What Happens After Your Employer Submits Payroll

Direct deposit is an electronic transfer of funds routed through the Automated Clearing House (ACH) network, moving in scheduled batches from an employer's financial institution to an employee's bank account. Two coworkers with the same employer might receive their pay on different days because their respective banks process incoming ACH files at different speeds; some modern institutions offer an "early direct deposit" feature that advances funds immediately upon receiving the initial electronic notification, whereas traditional banks wait until the official settlement day to release the money 1231.

The Relatable Anxiety of Waiting for Payday

The modern economy operates at lightning speed, yet the traditional payroll cycle often feels stubbornly analog. The anxiety of checking a bank balance early on a Friday morning, waiting for a promised paycheck to clear, is a universally relatable experience. Bills loom, rent is due, weekend plans pend, and financial peace of mind hinges entirely on digital numbers appearing in an account at the right time. The stakes are profoundly high; survey data indicates that 88 percent of employees report experiencing some degree of financial stress, and 55 percent of Americans report that their financial situation is actively worsening 234. Furthermore, financial disengagement in the workplace is estimated to cost the global economy approximately $10 trillion in lost productivity 4. When payday arrives, workers expect immediate access to their earned wages to navigate these pressures, yet the systems governing these digital transfers - primarily the ACH network - are rooted in batch-processing infrastructures designed decades ago.

FAQ: Why Do Two Coworkers With the Same Employer Get Paid on Different Days?

A frequent source of workplace confusion arises when two employees, working the exact same hours for the exact same company, see their wages deposited on completely different days. It is a common assumption that the employer's payroll department plays favorites, staggers payments, or processes batches inconsistently. In reality, the employer initiates the payroll for all employees simultaneously through a single consolidated file sent to their bank or payroll provider, such as ADP or Gusto 1289.

The discrepancy occurs entirely on the receiving end of the transaction. When a payroll processor submits the ACH file, it includes an "effective entry date" - the official payday, which is typically a Friday. The network transmits these instructions to the receiving banks a day or two in advance of the settlement. At this juncture, the banking policies diverge: * Traditional Banks: A legacy financial institution will typically hold this notification in its internal queue and wait for the funds to officially settle at the Federal Reserve before crediting the employee's checking account on the actual Friday morning 110. * Early Direct Deposit Banks: Many modern financial technology companies, credit unions, and challenger banks utilize this advance notification to offer an "Early Direct Deposit" feature. Once they receive the ACH file indicating a guaranteed deposit is incoming, they absorb the settlement risk and advance their own corporate funds to the employee, crediting the account on Wednesday or Thursday, up to two days ahead of the official payday 23110.

Therefore, early access to a paycheck is not an indicator of preferential employer treatment, but rather a marketing and customer acquisition strategy deployed by specific banking institutions to attract deposits 310.

Demystifying Jargon: How the ACH Network Actually Works

To fully comprehend the lifecycle of a paycheck, it is necessary to demystify the acronyms and processes that govern the United States financial system. The ACH network is the electronic backbone of the American economy. In 2025 alone, the network processed 35.2 billion payments valued at roughly $93 trillion, facilitating everything from direct deposits and tax refunds to business-to-business vendor payments 51213.

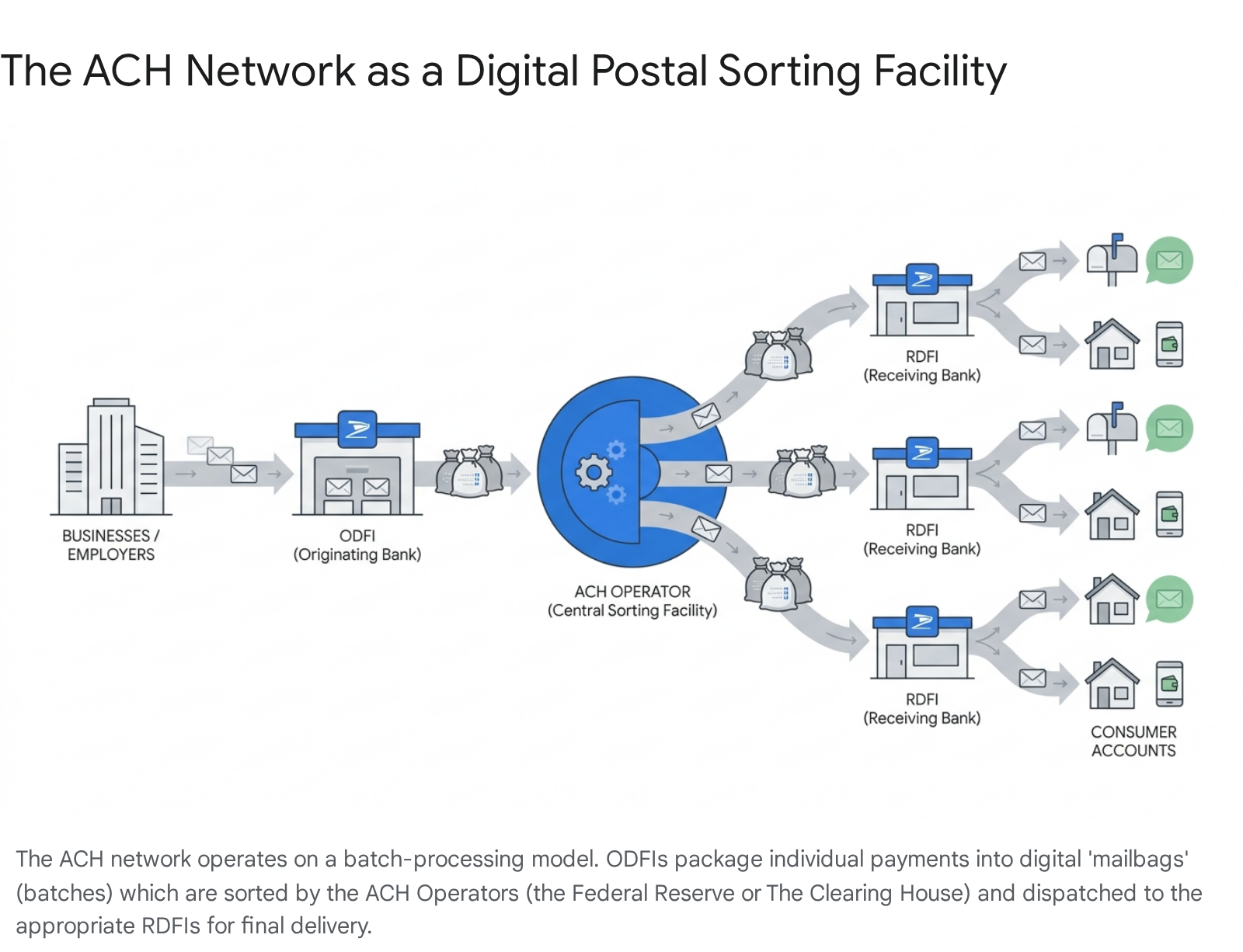

The most effective way to understand the ACH network is to compare it to a central postal sorting facility that moves massive batches of digital envelopes, rather than a courier dispatching individual letters one by one 16.

The sequence of a payroll transaction unfolds through several distinct institutional players: First, the employer acts as the Originator. When payroll is due, the employer compiles the payment instructions - including routing numbers, account numbers, and the precise wage amounts - for all employees into a single, standardized digital file 16. In some cases, to validate these account and routing numbers before sending actual funds, employers may utilize "prenotes" (prenotifications), which are zero-dollar transactions sent through the network to verify the destination's accuracy 15.

Second, the employer submits this consolidated file to their corporate bank, formally known as the Originating Depository Financial Institution (ODFI). The ODFI collects these files from thousands of businesses, bundles them together into a massive digital "mailbag," and holds them until a specific transmission window 11367.

Third, at scheduled intervals, the ODFI transmits these bulk files to an ACH Operator. In the United States, there are two national ACH Operators: the Federal Reserve (operating FedACH) and The Clearing House (operating the Electronic Payments Network, or EPN). Acting as the central sorting facility, the ACH Operator opens the bulk digital mailbags, sorts the millions of individual transaction "envelopes" by their final destination, and repackages them into new batches destined for specific receiving banks 1137.

Fourth, these newly sorted batches are transmitted to the employees' respective banks, classified as the Receiving Depository Financial Institutions (RDFI).

Finally, the RDFI opens its specific batch, parses the instructions, and credits the individual employee's checking or savings account, making the employee the ultimate Receiver of the funds 1136.

Because this entire ecosystem relies on batch processing - accumulating transactions over a designated period and moving them synchronously - it is incredibly cost-effective, typically costing pennies per transaction. However, this same architecture renders it inherently slower than real-time, one-to-one wire transfers or modern instant payment rails 121718.

Busting a Persistent Myth: The "Bank Float" Conspiracy

A deeply entrenched misconception among the American workforce is that banks deliberately hold onto incoming paychecks for two to three days to earn interest off the "float." The conspiracy theory posits that financial institutions intercept the payroll funds, park them in their own institutional accounts, collect interest at the prevailing federal funds rate, and then release the principal to the employee just before the weekend 198.

This is definitively a myth when applied to payroll direct deposits.

The National Automated Clearing House Association (NACHA), the non-profit regulatory body that authors and enforces the rules for the network, strictly dictates funds availability parameters 1315. If an employer's payroll file designates the effective payday as Friday, NACHA operating rules mandate that the funds must be available in the employee's account for withdrawal by 9:00 a.m. local time on that Friday, in virtually all circumstances 1589. The delay experienced between the employer executing the payroll software on Wednesday and the employee receiving funds on Friday is not a deliberate stalling tactic for institutional profit; rather, it is the mechanical time required for the batch files to traverse the ODFI, the ACH Operator, and the RDFI, and await the Federal Reserve's daily settlement windows 8.

However, the concept of "float capture" is not entirely fabricated; it simply occurs elsewhere in the banking ecosystem. When a consumer uses an ACH debit to pay a utility bill, their bank deducts the funds from their checking account immediately on Monday morning 719. The money is then batched and sent through the overnight settlement process to the utility company's bank. During this 24- to 48-hour transit window, the consumer's bank does indeed hold the equivalent funds in its master account at the Federal Reserve 19. The Federal Reserve pays interest on these reserve balances (IORB) to depository institutions - a mechanism designed by Congress to provide the Fed with a tool to manage macroeconomic interest rates and monetary policy 1922. At higher federal funds rates, this generates significant revenue for the bank when multiplied across millions of outbound debit transactions 19. But for incoming ACH credits - like a payroll direct deposit - the bank does not hold the funds from the consumer; the money is credited as soon as the settlement rules require it to be 58.

Comparing the Timelines: Traditional, Same Day, and Early Access

To facilitate varying business urgencies and consumer demands, the ACH network and individual financial institutions have developed different tiers of processing speeds for payroll delivery.

| Feature | Traditional ACH | Same Day ACH | Early Direct Deposit |

|---|---|---|---|

| Settlement Time | 1 to 3 business days 923. | Same business day (within hours) 523. | Up to 2 days prior to official payday 210. |

| Processing Mechanism | Batched overnight; settles next or subsequent business day 1224. | Batched across three specific intraday transmission windows 2324. | RDFI advances its own corporate funds upon receiving the pre-notification file 110. |

| Cost to Employer | Lowest cost (pennies per transaction) 171825. | Higher cost (requires a monthly or per-transaction Same Day Entry fee) 1723. | No additional cost to employer (handled entirely by employee's bank) 108. |

| Transaction Limits | Generally unlimited for standard corporate payroll volume 26. | Capped at $1 million per individual transaction 52327. | Dependent on the individual bank's internal policy limits. |

| Funds Availability | Typically by 9:00 a.m. on the scheduled payday 589. | Same day, mandated by 5:00 p.m. local time 23. | As soon as the ACH file is received by the RDFI (typically Wednesday or Thursday) 10. |

| Typical Use Case | Standard bi-weekly or semi-monthly corporate payroll runs 51210. | Emergency payroll corrections, gig worker payouts, urgent contractor fees 51217. | Consumer-facing feature utilized by neo-banks to attract deposits 10. |

The Mechanics of Same Day ACH

Traditional ACH is built for volume and predictability, whereas Same Day ACH is engineered for speed 29. Introduced in 2016 and continually enhanced, Same Day ACH provides accelerated clearing for urgent disbursements. Rather than waiting for a single overnight batch to clear the following day, ODFIs can submit files to the Federal Reserve through three specific intraday cut-off windows: 10:30 a.m., 2:45 p.m., and 4:45 p.m. Eastern Time 6823.

These submissions correspond to staggered settlement times later that same afternoon, ensuring that funds are available to the receiver by 5:00 p.m. local time 23. In 2022, NACHA raised the per-transaction limit for Same Day ACH from $100,000 to $1 million to accommodate larger business needs 523. While this speed requires the payment of a Same Day Entry fee to offset the banks' accelerated processing costs, it has become highly popular; the network handled 1.4 billion Same Day ACH payments valued at $3.9 trillion in 2025 alone 523. Despite this volume, the $1 million cap and fee structure make it less suitable for massive corporate bulk payroll runs, but ideal for off-cycle salary corrections or emergency advances 52329.

Practical Realities: Cutoffs, Weekends, and Bank Holidays

While the ACH network boasts exceptional reliability for standard payroll, the system is strictly bound by operational hours, banking cutoffs, and federal calendars, all of which dictate exactly when a worker actually receives their money 57.

The Rigidity of Employer Cutoff Times

The timing of payroll processing relies on rigid administrative schedules. If a payroll manager finalizes a payroll run and submits the ACH file to their ODFI just minutes after the bank's daily cutoff time, the file will not enter the ACH Operator network until the following business day 9231131. This single administrative delay at the corporate level cascades through the entire system, ultimately delaying the employee's direct deposit by a full 24 hours 931.

The Impact of Weekends and Federal Holidays

A critical, structural limitation of the current ACH network is that it only processes and settles payments when the Federal Reserve's National Settlement Service (NSS) is open for business 58. Consequently, the ACH network does not settle payments on weekends or on federal holidays 811. * Federal Holidays: If a scheduled payday falls on a Monday that happens to be a federal holiday (such as Labor Day or Columbus Day), the settlement cannot occur on that day 31. * Industry Standard Adjustments: To protect workers from going without funds over a weekend, standard industry practice and NACHA guidelines dictate that if a payday falls on a weekend or a holiday, the employer must submit the payroll files early so that the employee is paid on the preceding Friday 1811.

If an employer's payroll software or HR manager fails to adjust their processing schedule to account for an impending holiday like Thanksgiving or Independence Day, the deposit will inevitably be delayed until the next open banking window 3132.

FAQ: What Can a Worker Actually Do if a Deposit is Late?

When a payday arrives and a checking account balance remains unchanged, financial panic often sets in. Workers facing a missing direct deposit should follow a specific, escalating sequence of actions to locate their funds:

- Verify with the Employer Immediately: The vast majority of deposit delays originate at the source. The employee should contact their HR or payroll department to confirm the exact date and time the payroll file was successfully submitted to the bank 113132. It is paramount to verify that the routing and account numbers on file are perfectly accurate; a single transposed digit on a direct deposit form will cause the RDFI to reject the deposit and return it to the sender 113132.

- Inquire About Cutoff Times and Holidays: Ask the payroll manager if they accounted for any recent bank holidays, or if the initial file submission inadvertently missed the ODFI's specific cutoff window 31.

- Contact the Receiving Bank (RDFI): If the employer confirms the file was sent correctly and on time, the employee should contact their own bank. Occasionally, an RDFI will place an "exception hold" on a deposit. This can occur if the account is brand new, has a history of being overdrawn, or if the deposit is unusually large, which triggers internal fraud and risk management protocols 1132.

- Request an ACH Trace: If neither the employer nor the receiving bank can immediately locate the funds, the employer can instruct their bank (the ODFI) to initiate a formal payment trace through the ACH network to pinpoint exactly where the transaction is stalled in the system 31.

Global Context: US ACH vs. International Real-Time Rails

While the United States relies heavily on the batch-based ACH system for bulk corporate disbursements, the global payments landscape is rapidly shifting toward instantaneous, 24/7 continuous settlement systems. Contrasting the US with international markets highlights both the friction in the American payroll ecosystem and the direction in which global finance is moving.

The United Kingdom: Faster Payments vs. BACS

In the UK, domestic payroll is traditionally handled by BACS (Bankers' Automated Clearing Services), which operates on a rigid three-working-day cycle, structurally similar to standard US ACH. A payroll file submitted on a Monday will generally not clear into employee accounts until Wednesday 2529. BACS is built for volume and predictability, but not for speed. Conversely, the UK also operates the Faster Payments Service, a near-instant network that operates 24/7/365 and is capable of settling transactions in seconds 2933. While BACS remains the cost-effective default for bulk corporate payroll runs, Faster Payments is increasingly utilized for off-cycle salary disbursements, gig worker payouts, and emergency wage advances. The primary limitations of Faster Payments are its lack of native batch infrastructure, per-transaction limits (typically capped at £1 million by most participating banks), and higher corporate banking fees compared to BACS 2933.

Brazil: The Pix Revolution

Perhaps the most striking contrast to the US market is Brazil's Pix system. Launched in November 2020 by the Banco Central do Brasil, Pix was heavily mandated for all major financial institutions, ensuring immediate, country-wide interoperability from day one 253435. Pix operates 24 hours a day, settles transactions in under ten seconds, has no fixed transaction limit at the network level, and is entirely free for individual consumers 2535. By bypassing the fragmented, opt-in approach characteristic of the US market, Pix achieved near-universal cultural penetration within three years, and is currently utilized by over 150 million Brazilians to move money instantly 35.

Global Bridges for Cross-Border Payroll

Other nations have deployed similar instant infrastructure, such as India's Unified Payments Interface (UPI), which processes tens of billions of transactions monthly, and Europe's TARGET Instant Payment Settlement (TIPS) for cross-border euro transactions 253435. However, these real-time rails are distinctly domestic. If a US company wishes to pay a contractor in Bangalore or Rio de Janeiro, they cannot push funds directly from a US ACH account to an Indian UPI or Brazilian Pix account 25. Instead, cross-border payroll requires bridge fintechs (like Wise or Payoneer) to convert US dollars into the local currency and then disburse those funds natively on the local instant rail 2529. For larger corporate transfers, legacy SWIFT wire transfers remain an option, but at a significantly higher cost ($40 to $100 per transaction) and with a slower 1-5 day settlement timeframe 172534.

Recent Developments (2023+): FedNow, NACHA Rules, and Payroll Disruptors

The US payroll landscape is undergoing a structural evolution, driven by proactive regulatory updates, the launch of new central bank settlement infrastructure, and the explosive growth of financial technology applications seeking to monetize employee wage access.

Evolving NACHA Operating Rules for Fraud Prevention

To maintain trust in a network that moves $93 trillion annually, NACHA is continuously updating its operating rules to combat sophisticated cybercrime and unauthorized entries. Recognizing the rise in fraud, NACHA has instituted sweeping Risk Management framework updates taking effect in 2026. * Phase 1 (Effective March 2026): All ODFIs, as well as any non-consumer Originator or Third-Party Sender generating an annual volume of 6 million or more ACH entries, must establish and implement comprehensive, risk-based processes designed explicitly to identify transactions initiated due to fraud 1213. Furthermore, RDFIs that process over 10 million annual receipts must begin monitoring inbound ACH credits for fraudulent activity 12. * Phase 2 (Effective June 2026): The rigorous inbound credit monitoring requirement will expand to cover all remaining RDFIs, regardless of their receipt volume 12.

In conjunction with these security measures, NACHA has introduced standardized "Company Entry Descriptions." Originators are now required to specifically identify salary disbursements with the code "PAYROLL" 13. This standardization helps receiving banks better apply internal logic for early funds availability features and improves fraud detection by flagging anomalies in payroll frequency 13. Furthermore, NACHA enforces a strict Limitation on Warranty Claims Rule; for consumer accounts, an RDFI has up to two years from the settlement date to make a warranty claim against the ODFI for unauthorized entries, ensuring strong consumer protection 1538.

The Promise and Reality of the FedNow Service

In July 2023, the Federal Reserve launched the FedNow Service, a real-time gross settlement (RTGS) infrastructure meant to modernize the US payments grid and compete with private sector solutions like The Clearing House's RTP network 63539. Unlike the batch-processed ACH, FedNow clears and settles individual payments instantly, 24 hours a day, 365 days a year 3940.

For the payroll industry, FedNow offers a theoretical paradigm shift. Employers are no longer strictly bound to traditional bi-weekly schedules or restricted by weekend and holiday closures. Through FedNow, a business can approve an electronic timecard at 5:00 p.m. on a Sunday, and the employee can have those wages settled in their bank account seconds later 23. This immediate wage access allows employers to offer spot bonuses for unpopular shifts and drastically improves employee job satisfaction and financial control 2314.

However, as of 2025, FedNow is not yet a wholesale replacement for the ACH payroll ecosystem. While over 1,400 financial institutions participate in the network, many currently offer "receive-only" capabilities 15. This is due to intense concerns surrounding instant fraud; because FedNow payments settle in seconds and boast finality - meaning they cannot be reversed once sent, unlike ACH payments which can be reversed up to two days later - banks have limited time to detect malicious activity 3915. Furthermore, FedNow is currently constrained by a $500,000 maximum daily transaction limit, rendering it completely inadequate for large corporate bulk payroll runs compared to the ACH network's massive capacity 15. For the immediate future, ACH remains the cost-effective workhorse for standard batch payroll, while FedNow will increasingly handle urgent, off-cycle disbursements, and immediate gig-economy payouts 15.

The Earned Wage Access (EWA) Controversy

The friction inherent in traditional 14-day payroll cycles - combined with rising economic pressures, energy costs, and housing inflation - has spawned a massive sub-industry of Earned Wage Access (EWA) applications. EWA providers allow employees to access portions of their accrued wages before the official payday. In 2022 alone, these platforms provided over $31.9 billion in early wage access across 214 million transactions to approximately 10 million workers, and the market is projected to expand by 300% over the next decade 1416.

EWA operates on two distinct functional models: 1. Employer-Integrated Models: In this framework, the EWA firm integrates directly into the employer's HR and payroll software. The software verifies exactly how many hours the employee has worked. When an advance is requested, the funds are disbursed, and the EWA firm advises the employer to automatically deduct the advanced amount from the worker's official paycheck on payday. Because the integration intercepts the payroll directly, loss rates for these firms are exceptionally low, often recovering 97% of advanced wages 1417. 2. Direct-to-Consumer (D2C) Models: These applications operate entirely independently of the employer. They rely on screen-scraping consumers' bank account transaction histories to estimate a user's regular income. The app provides an advance and then debits the consumer's bank account directly via ACH when they detect the official paycheck has arrived 1417.

The rapid rise of EWA has sparked intense regulatory scrutiny and controversy. Critics argue that D2C apps, which frequently charge "expedited delivery fees" and solicit "tips" from users, function essentially as payday loans dressed in Silicon Valley branding. Studies indicate that heavy users often pay loan and overdraft fees resulting in effective Annual Percentage Rates (APRs) of 383%, trapping low-wage workers in cycles of recurring debt 1718.

This controversy culminated in a major regulatory clash. Following a lenient advisory opinion in 2020, the Consumer Financial Protection Bureau (CFPB) reversed course in July 2024, issuing a proposed interpretive rule seeking to classify all EWA products as "credit" under the Truth in Lending Act (TILA) and Regulation Z 17464719. Crucially, this rule proposed that any tips or expedited delivery fees must be classified as "finance charges," which would have subjected the entire EWA industry to strict federal lending disclosures and state usury rate caps 464719.

However, following fierce pushback from the financial technology industry - who argued that non-recourse payments advanced against already-earned wages do not constitute "debt" because the provider has no legal claim to seek repayment if the employer fails to pay - the regulatory stance pivoted dramatically 1649. In December 2025, the CFPB officially rescinded the 2024 proposed rule 1619. The Bureau issued a new advisory opinion concluding that employer-partnered EWA products are strictly not loans under TILA, provided the advanced amount does not exceed accrued wages, the provider has no legal claim to seek repayment through debt collection, no credit risk assessments are performed, and no mandatory fees are required 161949. This ruling solidifies the employer-integrated EWA model as a compliant, permanent fixture in the modern payroll ecosystem, functioning legally as an employer-facilitated early wage payment rather than an extension of credit 16.

API Infrastructure and the Standardization of Payroll Data

To facilitate employer-integrated EWA, as well as broader HR automation, the software industry relies heavily on payroll APIs. Platforms like ADP (the enterprise leader favored for complex, multi-state regulatory environments and deep compliance frameworks), Gusto (the modern, user-friendly platform dominating the small-to-medium business sector), and Paychex serve as the fundamental financial systems of record for employee compensation 89505152.

Integrating with these systems allows third-party SaaS applications to sync payroll runs, manage benefits, and enable on-demand pay features seamlessly 89. However, the ecosystem is highly fragmented; every platform models deductions, tax identifiers, and compensation data differently, making custom integrations fragile and difficult to maintain 852. This fragmentation has given rise to unified payroll APIs - intermediary integration layers that normalize data schemas across ADP, Gusto, Paychex, and others. These unified layers allow fintech developers to write a single codebase against a normalized schema to access secure wage data across the entire market, often using real-time pass-through architectures to avoid storing sensitive tax data 52. This API infrastructure is the invisible digital thread connecting the rigid batch rules of the legacy ACH network to the flexible, real-time demands of the modern workforce.

Bottom line

The United States payroll infrastructure is a remarkably reliable, yet antiquated system operating at the complex intersection of legacy banking mechanics and modern consumer expectations. At its core, the ACH network moves trillions of dollars efficiently by functioning like a massive central postal sorting facility, processing digital envelopes in rigid, scheduled overnight batches rather than executing real-time, one-to-one transfers. This fundamental batching mechanism - not a conspiracy by financial institutions to earn interest on the float of incoming credits - is exactly why standard direct deposits take days to clear, and why weekends, bank holidays, and missed administrative cutoff times result in delayed paychecks. Discrepancies among coworkers receiving pay on different days ultimately stem from how individual receiving banks choose to handle advanced notification files, with modern institutions increasingly offering early access as a competitive feature. While new rails like the Federal Reserve's FedNow service promise 24/7 instant settlement, broad adoption for bulk payroll remains constrained by strict transaction limits and intense fraud concerns. In the interim, Earned Wage Access platforms, bolstered by recent favorable CFPB rulings for employer-integrated models, and seamless unified API infrastructures have successfully bridged the gap, providing American workers with the vital liquidity they require while operating safely within the confines of a decades-old financial grid.