Should Your Startup Use PLG or Sales-Led Growth

Product-led growth fits simple, low-cost tools targeting individuals and small teams, while sales-led growth suits complex, high-value enterprise solutions requiring tailored implementations. In the current software landscape, however, the most successful startups combine both into a hybrid "product-led sales" approach. This model leverages self-serve product usage to efficiently identify and capture high-intent enterprise buyers without inflating acquisition costs.

The Evolution of Go-To-Market Strategies in Software

To understand the current debate surrounding software distribution, it is necessary to look at how technology has historically been sold. In the 1980s and 1990s, enterprise software was sold almost exclusively via high-touch, top-down sales 12. Vendors employed large field sales teams to navigate long requests for proposals (RFPs) and secure massive upfront deals 1. This traditional sales-led growth (SLG) was effective in a world of on-premise software and centralized IT budgets, but it was incredibly costly and slow 12.

The 2000s ushered in the cloud era and the software-as-a-service (SaaS) business model, which lowered the barrier to entry for buyers and shifted marketing toward inbound, content-driven lead generation 2. Eventually, the consumerization of B2B software led to the creation of product-led growth (PLG). Pioneered by companies like Slack, Dropbox, and Atlassian, this model operated on the premise that B2B users expect the same seamless, self-serve onboarding at work that they experience with consumer apps at home 122.

A helpful analogy to conceptualize these two primary motions is the "buffet versus the concierge" 34. The buffet creates a low-friction atmosphere where food is available immediately, eliminating the time required for order-taking and preparation 3. Customers provide their own service, which increases turnover and lowers overhead 3. In the software industry, this maps directly to the self-serve freemium model. Conversely, the concierge is assigned to take care of individual, complex needs, storing preferences and tailoring the experience to secure long-term loyalty and handle high-value requests 34. In SaaS, this represents the dedicated Account Executive and Customer Success Manager guiding a buyer through a complex, bespoke implementation.

Today, the software landscape is facing a profound efficiency squeeze. The era of cheap capital that subsidized massive marketing budgets has ended 5. By 2025, the median B2B SaaS company was spending $2.00 in sales and marketing to acquire just $1.00 of new Annual Recurring Revenue (ARR) - a 14% increase from 2024, with bottom-quartile performers spending as much as $2.82 568. With acquisition costs skyrocketing, inefficient growth engines are breaking down 5. To survive, startups must rigorously align their go-to-market (GTM) strategy with their product's fundamental economics, target audience, and geographic focus.

Understanding Product-Led Growth (PLG)

Product-led growth is a business methodology where the product itself acts as the primary driver of customer acquisition, conversion, and expansion 71089. Rather than relying on a salesperson to articulate the product's value through slide decks and discovery calls, the product demonstrates its value directly to the user through free trials or freemium tiers 109.

In a PLG motion, the traditional marketing funnel is flipped. Users discover the product, experience its core utility independently, and eventually pull their wider organizations in behind them - a dynamic often referred to as "bottom-up" adoption or a "land and expand" strategy 19.

The Unit Economics of PLG

The primary allure of PLG is its capital efficiency at the top of the funnel. Because the product does the selling, PLG companies can drastically reduce their customer acquisition cost (CAC) 10813. Industry data indicates that PLG companies can often acquire customers at a fraction of the cost of sales-led approaches, sometimes spending as little as $100 to $500 per customer compared to the $5,000 to $50,000 typically required in an SLG model 10.

Because of this lean acquisition model, successful PLG companies generate significantly higher revenue per employee. High Alpha's benchmark reports note that public SaaS companies are running much leaner, with best-in-class PLG organizations reporting over $350,000 to $400,000 in ARR per employee 1015. Furthermore, top-quartile PLG companies hit the "Rule of 40" (an investor metric demanding that revenue growth rate plus profit margin should clear 40%) with a median score of 34, compared to just 20 for their sales-led counterparts 16.

Crucial PLG Metrics and Benchmarks

For a PLG strategy to function, the product must be inherently intuitive, and value must be delivered rapidly. The entire business model hinges on specific user behavior metrics rather than traditional sales pipeline milestones.

- Time to Value (TTV): This measures how quickly users reach their "aha moment" - the point where they explicitly understand the product's core utility. In a modern software market, buyer patience is virtually non-existent; average time-to-value expectations have dropped from weeks to minutes 101711. Leading PLG products deliver value in under 10 minutes for consumer-leaning tools, and under one hour for B2B applications 1712. Research shows that every 10-minute delay in TTV costs a company 8% in overall conversion rates 11.

- Activation Rate: This represents the percentage of new signups who successfully experience the product's core value. The average activation rate for B2B SaaS sits around 37.5%, but top PLG companies aim for 40% to 60%, with elite performers clearing 70% 16172021. If activation falls below 40%, it indicates a structural flaw in the user onboarding process rather than a marketing failure 21.

- Free-to-Paid Conversion: The median free trial converts at roughly 18.5%, though trials requiring an upfront credit card naturally convert higher (closer to 30%) at the expense of top-of-funnel signup volume 1122. Freemium models have much lower conversion rates (typically 2% to 5%) but cast a significantly wider net, creating a vast pool of potential future buyers 1723. When establishing a PLG motion, approximately 75% of companies begin with a free trial or freemium model 13.

Understanding Sales-Led Growth (SLG)

Sales-led growth relies on a structured, human-driven process to acquire and retain customers. In this model, marketing generates leads, Sales Development Reps (SDRs) qualify them via outreach, Account Executives (AEs) run bespoke demonstrations and negotiate contracts, and Customer Success Managers (CSMs) handle post-sale implementation 9.

While PLG relies on users discovering value on their own, SLG is necessary when the value of a product requires deep explanation, extensive architectural configuration, or significant organizational change management 142615.

The Domain of Complex Enterprise Deals

SLG thrives in environments where buying decisions are highly complex and carry massive financial or operational risk. Gartner research notes that the average B2B enterprise deal now involves 6.8 stakeholders across IT, finance, legal, and operations - a sharp increase from 5.4 stakeholders in 2020 2816.

A self-serve checkout page cannot navigate a multi-department security review, negotiate legal redlines, provide a Service Level Agreement (SLA), or secure approval from a Chief Financial Officer whose involvement in software purchases has increased by 40% in recent years 1516.

As a result, SLG commands significantly higher Average Contract Values (ACVs). According to Bessemer Venture Partners, sales-led companies command initial ACVs three to five times higher than their product-led counterparts 14. Salesforce serves as the quintessential SLG organization, maintaining an average ACV above $100,000 for enterprise customers through deeply consultative selling that addresses complex organizational needs 14.

The Costs and Constraints of SLG

The downside of SLG is its sheer expense and linear scaling limitations. Growing revenue in a pure SLG model generally requires hiring more salespeople, which structurally limits margin expansion 914. High customer acquisition costs encompass salaries, software tools, commissions, and management overhead 9.

Furthermore, the sales cycles are inherently long and cash-intensive. While a PLG user might convert from a free trial in seven days, enterprise SLG cycles routinely stretch from 90 to over 180 days 916. The CAC payback period - the time required to recoup the sales and marketing dollars spent to acquire a customer - stretches to 18 to 24 months for enterprise SLG, compared to 8 to 12 months for SMB PLG motions 103017.

The Thresholds: Deciding Between PLG and SLG

The choice between product-led and sales-led growth is not a philosophical preference; it is dictated by hard economic realities, specifically product complexity and Average Contract Value (ACV) 5.

Data analysis of thousands of software companies reveals clear boundaries where specific strategies thrive or fail. Generally, products with an ACV under $10,000 that feature low operational complexity are uniquely suited for self-serve PLG 518. The product must be simple enough for an end-user to extract value in a single session without consulting a manual or requiring a guided tutorial 15. ChartMogul's analysis of 2,500 SaaS companies shows that for products priced below a $25 monthly average sale price (ASP), pure PLG yields 20% median ARR growth; however, companies that artificially layer human sales friction into this low-price tier see their growth plummet to zero 15.

Conversely, products with an ACV exceeding $25,000 to $50,000 necessitate SLG 518. At this price point, the purchasing decision is rarely made by a single user with a corporate credit card. It involves procurement teams, budget approvals, and executive sponsors. Attempting to force an enterprise buyer through a self-serve PLG funnel is often perceived poorly; large corporate buyers view a lack of high-touch sales support as a signal that the vendor cannot accommodate enterprise-grade requirements 33.

Summarizing the Core Differences

To understand which motion suits specific business models, it is helpful to compare their baseline benchmarks based on 2025 and 2026 industry data 1722163017.

| Metric / Characteristic | Product-Led Growth (PLG) | Sales-Led Growth (SLG) |

|---|---|---|

| Primary Target Market | Individual users, SMBs, Mid-market | Enterprise, C-Suite, Multi-stakeholder committees |

| Average Contract Value (ACV) | Generally <$10,000 | Generally >$25,000 |

| Primary Qualification Metric | Product Qualified Leads (PQLs) | Marketing Qualified Leads (MQLs) / SQLs |

| Median Sales Cycle Length | 14 - 30 days | 90 - 180+ days |

| CAC Payback Period | 8 - 12 months | 18 - 24 months |

| Time to Value (TTV) | Minutes to Hours | Weeks to Months (Implementation required) |

| Primary Growth Constraint | Top-of-funnel volume and user churn | Linear sales headcount and lead generation costs |

The HBR Warning and the "PLG Trap"

While PLG has been heavily hyped by venture capitalists as the ultimate growth engine, relying on it exclusively presents severe long-term risks. A prominent analysis published in the Harvard Business Review (HBR) outlined the precise dangers of what it coined the "PLG Trap" 192036.

The trap occurs when a PLG company achieves rapid, viral early success with small teams and individual users, but eventually hits a rigid revenue ceiling. Analysts note that pure self-serve momentum often stalls abruptly around the $10 million to $20 million ARR mark 261937. The self-serve engine successfully exhausts the "early adopter" and SMB market, but the company discovers that larger enterprises cannot buy six-figure software packages via a standard web portal 63337.

When a PLG company tries to move upmarket without building a proper enterprise sales function, their growth flatlines 2637. Pure self-service motions struggle to penetrate the enterprise because corporate buyers demand hands-on implementation, strict security guarantees, and bespoke billing terms that require human negotiation 6333839.

Furthermore, relying solely on PLG can result in missed expansion revenue. High-value customers with a massive willingness to pay may lurk within a company's free user base, but without a proactive sales team to navigate the corporate hierarchy and consolidate rogue individual licenses into a lucrative enterprise contract, that revenue remains unrealized 37. As one analysis notes, companies that remain purely product-led are eventually outflanked by competitors who offer the white-glove service that Fortune 500 executives demand 33.

The 2026 Consensus: The Era of Product-Led Sales (Hybrid)

The binary debate between PLG and SLG is largely over. By 2026, the market data has spoken definitively: the most competitive, capital-efficient, and resilient B2B SaaS companies run hybrid GTM motions 25694041.

This hybrid model, formally known as Product-Led Sales (PLS), seamlessly integrates the acquisition efficiency of PLG with the revenue depth and expansion power of SLG 693721. In a PLS architecture, the product acts as the net that captures a massive volume of individual users and small teams at the bottom of the funnel. Once those users demonstrate specific behavioral signals indicating they are ready for a larger enterprise deployment, a highly trained sales representative steps in to close the high-value deal 263822.

The financial data strongly supports this convergence. According to SaaS benchmark reports, 67% of hybrid PLG+SLG companies successfully hit their net revenue retention (NRR) targets, compared to only 58% of pure-PLG companies 41. Furthermore, companies running hybrid motions report twice the profitability of their pure PLG or pure SLG peers 10. Most category-defining B2B SaaS companies today - including Slack, Dropbox, Figma, and HubSpot - started with purely product-led strategies but eventually layered on robust enterprise sales teams to capture the full value of the market 12.

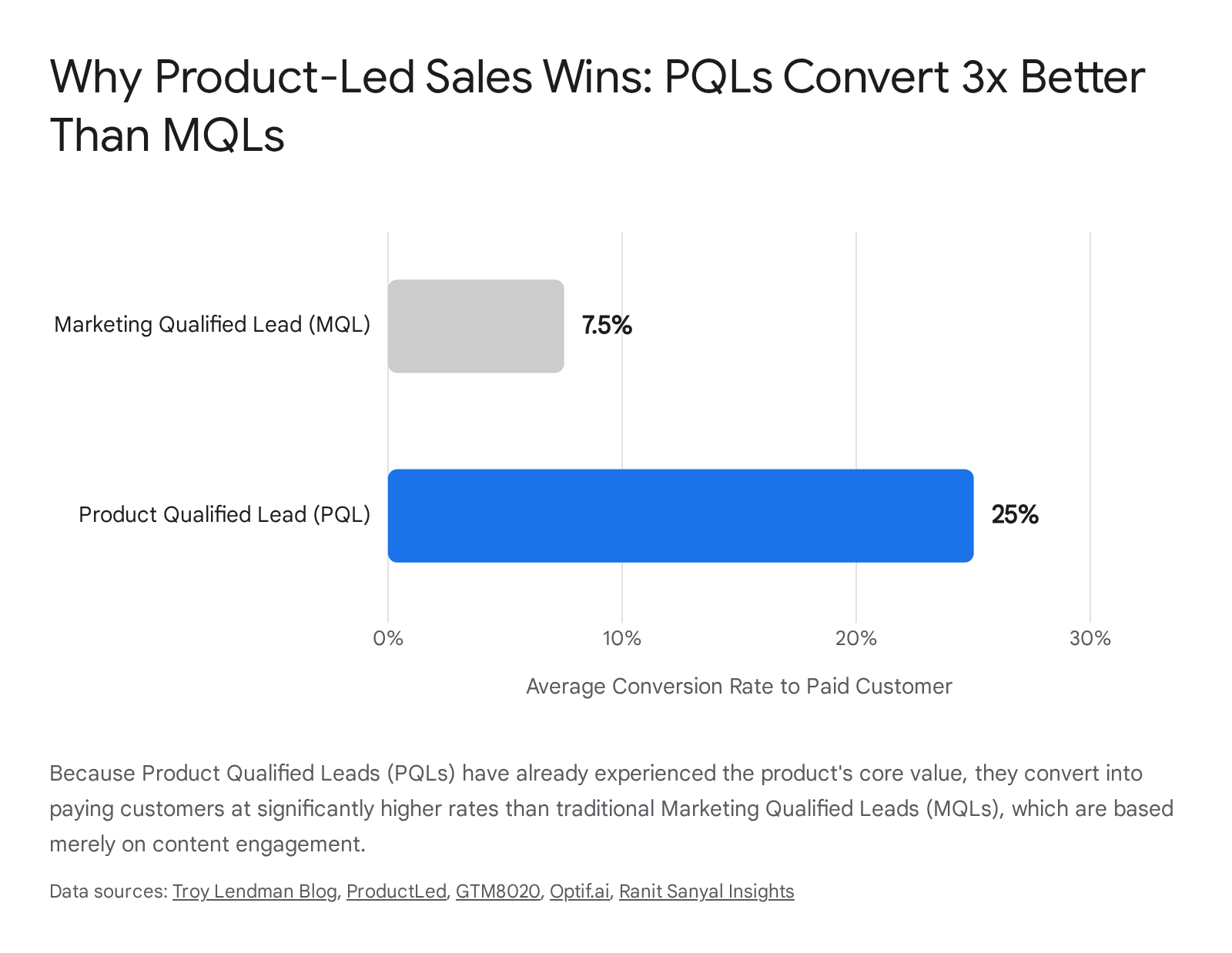

The Bridge Between Motions: Product Qualified Leads (PQLs)

The hybrid engine is entirely dependent on data telemetry, specifically the concept of the Product Qualified Lead (PQL).

In traditional sales-led organizations, marketing teams rely on Marketing Qualified Leads (MQLs). An MQL is generated when a prospect downloads a whitepaper, attends a webinar, or fills out a contact form. The fundamental flaw is that an MQL indicates interest in a topic, not necessarily intent to buy or product fit 1221.

A PQL, conversely, is a user who has already experienced meaningful value within the actual product and exhibited behavioral signals indicating they are ready to buy or expand 8202123. Because PQLs have already bypassed the friction of understanding what the product does, they convert at astronomically higher rates. Industry benchmarks reveal that PQLs convert to paying customers at rates of 20% to 30% - or nearly three times the typical 5% to 10% conversion rate of a traditional MQL 1016171213.

Defining PQL Triggers and Handoffs

In a successful hybrid motion, sales teams are strictly forbidden from cold-calling free users the moment they sign up. Doing so treats a product-led funnel like an outbound prospect list, alienating users who simply want to test the software in peace 22. Instead, Revenue Operations (RevOps) teams use product telemetry to build automated triggers that alert salespeople exactly when intervention is welcomed 291220.

The most effective signals that a self-serve account is ripe for enterprise sales intervention include: 1. The Multi-Player Shift: A single user inviting five or more colleagues to the platform is a clear signal that the software is moving from an individual tool to an organizational workflow 2122. 2. Hitting Usage Ceilings: An account repeatedly bouncing against data, storage, or computational limits proves the product is delivering immense value, meaning the user is highly motivated to upgrade to a capacity plan 123322. 3. Attempting to Access Enterprise Features: Users attempting to configure single sign-on (SSO), advanced security protocols, or complex third-party integrations are demonstrating a clear, budgeted appetite for enterprise-grade functionality 2122.

When a sales representative reaches out based on a PQL trigger, the conversation is highly contextualized. Rather than asking a generic question like "What are your pain points?", the rep can say, "I noticed your design team created 50 collaborative boards this month and is approaching your storage limit. Let's discuss how an enterprise license can help you scale securely" 12. This data-backed approach shortens enterprise sales cycles by up to 40% compared to traditional cold outreach 12.

Growth Metrics and Capital Efficiency in the Hybrid Era

Transitioning to a hybrid GTM motion requires tracking advanced SaaS metrics that measure how well a company retains and expands its existing customer base. As top-of-funnel acquisition becomes more expensive, the companies surviving the efficiency squeeze are those generating 40% to 50% or more of their new ARR through upsells and expansions from existing accounts 8182345.

Net Revenue Retention (NRR) vs. Gross Revenue Retention (GRR)

- Net Revenue Retention (NRR): NRR measures the total revenue retained from a specific cohort of customers over a given period, including all upgrades, cross-sells, and expansions, minus any churn or downgrades 51840. An NRR above 100% means the business can grow its revenue predictably even if it never acquires another new logo. The median NRR for B2B SaaS sits around 101% to 102%, but elite hybrid companies target 110% to 120%+ 8304045. Companies achieving NRR above 120% command significantly higher valuation multiples on the public markets because their growth is highly compounding 2346.

- Gross Revenue Retention (GRR): GRR measures pure retention without the flattering effect of expansion revenue; it tracks what percentage of baseline revenue stays, ignoring any upsells 818. While NRR gets the headlines, GRR is the metric that reveals true product health. The median GRR is roughly 88%, while top performers hit 95% 8. If a company's GRR slips below 90% or 92%, it indicates a fundamental product flaw - customers are quietly leaving, even if massive expansion deals from a few whales are masking the churn in the overall NRR number 821. No amount of marketing spend can fix a leaky bucket; GRR must be stabilized before pouring money into top-of-funnel acquisition 21.

Sales Velocity and CAC Payback

Understanding how long it takes to close a deal and recoup the marketing spend is vital for runway management. These metrics scale linearly with deal size.

| Deal Size / ACV Segment | Average Sales Cycle Length | Target CAC Payback Period | Typical GTM Motion |

|---|---|---|---|

| SMB (<$15,000 ACV) | 14 - 30 days | 8 - 12 months | Self-serve PLG |

| Mid-Market ($15K - $50K ACV) | 30 - 90 days | 14 - 18 months | Product-Led Sales (Hybrid) |

| Enterprise (>$100,000 ACV) | 90 - 180+ days | 18 - 24 months | High-touch SLG / ABM |

Sources: Optifai Pipeline Study 2026, Benchmarkit 2025, FirstPageSage 2024 163017.

Founders must align their cash reserves with these cycles. A startup utilizing an SLG motion for enterprise clients must have enough capital to sustain 18 months of sales representative salaries before the initial acquisition costs are recouped 1030.

Global Nuances: Adjusting GTM Strategy by Region

A common and devastating misstep for scaling SaaS companies is assuming that a GTM strategy that succeeded in North America will seamlessly translate overseas. Expanding internationally requires deep strategic localization, not just in language, but in the actual cultural mechanics of how software is evaluated and purchased 4748.

North America is the most mature market for both PLG and SLG motions, characterized by high cloud adoption, vast venture capital funding, and buyers who are highly comfortable evaluating software via self-serve trials or responding to cold outbound calls 4849. However, stepping outside this region forces fundamental shifts in the GTM playbook.

Europe (EMEA): Compliance and Consensus

While the UK market closely mirrors North American buying habits, continental Europe - particularly the DACH region (Germany, Austria, Switzerland) and the Nordics - presents unique hurdles 4849. Buyers in these markets are heavily focused on data compliance (GDPR), local server hosting, and digital trust 4749.

Crucially, German and Scandinavian buyers are notoriously resistant to aggressive, cold outbound sales tactics from foreign entities 48. Furthermore, enterprise sales cycles in Europe often take significantly longer than in the U.S. because European corporate culture relies heavily on consensus-based decision-making rather than top-down executive mandates 48. GTM alignment data shows that European teams collaborate internally more frequently during the procurement process, requiring SaaS vendors to cater to wider buying committees 50. Therefore, inbound-led marketing and highly compliant PLG funnels tend to perform better than aggressive outbound SLG 48.

Asia-Pacific (APAC): The Divide Between Japan and Southeast Asia

The APAC region cannot be treated as a monolith. Data infrastructure and business cultures vary wildly. GTM strategies must be bifurcated between mature, high-value economies like Japan and rapidly digitizing, high-volume regions like Southeast Asia 5152.

- Japan: Japan represents the third-largest economy globally and is rich in stable, high-value B2B contracts, making it a highly lucrative target 24. However, a pure, self-serve PLG motion will almost certainly fail here. The Japanese corporate purchasing process relies on a strict consensus system known as the Ringisho 54. Under this system, purchasing decisions are made by a formal committee of stakeholders who are rarely the actual end-users of the software 54. Consequently, Japanese buyers require a high-touch, relationship-driven SLG approach 482454. Trust is paramount, and companies usually must provide extensive localized documentation, engage in long face-to-face sales cycles, and utilize local distributors to close deals 2454.

- Southeast Asia (SEA): Conversely, Southeast Asia (including markets like Indonesia, Vietnam, and the Philippines) is characterized by a mobile-first population, rapid digital adoption, and a massive influx of e-commerce 512425. This region offers tremendous top-of-funnel volume and fast early traction, making it highly receptive to low-friction PLG motions 51. However, the market is highly price-sensitive. Overall B2B contract values remain smaller and suffer from higher churn rates compared to Japan or the U.S., meaning companies must rely on volume and self-serve efficiency rather than expensive sales headcount 5124.

The Middle East (GCC): The Relationship Mandate

The Gulf Cooperation Council (GCC) markets - including the UAE and Saudi Arabia - offer massive enterprise contracts fueled by sovereign wealth funds and "Vision 2030" government digital transformation mandates 56. Yet Western SaaS companies routinely fail here by utilizing the wrong GTM motion.

Automated PLG funnels and Western-style cold email outreach campaigns fall entirely flat in the GCC 56. Business in this region is deeply rooted in hierarchical decision-making, executive involvement, and personal relationships 56. Deals rarely close without multiple face-to-face meetings, and trust must be firmly established before commercial terms are even discussed 56. Furthermore, urgency-based closing techniques common in North American SLG motions are frequently perceived as disrespectful 56. Success in the GCC mandates a highly localized, patient, and high-touch SLG motion 56.

| Region | Primary GTM Preference | Key Market Characteristics | Potential Pitfalls for Western SaaS |

|---|---|---|---|

| North America | Hybrid / Balanced | High digital maturity, comfortable with self-serve and cold outreach. | Intense competition drives up CAC; high volume of marketing noise. |

| Europe (DACH & Nordics) | SLG / Inbound-led | Consensus-driven decisions, strict data compliance (GDPR). | High resistance to cold outbound; extended procurement cycles. |

| Japan | High-Touch SLG | Hierarchical Ringisho consensus process; long-term trust preferred. | Pure PLG bottoms-up motions fail because end-users lack purchasing authority. |

| Southeast Asia | PLG / Volume-led | Fast adoption, mobile-first workflows, rapid feedback loops. | High price sensitivity; smaller contract values; elevated customer churn. |

| Middle East (GCC) | High-Touch SLG | Executive-led purchasing; relies heavily on in-person meetings. | "Spray and pray" automated outreach damages brand reputation. |

The AI Disruption: Redefining Go-To-Market Mechanics

The calculus for choosing between PLG and SLG is currently being rewritten by artificial intelligence. Generative AI and agentic software are not just supplementary features; they are fundamentally altering SaaS economics, pricing structures, and user behavior 2658.

First, AI is aggressively compressing Time to Value (TTV). With AI-powered onboarding agents and copilots, users no longer need weeks to set up a software environment or watch tutorial videos; they can achieve their "aha moment" in minutes by simply prompting the tool to act 5827. Because value is delivered so rapidly, the standard 30-day SaaS free trial is becoming obsolete. Analysis of pricing data from late 2025 into 2026 shows that trial reductions are outnumbering extensions by a ratio of 3:1 58. The median trial is moving toward 14 days, and AI-native tools are aggressively shifting to just 7-day trials, operating on the logic that a shorter window with a richer product forces faster conversion 58.

Second, the intense computing costs associated with AI are accelerating the shift toward hybrid growth through the massive adoption of credit-based pricing 58. Flat-rate, unlimited "per-seat" subscriptions are economically unviable for heavy AI compute loads. As a result, credit-based pricing grew 126% year-over-year globally 1558. Credits represent the ultimate hybrid mechanism: they allow for frictionless, PLG-style self-serve consumption at the bottom tier, but inherently create built-in PQL triggers when a mid-market or enterprise account burns through its AI token allocation 58. When the tokens run out, a salesperson is automatically notified to step in and negotiate a high-volume, custom contract 58.

Finally, the very nature of the "user" in a PLG funnel is changing. In developer, infrastructure, and workflow SaaS, AI agents are beginning to independently use, test, and even purchase software. At companies like Netlify, up to 80% of new signups are now AI agents rather than human engineers 41. As these autonomous agents take over the discovery and activation layers of the funnel, traditional top-of-funnel marketing and initial SDR outreach become entirely irrelevant 4126. This dynamic forces enterprise sales teams to entirely re-orient their strategy away from cold acquisition and toward post-activation expansion, ensuring the human buyers understand the ROI the agents are generating 41.

Bottom line

Choosing between product-led and sales-led growth is no longer an either/or proposition for mature SaaS companies; it is a question of strategic sequencing based on product complexity and target contract value. Startups must leverage PLG mechanics to drive down acquisition costs and allow users to experience value instantly, while simultaneously building a data-driven sales motion to close complex enterprise deals and drive expansion revenue. While the transition to this hybrid "Product-Led Sales" model is universally accepted as the standard for 2026, the specific execution remains highly complex, requiring meticulous attention to product data, precise PQL triggers, and deep structural localization when expanding into international markets.