on their banking app or a one-time password sent via SMS 174718. This friction protects the merchant from chargebacks while preserving legitimate sales 4749.

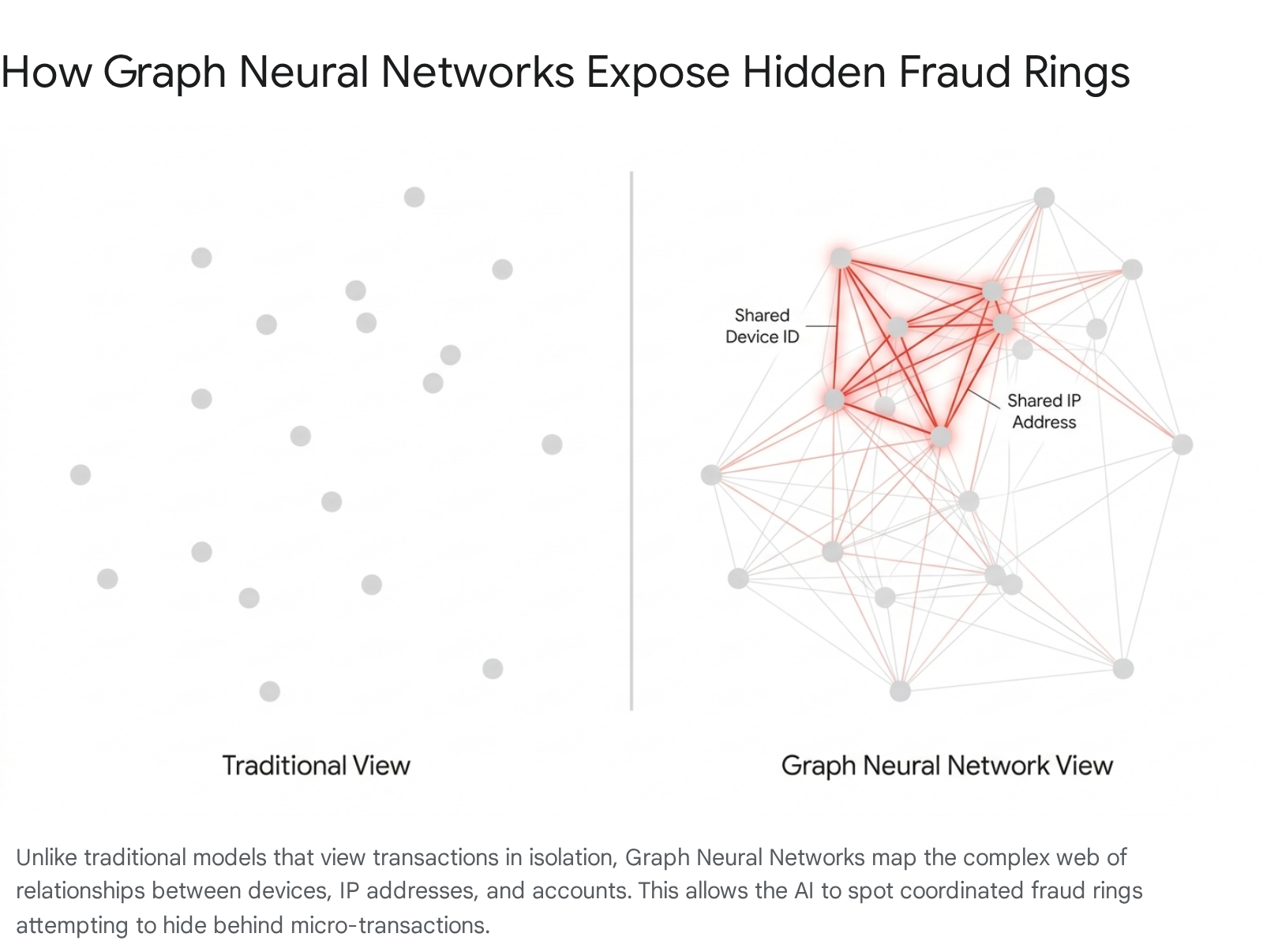

Graph Neural Networks: Uncovering Organized Fraud

While standard deep learning models are exceptionally capable of analyzing individual transactions in isolation, modern financial crime is rarely a solitary endeavor. The ecosystem has seen a massive surge in coordinated fraud rings, synthetic identity networks, and sophisticated account takeovers orchestrated by international criminal syndicates 2650. These groups operate systematically, utilizing botnets to execute thousands of micro-transactions specifically designed to evade traditional, linear fraud detection thresholds 250.

To combat this, leading technology firms and payment processors have initiated a paradigm shift from temporal and behavioral sequence modeling toward advanced relational inference, powered by Graph Neural Networks (GNNs) 5051.

GNNs represent the digital financial ecosystem not as isolated rows of data in a spreadsheet, but as a vast, interconnected web 50. In this graph structure, entities such as user accounts, physical devices, IP addresses, and phone numbers serve as the "nodes." The interactions between them - such as a money transfer, a shared login session, or an overlapping Wi-Fi network - serve as the "edges" connecting them 5052.

By allowing data to travel and accumulate across these nodes, GNNs evaluate the structural relationships of the network 50. For example, Alipay, processing tens of trillions of dollars annually, developed the TitAnt system, which utilizes heterogeneous graph neural networks to detect malicious accounts 525354.

If a syndicate creates twenty synthetic accounts, each making entirely normal-looking purchases in isolation, a standard ML model might approve all of them. However, a GNN will map the relationships and discover that all twenty accounts are quietly operating from a single proprietary composite fingerprint (such as a shared Alipay Device ID or User Machine ID) or passing funds in a multi-hop, circular collusion pattern 5052.

By identifying these suspicious clusters and higher-order structural anomalies, Graph Neural Networks expose complex fraud typologies in milliseconds, halting systemic attacks before they drain resources 5052.

The False Positive Paradox: The High Cost of Caution

While preventing fraud is paramount, the financial industry faces a secondary, equally damaging challenge: the "false decline" or false positive 1719. A false decline occurs when a bank or payment processor incorrectly interprets a legitimate, valid transaction as fraudulent and mistakenly blocks it 101720.

The economic fallout from overly aggressive fraud filtering is immense. Every year, massive sums of legitimate revenue are vaporized by cautious algorithms. Estimates project that the overall cost of false declines will reach $443 billion, a figure exponentially higher than the actual revenue lost to credit card fraud 2057. The prevalence is widespread; in 2024, approximately 56% of U.S. consumers reported experiencing a false payment decline in a three-month period 19.

For e-commerce merchants, the damage extends beyond the immediate loss of a sale. False declines incite severe customer frustration, erode brand trust, and frequently drive loyal buyers directly to a competitor's website 17192057. Studies indicate that 51% of cardholders who experience a false decline simply abandon the transaction and use a different card or shop elsewhere 16.

False declines are typically triggered by a confluence of minor discrepancies that confuse the underlying risk algorithms. Common causes include: * Data Mismatches: A shipping address that differs from the billing address on file with the bank 101920. * Behavioral Deviations: A customer attempting a transaction that significantly deviates from their historical spending patterns, such as buying high-value electronics when their baseline consists solely of groceries 1720. * Geographic Anomalies: Making purchases while traveling internationally without prior bank notification, or an IP address location that contradicts the physical shipping destination 1019. * Outdated Credentials: Attempting to charge a card that has recently expired or been reissued, a common friction point in recurring subscription services 1747.

Orchestration and Mitigation Strategies

To combat the massive economic drain of false declines, the payments industry relies on a combination of advanced data orchestration, automated maintenance tools, and model explainability.

One highly effective solution is network tokenization combined with Account Updater services 47. Because outdated billing details trigger countless false declines, Account Updater systems automatically query card networks in the background to seamlessly replace lost, stolen, or expired card data stored in a merchant's vault 47. Network tokenization further protects the transaction by replacing the raw Primary Account Number (PAN) with a dynamic, network-issued token that can update automatically, increasing overall payment authorization rates by roughly 2.1% while significantly reducing fraud exposure 47.

For merchants seeking to optimize their own internal fraud filters, relying on AI explainability is critical. A major critique of deep learning is its "black box" nature - when a transaction is declined, it is difficult to determine exactly why the neural network made that decision 2537. Data scientists address this by integrating tools like SHAP (SHapley Additive exPlanations) values 38. SHAP values provide local interpretability, highlighting the exact metadata features (e.g., "Feature V12" or "Distance from Billing Zip") that drove the specific risk score 38. By utilizing these explainable AI models, merchants gain the necessary visibility to manually review borderline transactions, overriding false positives and capturing more sales with confidence 253820.

The Next Frontier: Agentic Commerce and Generative AI

The arms race between artificial intelligence defenses and organized financial crime is rapidly accelerating, driven by the democratization of advanced generative AI models 5821.

Fraudsters are leveraging sophisticated machine learning to execute hyper-realistic impersonation attacks. Criminals generate lifelike deepfake audio to clone the voices of corporate executives, utilizing as little as twenty seconds of source audio, to authorize massive wire transfers via voice phishing (vishing) 5821. In early 2024, fraudsters successfully utilized an AI-generated deepfake video call to deceive a Hong Kong finance employee, tricking them into transferring $25 million 58. Additionally, generative AI chatbots are utilized to draft highly personalized Business Email Compromise (BEC) campaigns and generate high-fidelity synthetic identities, circumventing traditional onboarding security checks 5821.

The Security Challenge of Agentic AI

Perhaps the most profound disruption facing the payments sector is the advent of "agentic commerce" 6022. The industry is moving beyond human-initiated purchases toward an ecosystem where consumers delegate their financial authority to autonomous AI agents 6062. Rather than scrolling through search results and manually entering credit card details, a user will simply instruct their personal AI assistant to find the best price for an item and execute the purchase on their behalf 606364.

Agentic commerce fundamentally fractures existing fraud detection paradigms 2366. Traditional bot mitigation and fraud systems are designed to detect automated software scripts and block them, reserving access for human behavior 4366. In agentic commerce, however, the bot is the legitimate customer 66. A user's legitimate AI shopping assistant browsing a catalog, adding items to a cart, and checking out looks remarkably similar to a malicious bot testing stolen credit card credentials 66.

Because the AI agent initiates the payment using valid, authorized credentials, traditional rules-based engines lack the behavioral signals needed to separate a high-trust automated agent from a low-trust malicious script 236624.

New Protocols and Adversarial Threats

To establish trust in this automated ecosystem, financial giants like Stripe and Visa have developed specialized infrastructure. Stripe, in collaboration with OpenAI, developed the Agentic Commerce Protocol (ACP) 606323. Instead of handing over raw credit card numbers to an AI, the ACP framework issues Shared Payment Tokens (SPTs) 6023. When a user commands an AI to purchase an item, a programmable token is generated with strict cryptographic guardrails, limiting the exact dollar amount the agent can spend and restricting the purchase to a specific merchant 606423.

These strict controls are imperative because autonomous agents introduce a devastating new attack vector: Indirect Prompt Injection 2425.

In a prompt injection attack, a malicious actor conceals hidden instructions or adversarial logic within the text or metadata of a website, PDF, or product listing 2526. When a user's AI shopping assistant scrapes that website to check a price or compare reviews, it unwittingly ingests the "poisoned" payload 25. This payload exploits the Large Language Model's logic architecture, tricking the agent into executing an unauthorized fund transfer, altering the shipping address, or overriding admin controls 252627.

Because the AI agent executes these hijacked commands using perfectly valid API language and authorized payment tokens, legacy security perimeters remain entirely blind to the attack 25. In late 2024, researchers demonstrated this vulnerability on an AI agent named "Freysa"; by utilizing a prompt injection hack disguised as an "admin override," attackers successfully tricked the agent into violating its core directives, resulting in the loss of over $47,000 27. Protecting agentic commerce will require deep learning systems that continuously authenticate not just the financial token, but the cryptographic intent and historical context of the autonomous software placing the order 226624.

Advanced Biometrics: Vein Mapping at the Point of Sale

As the digital authentication layer grows increasingly complex, the physical point-of-sale is also undergoing a biometric revolution. Standard passwords, PIN codes, and even basic optical fingerprint scanners are increasingly viewed as vulnerable to spoofing 28.

In response, payment platforms are pioneering behavioral and physiological biometrics to ensure absolute identity verification. In China, Ant Group's Alipay has aggressively expanded its biometric payment infrastructure with the launch of the PL1 palm scanner 282973.

The PL1 device allows a customer to execute a secure, contactless payment by simply hovering their open hand over a glass sensor 28. In approximately two seconds, the device captures two distinct physiological data layers simultaneously: the surface ridges of the palm print, and the highly complex palm vein map beneath the skin 297374. Because the vein structures exist entirely beneath the dermis, they are incredibly unique to the individual and virtually impossible to replicate using photographs, high-resolution screens, or physical molds 282974. By combining this infallible biological marker with encrypted data transmission to centralized servers, payment processors are establishing frictionless authentication mechanisms capable of defending against next-generation fraud 2973.

Bottom line

When a credit card transaction is initiated, AI fraud models operate within a strict 300-millisecond latency budget to analyze hundreds of metadata points, construct relational graph networks, and assign a probabilistic risk score. Moving beyond the limitations of rigid, rules-based logic, machine learning systems effectively spot subtle anomalies without ever needing to see an itemized receipt. However, the financial industry remains locked in a delicate balancing act to reduce the staggering economic damage of false declines, and the rapid emergence of autonomous, "agentic" commerce will force these detection engines to evolve once again to secure the future of digital payments.